Board of Governors of the Federal Reserve System

International Finance Discussion Papers

Number 880, October 2006 --- Screen Reader

Version*

Optimal Fiscal and Monetary Policy When Money is Essential*

S. Borağan Aruoba†, University of Maryland

Sanjay K. Chugh‡, Federal Reserve Board

[The PDF document is dated "October 6, 2006."]

NOTE: International Finance Discussion Papers are

preliminary materials circulated to stimulate discussion and

critical comment. References in publications to International

Finance Discussion Papers (other than an acknowledgment that the

writer has had access to unpublished material) should be cleared

with the author or authors. Recent IFDPs are available on the Web

at http://www.federalreserve.gov/pubs/ifdp/. This

paper can be downloaded without charge from the Social Science

Research Network electronic library at http://www.ssrn.com/.

Abstract:

We study optimal fiscal and monetary policy in an environment where explicit frictions give

rise to valued money, making money essential in the sense that it expands the set of feasible

trades. Our main results are in stark contrast to the prescriptions of earlier flexible-price Ramsey models. Two especially important findings emerge from our work: the Friedman Rule is

typically not optimal and inflation is stable over time. Inflation is not a substitute instrument

for a missing tax, as is sometimes the case in standard Ramsey models. Rather, the inflation tax

is exactly the right tax to use because the use of money has a rent associated with it. Regarding

the optimal dynamic policy, realized (ex-post) inflation is quite stable over time, in contrast to

the very volatile ex-post inflation rates that arise in standard flexible-price Ramsey models. We

also find that because capital is underaccumulated, optimal policy includes a subsidy on capital income. Taken together, these findings turn conventional wisdom from traditional Ramsey

monetary models on its head.

Keywords: micro-founded models of money, Friedman Rule, inflation stability

JEL classification: E13, E52, E62, E63

* The views in this paper are solely the responsibility of the authors and should not be interpreted as reflecting the views of the Board of Governors of the Federal Reserve System or of any other person associated with the Federal Reserve System. Return to text

Monetary theory has made important advances of late, ones that

enable researchers interested in applied policy questions to

consider explicit frictions that give rise to valued money. In this

paper, we build on the works of Lagos and Wright (2005) and Aruoba,

Waller, and Wright (2006); in these new environments, we study

optimal fiscal and monetary policy, following the tradition of

Lucas and Stokey (1983) and Chari, Christiano, and Kehoe (1991).

Two important findings emerge from our work, both of which are

opposite those of earlier flexible-price Ramsey monetary models:

the Friedman Rule is typically not optimal and inflation is stable

over time. Our results thus turn conventional wisdom from

traditional Ramsey models on its head.

The contribution of Lagos and Wright (2005) and Aruoba, Waller,

and Wright (2006) -- hereafter, LW and AWW, respectively -- is to

integrate search-based monetary theory, in the spirit of Kiyotaki

and Wright (1989, 1993), with standard dynamic general equilibrium

macroeconomics. This integration makes the study of policy

questions much easier and potentially more relevant than in earlier

search-based models. However, these models have been criticized on

two grounds. First, they superficially resemble standard

cash-in-advance (CIA) or money-in-the-utility-function (MIU)

models, raising some question about whether they really are any

deeper than reduced-form models of money. This point has been

raised by, among others, Howitt (2003). Second, until now, the

policy questions addressed in these new models have been largely

confined to the deterministic welfare costs of inflation. When

parameterized to seem as close as possible to standard CIA and MIU

models, the quantitative answers they have yielded to this question

are similar to those obtained with CIA and MIU models, further

adding to the sense that these new models simply re-invent CIA or

MIU. In this paper, we ask a different policy-relevant question in

these new models, and even when we parameterize the model to look

very similar to standard applied models of money, we reach

conclusions very different from those reached by Chari, Christiano,

and Kehoe (1991) and others using typical CIA and MIU frameworks.

Our results thus show that the answers to policy questions may

indeed be very different once monetary frictions are treated

seriously.

We study the canonical Ramsey problem of optimal fiscal and

monetary policy using the LW and AWW models. Our first main finding

is that the optimal nominal interest rate is typically positive.

This optimal deviation from the Friedman Rule is not because the

inflation tax acts as a substitute instrument for a missing tax, as

is sometimes the case in Ramsey models. Rather, the inflation tax

is exactly the right tax for the government to use when money is

essential in Kocherlakota's (1998) sense that it expands the set of

feasible trades. Specifically, without money, trade can only occur

if there is a double coincidence of wants, whereas money allows

trade to occur with only a single coincidence of wants. Money is

thus a special object in this class of models and therefore has a

rent associated with it. Households in our economy require the

benefit of holding money to be strictly positive to be induced to

hold it. This benefit is realized only when the household is a

buyer in a bilateral match in the form of buyer's surplus, and it

is this surplus that we interpret as the rent associated with

holding money. It is well-known from Ramsey theory that it is

optimal to tax rents. The most direct way to tax rents accruing to

money is through inflation, hence the Friedman Rule is not optimal.

Interestingly, Kocherlakota (2005) conjectured that the Friedman

Rule may not be optimal in a Ramsey problem in search-based models.

Our results show his conjecture is correct.

Deviations from the Friedman Rule have also been obtained in

other modern Ramsey models. For example, Schmitt-Grohe and Uribe

(2004a) show that a positive nominal interest rate can tax

producers' monopoly profits, and Chugh (2006b) shows it can tax

monopolistic labor suppliers' rents.1 Both of these results, however, are

examples of the Ramsey planner using a positive nominal interest

rate to indirectly tax some rent. One

may wonder whether alternative tax instruments in our model could

tax the money rent. To investigate this, we introduce a sales tax

on goods whose purchase can only be achieved with money. It turns

out that adding this seemingly natural instrument does not admit a

Ramsey equilibrium in which the Friedman Rule is optimal. Thus, if

there does exist another tax instrument besides the inflation tax

that can seize the money rent, it is not an obvious one.

Our second main finding is that realized (ex-post) inflation is

quite stable over time in the face of shocks, which is in contrast

to the very volatile ex-post inflation rates that Chari,

Christiano, and Kehoe (1991) -- hereafter, CCK -- find. Inflation

volatility is high in CCK and the related literature because

surprise movements in the price level allow the government to

synthesize real state-contingent debt payments from nominally

risk-free government bonds, without distorting the relative prices

of consumption goods. The government then need not change other,

distortionary, tax rates much in response to shocks. In our model,

in contrast, real activity is distorted by ex-post inflation

because inflation affects relative prices of goods, in a way that a

flexible-price CIA or MIU model cannot articulate. The welfare cost

of this relative-price distortion dominates the insurance value of

generating state-contingent debt in our model, rendering inflation

very stable. The frictions underlying monetary trade thus provide

novel justification for the optimality of inflation stability, a

prescription that resonates with most central bankers. This result

also echos the long-standing idea in monetary economics that

inflation variability is undesirable because it induces relative

price shifts.

Finally, when we allow for capital accumulation, the optimal

policy includes a subsidy on capital income. Both the frictions

inherent in bilateral trade in our model as well as the deviation

from the Friedman Rule tend to depress capital accumulation

compared to its efficient level. A capital subsidy somewhat

alleviates this problem.

An important technical advantage of the LW and AWW frameworks is

that the distribution of money-holdings across agents is simple to

track: it simply collapses periodically to a point. At the expense

of a heavier computational burden, one may want to think about

optimal fiscal and monetary policy when this distribution is

non-trivial. Once one goes down that route, an interesting taxation

framework to apply may be the Mirrleesian one, in which

idiosyncratic shocks and private information become important

considerations in shaping optimal policy. However, because even the

simpler step of characterizing the Ramsey-optimal policy, which

assumes a representative agent, has not been studied in this class

of models, we think it makes sense to begin here.

