Interchange Fees and Payment Card Networks: Economics, Industry Developments, and Policy Issues

In many countries around the world, electronic card-based payments have been replacing older types of payments at a rapid rate. In the United States, use of both debit cards and credit cards has been rising rapidly, while check volumes have been declining. The increased use of electronic payment methods has generated a number of public policy debates. One prominent debate concerns interchange fees. This paper is intended to provide background for understanding the interchange fee debate. The paper describes the operation of a typical payment card system, presents a summary of the economic theory underlying interchange fees, and discusses various developments in the U.S. payment cards industry, as well as legal and regulatory developments abroad. The paper concludes with a discussion and critical evaluation of a number of potential policy interventions.

Interchange fees typically involve a payment from a merchant's bank to a card user's bank for each debit card or credit card transaction, are determined at the network level, and are the same for all banks participating in a network. These fees are generally passed through to merchants by their banks and comprise a large fraction of the fees that merchants pay to their banks for processing card transactions. Card-issuing banks often use a portion of their interchange fee revenue to encourage card use by offering their cardholders rewards, such as cash rebates or airline miles, that increase with card use. In recent years, increases in interchange fee rates, together with growth in the volume of card transactions, have led to a dramatic rise in the total value of interchange fee payments and, consequently, in merchants' cost of accepting payment cards. These cost increases have given rise to significant concerns among merchants.

Merchant concerns focus on the level and sometimes the very existence of interchange fees. Merchant groups and their supporters contend that a network-determined interchange fee serves as a means for otherwise competing banks to collude on their fees for card transactions and to avoid negotiation of fees with merchants. These parties argue further that the primary alternative available to merchants - rejection of a network's cards - is not a viable option in the case of the major card networks because customers have come to expect acceptance of those cards. As a result, merchants contend that the major card networks are able to set excessively high interchange fees, which lead to correspondingly high merchant fees, inflated incentives (i.e., rewards programs) for consumers to use the cards, and supranormal profits for the networks and their card-issuing banks. Merchants also raise concerns about restrictive network rules, such as honor-all-cards rules and no-surcharge rules.1

In contrast, the card networks and their supporters contend that payment cards provide substantial value to both consumers and merchants, and that interchange fees are essential for the proper operation of the card networks. They note that a common interchange fee standardizes the terms of exchange between the merchant's bank and the card user's bank and plays an economically important role in influencing the incentives of merchants to accept cards and consumers to hold and use them. These groups argue that, when setting its fees, a card network must recognize the need to attract consumers and merchants, both of whom are necessary for the card network to exist. In their view, the resulting fees attempt to balance the two sides of the payment card market to maximize the value of the network, including the value of card services for both consumers and merchants.

The core economic and policy issues concern the effects of interchange fees on the extent of card use and the welfare of different parties in the economy. In terms of efficiency, the key issue is whether current patterns of retail payments appropriately reflect the social costs and benefits of the various payment methods. If the transaction fees faced by either merchants or card users are too high (or too low), then some payment methods will be overused and others will be underused relative to the socially optimal outcome. However, determining whether observed patterns of card fees (including interchange fees) and card usage are socially optimal is an extremely difficult task.

In terms of equity, interchange fees and associated transaction fees can generate transfers among non-card users, card users, merchants, and banks that increase the welfare of some parties while reducing the welfare of others. High interchange fees could support low transaction fees (or high rewards) for cardholders, thereby potentially making card users better off. At the same time, if the net effect of card acceptance is to increase merchant costs, and if merchants do not set prices that vary by payment method, then merchant acceptance of cards could lead to higher retail prices for all consumers, including those who pay with alternative methods and receive none of the direct benefits associated with card use.

To consider these efficiency and equity issues, economists have recently developed theoretical models of the pricing of card services in payment card markets. These models generally suggest that a transfer payment between the merchant's bank and the consumer's bank (i.e., an interchange fee) may be necessary to induce efficient use of card-based payment methods. This transfer payment affects the costs of card transactions for those banks and, in turn, the transaction fees that they charge merchants and cardholders (i.e., merchant discounts and fees or rewards for card use). These fees ultimately influence the volume of transactions on a card system through their effect on the willingness of merchants to accept cards and consumers to use them for purchases. With an appropriately chosen interchange fee, a payment card will be used in a transaction whenever doing so yields a higher level of overall social welfare than would be obtained by using an alternative payment method. With such an interchange fee, the number of card transactions will be economically efficient.2 A few characteristics of an efficient interchange fee are worth noting:

- In general, an efficient interchange fee is not solely dependent on the cost of producing a card-based transaction nor is it equal to zero.

- An efficient interchange fee may yield prices for card services to each side of the market that are "unbalanced" in the sense that one side pays a higher price than the other.

- The efficient interchange fee for a particular card network is difficult to determine empirically.

Whether the private marketplace and competition in that marketplace will yield interchange fees that are efficient is an open question. The conclusions of the theoretical literature vary substantially, depending on the assumptions underlying the models. Although no findings are completely robust, most models suggest that, when merchant prices do not vary by payment method,

- Profit maximization does not, in general, lead a network to set an interchange fee at the efficient level.

- In theory, privately-set interchange fees can be either too high or too low relative to the efficient interchange fee, depending on a number of factors, including the cost and demand considerations underlying the merchant decision to accept cards and the extent of competition among issuing and acquiring banks.

- In most markets, an increase in the level of competition among firms generates downward pressure on prices; however, this is not necessarily true for interchange fees. In general, competition among payment networks is unlikely to exert downward pressure on interchange fees because the networks tend to focus their competitive efforts on getting their card to be the favored card of a consumer. This objective is facilitated by having a higher interchange fee that can be used to fund more attractive terms (e.g., lower fees and higher rewards) for the consumer. In the special case where all consumers hold and use the cards of multiple networks and are indifferent with respect to which network's card they use for a given transaction, competition among card networks can lead to lower interchange fees.

Extensive legal and regulatory activity worldwide reflects the intensity of the debate over interchange fees and payment cards. In several countries, central banks or competition authorities have taken action aimed at reducing interchange fees. In the United States, a consolidated class action antitrust lawsuit pitting numerous merchants and merchant groups against Visa, MasterCard, and their member banks is pending in the U.S. District Court for the Eastern District of New York. In addition, Congress has held hearings on interchange fees, and members of Congress have introduced several bills concerning them.

Motivated by this increased attention to pricing in payment card markets, this paper discusses and evaluates a number of potential policy interventions for the payment cards industry, which reflect both actions that authorities in other countries have taken and proposals that have been advanced by various parties in the United States. These interventions include

- Clarifying or eliminating restrictions on differential retail pricing across payment methods;

- Prohibiting network determination of interchange fees;

- Regulating the level of interchange fees;

- Relaxing card acceptance requirements;

- Mandating "multi-bugged" cards that can perform transactions on multiple networks with merchant control of network routing rules; and

- Doing nothing.

A number of common concerns arise in connection with all of these policy options. In particular, the effects of any intervention are uncertain and may involve unintended consequences. Among these possible consequences is the unintended redistribution of costs and benefits of card transactions across merchants, banks, card users, and non-card users. In addition, although much of the debate over payment cards has focused on interchange fees in credit card systems, similar issues arise for debit card systems as well as other card systems that do not have explicit interchange fees. A narrow intervention that targets interchange fees for credit cards could have effects on competition and pricing throughout the retail payments market.

