March 27, 2014

Regulating Large Foreign Banking Organizations

Governor Daniel K. Tarullo

At the Harvard Law School Symposium on Building the Financial System of the Twenty-first Century: An Agenda for Europe and the United States, Armonk, New York

The financial crisis exposed, in painful and dramatic fashion, the shortcomings of existing regulatory and supervisory regimes. In both the United States and the European Union (EU), the crisis also revealed some particular vulnerabilities created by foreign banking operations. This evening I would like to focus on these vulnerabilities and on how best we should address them.

Let me note at the outset the now commonplace observation that we have a quite integrated international financial system, with many large, globally active firms operating within a system of national government and regulation or, in the case of the EU, a hybrid of regional and national regulation. I add the equally commonplace observation that there is no realistic prospect for having a global banking regulator and, consequently, the responsibility and authority for financial stability will continue to rest with national or regional authorities.1 The question, then, is how responsibility for oversight of these large firms can be most effectively shared among regulators. This, of course, is the important issue underlying the perennial challenge of home-host supervisory relations.

Another introductory observation is that--at least in a world of nations with substantially different economic circumstances, different currencies, and banking and capital markets of quite different levels of depth and development--there will be good reason to vary at least some forms of regulation across countries. Presumptively, at least, nations should be able to adjust their regulatory systems based on local circumstances and their relative level of risk aversion as it pertains to the potential for financial instability. Although the financial systems and economies of the United States and the EU are more similar to one another than they are to those of many other jurisdictions, they are hardly identical. Even between these two, for example, there may be legitimate differences within the broader convergence around minimum regulatory and supervisory standards developed at the Basel Committee, the International Organization of Securities Commissions, the Financial Stability Board, and other forums.

These opening observations are important in responding to the curious charge of "Balkanization" that has been levelled at the United States and, to a lesser extent, some other jurisdictions, as a result of actions taken or proposed in response to problems presented by foreign banks during the crisis. I say "curious" for several reasons. One is that the charge reflects a misunderstanding of the allocation of responsibility between home and host supervisors that has evolved in the Basel Committee during the past several decades. Another is that the charge seems implicitly, and oddly, premised on the notion that what we had in 2007 was a well-functioning, integrated global financial system with effective consolidated supervision of global banks. A third is that the charge overlooks the fact that much of what the United States is now doing is matching what the EU has quite sensibly been doing for years.

In the rest of my remarks I will elaborate on these points, though not in the spirit of a debater's arguments, but in an effort to answer the question I posed a moment ago: How, that is, can we successfully reduce the risks to financial stability posed by large, internationally active banks? As I hope will become apparent, a theme I wish to emphasize is that we need to redouble efforts at genuine supervisory cooperation if we are to manage effectively the vulnerabilities and challenges posed by the perennial home-host issue.

International Principles on Home- and Host-Country Responsibilities

While the circumstances and risks may have changed, the issue of the appropriate roles of home and host countries is not a new one. Indeed, it was a key motivation for creation of the Basel Committee in 1975 following the failures of the Herstatt and Franklin National banks. Many of the Basel Committee's early activities were focused on the challenges created by gaps in the supervision of internationally active banks, as evidenced by the fact that Basel "Concordats" on supervision preceded Basel "Accords" and "Frameworks" on capital and other subjects. This task has, of necessity, been ongoing, as experience revealed gaps in supervisory coverage and as the scale and scope of internationally active banks grew. The principle of consolidated supervision emerged in the early 1980s to ensure that some specific banking authority--generally the home-country regulator--had a complete view of the assets and liabilities of the bank.2 This principle was reinforced and elaborated following the Bank of Credit and Commerce International episode in the early 1990s.3

It is important to note that each Basel Committee declaration on the importance of home-country consolidated oversight has also included a statement of the obligations and prerogatives of host states in which significant foreign bank operations are located. This feature of the Basel Committee's approach makes sense as a reflection both of the host authority's responsibility for stability of its financial system and of the practical point that a host authority will be more familiar with the characteristics and risks in its market. In accordance with this history, the current version of the "Core Principles for Effective Banking Supervision" sets out as one of its "essential criteria" for home-host relationships that "[t]he host supervisor's national laws or regulations require that the cross-border operations of foreign banks are subject to prudential, inspection and regulatory reporting requirements similar to those for domestic banks."4

