December 02, 2015

The Economic Outlook and Monetary Policy

Chair Janet L. Yellen

At the Economic Club of Washington, Washington, D.C.

Thank you to the Economic Club of Washington for inviting me to speak to you today. I would like to offer my assessment of the U.S. economy, nearly six and half years after the beginning of the current economic expansion, and my view of the economic outlook. I will describe the progress the economy has made toward the Federal Open Market Committee's (FOMC) goals of maximum employment and stable prices and what the current situation and the outlook imply for how monetary policy is likely to evolve to best foster the attainment of those objectives.

The Economic Outlook

The U.S. economy has recovered substantially since the Great Recession. The unemployment rate, which peaked at 10 percent in October 2009, declined to 5 percent in October of this year. At that level, the unemployment rate is near the median of FOMC participants' most recent estimates of its longer-run normal level.1 The economy has created about 13 million jobs since the low point for employment in early 2010, and total nonfarm payrolls are now almost 4-1/2 million higher than just prior to the recession. Most recently, after a couple months of relatively modest payroll growth, employers added an estimated 271,000 jobs in October. This increase brought the average monthly gain since June to about 195,000--close to the monthly pace of around 210,000 in the first half of the year and still sufficient to be consistent with continued improvement in the labor market.

Despite these substantial gains, we cannot yet, in my judgment, declare that the labor market has reached full employment. Let me describe the basis for that view.

To begin with, I believe that a significant number of individuals now classified as out of the labor force would find and accept jobs in an even stronger labor market. To be classified as unemployed, working-age people must report that they have actively sought work within the past four weeks. Most of those not seeking work are appropriately not counted as unemployed. These include most retirees, teenagers and young adults in school, and those staying home to care for children and other dependent family members. Even in a stronger job market, it is likely that many of these individuals would choose not to work.

But some who are counted as out of the labor force might be induced to seek work if the likelihood of finding a job rose or if the expected pay was higher. Examples here include people who had become too discouraged to search for work when the prospects for employment were poor and some who retired when their previous jobs ended. In October, almost 2 million individuals classified as outside the labor force because they had not searched for work in the previous four weeks reported that they wanted and were available for work. This is a considerable number of people, and some of them undoubtedly would be drawn back into the workforce as the labor market continued to strengthen. Likewise, some of those who report they don't want to work now could change their minds in a stronger job market.

Another margin of labor market slack not reflected in the unemployment rate consists of individuals who report that they are working part time but would prefer a full-time job and cannot find one--those classified as "part time for economic reasons." The share of such workers jumped from 3 percent of total employment prior to the Great Recession to around 6-1/2 percent by 2010. Since then, however, the share of these part time workers has fallen considerably and now is less than 4 percent of those employed. While this decline represents considerable progress, particularly given secular trends that over time may have increased the prevalence of part-time employment, I think some room remains for the hours of these workers to increase as the labor market improves further.

The pace of increases in labor compensation provides another possible indicator, albeit an imperfect one, of the degree of labor market slack. Until recently labor compensation had grown only modestly, at average annual rates of around 2 to 2-1/2 percent. More recently, however, we have seen a welcome pickup in the growth rate of average hourly earnings for all employees and of compensation per hour in the business sector. While it is too soon to conclude whether these more rapid rates of increase will continue, a sustained pickup would likely signal a diminution of labor market slack.

Turning to overall economic activity, U.S. economic output--as measured by inflation-adjusted gross domestic product (GDP), or real GDP--has increased at a moderate pace, on balance, during the expansion. Over the first three quarters of this year, real GDP is currently estimated to have advanced at an annual rate of 2-1/4 percent, close to its average pace over the previous five years. Many economic forecasters expect growth roughly along those same lines in the fourth quarter.

Growth this year has been held down by weak net exports, which have subtracted more than 1/2 percentage point, on average, from the annual rate of real GDP growth over the past three quarters. Foreign economic growth has slowed, damping increases in U.S. exports, and the U.S. dollar has appreciated substantially since the middle of last year, making our exports more expensive and imported goods cheaper.