The rest of the paper is organized as follows.

Section 2 lays out the baseline LW

model in which we first study optimal policy. Most of the important

results and intuition emerge in this basic model.

Section 3 presents the Ramsey

problem for the basic model. In Section 4, we characterize and discuss the optimal

policy in the basic model; we present in Section 4.1 a proof for a particularly important

version of the model that the Friedman Rule is not optimal and in

Section 4.2 the dynamic Ramsey

allocations and policy that demonstrate optimal inflation

stability. In Sections 5

and 6, we extend the Ramsey

problem to the AWW model, and Section 7 shows that the main results carry over

from the basic model virtually unchanged. Section 8 summarizes and offers ideas for future

work.

We begin by establishing our main results in a version of the LW

model. In this model, the agents in the economy participate in a

centralized market (CM) where they trade general consumption goods

and assets with the market and in a decentralized market (DM) where

they trade specialized consumption goods bilaterally. To enhance

comparability with the benchmark cash-credit environment used by

CCK, we alter slightly the timing of markets in the original LW

model. Specifically, in our version, the CM is the first market in

a given period, followed by the DM. We make this alteration because

we would like asset markets (which in the LW model meet in the CM)

to convene in any period before goods markets (in particular,

before goods markets in which money must be used for transactions),

which is the timing assumed by CCK. However, we do not see how any

of our results depend on the temporal ordering of markets within a

period. We proceed by describing the activities of the government,

households, and firms in our model.

Government consumption is assumed to be composed entirely of

goods produced in the CM. In nominal terms, the flow budget

constraint of the government is

(1)

which states that the government has three sources of revenues to

pay for its consumption: labor income tax revenues, nominal money

creation, and nominal debt issuance. The notation is standard:

denotes nominal

money outstanding at the end of period , is nominally risk-free government debt

outstanding at the end of period , is

the gross nominal interest rate on bonds,

is a

proportional labor income tax on aggregate hours worked

in the CM,

is the nominal

price level in the CM, and is the real wage in the CM. The nominal return

is known at the

time is issued and paid

in the CM of period . We

assume that bonds are simply book entries with no tangible proof

that one can carry around.

Households periodically transact in markets for general goods

and assets (the CM) and in markets for specialized goods (the DM).

In the DM, money is essential in the sense that transactions there

are infeasible without money.2 In the

CM, because markets are Walrasian trades can proceed with or

without money. We describe first the timing of events in a given

period and then present the household's CM and DM problems.

Events unfold for a household in a given period as follows:

The household begins the CM with portfolio and

The uncertainty for the current period is resolved, and the

household observes government consumption and the level of technology

. We denote the

aggregate state collectively by .

The household receives the receipts from bond holdings,

.

The household chooses its CM consumption , labor supply , portfolio

and pays

the labor income tax.

The household enters the DM with .

Depending on the household's trade in the DM, it exits the DM

with

, or

money holdings,

where is the buyer's

payment in bilateral trade.

For a household that enters the CM with money holdings

and bond

holdings , the

CM problem is

(2)

subject to

(3)

where denotes the

value of entering the CM and denotes the value of entering the DM that

convenes after the CM in period . Centralized market consumption is , and the household's hours

worked in the CM is .

Note that instantaneous utility in the CM is separable and linear

in labor; it is this quasi-linearity in preferences that allows the

LW model to be tractable, as it guarantees a degenerate

distribution of money holdings across households after every

meeting of the CM.

Eliminating in the

objective function using the budget constraint, the first-order

conditions with respect to , ,

and are

(4)

(5)

(6)

familiar from LW. These optimality conditions imply the usual LW

results about degeneracy of asset holdings

across

households because they are independent of

.3 All

households choose the same portfolio at the end of the CM

regardless of the portfolio they entered the market with. Thus, the

LW result of degeneracy of money holdings readily extends to bond

holdings as well. Moreover, we have standard envelope conditions

Now we turn to the household's DM problem. Knowing that the

distribution of money holdings is degenerate in equilibrium, we

will, for notational simplicity, write the household DM problem

assuming that when it meets a trading partner, the trading partner

has equilibrium money holdings ; this allows us to conserve on integrating over

all possible money holdings of trading partners that a given

household could meet. With probability , the household is a buyer in

the DM; with probability , the household is a seller in the DM; and with

probability , the

household does not participate in the DM and continues to the CM of

the next period without transacting.4Buyers consume in the DM, experiencing utility

; sellers produce

in the DM,

experiencing disutility, which can be interpreted as the cost of

production, , where

. We assume

throughout our basic model that

.5

We can write the problem of a household that enters the DM with

portfolio

as

(9)

(10)

(11)

The quantity

is the quantity produced and exchanged in a bilateral meeting in

the DM, where denotes

the money holdings of the buyer, denotes the money holdings of the seller, and

is the amount of money that changes hands. We refer to

as the

terms of trade in a single-coincidence meeting. Note that due to

the nature of the bonds, neither the buyer's nor the seller's bond

holdings will matter for

and .

In the DM, we must specify the protocol by which the price and

quantity in any bilateral trade are determined -- that is, we must

define the structure by which the terms of trade are determined.

The two main alternatives in the literature are Nash bargaining and

price-taking. We describe the bargaining version in detail. It

turns out -- see Rocheteau and Wright (2005) -- that price-taking

in the basic model amounts to a simple parameter restriction in the

bargaining version.

Denoting the portfolio of the buyer by

, that of

the seller by

, and the buyer's

bargaining power by ,

the generalized Nash bargaining problem is

(12)

(13)

subject to

(14)

where the constraint is simply a feasibility condition stating the

buyer cannot spend more than he has and the threat points are the

values of continuing on to the next CM in period . Using the envelope conditions

from above (in particular, the implied linearity of the function

), the

bargaining problem can be written more conveniently as

(15)

subject to

(16)

We define

which can be interpreted as the marginal utility of

consumption of CM

goods that are worth one unit of money using (4). Then, the Kuhn-Tucker conditions, which are

necessary and sufficient, for the bargaining problem are

(17)

(18)

(19)

where

is the

multiplier associated with the constraint. If

, the

first two conditions yield

, which defines

the efficient quantity

, and

, which

can be solved using the second equation.

If

, the

solution will have

, meaning

the buyer spends all his money in a bilateral meeting. Using the

first condition, the quantity produced and traded will solve

(20)

where

(21)

as in LW. In equilibrium,

, which

can be shown using a similar argument to the one in LW. Also, note

that because the expectation in is taken with respect to , we denote the bargaining

problem outcomes as

and

, where

the first argument is understood to be the money holdings of the

buyer.

Substituting this solution into the DM problem (9) and using the envelope conditions for

, we get

Although bargaining has been used almost exclusively as the

pricing scheme in bilateral meetings in this class of models, more

``competitive'' pricing schemes have been used recently, as well.

In addition to being closer to mainstream macroeconomics,

competitive pricing eliminates the holdup problems inherent in

bargaining. In the basic model, competitive pricing in the DM

amounts to sellers and buyers solving their respective supply and

demand problems taking the price as given; the market-clearing

price is determined in equilibrium. Based on the results of LW and

Rocheteau and Wright (2005), it follows that the price-taking

version of our model is the same as the bargaining version with

.

For the bargaining version we obtain the conditions that solve

the household's problem as follows. First, combining the

household's CM optimality conditions (4)-(6) with the envelope

conditions (23) and (24) gives us:

We will refer to these last two equations as the household's

first-order conditions with respect to money and bonds,

respectively, in analogy with a standard cash/credit CCK type of

model. Note that they imply a Fisher-like condition,

where the left hand side,

, is the

cost of holding money (the net nominal interest rate) and the right

hand side is the benefit of holding money. We note that the

right-hand-side of (34) will play an

important role in shaping the Ramsey allocations and hence the

optimal policy; we defer discussion and intuition regarding it

until we present the Ramsey problem in Section 3, in which we will see it in the context of

the complete Ramsey problem and will be able to easily compare it

to the benchmark Ramsey problems in Lucas and Stokey (1983) and

CCK.

