February 26, 2016

Discussion of the paper "Language after Liftoff: Fed Communication Away from the Zero Lower Bound"

At the 2016 U.S. Monetary Policy Forum, New York, New York

This paper reviews Federal Open Market Committee (FOMC) communications from the time the Committee began issuing regular postmeeting statements in 1999 to the present.1 The authors provide an extended and insightful discussion of the theory and practice of providing forward guidance about monetary policy. They offer one central lesson: Data-based forward guidance is mostly good, while time-based forward guidance is mostly bad.

The authors show that data-based guidance has desirable characteristics and can make monetary policy more effective. When clearly articulated and well understood, it allows markets to react appropriately to incoming data, doing the heavy lifting for the central bank.

Time-based guidance is found to have certain bad characteristics and should be avoided, except at the zero lower bound and when other options are not available or not working. Time-based guidance may reduce the sensitivity of rates to incoming macroeconomic data, suppress volatility, encourage risk-taking and increased leverage, and threaten financial stability. It may also put policymakers in a box when changes in the economy make it optimal to deviate from previously expressed guidance, but the Committee cannot do so without losing credibility.

The authors blame time-based guidance for several episodes in which the Committee zigged when the market looked for it to zag, leaving market participants unhappy and, in the authors' view, the FOMC's credibility damaged. They argue that the Committee has relied too much on time-based guidance in recent years and should use it only parsimoniously in the future.

I commend the authors for undertaking this enormously challenging and useful exercise. The paper forces us to reconsider the Committee's evolving understanding of the macroeconomic environment before, during, and after the Great Recession; its decisions and its communications; and the market's understanding of those decisions, which have sometimes deviated from what the Committee actually said.

The distinction between time-based and data-based guidance is an important one, and the potential problems with time-based guidance are real and well described in the paper. That said, I am not convinced that this distinction has played a central role in determining the successes and challenges of FOMC communications in this remarkable era, or that it helps us improve in the future. The authors are, in their words, "unabashedly judgmental" in labeling specific communications to be either time- or data-based.2 My own judgments differ in significant respects from those described in the paper.

Discussion of Forward Guidance

I will start in December 2008, when the Committee said that "weak economic conditions are likely to warrant exceptionally low levels of the federal funds rate for some time."3 This relatively weak time-based guidance was strengthened in a series of steps until August 2011, when the time-based language became "at least through mid-2013."4 The calendar reference was later extended in a couple of steps to "at least through mid-2015."5 This guidance was explicitly time-based, and the authors seem to agree that, through this point, the guidance served its intended purpose at the zero lower bound by pushing down medium- and longer-term rates.6

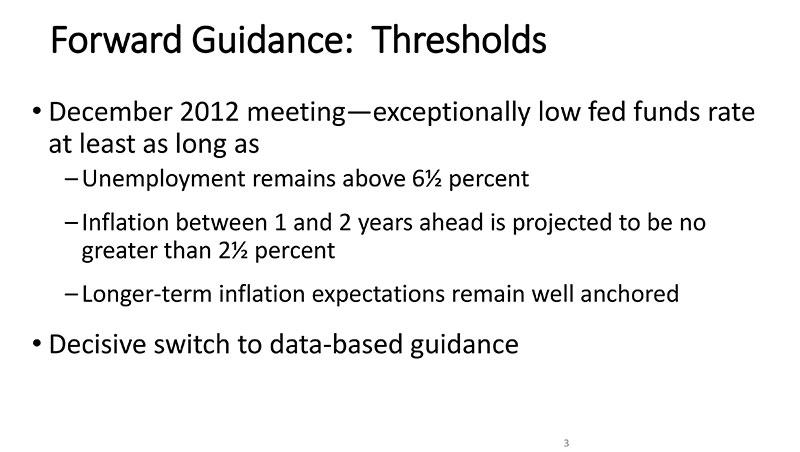

At the December 2012 meeting, the Committee ended this calendar-based guidance. The Committee instead adopted thresholds, saying that it did not intend to raise rates at least as long as unemployment remained above 6-1/2 percent, inflation one to two years ahead was projected to be no higher than 2-1/2 percent, and longer-term inflation expectations remained well anchored.7 The adoption of thresholds was a clear change to data-based guidance, as its principal sponsors had frequently urged.8 The point was not to provide additional stimulus at the time of adoption, but rather to allow market participants to adjust their expectations about future monetary policy in response to incoming data--exactly what the authors advocate.9

