March 21, 2014

Incorporating Financial Stability Considerations into a Monetary Policy Framework

Governor Jeremy C. Stein

At the International Research Forum on Monetary Policy, Washington, D.C.

Governor Stein presented identical remarks at the International Monetary Fund 2014 Spring Meetings on April 13, 2014, and at the 2014 Financial Markets Conference on April 16, 2014.

I would like to talk today about how one might explicitly incorporate financial stability considerations into a monetary policy framework.1 Doing so involves tackling two questions--one that is relatively easy and one that is much harder. The easier question is, should financial stability concerns, in principle, influence monetary policy decisions? To be specific, are there cases in which one might tolerate a larger forecast shortfall of the path of the unemployment rate from its full-employment level than one would otherwise, because of a concern that a more accommodative policy might entail a heightened risk of some sort of adverse financial market outcome? This question is about theory, not empirical magnitudes, and, in my view, the theoretical answer is a clear "yes." I will say a bit more about why shortly, but let me stress that I am not breaking any new conceptual ground here; the basic argument has been laid out by a number of others, including Woodford and Kocherlakota.2

The second question is, how does one operationalize the theory? What sorts of data should one look to, and what sorts of empirical methods should one use, to calibrate by how much the stance of monetary policy should be altered relative to the case in which financial stability considerations are completely set aside? This question is very difficult. In the interests of advancing the conversation, I will venture some tentative thoughts on one possible approach, which is somewhat different than what I have seen in other recent work on this topic. While I hope to convince you that this path is worth exploring, I cannot say that I know yet exactly where it will lead--and, in particular, whether it will ultimately deliver monetary policy prescriptions that differ in a quantitatively meaningful way from those offered by our current models. So I do not intend anything that follows as a comment on the current stance of our policy.

Before getting too deep into the details, let me preview my bottom line. I am going to try to make the case that, all else being equal, monetary policy should be less accommodative--by which I mean that it should be willing to tolerate a larger forecast shortfall of the path of the unemployment rate from its full-employment level--when estimates of risk premiums in the bond market are abnormally low. These risk premiums include the term premium on Treasury securities, as well as the expected returns to investors from bearing the credit risk on, for example, corporate bonds and asset-backed securities. As an illustration, consider the period in the spring of 2013 when the 10-year Treasury yield was in the neighborhood of 1.60 percent and estimates of the term premium were around negative 80 basis points.3 Applied to this period, my approach would suggest a lesser willingness to use large-scale asset purchases to push yields down even further, as compared with a scenario in which term premiums were not so low.4

The informal intuition I have in mind is that there is a cost associated with pushing risk premiums too low, because doing so increases the likelihood that they may revert back in a way that hinders the Federal Reserve's ability to achieve its mandated objectives. In what follows, I will try to make this intuition more precise and to generalize its applicability.

Do Financial Stability Considerations Belong in a Monetary Policy Framework?

However, let me start with the conceptual question of whether financial stability considerations belong at all in a monetary policy framework. As I said earlier, I think the clear in-principle answer here is "yes." The generic argument rests on three assumptions. First, suppose that the Federal Reserve focuses only on its traditional dual mandate of maximum employment and price stability. To keep things simple, suppose further that these two goals are not in conflict with one another--say, because aggregate demand is weak, depressing both employment and inflation--so that we can boil things down to one objective: keeping unemployment close to target. With the usual quadratic loss objective function, this assumption would say that the Federal Reserve cares about minimizing the expected value of (U – U*)2. A little bit of algebra shows that this objective function can in turn be decomposed into two pieces: (1) an "expected shortfall" term, given by the squared deviation of expected unemployment from the target level of U*; and (2) a "risk" term, given by the variance of realized unemployment, U.5

Second, the argument assumes that there is some variable summarizing financial market vulnerability--I will be abstract for the moment and just call it FMV--which is influenced by monetary policy. That is, easier monetary policy leads to increased vulnerability as measured by FMV. Moreover, when FMV is elevated, there is a greater probability of an adverse event--some kind of financial market shock--that, if it were to occur, would push up the unemployment rate, all else being equal.6