By contrast, total real private domestic final purchases (PDFP)--which includes household spending, business fixed investment, and residential investment, and currently represents about 85 percent of aggregate spending--has increased at an annual rate of 3 percent this year, significantly faster than real GDP. Household spending growth has been particularly solid in 2015, with purchases of new motor vehicles especially strong. Job growth has bolstered household income, and lower energy prices have left consumers with more to spend on other goods and services. These same factors likely have contributed to consumer confidence that is more upbeat this year than last year. Increases in home values and stock market prices in recent years, along with reductions in debt, have pushed up the net worth of households, which also supports consumer spending. Finally, interest rates for borrowers remain low, due in part to the FOMC's accommodative monetary policy, and these low rates appear to have been especially relevant for consumers considering the purchase of durable goods.2

Other components of PDFP, including residential and business investment, have also advanced this year. The same factors supporting consumer spending have supported further gains in the housing sector. Indeed, gains in real residential investment spending have been faster so far in 2015 than last year, although the level of new residential construction still remains fairly low. And outside of the drilling and mining sector, where lower oil prices have led to substantial cuts in outlays for new structures, business investment spending has posted moderate gains.

On balance, the moderate average pace of real GDP growth so far this year and over the entire expansion has been sufficient to help move the labor market closer to the FOMC's goal of maximum employment. However, less progress has been made on the second leg of our dual mandate--price stability--as inflation continues to run below the FOMC's longer-run objective of 2 percent. Overall consumer price inflation--as measured by the change in the price index for personal consumption expenditures--was only 1/4 percent over the 12 months ending in October. However, this number largely reflects the sharp fall in crude oil prices since the summer of 2014 that, in turn, has pushed down retail prices for gasoline and other consumer energy products. Because food and energy prices are volatile, it is often helpful to look at inflation excluding those two categories--known as core inflation--which is typically a better indicator of future overall inflation than recent readings of headline inflation. But core inflation--which ran at 1-1/4 percent over the 12 months ending in October--is also well below our 2 percent objective, partly reflecting the appreciation of the U.S. dollar. The stronger dollar has pushed down the prices of imported goods, placing temporary downward pressure on core inflation.3 The plunge in crude oil prices may also have had some small indirect effects in holding down the prices of non-energy items in core inflation, as producers passed on to their customers some of the reductions in their energy-related costs. Taking account of these effects, which may be holding down core inflation by around 1/4 to 1/2 percentage point, it appears that the underlying rate of inflation in the United States has been running in the vicinity of 1-1/2 to 1-3/4 percent.

Let me now turn to where I see the economy is likely headed over the next several years. To summarize, I anticipate continued economic growth at a moderate pace that will be sufficient to generate additional increases in employment, further reductions in the remaining margins of labor market slack, and a rise in inflation to our 2 percent objective. I expect that the fundamental factors supporting domestic spending that I have enumerated today will continue to do so, while the drag from some of the factors that have been weighing on economic growth should begin to lessen next year. Although the economic outlook, as always, is uncertain, I currently see the risks to the outlook for economic activity and the labor market as very close to balanced.

Turning to the factors that have been holding down growth, as I already noted, the higher foreign exchange value of the dollar, as well as weak growth in some foreign economies, has restrained the demand for U.S. exports over the past year. In addition, lower crude oil prices have reduced activity in the domestic oil sector. I anticipate that the drag on U.S. economic growth from these factors will diminish in the next couple of years as the global economy improves and the adjustment to prior declines in oil prices is completed.

Although developments in foreign economies still pose risks to U.S. economic growth that we are monitoring, these downside risks from abroad have lessened since late summer. Among emerging market economies, recent data support the view that the slowdown in the Chinese economy, which has received considerable attention, will likely continue to be modest and gradual. China has taken actions to stimulate its economy this year and could do more if necessary. A number of other emerging market economies have eased monetary and fiscal policy this year, and economic activity in these economies has improved of late. Accommodative monetary policy is also supporting economic growth in the advanced economies. A pickup in demand in many advanced economies and a stabilization in commodity prices should, in turn, boost the growth prospects of emerging market economies.

