Board of Governors of the Federal Reserve System

International Finance Discussion Papers

Number 898, June 2007 --- Screen Reader Version*

Three Great American Disinflations

NOTE: International Finance Discussion Papers are preliminary materials circulated to stimulate discussion and critical comment. References in publications to International Finance Discussion Papers (other than an acknowledgment that the writer has had access to unpublished material) should be cleared with the author or authors. Recent IFDPs are available on the Web at http://www.federalreserve.gov/pubs/ifdp/. This paper can be downloaded without charge from the Social Science Research Network electronic library at http://www.ssrn.com/.

Abstract:

This paper analyzes the role of transparency and credibility in accounting for the widely divergent macroeconomic effects of three episodes of deliberate monetary contraction: the post-Civil War deflation, the post-WWI deflation, and the Volcker disinflation. Using a dynamic general equilibrium model in which private agents use optimal filtering to infer the central bank's nominal anchor, we demonstrate that the salient features of these three historical episodes can be explained by differences in the design and transparency of monetary policy, even without any time variation in economic structure or model parameters. For a policy regime with relatively high credibility, our analysis highlights the benefits of a gradualist approach (as in the 1870s) rather than a sudden change in policy (as in 1920-21). In contrast, for a policy institution with relatively low credibility (such as the Federal Reserve in late 1980), an aggressive policy stance can play an important signalling role by making the policy shift more evident to private agents.

Keywords: monetary policy regimes, transparency, credibility, sacrifice ratio.

JEL classification: E32, E42, E52, E58

Acknowledgements: We thank Gauti Eggertson, Benjamin

Friedman, Dale Henderson, Jinill Kim, Lee Ohanian, Thomas Sargent,

Anna Schwartz, Lars Svensson, John Taylor, Francois Velde, Marc

Wiedenmeier, and Tack Yun for helpful comments and suggestions, as

well as seminar participants at the annual American Economic

Association Meeting in Chicago, Columbia University, the Federal

Reserve Board, the Federal Reserve Bank of San Francisco, Harvard

University, the fourth International Research Forum on Monetary

Policy conference, and at an NBER workshop honoring Anna Schwartz.

Bordo received financial support from the Federal Reserve Board on

this project. The views expressed in this paper are solely the

responsibility of the authors and should not be interpreted as

reflecting the views of the Board of Governors of the Federal

Reserve System or of any other person associated with the Federal

Reserve System.

1 Introduction

Since at least the time of David Hume (1752) in the mid-18th century, it has been recognized that episodes of deflation or disinflation may have costly implications for the real economy, and much attention has been devoted to assessing how policy should be conducted to reduce such costs. The interest of prominent classical economists in these questions, including Hume, Thornton, and Ricardo, was spurred by practical policy debates about how to return to the gold standard following episodes of pronounced wartime inflation.1Drawing on limited empirical evidence, these authors tried to identify factors that contributed to the real cost of deflation, including those factors controlled by policy. They advocated that a deflation should be implemented gradually, if at all; in a similar vein a century later, Keynes (1923) and Irving Fisher (1920) discussed the dangers of trying to quickly reverse the large runup in prices that occurred during World War I and its aftermath.

While the modern literature has provided substantial empirical evidence to support the case that deflations or disinflations are often quite costly , there is less agreement about the underlying factors that may have contributed to high real costs in some episodes, or that might explain pronounced differences in costs across episodes.2 Indeed, disagreement about the factors principally responsible for influencing the costs of disinflation helped fuel contentious debates about the appropriate way to reduce inflation during the 1970s and early 1980s. Many policymakers and academics recommended a policy of gradualism-reflecting the view that the costs of disinflation were largely due to structural persistence in wage and price setting-while others recommended aggressive monetary tightening on the grounds that the credibility of monetary policy in the 1970s had sunk too low for gradualism to be a viable approach.

In this paper, we examine three notable episodes of deliberate monetary contraction: the post-Civil War deflation, the post-WWI deflation, and the Volcker disinflation. One goal of our paper is to use these episodes to illuminate the factors that influence the costs of monetary contractions. These episodes provide a fascinating laboratory for this analysis, insofar as they exhibit sharp differences in the policy actions undertaken, in the credibility and transparency of the policies, and in the ultimate effects on inflation and output. Our second objective is to evaluate the ability of a variant of the New Keynesian model that has performed well in fitting certain features of post-war U.S. data to account for these historical episodes.

Our paper begins by providing a historical overview of each of these episodes. In the decade following the Public Credit Act of 1869, which set a 10 year timetable for returning to the Gold standard, the price level declined gradually by 30 percent, while real output grew at a robust 4-5 percent per year. We argue that the highly transparent policy objective, the credible nature of the authorities' commitment, and gradual implementation of the policy helped minimize disruptive effects on the real economy. By contrast, while prices fell by a similar magnitude during the deflation that began in 1920, the price decline was very rapid, and accompanied by a sharp fall in real activity. We interpret the large output contraction as attributable to the Federal Reserve's abrupt departure from the expansionary policies that had prevailed until that time; fortunately, because the ultimate policy objective was clear (reducing prices enough to raise gold reserves), the downturn was fairly short-lived. Finally, the Volcker disinflation succeeded in reducing inflation from double digit rates in the late 1970s to a steady 4 percent by 1983, though at the cost of a severe and prolonged recession. We argue that the substantial costs of this episode on the real economy reflected the interplay both of nominal rigidities, and the lack of policy credibility following the unstable monetary environment of the previous 15 years.

We next attempt to measure policy predictability during each of the three episodes in order to quantify the extent to which each deflation was anticipated by economic agents. For the two earlier periods, we construct a proxy for price level forecast errors by using commodity futures data and realized spot prices. While these commodity price forecast errors provide very imperfect measures of errors in forecasting the general price level, we believe that they provide useful characterizations of the level of policy uncertainty during each period: in particular, the commodity price forecast errors in the early 1920s were much larger and more persistent than in the 1870s. This pattern confirms other evidence on policy predictability during each episode taken from bond yields, contemporary narrative accounts, and informal surveys. Finally, for the Volcker period, we utilize direct measures of survey expectations on inflation to construct inflation forecast errors, and show that forecast errors were large and extremely persistent, suggesting a high degree of uncertainty about the Federal Reserve's policy objectives.

We then examine whether a relatively standard DGSE model is capable of accounting for these different episodes. The model that we employ is a slightly simplified version of the models used by Christiano, Eichenbaum, and Evans (2005) and Smets and Wouters (2003). Thus, our model incorporates staggered nominal wage and price contracts with random duration, as in Calvo (1983) and Yun (1996), and incorporates various real rigidities including investment adjustment costs and habit persistence in consumption. The structure of the model is identical across periods, aside from the characterization of monetary policy. In particular, we assume that the monetary authority targets the price level in the two earlier episodes, consistent with the authorities desire to reinstate or support the Gold standard; by contrast, we assume that the Federal Reserve followed a Taylor-style interest rate reaction function in the Volcker period, responding to the difference between inflation and its target value. Moreover, we assume that agents had imperfect information about the Federal Reserve's inflation target during the Volcker episode, and had to infer the underlying target through solving a signal extraction problem.

We find that our simple model performs remarkably well in accounting for each of the three episodes. Notably, the model is able to track the sharp but transient decline in output during the 1920s, as well as generate a substantial recession in response to the monetary tightening under Volcker. More generally, we interpret the overall success of our model in fitting these disparate episodes as reflecting favorably on the ability of the New Keynesian model - augmented with some of the dynamic complications suggested in the recent literature - to fit important business cycle facts. However, one important twist is our emphasis on the role of incomplete information in accounting for the range of outcomes.

Finally, we use counterfactual simulations of our model to evaluate the consequences of alternative strategies for implementing a new nominal target (i.e., either a lower price level, or a lower inflation rate). We find that under a highly transparent policy regime, a new nominal target can be achieved with minimal fallout on the real economy, provided the implementation occurs over a period of at least 3-4 years. In this vein, we use model simulations to show that a more predictable policy of gradual deflation - as occurred in the 1870s - could have helped avoid the sharp post-WWI downturn. However, our analysis of the Volcker period emphasizes that the strong argument for gradualism under a transparent and credible monetary regime becomes less persuasive if the monetary regime lacks credibility. In this lower credibility case, an aggressive policy stance can play an important signalling role insofar as it makes a policy shift - such as a reduction in the inflation target - more apparent to private agents. Because inflation expectations adjust more rapidly than under a gradualist policy stance, output can rebound more quickly.