The third and final assumption is that the risks associated with an elevated value of FMV cannot be fully offset at zero cost with other nonmonetary tools, such as financial regulation. To be clear, this assumption does not imply that regulation is not helpful in reducing financial vulnerabilities--it only says that regulation is not a perfect instrument. These imperfections could stem from regulatory arbitrage; political-economy constraints; or the fact that too much regulation can also impede economic growth, just like overly restrictive monetary policy.7 Thus one way to think of my construct of FMV is that it is a stand-in for the level of financial vulnerabilities that remain after regulation has done the best that it can do, given the existing real-world limitations.

In this setting, even with inflation concerns entirely set aside, monetary policy faces a tradeoff. Consider a situation in which unemployment is above target. A more accommodative policy has the usual benefit of lowering expected unemployment and thus reducing the expected shortfall term in the objective function.If, however, it also raises the conditional variance of the unemployment rate via an elevated-FMV channel--thereby increasing the risk term in the objective function--then there is a cost to be weighed alongside the benefit. And importantly, this is true even when financial stability is not a separate objective in and of itself; as I have framed it, financial stability matters only insofar as it affects the degree of risk around the employment leg of the Federal Reserve's mandate.8

To be sure, absent a concrete measure of FMV, as well as some sense of the responsiveness of FMV to monetary policy, this discussion is all pretty theoretical and non-operational. So I will turn to measurement in a moment. But it is worth noting one useful qualitative observation that emerges just from the logic and from the nature of a quadratic loss function. In making the tradeoff I just described, the marginal benefit of using easier policy to reduce the expected unemployment gap is greater when the gap itself is large--that is, when unemployment is far above target. In this case, even a quite high level of financial vulnerability may not imply a much different stance of monetary policy than would fall out of a more traditional analysis. However, as the unemployment gap shrinks, financial stability risks loom larger in relative terms, so an analysis that takes them on board may lead to more of an adjustment in the stance of policy.

Okay, But How Do You Measure Financial Market Vulnerability?

Financial Sector Leverage

At an abstract level, the framework that I have sketched corresponds closely to that in Woodford's work, although his model is much more fully articulated. When it gets down to implementation, Woodford suggests that the most natural measure of financial market vulnerability is a variable that captures "leverage in the financial sector." In other words, faced with unemployment above target, he would have monetary policy be less accommodative, all else being equal, when financial-sector leverage is high. This recommendation rests on three key premises. First, when financial-sector leverage is high, the probability of a severe crisis in which multiple large intermediaries become insolvent is elevated--that is, we are more likely to have a replay of what happened in 2008 and 2009. Second, easy monetary policy is asserted to increase the incentives for the financial sector to lever up. And, third, focusing on leverage as opposed to asset prices avoids putting the central bank in the position of having to "spot bubbles": Even if it is impossible for the central bank to know when an asset class is overvalued, the risks to the economy associated with overvaluation are presumably greater when intermediaries are highly levered.9

In my view, these are generally sensible arguments, and an approach of the sort that Woodford outlines may well turn out to be fruitful. At the same time, this leverage-centric approach also has some drawbacks, which suggest that there is likely to be value in a parallel exploration of other tracks. For one thing, the effective degree of leverage in the financial system is not easy to measure in a comprehensive fashion. One can certainly look at things like banks' capital ratios, but some of the important action, from a financial stability perspective, is likely to be in subtler forms of leverage that are either outside of the traditional banking sector or more prone to shape shifting. More to the point, recall that, for the purposes of informing monetary policy, one wants to focus on those sources of financial vulnerability that are least effectively dealt with via regulation. And the more reliably a form of leverage can be measured, the better a candidate it is for being handled with a regulatory or supervisory approach. In other words, if we were to see signs that banks' capital ratios were in danger of eroding, we would certainly want to do something, but it is hard for me to imagine that the something should involve monetary policy--the obvious first line of defense in this case would be to turn to our regulatory and supervisory tools.