A final positive development for the outlook that I will mention relates to fiscal policy. This year the effect of federal fiscal policy on real GDP growth has been roughly neutral, in contrast to earlier years in which the expiration of stimulus programs and fiscal policy actions to reduce the federal budget deficit created significant drags on growth.4 Also, the budget situation for many state and local governments has improved as the economic expansion has increased the revenues of these governments, allowing them to increase their hiring and spending after a number of years of cuts in the wake of the Great Recession. Looking ahead, I anticipate that total real government purchases of goods and services should have a modest positive effect on economic growth over the next few years.5

Regarding U.S. inflation, I anticipate that the drag from the large declines in prices for crude oil and imports over the past year and a half will diminish next year. With less downward pressure on inflation from these factors and some upward pressure from a further tightening in U.S. labor and product markets, I expect inflation to move up to the FOMC's 2 percent objective over the next few years. Of course, inflation expectations play an important role in the inflation process, and my forecast of a return to our 2 percent objective over the medium term relies on a judgment that longer-term inflation expectations remain reasonably well anchored. In this regard, recent measures from the Survey of Professional Forecasters, the Blue Chip Economic Indicators, and the Survey of Primary Dealers have continued to be generally stable. The measure of longer-term inflation expectations from the University of Michigan Surveys of Consumers, in contrast, has lately edged below its typical range in recent years. However, this measure often seems to respond modestly, though temporarily, to large changes in actual inflation, and the very low readings on headline inflation over the past year may help explain some of the recent decline in the Michigan measure.6 Market-based measures of inflation compensation have moved up some in recent weeks after declining to historically low levels earlier in the fall. While the low level of these measures appears to reflect, at least in part, changes in risk and liquidity premiums, we will continue to monitor this development closely. Convincing evidence that longer-term inflation expectations have moved lower would be a concern because declines in consumer and business expectations about inflation could put downward pressure on actual inflation, making the attainment of our 2 percent inflation goal more difficult.

Monetary Policy

Let me now turn to the implications of the economic outlook for monetary policy. Reflecting progress toward the Committee's objectives, many FOMC participants indicated in September that they anticipated, in light of their economic forecasts at the time, that it would be appropriate to raise the target range for the federal funds rate by the end of this year. Some participants projected that it would be appropriate to wait until later to raise the target funds rate range, but all agreed that the timing of a rate increase would depend on what the incoming data tell us about the economic outlook and the associated risks to that outlook.

In the policy statement issued after its October meeting, the FOMC reaffirmed its judgment that it would be appropriate to increase the target range for the federal funds rate when we had seen some further improvement in the labor market and were reasonably confident that inflation would move back to the Committee's 2 percent objective over the medium term. That initial rate increase would reflect the Committee's judgment, based on a range of indicators, that the economy would continue to grow at a pace sufficient to generate further labor market improvement and a return of inflation to 2 percent, even after the reduction in policy accommodation. As I have already noted, I currently judge that U.S. economic growth is likely to be sufficient over the next year or two to result in further improvement in the labor market. Ongoing gains in the labor market, coupled with my judgment that longer-term inflation expectations remain reasonably well anchored, serve to bolster my confidence in a return of inflation to 2 percent as the disinflationary effects of declines in energy and import prices wane.

Committee participants recognize that the future course of the economy is uncertain, and we take account of both the upside and downside risks around our projections when judging the appropriate stance of monetary policy. In particular, recent monetary policy decisions have reflected our recognition that, with the federal funds rate near zero, we can respond more readily to upside surprises to inflation, economic growth, and employment than to downside shocks. This asymmetry suggests that it is appropriate to be more cautious in raising our target for the federal funds rate than would be the case if short-term nominal interest rates were appreciably above zero.7 Reflecting these concerns, we have maintained our current policy stance even as the labor market has improved appreciably.

However, we must also take into account the well-documented lags in the effects of monetary policy.8 Were the FOMC to delay the start of policy normalization for too long, we would likely end up having to tighten policy relatively abruptly to keep the economy from significantly overshooting both of our goals. Such an abrupt tightening would risk disrupting financial markets and perhaps even inadvertently push the economy into recession. Moreover, holding the federal funds rate at its current level for too long could also encourage excessive risk-taking and thus undermine financial stability.

