November 19, 2015

Emerging Asia in Transition

Vice Chairman Stanley Fischer

At the "Policy Challenges in a Diverging Global Economy" 2015 Asia Economic Policy Conference sponsored by the Federal Reserve Bank of San Francisco, San Francisco, California

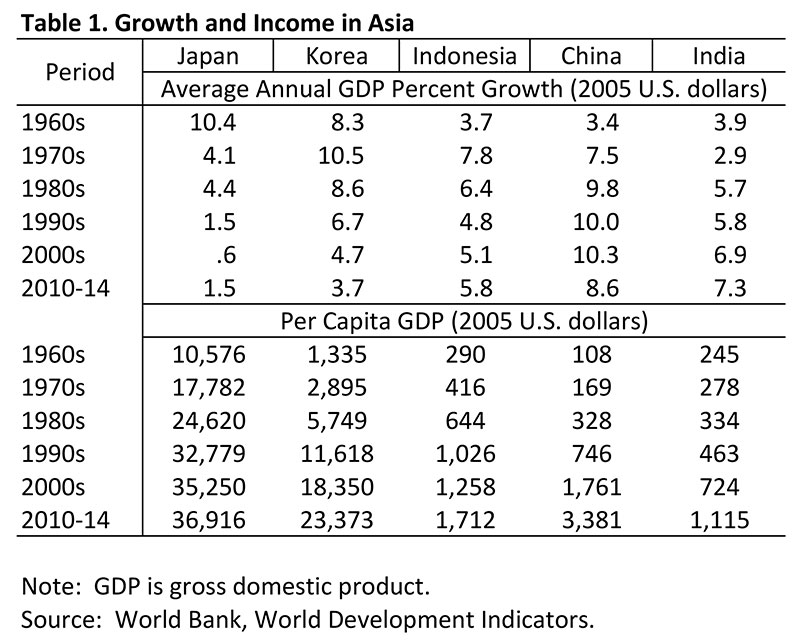

I am grateful for the opportunity to participate in the Federal Reserve Bank of San Francisco's Asia Economic Policy Conference, and I thank the organizers for inviting me.1 After a long period of rapid economic growth, Asia's emerging economies appear to have entered a transitional phase. For decades, emerging Asian economies have been among the fastest growing and most dynamic in the world. Supported by an export-oriented development model, annual growth averaged 7-1/2 percent in the three decades leading up to the global financial crisis. As shown in table 1, the fast pace of growth in emerging Asia has also supported impressive gains in per capita income within the region.

{kind=link}

As the economies of emerging Asia have developed, they have followed a similar growth trajectory, also apparent in table 1. Along a path pioneered by Japan in the 1960s, initial integration into the global economy has been followed by a period of rapid export-led economic growth, which subsequently slows as the economy develops and incomes rise. In a process that has been likened to the pattern of flying geese, development in Japan pushed more labor-intensive production from Japan into the "Asian tigers"--that is, Hong Kong, Korea, Singapore, and Taiwan--with that set of countries experiencing rapid growth in the 1970s and 1980s. As the tigers developed, low-value-added production was pushed further on, into the group of countries known as the Association of Southeast Asian Nations (ASEAN)--primarily Indonesia, Malaysia, Thailand, and, more recently, China, where growth took off in the 1980s and accelerated through the 2000s.2 At each step in this process, the slowing of growth in the relatively developed and globally integrated Asian economies was matched by an acceleration of growth in the less developed and less integrated economies, maintaining the overall rapid pace of growth in the region.3