To finally state the solution of the household problem: given

sequences

, initial

condition

, and

appropriate transversality conditions, the solution to the

household's problem is processes

satisfying conditions (3), (20

), (27), (31), and (33).

In the CM, a representative firm hires labor in a competitive

labor market and operates the linear production technology

.

Profit-maximization therefore implies the wage is

in

equilibrium.

Imposing equilibrium (

,

, etc.) and

combining the firms' and households' optimality conditions, we can

define the equilibrium as follows. Given policy variables

, the technology

realization

, the government spending

realization

, and initial condition

,

equilibrium is a set of processes

satisfying

(35)

(36)

(37)

(38)

(39)

(40)

For the Ramsey problem, it will be useful to combine (36) and (37) and rearrange for real money

balances,

(41)

Furthermore, in any monetary equilibrium,

because

otherwise households could earn unbounded profits by selling bonds

and buying money. We represent this restriction in terms of

allocations using (38) as

As is common in the Ramsey literature, we adopt the primal

approach and cast the Ramsey problem as that of a planner that

chooses allocations subject to feasibility and the need to raise

exogenous government revenue, making sure the resulting allocations

are implementable as a monetary equilibrium. We prove the following

in Appendix A.1:

Proposition 1The allocations in a

monetary equilibrium satisfy (39), (42),

and the present-value implementability constraint (PVIC),

(43)

In textbook Ramsey problems, implementability constraints

typically take the form , where

is the set of goods the

agent consumes at time .6 At first

glance, (43) does not seem to conform to

this general form because the term related to the DM,

does not look like marginal utility of a good times the

quantity of that good. However, this term does indeed have such an

interpretation; we can show that the term in the PVIC is simply the

product of money balances and its marginal utility.

To see this, note that from the bargaining problem and (20),

is the surplus of the buyer

and therefore

is

the marginal surplus of the buyer. Moreover, money has no use in

the DM unless the household is a buyer, which occurs with

probability . Thus,

the marginal utility of money can be expressed as

. From

(20) and (25), we

have

and

.

Combining these, we obtain the third term under the summation in

the PVIC. With this interpreration, one may argue that our model

lolks like a MIU model, which would have a term in the PVIC. In our context,

though, the marginal utility of money is linked to the fundamentals

of the economy -- allocations and technology -- and it is not an

arbitrary function.

If , the DM shuts

down and our PVIC collapses to the usual CCK PVIC in a real model. That is, the model collapses not

to the CCK monetary (cash-credit) economy, but to a purely real

model. This is a manifestation of the ``dichotomy" result the LW

model displays that Aruoba and Wright (2003) pointed out. The

inflation rate in the LW model does not affect CM allocations at

all.7

Because we restrict attention to only monetary equilibria, we

require that the Ramsey allocations satisfy

restriction (42), which we refer to

as the zero-lower-bound (ZLB) constraint. CCK show that in their

model, the ZLB constraint always holds with equality under the

solution of the Ramsey problem obtained by dropping the ZLB constraint; in other words, in the

CCK model the Friedman Rule () can be shown analytically to always be the

optimal policy. Thus, in the CCK model it turns out the ZLB

constraint is redundant regardless of the parameterization of the

model. This is not the case in general in our model and thus we

need to impose it. As a technical point, note that the ZLB

constraint is an inequality constraint. Thus, when solving for the

dynamics of the model, we must employ a nonlinear global numerical

approximation to handle the occasionally binding constraint. In

practice, though, for a very important parameterization of interest

of the model, it turns out that the ZLB constraint can be shown to

be slack -- in fact, that it is always satisfied with strict

inequality. We discuss this further below, and it is one of our

main results.

We assume the Ramsey planner is able to commit at time zero to a

policy for . We

thus sidestep here the potentially interesting issue of

time-inconsistency in this model. The Ramsey problem is thus to

choose

to maximize

(44)

subject to the resource constraint

(45)

the PVIC (43), and the ZLB

constraint (42), taking as given

. In

Appendix A.2, we list the

conditions that characterize the solution to this problem, along

with the conditions that allow us to construct the policies and

prices that support the Ramsey allocation. Thus, as we already

noted, our approach is a straightforward application of Ramsey

theory.

One of our central results is that for a range of values for

, the optimal

nominal interest rate is positive. We can establish this

analytically for the case , which we do next. The case is an especially important

one because Rocheteau and Wright (2005) show that for this case,

bargaining yields the same outcomes as if there were competitive

forces in the DM, making DM trades look less non-standard from the

point of view of modern DGE theory. For , analytical solutions

are not as easy to obtain, and we resort to numerical

solutions.

The Friedman Rule is not optimal if , as we now show:

Proposition

2

(Optimal Deviation from the Friedman Rule in Basic

Model) If , the optimal policy features a strictly

positive net nominal interest rate in every period . Furthermore, if is CRRA (constant relative risk

aversion) then the optimal nominal interest rate is constant over

time.

Proof. Let be the multiplier on the PVIC (43) in the Ramsey problem, and consider the

Ramsey problem with the ZLB constraint dropped. The first-order

condition of this problem with respect to for is given in Appendix A.2. With , we have that

, so

this FOC simplifies considerably,

(46)

First, let us assume ,

which means the PVIC constraint is not binding. This implies

, or

. This also

means the ZLB constraint binds. Using (35) and the FOC of this problem with

respect to presented

in Appendix A.2, we also get

. All of

this implies that the real liabilities of the government grow

without bound and this cannot be sustained in equilibrium. As such,

the solution to this problem must have .

Because is strictly concave, the multiplier

under the

Ramsey allocation, and of course in a monetary equilibrium, the right hand

side of the first order condition above is strictly positive. This

implies

,

which in turn implies

(47)

imposing

because

. But this

implies, by the equilibrium condition (38), that , so we have established that the Friedman

Rule is not optimal.

Next, suppose

. Looking at (38), we see that for to be constant over time,

has to be constant. With , this requires that

is

constant. The CRRA utility function has the property

. Imposing this in

(46) and collecting the

terms, we

have

(48)

which shows that

is

constant.

Deviations from the Friedman Rule have been obtained in other

Ramsey models, as well. For example, Schmitt-Grohe and Uribe

(2004a) show that a positive nominal interest can tax producers'

monopoly profits, and Chugh (2006b) shows that it can tax

monopolistic labor suppliers' rents. We know from Ramsey theory

that taxing rents is optimal because it is non-distorting. However,

the deviations from the Friedman Rule in Schmitt-Grohe and Uribe

(2004a) and Chugh (2006b) are instances of the Ramsey planner using

a positive nominal interest rate to indirectly tax some rent -- in neither case is

money the ultimate object the Ramsey planner wants to tax.

In contrast, in our environment, inflation directly taxes the rent that the Ramsey planner

wants to seize, which is the rent associated with money. Money has

a rent in our model because without it, certain trades simply could

not occur, which would decrease welfare. A household chooses to

hold money with the anticipation of being a buyer in the next DM. A

household would never choose to hold money unless

, which can be interpreted

as the rent that money-holders enjoy. It is precisely this rent

that the Ramsey planner wants to tax, and the inflation tax is the

most obvious way of doing this.

Our conclusion that the Friedman Rule is not optimal of course

differs from that of CCK. However, it can be reconciled with their

result by considering basic principles of public finance. In CCK,

optimality of the Friedman Rule depends on a certain class of

utility functions. In particular, CCK require cash goods and credit

goods to enter the utility function homothetically and separably

from leisure. Similarly, in Chari and Kehoe's (1999) MIU model,

money and consumption must enter utility homothetically and

separably from leisure in order for the Friedman Rule to be

optimal. These results are essentially an application of the

uniform taxation result of Atkinson and Stiglitz (1980), requiring

cash-good consumption and credit-good consumption (or money and

consumption) to be taxed uniformly; a deviation from the Friedman

Rule would mean that cash goods are taxed more heavily than credit

goods, hence cannot be optimal.