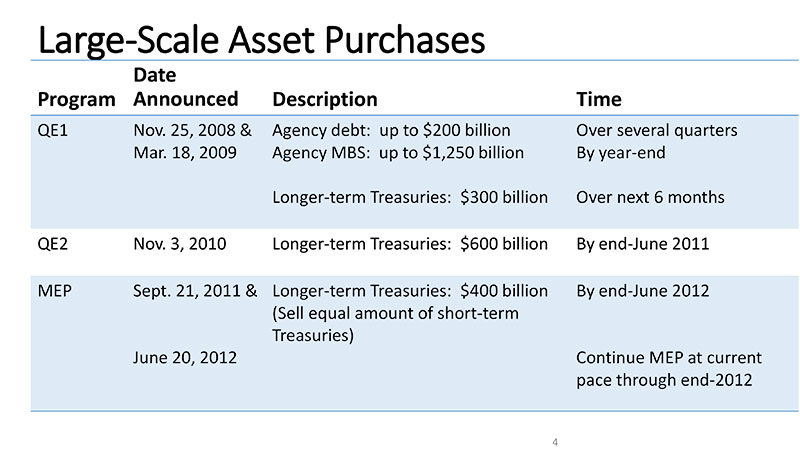

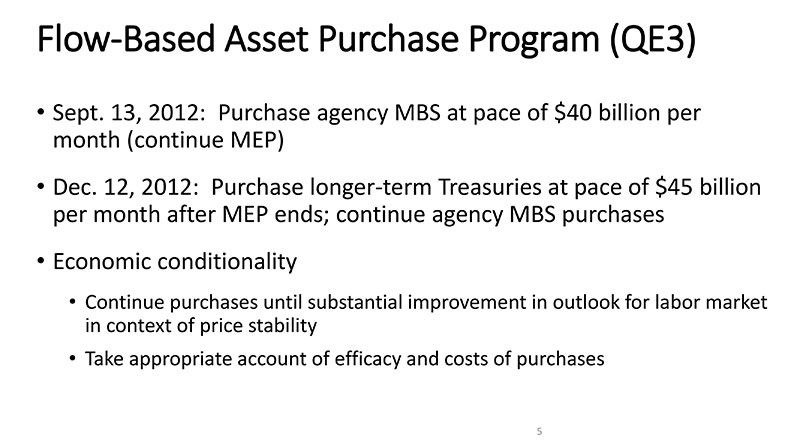

The Committee also used balance sheet policy through most of this period. The first two programs of large-scale asset purchases (LSAPs), popularly known as QE1 and QE2, and the maturity extension program were announced in terms of time and quantity--that is, a certain quantity of assets would be purchased over a certain time. In adopting QE3, by contrast, the Committee committed to continuing purchases until there was a substantial improvement in the outlook for the labor market.10 QE3 was fully data-contingent.

Former Chairman Bernanke recounts in his recent book that he saw QE3 as akin to Mario Draghi's statement that the European Central Bank would do "whatever it takes."11 He also notes that FOMC participants held divergent views on the potential costs and benefits of the program. Minutes of the relevant meetings described the complex discussions and differing views. Contemporaneous reports by Wall Street analysts show frustration and confusion about the Committee's intentions.

When various FOMC communications suggested that the time to begin reducing purchases was nearing, long-term rates rose sharply--the so-called taper tantrum. The contention of this paper is that time-based guidance was responsible. But as the paper acknowledges, the open-ended, data-contingent nature of the QE3 program created a strong sense that the Fed was "all in" and that the purchases might go on for a long time. That powerful commitment "would set things up for some fireworks" when the time came to provide more precise guidance as to the timing of tapering, whether that was done through time- or data-based guidance.12 While Committee communications are subject to fair criticism, I don't see an important role in this narrative for time-based guidance.