In addition to these general concerns, each of these options has specific benefits and costs that should be carefully considered by policymakers before taking any legislative or regulatory action. The various options differ in their transparency and ease of implementation, as well as in the extent to which they may be able to redress any potential inefficiencies in the payment card market.

I. Introduction

In many countries around the world, electronic card-based payments have been replacing older types of payments at a rapid rate. In the United States, use of both debit cards and credit cards has been rising, while check volumes have been declining. In addition, the amount of cash in circulation has been growing more slowly in recent years.3 This transition from paper-based payment methods to electronic payment methods has certainly modernized the payment system; however, it is not clear whether the incentives inherent in the current payment system infrastructure will lead participants to make socially optimal choices among alternative payment methods. In addition, increased use of electronic payment methods has generated a number of public policy debates.

One prominent policy debate concerns interchange fees.4 These fees, which typically involve a payment from a merchant's bank to a card user's bank for each debit card or credit card transaction, are determined at the network level and are generally the same for all banks participating in a network.5 Merchants' banks generally pass the costs associated with interchange fees through to merchants. In recent years, increases in interchange fee rates, together with growth in the volume of card transactions, have led to a dramatic rise in interchange fee payments, and consequently in merchants' cost of accepting payment cards.6 As a result of these developments, merchants have increasingly expressed concern about their costs associated with card transactions.

Merchant concerns focus on the level and sometimes the very existence of interchange fees. Merchant groups and their supporters contend that a common interchange fee serves as a means for otherwise competing banks to collude on their fees for card transactions and to avoid negotiation of fees with merchants. These parties argue further that the primary alternative available to merchants - rejection of a network's cards - is not a viable option in the case of the major card networks because customers have come to expect acceptance of those cards. As a result, merchants contend that the major card networks are able to set excessively high interchange fees, which lead to correspondingly high merchant fees, inflated incentives (i.e., rewards programs) for consumers to use the cards, and supranormal profits for the networks and their card-issuing banks.7

In contrast, the card networks and their supporters contend that payment cards provide substantial value to both consumers and merchants, and that interchange fees are essential for the proper operation of the card networks.8 They note that a common interchange fee standardizes the terms of exchange between the merchant's bank and the card user's bank and plays an economically important role in influencing the incentives of merchants to accept cards and consumers to hold and use them. These groups argue that, when setting its fees, a card network must recognize the need to attract consumers and merchants, both of whom are necessary for the card network to exist. In their view, the resulting fees attempt to balance the two sides of the payment card market to maximize the value of the network, including the value of card services for both consumers and merchants.

Extensive legal and regulatory activity worldwide reflects the intensity of the debate over interchange fees and payment cards. In several countries, central banks or competition authorities have taken action aimed at reducing interchange fees. In the United States, a consolidated class action antitrust lawsuit pitting numerous merchants and merchant groups against Visa, MasterCard, and their member banks is pending in the U.S. District Court for the Eastern District of New York. In addition, Congress has held hearings on interchange fees, and members of Congress have introduced several bills concerning them.

The core economic and policy issues concern the effects of interchange fees on the extent of card use and the welfare of different parties in the economy. In terms of efficiency, the key issue is whether current patterns of retail payments appropriately reflect the costs and benefits of the various payment methods. If the transaction fees faced by either merchants or card users are too high (or too low), then some payment methods will be overused and others will be underused relative to the socially optimal outcome. In particular, high fees for merchants and low or negative fees for card users may cause overuse of payment cards, or certain types of payment cards, relative to alternative payment methods. However, determining whether observed patterns of card fees (including interchange fees) and card usage are socially optimal is an extremely difficult task.

In terms of equity, interchange fees and associated transaction fees can generate transfers among non-card users, card users, merchants, and banks that increase the welfare of some parties while reducing the welfare of others. For example, high interchange fees could support low transaction fees

(or high rewards) for cardholders, thereby potentially making card users better off. However, if the net effect of card acceptance is to increase merchant costs (that is, if card acceptance fees exceed any reduction in merchants' transaction costs due to card acceptance), and if merchants do not

set prices that vary by payment method, then merchant acceptance of cards could lead to higher retail prices for all consumers, including those who pay with alternative methods and receive none of the direct benefits associated with card use.9![]() 10

10

This paper is intended to provide background for understanding the current debate surrounding interchange fees. It presents a comprehensive, yet accessible, description of the economic theory underlying interchange fees, as well as a discussion of industry trends and the regulatory environment relevant to the debate. More specifically, section II describes the operation of a typical payment card system and the various parties and fees, including interchange fees, associated with each transaction. Section III then examines the economic theory that has been developed to analyze payment card systems. It examines the role that interchange fees play in this market, and in particular, the role that interchange fees play when externalities are present. The determination of the socially optimal level of interchange fees and the question of whether the private market will attain that level are also discussed.

Section IV turns from the theoretical to the institutional and empirical, describing the recent history of payment card use and pricing in the United States. It discusses the structure and nature of competition within the industry in order to highlight the various dynamics affecting interchange fees. The next two sections discuss recent developments affecting the payments industry: Section V describes recent innovations by participants in the payment card industry, and section VI focuses on regulatory and legal developments in the United States and abroad. Finally, section VII discusses and evaluates a series of options that are representative of the types of policy measures that have been or could be proposed to address concerns associated with interchange fees.

II. Basic Features of U.S. Payment Card Systems

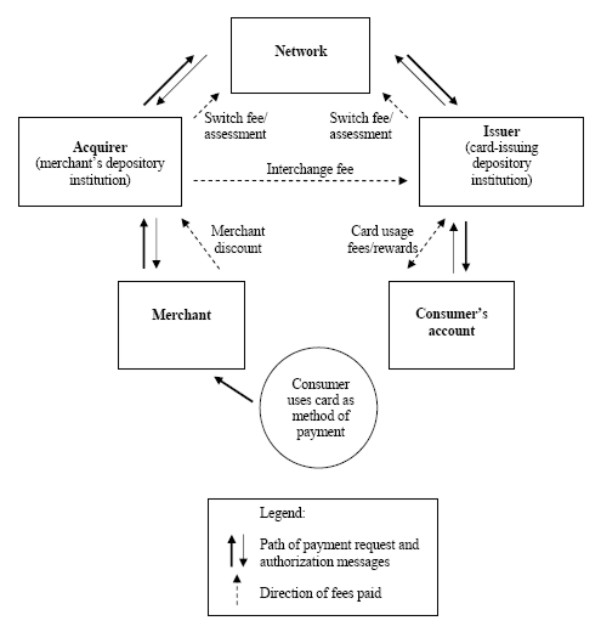

There are three main types of payment card transactions: credit, signature debit, and PIN debit.11 Two main organizational forms for general purpose payment card systems, often referred to as four-party and three-party systems, currently operate in the United States.12 The so-called four-party system is the model used for most card transactions and is employed by Visa and MasterCard for their credit card and signature debit card operations, as well as by all the PIN debit card networks.13 The four parties in the system are the consumer, the depository institution that issued the payment card to the consumer (the issuer), the retail merchant, and the merchant's depository institution (the merchant acquirer). The network coordinates monetary transfers and the transmission of information between the issuing and acquiring sides of the market.14 In a three-party system, the network itself acts as both issuer and acquirer. Thus, the three parties involved in a transaction are the consumer, the merchant, and the network. American Express and Discover have traditionally used this form, although both have expanded their card programs in recent years to include depository institution issuers.15

As illustrated in figure 1, a typical transaction over a four-party system proceeds as follows. The consumer initiates a purchase by presenting his or her card or card information to a merchant.16 An electronic authorization request with a specific dollar amount and the cardholder's identity is sent from the merchant to the acquirer to the network, which forwards the request to the card-issuing institution.17 The transaction is checked against a file of active card accounts that resides with either the card issuer or its processor. A message authorizing (or declining) the transaction is returned to the merchant via the reverse path.

