November 06, 2014

A Financial System Perspective on Central Clearing of Derivatives

At the "The New International Financial System: Analyzing the Cumulative Impact of Regulatory Reform", 17th Annual International Banking Conference, Chicago, Illinois

Thank you for the opportunity to address the important topic of how the financial system and its regulation have evolved in response to the global financial crisis. I will focus my remarks on the global initiative to expand central clearing of over-the-counter (OTC) derivatives. While we have made significant progress in enlisting central clearing to reduce systemic risks, I will argue that there is a good deal more to do to ensure that the reforms achieve their potential and minimize the possibility of unintended and undesirable consequences.1

Prior to the crisis, the then highly opaque market for OTC derivatives grew at an astonishing and unsustainable pace of nearly 25 percent per annum in a context of relatively light regulation and bilateral clearing.2 With the benefit of hindsight, we know that along with this torrid growth came an unmeasured and underappreciated buildup of risk. The spectacular losses suffered by American International Group, Inc., or AIG, on its derivatives positions, and the resulting concerns about the potential effect of AIG's failure on its major derivatives counterparties, serve as particularly apt reminders of the wider failures and weaknesses that were revealed by the crisis.

The threats posed were global, and the response was global as well. In September 2009, the Group of Twenty (G-20) mandated that all sufficiently standardized derivatives should be centrally cleared--a sea change in the functioning and regulation of these markets. And in the five intervening years, substantial progress has been made in the United States and abroad to implement this reform and begin to reduce systemic risk in these markets. According to public data, roughly 20 percent of all credit derivatives and 45 percent of all interest rate derivatives are now centrally cleared--amounts that have grown substantially since 2009, when central clearing of credit derivatives began and the amount of cleared interest rate derivatives was at roughly one-half of its current level.3 These amounts should continue to grow over time as central clearing and, especially, client clearing requirements take effect in more jurisdictions.

Given the global nature of derivatives markets, the success of the reform agenda depends critically on international coordination. Thus, to support the move to central clearing and address other lessons from the financial crisis, regulators developed the new Principles for Financial Market Infrastructures (PFMIs) for the infrastructures that clear derivatives, securities, and payments.4 The PFMIs are comprehensive international standards for the governance, risk management, and operation of central counterparties (CCPs) and other financial market infrastructures. Such standards are essential given that, in the interest of transparency and improved risk management, policymakers have encouraged the concentration of activities at these key nodes. And it is particularly important that the standards be promulgated globally, given the potential for OTC derivatives to span multiple jurisdictions and to migrate to jurisdictions where standards and risk management are less robust. Regulators are now engaged in the important work of translating these principles into national regulations. Only when these strong international standards have been implemented at CCPs around the world can the risk reduction promised by the global clearing mandate be fully realized.

Further Challenges Facing Central Clearing

The task is far from complete. We must consider how central clearing and CCPs fit into the rest of the financial system. From this systemwide perspective, central clearing raises a number of important issues that should be kept in mind as its use increases. I will now consider several of those issues and associated challenges in some detail.

A number of commentators have argued that the move to central clearing will further concentrate risk in the financial system. There is some truth in that assertion. Moving a significant share of the $700 trillion OTC derivatives market to central clearing will concentrate risk at CCPs. But the intent is not simply to concentrate risk, but also to reduce it--through netting of positions, greater transparency, better and more uniform risk-management practices, and more comprehensive regulation. This strategy places a heavy burden on CCPs, market participants, and regulators alike to build a strong market and regulatory infrastructure and to get it right the first time.