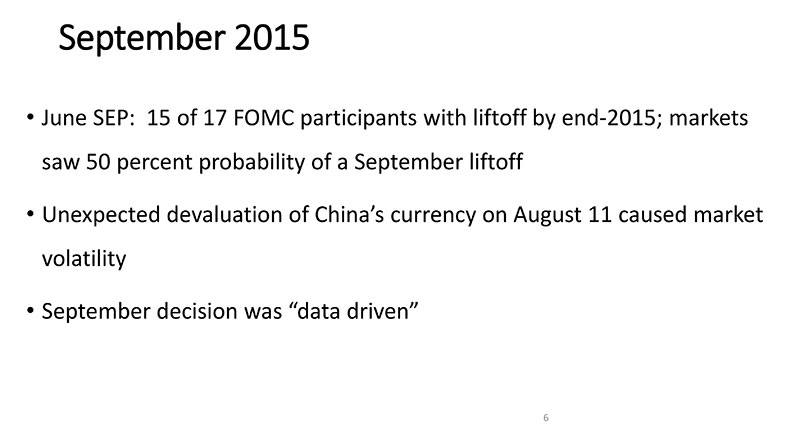

Let's turn briefly to 2015 and the run-up to last December's increase in the federal funds rate--also an important focus of the paper. The authors and many market participants are critical of communication around the September meeting. With the June 2015 Summary of Economic Projections (SEP) showing that 15 of 17 FOMC participants judged that appropriate policy would entail an initial increase in the federal funds rate by the end of 2015, markets saw about a 50 percent chance that the first increase would occur in September. This probability fell to about 30 percent after global markets experienced a sudden bout of volatility following China's surprise devaluation of its currency in August. At the September meeting, the FOMC decided to wait to see how global markets and the economy evolved, noting in its statement that "Recent global economic and financial developments may restrain economic activity somewhat and are likely to put further downward pressure on inflation in the near term."13

A data-driven Committee, making decisions meeting by meeting, is likely to surprise markets from time to time. The authors join many others in criticizing the "measured pace" period of 2004 through 2006, during which the Committee increased rates by 25 basis points at 17 consecutive FOMC meetings. A common criticism has been that this high level of predictability made investors complacent, encouraging a buildup of leverage and helping set the stage for the Global Financial Crisis. That criticism may well overstate the importance of the Committee's communications; nonetheless, a number of FOMC participants have said that the Committee intends to be "data driven" and not fall into an excessively predictable, data-insensitive path. Lower predictability implies more surprises.

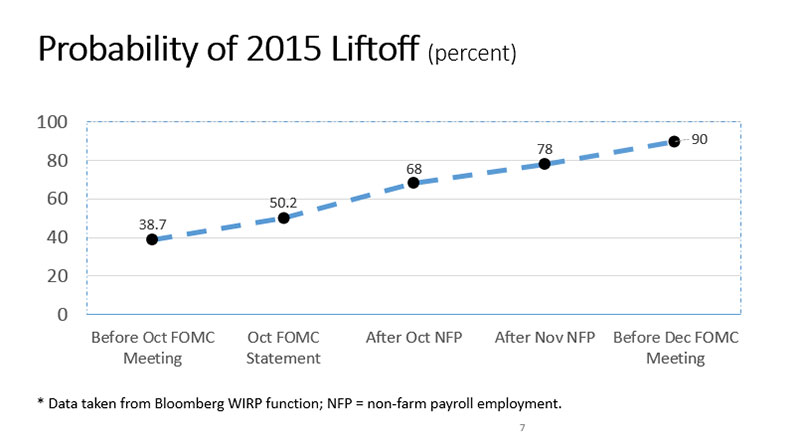

In the statement released after its October 2015 meeting, the Committee reemphasized data dependence and focused on the importance of incoming data for the Committee's decision "at its next meeting," which led the market to increase its estimated probability of a December rate increase from 38 percent to 50 percent.14 The October and November non-farm payroll reports came in strong and above expectations, raising that probability by the time of the December meeting to about 90 percent. In other words, the Committee used modest time-based guidance to set the stage and then let incoming data do the heavy lifting. In the statement released after the FOMC's most recent meeting in January, the Committee said that, in evaluating future adjustments to the target range for the federal funds rate, it would "assess realized and expected economic conditions relative to its objectives of maximum employment and 2 percent inflation."15 This language shows that the Committee has moved away from the time-based guidance of the crisis years.

Although time-based guidance can create communications challenges, I see other factors as having been more important in recent years. In particular, the challenge of deciding when and how to use unconventional tools--and ultimately when and how to reduce that usage--is a great one. The task of communicating clearly about those decisions is equally great. And the reality of the FOMC's size and diversity, not to mention uncertainty about the evolving structure of the economy and the effects of monetary policy actions, means that we are still far from the ideal world of a fully worked out, clearly specified and transparent consensus on what economists call a "reaction function"--a complete description of how policy will respond to changes in economic conditions.

Often when communicating about the path of policy, it will be hard to avoid a combination of the two forms of guidance. For example, the Committee has embraced the view that the equilibrium level of the federal funds rate is currently below its pre-crisis level and expects the funds rate to return only gradually to its longer-run value.16 This view is a key aspect of many Committee participants' reaction functions, including mine. Try saying that without referring to time.