Subsequently, the issuer posts a charge for the transaction to the cardholder's account, and the acquirer posts a credit for the transaction to the merchant's account. The timing of these charges and credits varies depending on the arrangements that cardholders and merchants have with their respective banks. For PIN debit transactions, the cardholder charges are posted immediately following the receipt of the authorization message. For credit and signature debit transactions, the issuer usually posts the transaction to the consumer's account within one day of the transaction.18 The acquirer usually credits the merchant's account within four days of the transaction (though the acquirer often credits the merchant's account much sooner, especially in the case of PIN debit).19

At the end of a business day, the merchant submits records of all card transactions for that day to its acquirer.20 The acquirer reconciles these data against the earlier authorization information and transfers the reconciled data to the network. The network then clears the transactions; that is, it determines the net financial positions, including interchange fees and other network fees, as discussed below, of all issuers and acquirers. Usually within two days for credit and signature debit card transactions and one day for PIN debit card transactions, banks settle their accounts; that is, they receive and send payments based on their net financial positions through their accounts at settlement banks associated with the network.

Various fees are involved in every payment card transaction.21 In a four-party system, an interchange fee is paid by the merchant acquirer to the card issuer.22 The network collects a switch fee (or assessment) from the acquirer and the issuer. The acquirer charges the merchant a merchant discount, which is the difference between the face value of the transaction and the amount the acquirer transfers to the merchant. In some cases, consumers pay fees to or receive rewards from their card issuers for each card transaction.

An interchange fee typically comprises a large fraction of the merchant discount for a particular card transaction.23![]() 24 An interchange fee may take the form of a flat fee per transaction, a

percentage of the purchase price, or a combination of the two. As discussed in more detail in section IV, interchange fees for credit and signature debit transactions generally exceed those for PIN debit transactions. In the United States, interchange fees for PIN debit typically average $0.35 to

$0.50 per transaction; interchange fees for a typical signature debit transaction are about 1.2 percent of the transaction value; and interchange fees for a typical credit card transaction for Visa and MasterCard are in the range of 1.5 to 2 percent of the transaction value. Interchange fees also

vary by merchant type (e.g., grocery store, department store, fast food restaurant), merchant sales volume, and credit card program within a network (e.g., "premium" cards such as gold or platinum cards may carry higher interchange fees than "basic" cards).

24 An interchange fee may take the form of a flat fee per transaction, a

percentage of the purchase price, or a combination of the two. As discussed in more detail in section IV, interchange fees for credit and signature debit transactions generally exceed those for PIN debit transactions. In the United States, interchange fees for PIN debit typically average $0.35 to

$0.50 per transaction; interchange fees for a typical signature debit transaction are about 1.2 percent of the transaction value; and interchange fees for a typical credit card transaction for Visa and MasterCard are in the range of 1.5 to 2 percent of the transaction value. Interchange fees also

vary by merchant type (e.g., grocery store, department store, fast food restaurant), merchant sales volume, and credit card program within a network (e.g., "premium" cards such as gold or platinum cards may carry higher interchange fees than "basic" cards).

A noteworthy feature of an interchange fee is that it is set by the network that carries the transaction, and not by the individual card issuers that receive the fee from acquirers. Until recently, both the Visa and MasterCard networks were organized as joint ventures of their member banks. Some observers have argued that, under this ownership structure, the setting of a common interchange fee by the network for all member banks could be interpreted as collective price determination by the member banks. This approach towards setting interchange fees, and the possibility that it could constitute illegal collusion under the antitrust laws, is one of the points of controversy surrounding payment card networks. As discussed in section V, however, both Visa and MasterCard have recently converted to publicly traded companies. The implications of these reorganizations for the disposition of antitrust complaints regarding collective price determination are unclear.

In addition to setting the structure and level of interchange fees, each card network specifies operating rules that govern how network participants interact. Although contracts are written only between the network and its issuers and acquirers, merchants and processors must also comply with the network rules or risk losing access to that network.25 Network operating rules cover a broad range of activities, including merchant card acceptance practices, technological specifications for cards and terminals, risk management, and determination of transaction routing when multiple networks are available for a given transaction.

The operating rules include some key provisions that have important ramifications for the operation of the networks. First, each network requires a merchant that agrees to accept a given type of card to accept that type of card regardless of the identity of the card issuer or specific card program. For example, a merchant that accepts Visa credit cards must accept all Visa credit cards and may not reject a particular bank's Visa credit card or a Visa credit card associated with a particular rewards program. This type of universal acceptance requirement is commonly referred to as an honor-all-cards rule.26 Such rules are significant because a network's interchange fees may vary across card programs. Specifically, premium cards, typically associated with generous rewards programs for card users, tend to carry higher interchange fees than basic cards.

Another important operating rule is the no-surcharge rule, which prohibits a merchant from adding a surcharge to a customer's bill if the customer pays with one of the network's payment cards.27![]() 28 (Exceptions to this rule include certain payments to government entities and tuition payments to educational institutions.) As required by the Cash Discount Act, the networks generally do allow merchants to offer discounts for cash payments.29 Merchant groups allege that the card networks place restrictions on the form that such discounts may take, but other industry observers deny that such

restrictions exist.30 In addition, although discounts for cash and surcharges for cards may appear at first to be equivalent, allowing only a cash discount

effectively prohibits differential pricing across types of cards.

28 (Exceptions to this rule include certain payments to government entities and tuition payments to educational institutions.) As required by the Cash Discount Act, the networks generally do allow merchants to offer discounts for cash payments.29 Merchant groups allege that the card networks place restrictions on the form that such discounts may take, but other industry observers deny that such

restrictions exist.30 In addition, although discounts for cash and surcharges for cards may appear at first to be equivalent, allowing only a cash discount

effectively prohibits differential pricing across types of cards.

III. The Economics of Payment Cards

Payment card markets are often described by economists as being two-sided. A two-sided market is a market for the provision of a product whose value is realized only if a member of each of two distinct and complementary sets of users simultaneously agrees to its use (Rochet and Tirole 2006a). A payment card has value only if a merchant and the merchant's customer agree on its use to carry out a transaction. The two-sided nature of demand for payment cards has important implications for pricing that are absent in standard markets. In particular, the prices faced by the two sides of the market must be set at levels that "balance demand," because a payment card that appeals to one side of the market will not be used if it does not also attract the other side of the market.

In a four-party card system, a payment card transaction can be characterized as a product jointly supplied by the card issuer and the merchant acquirer, and jointly demanded by the consumer and the merchant. Each of these parties experiences benefits and costs from engaging in a payment card transaction; the difference between a party's benefits and costs constitutes that party's economic surplus from a card transaction. A card transaction is economically efficient if the sum of the surplus accruing to all of the parties involved is non-negative - that is, if the sum of the benefits that all of the parties derive from using a card is greater than or equal to the sum of the costs incurred by all of the parties. However, the parties will agree to conduct a card transaction only if the surplus realized by each of the individual parties is non-negative. The fact that efficiency depends on aggregate costs and benefits while actual use of a card depends on the separate decisions of several distinct parties implies that, in the absence of transfer payments, some efficient card transactions may not in fact take place (Baxter 1983).