In response to this critique, one might instead seek to focus the attention of monetary policymakers on broader measures of private-sector leverage that are outside the reach of traditional financial regulation. For example, Borio and Drehmann document that the ratio of credit to the private nonfinancial sector relative to gross domestic product (GDP), once suitably detrended, has substantial predictive power for financial crises, so perhaps it might make sense for monetary policy to condition on this kind of broad credit-to-GDP ratio.10 However, if one goes this route, another measurement challenge arises: How, if at all, does monetary policy influence the evolution of the ratio? Without an answer to this question, it is hard to say how much one would want to alter the stance of policy when, say, the ratio is abnormally high relative to trend. And the measurement problem is likely to be a difficult one, given that the credit-to-GDP ratio is a slow-moving variable: Unlike with asset prices, there is no scope for doing an event-study analysis of the effect of a change in policy on the item of interest.11

Risk Premiums in the Bond Market

Motivated in part by these observations, I would like to spend the rest of this talk exploring an alternative, albeit potentially complementary, approach to the problem. Rather than focusing primarily on some measure of intermediary leverage as an input into the monetary policy framework, my suggestion is to also look at estimates of risk premiums in the bond market. Thus, at a broad thematic level, I am taking a capital-markets-centric view of financial stability, as opposed to a purely intermediary-centric view. This is, of course, not to suggest that shocks to large leveraged intermediaries are not as important--if not more so--as those that play out primarily in capital markets. Rather, the premise is simply that disruptions originating in the capital market can be of consequence in their own right, and that they may be less amenable to being dealt with via financial regulation. In this regard, I am echoing a point made recently by Feroli and others, who have emphasized the fragilities related to bond fund flows.12

Let me start by being clear on terminology: By the "risk premium" on an asset category, I mean the ex ante expected return, based on an objective statistical model, that an investor can anticipate earning on the asset in excess of that on short-term Treasury bills. So I will use the words "risk premium" and "expected return" interchangeably in what follows. And, for the sake of concreteness, I will focus on two of these bond market risk premiums in particular: the so-called term premium, which is the expected excess return on longer-term Treasury bonds relative to short-term bills, and the credit risk premium, which is the expected excess return on bonds with credit risk (for example, corporate bonds, or asset-backed securities) relative to safe Treasury securities.

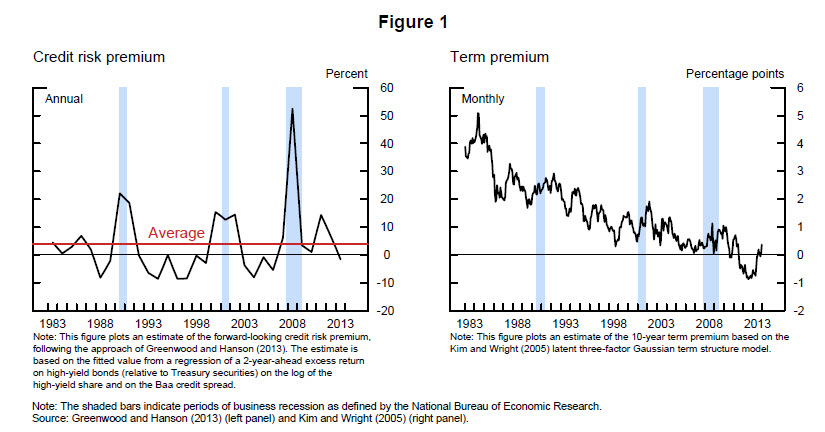

With all of the rhetorical heat that gets generated about whether the Federal Reserve can or should try to spot bubbles, it is worth keeping some uncontroversial facts in mind. It is widely accepted among researchers in finance that there is an economically large amount of predictable variation in the risk premiums on a wide range of assets classes.13 For example, Cochrane and Piazzesi document that the excess returns on longer-term Treasury securities can be predicted one year ahead with a simple model that delivers an R-squared in excess of 40 percent.14 Analogously, Greenwood and Hanson show that the returns on junk bonds relative to Treasury securities over two- to three-year horizons can also be forecast with R-squared values in the ballpark of 30 to 40 percent, in this case by using two intuitively appealing forecasting variables: credit spreads and the high-yield share, which is the fraction of total bond issuance that comes from the high-yield category.15 Figure 1 illustrates the time-series variation in estimates of both of these risk premiums.