The rest of the paper proceeds as follows. Section 2 describes the three episodes, while Section 3 examines empirical evidence on the evolution of expectations during each episode. Section 4 outlines the model, and Section 5 describes the calibration. Section 6 matches the model to the salient features of the three episodes, and considers counterfactual policy experiments. Section 8 concludes.

2 Historical Background

2.1 The Post-Civil War Episode

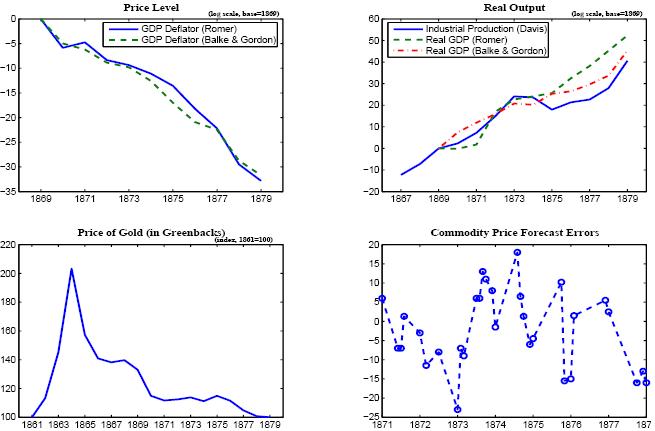

Given the high cost of financing the Civil War, the U.S. government suspended gold convertibility in 1862 and issued fiat money ("greenbacks"). The monetary base expanded dramatically in the subsequent two years, precipitating a sharp decline in the value of greenbacks relative to gold. The dollar price of a standard ounce of gold rose from its official price of $20.67 that had prevailed since 1834 to over $40 by 1864 (the lower panel of Figure 1 shows an index of the greenback price of gold relative to its official price of $20.67). Despite some retracing in the late stages of the war, the dollar price of gold remained about 50 percent above its official price by the cessation of hostilities in mid-1865.

Following the war, there was widespread support for reverting to a specie standard at the pre-war parity. In the parlance of the period, this meant eliminating the "gold premium," the difference between the market price of gold and the official price. Using simple quantity theory reasoning, policymakers regarded monetary tightening as the appropriate instrument for achieving this objective: if the overall price level fell sufficiently, the dollar price of gold would drop, and the gold premium eventually disappear. Accordingly, Congress passed the Contraction Act in April 1866, with the backing of President Johnson. This act instructed the U.S. Treasury - the effective monetary authority during that period - to retire the supply of greenbacks. Given initial public support for a quick return to convertibility, the Treasury proceeded aggressively, reducing the monetary base about 20 percent between 1865 and 1867. However, the sharp price deflation that ensued had a contractionary impact on the economy, with certain sectors experiencing disproportionate effects (e.g., heavily leveraged farmers). Thus, Congress and President Johnson were forced to temporarily suspend monetary tightening in the face of strong public protest (Friedman and Schwartz, 1963).

President Grant promised to renew the march toward resumption when he delivered his first inaugural in March 1869, but with the important difference that the deflation would be gradual. The president received key legislative support with the passage of the Public Credit Act of 1869, which pledged that the Federal Government would repay its debt in specie within ten years. The long timeframe reflected the new political imperative of a gradualist approach. With further monetary contraction deemed infeasible, supporters of resumption planned to keep the money stock roughly constant, and allow prices to fall slowly as the economy expanded. This philosophy helped guide legislation, and in turn the U.S. Treasury's operational procedures for conducting monetary policy. Thus, Treasury policy kept the monetary base fairly constant through most of the 1870s, offsetting the issuance of National Bank notes with the retirement of Greenbacks. The Treasury's ability to adhere to this policy was facilitated by the passage of the Resumption Act in 1875, which sealed January 1, 1879 as the date of resumption of convertibility, and by the election of the hard-money Republican candidate Rutherford Hayes in the 1876 election.

As seen in the upper-left panel of Figure 1, these policies succeeded in producing a fairly smooth and continuous decline in the aggregate price level, and allowed the authorities to comfortably meet the January 1879 deadline for the resumption of specie payments. Furthermore, as shown in the upper-right panel, all three of the available measures of real output grew at a fairly rapid and steady pace over the period from 1869 to 1872. Of course, the worldwide financial panic of 1873 had marked consequences for U.S. markets and economic activity; nevertheless, real output growth over the decade of the 1870s was remarkably strong, averaging about 4 to 5 percent per year.3

This strong economic growth in the face of persistent deflation seems to have been made possible because of the slow and fairly predictable nature of the price decline between the passage of the Public Credit Act in 1869 and resumption a decade later. Two factors played an important role in making the price decline predictable. First, the ultimate objective of restoring the gold price to its official (pre-war) level was highly credible. This served to anchor expectations about the long-run expected price level within a fairly narrow range, so that uncertainty about the future price level mainly reflected uncertainty about the path of the real value of gold (in terms of goods). Second, it was clear after 1868 that the target of restoring convertibility would be achieved gradually. As discussed above, there was little support in Congress for returning to the rapid pace of monetary contraction that followed the Civil War.

Our contention that the policy of restoring gold convertibility at the official pre-war price was highly credible may seem difficult to reconcile with the political agitation in favor of Greenbacks that seemed a salient feature of the 1870s. But support for the Gold standard - both within the U.S. government, and the public at large - remained extremely strong in the post-Civil War period, so that the net effect of the political agitation was simply to graduate progress towards convertibility.4 This support for resumption stemmed in part from historical precedent: the United States had been on a specie standard for almost its entire history, dating to the passage of the Coinage Act of 1792. It also reflected deeply-seated views about how a specie standard protected private property rights against unjust seizure, which was regarded as a moral and political imperative.

Overall, this analysis suggests that it is appropriate to characterize the U.S. deflation experience over at least the 1869-79 period as one in which both the final objective of policy was transparent and credible, and which implied a fairly clear path for the overall price level. Moreover, the authorities appeared to place a large weight on minimizing the adverse consequences to the real economy, and hence were content to achieve convertibility gradually in an environment of predictable deflation.5

2.2 The Post-WWI Episode

The U.S. government suspended the gold standard de facto shortly after it entered World War I and began an enormous arms build-up that fueled inflation. President Wilson ordered the suspension and placed an embargo on the export of gold in order to protect the country's stock. In the absence of the embargo, high inflation likely would have triggered large outflows of gold: GNP prices rose almost 40 percent while the U.S. was at war, which was equal to the cumulative increase in prices over the previous 15-year period. Wartime inflation had its roots in a roughly twenty-fold increase in federal government expenditure from the time the U.S. entered the war in April 1917 to the armistice in November 1918 (see Firestone, 1960, Table A3).6

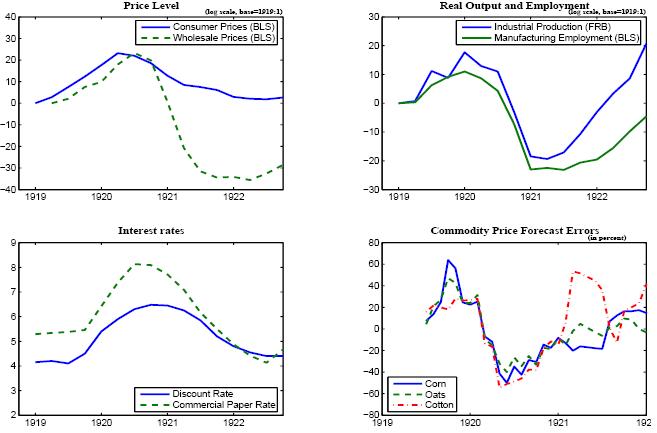

When the war ended, the embargo was lifted, and the Treasury and the Federal Reserve had to negotiate monetary policy in order to protect the Gold standard.7The Federal Reserve's Board of Governors included five appointees and two ex-officio members, the Secretary of Treasury and the Comptroller of the Currency. This governance structure gave the Secretary of the Treasury a disproportionate influence over monetary policy, since the five appointees to the Board were reluctant to cross the Treasury. Faced with a 25-fold increase in gross public debt after the War (Meltzer 2003), the Secretary refused to support an increase in discount rates despite an acceleration in inflation into double digits in 1919.8However, the Treasury's reputation was strongly linked to the success of the gold standard. In particular, U.S. law required the Federal Reserve to ensure a stock of monetary gold equal to at least 40 percent of the supply of base money. By November 1919, sizeable gold outflows put the legal minimum in sight, and the Treasury finally supported Board action to raise the discount rate.