The example in table 1 illustrates how transfer payments can facilitate efficient card transactions that would not otherwise occur. Suppose that the issuer and acquirer each incur a production cost of $.50 for a card transaction. Assuming that they do not derive any direct benefit from the transaction, the issuer and acquirer each obtain a surplus of -$.50. In addition, suppose the merchant derives benefits of $2.25 while incurring costs of $.25, yielding a surplus of $2 for the merchant. Similarly, suppose the consumer experiences a benefit of $.50 and a cost of $.75, yielding a surplus of -$.25.31 As shown in the first column of table 1, use of the card to perform the transaction between the merchant and consumer is efficient, producing an aggregate surplus of $.75. However, in the absence of a transfer payment, none of the parties, except for the merchant, would be willing to participate in a card transaction.

Now, assume that the merchant is required to pay a transfer equal to $1.50, divided equally among the other three parties, as illustrated in the second column of table 1. With this transfer, each party would derive a non-negative surplus from the card transaction and therefore all parties would be willing to participate. Thus, transfer payments can provide a mechanism for improving efficiency in a two-sided market by redistributing private benefits and costs in a way that leads private decision makers to choose a more socially efficient outcome.

More formally, the two-sided nature of the market for payment cards introduces the possibility of externalities. An externality arises when one agent's action affects the welfare of another agent, without any compensation for the effect. Because an agent's private incentives in the presence of an externality do not reflect the true social cost or benefit of his or her actions, socially inefficient outcomes can result.

The economics literature has emphasized the importance of two potential externalities in the context of payment cards (Rochet 2003). The first, described in the numerical example above, has been termed the usage externality and arises because each party in a given transaction evaluates his or her own costs and benefits associated with a particular payment method, but does not consider the costs and benefits of the other party. A second type of externality, referred to as a network (or adoption) externality, reflects the fact that the value of a payment card network increases for both merchants and consumers as the card becomes more ubiquitous. In other words, a larger cardholder base makes card acceptance more valuable for merchants, while broader merchant acceptance makes cardholding more attractive for consumers. When deciding whether to accept cards, the merchant may not account for the increased network value associated with his or her acceptance. Similarly, a consumer's decision about whether or not to hold a card may not account for the effect of his or her decision on the value of the overall network.32

A standard economic prescription to deal with externalities involves adjusting prices (through taxes, subsidies, or transfers) so that agents' private incentives reflect the true social costs and benefits of their decisions. In the context of payment cards, this involves appropriate pricing of card services for all of the parties involved in a card transaction. How this could be accomplished depends on the organizational form of the card system. In the three-party card system (in which the network itself is both issuer and acquirer), the network could, theoretically, set transaction prices for consumers and merchants that would align private and social costs and benefits. In a four-party card system, the network cannot directly set transaction fees for merchants and consumers. It can, however, establish an interchange fee - a transfer payment between the merchant's bank (acquirer) and the consumer's bank (issuer) - that influences the costs of card transactions for those banks and the transaction fees that they subsequently charge merchants and consumers (i.e., merchant discounts and card use fees or rewards). As a result, an interchange fee can, at least theoretically, improve efficiency by internalizing externalities.

It is important to recognize that an interchange fee is not the only tool that can serve this purpose. The four-party systems also charge switch fees (payments from acquirers and issuers directly to the network, sometimes called assessments), which could be used to influence prices of card transactions for the two sides of the market, even if the interchange fee were zero (Katz 2005). Particularly in light of the recent corporate restructurings of Visa and MasterCard, the four-party card systems could substitute these types of direct fees (and possibly rebates) to acquirers and issuers for explicit interchange fees. However, the economic considerations underlying the pricing of payment card services, from both a social and a private perspective, do not depend on whether a card system uses an interchange fee between banks or direct fees to participating banks.33

III.A Efficient Interchange Fees

An efficient interchange fee would lead to a socially optimal number of payment card transactions. That is, with an efficient interchange fee, a payment card would be used in a transaction if and only if using the card would result in a non-negative change in total surplus. Technically, the number of card transactions would be such that the marginal social benefit of the last card transaction would be equal to its marginal social cost. A few characteristics of an efficient interchange fee are worth noting:34

- An efficient interchange fee transfers surplus (i.e., costs and benefits) from one side of the market to the other in order to internalize the external effect that one party has on the other. In general, an efficient interchange fee is not solely related to the cost of producing a card-based transaction nor is it equal to zero.

- In order to provide appropriate incentives to parties in a transaction, an efficient interchange fee may yield prices for card services to each side of the market that are "unbalanced" in the sense that one side pays a higher price than the other. Indeed, efficiency may, in some cases, require a negative price for one side of the market.

- Even in the simplest case, the efficient interchange fee can be difficult to determine. At a minimum, calculation of the efficient interchange fee requires estimation of the demand curves for card services for heterogeneous consumers and merchants, in addition to precise cost data for acquirers, issuers, merchants, and consumers.

In summary, the basic economic role of an interchange fee is to affect the prices of card services for the merchant and the consumer in a transaction. Both prices are important because, unlike in a standard market where a single agent makes an independent purchase decision, two parties must jointly agree to use a particular payment service. The card transaction will not take place unless both parties agree to participate given the prices they face (Schmalensee 2002, Rochet and Tirole 2002). Efficient prices induce each party in a transaction to account for the external costs and benefits resulting from his or her behavior, factors that a self-interested agent might otherwise not consider. An appropriate interchange fee is one way to achieve such prices for card services.

III.B A common interchange fee in four-party card systems

As noted in section II, the fact that interchange fees (for a given combination of transaction type, merchant category, and card program) are the same for all issuing and acquiring banks is a highly controversial aspect of the four-party card networks. Because the previous discussion about efficient interchange fees does not rely on a common interchange fee, it is natural to ask whether a common, pre-determined interchange fee between banks in a four-party card network is necessary at all.

In the absence of a common interchange fee, banks would need to negotiate bilateral fee agreements with each other. In a system with thousands of banks, the number of such bilateral agreements would be quite large. Even if bilateral negotiation of fees between banks were feasible, the existence of a common interchange fee plays a key role in establishing the value of a four-party card network. In particular, a common interchange fee facilitates the maintenance of an honor-all-cards rule, and some sort of honor-all-cards rule is a core feature of a four-party card network. The logic is as follows: In the absence of common terms of exchange between banks, each issuer could set its own interchange fee. However, an honor-all-cards rule would require that every merchant that accepts a particular network brand and type of card (e.g., Visa credit card) accept every card with that brand and type, regardless of the level of the interchange fee set by the issuer. As a result, an honor-all-cards rule with bilaterally negotiated interchange fees would introduce the possibility of a "holdup problem" (Small and Wright 2002, Klein et al. 2006). That is, an individual issuing bank could demand very high interchange fees from acquiring banks. The acquirers would then factor the high fees charged by this issuer into the merchant discounts that they charge their merchants.35 A merchant, in turn, could avoid those fees only by rejecting all of a network's cards of that type, in which case card acceptance could be inefficiently low. A common interchange fee avoids this holdup problem.