{kind=link}

Again, these sorts of findings are largely undisputed. Where there is more controversy is over the interpretation of these patterns, with some arguing that they reflect waves of irrational investor sentiment and others taking the view that they come from more rational factors, such as time variation in either the risks facing investors or their tolerance for bearing such risks. Here is where one can get into hard-to-resolve debates about bubble spotting and about whether one can expect the Federal Reserve to be smarter than other market participants. However, at least for some purposes, these debates are beside the point. In particular, the implications for monetary policy that I have in mind do not seem to depend critically on the difficult question of why there is so much time variation in expected bond market returns; they only require that this variation exists, as we know it does. In other words, there may be scope to make considerable practical progress while remaining largely agnostic about the whole metaphysical are-there-bubbles question.16

Okay. So let's stipulate that risk premiums in the bond market move around a lot. The next observation to throw into the mix is that monetary policy is one of the factors that have an important influence on these movements. An emerging body of empirical work finds that an easing of monetary policy--even via conventional policy tools in normal times--tends to reduce both the term premiums on long-term Treasury securities and the credit spreads on corporate bonds.17 That is, monetary policy always tends to work in part through its effect on capital market risk premiums, perhaps through a risk-taking or reaching-for-yield mechanism.18

However, while this empirical observation sheds some interesting light on how monetary policy influences the real economy, it does not by itself suggest that there is any financial stability dark side--that is, any meaningful increase in what I have been calling FMV--to the lowered risk premiums that go with monetary accommodation. For there to be such a dark side, there would have to be some sort of asymmetry in the unwinding of the effects of monetary policy on these risk premiums, whereby the eventual reversal either happens more abruptly, or causes larger economic effects, than the initial compression.

Let's take an example. Suppose that initially, the credit risk premium on high-yield bonds is 400 basis points, and that, because the unemployment rate is well above target, the Federal Reserve wants to add monetary accommodation. Suppose further that doing so lowers the credit risk premium to 200 basis points temporarily but also increases the odds that this risk premium will, at some point in the next couple of years, revert sharply, moving back in the direction of 400 basis points. What is the downside here? Given a desire for accommodation, is it not better to have credit risk premiums pushed down to a lower on-average level, even if that potentially involves a more volatile down-then-up path? Again, the answer depends critically on whether there is some kind of asymmetry, whereby the eventual increase in spreads either is more abrupt, or has a larger effect on the real economy, than the initial compression.