On balance, economic and financial information received since our October meeting has been consistent with our expectations of continued improvement in the labor market. And, as I have noted, continuing improvement in the labor market helps strengthen confidence that inflation will move back to our 2 percent objective over the medium term. That said, between today and the next FOMC meeting, we will receive additional data that bear on the economic outlook. These data include a range of indicators regarding the labor market, inflation, and economic activity. When my colleagues and I meet, we will assess all of the available data and their implications for the economic outlook in making our policy decision.

As you know, there has been considerable focus on the first increase in the federal funds rate after nearly seven years in which that rate has been at its effective lower bound. We have tried to be as clear as possible about the considerations that will affect that decision. Of course, even after the initial increase in the federal funds rate, monetary policy will remain accommodative. And it bears emphasizing that what matters for the economic outlook are the public's expectations concerning the path of the federal funds rate over time: It is those expectations that affect financial conditions and thereby influence spending and investment decisions. In this regard, the Committee anticipates that even after employment and inflation are near mandate-consistent levels, economic conditions may, for some time, warrant keeping the target federal funds rate below levels the Committee views as normal in the longer run.

This expectation is consistent with an implicit assessment that the neutral nominal federal funds rate--defined as the value of the federal funds rate that would be neither expansionary nor contractionary if the economy were operating near its potential--is currently low by historical standards and is likely to rise only gradually over time. One indication that the neutral funds rate is unusually low is that U.S. economic growth has been quite modest in recent years despite the very low level of the federal funds rate and the Federal Reserve's very large holdings of longer-term securities. Had the neutral rate been running closer to the levels that are thought to have prevailed prior to the financial crisis, current monetary policy settings would have been expected to foster a very rapid economic expansion, with inflation likely rising significantly above our 2 percent objective.