Once freed to act, the Board raised the System-wide average discount rate over 2 percentage points between late 1919 and mid-1920 (see Figure 2). Although an eventual tightening of policy was anticipated insofar as private agents believed that the government was committed to defending the Gold standard, both the timing and severity of the contraction were a surprise. The highly persistent rise in nominal rates in the face of rapidly shifting expectations about inflation (i.e., towards deflation) represented a much tighter policy stance than agents had anticipated. As seen in Figure 2, the aggregate price level plunged 20 percent between mid-1920 and mid-1921, and commodity prices declined much more precipitously. Output also declined very abruptly, especially in manufacturing. As seen in Figure 2, the FRB's index of industrial production fell more than 30 percent between mid-1920 and early 1921, while manufacturing employment showed a commensurate decline. But the short-lived nature of the depression appears equally striking, as a robust expansion pushed output back to its pre-deflation level by early 1922.

The deflation of 1920 was recognized both by contemporary observers and by later historians as a dramatic event in U.S. monetary history. Irving Fisher (1934) was strongly critical of the Federal Reserve's role in engineering a "disastrous deflation" for which "millions of workers were thrown out of work." Friedman and Schwartz (1963) observed that the price decline was "perhaps the sharpest in the entire history of the United States" and characterized the output contraction as "one of the severest on record."

The industrial production and employment measures shown in Figure 2 indicate a much more severe recession than would be suggested from annual data for the aggregate economy.9 First, the magnitude of the downturn is obscured by its relatively transitory nature, particularly since the decline in output and employment began in mid-1920 and ended partway through the following year; indeed, Friedman and Schwartz argued that this recession was so abrupt that ``annual data provide a misleading indicator of its severity." Second, the fluctuations in real GNP were dampened by the stability of real agricultural output (which comprised a substantial fraction of aggregate output) and hence this measure is somewhat less relevant for gauging the effects of monetary policy during this period.10

As in the post-Civil War episode, the authorities' commitment to supporting the Gold Standard after WWI seems beyond doubt. By the 1920s, the Gold standard was entrenched as both a national and international norm, and even countries that had experienced much larger wartime inflations expected to return to gold. The high credibility of the monetary regime ultimately served an important role in allowing the economy to recover quickly once it was clear that prices had fallen enough. But clearly, the major difference between the episodes was in the Federal Reserve's decision to implement a very rapid deflation in the early 1920s, which contrasted starkly with the gradualist policy of 1869-1879. Influential Federal Reserve policymakers including Benjamin Strong believed that it was of foremost importance to reverse quickly most of the price level increase that had occurred since the U.S. entry into the war; while they acknowledged this might cause a substantial output contraction, they believed the recessionary effects would be transient and did not warrant dragging out the deflation (Meltzer 2003). Thus, policymakers kept nominal interest rates at elevated levels even as prices fell dramatically. This departure from traditional gold standard rules - which would have prescribed cutting interest rates in the face of a massive deflation and sizeable gold inflows - helped create a depression in activity through its effect on real interest rates.

2.3 The Volcker Disinflation

As of 1979, the Federal Reserve had been in operational control of U.S. monetary policy for about 25 years, even if it remained sensitive to the political climate. The Accord of 1951 between the central bank and the Treasury had ceded monetary policy to the Federal Reserve. For a dozen years after the Accord, the Federal Reserve generally maintained a low and steady inflation rate. But beginning in the mid-1960s, the Federal Reserve permitted inflation to rise to progressively higher levels. By the time President Carter appointed in 1979 a well-known inflation "hawk", Paul Volcker, to run the Federal Reserve, (GNP) price inflation had reached 9 percent.

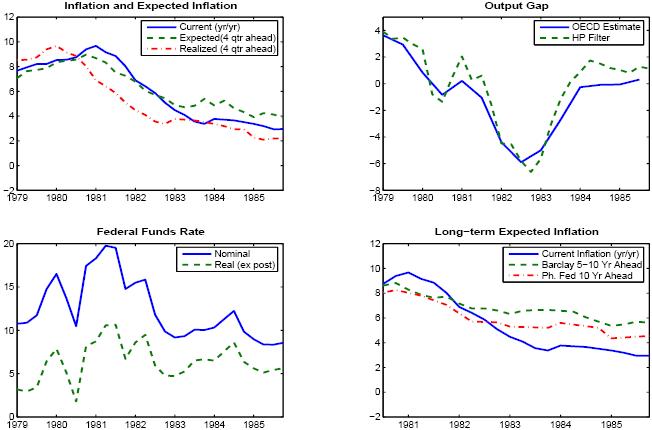

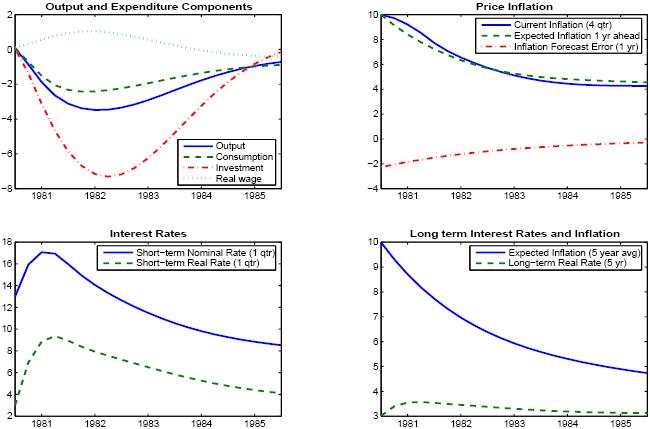

Two months after taking office in August 1979, Volcker announced a major shift in policy aimed at rapidly lowering the inflation rate. Volcker desired the policy change to be interpreted as a decisive break from past policies that had allowed the inflation rate to rise to double digit levels (Figure 3). The announcement was followed by a series of sizeable hikes in the federal funds rate: the roughly 7 percentage point rise in the nominal federal funds rate between October 1979 and April 1980 represented the largest increase over a sixth month period in the history of the Federal Reserve System. However, this tight monetary stance was temporarily abandoned in mid-1980 as economic activity decelerated sharply. Reluctantly, the FOMC imposed credit controls and let the funds rate decline - moves that the Carter Administration had publically supported. The FOMC's policy reversal and acquiesence to political pressure was widely viewed as a signal that it was not committed to achieving a sustained fall in inflation (Blanchard, 1984). Having failed to convince price and wage setters that inflation was going to fall, GNP prices rose almost 10 percent in 1980.

The Federal Reserve embarked on a new round of monetary tightening in late 1980. The federal funds rate rose to 20 percent in late December, implying an ex post real interest rate of about 10 percent. Real ex post rates were allowed to fall only slightly from this extraordinarily high level over the following two years. Newly-elected President Reagan's support of Volcker's policy was significant in giving the Federal Reserve the political mandate it needed to keep interest rates elevated for a prolonged period, and provided some shield from growing opposition in Congress; cf. Feldstein (1993). This second and more durable round of tightening succeeded in reducing the inflation rate from about 10 percent in early 1981 to about 4 percent in 1983, but at the cost of a sharp and very prolonged recession. The OECD's measure of the output gap expanded by 6 percent between mid-1980 and mid-1982, and the unemployment rate (not shown) hovered at 10 percent until mid-1983.

While policymakers in the Gold standard environment examined in the earlier episodes had the advantage of a transparent and credible long-run nominal anchor, the Volcker disinflation was conducted in a setting in which there was a high degree of uncertainty about whether policymakers had the desire and ability to maintain low inflation rates. But notwithstanding that Federal Reserve policy during the 1970s and early 1980s merits some criticism for a lack of transparent objectives, it seems unlikely that simple announcements about long-run policy goals (e.g., an inflation target of three percent) would have carried much weight given the poor track record of the preceding two decades. Thus, it seems arguable that Volcker's FOMC had little hope of harnessing inflation expectations in a way that could facilitate lower inflation without sizeable output costs.