The instantaneous social utility function in our model takes the

form

( denotes the

effort of sellers in the DM). If we interpret as the cash good and as the credit good, and must enter

homothetically to satisfy the CCK requirement. Our

Proposition 2 admits this case.

For example, we can set and Proposition 2 of course still holds. However, realize

that, given the structure of the LW model, . The reduced-form social utility function (the one that

the Ramsey planner maximizes) thus has the form

. Regardless of what we assume about and , and will

in general not enter the reduced-form utility function

homothetically. In other words, even though we might have

homothetic preferences in terms of the primitives, the reduced-form

representation, which is the one relevant for the Ramsey planner,

would have non-homothetic preferences. Our results thus reconcile

with those of CCK.

One may still wonder, though, if there is another instrument

that, if the Ramsey planner had it available and were to use it,

would reinstate the optimality of the Friedman Rule. Following the

logic of Schmitt-Grohe and Uribe (2004a) and Chugh (2006b), such an

instrument would seemingly need to be a direct means of taxing DM activity. A natural

candidate, then, is a sales tax in the DM. However, we show in

Appendix B that allowing for a

DM sales tax in what seems to be a straightforward way does not

admit a Ramsey equilibrium in which the Friedman Rule is

optimal.8 This

result implies that the sub-optimality of the Friedman Rule we have

documented is not sensitive to the inclusion of at least this tax

instrument. Admittedly, this is only one candidate alternative tax

to consider, although seemingly a very natural one -- but it does

not restore the Friedman Rule.

Left to still consider is the quantitative degree of the

departure from the Friedman Rule. The rent-seizing argument would

suggest that the optimal inflation rate should be one that

confiscates the entire rent, but this would imply . Thus, the optimal inflation rate

must balance the motive to seize the money rent versus pushing

too low. Our

numerical results, presented next, seem to confirm this

intuition.

As we explain in Appendix A.2, given

, the

first-order conditions of the Ramsey problem and the feasibility

condition for the CM characterize the allocations

and the multiplier on the ZLB constraint,

.9 Then we can use the equilibrium

conditions to back out

. Due to the nature of

our model, we can exactly solve for all of these variables, except

for , using a

nonlinear equation solver. However, to reduce computational time,

we nonetheless approximate the functions

and

, along

with

. Our

strategy is to construct global nonlinear approximations of these

functions because of the presence of the potentially

occasionally-binding ZLB constraint.10 Of interest to many practitioners,

however, should be our (unreported) findings that, for the versions

of the model in which we know for sure the ZLB constraint is always

slack, first-order and second-order local approximations yielded

results virtually identical to our global approximation.11To construct the approximations, we use

as the functional equations the first-order conditions of the

Ramsey problem with respect to and and the equilibrium condition (37). We use the remaining equations to

solve for the other variables of interest.

Before presenting numerical results, we briefly describe the

parameterization of the model. To the extent possible, we use the

parameters and functional forms that LW provide, whose model is

calibrated to match some long-run features of the US economy. The

DM utility function is

(49)

with , which is a

parameter that forces , which can occur in the DM if a household does

not meet another agent with whom to trade. In the CM, instantaneous

utility is

.

We consider two cases: buyer-take-all in the bargaining problem

, which is

equivalent to price-taking, and . For the former case we use

and for the latter

case we use

.

The exogenous government spending and TFP processes each evolve

as an AR(1) in logs,

(50)

(51)

with

and

. We

calibrate

, so that

government purchases constitute about 18 percent of total GDP in

steady-state.12 In line

with Schmitt-Grohe and Uribe (2004b) and the RBC literature, we set

the parameters of the stochastic processes

,

,

, and

. With

these volatility parameters, our model has a standard deviation of

government purchases of about 7 percent of the mean level of

government spending, and the volatility of total output is about

1.8 percent, both in line with data. The persistence parameters of

the exogenous processes are for an annual calibration, thus we set

the annual subjective discount factor

, which

delivers an annual real interest rate of about 4 percent. Finally,

we choose the level of steady-state government debt, an object not

pinned down by the model, so that it is 45 percent of steady-state

output, consistent with the parameterizations of CCK and

Schmitt-Grohe and Uribe (2004b).

In Section 4.1, we

established that the Friedman Rule is not optimal when . Obtaining analytic

solutions for

is not as easy, so we study the optimal steady-state policy for

this case numerically.

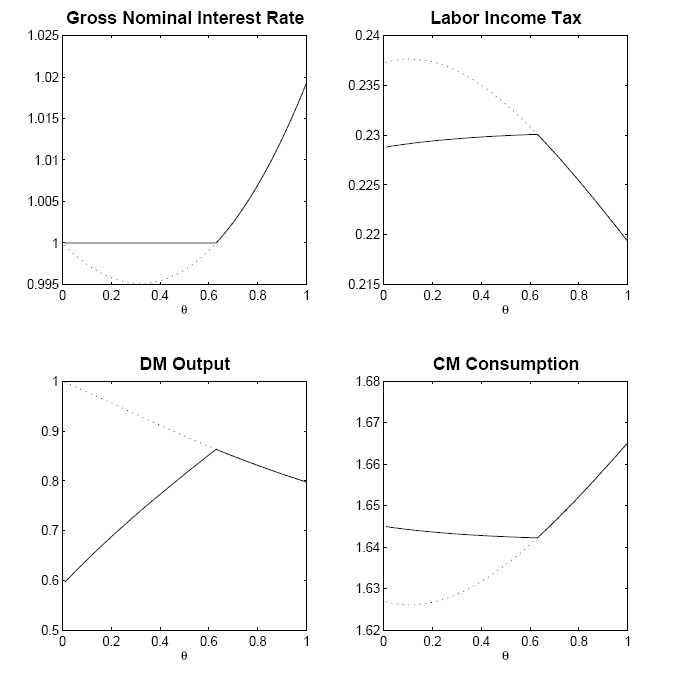

The solid line in Figure 1 shows the steady-state Ramsey policy

and key allocation variables as functions of . At , the optimal nominal

interest rate is about 2 percent at an annual rate; the associated

optimal inflation rate is thus -1.6 percent, higher than the

Friedman rate of deflation, which would be -3.4 percent in our

model.

As falls below

unity, the optimal nominal interest rate falls. This is due to the

holdup problem associated with holding money when discussed by LW.

Specifically, when , the buyer does not get the full benefit

from the match and this reduces his incentive to hold money,

causing the equilibrium

to fall. Realizing this, the Ramsey planner reduces the inflation

tax, balancing his desire to tax the buyer's surplus with the

desire to reduce the effects of the holdup problem. Because

seignorage revenue (not shown) falls along with the nominal

interest rate, the government's revenue shortfall must be made up

with the labor tax, causing the labor tax rate to rise, as the top

right panel of Figure 1 shows. The associated responses of the

allocation variables and

are easy to

understand as well. As the labor income tax rate rises with the

fall in , hours

worked and hence consumption in the CM decline.

If falls far

enough the ZLB constraint binds, making the Friedman Rule the

optimal policy. For our calibration, the ZLB constraint binds if

, as

can be seen by the fact that the net nominal interest rate is zero

over that interval. The kink when the ZLB constraint binds leads to

kinks in the labor tax rate and allocations as well.