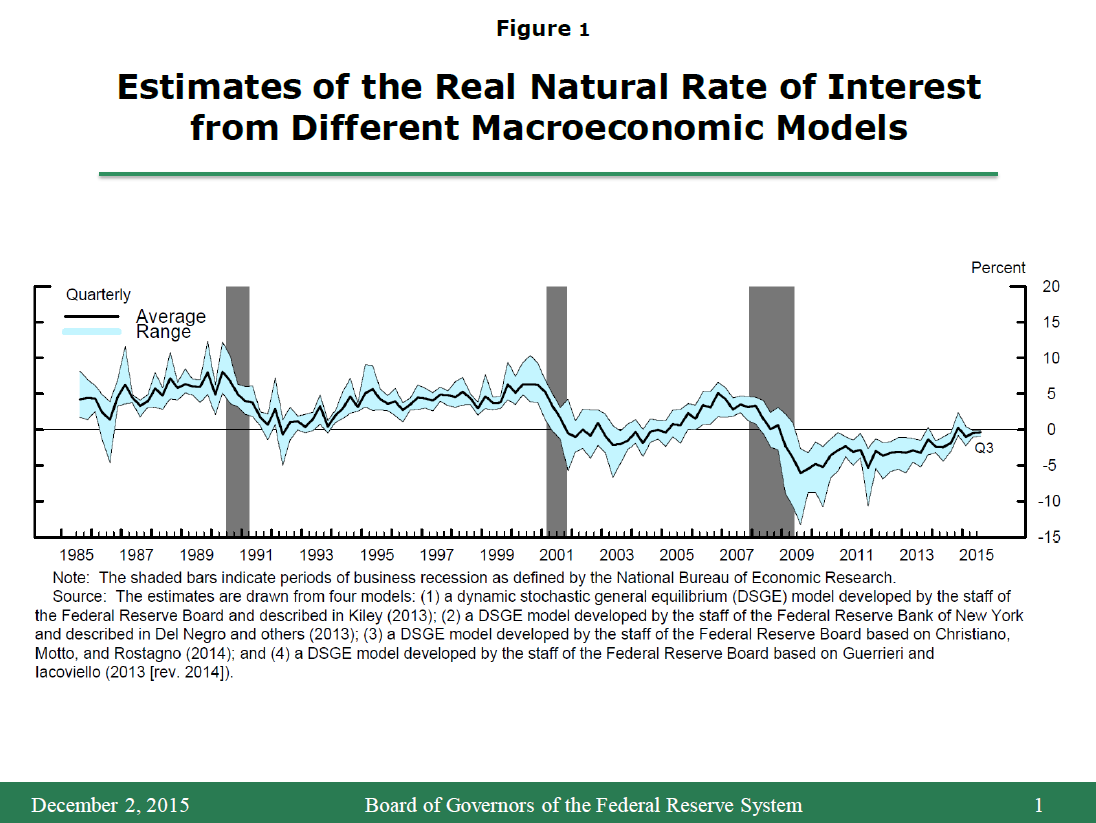

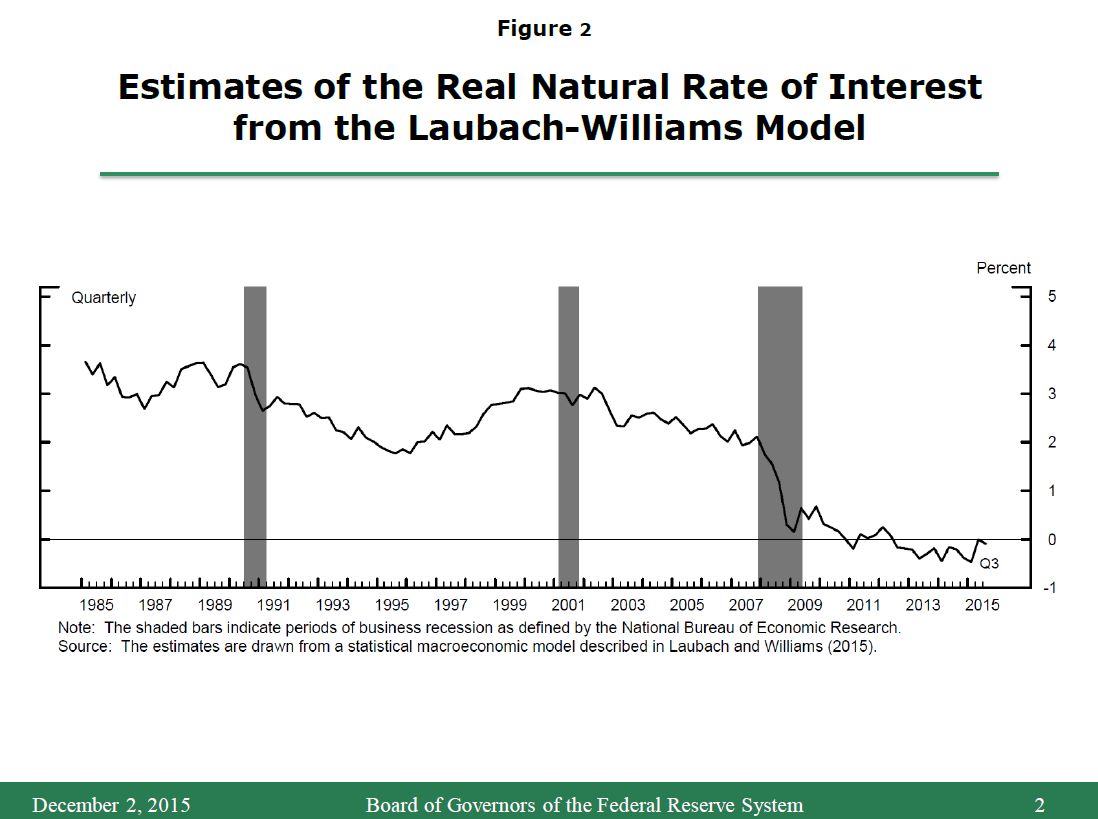

Empirical support for the judgment that the neutral federal funds rate is low comes from both academic research and Federal Reserve staff analysis. Figure 1 employs four macroeconomic models used by Federal Reserve staff to estimate the "natural" real rate of interest, a concept closely related to the neutral rate.9 The measures of the natural rate shown in this figure represent the real short-term interest rate that would prevail in the absence of frictions that slow the adjustment of wages and prices to changes in the economy; under a variety of assumptions, this interest rate has been shown to promote full employment.10 The shaded blue band represents the range of the estimates of the natural real rate at each point in time. This analysis suggests that the natural real rate fell sharply with the onset of the crisis and has recovered only partially. These findings are broadly consistent with those reported in a paper by Thomas Laubach and John Williams, shown in figure 2.11