3 Policy Predictability: Empirical Evidence

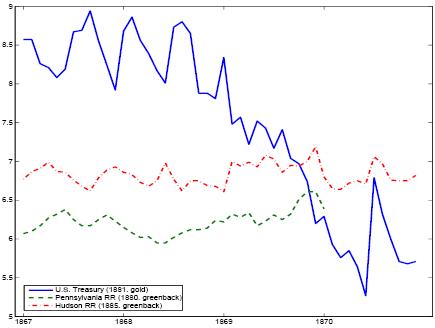

Empirical evidence about the predictability of price decline that preceded Resumption in 1879 appears fairly limited. However, as argued by Friedman and Schwartz (1963) and later Calomiris (1985 and 1993), the behavior of longer term bond yields seems at least consistent with the view that private agents expected the dollar to appreciate (and prices to fall) by enough to support an eventual return to gold. As seen in Figure 4, the nominal yields on high quality greenback-denominated railroad bonds were actually somewhat lower than the yield on gold-denominated U.S. treasury bonds at the passage of the Public Credit Act in 1869. By that time, confidence was very high that the government would satisfy its obligation to repay its bonds in gold. Thus, drawing on uncovered interest parity, Friedman and Schwartz interpreted the lower interest rate on privately issued railroad bonds as suggesting that private agents on balance expected some appreciation of the greenback relative to gold. Of course, the simple difference between the interest rate series would understate expected appreciation of the Greenback to the extent that the interest rate on the railroad bonds included a premium for default risk.11

Some evidence from commodity futures markets also appears consistent with our interpretation that the gradual price decline prior to Resumption was largely anticipated. Taking the futures price as a proxy for the expected price of a given commodity at a date K months ahead, we constructed a series of forecast errors as the difference between the realized commodity price and the (futures-based) forecast. The futures prices are on 4-5 month contracts (the longest maturities regularly available during that period) on pork, corn, wheat, and lard.12 Given the paucity of observations on each individual commodity, Figure 1 pools forecast errors for all four of the commodities (yielding 30 observations over our 1871-78 sample period). The forecast errors seem relatively small, especially given the substantial volatility in spot prices of the underlying commodities: the average absolute error using these pooled observations is around 10 percent. Moreover, realized prices do not appear consistently lower than forecast (i.e., the forecast errors are not consistently negative). Despite obvious limitations of our data - including the short duration of futures contracts, and small number of observations - they are at least suggestive that agents were not surprised by declining prices.

There is considerably more evidence about the predictability of policy in the case of the deflationary episode following WWI. One very useful source is Harvard's Monthly Survey of General Business Conditions, which appeared as a monthly supplement to the Review of Economics and Statistics beginning in 1919. Harvard's Monthly Survey (HMS) interpreted recent financial and macroeconomic developments, and also made projections about the future evolution of output, prices, and short-term interest rates. While projections about individual macroeconomic series were primarily qualitative, the HMS did make some explicit forecasts about the likely duration of the business downturn during the course of 1920-21.

Drawing on the surveys from the first half of 1920, the HMS forecasters correctly predicted that the post-war inflation would be followed by a period of monetary retrenchment, and appeared to have a fairly clear understanding of the channels through which the monetary tightening would operate. In particular, they argued that the Federal Reserve's imposition of higher discount rates beginning in late 1919 would precipitate a fall in commodity prices, followed by a decline in consumer prices, wages, and business activity; but drawing on historical experience, they expected that lower prices would allow monetary easing, and promote a vigorous recovery within about a year.

The HMS forecasters turned out to be surprised by the severity of the monetary tightening, and by the associated magnitude of price and output decline. At the onset of the tightening, the HMS commented that "both the Treasury and the Federal Reserve Board have embarked on a policy of orderly deflation," and projected in April 1920 that "it does not seem probable ... that liquidation in the near future will cause prices to fall below the level of a year ago and perhaps not below the level of November 1918," suggesting an anticipated fall in commodity prices of only 15-20 percent.13 But in the wake of a 40 percent decline in commodity prices by early 1921 and depression in business activity, Bullock (1921) observed that he and the other HMS forecasters "had not expected a (monetary) reaction of such acute severity. We had looked for a return [of commodity prices] to some such level as had prevailed in the few months following the armistice, and as late as July expected nothing so drastic as the events of the last half of the year." Moreover, the HMS forecasters were forced to revise their optimistic initial predictions (made in the spring of 1920) that recovery would occur within a year as the sharp nature of the downturn became more apparent. The HMS attributed the severity of the downturn in part to persistently high interest rates, as interest rates remained elevated for a longer duration than in previous cyclical downturns dating back to the 1890s.14 Nevertheless, given the enormous price contraction by early 1921, the HMS forecasters were confident that prices would soon stabilize (as in fact occurred by late 1921), and that an eventual easing of monetary conditions would facilitate a rebound in real activity.

Commodity price forecast errors provide complementary evidence that prices fell more quickly and by a greater magnitude than expected by private agents. Figure 2 shows commodity price forecast errors for three individual commodities - corn, oats, and cotton - measured again as the realized price of each commodity minus the `` forecast" implied by the futures price.15In the post-World War I deflation, commodity price forecast errors turned consistently negative shortly after monetary policy was tightened in early 1920, and reached 50 percentage points or higher in absolute value terms. The average forecast errors over the 1920-21 tightening period are several times as large as the commodity price forecast errors derived from the post-Civil War data. But interestingly, forecast errors are generally much smaller after early 1921. This seems consistent with our intepretation that after a markedly lower price level was achieved, the policy environment became much more predictable, as agents expected the aggregate price level to remain roughly stable.

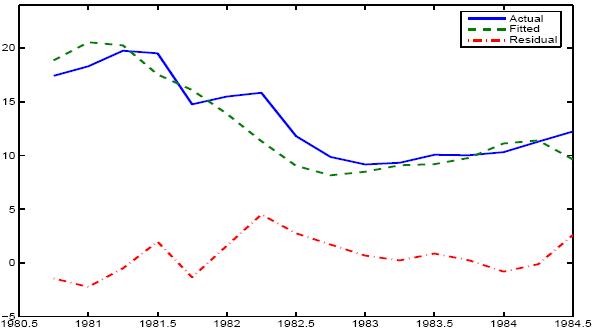

Lastly, we turn to the Volcker disinflation, for which there is considerable survey data available on inflation expectations at different horizons. Figure 3 plots the median projection of four quarter ahead GNP price inflation from the Survey of Professional Forecasters. The average inflation forecast error at a one year horizon (the gap between realized inflation over the subsequent year, the dash-dotted line, and the forecast, the dashed line) averaged about 2 percentage points over the 1981-84 period. Importantly, the inflation forecast errors show little tendency to die out, reflecting that inflation was consistently lower than what agents projected. The lower right panel of Figure 3 also contrasts the relatively quick decline in current inflation with the much more sluggish adjustment of long-run inflation expectations (as proxied by Barclay's projection of inflation 5-10 years ahead, and by the 10 year ahead inflation projection of the Philadephia Federal Reserve Bank). Taken together, the survey data suggests that inflation expectations were very slow to react to the decline in realized inflation, which we interpret as strong evidence that private agents doubted the ability or desire of policymakers to maintain low inflation rates. This interpretation is consistent with that of Goodfriend (1993) and Goodfriend and King (2005), who argued that the slow adjustment of inflation expectations was a primary factor accounting for the high nominal interest rates on long-term bonds that prevailed through most of the 1980s.

4 The Model

We utilize the same basic model to analyze each of the three historical episodes, aside from differences in the characterization of monetary policy. The model can be regarded as a slightly simplified version of the model utilized by Christiano, Eichenbaum and Evans (2005), and Smets and Wouters (2003). Thus, our model incorporates nominal rigidities by assuming that labor and product markets each exhibit monopolistic competition, and that wages and prices are determined by staggered nominal contracts of random duration (following Calvo (1983) and Yun (1996)). We also include various real rigidities emphasized in the recent literature, including habit persistence in consumption, and costs of changing the rate of investment. Given that our characterization of monetary policy differs across episodes, we defer this discussion to Section 6 (when we present simulation results for each episode).

4.1 Firms and Price Setting

Final Goods Production As in Chari, Kehoe, and McGratten

(2000), we assume that there is a single final output good

![]() that is produced using a continuum of

differentiated intermediate goods

that is produced using a continuum of

differentiated intermediate goods ![]() The

technology for transforming these intermediate goods into the final

output good is constant returns to scale, and is of the

Dixit-Stiglitz form:

The

technology for transforming these intermediate goods into the final

output good is constant returns to scale, and is of the

Dixit-Stiglitz form:

![$\displaystyle Y_{t}=\left[ \int_{0}^{1}Y_{t}\left( f\right) ^{\frac{1}{1+\theta_{p}} }df\right] ^{1+\theta_{p}}$](img9.gif)

where

Firms that produce the final output good are perfectly

competitive in both product and factor markets. Thus, final goods

producers minimize the cost of producing a given quantity of the

output index ![]() , taking as given the price

, taking as given the price

![]() of each intermediate

good

of each intermediate

good ![]() . Moreover, final goods producers

sell units of the final output good at a price

. Moreover, final goods producers

sell units of the final output good at a price ![]() that is equal to the marginal cost of production:

that is equal to the marginal cost of production:

![$\displaystyle P_{t}=\left[ \int_{0}^{1}P_{t}{}\left( f\right) ^{\frac{-1}{\theta_{p}} }df\right] ^{-\theta_{p}}$](img15.gif)