The dotted line in Figure 1 shows the allocations and implied

and that emerge from the Ramsey

problem with the ZLB constraint (42)

dropped. The results for

are

of course identical because in that region the ZLB constraint did

not bind anyway. With the ZLB constraint dropped and

, we

see that the Ramsey planner would like to implement, if it were

consistent with monetary equilibrium, a negative net nominal

interest rate, apparently to boost . Of course, deflation faster than the Friedman Rule

is inconsistent with a monetary steady-state equilibrium. Hence,

the Friedman Rule becomes the constrained optimal policy.

We now turn to the dynamics of the Ramsey policy, which reveals

our second central result: optimal inflation is very stable. To

investigate the dynamic behavior of our model, we solve for the

dynamic Ramsey equilibrium and simulate the model. We conduct 1000

simulations of 500 periods each and discard the first 100 periods.

As in Khan, King, and Wolman (2003) and others, we assume that the

initial state of the economy is the asymptotic Ramsey steady-state.

For each simulation, we then compute first and second moments and

report the averages of these moments over the 1000 simulations.

Before turning to simulations, we make a few observations by

inspecting the first-order conditions of the Ramsey problem. First,

government spending affects only CM hours because none of the

first-order conditions for , ,

and (the

multiplier on the ZLB constraint) involve . Once is determined, adjusts according to the shocks

to . This result

follows from the quasi-linearity of preferences in the CM. Because

households essentially have risk-neutral preferences over hours,

fluctuations in

are fully reflected in .13 Simply

put, the dichotomy result is that CM and DM allocations have

nothing to do with each other unless production in each market

depends on a common capital stock (as we introduce in

Section 5). Second, and related,

the dynamics of

and follow the

dynamics of the technology shock as the latter is the only driving

force for the former. Third, for the particular utility function we

choose in the CM - in fact for any CRRA utility function -- the

labor income tax rate is constant over time.14 This can be viewed as the extreme case

of the usual consumption-smoothing motive as spelled out in, say,

Barro (1979).

Table 1 presents simulation-based moments for the key allocation

and policy variables for (which, again, is equivalent to

price-taking) and for . Let us first discuss the results for

. The first

three rows show the dynamics of realized inflation, the labor

income tax rate, and the net nominal interest rate under the Ramsey

policy. We hone in first on the result that the optimal inflation

rate is quite smooth over time, with a standard deviation of about

only about 24 basis points (at an annual rate) around a mean

deflation rate of 2 percent. The very stable inflation rate is in

sharp contrast to the extremely volatile optimal inflation rate

first found by CCK in a flexible-price Ramsey model and recently

verified in, among others, the flexible-price versions of

Schmitt-Grohe and Uribe (2004a, 2004b), Siu (2004), and Chugh

(2006a, 2006b).15

In these baseline Ramsey monetary models, inflation does not

distort the relative prices of goods. It is easiest to see this in

a cash-credit economy: the nominal price of both cash and credit

goods is , and the

relative price depends only on the nominal interest rate,

reflecting the opportunity cost of the money used to purchase the

cash good. In other words, given a nominal interest rate, dynamic

fluctuations in the price level do not alter the relative price

between cash and credit goods and therefore do not affect

equilibrium allocations. In these baseline models, then, the

driving force behind price-level dynamics is just the (desirable)

ability of price-level fluctuations to tailor the real returns on

nominal government debt, thus avoiding the need to change other

distortionary taxes in the face of shocks to the government budget.

Quantitatively, assuming business-cycle magnitude shocks, realized

inflation turns out to be very volatile.16

With money essential, this result is overturned because

inflation affects the relative price of DM and CM goods. To see

this, note that the nominal price of a DM good in period

can be expressed as

, which is

simply per-unit expenditure in the DM. This means the relative

price of DM goods in terms of CM goods is simply real money

balances divided by DM consumption. Both of these objects are

functions of inflation in equilibrium and therefore the relative

price is in principle a function of inflation in equilibrium. In

equilibrium, inflation thus affects the household's margin between

DM and CM goods in a way that simply cannot occur in a cash-credit

environment. Usual tax-smoothing reasons then suggest that it is

optimal to have smooth (low-volatility) inflation because otherwise

this margin would be disrupted. In Table 1 we also report the

dynamic properties of this relative price, and they are quite

similar to -- indeed, even smoother than -- the dynamic properties

of inflation. This demonstrates that even though the Ramsey planner

has available the option of moving this relative price around over

time, it is optimal to not do so.

Other Ramsey models make the prediction that inflation stability

is optimal, most notably Schmitt-Grohe and Uribe (2004b), Siu

(2004) and Chugh (2006b). The basic mechanism behind their

inflation stability results is also a relative-price distortion

caused by inflation; however, these models all rely on nominal

rigidities to generate the relative-price effect. We emphasize that

in our model, prices are fully flexible and yet inflation causes

relative price distortions. The real frictions underlying monetary

exchange are behind our result.

Another perhaps noteworthy feature of inflation dynamics is that

it displays high persistence. In the benchmark CCK model, which

assumed fixed capital, inflation persistence is virtually zero no

matter how persistent are the driving shocks. Chugh (2006a) shows

that allowing for capital accumulation or habit formation generates

optimal inflation persistence, but clearly here we have that result

with neither of these features. If one inspects the equilibrium

Euler equation for bonds, which is what we use to solve for the

dynamics of inflation, it is not surprising that the dynamics of

inflation would closely track the dynamics of and , which in turn closely track

the dynamics of the technology shock.

Finally, consider the results for , reported in the second panel of Table 1.

The means of the variables of interest are of course in line with

the steady state results. Compared to the price-taking case

(), the average

labor income tax rate is higher and average consumption (both CM

and DM) and GDP are lower. The Friedman rule is optimal with an

average deflation equal to the rate of time preference. In our

simulations, which are driven by business-cycle-magnitude shocks,

we find that the optimal nominal interest rate is once again

constant over time.17 Thus,

even though the ZLB constraint can be an occasionally-binding

constraint in principle, for our calibration it either always binds

() or never

binds (). We

also find that

is less volatile if , which in turn causes GDP to be less

volatile and the correlations of other variables with GDP to be

lower than what we find when . In short, we find that except for the

expected changes in the means, the dynamic behavior of the Ramsey

problem with

is qualitatively identical to the case with .

Ramsey models of optimal fiscal and monetary policy have only

recently begun considering how the presence of capital accumulation

affects optimal policy.18 Here, we

add capital to our baseline model following AWW: we assume that

capital is accumulated in the CM and used in production in both the

CM and the DM. As AWW show, with capital productive in both

markets, the LW and Aruoba and Wright (2003) ``dichotomy" result,

in which CM and DM allocations have nothing to do with each other,

disappears. We proceed by briefly describing how the model is

modified to accommodate capital and then present results.

The critical change from the basic model is that capital is

introduced as a factor of production in both the DM and CM. In the

CM, this is done in the obvious way: production takes place

according to a constant returns technology subject to TFP shocks,

.

Profit-maximization by firms in the CM leads to standard

factor-price conditions,

and

.

In the period- DM,

sellers use the capital they have, which is according to our timing

convention.19 As

explained in AWW, this amounts to modifying the cost function to

include capital as

, with , and .

The household CM budget constraint modifies in the obvious

way,

(52)

where is the

household's capital holdings at the start of period , is the rental rate on capital, is its deprecation rate, and

is the

tax rate on capital income.20 The

value functions in the CM and the DM now of course include the

household's capital holdings as a state variable. The household's

CM problem is

The first order conditions of this problem are exactly as they

were in the basic model, with a new condition for capital

accumulation given by

(54)

The results regarding the degenerate distribution of bonds and

money readily extend to capital. is still linear in all its arguments, with

given by

(55)

In the DM, we again consider two pricing schemes: bargaining and

price-taking. Unlike the basic model, price-taking cannot be

obtained by a simple parameter restriction of the bargaining model

and as such we briefly discuss it below. The DM problem for the

household is still given by (9)

after obvious changes in arguments and using

and

to represent the terms of trade from the viewpoint of the buyers

and the sellers, respectively. This simplifies to

(56)

using the linearity of

. All we

have to do to characterize the solution to the household's problem

is to compute the partial derivatives of , which we do for both pricing

schemes below. As in AWW, capital is only a productive input in

this market and cannot be used as a medium of exchange. Those

familiar with the AWW model may choose to skip the following

exposition and proceed directly to the Ramsey problem in

Section 6.