{kind=link}

{kind=link}

The marked decline in the neutral federal funds rate after the crisis may be partially attributable to a range of persistent economic headwinds that have weighed on aggregate demand. These headwinds have included tighter underwriting standards and limited access to credit for some borrowers, deleveraging by many households to reduce debt burdens, contractionary fiscal policy at all levels of government, weak growth abroad coupled with a significant appreciation of the dollar, slower productivity and labor force growth, and elevated uncertainty about the economic outlook.12 As the restraint from these headwinds further abates, I anticipate that the neutral federal funds rate will gradually move higher over time. Indeed, in September, most FOMC participants projected that, in the long run, the nominal federal funds rate would be near 3.5 percent, and that the actual federal funds rate would rise to that level fairly slowly.13

Because the value of the neutral federal funds rate is not directly measureable and must be estimated based on our imperfect understanding of the economy and the available data, I would stress that considerable uncertainty attends our estimates of its current level and even more to its likely path going forward.14 That said, we will learn more from observing economic developments in the period ahead. It is thereby important to emphasize that the actual path of monetary policy will depend on how incoming data affect the evolution of the economic outlook. Stronger growth or a more rapid increase in inflation than we currently anticipate would suggest that the neutral federal funds rate is rising more quickly than expected, making it appropriate to raise the federal funds rate more quickly as well; conversely, if the economy disappoints, the federal funds rate would likely rise more slowly. Given the persistent shortfall in inflation from our 2 percent objective, the Committee will, of course, carefully monitor actual progress toward our inflation goal as we make decisions over time on the appropriate path for the federal funds rate.

In closing, let me again thank the Economic Club of Washington for this opportunity to speak about the economy and monetary policy. The economy has come a long way toward the FOMC's objectives of maximum employment and price stability. When the Committee begins to normalize the stance of policy, doing so will be a testament, also, to how far our economy has come in recovering from the effects of the financial crisis and the Great Recession. In that sense, it is a day that I expect we all are looking forward to.

References

Adam, Klaus, and Roberto M. Billi (2007). "Discretionary Monetary Policy and the Zero Lower Bound on Nominal Interest Rates," Journal of Monetary Economics, vol. 54 (3), pp. 728-52.

Barsky, Robert, Alejandro Justiniano, and Leonardo Melosi (2014). "The Natural Rate of Interest and Its Usefulness for Monetary Policy," American Economic Review, vol. 104 (May), pp. 37-43.

Board of Governors of the Federal Reserve System (2014). "Minutes of the Federal Open Market Committee, September 16-17, 2014," press release, October 8.

--------- (2015a). "Minutes of the Federal Open Market Committee, March 17-18, 2015," press release, April 8.

--------- (2015b). "Minutes of the Federal Open Market Committee, September 16-17, 2015," press release, October 8.

Christiano, Lawrence J., Martin Eichenbaum, and Charles L. Evans (2005). "Nominal Rigidities and the Dynamic Effects of a Shock to Monetary Policy," Journal of Political Economy, vol. 113 (February), pp. 1-45.

Christiano, Lawrence J., Roberto Motto, and Massimo Rostagno (2014). "Risk Shocks," American Economic Review, vol. 104 (January), pp. 27-65.

Congressional Budget Office (2015a). The Budget and Economic Outlook: 2015 to 2025. Washington: CBO, January.

--------- (2015b). An Update to the Budget and Economic Outlook: 2015 to 2025. Washington: CBO, August.