It is natural to interpret

Intermediate Goods Production A continuum of intermediate

goods ![]() for

for

![]() is produced by

monopolistically competitive firms, each of which produces a single

differentiated good. Each intermediate goods producer faces a

demand function for its output good that varies inversely with its

output price

is produced by

monopolistically competitive firms, each of which produces a single

differentiated good. Each intermediate goods producer faces a

demand function for its output good that varies inversely with its

output price

![]() and directly with

aggregate demand

and directly with

aggregate demand ![]()

![$\displaystyle Y_{t}\left( f\right) =\left[ \frac{P_{t}\left( f\right) }{P_{t}}\right] ^{\frac{-\left( 1+\theta_{p}\right) }{\theta_{p}}}Y_{t}$](img21.gif)

Each intermediate goods producer utilizes capital services

![]() and a labor index

and a labor index

![]() (defined below) to

produce its respective output good. The form of the production

function is Cobb-Douglas:

(defined below) to

produce its respective output good. The form of the production

function is Cobb-Douglas:

Firms face perfectly competitive factor markets for hiring capital and the labor index. Thus, each firm chooses

We assume that the prices of the intermediate goods are

determined by Calvo-Yun style staggered nominal contracts. In each

period, each firm f faces a constant probability, ![]() , of being able to reoptimize its price

, of being able to reoptimize its price ![]() . The probability that any firm receives a signal to

reset its price is assumed to be independent of the time that it

last reset its price. If a firm is not allowed to optimize its

price in a given period, we follow Yun (1996) by assuming that it

simply adjusts its price by the steady state rate of inflation

. The probability that any firm receives a signal to

reset its price is assumed to be independent of the time that it

last reset its price. If a firm is not allowed to optimize its

price in a given period, we follow Yun (1996) by assuming that it

simply adjusts its price by the steady state rate of inflation

![]() (i.e.,

(i.e.,

![]() . Finally, the firm's

output is subsidized at a fixed rate

. Finally, the firm's

output is subsidized at a fixed rate ![]() (this

allows us to eliminate the monopolistic competition wedge in prices

by setting

(this

allows us to eliminate the monopolistic competition wedge in prices

by setting

![]() ).

).

4.2 Households and Wage Setting

We assume a continuum of monopolistically competitive households

(indexed on the unit interval), each of which supplies a

differentiated labor service to the production sector; that is,

goods-producing firms regard each household's labor services

![]() ,

,

![]() , as an imperfect substitute

for the labor services of other households. It is convenient to

assume that a representative labor aggregator (or "employment

agency") combines households' labor hours in the same proportions

as firms would choose. Thus, the aggregator's demand for each

household's labor is equal to the sum of firms' demands. The labor

index

, as an imperfect substitute

for the labor services of other households. It is convenient to

assume that a representative labor aggregator (or "employment

agency") combines households' labor hours in the same proportions

as firms would choose. Thus, the aggregator's demand for each

household's labor is equal to the sum of firms' demands. The labor

index ![]() has the Dixit-Stiglitz form:

has the Dixit-Stiglitz form:

![$\displaystyle L_{t}=\left[ \int_{0}^{1}N_{t}\left( h\right) ^{\frac{1}{1+\theta_{w}} }dh\right] ^{1+\theta_{w}}$](img44.gif)

where

![$\displaystyle W_{t}=\left[ \int_{0}^{1}W_{t}{}\left( h\right) ^{\frac{-1}{\theta_{w}} }dh\right] ^{-\theta_{w}}$](img48.gif)

It is natural to interpret ![]() as the

aggregate wage index. The aggregator's demand for the labor hours

of household

as the

aggregate wage index. The aggregator's demand for the labor hours

of household ![]() - or equivalently, the total demand for

this household's labor by all goods-producing firms - is given by

- or equivalently, the total demand for

this household's labor by all goods-producing firms - is given by

![$\displaystyle N_{t}\left( h\right) =\left[ \frac{W_{t}\left( h\right) }{W_{t}}\right] ^{-\frac{1+\theta_{w}}{\theta_{w}}}L_{t}$](img51.gif)

The utility functional of a typical member of household

![]() is

is

|

(9) | |

|

(10) |

where the discount factor ![]() satisfies

satisfies

![]() The dependence of the period

utility function on consumption in both the current and previous

period allows for the possibility of external habit persistence in

consumption spending (e.g., Smet and Wouters, 2003). In addition,

the period utility function depends on current leisure

The dependence of the period

utility function on consumption in both the current and previous

period allows for the possibility of external habit persistence in

consumption spending (e.g., Smet and Wouters, 2003). In addition,

the period utility function depends on current leisure

![]() , and current real

money balances.

, and current real

money balances.

![]()

Household ![]() 's budget constraint in period

's budget constraint in period

![]() states that its expenditure on goods and

net purchases of financial assets must equal its disposable

income:

states that its expenditure on goods and

net purchases of financial assets must equal its disposable

income:

![\begin{displaymath}\begin{array}[c]{c} P_{t}C_{t}\left( h\right) +P_{t}I_{t}\left( h\right) +\frac{1}{2}\psi _{I}P_{t}\frac{\left( I_{t}(h)-I_{t-1}(h)\right) ^{2}}{I_{t-1}(h)}\\ \\ M_{t+1}\left( h\right) -M_{t}\left( h\right) +\int_{s}\xi_{t,t+1} B_{D,t+1}(h)-B_{D,t}(h)\\ \\ =(1+\tau_{W})W_{t}\left( h\right) N_{t}\left( h\right) +R_{Kt} K_{t}(h)+\Gamma_{t}\left( h\right) -T_{t}(h)\\ \end{array}\end{displaymath}](img61.gif)

Thus, the household purchases the final output good (at a price of ![]() which it chooses either to consume

which it chooses either to consume

![]() or invest

or invest

![]() in physical capital.

The total cost of investment to each household h is assumed

to depend on how rapidly the household changes its rate of

investment (as well as on the purchase price). Our specification of

such investment adjustment costs as depending on the square of the

change in the household's gross investment rate follows Christiano,

Eichenbaum, and Evans (2005). Investment in physical capital

augments the household's (end-of-period) capital stock

in physical capital.

The total cost of investment to each household h is assumed

to depend on how rapidly the household changes its rate of

investment (as well as on the purchase price). Our specification of

such investment adjustment costs as depending on the square of the

change in the household's gross investment rate follows Christiano,

Eichenbaum, and Evans (2005). Investment in physical capital

augments the household's (end-of-period) capital stock

![]() according to a linear transition

law of the form:

according to a linear transition

law of the form:

In addition to accumulating physical capital, households may

augment their financial assets through increasing their nominal

money holdings (

![]() and through

the net acquisition of bonds. We assume that agents can engage in

frictionless trading of a complete set of contingent claims. The

term

and through

the net acquisition of bonds. We assume that agents can engage in

frictionless trading of a complete set of contingent claims. The

term

![]() represents net purchases of state-contingent domestic bonds, with

represents net purchases of state-contingent domestic bonds, with

![]() denoting the state price, and

denoting the state price, and

![]() the quantity of

such claims purchased at time

the quantity of

such claims purchased at time ![]() . Each member of

household

. Each member of

household ![]() earns labor income

earns labor income

![]() (where

(where

![]() is a subsidy that allows us to

offset monopolistic distortions in wage-setting) , and receives

gross rental income of

is a subsidy that allows us to

offset monopolistic distortions in wage-setting) , and receives

gross rental income of

![]() from renting its capital stock

to firms. Each member also receives an aliquot share

from renting its capital stock

to firms. Each member also receives an aliquot share

![]() of the profits of

all firms, and pays a lump-sum tax of

of the profits of

all firms, and pays a lump-sum tax of

![]() (this may be regarded

as taxes net of any transfers).

(this may be regarded

as taxes net of any transfers).