It is clear, then, that consolidated supervision is not intended to displace host-country supervision. Instead, as the Basel Committee has regularly noted, the two are intended to be complementary, so as to assure effective oversight of large, internationally active banks. Similarly, the stated purpose of the Basel Committee in requiring consolidated capital requirements is not to remove from host countries any responsibility or discretion to apply regulatory capital requirements, but to "preserve the integrity of capital in banks with subsidiaries by eliminating double gearing."5 Likewise, and contrary to suggestions that are sometimes made, the capital accords and frameworks developed by the Basel Committee have always been explicitly minimum requirements. They are floors, not ceilings.

Finally, it is worth noting that, in establishing a post-crisis framework for domestic systemically important banks (D-SIBs), the Basel Committee made clear that a host country may in appropriate circumstances designate domestic operations of a foreign bank as systemically important for that country, even if the parent foreign bank has already been designated a global systemically important bank (G-SIB).6 The idea informing the newly created concept of a D-SIB is that an entity whose stress or failure could destabilize a domestic financial system might thereby indirectly destabilize the international financial system. Thus, the D-SIB category carries along with it higher loss-absorbency requirements than are generally applicable to domestic banks, although perhaps not as high as requirements for G-SIBs. Of course, our regulation for foreign banking organizations (FBOs) does not entail D-SIB designation or require higher than generally applicable loss absorbency. But I cite this feature of the D-SIB framework that permits designation of the domestic operations of foreign G-SIBs because it reflects rather clearly the principle that the specific characteristics of domestic markets may call for regulation of foreign banks in the host country, not just at a consolidated level.

In short, the work of the Basel Committee over the years has not been directed at restraining host-country authorities from supervising and regulating foreign banking operations in their country. On the contrary, the committee has repeatedly asserted the complementary responsibilities of both home and host countries to oversee large, internationally active banking groups, in the interests of both national and international financial stability. And the committee has frequently returned to this set of issues in responding to developments that pose a threat to the safety and soundness of the international financial system.