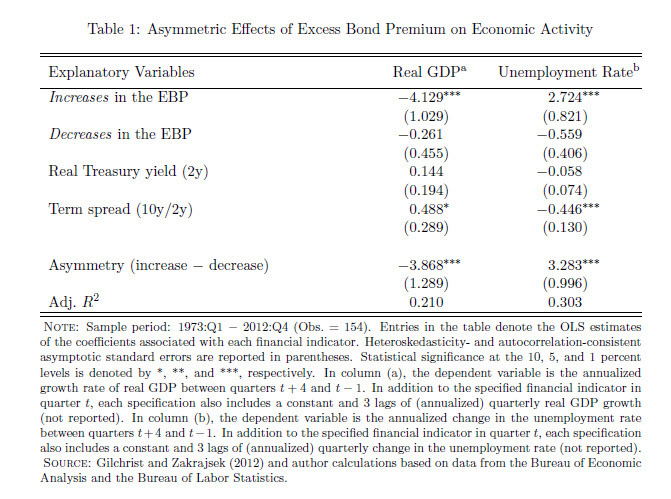

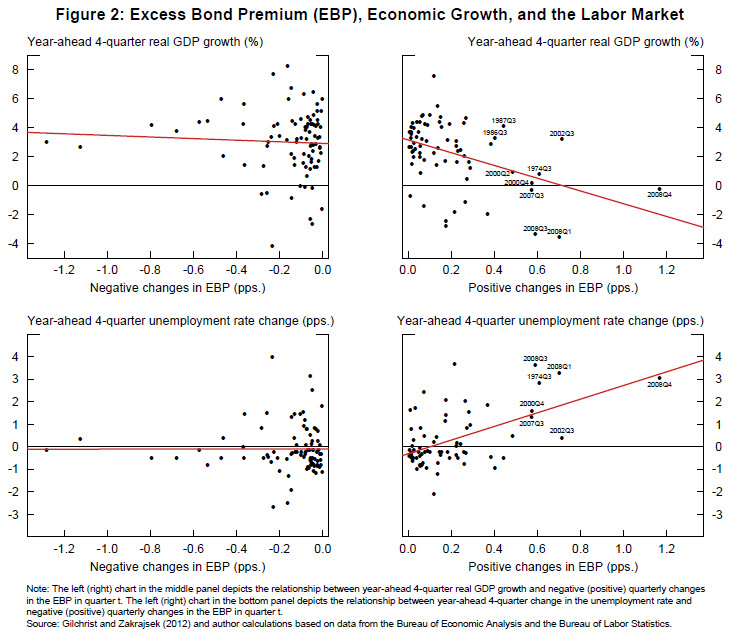

In table 1 and figure 2, I present some new evidence that bears on this asymmetry. To do so, I build directly on recent work by Gilchrist and Zakrajsek (hereafter, GZ).19 GZ show that changes in credit risk premiums have substantial predictive power for measures of economic activity like GDP and unemployment. More specifically, GZ construct a variable called the excess bond premium (EBP). The EBP at any point in time is, roughly speaking, a measure of marketwide credit spreads minus an estimate of the expected default losses on bonds. Hence, it can be thought of as a proxy for the excess return that bondholders can expect to earn, net of defaults, on a going-forward basis--very much in the spirit of the risk premium concept to which I have been referring. Not surprisingly, the EBP exhibits considerable time-series variation, reaching a peak in the wake of the Lehman Brothers bankruptcy. Moreover, in simple forecasting regressions, changes in the EBP are associated with significant movements in GDP and unemployment one year later. In other words, an increase in the EBP--that is, a widening of the non-default-related component of credit spreads--portends a decline in economic activity and employment a year later.

{kind=link}

{kind=link}

The specifications of GZ are linear, so they impose the assumption that increases in the EBP have an effect that is symmetric to decreases. In table 1 and figure 2, I look explicitly for asymmetries, with a specification that allows an upward move in the EBP to have a different effect on the economy than a downward move. The results, which come from a sample spanning the period from January 1973 to December 2012, are striking. Upward moves in EBP--again, those corresponding to a widening of credit spreads--are very informative about the future evolution of the real economy. The coefficient estimates imply that an increase of 50 basis points in the EBP in a single quarter, which is roughly a once-every-five-years kind of move, is associated with a two percentage point slowing of GDP growth over the next four quarters and slightly more than a one percentage point increase in the unemployment rate over the same interval.20 These effects are, by any standard, economically important. By contrast, declines in the EBP have no discernible effect at all on economic activity.

Putting it all together, this reasoning suggests that the credit risk premium--as measured, say, by a forecasting model like that of Greenwood and Hanson--may be an operationally useful measure of financial market vulnerability. When this risk premium is low, there is a greater probability of a subsequent upward spike in credit spreads and the EBP. Moreover, such upward spikes, when they do occur, are associated with significant adverse economic effects. To be clear, we are not necessarily talking about once-in-a-generation financial crises here, with major financial institutions teetering on the brink of failure. Nevertheless, the evidence suggests that even more modest capital market disruptions may have consequences that are large enough to warrant consideration when formulating monetary policy. If so, the indicated directional adjustment would be to be less aggressive in providing monetary accommodation in the face of above-target unemployment, all else being equal, when risk premiums are abnormally low.