In every period ![]() , each member of household

, each member of household

![]() maximizes the utility functional (9) with respect to

its consumption, investment, (end-of-period) capital stock, money

balances, and holdings of contingent claims, subject to its labor

demand function (8), budget

constraint (11), and

transition equation for capital (12). Households

also set nominal wages in Calvo-style staggered contracts that are

generally similar to the price contracts described above. Thus, the

probability that a household receives a signal to reoptimize its

wage contract in a given period is denoted by

maximizes the utility functional (9) with respect to

its consumption, investment, (end-of-period) capital stock, money

balances, and holdings of contingent claims, subject to its labor

demand function (8), budget

constraint (11), and

transition equation for capital (12). Households

also set nominal wages in Calvo-style staggered contracts that are

generally similar to the price contracts described above. Thus, the

probability that a household receives a signal to reoptimize its

wage contract in a given period is denoted by ![]() , and as in the case of price contracts this

probability is independent of the date at which the household last

reset its wage. However, we specify a dynamic indexation scheme for

the adjustment of the wages of those households that do not get a

signal to reoptimize, i.e.,

, and as in the case of price contracts this

probability is independent of the date at which the household last

reset its wage. However, we specify a dynamic indexation scheme for

the adjustment of the wages of those households that do not get a

signal to reoptimize, i.e.,

![]() in contrast to

the static indexing assumed for prices. As discussed by Christiano,

Eichenbaum, and Evans (2005), dynamic indexation of this form

introduces some element of structural persistence into the

wage-setting process. Our asymmetric treatment is motivated by the

empirical analysis of Levin, Onatski, Williams, and Williams

(2005). These authors estimated a similar model using U.S. data

over the 1955:1-2001:4 period, and found evidence in favor of

nearly full indexation of wages, but not of prices (hence our

specification of prices as purely forward-looking).

in contrast to

the static indexing assumed for prices. As discussed by Christiano,

Eichenbaum, and Evans (2005), dynamic indexation of this form

introduces some element of structural persistence into the

wage-setting process. Our asymmetric treatment is motivated by the

empirical analysis of Levin, Onatski, Williams, and Williams

(2005). These authors estimated a similar model using U.S. data

over the 1955:1-2001:4 period, and found evidence in favor of

nearly full indexation of wages, but not of prices (hence our

specification of prices as purely forward-looking).

4.3 Fiscal Policy and the Aggregate Resource Constraint

The government's budget is balanced every period, so that total lump-sum taxes plus seignorage revenue are equal to output and labor subsidies plus the cost of government purchases:

| (13) |

where ![]() indicates real government purchases. We

assume that government spending is a fixed share of output in our

analysis. Finally, the total output of the service sector is

subject to the following resource constraint:

indicates real government purchases. We

assume that government spending is a fixed share of output in our

analysis. Finally, the total output of the service sector is

subject to the following resource constraint:

| (14) |

5 Solution and Calibration

To analyze the behavior of the model, we log-linearize the model's equations around the non-stochastic steady state. Nominal variables, such as the contract price and wage, are rendered stationary by suitable transformations. We then compute the reduced-form solution of the model for a given set of parameters using the numerical algorithm of Anderson and Moore (1985), which provides an efficient implementation of the solution method proposed by Blanchard and Kahn (1980).

5.1 Parameters of Private Sector Behavioral Equations

The model is calibrated at a quarterly frequency. Thus, we

assume that the discount factor

![]() consistent with a steady-state

annualized real interest rate

consistent with a steady-state

annualized real interest rate

![]() of about 3 percent. We assume

that the subutility function over consumption is logarithmic, so

that

of about 3 percent. We assume

that the subutility function over consumption is logarithmic, so

that ![]() while we set the parameter

determining the degree of habit persistence in consumption

while we set the parameter

determining the degree of habit persistence in consumption

![]() = 0.6 (similar to the empirical

estimate of Smets and Wouters 2003). The parameter

= 0.6 (similar to the empirical

estimate of Smets and Wouters 2003). The parameter ![]() which determines the curvature of the subutility

function over leisure, is set equal to 10, implying a Frisch

elasticity of labor supply of 1/5. This is considerably lower than

if preferences were logarithmic in leisure, but within the range of

most estimates from the empirical labor supply literature. The

scaling parameter

which determines the curvature of the subutility

function over leisure, is set equal to 10, implying a Frisch

elasticity of labor supply of 1/5. This is considerably lower than

if preferences were logarithmic in leisure, but within the range of

most estimates from the empirical labor supply literature. The

scaling parameter ![]() is set so that

employment comprises one-third of the household's time endowment,

while the parameter

is set so that

employment comprises one-third of the household's time endowment,

while the parameter ![]() on the subutility

function for real balances is set an arbitrarily low value (so that

variation in real balances has a negligible impact on other

variables). The share of government spending of total expenditure

is set equal to 12 percent.

on the subutility

function for real balances is set an arbitrarily low value (so that

variation in real balances has a negligible impact on other

variables). The share of government spending of total expenditure

is set equal to 12 percent.

The capital share parameters

![]() . The quarterly depreciation rate

of the capital stock

. The quarterly depreciation rate

of the capital stock

![]() , implying an annual depreciation

rate of 8 percent. The price and wage markup parameters

, implying an annual depreciation

rate of 8 percent. The price and wage markup parameters

![]() . We set the cost of

adjusting investment parameter

. We set the cost of

adjusting investment parameter ![]() = 2, which

is somewhat smaller than the value estimated by Christiano,

Eichenbaum, and Evans (2001) using a limited information approach;

however, the analysis of Erceg, Guerrieri, and Gust (2005) suggests

that a lower value in the range of unity may be better able to

capture the unconditional volatility of investment within a similar

modeling framework. We assume that price contracts last three

quarters, while nominal wage contracts last four quarters. The

calibration of contract duration is in the range typically

estimated in the literature.

= 2, which

is somewhat smaller than the value estimated by Christiano,

Eichenbaum, and Evans (2001) using a limited information approach;

however, the analysis of Erceg, Guerrieri, and Gust (2005) suggests

that a lower value in the range of unity may be better able to

capture the unconditional volatility of investment within a similar

modeling framework. We assume that price contracts last three

quarters, while nominal wage contracts last four quarters. The

calibration of contract duration is in the range typically

estimated in the literature.

6 Model Simulations

6.1 The Post Civil War Deflation

While we will attempt to use our model to account for the evolution of real activity during the latter two episodes - on the premise that monetary changes played a principal role in driving the output fluctuations that occurred - our objective in applying the model to the post Civil War deflation is narrower in scope. In particular, while a more complicated model with a richer set of shocks would be required to account for output behavior over the long period prior to Resumption, our focus here is simply to rationalize why the "secular" deflation of 2-3 percent per year appeared to exert little drag on output growth in the decade following the Public Credit Act of 1869.

In this vein, we characterize the monetary authorities in the

1869-1879 period as following a simple targeting rule derived from

minimizing a loss function that depends on the gap between the

price level ![]() and its target value

and its target value

![]() (which we call the price level

gap), and on the output gap

(which we call the price level

gap), and on the output gap ![]() . Under a

quadratic period loss function in each of these gaps, the targeting

rule is derived by minimizing a discounted conditional loss

function of the form:

. Under a

quadratic period loss function in each of these gaps, the targeting

rule is derived by minimizing a discounted conditional loss

function of the form:

subject to the behavioral constraints implied by household and firm optimization from the model of Section 4.16

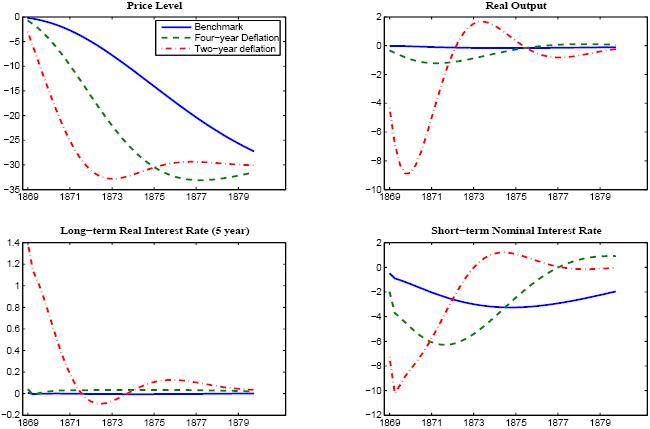

The solid blue line in Figure 5 presents our

benchmark characterization of the post Civil War deflation period

in response to a permanent reduction in

![]() of 30 percent. The weight on

the output gap in the loss function is chosen to stretch out the

price decline over the course of a decade, so that the simulated

price level decline appears quite similar to the historical

experience (this is achieved by setting

of 30 percent. The weight on

the output gap in the loss function is chosen to stretch out the

price decline over the course of a decade, so that the simulated

price level decline appears quite similar to the historical

experience (this is achieved by setting

![]() in (15)). It is evident

from the figure that the large cumulative decline in prices has

little impact on real activity: in fact, output never falls more

than 0.1 percent below potential. The optimal policy achieves this

sizeable price decline at minimal output cost by relying heavily on

an "expectations channel": current price-setters are willing to

lower prices today in the expectation that future prices will be

lower (and hence deflation does not require a recession). A notable

characteristic of the optimal policy is that it implies a

persistent decline in short-term nominal interest rates, which is

consistent with the policy shift exerting little effect on

long-term real interest rates.

in (15)). It is evident

from the figure that the large cumulative decline in prices has

little impact on real activity: in fact, output never falls more

than 0.1 percent below potential. The optimal policy achieves this

sizeable price decline at minimal output cost by relying heavily on

an "expectations channel": current price-setters are willing to

lower prices today in the expectation that future prices will be

lower (and hence deflation does not require a recession). A notable

characteristic of the optimal policy is that it implies a

persistent decline in short-term nominal interest rates, which is

consistent with the policy shift exerting little effect on

long-term real interest rates.

