FEDS Notes

Print

PrintMarch 6, 2015

Do Lower Gasoline Prices Boost Confidence?

Aditya Aladangady and Claudia R. Sahm

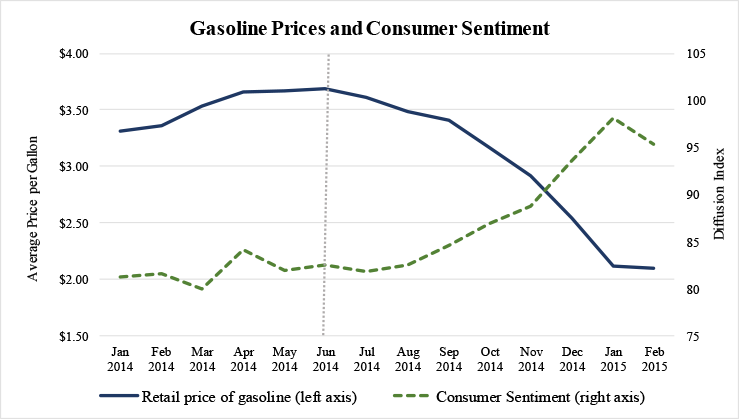

A gallon of gasoline currently costs one third less than it did last summer, as shown by the solid line in Figure 1. Gasoline makes up 5 percent of average family spending, so lower prices at the pump should increase current purchasing power for many.1 A drop in gasoline prices may also make people more confident about their future resources--the focus of this note.

| Figure 1 |

|---|

|

Source: Energy Information Administration for motor gasoline regular retail price (including taxes): http://www.eia.gov/forecasts/steo/realprices/ February is an EIA forecast, Univerisity of Michigan Surveys of Consumers for sentiment: http://www.sca.isr.umich.edu/

In fact, recent surveys show a rise in confidence that coincides with the decline in gasoline prices. As one example, we estimate that energy price declines can account for about two-thirds of the increase since last June in the Index of Consumer Sentiment (the dashed line in Figure 1).2

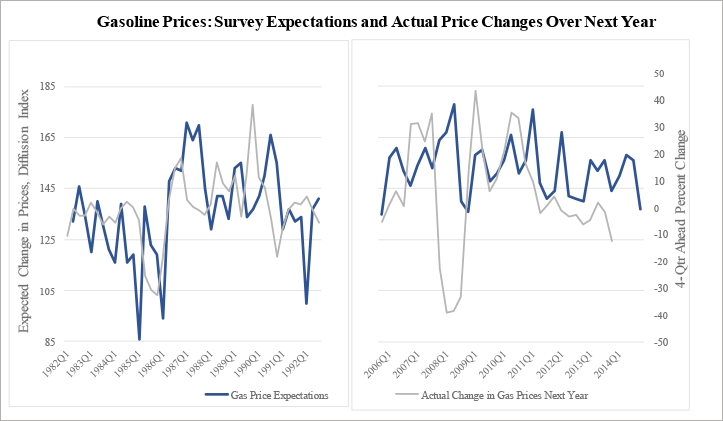

Summary measures of confidence can be difficult to interpret, however, so we turn now to specific questions about expectations and buying conditions to explore the impact of gasoline prices further. First, we see that individuals' expectations about future changes in gasoline prices are informative of actual prices changes, suggesting that individuals update their views as conditions change. Specifically, the survey asks "... do you think that the price of gasoline will go up during the next twelve months, will gasoline prices go down, or will they stay about the same as they are now?" In Figure 2, the diffusion index of expected gasoline price changes for the next year from individuals (blue line) is quite volatile but appears to align fairly well with the realized year-ahead percent change in gasoline prices (gray line).3 The correlation between the two series of 0.19 is notable given the unpredictability of gasoline prices.

| Figure 2 |

|---|

|

Source: Energy Information Administration for motor gasoline regular retail price (including taxes): http://www.eia.gov/forecasts/steo/realprices/, Univerisity of Michigan Surveys of Consumers for sentiment: http://www.sca.isr.umich.edu/ . Quarterly data from 1982:Q2 to 2014:Q4

Note: The one-year-ahead survey expectations for gas prices were not asked 1993-2006

As actual gasoline prices have fallen recently, expectations about gasoline prices have also softened. This suggests that individuals have a more optimistic view about their future purchasing power. To test this connection, we examine views on expected real income growth conditional on individuals' expectations about gasoline prices.