As an alternative solution to this holdup problem, a card network could drop its honor-all-cards rule, allowing merchants to reject an individual issuer's cards if they carried inordinately high fees. However, without the acceptance guarantee provided by some sort of honor-all-cards rule, a consumer would need to ascertain whether each individual merchant's acceptance policy applied to the consumer's specific card. The complexity involved in obtaining or providing this information would substantially diminish the value of the network. Consequently, some observers have argued that a common interchange fee does not serve as a purely collusive mechanism for banks to set excessive and anticompetitive fees; rather, it allows a four-party card network to maintain an honor-all-cards rule, some form of which is an important factor underlying the value of the network (Klein et al. 2006).36

III.C Private determination of interchange fees

In light of these potentially important roles of a common interchange fee, a crucial question remains: Will the private marketplace, and competition in that marketplace, yield interchange fees that are efficient? Competition is generally viewed as an effective mechanism for providing incentives that lead private agents to make choices that yield efficient outcomes. Hence, the central question is whether a card network, in competition with other card networks and payment methods, has appropriate incentives to choose an interchange fee that yields efficient prices to both sides of the market.

The conclusions of the theoretical literature vary substantially depending on the assumptions underlying the models.37 Assumptions about the degree of market power for acquiring banks, issuing banks, merchants, or networks, and the elasticities of demand for card services and final goods all influence the results. While no findings are completely robust, a number of common themes do emerge regarding privately-set interchange fees, when merchant prices do not vary by payment method.

- Although a card network's objective to maximize profits (for itself or its member banks) requires the network to recognize the two-sided nature of demand, profit maximization does not, in general, lead the network to set the interchange fee at the level that maximizes social welfare.

- Privately optimal interchange fees will typically yield an unbalanced price structure (i.e., a price structure in which the two sides of the market pay different prices), a common feature of two-sided markets, both in theory and in practice. Many models of payment card systems find that unbalanced prices are necessary to achieve efficiency; however, it does not follow that any privately determined pattern of unbalanced prices is efficient.

- In theory, privately-set interchange fees can be too high or too low relative to the efficient interchange fee, depending on a number of factors.38 However, the incentives underlying merchants' card acceptance decisions in the theoretical models tend, all else equal, to support interchange fees that are higher than the social optimum. In such a situation, merchant fees will be inefficiently high and card use fees will be inefficiently low (or card rewards will be inefficiently high), leading to excessive card use.39

The economic theory literature has emphasized two closely related reasons why merchants may be willing to accept cards with inefficiently high merchant fees. First, by increasing a merchant's "quality of service," card acceptance makes a merchant more attractive to consumers, leading to an increase in sales volume.40 The merchant will take into account this private benefit when he or she evaluates the costs and benefits of card acceptance. To the extent that this increase in sales represents a diversion of transactions away from other merchants that do not accept cards, without any increase in aggregate sales, the private benefit to the merchant from its decision to accept cards will exceed the social benefit. As a result, the merchant will be willing to pay an inefficiently high merchant discount.41

Second, as long as some merchants are willing to accept cards despite an inefficiently high merchant discount, others will feel compelled to do so in order to avoid losing business. Thus, even if merchant discounts are high enough that merchants as a whole would be better off rejecting cards, they may nonetheless all choose to accept cards because no single merchant would find it profitable to unilaterally reject them.42

Although most of the theoretical literature examines the price-setting behavior of a monopoly payment card network, some recent models consider the effects of competition among networks for issuers and their associated cardholders (Guthrie and Wright 2007, Rochet and Tirole 2002, 2006b, Chakravorti and Roson 2006). In these models, network competition has varying effects on interchange fees, depending crucially on the cardholding behavior of consumers. Specifically, if consumers tend to hold and use the cards of multiple networks and are indifferent with respect to which network's card they use for a given transaction, then competition between card networks should tend to lower interchange fees because merchants can choose to accept only the cards that provide the most favorable terms for them, without losing customers. The empirical evidence, however, suggests that even though most consumers do hold multiple cards, they tend to favor a single card when making purchases (e.g., the card that provides the greatest rewards).43 In this case, competition is unlikely to exert downward pressure on interchange fees because competition between networks is focused on becoming the favored card of a consumer, an objective that is facilitated by a higher interchange fee, which can be used to fund more attractive terms for the consumer. Moreover, heterogeneity among consumers with respect to their preferred card makes it difficult for merchants to reject cards from networks that have high interchange fees. Regardless of the direction in which it pushes interchange fees, competition between card systems is not a sufficient condition to yield an efficient interchange fee.44

Finally, the actual distribution of total surplus associated with card transactions (i.e., the difference between benefits and costs for each of the parties involved) under a privately determined interchange fee depends on how merchant fees affect the end prices of goods and services. Merchants that accept cards may adjust their product prices to reflect the effect of card transactions on their costs. Thus, if the net effect of card acceptance is to increase merchant costs, merchants may increase their product prices, leading to a possible decline in both sales volume and merchant surplus. At the same time, if all consumers pay the same price regardless of the payment method used, consumers who use other payment methods (e.g., cash) would bear some of the costs associated with card transactions without receiving the benefits that accrue to card users.45 The possibility of a transfer of surplus to card users from users of other payment methods is often viewed as a regressive redistribution due to the fact that card users tend to have higher incomes than non-card users.

IV. Payment card use and pricing in the United States

Two major trends underlie the recent increase in attention to interchange fees among both merchants and policymakers: the shift away from checks and cash toward card payments, and changes in the level and structure of interchange fees. As shown in figure 2 and table 2, both the number and the total value of debit card payments grew dramatically between 1990 and 2006.46 The Federal Reserve estimates that, by either measure, debit card payments approximately tripled between 2000 and 2006, with average annual growth rates close to 20 percent. At the same time, the number and value of credit card payments increased at annual rates of roughly six percent and nine percent, respectively. Given the relatively rapid growth in debit card use as compared with credit card use, the Federal Reserve estimates that the number of debit card transactions exceeded the number of credit card transactions by 2006.47 However, because the average value of a credit card transaction substantially exceeds the average value of a debit card transaction, the total value of credit card transactions is still significantly larger than that of debit card transactions.48

In contrast, as seen in table 2, the Federal Reserve estimates that the number of checks paid by depository institutions declined at a rate of approximately 5 percent per year between 2000 and 2006. Although direct evidence regarding the number of cash payments is not available, indirect evidence suggests that cash use may be declining (or at least growing more slowly) as well.49 As of 2005, card transactions are estimated to have comprised more than half of total retail sector transactions, and their share has continued to rise.50

IV.A Interchange Fees

Contemporaneous with the increase in the share of purchases conducted with cards, network-determined fees for card payments have risen, and the pricing structures have become more complex. For many years, the interchange fee for an individual card transaction at a given merchant has varied with transaction type (credit, signature debit, or PIN debit) and purchase value. Interchange fees also vary across merchants according to merchant type (e.g., supermarket or gas station) and merchant sales volume, and the number of distinct merchant types listed in interchange fee schedules continues to proliferate. Recently, Visa and MasterCard have introduced interchange fees that vary across card programs, even for a given merchant type and sales volume.

