February 27, 2015

Conducting Monetary Policy with a Large Balance Sheet

Vice Chairman Stanley Fischer

At the 2015 U.S. Monetary Policy Forum, Sponsored by the University of Chicago Booth School of Business, New York, New York

Thank you. It is a great pleasure to be here to discuss some of the important issues facing the Federal Reserve and other central banks in conducting monetary policy with a large balance sheet. I will focus on two main sets of issues that the Fed has faced and will continue to face for some time. The first involves our ongoing assessment of the effects of the asset purchases. The second concerns policy normalization in the presence of a very large balance sheet.

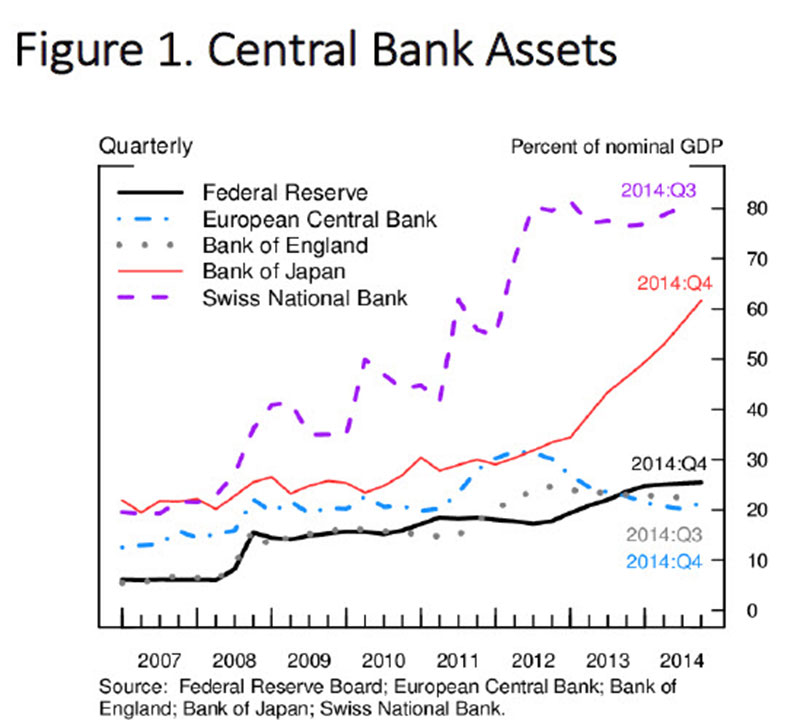

To set the stage, consider the size of the Fed's balance sheet over the past several years. Assets have risen from about $900 billion in 2006 to about $4.5 trillion today, or--as seen in figure 1--from 6 percent of nominal gross domestic product (GDP) to about 26 percent of nominal GDP. The net expansion over this period reflects primarily our large-scale asset purchase programs.

{kind=link}

Of course, many other central banks have expanded their balance sheets substantially over recent years as well. For example, assets of the Bank of Japan have increased from about 20 percent of nominal GDP to more than 60 percent of nominal GDP over this period, and assets of the Swiss National Bank have increased from 20 percent of nominal GDP to more than 80 percent of nominal GDP. The net increase in assets of the European Central Bank has so far been more modest, with assets increasing from less than 10 percent of nominal GDP to more than 20 percent of nominal GDP--but their quantitative easing (QE) program is not yet under way.

For the remainder of my remarks, I will focus on the Fed, beginning with some remarks about the asset purchase programs.

The Federal Reserve Asset Purchase Programs

The nature of our purchase programs has changed over time. In the early programs--that is to say, QE1, QE2, and the program we call the MEP, or the maturity extension program, otherwise known as "Operation Twist"--the Federal Open Market Committee (FOMC) specified the expected quantities of assets to be acquired over a defined period. Early in the crisis, this strategy seemed to help bolster confidence that the Fed was acting aggressively to offset the tightening in credit conditions and the steep downturn in economic activity.