The Shift in Foreign Bank Activities

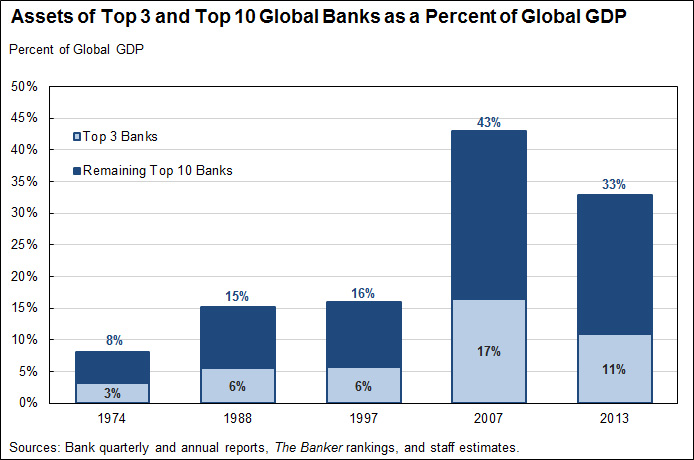

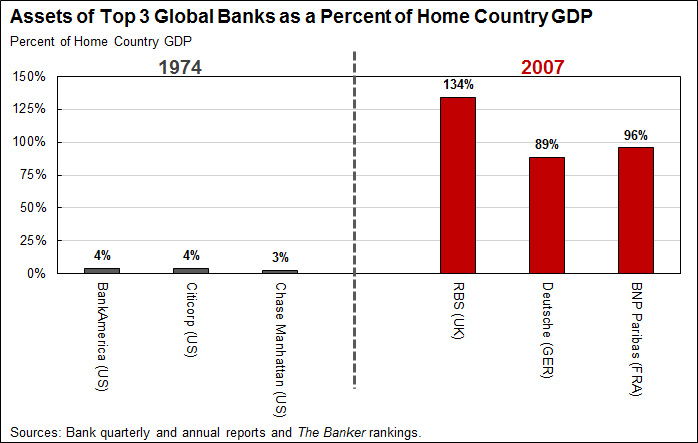

Unfortunately, neither the Basel Committee nor national regulators responded in a timely fashion to the magnitude of the expansion in scale and scope of the world's largest banking organizations in the roughly 15 years before the financial crisis. As illustrated in figure 1, at the end of 1974, just before the Basel Committee was created, the assets of the world's 10 largest banking organizations together equaled about 8 percent of global GDP. The three largest were all American--BankAmerica, Citicorp, and Chase Manhattan. But their combined assets were equal to less than 3-1/2 percent of world GDP and, as illustrated in figure 2, about 10 percent of the GDP of their home country, the United States. By 1988 the combined assets of the world's 10 largest banking organizations as a proportion of world GDP had nearly doubled to about 15 percent, a ratio that held constant during the succeeding decade, at the beginning of the emerging market financial crisis in 1997.

{kind=link}

{kind=link}

Then the explosive growth began. In the next decade--that is, up to the onset of the financial crisis in 2007--the combined assets of the world's 10 largest banks as a share of global GDP nearly tripled, to about 43 percent. The largest bank in the world at that time, Royal Bank of Scotland (RBS), had assets equivalent to about 6.8 percent of global GDP, nearly twice the comparable figure for the three largest banks combined in 1974. Adding the assets of Deutsche Bank and BNP Paribas--the second and third largest banks in 2007--to those of RBS, the three had combined assets equal to about 17 percent of global GDP. And each of the three had assets nearly equal to, or in one instance substantially more than, the GDP of its home country. Even the eighth-ranked bank, UBS, had assets well over four times the GDP of its home country, Switzerland.

Not only did the size of the largest banks change dramatically, so, too, did their scope, reflecting the overall integration of capital market and traditional lending activities that accelerated in the decade and a half preceding the crisis. This trend was particularly apparent in the United States and the United Kingdom, homes to the world's two largest financial centers. In the United States, the proportion of foreign banking assets to total U.S. banking assets has remained constant at approximately one-fifth since the late 1990s. But the concentration and character of those assets have changed noticeably. Today there are as many foreign as U.S.-owned banks with at least $50 billion in U.S. assets, the threshold established by the Dodd-Frank Wall Street Reform and Consumer Protection Act for banks for which more stringent prudential measures must be established.7 Perhaps even more important was the shift in composition of foreign bank assets in the 15 years before the crisis, with the proportion of assets held in the U.S. broker-dealers of the 10 largest FBOs rising from approximately 15 percent to roughly 50 percent.8 Today, 4 of the top 10 broker-dealers in the United States, and 12 of the top 20, are owned by foreign banks.

Meanwhile, even the traditional branching model of large foreign commercial banks in the United States had changed. Reliance on less stable, short-term wholesale funding increased significantly. Many foreign banks shifted from the "lending branch" model to a "funding branch" model, in which U.S. branches of foreign banks were borrowing large amounts of U.S. dollars to upstream to their parents. These "funding branches" went from holding 40 percent of foreign bank branch assets in the mid-1990s to holding 75 percent of foreign bank branch assets by 2009. Foreign banks as a group moved from a position of receiving funding from their parents on a net basis in 1999 to providing significant funding to non-U.S. affiliates by the mid-2000s--more than $600 billion on a net basis by 2008.9

A good bit of this short-term funding was used to finance long-term, U.S. dollar-denominated project and trade finance around the world. There is also evidence that a significant portion of the dollars raised by European banks in the pre-crisis period ultimately returned to the United States in the form of investments in U.S. securities. Indeed, the amount of U.S. dollar-denominated asset-backed securities and other securities held by Europeans increased significantly between 2003 and 2007, much of it financed by the short-term, dollar-denominated liabilities of European banks.10

Just as regulatory systems did not, in the years preceding the crisis, address vulnerabilities such as reliance on short-term wholesale funding that were created by the integration of capital markets and traditional lending, so they did not respond to the transformation of foreign banking operations. Accordingly, just as home countries of systemically important banks have been playing catch-up on capital, liquidity, and other requirements, so host countries of very large foreign banking operations are playing catch-up in dealing with the very different character of many internationally active banks from that of 20 or 30 years ago.