We believe that this simple characterization of policy captures many of the relevant features of the historical environment following the passage of the Public Credit Act in 1869 that were recounted in Section 2. These features included: first, the mandate to effect a substantial reduction in the general price level, subject to the proviso that the deflation would be gradual enough to avoid a reprise of the post war monetary recession; and second, the ability of the authorities to commit to such a policy. Admittedly, our characterization abstracts from some aspects of implementation that were discussed in Section 2, including the operational procedure of controlling the monetary base. However, taking account of such features would require significant complications to our model, and would seem highly unlikely to change our basic message that a very gradual and predictable deflation exerts small effects on real activity under a reasonable and well-understood rule (specified either in terms of the money stock or nominal interest rate).17

Given the negligible output losses under the ten year

implementation window, it is also natural to inquire whether the

1869-1879 price level decline could have occurred more rapidly

without significantly exacerbating the effects on the real economy:

did the authorities perhaps become overly cautious in response to

the public acrimony that followed their first attempts to deflate?

This rather general question about how quickly a deflation can be

implemented without causing substantial fallout on the real economy

has close parallel in earlier work by Taylor (1983) and Ball

(1994b, 1995), but with the important difference that the latter

authors assessed how the real costs depended on the horizon over

which the inflation rate was changed, rather than the

price level. While these authors found that a disinflation

could be implemented over a short horizon of roughly two years or

less with minimal output costs, our results suggest that a

considerably longer horizon is required to implement a change in

the price level; the difference reflects that while the staggered

contracts framework implies little endogenous persistence in the

inflation rate - so that it is relatively easy for inflation to

jump - it implies considerably more price level persistence. Under

our baseline calibration, the implied tradeoff between a shorter

horizon for implementing the disinflation and higher output losses

can be derived by varying the relative weight on the output gap (

![]() in the targeting rule (15). Two

alternative cases are shown in Figure 5. The dashed

green line shows that a value of

in the targeting rule (15). Two

alternative cases are shown in Figure 5. The dashed

green line shows that a value of

![]() which causes the 30 percent

price decline to occur over only four years causes the output loss

to rise to about 1 percent, which still seems quite modest.

However, while our benchmark model allows an inflation target to be

reduced over a narrow 2 year window with minimal output losses (as

verified below, consistent with the earlier literature cited),

implementing a new price level target over such an abbreviated time

frame causes a pronounced recession (as depicted by the red

dash-dotted line).

which causes the 30 percent

price decline to occur over only four years causes the output loss

to rise to about 1 percent, which still seems quite modest.

However, while our benchmark model allows an inflation target to be

reduced over a narrow 2 year window with minimal output losses (as

verified below, consistent with the earlier literature cited),

implementing a new price level target over such an abbreviated time

frame causes a pronounced recession (as depicted by the red

dash-dotted line).

These results suggest that the ten-year window for phasing in the deflation might have been reduced considerably without much of an adverse effect on output. Moreover, to the extent that wages and prices may have been somewhat more flexible in this episode than implied by our benchmark calibration, the output losses associated with shortening the implementation horizon would be mitigated relative to those indicated in Figure 5. Nevertheless, provided there is some sluggishness in prices and wages - even if less than embedded in our benchmark - real interest rates must rise sharply to implement a discrete downward shift in the price level over a short horizon. Thus, it is arguable that a short implementation window in the neighborhood of a year or two might have risked a substantial recession.

6.2 The Post-WWI Deflation

We now turn to using our model to characterize the severe monetary recession that began in 1920. As discussed above, the salient feature was a precipitous and largely unexpected decline in the price level of about 20 percent over a period of less than two years, and a sharp but fairly short-lived contraction in activity. Our model simulations in Figure 5 suggest that attempting to achieve a new price level objective so quickly would precipitate a severe recession even under a well-designed policy derived in an optimization-based setting. But given that monetary policy seemed far from optimal during the 1920s, it remains of interest to assess the implications of a large shift in the price level target under an alternative monetary rule that may better account for the nature of policy.

Despite obvious difficulties in characterizing policy during this turbulent period, we believe that many of the prominent features of the policymaking framework can be summarized in a simple instrument rule of the form:

This rule posits the nominal interest rate ![]() as

responding to the price level gap

as

responding to the price level gap

![]() , as well as to its own

lag (a constant term is suppressed for simplicity). This

specification has two salient features. First, policy rates are

driven exclusively by the difference between the current price

level and its target

, as well as to its own

lag (a constant term is suppressed for simplicity). This

specification has two salient features. First, policy rates are

driven exclusively by the difference between the current price

level and its target

![]() This specification is intended

to capture the belief of key Federal Reserve policymakers that

continued adherence to the Gold standard hinged on rolling back the

rise in the U.S. price level that had occurred following the U.S.

entry into the war. While it was recognized that real activity

might suffer in the short-run, it was regarded of paramount

importance to reduce prices enough to faciliate an adequate buildup

of gold reserves. The second key feature of (16) is that nominal

rates do not respond to inflation (either ex post or ex ante). As

shown below, this helps account for the empirical observation that

nominal rates remained high despite an enormous decline in the

price level in 1920-21. This feature of the instrument rule

evidently contrasts with the behavior of nominal rates under the

optimal rule shown in Figure 5, in which declining inflation exerts

sizeable downward pressure on nominal rates.

This specification is intended

to capture the belief of key Federal Reserve policymakers that

continued adherence to the Gold standard hinged on rolling back the

rise in the U.S. price level that had occurred following the U.S.

entry into the war. While it was recognized that real activity

might suffer in the short-run, it was regarded of paramount

importance to reduce prices enough to faciliate an adequate buildup

of gold reserves. The second key feature of (16) is that nominal

rates do not respond to inflation (either ex post or ex ante). As

shown below, this helps account for the empirical observation that

nominal rates remained high despite an enormous decline in the

price level in 1920-21. This feature of the instrument rule

evidently contrasts with the behavior of nominal rates under the

optimal rule shown in Figure 5, in which declining inflation exerts

sizeable downward pressure on nominal rates.

The price level target is assumed to follow an exogenous random

walk, so that any shift in the target is perceived as permanent.

The shock we consider involves a 20 percent cumulative reduction in

![]() that begins in 1920q1. While

private agents are assumed to observe the underlying price level

target, we assume that the shock is phased-in over three quarters,

in part to match the modest persistence suggested by the commodity

price forecast errors discussed in Section 3. Finally, we set

that begins in 1920q1. While

private agents are assumed to observe the underlying price level

target, we assume that the shock is phased-in over three quarters,

in part to match the modest persistence suggested by the commodity

price forecast errors discussed in Section 3. Finally, we set

![]() to allow for a bit of interest

rate smoothing, and

to allow for a bit of interest

rate smoothing, and

![]() in order to allow our model

to do reasonably well in matching the rise in nominal interest

rates that occurred in the historical episode.

in order to allow our model

to do reasonably well in matching the rise in nominal interest

rates that occurred in the historical episode.

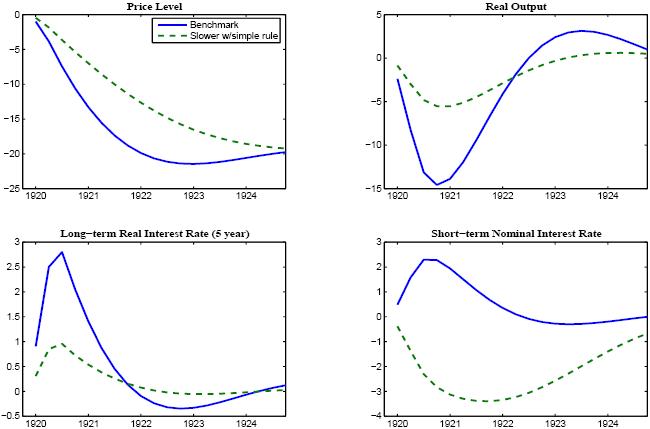

Simulation results for our benchmark case are shown by the solid blue lines in Figure 6. The model simulation generates a large decline in the price level beginning in 1920 that is similar in magnitude to that observed. The sharpness of this price decline is well-captured by our modelling framework, in which prices are determined by Calvo-style contracts with no dynamic indexation. The speed of the price decline would be much more difficult to rationalize in a model that incorporated dynamic indexation or other forms of intrinsic inflation persistence.