The communication of asset purchases changed with QE3. In September 2012, the FOMC launched an open-ended asset purchase program in which it directed the New York Fed's Open Market Desk to conduct purchases at an announced monthly pace until there was "significant improvement" in the outlook for the labor market. Later, the FOMC noted that the monthly pace of purchases was data dependent, allowing the pace to be revised up or down based on its assessment of progress toward its long-run objectives.

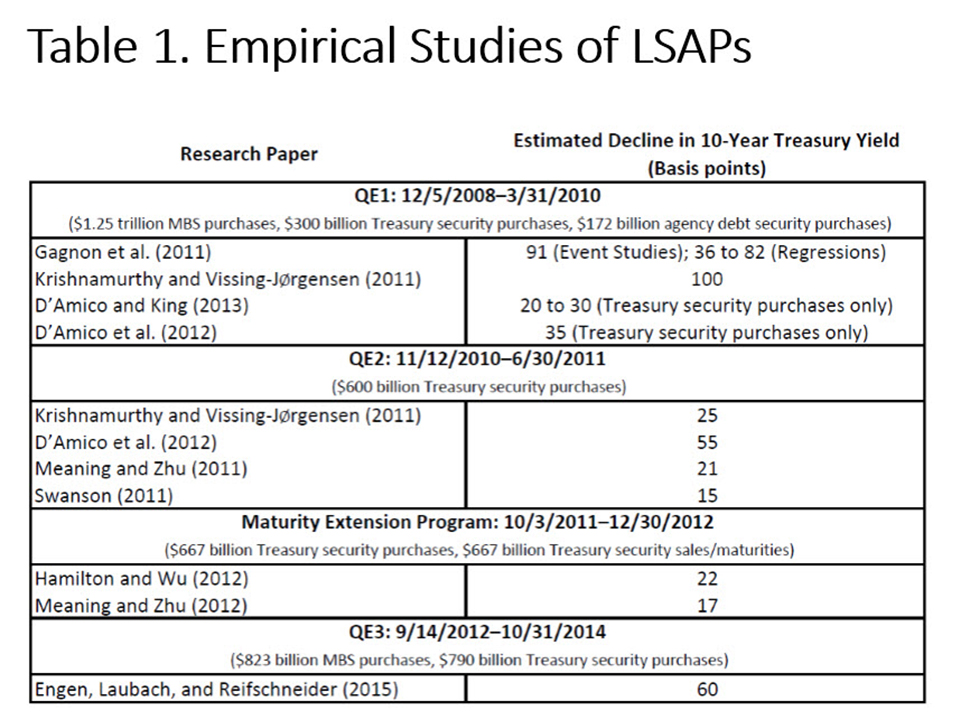

Both of these types of asset purchase programs were aimed at putting downward pressure on long-term yields.1 Table 1 provides a summary of various studies' estimated effects of these programs on the term premium on 10-year Treasury securities. For example, the decline in 10-year Treasury yields associated with the first purchase program is estimated to have been as large as 100 basis points. The documented effects associated with subsequent programs are generally smaller. These results raise the question of whether the marginal effect of asset purchases has declined over time. While that question is a valid one, our conclusion is that asset purchases over more recent years have provided meaningful stimulus to the economy, and continue to do so.