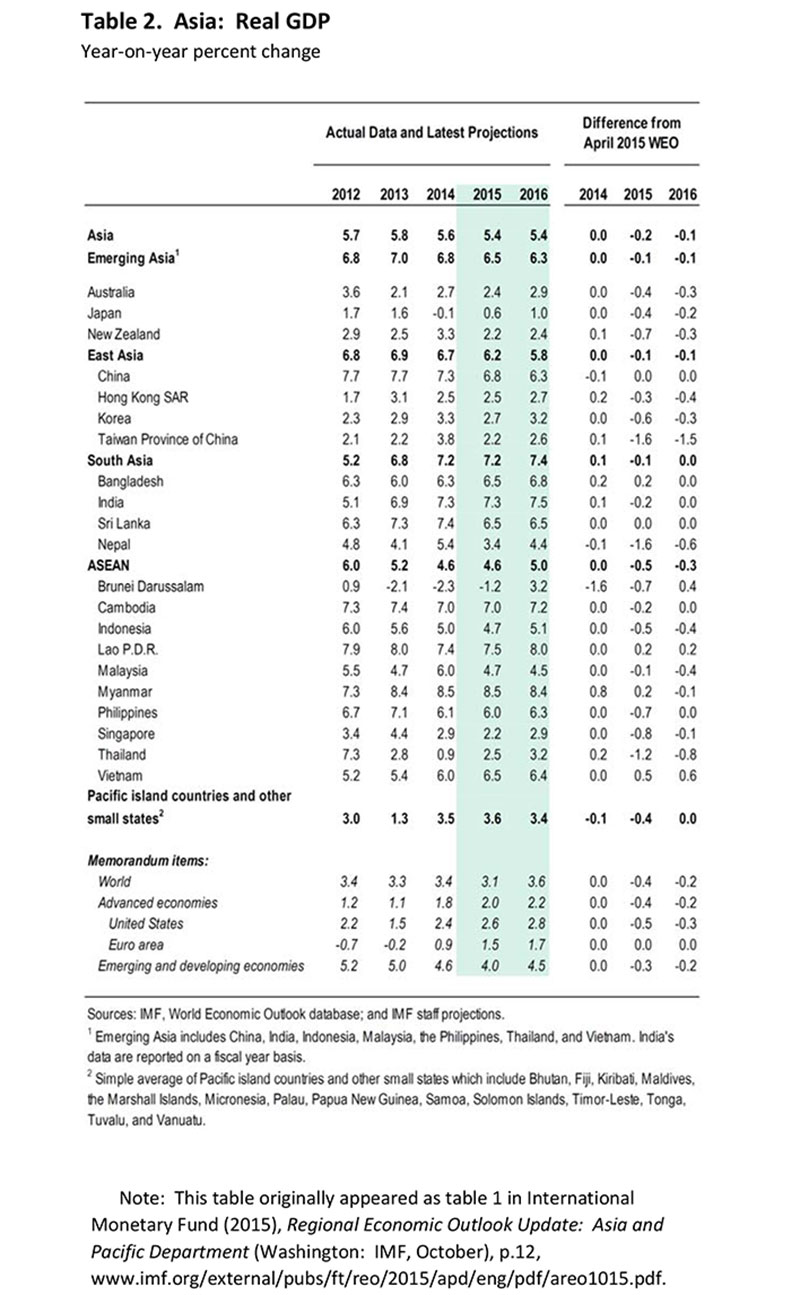

Now, with China perhaps beginning to follow the same trajectory of slowing growth as has been experienced by its predecessors in the East Asian growth model and without economies of sufficient scale to fill the gap (with the notable exception of India, which I will discuss later), growth for the region as a whole is declining. As shown in table 2, taken from the most recent International Monetary Fund (IMF) regional outlook for Asia, growth in emerging Asia is set to decline in 2015 and 2016, with China's growth decelerating.4 Furthermore, the IMF projections through 2020 call for almost no pickup from this slower pace.

{kind=link}

In my discussion, I will first address some of the factors behind slowing growth in emerging Asia, importantly including demographics. I will then cover one of the global implications of this deceleration, the effect on commodity markets, before looking at the prospects for India to recharge the region's growth dynamic. I will end with some thoughts on Asia's place in the global economy both now and in the years to come.

Why Is Growth in Emerging Asia Slowing?

The first thing to say and think about Asian growth is that growth at a rate of above 6 percent is not slow; it is slower than it has been, but it remains impressive. There are four factors weighing on emerging Asian growth that I would like to highlight. First, emerging Asia continues to be negatively affected by slow demand growth elsewhere, including in the advanced economies. Second, economies generally decelerate as they develop, a pattern that has already been evidenced in many of emerging Asia's growth pioneers. Third, the tremendous growth of trade in the region, driven by the process of global integration and the growth of production-sharing networks, may have plateaued. Lastly, demographic trends in a number of emerging Asian countries are likely to affect growth in the coming years.5

Regarding the first of the factors that I just listed, contrary to often-repeated and often-resurrected stories of emerging market growth "decoupling" from that of the advanced economies, the truth is that advanced-economy demand continues to play a key role in emerging Asia's economic conditions.6 And, as we all know, advanced-economy demand for imports in recent years has been lackluster. Real goods imports in the United States, Japan, and the euro area have all increased at an average annual pace of about 3-1/2 percent over the past three years, in all cases about half the average pace recorded in the two decades leading up to the financial crisis.