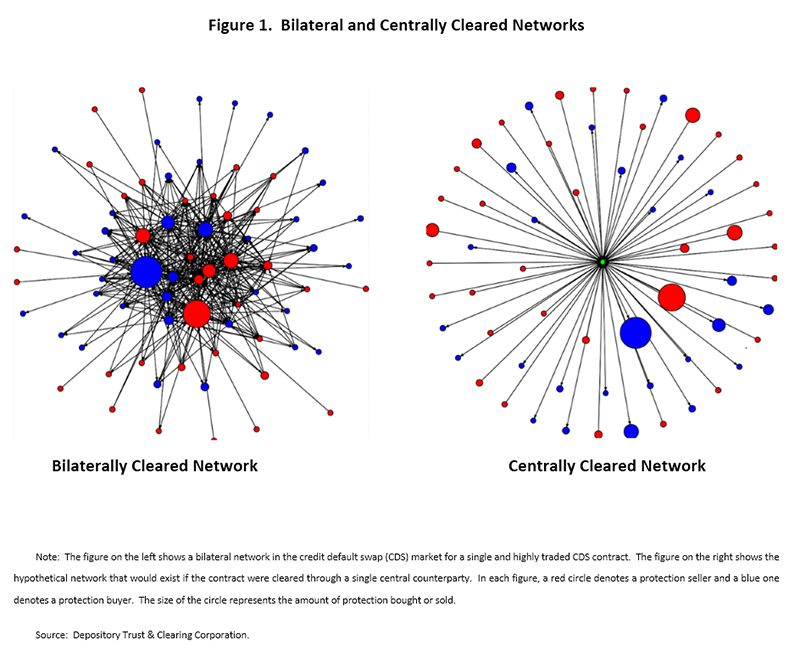

It has also been frequently observed that central clearing simplifies and makes the financial system more transparent. That, too, has an element of truth to it, but let's take a closer look. Charts similar to the ones shown in figure 1 are frequently offered to illustrate the point that, as a CCP becomes a buyer to every seller and a seller to every buyer, it causes risks to be netted and simplifies the network of counterparties. The dizzying and opaque constellation of exposures that exists in a purely bilateral market, illustrated in the chart on the left, is replaced by a neat hub-and-spoke network that is both known and more comprehensible, illustrated in the chart on the right. The CCP and its regulators are then in a position to observe the CCP's entire network, which can be important in the event that one or more clearing members become impaired. CCPs may also be able to coordinate a response to problems in their markets in ways that individual clearing members would find very difficult.

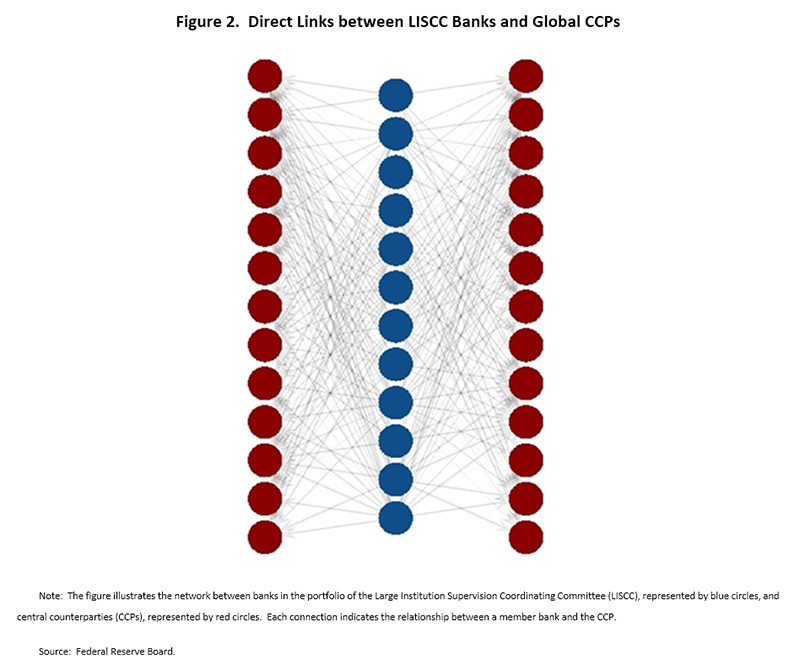

Figure 2 shows that, at the same time, in the real world CCPs bring with them their own complexities. As the figure shows, we do not live in a simple world with only one CCP. We do not even live in a world with one CCP per product class, since some products are cleared by multiple, large CCPs.5 Also, significant clearing members are often members of multiple CCPs in different jurisdictions. The disruption of a single member can have far-reaching effects. Accordingly, while CCPs simplify some aspects of the financial system, in reality, the overall system supporting the OTC derivatives markets remains quite complex.