Figure 3 shows the path of interchange rates over time (monthly), by network and transaction type.51 Visa and MasterCard carry all three types of transactions, with separate interchange schedules for each. PIN debit interchange is shown for Visa's Interlink network, MasterCard's Maestro network, and the four leading regional PIN debit networks (Star, NYCE, Pulse, and Accel/Exchange). The three-party credit card systems (American Express and Discover) are excluded from this diagram because they do not have explicit interchange fees.52 Instead, they negotiate merchant service charges directly with merchants and do not report the rates publicly.

As figure 3 shows, interchange rates for basic credit cards rose during the early 2000s, a trend that began in the 1990s. These rates have plateaued over the past 3 years, possibly due, at least in part, to increased regulatory scrutiny abroad and civil litigation in the United States. It is worth noting, however, that the interchange fees associated with Visa's and MasterCard's premium rewards cards are markedly higher than the interchange fees associated with their basic credit cards.

Credit card interchange fees have been above signature debit card interchange fees since 2003, and both credit and signature debit interchange fees have consistently exceeded PIN debit interchange fees. Several possible explanations account for these differences. A possible demand- or market-power-based reason for higher credit card interchange fees is the broad penetration of Visa and MasterCard and the associated consumer expectation that merchants accept these credit cards (that is, merchants agree to accept cards with high interchange fees to avoid losing business), as described in section III.C. Another reason why credit interchange fees may be higher than those of debit is to compensate for the credit risk taken on by the issuing bank in extending credit (over the billing cycle or longer) for the full amount of the transaction.

The difference between signature and PIN debit interchange fees, which has diminished considerably in recent years, may be due to several factors. First, prior to 2003, Visa's (MasterCard's) honor-all-cards rule required merchants who accepted Visa's (MasterCard's) credit cards to also accept its signature debit cards. This rule placed pressure on merchants to accept signature debit. During that period, Visa and MasterCard maintained signature debit interchange rates at essentially the same levels as their credit card interchange rates. In 2003, a settlement agreement reached in a lawsuit that had been filed against Visa and MasterCard eliminated the tying of signature debit card acceptance to credit card acceptance and required a reduction in signature debit interchange fees.53 As shown in figure 3, implementation of this settlement agreement led to a decline in signature debit interchange fees, but did not completely eliminate the differential between signature debit and PIN debit fees.

Second, the differential between PIN and signature debit interchange fees may reflect more intense competition among PIN debit networks due to the presence of multiple brands on a given card. In the early days of PIN debit, each network covered a fairly small geographic area, and many banks sought to offer their customers wider merchant acceptance of their PIN debit cards by "multi-bugging" the cards (i.e., issuing cards that bore the logos of and could be used on multiple PIN networks).54 Over time, individual networks expanded their geographic coverage through a combination of mergers and organic growth, and in some cases, networks' geographic regions began to overlap one another. In this environment, merchant acquirers or their processors could often choose which one of the networks whose brands appeared on a card would carry the transaction. Merchants generally prefer that their acquirers route PIN debit transactions over the network with the lowest interchange fee, resulting in direct price competition among PIN debit networks. More recently, this price competition appears to have diminished (and, as shown in figure 3, PIN debit interchange fees have risen) as the largest national PIN debit networks have increasingly required issuers to sign exclusive agreements under which they become the sole PIN network whose logo appears on an issuer's cards (Breitkopf 2007).

The need to encourage merchant investment in PIN terminals may also have contributed to relatively low PIN debit interchange fees, particularly in the early years of PIN debit. In contrast, signature debit, which utilizes the same infrastructure as MasterCard and Visa credit cards, does not require merchant investment in new equipment. In addition, higher fraud costs (due to the lack of a PIN requirement) for signature debit may have led to higher signature debit interchange fees compared to PIN debit.

Turning to variation in the structure of interchange fees at a given point in time, figure 4 illustrates interchange fee schedules over a range of possible purchase values at a moderate-sized general-purpose retailer, by transaction type and network, at year-end 2008. Each interchange fee has a minimum value and then rises with the purchase amount.55 Until very recently, all of the PIN debit networks capped their interchange fees; however, both Interlink and Pulse removed their caps in 2008 (Musante 2008), while NYCE removed its cap in early 2009.56 Fees for credit and signature debit are not capped.57

Although interchange fees have historically varied by merchant type, the number of merchant types has recently proliferated. In addition, over the past three to five years, Visa and MasterCard have established rate schedules that vary across credit card programs. Figure 5 shows a few examples of credit card interchange fees for different types of merchants and card programs.58 These schedules show wide variation - the basic card used at a large-volume supermarket generates a fee just over 1 percent of the purchase value, while the fee for the highest-reward card used at any merchant exceeds 2 percent. Merchants frequently express concern about the variation in fee schedules across card programs for two reasons. First, at the time of a transaction, they cannot determine the interchange fee associated with the particular card used by the customer.59 Second, and perhaps more important, each network's honor-all-cards rule requires merchants to accept all cards of a given type (i.e., credit or signature debit) within that network and not to exclude cards associated with specific rewards programs.

IV.B Industry Structure

The pricing developments described above have occurred during a period of consolidation and shifting market shares among payment networks, card issuers, and merchant acquirers. The underlying causes of consolidation vary across segments of the payment card industry; nonetheless, the resulting market structure places a large share of consumer payment system operations in the hands of a relatively small number of service providers. The discussion below highlights some of the trends in concentration and market shares for each set of providers and explores some competitive implications of these trends.

IV.B.1 Network Market Structure

Concentration among card networks is important from a policy perspective; recent litigation and calls for regulatory intervention focus on the market power of the largest networks. Specifically, the largest networks are setting the terms of trade among merchants, cardholders, acquirers, and issuers for a large share of all purchase transactions.

Figure 6 shows network shares of transactions over time by type of transaction.60![]() 61 As shown in the top panel, Visa's and MasterCard's individual shares of credit card transactions have remained

relatively constant over the past several years, with Visa and MasterCard holding respective shares of 44 percent and 31 percent as of 2007. American Express and Discover followed with shares of 18 percent and 7 percent, respectively.

61 As shown in the top panel, Visa's and MasterCard's individual shares of credit card transactions have remained

relatively constant over the past several years, with Visa and MasterCard holding respective shares of 44 percent and 31 percent as of 2007. American Express and Discover followed with shares of 18 percent and 7 percent, respectively.

Signature debit transactions run almost exclusively over the Visa and MasterCard credit card infrastructure and were estimated by the Federal Reserve to comprise about 63 percent of total debit card transactions in 2006, as shown in table 2.62 This large share is likely due to a number of factors that influence merchant acceptance and customer card use, including (1) Visa's and MasterCard's earlier honor-all-cards rules (overturned in the 2003 court settlement discussed in section VI), which required merchants that accepted a network's credit cards also to accept like-branded signature debit cards; (2) aggressive marketing programs by Visa and MasterCard, aimed at both issuers and consumers, including higher interchange fees for issuers and the associated rewards programs for card users; and (3) the ease of adoption of signature debit relative to PIN debit due to the fact that no new equipment beyond credit card readers need be installed.63 Within signature debit, Visa has held a large and fairly stable share, with about 75 percent of transactions in 2007, as shown in the second panel of figure 6.

PIN debit transactions are less concentrated than either credit card transactions or signature debit transactions, and the PIN debit transaction shares of the networks have exhibited greater variation over time. The third panel of figure 6 shows the transaction shares of what are now the top four PIN debit networks (Interlink, Star, NYCE, and Pulse), over time.64 There is a marked contrast between the positions of Visa and MasterCard in this market segment: Interlink, Visa's PIN debit network, experienced rapid growth in recent years and was the largest PIN debit network in 2007, with a transaction share of 37 percent, while Maestro, MasterCard's PIN debit network, had only a negligible transaction share.