Regarding the second factor, as is well established by theory and supported by empirical experience, economic growth tends to decelerate as a country develops. In a capital-poor developing economy, initial increases in investment generally have high returns, which then decline as capital accumulates. Likewise, the initial phase of integration with the global economy is typically marked by strong gains in productivity as methods and technologies are adopted from more advanced economies. Over time, the boost to growth from this catch-up in productivity fades. Also, as incomes rise and consumption grows, there is a tendency for a relatively rapid increase in demand for services. The shift of domestic resources toward the production of services, which are typically associated with lower productivity growth, tends to further lower trend growth.

The factors that have tended to temper growth as economies develop appear to be at play in China. Following years of exceptionally high investment, the return on capital appears to be moderating, and the ratio of investment to gross domestic product (GDP), after peaking near 50 percent of GDP in 2011, has begun to edge down. As viewed in the context of the Lewis model, China could be reaching the stage at which the supply of labor from the subsistence agricultural sector becomes a constraint on growth. Further, productivity growth, though robust by global standards, has been declining.

This decrease is likely due, at least in part, to the rapid growth of services consumption. One of the most noteworthy aspects of China's recent GDP data has been the strength of services, with services now accounting for half of the value added in GDP, up from just over 40 percent in 2008.

Next, I would like to discuss the third factor weighing on Asian growth--trade. Global integration and trade growth have played a key role in the Asian economic success story, and the recent slowdown in global trade, over and above what might be expected given the weakness of advanced-economy demand discussed earlier, is likely to affect emerging Asian growth prospects.

During the financial crisis, global trade collapsed. After the immediate crisis faded, trade bounced back in many cases. But the bounceback was more limited than the decline, with the increase in the volume of trade since 2012 only matching the pace of global output growth, a considerable deceleration from the previous two decades, when trade increased at twice the pace of global output. While the legacy of the crisis, particularly the continued weakness of traded-good-intensive investment in many economies, has likely contributed to the weakness of global trade, a slowdown in intra-Asian regional trade also appears to be a factor. After increasing at an average rate of about 15 percent a year through the 2000s, nominal intra-Asian trade flows have flattened out considerably over the past couple of years, in part reflecting a slowdown in the growth of production sharing within the region.

The outlook for a renewed surge in intra-Asian trade does not appear to be promising. The growth of production-sharing networks in Asia has been tied to the region's export-oriented growth model. In particular, China's integration into the global economy as the hub of this production network provided a significant boost to the development and growth of these networks. As China and the region shift toward domestic demand and away from external demand, it seems unlikely that trade growth in the region will return to its earlier exceptional pace.

To the extent that the expansion of these networks was tied to export-led growth that depended partly on preferential treatment of the export sector, more-balanced growth in these economies may also result in a better allocation of production across countries. If growth of trade is lower as a result, that is not necessarily a problem. However, there is a well-established literature indicating that trade encourages greater efficiency, along with the dissemination of technological innovation, and slower growth of trade could reduce this effect.

It also bears noting that Asian trade growth has been accompanied by the creation of a variety of intraregional and broader trade agreements--including the 10-nation ASEAN and membership in the World Trade Organization, which China achieved in 2001 and Vietnam in 2007--as well as a host of bilateral agreements, both within and outside the region. I will return briefly to the Trans-Pacific Partnership (TPP) at the end of the talk.