To carry out their critical functions, CCPs rely on a wide variety of financial services from other financial firms, such as custody, clearing, and settlement. Many of these services are provided by the same global financial institutions that are also the largest clearing members of the CCPs. The failure of a large clearing member that is also a key service provider could disrupt the smooth and efficient operation of one or multiple CCPs, and vice versa. In the event of disorderly CCP failures, the netting benefits and other efficiencies that CCPs offer would be lost at a point when the financial system is already under significant stress. Ultimately, the system as a whole is only as strong as its weakest link.

People often think of these relationships between CCPs and clearing members in terms of credit exposures, but there are also important interconnections in the need for and use of liquidity. Historically, some CCPs viewed liquidity in terms of daily operational needs. From a macroprudential perspective, this view of liquidity is far too narrow. If a CCP is to act as a buffer against the transmission of liquidity shocks from a clearing member's default, the CCP itself must have a buffer of liquidity it can draw on to make its payments on time even during periods of market stress. The PFMIs introduced a new liquidity standard that requires CCPs to cover, at a minimum, the liquidity needs of the CCP on the failure of the single clearing member and its affiliates with the largest aggregate position, in extreme but plausible market conditions. Liquidity needs are to be met with a predefined list of liquid resources, starting with cash.

Moreover, the largest clearing members participate in many CCPs around the world. Cash management at these clearing members, particularly intraday cash management, involves interconnected cash flows to and from a clearing member's various CCPs, other market infrastructures, and other financial institutions. If a clearing member were to default, cash flows and needed financial services could be disrupted simultaneously at several CCPs. Failure of one or more CCPs to pay margin or settle obligations as promised could impair the ability of a clearing member to meet other obligations and transmit liquidity risk to others in the financial system. Accordingly, CCPs require a liquidity profile that will allow them to absorb rather than amplify the liquidity shocks that are likely to materialize during a period of financial stress following a member's default.

Of course, clearinghouses have been around for quite some time and have generally stood up well even in severe crises.6 But let's look a little deeper at the risks. During the global financial crisis, governments around the world took extraordinary actions to shore up many of the large financial institutions that are also large clearing members. While it is not possible to say with confidence what would have happened if these measures had not been taken, it is surely the case that whatever pressures CCPs faced would have been many times greater, and the potential consequences much greater as well. Moreover, as CCPs grow into their enhanced role in the financial system, they will represent an ever larger locus for systemic risk. It is therefore important not to be lulled into a false sense of security that past performance is a guarantee of future CCP success.

After the crisis, governments firmly resolved that even the largest financial institutions must be allowed to fail and be resolved without taxpayer support and without threatening the broader financial system or the economy. CCPs therefore need to adapt to a world in which their largest clearing members will be allowed to fail and to be resolved without taxpayer support. And, as I will discuss a little later, the same is true of CCPs--they, too, should have no expectation of taxpayer support if they fail. To say it as plainly as possible, the purpose of all of this new infrastructure and regulation is not to facilitate the orderly bailout of a CCP in the next crisis. Quite to the contrary, CCPs and their members must plan to stand on their own and continue to provide critical services to the financial system, without support from the taxpayer.

The Road Ahead: Meeting the Challenges

As you can see, central clearing represents the confluence of critical market infrastructure and systemic financial institutions. As a result, the regulation and supervision of CCPs present particular challenges. What matters most is the stability of the entire system, not that of one sector or another. In the United States, CCPs are primarily regulated by either the Commodity Futures Trading Commission or the Securities and Exchange Commission. Under authority provided by the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010, the Federal Reserve also plays a role in supervising and regulating systemically important CCPs and other financial market utilities.7 In addition, the Federal Reserve is the holding company supervisor of a number of the largest clearing members. The challenge is to ensure that regulation and supervision take into account the broad implications of derivatives trading for CCPs, their members, and the broader financial system. Close collaboration between regulators--both domestically and internationally--will be necessary to ensure that central clearing can promote the kind of financial system resiliency that will be required when another severe crisis threatens.

While central clearing and CCPs do present a number of complex and unique challenges, these challenges are not insurmountable. Several measures should be considered in the near term to further strengthen the market and regulatory infrastructure relating to liquidity, transparency, stress testing, "skin in the game," and recovery and resolution.