The Regulatory Response

In a sense, the major strengthening during the past few years of capital and liquidity requirements for internationally active banks--including the capital surcharge for banks of global systemic importance--has to date been the most important international regulatory response to the revealed vulnerabilities associated with large foreign banking operations. Building capital and improving the liquidity positions of banks on a consolidated basis is surely a key step toward assuring the stability of major FBOs in host countries.

Of course, these agreed changes have not yet been fully implemented. It is critical not just that all jurisdictions adopt appropriate regulations that fully incorporate the new Basel standards, but also that we ensure our banks will be substantively, and not just formally, compliant as the various transition target dates are reached. It is also the case that there is more to be done in addressing the risks posed by large global banking organizations, including additional measures to deal with the run risks associated with short-term wholesale funding and ensuring that even the largest firms can be successfully resolved without either creating major systemic problems or requiring an infusion of public capital. I will return to these subjects a bit later, in discussing the cooperative agenda that lies ahead for the United States, Europe, and our partners throughout the world.

First, though, I want to describe how Europe, the United Kingdom, and the United States are dealing with the vulnerabilities associated with large foreign banking operations, and thus are fulfilling their responsibilities as host-country supervisors. I discuss the United Kingdom separately from the EU both because it is outside the euro zone and because, as a host jurisdiction, it is more similar to the United States than to other EU member states or, indeed, to any other country in the world.

The EU has not, since the crisis, specifically adjusted the structure of regulation of foreign banks by its member states in their role as host supervisors. For more than a decade before the crisis, EU member states had prudently required that not only commercial banking, but also investment banking subsidiaries of foreign (non-EU-based) banking organizations, be subject to Basel capital requirements in the same way as EU-based firms. With the adoption of CRD IV,11 the directive implementing the new EU capital requirements, Basel III will now be applied to all EU firms, including EU bank and investment bank subsidiaries of non-EU banking organizations. Branches of non-EU banks are generally not subject to local requirements.

Before the crisis and the subsequent development of Basel III, there was no leverage ratio requirement in EU capital directives. Insofar as a new leverage ratio is part of the Basel III package agreed upon internationally, one would anticipate that it will be applied to commercial banking and investment banking firms in the EU, again including local subsidiaries of non-EU firms. Likewise, one would anticipate that the Basel III liquidity requirements will be implemented in the EU in accordance with the internationally agreed timeline and, again, that it will apply to EU subsidiaries of FBOs.

A greater challenge for the EU has been dealing with banks headquartered in one EU country but doing business in other EU countries under the "single passport," which basically allows for full access in the rest of the EU, with supervision provided only by the home country. During the crisis, there were some notable instances of banking stresses and failures involving such institutions, with consequent negative effects on depositors, counterparties, and economies in other parts of the EU. Much of the ongoing post-crisis reform agenda in Europe seems directed at ensuring the safety and soundness of EU-based institutions. The most important of these changes may be the assumption by the European Central Bank of supervisory responsibility for larger euro area banks. And, as we saw just last week, work continues on the long process of creating a credible resolution mechanism for those banks.

As a member state of the EU, the United Kingdom of course implements the EU policies I have just described. But that country has applied an additional set of requirements on the local operations of foreign banks, particularly with respect to liquidity. The Prudential Regulation Authority of the Bank of England applies local liquidity requirements to commercial and investment banking subsidiaries of non-U.K. banks, requiring them to hold local buffers as determined by internal stress tests with both 14- and 90-day components. The assumptions on which the stress tests are premised are quite strict. For example, the U.K. subsidiary generally must assume zero inflows from non-U.K. affiliates--even for claims on non-U.K. affiliates with short terms that mature within the stress test period--and 100 percent outflows to non-U.K. affiliates. The requirements generated by the test are subject to a supervisory review and add-on that for some firms has resulted in a significant increase in the buffer requirement. Branches of foreign commercial banks may in some circumstances be subject to local liquidity requirements as well.