The model implies a pronounced output decline that is followed by a rapid recovery, which is similar to the pattern observed historically. The output decline in our model simulation is attributable to a sizeable and fairly persistent rise in the real interest rate. The substantial rise in real long-term interest rates despite little movement in the nominal interest rate reflects both that agents came to expect large price declines, and that policy would maintain high nominal rates even in a deflationary environment.18

Thus, our simulation results suggest that the high costs of the 1920-21 deflation reflect that the Federal Reserve attempted to engineer an extremely rapid deflation, and that it was perceived as following a monetary policy stance in which future nominal rates were expected to remain high (at least for a few quarters) in the face of deflation: in effect, consistent with our historical analysis, the Federal Reserve used the blunt instrument of a severe recession to push down prices, rather than operating through an expectations channel. Accordingly, it is of interest to consider the counterfactual simulation depicted by the dotted green lines, which shows a case in which the central bank is assumed to change its target path level incrementally, and to follow a rule in which the nominal interest rate also responds to ex post inflation (but is otherwise identical to equation (16)). Clearly, while allowing for nominal rates to decline with inflation would have induced a more gradual convergence in prices to target, it would have greatly ameliorated the output costs. Obviously, even more favorable outcomes could be derived to the extent that policy could better approximate the optimal targeting rules discussed in the previous section rather than a simple ad hoc instrument rule.

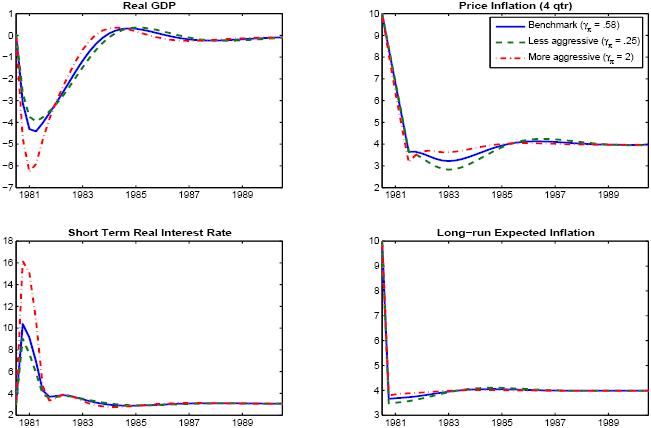

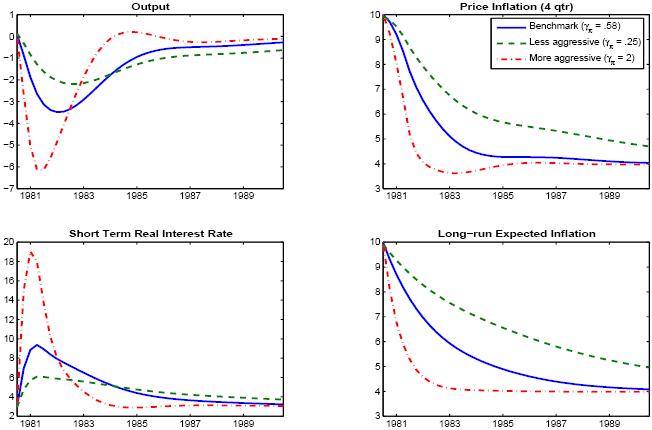

6.3 The Volcker Disinflation

A striking feature of the Volcker disinflation period was the fact that inflation forecast errors were extremely persistent. Erceg and Levin (2003) argued that the persistence in the forecast errors - and associated high persistence in realized inflation - may have reflected a high level of uncertainty about the central bank's inflation target.19In this paper, we take a similar stylized approach to characterizing uncertainty about the inflation target of the central bank by assuming that agents cannot differentiate permanent shocks to the inflation target from transient shocks to the monetary policy reaction function.

We specify the central bank's reaction function over the Volcker period as a slightly modified version of the Taylor rule:

where ![]() is the short-term nominal interest

rate,

is the short-term nominal interest

rate, ![]() is the four-quarter change in the

GDP price deflator,

is the four-quarter change in the

GDP price deflator,

![]() is the central bank's

inflation target,

is the central bank's

inflation target,

![]() is the four-quarter change in

real GDP, and

is the four-quarter change in

real GDP, and ![]() denotes the shock to the policy

reaction function, where all variables are expressed at annual

rates in percentage points.20

denotes the shock to the policy

reaction function, where all variables are expressed at annual

rates in percentage points.20

In estimating this policy reaction function, we utilize the

sample period 1980:4 through 1986:4, thereby excluding the policy

reversals that occurred during the first year of Volcker's tenure

(as discussed in section 2.3).21 Least squares estimation over

this sample period yields

![]()

![]() and

and

![]() As seen in Figure 7, this simple

form of the reaction function accounts reasonably well for the

evolution of the funds rate over the sample period.

As seen in Figure 7, this simple

form of the reaction function accounts reasonably well for the

evolution of the funds rate over the sample period.

Agents cannot directly observe the long-run inflation target

![]() or the monetary shock

or the monetary shock

![]() but given that agents observe

interest rates, inflation, and output growth (as well as all of the

structural parameters of the model), they can infer a composite

shock

but given that agents observe

interest rates, inflation, and output growth (as well as all of the

structural parameters of the model), they can infer a composite

shock ![]() which is a hybrid of the inflation

target shock and the monetary policy shock:

which is a hybrid of the inflation

target shock and the monetary policy shock:

| (18) |

The unobserved components in turn are perceived to follow a first-order vector autoregression:

![\begin{displaymath}\begin{array}[c]{c} \left[ \begin{array}[c]{c} \pi_{t}^{\ast}\\ e_{t} \end{array} \right] =\left[ \begin{array}[c]{cc} \rho_{p} & 0\\ 0 & \rho_{q} \end{array} \right] \left[ \begin{array}[c]{c} \pi_{t-1}^{\ast}\\ e_{t-1} \end{array} \right] +\left[ \begin{array}[c]{cc} \upsilon_{1} & 0\\ 0 & \upsilon_{2} \end{array} \right] \left[ \begin{array}[c]{c} \varepsilon_{pt}\\ \varepsilon_{qt} \end{array} \right] \\ \end{array}\end{displaymath}](img131.gif)

The inflation target

![]() is highly persistent, and has

an autoregressive root

is highly persistent, and has

an autoregressive root ![]() arbitrarily close to

unity. For simplicity, we assume that the random policy shock

arbitrarily close to

unity. For simplicity, we assume that the random policy shock

![]() is white noise (so

is white noise (so

![]() . The innovations associated with

each shock,

. The innovations associated with

each shock,

![]() and

and

![]() , are mutually uncorrelated

with unit variance.

, are mutually uncorrelated

with unit variance.

Given this linear structure, we assume that agents use the

Kalman filter to make optimal projections about the unobserved

inflation target

![]() The inflation target

perceived by agents evolves according to a first order

autoregression. Agents update their assessment of the inflation

target by the product of the forecast error innovation and a

constant coefficient. This coefficient, which is proportional to

the Kalman gain, can be expressed as a function of the

signal-to-noise ratio

The inflation target

perceived by agents evolves according to a first order

autoregression. Agents update their assessment of the inflation

target by the product of the forecast error innovation and a

constant coefficient. This coefficient, which is proportional to

the Kalman gain, can be expressed as a function of the

signal-to-noise ratio

![]() Clearly,

the signal-to-noise ratio depends on the relative magnitude of

innovations to each of the components of the observed shock

Clearly,

the signal-to-noise ratio depends on the relative magnitude of

innovations to each of the components of the observed shock

![]() but importantly, it also depends

directly on the weight

but importantly, it also depends

directly on the weight

![]() on the inflation target in the

central bank's reaction function. Intuitively, if policy is

aggressive in reacting to the inflation gap, agents will attribute

more of any unexplained rise in interest rates to a reduction in

the central bank's long-run inflation target, rather than to random

policy shocks.

on the inflation target in the

central bank's reaction function. Intuitively, if policy is

aggressive in reacting to the inflation gap, agents will attribute

more of any unexplained rise in interest rates to a reduction in

the central bank's long-run inflation target, rather than to random

policy shocks.

As argued by Erceg and Levin (2003) in the context of a somewhat

simpler dynamic model, the signal-to-noise ratio plays a crucial

role in affecting model responses to a shock to the inflation

target. Following their approach, we estimate this composite

parameter (i.e.,

![]() using the estimated

value of

using the estimated

value of

![]() by choosing the value that

minimizes the difference between historical four-quarter-ahead

expected inflation (taken from survey data) and the corresponding

expected inflation path implied by our model.22) In particular,

we minimize the loss function:

by choosing the value that