Cúrdia, Vasco, Andrea Ferrero, Ging Cee Ng, and Andrea Tambalotti (2015). "Has U.S. Monetary Policy Tracked the Efficient Interest Rate?" Journal of Monetary Economics, vol. 70 (March), pp. 72-83.

Del Negro, Marco, Stefano Eusepi, Marc Giannoni, Argia Sbordone, Andrea Tambalotti, Matthew Cocci, Raiden Hasegawa, and M. Henry Linder (2013). "The FRBNY DSGE Model (PDF)," Federal Reserve Bank of New York Staff Reports 647. New York: Federal Reserve Bank of New York, October.

Eggertsson, Gauti B., and Paul R. Krugman (2012). "Debt, Deleveraging, and the Liquidity Trap: A Fisher-Minsky-Koo Approach," Quarterly Journal of Economics, vol. 123 (3), pp. 1469-513.

Evans, Charles, Jonas Fisher, François Gourio, and Spencer Krane (2015). "Risk Management for Monetary Policy Near the Zero Lower Bound (PDF)," Brookings Papers on Economic Activity Conference Draft, March 19-20, 2015. Washington: Brookings Institution, March.

Friedman, Milton (1961). "The Lag in Effect of Monetary Policy," Journal of Political Economy, vol. 69 (October), pp. 447-66.

Guerrieri, Luca, and Matteo Iacoviello (2013). "Collateral Constraints and Macroeconomic Asymmetries (PDF)," International Finance Discussion Papers 1082r. Washington: Board of Governors of the Federal Reserve System, June; revised July 2014.

Guerrieri, Veronica, and Guido Lorenzoni (2015). "Credit Crises, Precautionary Savings, and the Liquidity Trap (PDF)," unpublished paper, University of Chicago, January.

Johnson, Kathleen W., Karen M. Pence, and Daniel J. Vine (2014). "Auto Sales and Credit Suppl (PDF)," Finance and Economics Discussion Series 2014-82. Washington: Board of Governors of the Federal Reserve System, September.

Kiley, Michael T. (2013). "Output Gaps," Journal of Macroeconomics, vol. 37 (September), pp. 1-18.

Laubach, Thomas, and John C. Williams (2003). "Measuring the Natural Rate of Interest," Review of Economics and Statistics, vol. 85 (November), pp. 1063-70.

--------- (2015). "Measuring the Natural Rate of Interest Redux," Hutchins Center Working Papers 15. Washington: Brookings Institution, November.

Nakata, Taisuke (2012). "Uncertainty at the Zero Lower Bound (PDF)," Finance and Economics Discussion Series 2013-09. Washington: Board of Governors of the Federal Reserve System, December.

Uhlig, Harald (2005). "What Are the Effects of Monetary Policy on Output? Results from an Agnostic Identification Procedure," Journal of Monetary Economics, vol. 52 (March), pp. 381-419.

Wicksell, Knut (1936). Interest and Prices: A Study of the Causes Regulating the Value of Money. Translated by R.F. Kahn. London: Macmillan and Co. First published 1898.

Yellen, Janet L. (2015). "Inflation Dynamics and Monetary Policy," speech delivered at the Philip Gamble Memorial Lecture, University of Massachusetts at Amherst, Amherst, Mass., September 24.

1. See table 1 in the Summary of Economic Projections, an addendum to the minutes of the September 2015 FOMC meeting. See Board of Governors (2015b). Return to text

2. For a recent empirical assessment, see Johnson, Pence, and Vine (2014). Return to text

3. For a more detailed discussion of the recent behavior of inflation, see Yellen (2015). Return to text

4. The Congressional Budget Office estimates that current federal fiscal policies will have little effect on economic growth this year, but that earlier fiscal policy actions reduced the rate of real GDP growth roughly 1-1/2 percentage points in 2013 and about 1/4 percentage point in 2014 relative to what it would have been otherwise. See Congressional Budget Office (2015a). Return to text

5. See Congressional Budget Office (2015b). Return to text

6. For example, the University of Michigan survey measure of longer-term inflation expectations was temporarily elevated relative to its usual range in 2008 when crude oil and other commodity prices spiked and pushed up actual headline inflation for a time. Return to text