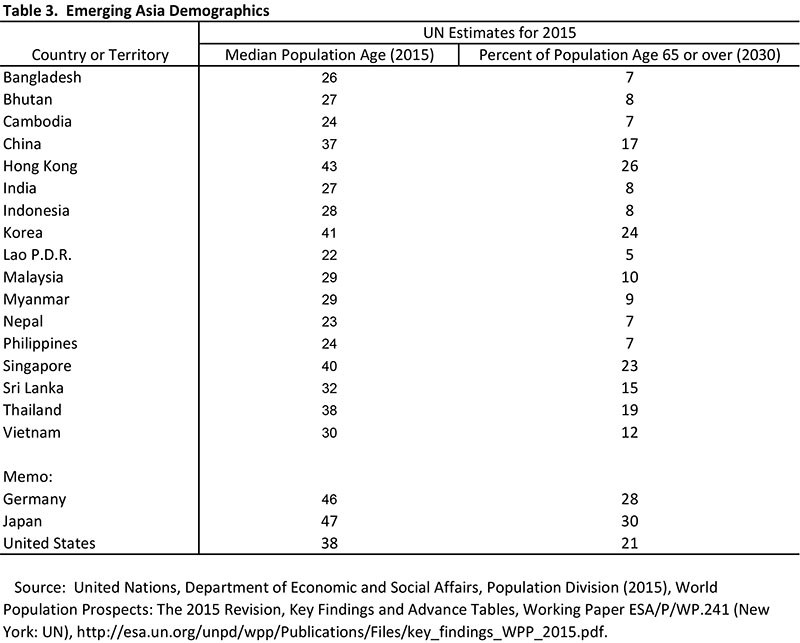

Finally, demographics are an additional factor likely to lower growth in the region, particularly in Hong Kong, Korea, Singapore, Thailand, and China, notwithstanding the recent relaxation of the one-child policy. As shown in table 3, both China and Thailand have a median population age of about 37 years, about the same as the median in the United States. The median age is even higher in Hong Kong, Korea, and Singapore, all of which have medians of 40 years or more. Relatedly, as shown in the second column of the table, China, Thailand, and the relatively developed emerging Asian economies are expected to have a significant percentage of their populations older than 65 years by 2030, with the proportion similar to that in the United States, though still below those in Germany and Japan. In contrast, demographics are less of an issue elsewhere in the region, particularly in India and most of ASEAN, including Indonesia, Malaysia, the Philippines, and Vietnam, which have medians of 30 years or less. Just as slowing workforce growth is likely to be a drag on growth in many developed countries, trend growth is likely to be held back by demographic developments in relatively elderly emerging Asian economies as well.

{kind=link}

Up to this point, I have discussed a number of factors that are likely to lower emerging Asia's growth trajectory in the coming years. However, the overall message is not a pessimistic one; rather, for the most part, the slowing of growth is a natural transition and an outcome of Asia's remarkable economic success.

As many have noted over the years, maintaining growth sufficiently rapid to meet the development aspirations of the region will require a transition toward an economic paradigm more rooted in domestic demand, particularly consumption. The need for this transition, or rebalancing, is most apparent and also widely acknowledged in China, the current hub of emerging Asia's export-led model. The need for these economies--primarily China, but also those economies that export through China--to switch toward domestic demand largely reflects their having become too big and too important to rely to the extent they have on the export-led models of the past.

On growth, the bottom line that should be emphasized is that even with a diminished pace of growth, the region is still expected to significantly outpace the global economy and make by far the largest contribution to global growth in the years ahead.

Spillovers from Asia's Economic Transition: Commodity Markets

I will now focus on an area where the spillovers of Asia' economic transition are likely to be substantial--global commodity markets.

Emerging Asia has played an outsized role in commodity markets for some time now. Specifically, China, with its investment-heavy growth model, has accounted for a substantial amount of incremental commodity demand over the past two decades. Since 2000, China has accounted for roughly 40 percent of the increase in global demand for oil and 80 percent of the growth in demand for steel. For copper, all of the incremental rise in global demand has come from China, with demand excluding China falling over the period.

The strength of emerging Asian demand growth pushed commodity prices up sharply over most of the past decade, at least temporarily reversing what seemed to be an inexorable decline in both commodity prices and the terms of trade of commodity producers in the preceding two decades. Higher prices were a tremendous boon to commodity producers and supported a decade of strong growth in a number of emerging market economies, as well as commodity sectors in certain advanced economies, including Australia and the United States.

Since mid-2014, commodity prices have plummeted, with oil prices falling almost 60 percent and a broad index of metals prices losing about one-third of its value, dragging down growth in many commodity producers. Although rapid commodity output growth in recent years, which has reflected in part the response of producers to previous price increases, has certainly contributed to the fall in commodity prices, the slowing of demand growth from China and emerging Asia has also been an important factor.