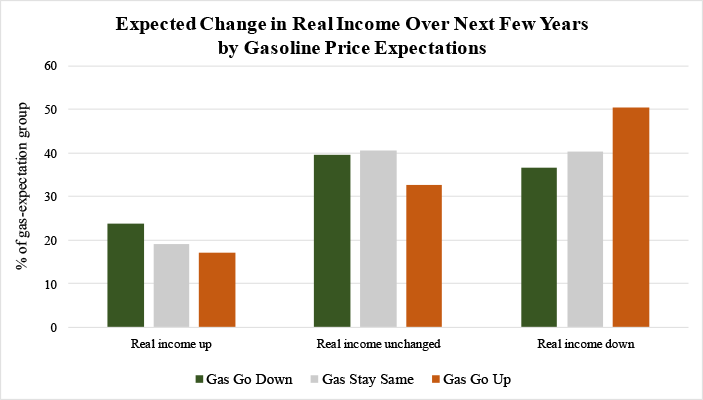

The remaining analysis uses the individual survey responses in Michigan survey from July 2014 to February 2015 from about 4000 people. In those eight months, on average, nearly 10 percent of individuals expected gasoline prices to go down, twice the rate in 2013. Figure 3 shows that during this period individuals who expect gas prices to go down in the next twelve months (green bars) are more optimistic about their real income prospects than individuals who expect gas prices to go up (orange bars) or gas prices to stay the same (gray bars).4

| Figure 3 |

|---|

|

Source: University of Michigan Surveys of Consumers.

Note: In total, 18 percent expect real income to go up, 36 percent expect real income to be unchanged, and 46 percent expect real income to go down. Differences between green and orange bars are statistically significant at 1-percent level.

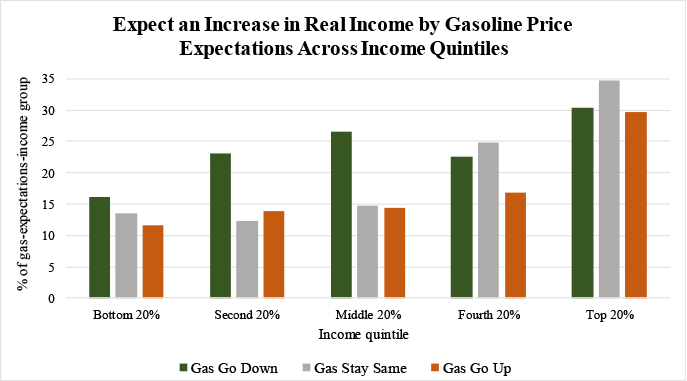

Second, this inverse relationship between expectations about gasoline prices and expectations about real income appears robust throughout the distribution of current income. Figure 4 expands the left-most grouping in Figure 3--those expecting real income to increase--by income quintiles. At each quintile, those expecting gas prices to go down (green bars) are more likely to expect their real income to increase than those who expect gas prices to go up (orange bars). With the smaller subsample--only those expecting a real income increase--the differences by gasoline price expectations are less precisely estimated. Since last summer, the difference is largest (and statistically significant) in the middle of the income distribution.

| Figure 4 |

|---|

|

Source: University of Michigan Surveys of Consumers.

Note: In total, 18 percent expect real income to go up, 36 percent expect real income to be unchanged, and 46 percent expect real income to go down. Differences between green and orange bars are statistically significant at 1-percent level.

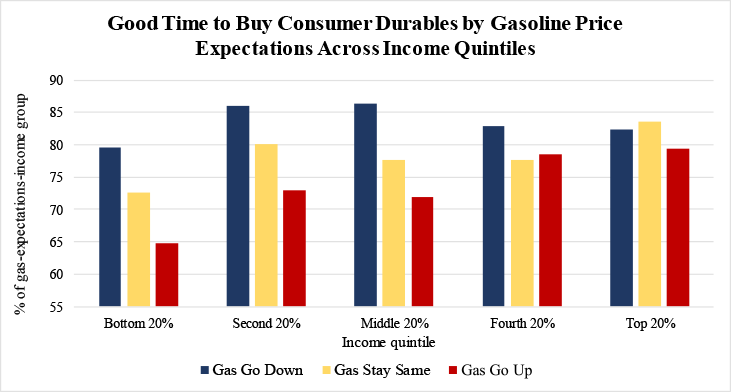

These data suggest that the lower gasoline prices have made a broad set of individuals more confident. Of course, whether and when this heightened optimism translates to more consumer spending is another question. While the Michigan survey does not ask about spending, it does ask whether it is a good time to buy durables.5 As shown in Figure 5, individuals who expect gasoline prices to decline further are more likely to view buying conditions as favorable.

| Figure 5 |

|---|

|

Source: University of Michigan Surveys of Consumers.