The authors acknowledge that the distinction between rules and discretion is too simple to capture the problems that monetary policymakers face.17 I would say the same of the distinction between time-based and data-based forward guidance.

Lessons Learned and Suggested Improvements

Before turning to the paper's conclusions, I would like to put the Federal Reserve's communications into a broader context. In recent years, the FOMC has adopted many new and significant communications tools. Since the fall of 2007, policymakers have submitted projections in conjunction with four FOMC meetings each year; in 2012, those projections were augmented to include each participant's path for appropriate monetary policy. In 2011, the Chairman began holding quarterly press conferences. In 2012, the Committee first released its statement on Longer-run Goals and Monetary Policy Strategy, which formalized the FOMC's 2 percent inflation objective and is reaffirmed each year at the January meeting. These and other changes have kept the Federal Reserve among the world's most transparent central banks in its communications with the public.

With that as background, I find significant grounds for agreement and further analysis in the paper's concluding section, which lays out lessons learned and suggested improvements. The discussion of what is colloquially known as the "dot plot" included in the SEP is particularly interesting. The dot plot represents each FOMC participant's individual assessment of the path of the federal funds rate over the next three years that is most likely to promote maximum employment and stable prices.18

The dot plot presents a number of challenges. The individual dots are not tied to the individual macroeconomic forecasts presented in the SEP, and no information is provided on the identity of the forecaster--for example, voting members of the Committee are not distinguished from non-voting participants. There is no easy path to the identification of a Committee reaction function. The dots speak as of their date of publication after the FOMC meetings held in March, June, September, and December. Three months pass between SEPs. The economic outlook can change quite significantly, making the reigning dots look out of touch. On occasion, the dot plot and the postmeeting statement have seemed to send conflicting signals. The dot plot reflects individual views of appropriate policy, while the postmeeting statement reflects the consensus of the Committee.

The authors weigh these challenges and ponder whether to eliminate the dot plot; some appear to favor that idea.19 I doubt that most market participants would welcome the elimination of this chart. The SEP provides a number of benefits. It requires FOMC participants to write down their forecasts for inflation, unemployment, and growth, as well as their assessments of appropriate monetary policy. This exercise helps policymakers to be more systematic. In addition, by observing how the SEP changes over time, the public can better understand how Committee members react to changes in the economy. My view is that the dot plot, on balance, is helpful to market participants and hence to the Committee. As the dot plot enters its fifth year of existence, my hope is that we will be able to capture those benefits while avoiding its shortcomings.

I agree with the paper's suggestion of greater emphasis on the degree of uncertainty around the projections, which is much larger than the dispersion of the individual forecasts. As you know, at its January meeting, the Committee discussed adding fan charts to the SEP. Fan charts could help emphasize that the economic outlook is uncertain, and that consequently there is considerable uncertainty around the path of policy.

1. The views expressed here are my own, and not those of the FOMC.

See Michael Feroli, David Greenlaw, Peter Hooper, Frederic Mishkin, and Amir Sufi (2016), "Language after Liftoff: Fed Communication Away from the Zero Lower Bound," paper presented at the 2016 U.S. Monetary Policy Forum, a conference sponsored by the University of Chicago Booth School of Business, held in New York, February 26; see https://research.chicagobooth.edu/igm/events/conferences/2016-usmonetaryforum.aspx. Return to text

2. See Feroli and others, "Language after Liftoff," in note 1, p. 20. Return to text

3. Board of Governors of the Federal Reserve System (2008), "FOMC Statement and Board Approval of Discount Rate Requests of the Federal Reserve Banks of New York, Cleveland, Richmond, Atlanta, Minneapolis, and San Francisco," press release, December 16, paragraph 4. Return to text

4. Board of Governors of the Federal Reserve System (2011), "FOMC Statement," press release, August 9, paragraph 3. Return to text

5. Board of Governors of the Federal Reserve System (2012), "Federal Reserve Issues FOMC Statement," press release, September 13, paragraph 5. Return to text