Liquidity

The adoption of the PFMIs around the world is driving improvements in CCP liquidity.8 Ultimately, CCPs and their supervisors will need to maintain vigilance to ensure that liquid resources are sufficient to withstand the kinds of liquidity shocks that would likely accompany a member's default. In addition, it is crucial that liquidity scenario analysis be a regular part of a CCP's stress-testing program to help ensure that appropriate liquidity planning does not suffer from a lack of vision or imagination.

Transparency

Enhanced transparency is central to the reform agenda, and there has been some progress in this area. But CCPs need to provide still greater transparency to their clearing members and to the public. The G-20's central clearing mandate shifted a significant amount of activity and control away from dealers to CCPs. With this shift, CCPs took on the responsibility of managing risks in a way that is transparent to the clearing members who are subject to the decisions of the CCP. Clearing members need a full and detailed understanding of their risk exposure to CCPs, which means that clearing members must have detailed and appropriate information on stress-test results, the specification and application of margin models, and the sizing of default funds to cover losses. Without a clear picture of a CCP's risk profile, clearing members cannot make informed decisions about whether to clear with a particular CCP or how to judge their exposures to it. All major stakeholders--clearing members, clients, regulators, and the broader market--should be aware of the risks involved so that they can take appropriate steps to mitigate them.

Stress testing

The disclosure of CCP stress-test results to clearing members is important so that clearing members can have a full understanding of a CCP's risk profile. This disclosure, however, would be of little help if the stress tests themselves were insufficiently comprehensive and robust. For example, consider a case in which a bank belongs to two CCPs that clear similar products but the disclosed stress tests for the CCPs are based on materially different scenarios. This state of affairs could easily result in more confusion than clarity.

It is time for domestic and international regulators to consider steps to strengthen credit and liquidity stress testing conducted by CCPs. Currently, most major CCPs engage in some form of stress testing. However, both clearing members and regulators need a more systematic view of what stress tests are performed, at what frequency, with what assumptions, and with what results. Aside from these issues involving individual stress tests, there are also important questions about the comparability of stress scenarios, assumptions, and results across similar and different types of CCPs. A related issue is whether regulators should consider some sort of standardized approach to supervisory stress testing. Not all CCPs are alike. But there may be approaches that could bring some of the benefits of standardization while allowing tailoring of some scenarios to the activities of particular CCPs or groups of CCPs. Clearly, a greater degree of uniformity would be helpful to clearing members that are comparing test results across several CCPs and to regulators that are considering systemwide stability. For example, there are likely some financial market stresses, such as rapid and significant increases in market volatility, that would be expected to have broad effects across financial markets and participants. Coordinated stress tests could also help us better understand the macroprudential risks around liquidity that I discussed earlier. Understanding the effect of such correlated stresses on a wide array of CCPs will be important for ensuring overall system resiliency. Going forward, regulators will need to work collaboratively to ensure that stress tests are robust, informative, and appropriately comparable.

Skin in the game

A number of commentators have urged U.S. authorities to consider requiring CCPs to place significant amounts of their own loss-absorbing resources in front of the mutualized clearing fund or other financial resources provided by clearing members. These skin-in-the-game requirements are intended to create incentives for the owners of CCPs for careful consideration of new products for clearing, for conservative modeling of risks, and for robust default waterfalls and other resources to meet such risks as may materialize.9 The issue is a complex one, however, and a number of factors would need to be considered in formulating such a requirement.

Recovery and resolution

I have focused so far on what we can do to ensure that CCPs do not fail: more transparency, enhanced stress testing, more robust capital and default waterfalls, stronger liquidity, and increased incentives to appropriately manage risks. I will conclude my remarks today by discussing what happens when all of these efforts encounter a severe stress event. Try as we might to prevent the buildup of excessive risk, we need to be prepared for the possibility that a CCP may fail or approach failure in the future. When and if such a crisis materializes, CCPs will be called on to stand on their own. CCPs and regulators need to develop clear and detailed CCP recovery and resolution strategies that are well designed to minimize transmission of the CCP's distress to its clearing members and beyond.