Note: The percent of who say it is a good time to buy generaly rises across the income quintiles: 69, 76, 75, 79, and 81 percent. The differences between the blue and red bars are statistically significant at the 5 percent level for the the first three income quintiles.

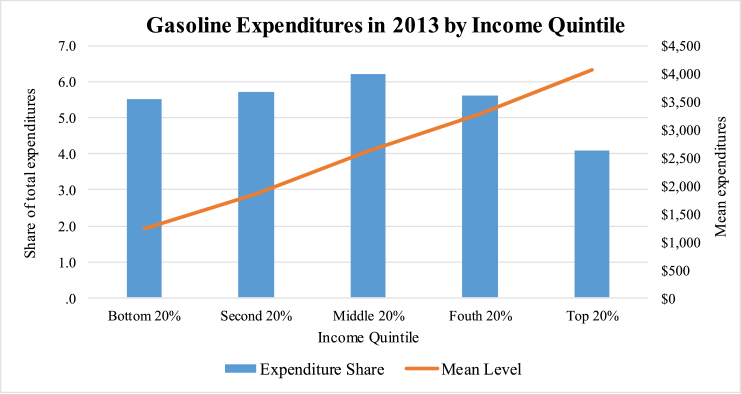

Interestingly, the differences in reported buying conditions in the bottom half of the income distribution are even more pronounced than the differences in expected real income. One possible explanation for the stronger responses at lower income levels is that gasoline represents a larger share of family budgets. As shown by the bars in Figure 6, the gasoline expenditure shares from the Consumer Expenditure Survey peak in the middle income quintile and are lowest for top income quintile. Nonetheless, the solid line in Figure 6, indicates that the mean spending on gasoline does rise with income, meaning that while those with low income may see a larger fraction of their income freed up, falling gasoline prices cause the largest real income boost in dollar terms for those with higher income. The extent to which this income boost translates into new spending may also differ across individuals. In particular, those whose spending had previously been limited may exhibit a higher marginal propensity to consume.

All told, it appears that the decline in gasoline prices since last summer have both made individuals more optimistic about their future real incomes and bolstered their assessment of current buying conditions. Together with the direct savings from lower gasoline prices that are currently being realized, the extra confidence may also boost consumer spending going forward. Importantly, the impact of lower gas prices on confidence appears broad-based across income groups and may therefore lead to increased spending for a wide range of individuals.

1. Expenditure shares for gasoline from Consumer Expenditure Survey, 2013, for example: http://www.bls.gov/cex/2013/combined/quintile.pdf Return to text

2. Index of Consumer Sentiment combines the relative score (percent giving favorable replies minus percent giving unfavorable replies plus 100) to five questions about current and expected economic conditions. Our estimate of the energy-price effect is from a monthly regression model of sentiment that also includes CPI inflation, percent change in stock prices, unemployment rate, and change in payroll employment as covariates. The estimation range includes January 1978 to February 2015. Return to text

3. The diffusion index is the percent expecting an increase in gasoline prices minus the percent expecting a decrease in gasoline prices plus 100. Return to text

4. Specifically, the income question asks: "During the next year or two, do you expect that your (family) income will go up more than prices will go up, about the same, or less than prices will go up?" In Figure 2, the bars of the same color sum to 100 percent. The relative heights of the bars of the same color reflect differences in expectations about real income. In general, households are pessimistic about their income prospects. See earlier analysis of income expectations in Sahm (2013): http://www.federalreserve.gov/econresdata/notes/feds-notes/2013/why-have-americans-income-expectations-declined-so-sharply-20130926.html Return to text

5. Specifically, the buying conditions question asks: "About the big things people buy for their homes--such as furniture, a refrigerator, stove, television, and things like that. Generally speaking, do you think now is a good or a bad time for people to buy major household items?" Return to text

Please cite as:

Aladangady, Aditya, and Claudia R. Sahm (2015). "Do Lower Gasoline Prices Boost Confidence?" FEDS Notes. Washington: Board of Governors of the Federal Reserve System, March 06, 2015. https://doi.org/10.17016/2380-7172.1501

Disclaimer: FEDS Notes are articles in which Board economists offer their own views and present analysis on a range of topics in economics and finance. These articles are shorter and less technically oriented than FEDS Working Papers.