While the path ahead for commodity prices is, as always, uncertain, declining investment rates in emerging Asia, particularly China, present the prospect of a prolonged decline in the growth rate of commodity demand. And prices could remain low for quite some time, which seems particularly true for metals, such as copper and steel, used heavily in construction and investment. However, for oil, the implications of a shift from investment-led growth to a consumption-led model are less certain. On a per capita basis, China's consumption of oil remains far below that of advanced economies, in line with China's lower rate of car ownership. Per capita oil consumption tends to increase with wealth, such that further income growth in China has the potential to provide strong support for the oil market in the coming years.

Indeed, more generally, the world stands to benefit from a transition to more consumption-led growth in emerging Asia. Under a successful transition toward more-balanced growth, emerging Asia can be expected to import a broader array of goods and services both from within the region and globally. Whether a country benefits from or is harmed by emerging Asia's transition is likely to be determined by the flexibility of that country's economy in adapting to shifts in Asian demand away from commodities and inputs for assembly into the region's exports and toward services and goods to meet Asian final demand.

To recap, the transition to slower growth in the emerging Asian economies, as well as a shift toward domestic demand and consumption and away from external demand and investment in the region, is likely to have profound implications for the global economy. For one, trade growth is unlikely to resume its rapid pace of recent decades, and the long climb in commodity prices, which has benefited commodity producers, appears to have come to an end.

Can India Recharge Growth in Emerging Asia?

One source of uncertainty in this outlook, as alluded to earlier, is the prospect for India to provide a new growth engine for Asian development. In principle, India has enormous potential to recharge the Asian growth engine. For one, India is relatively unintegrated into global production-sharing networks. For example, machinery and electrical products, which feature heavily in production-sharing and which make up about half of exports in other emerging Asian economies, account for only 15 percent of India's exports. Foreign direct investment into India is about half the size of similar flows into China as a percentage of GDP, and GDP per capita, at $1,600 in 2014, remains considerably below emerging Asia's average.

All told, while the export-led growth model that propelled growth in China and other economies in emerging Asia has matured, pushing down growth rates, India remains at a relatively early stage of its development trajectory. Further capital deepening and the potential for further productivity gains suggest that India could maintain rapid economic growth for a number of years. As mentioned previously, India is also a young country, with a relatively low dependency ratio and a growing workforce. By United Nations estimates, India is set to overtake China during the next decade as the world's most populous nation.

In the 1960s and 1970s, the Indian economy grew at around 3 to 4 percent. In subsequent decades the growth rate averaged close to 6 percent, and in the early years of this century it rose further, as can be seen in Table 1. In 2015, growth in India is expected to be 7-1/4 percent, the fastest among large economies, and the IMF expects growth to pick up from this already rapid pace through the end of the decade. Growth has been supported by an improved macroeconomic policy framework, including a strengthening of the framework for conducting monetary policy, as well as legal and regulatory reform. And the authorities have embarked on an ambitious program to improve the business environment.

That said, significant roadblocks need to be overcome for India to reach its full potential. The economy continues to suffer from a number of infrastructure bottlenecks that will be alleviated only through a pronounced increase in investment rates, a process that would likely be helped by a relaxation of restrictions on foreign direct investment. Likewise, efforts at difficult reform will have to be sustained. There is much hard work ahead if India is to come closer to fulfilling the potential that it so manifestly has.

Concluding Remarks

The performance of the Asian economies--notably those of East Asia, particularly China, Japan, and Korea--especially in the past six or seven decades, is an outstanding, if not unique, episode in the history of the global economy.

What lies ahead? In the relatively near future probably some major central banks will begin gradually moving away from near-zero interest rates. The question here is whether the emerging market countries of Asia--and, indeed, of the world--are sufficiently prepared for these decisions, to the extent that potential capital flows and market adjustments can take place without major macroeconomic consequences. While we continue to scrutinize incoming data, and no final decisions have been made, we have done everything we can to avoid surprising the markets and governments when we move, to the extent that several emerging market (and other) central bankers have, for some time, been telling the Fed to "just do it."

Further ahead lies the answer to the question of whether developments in the global economy will permit the continuation of the export-centered growth strategy that underlies the Asian miracle or whether we will later conclude that this period, the period after the Great Recession and the global financial crisis, marked the beginning of a new phase in the economic history of the modern global economy.7 Either way, the question of the economic future of India is of major importance not only to the 18 percent of the world's population that lives in India, but also to the other 82 percent of the global population.