The bargaining problem is still given by (15) with the obvious modifications

regarding capital. The solution to the problem gives

,

where solves

, refers to the buyer's money

holdings and refers to

the seller's capital stock. The function

is a straightforward

modification of the one in the basic model.

The only new partial derivative we need is

which is

given by

(57)

Noting

, defining

(58)

and combining the optimality conditions (4)

and (54) with the envelope condition

(57), we get the household's Euler

equation for capital accumulation,

(59)

which shows that investment takes into account the fact that

capital affects productivity in the DM as well as in the CM. The

additional term related to the DM represents the seller's payoff

from carrying units

of capital into the DM and producing units, which occurs with probability

. As such, we can

think of it as the return of capital in the DM. Therefore when

making an investment decision in the CM of period , the households take the return of

extra capital in the CM of period , which is the usual term on the right hand side as

well as the return in the DM. It is also straightforward to show

that the analog of the Fisher-like condition (33) from our baseline model is

(60)

which we need in order to write the ZLB constraint on the Ramsey

problem.

An alternative to bargaining is price taking, in which buyers

and sellers each take the price of a unit of good in the DM,

, as given

and solve their respective demand and supply problems. The buyer's

problem is

(61)

subject to

.

In equilibrium this constraint binds, and we have

. The seller's problem is

(62)

with the first order condition

.

Using these two expressions, the two envelope conditions we need to

solve the problem of the household are given by

(63)

(64)

The analog of the Fisher-like condition (33) from our baseline model is

The government now collects revenue from capital income and

labor income taxation, along with money creation and debt issuance.

Its CM flow budget constraint is thus

Combining the relevant conditions derived in this section with

the ones that were unchanged from the basic model, we now list the

equilibrium conditions we use in writing the Ramsey problem.

Given policy variables

,

the technology realization

, the government spending

realization

, and initial condition

,

equilibrium is a set of processes satisfying

(67)

(68)

(69)

(70)

(71)

(72)

(73)

In the bargaining version, real money balances can be expressed as

Given policy variables

,

the technology realization

, the government spending

realization

, and initial condition

,

equilibrium is a set of processes satisfying (67), (71), (72), and

(73) along with

(76)

(77)

(78)

In the price-taking version, real money balances can be expressed

as

As we show in Appendix C.1, we can state the analog of

Proposition 1 for the model

with capital:

Proposition 3The allocations in a

monetary equilibrium in the model with capital satisfy the resource

constraint (72), the ZLB constraint

(75) for the bargaining model and

(80) for the price-taking model, and

the present-value implementability constraint (PVIC),

(81)

for the bargaining model and

(82)

for the price-taking model where the constant depends on

, and

,

(83)

With the introduction of capital, the term in the PVIC that is

related to the DM is similar to the one we derived in the basic

model, augmented by a new term

for the bargaining model and

for the price-taking model. As

we argued above, the expressions multiplying describe the DM return to

holding capital in each version of the model. In our basic model,

the surplus in a meeting between a buyer and seller was created due

to only the actions of the buyer, who had to choose money-holdings

prior to the meeting. Here, with capital, the seller also must make

a decision prior to the meeting in the form of investing in capital

in the previous CM. Because a household can be a buyer or a seller

with symmetric probabilities , the two terms in the PVIC related to the DM

represent the marginal surplus times the decision of the

household.

The Ramsey problem is to choose

to maximize

(84)

subject to the resource constraint (72), the PVIC ((81) for the bargaining model or (82) for the price-taking model), and the ZLB

constraint ((75) for the bargaining

model or (80) for the price-taking

model), taking as given

. In

Appendix C.2, we list the

conditions that characterize the solution to this problem, along

with the conditions that let us construct the policies and prices

that support the Ramsey allocation.

As was the case in the basic model, we are able to prove

analytically that the optimal nominal interest rate is positive for

the bargaining model with . For and for the price taking model, we must

resort to numerical methods.

Most of the discussion in this section will be very brief as

almost all the results from the basic model carry over to the model

with capital. We begin by proving that under bargaining we have an

optimal deviation from the Friedman Rule if .

Proposition 4

(Optimal Deviation from the Friedman Rule in the Model

with Capital under Bargaining) Under bargaining, if

, the optimal

policy features a strictly positive net nominal interest rate in

every period .

Proof. The proof follows very closely the one for the

basic model. With , we have that

and

, and

the first-order condition of the Ramsey problem with respect to

is given by

(85)

Because the multiplier under the Ramsey allocation as we prove in

the proof of Proposition 1, is strictly concave, , and

, the

right hand side is strictly positive. This in turn implies

, and

(86)

imposing

because

. But this

implies, by the equilibrium condition (75), that .

The intuition is as in the basic model: the essentiality of

money creates rents in the DM, which the Ramsey planner would like

to tax. In this version of the model, one can think of the rent in

the DM consisting of two parts, one due to holding money, realized

when the household is a buyer, and one due to holding capital,

realized when the household is a seller. The inflation tax is the

most direct way of taxing DM activity.

We follow the same solution strategy and adopt the same

functional forms as before with the following additions. The DM

cost function is

(87)

where

, and the

CM production function is standard Cobb-Douglas,

with

. We use

the parameter values provided in AWW.21 We keep the same stochastic processes

for and , but we alter and the level of steady-state

debt to match the same targets as in the basic model.

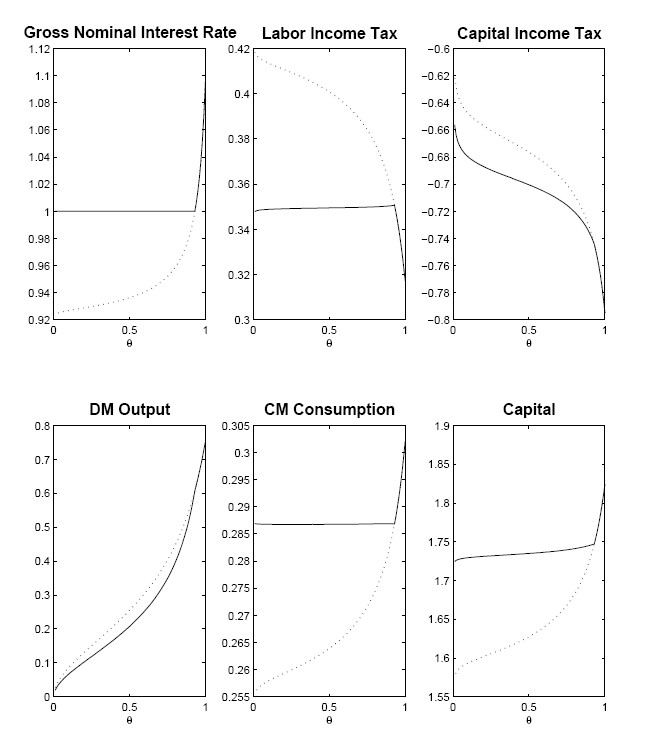

Figure 2 shows how the Ramsey steady-state varies with

with and

without the ZLB. As the upper left panel shows, the range of

over which the

ZLB constraint binds is clearly larger here than in Figure 1, but

this may be due to the somewhat different parametrizations across

models. It is important to note that due to Proposition 4, there will always be an interior

where the

Friedman rule will not be optimal for all

. Clearly, the same message as

in Section 4 comes through: when

is low enough,

the ZLB constraint binds and the Friedman Rule is optimal. But for

large enough -- in

particular for the interesting case -- the Friedman Rule is not optimal. Here,

not only is the Friedman Rule not optimal, but the optimal

inflation rate (not shown) is actually positive, around 7 percent,

in contrast to the small deflation that was optimal in the model

without capital.