{kind=link}

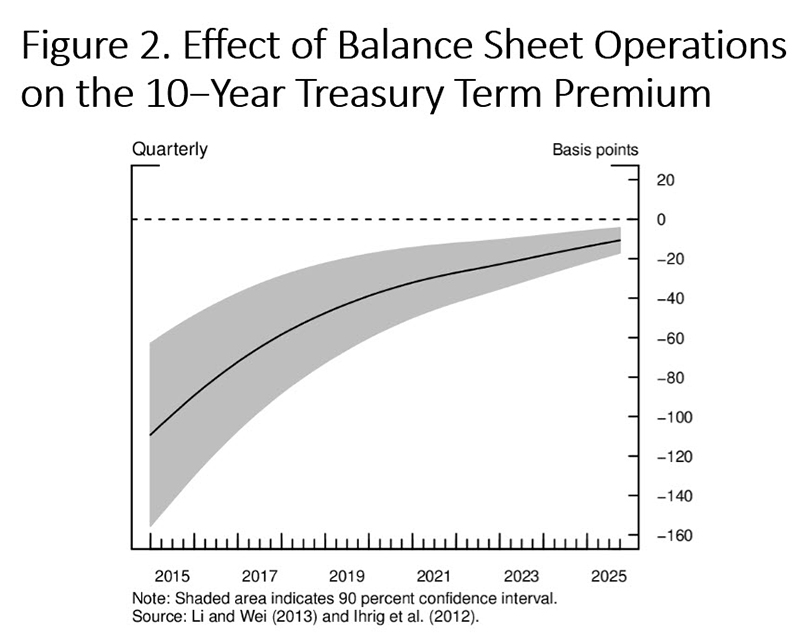

Figure 2 provides a current estimate, based on Fed staff calculations, of the effect on the term premium on 10-year Treasury securities from the combination of all asset programs.2 The results suggest that the Fed's balance sheet programs are currently depressing 10-year Treasury yields by about 110 basis points. And, with the Fed continuing to hold these securities, they should apply downward pressure on rates for some time.

{kind=link}

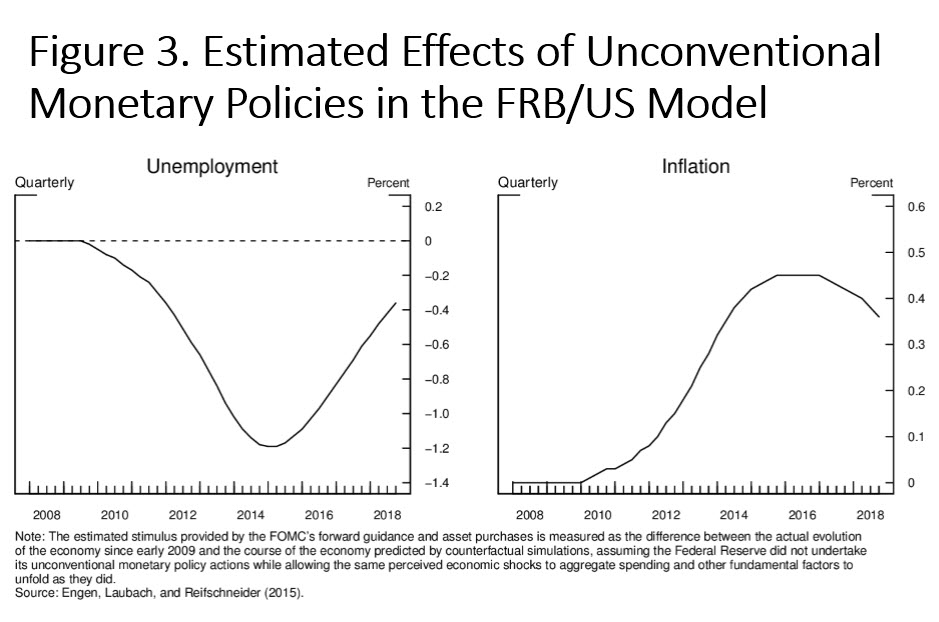

The declines in long-term yields have led to an associated drop in long-term borrowing costs for households and firms and higher equity valuations. Thus, the asset purchases have helped make financial conditions overall more accommodative and have provided significant stimulus for the broader economy. As shown in figure 3, a recent study estimates that the QE programs along with increasingly explicit forward guidance have reduced the unemployment rate by 1-1/4 percentage points and increased the inflation rate by 1/2 percentage point relative to what would have occurred in the absence of these policies.3 Moreover, the estimates imply that these macroeconomic effects are only now manifesting themselves in full, reflecting the inherent lags in the monetary transmission mechanism. Of course, such estimates have a wide band of uncertainty around them.