6. Some viewed this guidance as merely a forecast of Committee action, designed to better inform the market and reduce uncertainty. Others have argued that such guidance is understood as a promise to which the Committee will be held irrespective of future macroeconomic developments. The Committee never offered a single explanation, and participants may have had different views. Engen, Laubach, and Reifschneider (2015) argue that the Federal Reserve's time-based guidance initiated in August 2011 was highly effective in inducing market participants to change their beliefs about the Committee's reaction function and to regard monetary policy as more accommodative. Using Blue Chip survey data, the authors estimate that the perceived weight on resource slack roughly doubled between March 2011 and March 2012. In an August 2011 speech, Chairman Bernanke indicated that the guidance about the federal funds rate path was highly conditional on the outlook, saying, "in what the Committee judges to be the most likely scenarios for resource utilization and inflation in the medium term, the target for the federal funds rate would be held at its current low levels for at least two more years." (Ben S. Bernanke (2011), "The Near- and Longer-Term Prospects for the U.S. Economy," a speech delivered at "Achieving Maximum Long-Run Growth (PDF)," a symposium sponsored by the Federal Reserve Bank of Kansas City, held in Jackson Hole, Wyo., August 26, p. 7.) Return to text

7. Board of Governors of the Federal Reserve System (2012), "Federal Reserve Issues FOMC Statement," press release, December 12, paragraph 5. Return to text

8. For example, see Charles L. Evans (2012), "Macroeconomic Effects of FOMC Forward Guidance," speech delivered at the Spring Panel on Economic Activity, Brookings Institution, Washington, March 22; and Alejandro Justiniano, Charles L. Evans, Jeffrey R. Campbell, and Jonas D.M. Fisher (2012), "Macroeconomic Effects of FOMC Forward Guidance (PDF)," Brookings Papers on Economic Activity, Spring, pp. 1-54. Return to text

9. The thresholds' useful life was fairly short because the unemployment rate fell sharply, from 8.0 percent in December 2012 to 6.2 percent in April 2014, while inflation remained below 2.0 percent. Return to text

10. The December 2012 FOMC statement indicated that, "If the outlook for the labor market does not improve substantially, the Committee will continue its purchases of Treasury and agency mortgage-backed securities, and employ its other policy tools as appropriate, until such improvement is achieved in a context of price stability. In determining the size, pace, and composition of its asset purchases, the Committee will, as always, take appropriate account of the likely efficacy and costs of such purchases." (Board of Governors of the Federal Reserve System (2012), "Federal Reserve Issues FOMC Statement," press release, December 12, paragraph 4.) Return to text

11. Ben S. Bernanke (2015), The Courage to Act: A Memoir of a Crisis and Its Aftermath (New York: W.W. Norton), p. 532. Return to text

12. See Feroli and others, "Language after Liftoff," in note 1, p. 29. Return to text

13. Board of Governors of the Federal Reserve System (2015), "Federal Reserve Issues FOMC Statement," press release, September 17, paragraph 2. Return to text

14. Board of Governors of the Federal Reserve System (2015), "Federal Reserve Issues FOMC Statement," press release, October 28, paragraph 3. Return to text

15. Board of Governors of the Federal Reserve System (2016), "Federal Reserve Issues FOMC Statement," press release, January 27, paragraph 4. Return to text

16. For example, the January 2016 FOMC statement says, "The Committee expects that economic conditions will evolve in a manner that will warrant only gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run." (Board of Governors of the Federal Reserve System (2016), "Federal Reserve Issues FOMC Statement," press release, January 27, paragraph 4.) Return to text

17. Feroli and others, "Language after Liftoff," in note 1, p. 11; and Ben S. Bernanke and Frederic S. Mishkin (1997), "Inflation Targeting: A New Framework for Monetary Policy?" Journal of Economic Perspectives, vol. 11 (Spring), pp. 97-116. Return to text

18. In the SEP collected prior to the March and June FOMC meetings, participants submit projections for the current calendar year and two subsequent years; in the September SEP, the forecast horizon is extended out an additional calendar year. Thus, the forecast window does not remain constant for the different SEPs in a given year; Wrightson commentary has suggested that a rolling forecast horizon might be an improvement over the current calendar-year focus (Wrightson ICAP (2016), "January 26-27 FOMC Minutes Recap," February 18). Return to text

19. For instance, Michael Feroli (as quoted in a recent article) said, "I think they have outlived their usefulness and they risk sending a signal that (Fed officials) have a ‘plan' rather than that they are data dependent" (see Ann Saphir (2016), "Fed's ‘Dot Plot' Looks Increasingly out of Touch on Rates," Markets, Reuters, February 14, paragraph 8, http://in.reuters.com/article/us-usa-fed-path-analysis-idINKCN0VN0PU); and in a 2012 speech, former Governor of the Bank of Canada Mark Carney stated, "Overall research has not generally found that publishing a path leads to better outcomes." (Mark Carney (2012), "Guidance," a speech delivered to the CFA Society Toronto, Toronto, Canada, December 11, paragraph 24, www.bankofcanada.ca/2012/12/guidance. Return to text

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}