The U.K. initiative in applying local liquidity requirements is wholly understandable in light of the difficulties encountered because of stress on foreign institutions, including the Lehman bankruptcy, during the crisis. Because London is one of the world's two largest financial center hosts, the United Kingdom is the only country other than the United States hosting numerous, very large broker-dealers that are owned by foreign banks and also a broad array of commercial bank subsidiaries and branches that are owned by foreign banks. In fact, the six institutions headquartered outside the United States and the United Kingdom that are in the top three tiers of G-SIBs hold roughly 40 percent of their worldwide assets in those two jurisdictions.12 Thus the U.K. initiative on liquidity and its internal debates on matters such as structural supervision, the Vickers proposals, and stress testing have all been very instructive for the Federal Reserve Board. Even where we have eventually adopted somewhat different approaches, we respect the motivation and scrupulousness of the U.K. banking authorities in addressing the systemic vulnerabilities posed by FBOs and in fulfilling their responsibility to the rest of the world to assure the stability of one of the world's two most important financial centers.

Unlike the EU, the United States did not--prior to the financial crisis--require that all broker-dealers and investment banks meet Basel capital standards. The legacy of the Glass-Steagall Act, which had separated investment banking from commercial banking, meant that only commercial banks were subject to the prudential regulation of the federal banking agencies. In Europe, the dominance of universal banking, or variants thereon, led more naturally to application of capital and other prudential standards to all forms of banking activity. Even after the Gramm-Leach-Bliley Act removed the remaining barriers to affiliation between investment banks and commercial banks in the United States, Basel capital requirements applied at a consolidated level to the activities of an investment bank or broker-dealer only if it did affiliate with a commercial bank. Thus, the five large "free-standing" U.S. investment banks were generally not subject to full application of Basel capital standards.

During the crisis, the ill-advised nature of this regulatory state of affairs became apparent. The decline in value of many mortgage-backed securities and the consequent market uncertainty as to the true value of that entire class of securities raised questions about the solvency of major broker-dealers. Because the dealers were so highly leveraged and dependent on short-term financing, the uncertainty also led to serious liquidity strains, first at Bear Stearns and Lehman Brothers and eventually at most dealers--domestic and foreign owned. Bear Stearns and Merrill Lynch were acquired by existing bank holding companies after coming close to failure. Lehman Brothers went bankrupt. Goldman Sachs and Morgan Stanley became bank holding companies.

Through its Primary Dealer Credit Facility, the Federal Reserve provided substantial liquidity to the broker-dealer affiliates of the bank holding companies, as well as to the primary dealer subsidiaries of foreign banks. At the same time, the shift in strategy of many foreign banks toward using their U.S. branches to raise dollars in short-term markets for lending around the world created another set of vulnerabilities that resulted in substantial and, relative to total assets, disproportionate use of the Federal Reserve's discount window by foreign bank branches.

The experience of the crisis made clear, first, that the perimeter of prudential regulation around U.S. financial institutions needed to be expanded. As noted a moment ago, this had occurred de facto during the crisis. The Dodd-Frank Act has given a legal foundation for this change, first by mandating that Goldman Sachs and Morgan Stanley will remain subject to consolidated prudential regulation even were they to divest their insured depository institutions and, second, by giving the Financial Stability Oversight Council the authority to designate other financial firms as systemically important, a step that would place them under Federal Reserve regulation and supervision. Dodd-Frank further required the Federal Reserve to apply progressively more stringent prudential regulation to bank holding companies with more than $50 billion in assets.

Congress also required the Federal Reserve to apply special prudential standards to large FBOs. As I have already implied, much of what we have done is simply to catch up to EU and U.K. practice. Under our recently finalized Section 165 enhanced prudential standards regulation, an FBO with U.S. non-branch assets of $50 billion or more must hold its U.S. subsidiaries under an intermediate holding company (IHC), which must meet the risk-based and leverage capital standards generally applicable to bank holding companies under U.S. law.13 Such an FBO must also certify that it meets consolidated capital adequacy standards established by its home-country supervisor that are consistent with the Basel Capital Framework. FBOs with combined U.S. assets of $50 billion or more must also meet liquidity risk-management standards and conduct internal liquidity stress tests. The IHC must maintain a liquidity buffer in the United States for a 30-day liquidity stress test. The U.S. branches and agencies of an FBO must maintain a liquidity buffer in the United States equal to the liquidity needs for 14 days, as determined by a 30-day liquidity stress test.14 The IHCs of FBOs must also conform to certain risk-management and supervisory requirements at the IHC level.