{kind=link}

As is well known, a number of potential costs might be associated with QE and the Fed's elevated balance sheet. Among these are the possibility that elevated securities holdings and low interest rates could pose risks to financial stability, possible effects on the Fed's income and remittances to the U.S. Treasury, and possible difficulties in conducting policy normalization.4 Such potential difficulties arise because the level of reserve balances will be very high when the FOMC begins to raise the federal funds rate, and, consequently, the Federal Reserve will employ new tools, which have their own benefits and costs, to implement monetary policy.

Despite these potential costs, we think that asset purchases have had a meaningful effect in promoting economic recovery and helping to keep inflation closer to the FOMC's 2 percent goal than would otherwise have been the case.

Policy Normalization

Turning to policy normalization, the FOMC and market participants anticipate that the federal funds rate will be raised sometime this year. We have for some years been considering ways to operate monetary policy with an elevated balance sheet.

Prior to the financial crisis, because reserve balances outstanding averaged only around $25 billion, relatively minor variations in the total amount of reserves supplied by the Desk could move the equilibrium federal funds rate up or down. With the nearly $3 trillion in excess reserves today, the traditional mechanism of adjustments in the quantity of reserve balances to achieve the desired level of the effective federal funds rate may well not be feasible or sufficiently predictable.

As discussed in the FOMC's statement on its Policy Normalization Principles and Plans, which was published following the September 2014 FOMC meeting, we will use the rate of interest paid on excess reserves (IOER) as our primary tool to move the federal funds rate into the target range.5 This action should encourage banks not to lend to any private counterparty at a rate lower than the rate they can earn on balances maintained at the Fed, which should put upward pressure on a range of short-term interest rates.

Because not all institutions have access to the IOER rate, we will also use an overnight reverse repurchase agreement (ON RRP) facility, as needed. In an ON RRP operation, eligible counterparties may invest funds with the Fed overnight at a given rate. The ON RRP counterparties include 106 money market funds, 22 broker-dealers, 24 depository institutions, and 12 government-sponsored enterprises, including several Federal Home Loan Banks, Fannie Mae, Freddie Mac, and Farmer Mac. This facility should encourage these institutions to be unwilling to lend to private counterparties in money markets at a rate below that offered on overnight reverse repos by the Fed. Indeed, testing to date suggests that ON RRP operations have generally been successful in establishing a soft floor for money market interest rates.6

The Fed could also employ other tools, such as term deposits issued through the Term Deposit Facility and term RRPs, to help drain reserves and put additional upward pressure on short-term interest rates. We have been testing these tools and believe they would help support money market rates, if needed.