The various developments in the debit card arena over the past decade have resulted in an increase in Visa's and MasterCard's shares of all debit card transactions. In particular, the continued growth of signature debit and the dominant position of Visa and MasterCard in that segment have yielded a combined share near 77 percent of all debit card transactions in 2007, as shown in the fourth panel of figure 6. Due to the additional expansion of its PIN debit operations, Visa alone has seen its share grow to almost 61 percent of all debit card transactions as of 2007.

Across all card transactions, Visa and MasterCard's combined share has increased slightly since 2001, mainly due to Visa's growing share of debit card transactions, as shown in the last panel of figure 6. As of 2007, the combined share of Visa and MasterCard stood at about 76 percent of all card transactions. The remaining card transactions were divided among American Express (7.4 percent), Star (6.3 percent), Discover (including the Pulse PIN debit network) (5 percent), and a number of small PIN debit networks.

IV.B.2 Issuer Market Structure

Issuer concentration is of interest for several reasons. First, credit card issuers serve as important points of access for consumer credit, in addition to serving as providers of a means of conducting purchase transactions. Second, debit cards now represent an important tool for accessing deposits, through either purchases or withdrawals. Finally, card issuer concentration is important for network competition because (1) an individual issuer may serve on the board of a four-party payment card network, and therefore may be able to influence its pricing behavior, and (2) large issuers could potentially serve as competitors to either credit or debit card networks by abandoning the existing networks and forming new networks, either on their own or in conjunction with other issuers. The potential effect of this type of entry on interchange fees is unclear.

Figure 7 shows that the 3-firm issuer concentration ratio of total credit card dollar volume (black line) rose from 48 percent in 2003 to 57 percent in 2007, if the three-party networks (American Express and Discover) are included as issuers.65 Excluding the three-party networks, the increase in the 3-firm concentration ratio was more rapid, from 49 to 63 percent over the same period (red line). The two identifiable increases in concentration are the direct result of the Bank One - JP Morgan Chase merger in 2004 and the purchase of MBNA by Bank of America in 2005.66

The top panel of table 3 shows market shares of the major credit-card issuers in 2007.67 American Express had the largest market share, with 25 percent of volume. Excluding the three-party issuers, JP Morgan Chase was the top bank card issuer in 2007 with a market share of 25 percent of volume, followed by Bank of America and Citigroup with shares of 21 percent and 18 percent, respectively.68 The distribution of market shares drops off quickly after the top three bank card issuers. If the three-party issuers are included, then the top ten issuers accounted for approximately 90 percent of all credit card volume in 2007.

As seen in middle and bottom panels of table 3, the top issuers for signature and PIN debit differ somewhat from those for credit cards because, unlike credit cards, debit shares are closely linked to relationships with deposit account customers. Debit shares are also affected by the marketing efforts - including rewards programs - of both the individual banks and the national networks to induce customers to use their debit cards (particularly for signature transactions). Some regional variation exists in overall debit card use due to merchant acceptance as well as marketing by the regional PIN debit networks.69 The 3-firm concentration ratios in figure 7 show both signature and PIN debit issuing, as measured by dollar volume, to be historically less concentrated than credit card issuing. As of the end of 2007, the signature debit 3-firm concentration ratio had risen slightly since 2000 to 37 percent, and the analogous PIN ratio stood at 48 percent. However, the recent acquisitions of Wachovia by Wells Fargo, Washington Mutual by JP Morgan Chase, and Merrill Lynch by Bank of America have substantially increased the concentration of debit card issuance. Adjusting the 2007 year-end numbers to account for these acquisitions yields 3-firm concentration ratios of 53 percent and 62 percent for signature debit and PIN debit, respectively.

IV.B.3 Acquirer Market Structure

Since 2000, concentration levels for acquiring payment transactions have also increased. As shown in figure 8, the 3-firm acquiring concentration ratio for all types of card transactions rose from 48 percent in 2000 to 62 percent in 2007.70 By transaction type, the 3-firm concentration ratio for credit and signature debit was 49 percent in 2000, rising to 62 percent by 2007.71 The increase for PIN debit is more substantial, with a rise in the 3-firm concentration ratio from 52 percent to 78 percent over the same period. As shown in table 4, First Data held the largest share of all acquired transactions (credit, signature debit and PIN debit combined) as of 2007, with its share conservatively estimated at around 32 percent.72 Bank of America and Chase ranked second and third, with shares of about 18 and 12 percent, respectively.

The market for acquiring differs substantially from the market for payment networks or for card issuing.73 Acquiring services are not strongly "brand-based;" that is, acquiring services obtained from different providers are very close substitutes for each other since no provider's service is particularly unique. Although there are substantial (indeed, overwhelming) scale economies, there is no obvious network effect. In other words, a merchant's benefit from using a given acquirer will depend on the prices and services of that acquirer, but will not depend on the number of other merchants who also use that acquirer. Furthermore, a merchant's customers generally have no preference for or knowledge of the identity of its acquirer. A merchant may therefore choose relatively freely among existing acquirers. (The limits on this free choice derive from multi-year contracts, bundled services, and other switching costs.) In addition, although fixed costs may serve as a barrier to entry, a new entrant could likely provide the data processing functions of merchant acquirers after an initial investment and scaling-up period. Nonetheless, some evidence suggests that the share of the total merchant discount received by acquirers (as opposed to flowing through to issuers in the form of interchange) has increased recently. One recent estimate is that for smaller merchants, roughly one third of their fees is paid to the acquirers (including independent sales organizations, which serve as resellers of acquirer services), while two thirds is passed along as interchange.74

IV.B.4 Issuers, Acquirers, and Processors as Potential Competitors to Networks

Individual issuer and acquirer market shares - particularly in combination - are important in the context of network competition. A bank with a substantial share of card issuance, large transaction volume, and well-established merchant acquiring relationships has considerably greater potential to enter the market successfully as a new network than would a de novo firm. Entry for a new network is difficult in part because of the two-sided nature of the market: In order to attract issuers to join the network, enough merchants must have joined on the acquiring side, while in order to attract merchants to join, a sufficient number of individuals must hold the network's cards. A firm that already serves as both a large issuer and a large acquirer would begin with a substantial built-in base of users on each side of the market, and could therefore enter more easily than could a network starting from scratch to attract either set of users.

Similarly, processors that provide services to merchants or acquirers on one side of the market and issuers on the other side could potentially serve as competitors to the existing networks. A processor serving both sides of the market could, at least in theory, provide on-us processing in which transactions are authorized, cleared, and settled by the processor itself without using any of the existing networks.75 Alternatively, the existence of such processors could facilitate the entry of new card networks affiliated with issuers that have large existing cardholder bases or acquirers with large numbers of merchant contracts.

V. Recent industry developments

A number of recent industry developments may affect the competitive environment in which payment card systems operate. These include changes in the organizational forms of Visa and MasterCard, adaptations of the business model of American Express and Discover, and the development of new credit and debit card products, some of which rely on the automated clearinghouse (ACH) system.