The upper middle panel shows that the labor income tax rate is

roughly constant at about 35 percent over

,

then falls somewhat for higher values of . The intuition is just as

before: as the inflation tax begins generating revenue, the

distortionary labor income tax can be reduced.

The capital income tax rate is negative for all values of

, as the upper

right panel of Figure 2 shows. Indeed, for , it is relatively easy to

see that the steady-state capital tax rate in general is

non-positive. Dropping the ZLB constraint (because we know it does

not bind if ),

and using some simplifications that follow from our functional

forms, the steady-state version of the Ramsey first-order condition

with respect to capital is

(88)

where is the Ramsey

multiplier on the resource constraint and we have used the fact

that

and

. When

, the

steady-state household Euler equation for capital accumulation

reads

(89)

again using

. In a

standard Ramsey model, of course,

;

comparing the two conditions then readily shows that in steady

state, the optimal capital tax is zero. Here, however, using

(88) and (89)

and substituting in

,

we can solve for the capital tax rate,

(90)

As long as

and

, which

holds as long as , the limiting capital income tax rate is

negative. The crucial difference between our model and a standard

Judd (1985) or Chamley (1986) argument is that the presence of the

terms in the

implementability constraint, arising from the trading arrangements

in the DM, drive another wedge between the Ramsey and household

FOCs on capital.

In terms of the economics, there are two reasons for the capital

subsidy. First, there is a holdup problem for investment in this

model as long as , which is analogous to (and in addition

to) the money holdup problem in the basic model; this holdup

problem causes capital to be underaccumulated relative to the

efficient capital stock. Specifically, DM sellers bear the entire

cost of investment in capital but, unless , must share part of the

surplus created from capital with DM buyers. Seller thus do not

have the socially-correct incentive to accumulate capital. Second,

the deviation from the Friedman Rule itself causes an inefficiency

in the capital stock, along with other allocation variables. The

Ramsey planner subsidizes capital income in an effort to reduce the

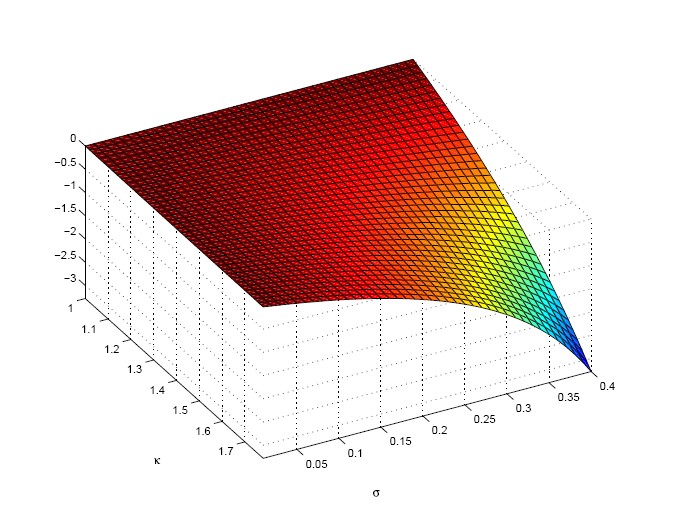

effects of both of these sources of inefficiency. In Figure 3, we

plot the steady-state value of the optimal capital income tax for

the case as we

vary and

.22 If , the DM shuts down and we recover the usual

result that capital income is not taxed (or subsidized) because

both of the channels just described are absent. If , capital is not a factor of

production in the DM and the holdup problem we mention above is not

present. As and

increase, the

optimal capital subsidy increases.

For our baseline parameter values, the capital income subsidies

in the range 60 to 80 percent that we find in Figure 2 are large,

but not out of line with capital subsidy rates found in other

Ramsey studies. For example, Schmitt-Grohe and Uribe (2005, Table

2) find an optimal capital subsidy rate of 44 percent in their

benchmark model featuring a host of real and nominal rigidities and

report that it can be as high as 85 percent.

Optimal policies and allocations in the price-taking version of

the model share the same characteristics as the bargaining version:

the optimal nominal interest rate is and the capital income subsidy is . The capital subsidy is lower

with price-taking because price-taking avoids the capital holdup

(as well as money holdup) problem inherent in Nash bargaining. If

somehow the Friedman rule had been part of the Ramsey policy, then

the optimal capital income tax with price-taking in fact would have

been zero.

In Table 2, we report simulation-based moments for the Ramsey

allocations and policy variables for the three versions of our

model with capital. While we track ex-post inflation as before, we

track the ex-ante capital income tax, following the convention in

much of the optimal capital taxation literature.23 Note that, unlike in the basic model,

both and shocks affect the Ramsey

solution in the models with capital. Also, while we do not

analytically prove they are constant, the simulated values for the

labor and capital income taxes and the nominal interest rate are

essentially constant.24 As such,

we do not report the second moments for these variables.

Turning to the results, in all three versions of the model, we

find that inflation is once again very stable, with a standard

deviation of about 20 basis points at an annual rate. This is in

line with the results of Chugh (2006a) and Schmitt-Grohe and Uribe

(2005) in that they both also find that, so long as prices are

flexible, capital accumulation does little to change the volatility

of Ramsey inflation relative to a flexible-price environment

without capital. That is, the volatility of Ramsey inflation has

nothing to do with whether or not there is capital accumulation. Of

course, in our basic model without capital, inflation was already

quite stable; this result carries over unchanged. The intuition for

the optimality of inflation stability is just as in the model

without capital: the relative price between CM and DM consumption

depends on the inflation rate, and distorting this relative price

imposes welfare costs so large that the Ramsey planner largely

refrains from varying inflation despite its ability to absorb

shocks to the government budget.

We view our work and results as a first step in taking more

seriously the new class of micro-founded models of money as a

laboratory for studying policy questions. Our central findings are

that the Friedman Rule is typically not the optimal policy and that

inflation fluctuates very little over time. These findings are

opposite those of the workhorse Chari, Christiano, and Kehoe (1991)

flexible-price Ramsey model. The presence of real frictions that

give rise to valued money also provide completely different

justification for a central bank's pursuit of inflation stability

than the typically-invoked ones of nominal rigidities.

There are of course a number of ways one might want to modify

our framework. Monopoly power in goods and labor markets are

thought by many to be important realistic features. It would be

straightforward to introduce monopoly power in the centralized

market. The results of Schmitt-Grohe and Uribe (2004a) and Chugh

(2006b) suggest that inflation in such an environment would be

partly a direct tax on the money rent we identify and partly an

indirect tax on producers' and labor suppliers' rents. It may be

interesting to know quantitatively how these direct and indirect

uses of the inflation tax interact.

Once one has monopoly power in the centralized market, one could

go further in adding elements monetary policy makers often think

are important, such as sticky prices and sticky wages. However,

given our finding of optimal inflation stability (albeit around a

non-zero average inflation rate), we do not see how the results

could be very different with such features.

Pushing our first step in different directions, another

interesting issue to study may be the nature of and solution to the

time-inconsistency problem of the Ramsey policy in this sort of

environment. It is not clear how the time-consistency results of,

say, Alvarez, Kehoe, and Neumeyer (2004) or Persson, Persson, and

Svensson (2006), would extend to our environment. Neither is it

clear how the emerging results in the new dynamic public finance

literature, which places at center stage distributional concerns,

might extend to a version of our environment in which money

holdings were allowed to differ across individuals.