Recovery and resolution planning is a matter of intense focus among regulators and industry participants. Just last month, the Committee on Payments and Market Infrastructures and the Board of the International Organization of Securities Commissions released their final report on the recovery of financial market infrastructures.10 The report is part of an ongoing effort to provide guidance on implementing the PFMI requirements for recovery planning. On the same day, the Financial Stability Board released a new report on the resolution of financial market infrastructures and their participants to supplement its earlier work on the report Key Attributes of Effective Resolution Regimes for Financial Institutions.11

These reports stress that CCPs must adopt plans and tools that will help them recover from financial shocks and continue to provide their critical services without government assistance. It has been a challenge for some market participants to confront the fact that risks and losses, however well managed, do not simply disappear within a CCP but are ultimately allocated in some way to the various stakeholders in the organization--even if the risk of loss is quite remote. This realization has generated a healthy debate among CCPs, members, and members' clients and regulators that has provided fertile ground for new thinking about risk design, risk-management tools, and recovery planning. To ensure that CCPs do not themselves become too-big-to-fail entities, we need transparent, actionable, and effective plans for dealing with financial shocks that do not leave either an explicit or implicit role for the government.

Conclusion: Realizing the Promise of Central Clearing

A key question posed at this conference is whether the reforms instituted in response to the crisis have improved the strength and stability of the financial system. In my view, the answer for OTC derivatives reform--and central clearing, in particular--is a positive one. But final pronouncements are premature. Post-crisis reforms and the rise of central clearing have started us down a path toward greater financial stability. At the same time, central clearing brings with it a number of complexities that relate to the interaction between CCPs and the rest of the financial system, especially the global systemically important financial institutions that represent many of their largest clearing members. Given the increasingly prominent role that central clearing will play in the financial system going forward, it is critical that we collectively get central clearing right. To do so, I have argued that it is imperative that we consider central clearing from a systemwide perspective, and that regulators will need to continue to work collaboratively with each other, both domestically and internationally.

1. The views expressed here are my own and are not necessarily shared by other members of the Federal Reserve Board or the Federal Open Market Committee. Return to text

2. According to the Bank for International Settlements, the notional amount of OTC derivatives outstanding grew from $80.3 trillion in December 1998 to $598.1 trillion in December 2008, which corresponds to an annual growth rate of 22.2 percent per year. For more information, see Bank for International Settlements, "Derivatives Statistics ," webpage. Return to text

3. Financial Stability Board (2014), OTC Derivatives Market Reforms: Seventh Progress Report on Implementation (PDF) (Basel, Switzerland: FSB, April). Return to text

4. See Committee on Payment and Settlement Systems and Technical Committee of the International Organization of Securities Commissions (2012), Principles for Financial Market Infrastructures (PDF) (Basel, Switzerland: Bank for International Settlements and International Organization of Securities Commissions, April). Return to text

5. As an example, both the Chicago Mercantile Exchange and the Intercontinental Exchange clear credit default swaps. Return to text

6. See, for example, Jerome H. Powell (2013), "OTC Market Infrastructure Reform: Opportunities and Challenges," speech delivered at the Clearing House 2013 annual meeting, New York, November 21; and Ben S. Bernanke (2011), "Clearinghouses, Financial Stability, and Financial Reform," speech delivered at the 2011 Financial Markets Conference, a meeting sponsored by the Federal Reserve Bank of Atlanta, held in Stone Mountain, Ga., April 4. Return to text

7. The Federal Reserve Board's authority to supervise systemically important CCPs is provided in title VIII of the Dodd-Frank Act. Return to text

8. In the United States, these standards were implemented by the Commodity Futures Trading Commission for derivative-clearing organizations in November 2013 and by the Federal Reserve for certain financial market utilities that are designated as systemically important by the Financial Stability Oversight Council in October 2014. Return to text

9. See, for example, the related discussion in Committee on Payment and Settlement Systems (2010), Market Structure Developments in the Clearing Industry: Implications for Financial Stability (PDF) (Basel, Switzerland: Bank for International Settlements, November). Return to text

10. See Committee on Payments and Market Infrastructures and Board of the International Organization of Securities Commissions (2014), Recovery of Financial Market Infrastructures (PDF) (Basel, Switzerland: Bank for International Settlements and International Organization of Securities Commissions, October). Return to text

11. See Financial Stability Board (2014), Key Attributes of Effective Resolution Regimes for Financial Institutions (PDF) (Basel, Switzerland: FSB, October). Return to text

{kind=link}

{kind=link}