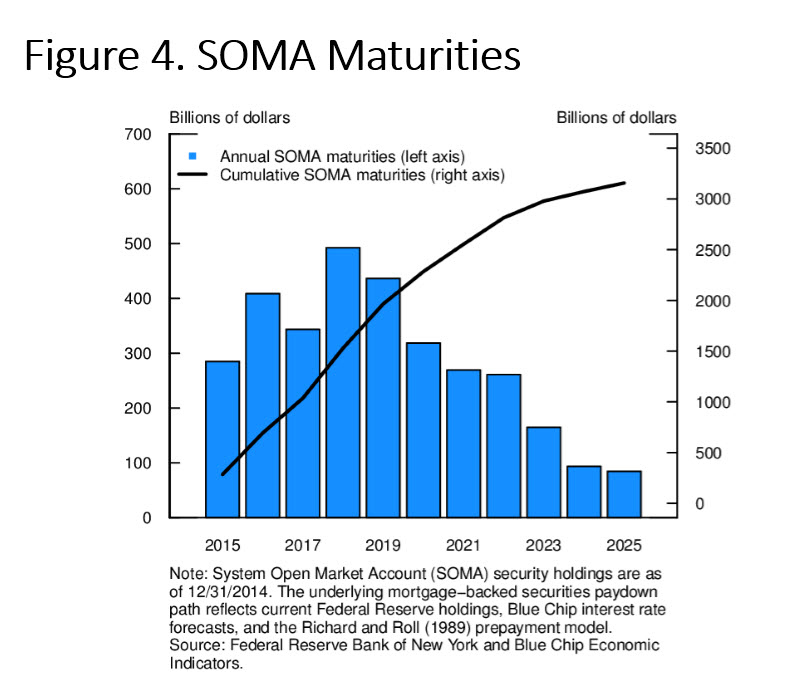

Finally, with regard to balance sheet normalization, the FOMC has indicated that it does not anticipate sales of agency mortgage-backed securities, and that it plans to normalize the size of the balance sheet primarily by ceasing reinvestment of principal payments on its existing securities holdings when the time comes. As illustrated in figure 4, cumulative repayments of principal on our existing securities holdings from now through the end of 2025 are projected to be about $3.2 trillion. As a result, when the FOMC chooses to cease reinvestments, the size of the balance sheet will naturally decline, with a corresponding reduction in reserve balances.

{kind=link}

Conclusion

I will close by highlighting that the Fed's asset purchases have been a critical means by which the FOMC has provided policy accommodation at the zero lower bound on nominal interest rates. In other words, the Fed--and other central banks--can implement an expansionary monetary policy even when the policy interest rate is at the zero lower bound. The current high level of securities holdings will present some challenges for policy normalization, but we are confident that we have the tools necessary to remove accommodation at the appropriate time and at the appropriate pace.

1. The Fed staff analysis has focused mostly on the so-called stock effects of the purchase programs--that is, persistent shifts in asset prices observed as the result of a QE program. While these stock effects are well documented in the literature, there have been relatively fewer studies of "flow effects" that may occur at the time of QE transactions (for example, see Stefania D'Amico and Thomas B. King (2013), "Flow and Stock Effects of Large-Scale Treasury Purchases: Evidence on the Importance of Local Supply," Journal of Financial Economics, vol. 108 (May), pp. 425-48; and John Kandrac and Bernd Schlusche (2013), "Flow Effects of Large-Scale Asset Purchases," Economics Letters, vol. 121 (November), pp. 330-35). Return to text

2. The estimates shown in figure 2 are based on an extension of the work done in Ihrig, Klee, Li, Schulte, and Wei (2012). Because the term premium effect depends on both the Fed's current and expected future asset holdings, most of this effect--without further unexpected policy actions--will likely wane over the next few years as the balance sheet begins to normalize. See Jane Ihrig, Elizabeth Klee, Canlin Li, Brett Schulte, and Min Wei (2012), "Expectations about the Federal Reserve's Balance Sheet and the Term Structure of Interest Rates (PDF)," Finance and Economics Discussion Series 2012-57 (Washington: Board of Governors of the Federal Reserve System, July). Return to text

3. See Eric Engen, Thomas Laubach, and David Reifschneider (2015), "The Macroeconomic Effects of the Federal Reserve's Unconventional Monetary Policies (PDF)," Finance and Economics Discussion Series 2015‑005 (Washington: Board of Governors of the Federal Reserve System, January). Return to text

4. Reflecting securities holdings from the asset purchases, the Federal Reserve has remitted about $500 billion to the U.S. Treasury from 2008 to 2014 and is expected to have cumulative net income from 2008 to 2025 that is far higher than would have been the case in the absence of these asset purchases. Return to text

5. See Board of Governors of the Federal Reserve System (2014), "Federal Reserve Issues Statement on Policy Normalization Principles and Plans," press release, September 17. Return to text

6. Policymakers have discussed benefits and costs of an ON RRP facility. For further discussion on this topic, see, for example, the FOMC minutes for June 2014, July 2014, and January 2015 available on the Board's webpage "Federal Open Market Committee: Meeting Calendars, Statements, and Minutes (2009-2015)" ; and Josh Frost, Lorie Logan, Antoine Martin, Patrick McCabe, Fabio Natalucci, and Julie Remache (2015), "Overnight RRP Operations as a Monetary Policy Tool: Some Design Considerations (PDF)," Finance and Economics Discussion Series 2015-010 (Washington: Board of Governors of the Federal Reserve System, February). Return to text

{kind=link}

{kind=link}