Structurally, the U.S. capital requirements for FBOs are similar to those that apply to foreign banks in the EU. That is, generally applicable Basel capital requirements are applied to the U.S. operations of FBOs that own local banking subsidiaries, investment banks, and broker-dealers. In fact, the new U.S. rules are somewhat more favorable to foreign institutions, in that they only apply once the non-branch U.S. assets of an FBO exceed $50 billion. That dollar amount, incidentally, is the same as the Dodd-Frank threshold for more stringent prudential measures, though note that this statutory threshold applies if the total assets of any U.S. banking organization--foreign, as well as domestic--exceed that level. As in the EU, the capital requirements do not apply to U.S. branches of foreign banks, even though the crisis experience provides some credible arguments for doing so.

The leverage ratio requirement has received particular attention. One complaint is that the foreign operations of U.S. banks are not subject to leverage ratios for their local operations. It is true that many foreign countries--including the EU member states--do not currently have leverage ratio standards for their banks. As noted earlier, however, one may reasonably expect that those countries will be implementing the Basel III leverage ratio in a timely fashion. Also, I would note in passing that the U.S. leverage ratio requirement for foreign firms will be phased in more slowly than originally proposed, so as to align it more closely with the effective date of the Basel III leverage ratio requirement.

A second complaint is that there is something unfair about the United States requiring an FBO to meet the international leverage ratio in its U.S. operations, because its operations may be heavily weighted toward broker-dealer activities, which generally have higher leverage, whereas the leverage ratio for U.S. firms is based on their global operations. Again, one suspects that the foreign operations of U.S. firms could be subject to a similar ratio requirement abroad as countries implement their Basel III commitments. However, quite apart from what may happen in the future, there are two U.S.-based firms--Goldman Sachs and Morgan Stanley--whose global business mix resembles that of the U.S. subsidiaries of FBOs that are predominantly engaged in broker-dealer activities in the United States. In fact, under the enhanced supplementary leverage ratio the Board proposed during the summer, these and other U.S. G-SIBs would be subject to a higher Basel III leverage ratio requirement (5 percent) than would apply to FBO IHCs (3 percent).

The applicable liquidity requirements, while somewhat differently defined, are roughly comparable to those already applicable to FBOs in the United Kingdom. The similar positions of our two nations as host countries for foreign bank operations heavily involved in trading and significantly reliant on potentially runnable short-term wholesale funding explain this rough parallelism.

The most notable departure of the new U.S. FBO standards from existing EU and U.K. practice lies in the IHC requirement for foreign banks with large domestic operations. Given the structure of U.S. financial regulation that is a legacy of Glass-Steagall, as well as the efforts by a small number of very large foreign banks to evade the intent of Congress that capital standards apply to their U.S. operations, we needed to create this structural requirement. It is unclear how much difference this makes for the capital requirements of FBOs in the United States as opposed, say, to those of U.S. operations in the EU. That would depend on the existence and size of financial affiliates owned by the U.S. firm that are not subject to Basel standards directly. In any case, it seems sound prudential practice--and consistent with the various Basel Committee principles to which I earlier referred--that large domestic operations of foreign banks meet capital standards on the basis of all exposures in the host jurisdiction and, indeed, that they manage their risks in that country across all their affiliates.

"Balkanization" and Home-Host Responsibilities

To return to the issue of Balkanization, three things should now be apparent. First, in its new capital regulations applicable to FBOs, the United States is more a follower of the pattern set by the EU than it is an initiator of new kinds of requirements. Of course, a few foreign banks would prefer the old system under which they held relatively little capital in their very extensive U.S. operations. But that was neither safe for the financial system nor particularly fair to their competitors--U.S. and foreign--that hold significant amounts of capital here. Indeed, a firm that is genuinely well capitalized, including holding the G-SIB surcharge at its global consolidated level, should require only moderate adjustment efforts during the transition period established in the FBO rule.

Second, there is considerable scope for a foreign bank to integrate its U.S. operations with its global activities within the rule the Federal Reserve adopted last month. For example, while foreign firms with more than $10 billion in non-branch assets have some additional reporting requirements, only when U.S. non-branch assets rise above $50 billion do the quantitative Basel capital requirements become applicable to the U.S. subsidiaries. Moreover, no capital requirements apply to branches so long as their parent is subject to home-country consolidated capital rules consistent with Basel standards. The U.S. operations of FBO branches and subsidiaries will not be subject to "due from" restrictions. They remain free to lend money to their worldwide affiliates; they must simply do so with a more stable funding base. Finally, I note that many FBOs, like many U.S.-based banks, have made considerable progress in reducing dependence on short-term wholesale funding and in building capital. To some extent, the new requirements are intended to preserve this progress.