7. See, for example, Adam and Billi (2007), Nakata (2012), and Evans and others (2015). Return to text

8. Milton Friedman famously concluded that "monetary actions affect economic conditions only after a lag that is both long and variable" (1961, p. 447). Evidence that monetary policy affects inflation with a lag comes in part from vector autoregressions in which monetary policy shocks have been identified under a variety of identification assumptions. See, for example, Christiano, Eichenbaum and Evans (2005) and Uhlig (2005). Return to text

9. Note that these estimates are in real terms; to obtain estimates of the nominal natural interest rate, one would add a measure of expected inflation. The four models used are (1) a dynamic stochastic general equilibrium (DSGE) model developed by the staff of the Federal Reserve Board and described in Kiley (2013); (2) a DSGE model developed by the staff of the Federal Reserve Bank of New York and described in Del Negro and others (2013); (3) a DSGE model developed by the staff of the Federal Reserve Board based on Christiano, Motto, and Rostagno (2014); and (4) a DSGE model developed by the staff of the Federal Reserve Board based on Guerrieri and Iacoviello (2013 [rev. 2014]). Return to text

10. The concept of the natural rate goes back to Wicksell, who defined it as the rate that "tends neither to raise nor to lower" (1936 [1898], p. 102) commodity prices. Wicksell posited that the natural rate would be equal to the real interest rate that would balance supply and demand absent monetary frictions. The recent academic literature draws on this notion to define the natural rate as the real interest rate that would prevail in the absence of sluggish adjustment in nominal prices and wages. In simple models, this interest rate would result in stable prices and full employment; in some more complex models, this interest rate has been found to promote stable inflation and appropriate economic activity, although monetary policymakers face important tradeoffs in such settings. Importantly, the natural rate varies over time. For example, it generally rises with expected productivity growth and with "preference shocks" that capture households' desire to consume today rather than save. For further discussion of the potential usefulness of the natural rate for monetary policy, see, for example, Barsky, Justiniano, and Melosi (2014) and Cúrdia and others (2015). By contrast, Laubach and Williams (2015) employ a statistical approach that defines the natural rate as one consistent with the economy operating at its full potential once transitory shocks to aggregate supply and demand have abated. These two approaches to the measurement of the natural real rate are different but have important similarities. Qualitatively, the two measures would be expected to move together in response to shocks to productivity growth and preferences so long as those shocks were very persistent. Return to text

11. See Laubach and Williams (2015). Return to text

12. For analyses of how a sudden tightening in access to credit can lead to household deleveraging, pushing down the neutral rate of interest, see Eggertsson and Krugman (2012) and Guerrieri and Lorenzoni (2015). Return to text

13. See figure 2 in the Summary of Economic Projections, an addendum to the minutes of the September 2015 FOMC meeting. See Board of Governors (2015b). The longer-run normal level of the federal funds rate reported in the SEP presumably matches participants' assessment of the neutral nominal federal funds rate that will prevail in the longer run. Between June 2012 and September 2015 the median of FOMC participants' estimates of the longer-run level of the federal funds rate declined 75 basis points, to 3.5 percent. When revising down their estimates of the longer-run federal funds rate, participants have generally cited a lower assessment of the economy's longer-run potential growth rate as a contributing factor. Return to text

14. One source of uncertainty regarding the neutral federal funds rate is so-called model uncertainty. As shown in figure 1, a variety of models that provide plausible descriptions of the economy give somewhat different estimates of the neutral rate. A second source of uncertainty is the limited sample size of relevant macroeconomic data: Our estimates of the neutral federal funds rate represent inferences about a moving target. As a result, although the data provide important signals about the neutral rate, our estimates are necessarily imprecise. In Laubach and Williams (2003), for example, the standard error of the estimate of the neutral rate in one baseline model was about 2 percentage points on average. Moreover, one-sided estimates of the neutral rate--those available to policymakers, based only on data known at the time--are generally noisier than estimates of the neutral rate at some previous time that incorporate all the data available. Return to text