At a more structural level are three recent developments whose potential importance is currently difficult to assess: the setting up of the Asian Infrastructure Investment Bank; the likely inclusion of the Chinese yuan in the Special Drawing Rights basket; and the possible establishment of the TPP, a partnership in which China is not expected to be a founding member.8

These are interesting and potentially important developments. Underlying the answer to the questions of what they portend, is the answer to the basic question of whether the economic center of gravity of the world will continue its shift of recent decades toward Asia--in particular, to China or, perhaps, to China and India. This shift would represent a return in some key respects to the global order of two centuries ago and earlier, before the economic rise of the West.

A partial answer to that question is that China is for some time likely to continue to grow faster than the rest of the world and thus to produce an increasing share of global output. Its importance in the global economy is likely to increase, and it is probable that, one way or another, its growth will result in its playing a more decisive role in the international economy and in international economic institutions.

Finally, we need to remind ourselves that geopolitical factors will play a critical role in the unfolding of that process.

References

Brandt, Loren, and Thomas G. Rawski (2008). "China's Great Economic Transformation," in Loren Brandt and Thomas G. Rawski, eds., China's Great Economic Transformation. New York: Cambridge University Press.

Haltmaier, Jane T., Shaghil Ahmed, Brahima Coulibaly, Ross Knippenberg, Sylvain Leduc, Mario Marazzi, and Beth Anne Wilson (2007). "The Role of China in Asia: Engine, Conduit, or Steamroller? (PDF)" International Finance Discussion Papers 904. Washington: Board of Governors of the Federal Reserve System, September.

Monetary Authority of Singapore (2007). "Revisiting the US-Asia Decoupling Hypothesis," special feature B, Macroeconomic Review, vol. 6 (October), pp. 72-80.

World Bank (1993). The East Asian Miracle: Economic Growth and Public Policy . Washington: WB, September.

Zheng, Kit Wei, Ong Jia Wern, and Kevin Kwan Tai You (2005). "China's Rise as a Manufacturing Powerhouse: Implications for Asia (PDF)," MAS Staff Paper 42. Singapore: Monetary Authority of Singapore, December.

1. The views expressed here are my own and not necessarily those of others at the Board, on the Federal Open Market Committee, or in the Federal Reserve System. I am grateful to Joseph Gruber and Jasper Hoek for their contributions to this speech. I also thank Ravi Menon of the Monetary Authority of Singapore and Changyong Rhee, Ratna Sahay, and James Walsh of the International Monetary Fund for their assistance. Return to text

2. With some delay, the Philippines could be added to this group.

As production of labor-intensive goods has moved from one group of countries to the next, concerns have been raised about a decrease in "competitiveness" in the relatively more developed Asian economies. These concerns have been particularly pronounced in regard to China, where commentators have questioned whether China's rise has come at the expense of growth in its neighbors or provided an extra impetus to growth. Research studies (see Zheng, Wern, and You (2005) and Haltmaier and others (2007)) have generally found that China's rise has been positive for regional growth, with China's development as an export platform boosting the overall competitiveness of the region's exports. Return to text

3. In addition to integration with the global economy, a number of other factors have also contributed to the East Asian growth miracle. With regard to China, Brandt and Rawski (2008) highlight the importance of incremental reform focused on removing the most binding constraints on economic activity. Of course, reform is not independent of global integration, as the heightened international competition associated with opening an economy likely incentivizes increased reform. Return to text

4. The IMF does not include Hong Kong, Korea, Singapore, or Taiwan in its definition of emerging Asia. For the purposes of my discussion, I group these four economies along with China, India, Indonesia, Malaysia, the Philippines, Thailand, and Vietnam as emerging Asia. Return to text

{kind=link}

5. In a speech of this length and scope, it is not possible to relate all important developments affecting Asian growth. In particular, I will not address the need for further development of financial systems and infrastructure in Asian emerging economies, which will be important factors in determining future rates of growth. Return to text

6. This point is particularly well made in Monetary Authority of Singapore (2007). Return to text

7. See World Bank (1993) for an early attempt to define the sources of East Asian growth. Return to text

8. At this point, the reader will recall the supposed remark by Chou En-lai that it is too early to assess the importance of the French revolution. The most plausible current version of that story is that Chou was answering a question about the importance of the 1968 student riots in Paris.

The countries expected to become members of the TPP are, in alphabetical order, Australia, Brunei, Canada, Chile, Japan, Malaysia, Mexico, New Zealand, Peru, Singapore, the United States, and Vietnam. Return to text