Third, the capital and liquidity requirements that do apply are wholly consistent with the responsibility of host-country supervisors to assure financial stability in their own markets. Collectively, foreign banks with a large presence in the United States conduct activities of a scope, and at a scale, that could lead to problems for the U.S. financial system should they come under stress. Realistically, exposures and vulnerabilities in a large host-country market are much more difficult for home-country supervisors to assess. Indeed, U.S. regulators count on the expertise and proximity of U.K. regulators in overseeing the London operations of large U.S. financial institutions to enhance the effective consolidated supervision and regulation for which we are responsible.

On the issue of home-host-country coordination in regulating large, globally active banking organizations, I would make three additional points. First, our FBO capital requirements, like those of the EU for foreign commercial and investment banks, are based on the capital rules agreed to in the Basel Committee.15 Thus, there is an overall compatibility between national and international rules with respect to applicable definitions, standards, and required ratios.

Second, home countries must implement and enforce faithfully at a consolidated level these same capital rules. More broadly, home-country supervisory expectations for strong consolidated capital levels, liquidity positions, and risk-management practices are likely to facilitate compliance with domestic requirements for large FBOs of the sort applicable in the United States and the EU. It is also important that home countries assure the credibility of resolution mechanisms for their large banking organizations. This task entails the implementation of the Financial Stability Board's principles for effective resolution regimes, including establishing a resolution authority with adequate legal powers to manage the process in an orderly fashion without injection of public capital.16 It also includes requiring each such institution to have total loss absorption capacity sufficient to recapitalize the firm even if its substantial equity buffer is lost in an extreme tail event. Home and host countries should work together toward international standards that will ensure that an appropriate amount of this capacity would be available to host authorities faced with the potential insolvency of large FBOs in their jurisdiction or with the consequences for their market of the failure of parent banks.

In this regard, I think that capital requirements for FBOs of the sort now required by the EU and the United States are very likely to reduce the considerable strains that have traditionally accompanied financial distress at global banking firms. In most cases, including both internationally and within the EU itself in recent years, stress has resulted in the demand by host authorities for ex post ring fencing of capital, liquidity, or both, often in the absence of any ex ante requirements. The existence of FBO capital and liquidity standards, particularly if supplemented with the total loss absorbency measures to which I just referred, should mitigate the need for such demands, which of course come at the worst possible time for the firm trying to meet them.

Third, we--by which I mean both home and major host banking regulators--need to find better ways of fostering genuine regulatory and supervisory cooperation. Particularly at the most senior levels of the agencies that actually supervise globally active banks, our interactions with our counterparts from other countries have become almost exclusively focused on developing international standards or reviewing compliance with existing ones. These discussions are usually conducted with numerous colleagues who are not themselves responsible for banking regulation in their own jurisdictions. As important as these efforts have been, and continue to be, following the crisis, there is a risk that by not having opportunities for senior officials of the various national agencies that have direct supervisory responsibility for banking organizations to meet and discuss shared challenges, we give short shrift to the collective interest of bank regulators in effective supervision of all globally active firms. Proposals to include prudential requirements or, more precisely, to include limitations on prudential requirements in trade agreements would lead us farther away from the aforementioned goal of emphasizing shared financial stability interests, in favor of an approach to prudential matters informed principally by considerations of commercial advantage.

Conclusion

The job of regulating and supervising large, globally active banking organizations is a tough one. Issues of moral hazard, negative externalities, and asymmetric information are, if not pervasive, then at least significant and recurring. The job is made only harder by the fact that these firms cross borders in ways their regulators do not. But we cannot ignore this fact and pretend that we have global oversight. International standards for prudential regulation are not the same as global regulations, and consolidated supervision is not the same as comprehensive supervision. The jurisdictions represented on the Basel Committee not only have the right to regulate their financial markets--including large FBOs participating in those markets--they have a responsibility to their home jurisdictions, and to the rest of the world, to do so. The most important contribution the United States can make to global financial stability is to ensure the stability of our own financial system.