Of course, there are many caveats. Foremost among them is the fact that the ability of increases in the EBP to predict future economic activity may not reflect a causal link from the former to the latter. Perhaps there are economic slowdowns that are caused entirely by nonfinancial factors, and, when investors see one on the horizon, they get skittish, causing the EBP to rise. If so, it would be wrong to conclude that easy monetary policy--even if it does, in fact, cause lower risk premiums--has any causal effect on the probability of a future slowdown. So at this point, the evidence that I have reviewed can only be thought of as suggestive.

Making progress on these difficult issues of causality will likely require a clearer articulation of the underlying mechanism that leads to such pronounced asymmetries in the relationship between credit spreads and economic activity. If a causal link is, indeed, present, what is there about it that leads increases in spreads to have a much stronger effect on the economy than decreases? I suspect that the answer has to do with something that mimics the effect of leveraged losses to financial intermediaries--and the attendant effect on credit supply. For example, GZ document that their EBP measure is closely correlated with the credit default swap spreads of broker-dealer firms. The reason could be that losses on their inventories of risky bonds erode the capital positions of these firms, which might in turn compromise their ability to provide valuable intermediation services. Alternatively, a similar mechanism may play out with open-end bond funds, whereby losses cause large outflows of assets under management, again compromising the intermediation function and aggregate credit supply.21

Conclusion

To restate my main point, I believe that measures of bond market risk premiums--for example, estimates of the expected excess returns on long-term Treasury securities relative to Treasury bills and on credit-risky bonds relative to Treasury securities--may turn out to be useful inputs into the monetary policy framework. These variables have the potential to serve as simple proxies for a particular sort of financial market vulnerability that may not be easily addressed by supervision and regulation. Again, however, let me emphasize the conjectural nature of these remarks. Even if this broad way of thinking about the problem turns out to be useful, there is a ways to go--in terms of modeling and calibration--before it can be used to make quantitative statements. Thus, at this early stage, I would not want to claim that one is likely to get policy prescriptions that differ significantly from those of our standard models. We will have to do the work and see what emerges.

Finally, a more general theme that has been lurking in the background here is the sharp difference in perspective that subfields of economics sometimes bring to a given question. As I noted earlier, one of the central and most widely shared ideas in the academic finance literature is the importance of time variation in the risk premiums (or expected returns) on a wide range of assets. At the same time, canonical macro models in the New Keynesian genre of the sort that are often used to inform monetary policy tend to exhibit little or no meaningful risk premium variation.22 Even if most of the specifics of what I have had to say in this talk turn out to be off base, I have to believe that our macro models will ultimately be more useful as a guide to policy if they build on a more empirically realistic foundation with respect to the behavior of interest rates and credit spreads.

References

Bassett, William F., Mary Beth Chosak, John C. Driscoll, and Egon Zakrajsek (2014). "Changes in Bank Lending Standards and the Macroeconomy," Journal of Monetary Economics, vol. 62 (March), pp. 23-40.

Bernanke, Ben S., and Mark L. Gertler (1989). "Agency Costs, Net Worth, and Business Fluctuations," American Economic Review, vol. 79 (March), pp. 14-31.

Borio, Claudio, and Mathias Drehmann (2009). "Assessing the Risk of Banking Crises--Revisited," BIS Quarterly Review, March, pp. 29-46.

Cochrane, John H. (2011). "Presidential Address: Discount Rates," Journal of Finance, vol. 66 (August), pp. 1047-1108.

Cochrane, John H., and Monika Piazzesi (2005). "Bond Risk Premia," American Economic Review, vol. 95 (March), pp. 138-60.