One notable development over the past few years has been the conversion of Visa and MasterCard from not-for-profit, membership-based organizations to for-profit, publicly traded firms. MasterCard converted from a membership organization to a private share corporation in 2002, and its initial public offering (IPO) on the New York Stock Exchange occurred in 2006. In March 2008, Visa completed its IPO. Commentators have speculated that these conversions were motivated, at least in part, by a desire to limit possible antitrust liability, although the implications of the conversions for such liability are unclear (Shinder 2009). Even if these organizational changes alleviate antitrust concerns, it is unclear how they may affect the behavior of the two companies. The networks state that their objective is to maximize the number of transactions that they carry, an objective that is furthered by establishing an interchange fee that rewards issuers and consumers for using the network.

In recent years, both American Express and Discover have begun to allow bank issuance of their respective brands' credit cards. This change followed a 2001 court decision (discussed in the next section) that Visa and MasterCard could not prohibit banks that issue their cards from also issuing American Express or Discover cards. This change is likely to intensify competition among the networks for card-issuing banks. However, as discussed earlier, competition among networks for issuers does not necessarily lead to downward pressure on interchange rates, because networks can attract issuers and card users by setting higher interchange fees.

Several companies have tried, with varying degrees of success, to introduce new payment card products. While some of these products aim to compete directly with the existing networks by reducing merchants' card acceptance costs, others build on the existing card networks. The types of entry that have occurred largely represent either competition to undercut high merchant fees or attempts to capture interchange fee revenue. Although the former may be expected to place downward pressure on interchange fees, the latter is unlikely to do so. Appendix III describes some of the specific products that have been introduced.

VI. Regulatory and Legal Developments in the United States and Abroad

In a number of countries throughout the world, payment card systems have been targeted for investigation and, in some cases, for regulatory or legal action, by the courts, the competition authority, or the central bank. This section reviews regulatory and legal developments in the United States, Australia, and other countries.

VI.A United States

In the United States, concerns about interchange fees and rules imposed on merchants by the card networks have been addressed mainly through private litigation, with occasional government intervention through antitrust lawsuits. Thus far, there have been no direct regulatory interventions.76

The first and most prominent civil case that addressed interchange fees was filed in 1979. In this case, National Bancard Corp. (NaBanco) asserted that Visa's interchange fees constituted illegal price fixing. The courts decided in favor of Visa in 1984, stating that interchange fees were a legitimate mechanism to transfer costs from the side of the market that the court determined to have lower costs (merchant acquirers) to the side with higher costs (card issuers), thereby inducing the side bearing the greater cost to participate.77

In another influential case initiated in 1998, the U.S. Department of Justice filed a Sherman Act complaint against Visa and MasterCard that addressed two practices.78 First, both networks contractually prohibited card issuers from issuing cards on other competing networks, such as Discover and American Express (exclusivity).79 Second, Visa and MasterCard had overlapping members on their corporate boards (duality), resulting in a mechanism by which the two networks could potentially collude. The court's decision, reached in 2001, stated that Visa and MasterCard's dual board memberships were not a Sherman Act violation, but that exclusivity was. As a result of this decision, no credit card issuer may be prohibited by any payment network from issuing cards on a competing network. As previously noted, following the decision, a number of banks that issue cards on the Visa and MasterCard networks have begun to issue cards on the American Express or Discover networks as well.

In 1996, a number of merchants and retail trade associations filed lawsuits against Visa and MasterCard challenging the networks' rules that required merchants that accepted their credit cards to also accept their signature debit cards (the honor-all-cards rules). The various lawsuits were combined into a single, consolidated action, which became known as the Wal-Mart case.80 In 2003, the Wal-Mart case was settled, with Visa and MasterCard agreeing to pay over $3 billion in damages and to rescind partially the honor-all-cards rules.81

In 2005 and 2006, a large number of retail merchants and trade associations filed approximately fifty civil lawsuits in U.S. courts against Visa, MasterCard, and several card-issuing banks alleging, among other charges, that interchange fees are too high and that the collective setting of interchange fees by members of the payment card associations constitutes illegal price fixing under U.S. antitrust laws. A large number of these lawsuits were consolidated into a single class action lawsuit that is pending in the U.S. District Court for the Eastern District of New York.82 In recent testimony before Congress, a witness on behalf of MasterCard stated that the two sides have agreed to mediation, in an effort to resolve the lawsuit.83

In the past few years, merchant organizations have expressed their concerns to Congress about interchange fees and network operating rules. Both the Senate and the House have held multiple hearings on those topics.84 In 2008, members of both chambers introduced legislation aimed at addressing a number of concerns associated with interchange fees and various rules and practices of payment card networks.85

VI.B Australia

The Australian government established a Payments System Board (PSB) at the Reserve Bank of Australia (RBA) in 1998, which was given responsibility for promoting competition, efficiency, and stability in the payment system. The PSB undertook extensive data collection and analysis, leading to the publication in October 2000 (together with the Australian Competition and Consumer Commission) of Debit and Credit Card Schemes in Australia: A Study of Interchange Fees and Access (RBA Study).

The RBA Study concluded that credit and debit card interchange fees were well above the levels that could be justified on the basis of costs, and that these fees were not subject to the normal forces of competition.86 To address these issues, the RBA imposed a number of reforms on the Australian payment system. Key elements of these reforms included (i) requiring the Visa and MasterCard networks to remove their no-surcharge rules, and (ii) imposing standards that required substantial reductions in credit and debit card interchange fees.

Since the reforms were implemented, the number of merchants levying surcharges on credit card transactions has increased steadily, and interchange fees have fallen. As of year-end 2007, about 10 percent of small merchants, 15 percent of large merchants, and 23 percent of very large merchants imposed surcharges.87 The average interchange fee in the MasterCard and Visa systems fell from about 0.95 percent prior to the reforms to about 0.50 percent after the reforms, and the decline in interchange fees led to a significant reduction in merchant service fees. At the same time, the average value of cardholder rewards has declined, and average annual cardholder fees have risen.88

In September 2006, the RBA launched a comprehensive review of its reforms to Australia's payment card systems. Preliminary conclusions from this review were released in April 2008, and final conclusions were published in September 2008.89 The RBA concluded that

(T)he reforms have met their key objectives. They have: increased transparency; improved competition by removing restrictions on merchants and liberalising access; and promoted more appropriate price signals to consumers. Nevertheless ... the Board remains of the view that the competitive forces acting on interchange fees are still relatively weak.90

In light of the improvements in the competitive environment, the RBA is prepared to remove the existing interchange fee regulations if industry participants take appropriate steps to ensure that interchange fees do not rise above their current levels. In August 2009, the RBA will assess the extent to which industry participants have addressed its concerns. If it is satisfied with the measures they have taken, it will deregulate interchange fees; otherwise, regulation will be continued and strengthened.

VI.C Other Countries

In a large and growing number of countries, authorities have taken steps aimed at reducing or eliminating common interchange fees.91 In several countries, including New Zealand, Poland, and the United Kingdom, competition authorities have determined that multilateral setting of interchange fees is illegal and must be discontinued. In Spain, the competition authority denied the legally-required authorization of the payment card schemes' interchange fee agreements and instructed the schemes to submit new plans for authorization. In other cases, either the competition authority (e.g., Switzerland) or the central bank (e.g., Mexico) has reached an agreement with the card issuers to reduce interchange fees. No-surcharge rules have been examined in a number of countries and have been eliminated in the Netherlands, Sweden, and the United Kingdom.92