There must be some assurance beyond mere words from parent banks or home-country supervisors that a large FBO will remain strong or supported in periods of stress. After all, as we saw in the crisis, while a parent bank or home-country authorities may have offered those words with total good faith in calm times, they may be unable to carry through on them in more financially turbulent periods. None of this means that we need be at odds with one another. On the contrary, these very circumstances call not only for more tangible safeguards in host countries, but also for more genuine cooperation among supervisory authorities. Indeed, as I hope will continue to be the case with the international agenda on resolution, total loss absorbency, and related matters, we should aspire to converge around the kinds of protections that we can expect at both consolidated and local levels.

1. I would add, in passing, the observation that I am not at all sure it would be desirable to have a single global bank regulator even if it were remotely within the realm of political possibility. Return to text

2. Basel Committee on Banking Supervision (1983), "Principles for the Supervision of Banks' Foreign Establishments (PDF)" (Basel: Bank for International Settlements, May). Return to text

3. Basel Committee on Banking Supervision (1992), "Minimum Standards for Supervision of International Banking Groups and Their Cross-Border Establishments (PDF)" (Basel: Bank for International Settlements, July). Return to text

4. Basel Committee on Banking Supervision (2012), "Core Principles for Effective Banking Supervision (PDF)" (Basel: Bank for International Settlements, September), p. 38. Return to text

5. Basel Committee on Banking Supervision (2006), "International Convergence of Capital Measures and Capital Standards (PDF)" (Basel: Bank for International Settlements, June), p. 7. Return to text

6. Basel Committee on Banking Supervision (2012), "A Framework for Dealing with Domestic Systemically Important Banks (PDF)" (Basel: Bank for International Settlements, October). Return to text

7. As of September 30, 2013, there were 24 such foreign banks, compared with 24 U.S. firms. Source: For U.S. bank holding companies: FR Y-9C; for foreign banks: FR Y-9C, FFIEC 002, FR 2886b, FFIEC 031/041, FR Y-7N/NS, X-17A-5 Part II, and X-17A-5 Part IIA, and X-17A-5 Part II CSE. Return to text

8. Source: FR Y-9C, FFIEC 002, FR 2886b, FFIEC 031/041, FR Y-7N/NS, X-17A-5 Part II, and X-17A-5 Part IIA, and X-17A-5 Part II CSE. Return to text

9. Source: FFIEC 002, various years. Return to text

10. Ben S. Bernanke, Carol Bertaut, Laurie Pounder DeMarco, and Steven Kamin (2011), "International Capital Flows and the Returns to Safe Assets in the United States, 2003-2007," International Finance Discussion Papers Number 1014 (Washington: Board of Governors of the Federal Reserve System, February). Return to text

11. The European CRD IV package, which implemented the global Basel III capital standards into EU law, entered into force on July 17, 2013. See http://ec.europa.eu/internal_market/bank/regcapital/legislation_in_force_en.htm . Return to text

12. Staff estimates, using data from the Federal Reserve and the Bank of England. The U.K. data include only U.K. resident banking entities of each banking group. The U.S. data include all entities of each banking group. Both U.K. and U.S. assets include intragroup claims on related affiliates. Worldwide assets are calculated using the accounting standards of home country jurisdictions. The list of G-SIBs is available at www.financialstabilityboard.org/publications/r_131111.pdf . Return to text

13. Actually, FBOs need not meet advanced approach risk-based capital requirements in the United States, unless they specifically opt in to that treatment. See www.federalreserve.gov/newsevents/press/bcreg/20140218a.htm. Return to text

14. An FBO with total consolidated assets of $50 billion or more but with combined U.S. assets of less than $50 billion must report the results of an internal liquidity stress test (either on a consolidated basis or for its combined U.S. operations) to the Board on an annual basis. Return to text

15. As a technical matter, the relevant FBOs are subject to the traditional 4 percent U.S. leverage ratio, but it is very likely that this requirement will be less binding than the 3 percent international leverage ratio because of the inclusion in the denominator of the latter of off-balance-sheet activities and exposures. Return to text

16. Financial Stability Board (2011), "Key Attributes of Effective Resolution Regimes for Financial Institutions" (Basel: Financial Stability Board, November 4). Return to text