Edge, Rochelle M., and Ralf R. Meisenzahl (2011). "The Unreliability of Credit-to-GDP Ratio Gaps in Real Time: Implications for Countercyclical Capital Buffers," International Journal of Central Banking, vol. 7 (December), pp. 261-98.

Feroli, Michael, Anil K. Kashyap, Kermit Schoenholtz, and Hyun Song Shin (2014). "Market Tantrums and Monetary Policy," paper presented at the 2014 U.S. Monetary Policy Forum, a conference sponsored by the Initiative on Global Markets at the University of Chicago Booth School of Business, held in New York, February 28.

Gertler, Mark, and Peter Karadi (2013). "Monetary Policy Surprises, Credit Costs, and Economic Activity (PDF)," working paper, October.

Gilchrist, Simon, David Lopez-Salido, and Egon Zakrajsek (2014). "Monetary Policy and Real Borrowing Costs at the Zero Lower Bound," Finance and Economics Discussion Series 2014-03. Washington: Board of Governors of the Federal Reserve System, December 2013.

Gilchrist, Simon, and Egon Zakrajsek (2012). "Credit Spreads and Business Cycle Fluctuations," American Economic Review, vol. 102 (June), pp. 1692-1720.

Greenwood, Robin, and Samuel G. Hanson (2013). "Issuer Quality and Corporate Bond Returns," Review of Financial Studies, vol. 26 (June), pp. 1483-1525.

Hanson, Samuel G., and Jeremy C. Stein (2012). "Monetary Policy and Long-Term Real Rates," Finance and Economics Discussion Series 2012-46. Washington: Board of Governors of the Federal Reserve System, July.

Kim, Don H., and Jonathan H. Wright (2005). "An Arbitrage-Free Three-Factor Term Structure Model and the Recent Behavior of Long-Term Yields and Distant-Horizon Forward Rates," Finance and Economics Discussion Series 2005-33. Washington: Board of Governors of the Federal Reserve System, August.

Kocherlakota, Narayana (2013). "Low Real Interest Rates," speech delivered at the 22nd Annual Hyman P. Minsky Conference, Levy Economics Institute of Bard College, Annandale-on-Hudson, N.Y., April 18.

------ (2014). "Discussion of 2014 USMPF Monetary Policy Report," speech delivered at the U.S. Monetary Policy Forum, a conference sponsored by the Initiative on Global Markets at the University of Chicago Booth School of Business, held in New York, February 28.

Stein, Jeremy C. (2013). "Overheating in Credit Markets: Origins, Measurement, and Policy Responses," speech delivered at "Restoring Household Financial Stability after the Great Recession: Why Household Balance Sheets Matter," a symposium sponsored by the Federal Reserve Bank of St. Louis, February 7.

Tarullo, Daniel K. (2014). "Monetary Policy and Financial Stability," speech delivered at the 30th Annual National Association for Business Economics Economic Policy Conference, Arlington, Va., February 25.

Woodford, Michael (2012). "Inflation Targeting and Financial Stability," NBER Working Paper Series 17967. Cambridge, Mass.: National Bureau of Economic Research, April.

1. The views expressed here are my own and are not necessarily shared by other members of the Federal Reserve Board and the Federal Open Market Committee. I am grateful to David Lopez-Salido and Egon Zakrajsek for a number of helpful conversations and for carrying out the empirical work reported here. Thanks also to William English and Jon Faust for their comments. Return to text

2. See Woodford (2012) and Kocherlakota (2013, 2014). Return to text

3. The 10-year nominal rate hit 1.63 percent on May 2, 2013. An estimate of the term premium based on the oft-cited methodology of Kim and Wright (2005) was negative 0.78 percent on this day. Return to text

4. Again, I stress that this statement is directional, not quantitative--I am not claiming that the magnitude of the adjustment one would want to make is large, or that the policy we had in place at the time was miscalibrated in any absolute sense. Rather, my point is just that the financial stability costs of asset purchases are likely to loom larger when term premiums are more negative, and that this consideration belongs in the discussion. Return to text