Recent developments in understanding the micro-foundations of

monetary exchange are sometimes viewed as simply having provided

justification for the reduced-form models of money commonly used in

practice, not least of all because they superficially end up

resembling the reduced-form models. Our results throw into question

the conclusion that they must therefore yield the same answers to

interesting questions as existing models. We think it may be

worthwhile to re-examine a number of issues in monetary policy

using this now-tractable framework.

That allocations from a monetary equilibrium should satisfy the

CM feasibility condition (39)

and the zero-lower-bound constraint (42) is obvious.

Using the household optimality conditions (27 ), (31),

and (32) along with the equilibrium

conditions, we now derive the present-value implementability

constraint the Ramsey planner must respect. Begin as usual with the

CM household flow budget constraint,

(91)

To construct the present-value implementability constraint,

begin by multiplying the flow budget constraint by

and summing from

,

(92)

We point out that, as usual in a dynamic Ramsey problem assuming

commitment to the time-zero policy, any terms that appear in

intermediate expressions are eliminated by the law of iterated

expectations because the entire implementability constraint is

conditioned on the time-zero information set, hence the

. For ease of

exposition, we therefore proceed dropping operators that would appear in

intermediate expressions as well as the operator because it is

understood to be present in all subsequent expressions.

Substitute into the second term on the left-hand-side using

expression (32) to get

(93)

(94)

The second summation on the left-hand-side cancels with the the

last summation on the right-hand-side to leave only the initial

bond position,

(95)

(96)

Next, substitute into the second term on the left-hand-side

using (31) to get

(97)

(98)

Expand the second summation on the left-hand-side to get

(99)

(100)

Cancel the second summation on the left-hand-side with the second

summation on the right-hand-side to leave only the initial money

holdings,

(101)

(102)

Using (27), we can substitute

into the first term on the right-hand-side to get

Finally, from (31), we can make the

substitution

in the third summation on the left-hand-side. Cancelling

terms and reintroducing the operator leaves us with

(106)

which is the present-value implementability (PVIC) constraint for

the Ramsey problem in the LW model. Any allocation that satisfies

this restriction, the resource constraint, and the ZLB constraint

can be supported as a monetary equilibrium; furthermore, the

allocations from any monetary equilibrium can be described by these

three conditions.

The Kuhn-Tucker conditions for the problem in Section 3 are

(107)

(108)

(109)

(110)

and

(111)

We can represent the right-hand side of the PVIC in terms of

allocations as

(112)

where

is the

steady state real bond balances and variables without subscripts

are steady state values.

With these FOCs in hand, we proceed as follows. Imposing steady

state on these conditions, we solve for the steady state values of

allocations and the multiplier . Next, given and

, the

conditions above characterize

and (39) defines . Finally, we back out

policies

from (35) and (38) statically, and inflation can be

obtained from solving (37)

dynamically.

Here, we prove a claim we make in Section 4.1. To demonstrate that the deviation

from the Friedman Rule in our basic model is not proxying for a

sales tax in the DM, we modify our basic model. We introduce a

sales tax in the DM and show that the resulting Ramsey problem does

not have a solution in which the Friedman Rule holds. Our result

here is only for the case (which is equivalent to price-taking in the

DM), just as is our Proposition 2. It is somewhat easier to work with the

price-taking version to establish this result, which is why we use

this version here.

We introduce a DM sales tax in the following way: with

price-taking in the DM, buyers, taking

as

given, turn over

units of money in each transaction. The sellers must remit

to the government in

the next CM, which, given our timing assumptions, occurs in period

.25Equivalently, we can suppose that the

government receives the revenue in the DM but waits until the next

CM to spend it. Because the assets markets are not open in the DM,

the government cannot invest this extra revenue in an

interest-bearing asset.

The government's flow budget constraint in nominal terms is

thus

(113)

in which the appears

because it is only DM sellers in period (of which there is a measure

) that turn over

sales taxes to the government. Because in equilibrium,

(that is, any DM

meeting in which a transaction occurs leads to the buyer turning

over all his cash to the seller), we may write the

period- government

budget constraint as

(114)

If we sum the CM budget constraints of all households (a measure

of whom were

buyers in period and

thus enter period with no

money; a measure

of whom were sellers and thus enter period with

; and a measure

of whom did

not trade and thus have ), we have in equilibrium

(115)

Clearly, the government budget constraint and the summation of all

the households' budget constraints yields the CM resource

constraint. In the Ramsey problem, then, we can use the resource

constraint and the summation of all households' budget constraints,

which implies the government budget constraint is satisfied.

In order to solve the Ramsey problem, first let us derive the

equilibrium conditions with this new tax instrument in place. To

keep the discussion short, we simply point out the differences from

the conditions we derive above. The CM problem summarized in

(2)-(6) is

unchanged. In the DM, from the buyer's problem (derived as in, say,

Rocheteau and Wright (2005)), we get

(116)

The seller's problem can be written as

(117)

with the first order condition

, which leads to the following expression for :

(118)

This leads to the following equilibrium condition, which replaces

(37),

(119)

It is also straightforward to show that the analog of the

Fisher-like condition (33) from our

baseline model is

(120)

which we need in order to write the ZLB constraint on the Ramsey

problem. Note that in the main text we assumed

which is

simply a normalization because is in terms of utility. Using this, we have

. Also

note that by construction .

To construct the PVIC in this version of the model, we proceed

exactly as in Appendix A.1, using (115). The resulting PVIC is given by

(121)

As usual, the Ramsey problem is to maximize the consumer's lifetime

utility subject to the resource constraint, the PVIC, and the ZLB

constraint. In the timeless solution of the Ramsey problem, which

is what we restrict attention to, the initial tax rate

is

endogenous and equal to the steady-state implied by the Ramsey first-order conditions.

The sales tax has a natural upper bound, unity, but it does not

have a natural lower bound. Denote by the lower bound of

. We think

is the

most natural case to consider.

We proceed by stating and proving two lemmas. The first lemma

shows that the Ramsey planner always chooses

for all . The second lemma shows that if

, the

ZLB cannot be binding, meaning that the Friedman Rule cannot be a

part of the Ramsey policy. Thus, we establish through these two

lemmas that the Friedman Rule cannot be part of the Ramsey policy

even in the presence of a sales tax in the DM.

Lemma 1The solution to the Ramsey problem with a DM sales tax features

.

Proof. Associating the multiplier with the PVIC and the multiplier

with the ZLB

constraint

(122)

the Ramsey first-order-conditions with respect to is

if

(123)

In any monetary equilibrium, we have

.

This means

because solves

and

the utility function is strictly increasing. Examining this first

order condition and given that the utility function is strictly

increasing and strictly concave (and realizing the multipliers

and are non-negative), the

left-hand-side is strictly negative. This means the Ramsey planner

wants to choose the smallest possible ,

.

Lemma 2If

, the

solution to the Ramsey problem with a DM sales tax cannot feature a

binding ZLB constraint.

Proof. In Proposition 1, we implicitly had

and showed

the Friedman Rule was not optimal (meaning the ZLB constraint was

not binding). Now assume

. Given

that we focus on monetary equilibria (i.e.,

), we

have

. We know from the lemma above

that

. If

, then

, which means the

ZLB constraint is slack.

This completes our argument that if we introduce a sales tax in

the DM, the Ramsey problem has no solution that includes the

Friedman rule as part of the optimal policy.

The proof is similar to the proof of Proposition 1. Here we only show how to derive

the PVIC for the bargaining version of the model. The expression

for the price-taking version follows the same steps.

Having derived the implementability constraint for the LW model

in Appendix A.1, it is

straightforward to extend it for the AWW environment. Multiplying

the consumer's CM budget constraint by

and then summing

over dates and states beginning at as above, we have

(124)

where the ellipsis indicate that the other terms are the same as

those in (92). The

manipulations following (92) proceed just as before (with, of

course, now

included inside the function ), so we present here only the derivation of the