5. Kocherlakota (2014) emphasizes the same decomposition of the Federal Reserve's loss function. Note that, in focusing only on mean and variance, this functional form sets aside what may be another important aspect of vulnerabilities: tail risks that are not well captured in variance as opposed to higher moments. Return to text

6. If I had introduced an explicit time dimension, it might be more natural to assume that easier monetary policy today raises the probability of an adverse event at some medium-run future date, even while reducing the probability in the short run. In this case, there might be an interesting set of intertemporal tradeoffs to be considered, particularly if the economy were in a very vulnerable position today. In any event, these are just assumptions at this point, meant to illustrate the logic of the argument. Return to text

7. See, for example, Stein (2013) for an elaboration of these points. Return to text

8. See Tarullo (2014) for a similar observation. Return to text

9. Woodford (2012) writes, "It is important, I believe, to realize that the real issue is not identifying whether one type of asset or another is currently overvalued. Instead, what central banks (and potentially other ‘macro-prudential' regulators) need to be able to monitor is the degree to which the positions taken by leveraged institutions pose a risk to financial stability. . . . A central bank need not be able to identify asset over-valuations in order to recognize situations in which the probability of simultaneous financial distress at several institutions is non-trivial." Return to text

10. See Borio and Drehmann (2009). But here, too, one might argue that macroprudential tools that reach beyond the banking sector to target broad measures of household leverage might be more direct, if such tools were available. An example would be limits on the loan-to-value ratios of all mortgage loans, irrespective of whether they reside on bank balance sheets. Return to text

11. A further difficulty lies in the real-time estimation of the underlying trend in the credit-to-GDP ratio and, hence, in the gap relative to trend. See Edge and Meisenzahl (2011). Return to text

12. See Feroli and others (2014). Return to text

13. See Cochrane (2011) for a recent survey of what is by now an enormous literature. Return to text

14. See Cochrane and Piazzesi (2005). Return to text

15. See Greenwood and Hanson (2013). Return to text

16. This statement admittedly sweeps some important subtleties under the rug. More precisely, I suspect that, if one takes the Federal Reserve's legal mandate as given--and, more specifically, takes as given an objective function such as minimizing the expected value of (U – U*)2--then one can remain agnostic about the source of variation in risk premiums and still reach the kinds of conclusions that I do in what follows. However, if one asks whether such a mandate is itself normatively optimal in a fully micro-founded model, my intuition is that the source of variation may matter quite a bit. For example, I would conjecture that it might be more normatively appropriate, holding fixed the consequences for aggregate activity and unemployment, to lean against a sharp reduction in risk premiums that is driven by investor sentiment rather than against one that is driven by a rational response to changes in the risk environment. Return to text

17. See, for example, Hanson and Stein (2012); Gertler and Karadi (2013); and Gilchrist, Lopez-Salido, and Zakrajsek (2014). Return to text

18. Note that, as an econometric matter, it is easier to establish a causal effect of monetary policy on risk premiums than on broad measures of leverage, because asset prices can be measured on a daily or even intraday basis. So they can be directly related to innovations in the stance of policy, as proxied for by, for example, movements in short-term rates in the wake of an announcement by the Federal Open Market Committee. A similar identification strategy is not available for linking monetary policy changes to movements in, say, nonfinancial-sector leverage, given that the latter is measured infrequently. Return to text

19. See Gilchrist and Zakrajsek (2012). Return to text

20. To be a bit more precise, in the 40-year sample period, there are seven observations in which the EBP increases by more than 50 basis points in a single quarter. Return to text

21. Basset and others (2014) document that changes in the EBP are associated with significant changes in bank lending standards, which suggests a broader pullback in the credit intermediation process. Return to text

22. This is true even of those models that--following in the tradition of Bernanke and Gertler (1989)--incorporate some form of financial market friction. Typically, the friction is modeled as something that effectively changes the expected cash flows associated with financial intermediation, but not the net-of-default risk premium earned by investors. Return to text