FEDS Notes

Print

PrintMarch 3, 2016

Funding Agreement-Backed Securities in the Financial Accounts of the United States1

Elizabeth Holmquist and Maria Perozek

Introduction

This note describes a new method of accounting for funding agreement-backed securities (FABS) in the Financial Accounts of the United States.2 A funding agreement is a deposit-type contract, sold by life insurance companies, that typically allows funds to accumulate at a guaranteed rate of return over a specified period of time. Some funding agreements are purchased by domestic or foreign special purpose entities (SPEs) which securitize them into funding agreement-backed securities (FABS) and sell them to institutional investors. Raising funds using FABS typically involves converting an illiquid, longer-duration funding agreement contract into a relatively liquid, often shorter-duration security. Some observers have pointed out that the liquidity transformation and maturity transformation involved in FABS issuance entail risks to the financial stability of both the insurer and potentially the broader financial system (see Foley-Fisher, Narajabad, and Verani (2015) for additional information on risks associated with FABS). Beginning with the December 10, 2015 publication of the Financial Accounts, we now provide additional detail on these arrangements by separately identifying the funding agreements held by foreign and domestic SPEs that back FABS issuance.

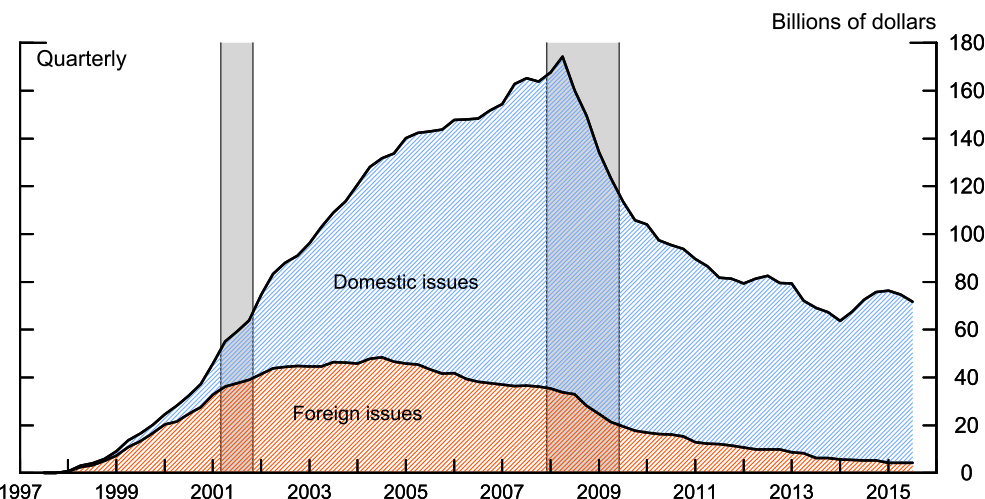

Trends in FABS issuance

The new FABS data are available beginning 1997:Q3 and include FABS issued in both domestic and foreign markets that are backed by funding agreements purchased from U.S. life insurance companies. As figure 1 below shows, foreign issuance of FABS accounted for most of this market through the early 2000s, after which foreign issuance began to flatten out and domestic issuance picked up sharply. Foreign FABS outstanding peaked at $48 billion in 2004:Q3, and then declined over the subsequent years to a level of only $5 billion in 2015:Q3.

| Figure 1. Funding Agreement-Backed Securities Outstanding |

|---|

|

Note: The gray shaded bars indicate NBER recession periods.

Source: Financial Accounts of the United States, December 10, 2015.

Domestic FABS issuance, on the other hand, continued at a robust pace through the 2000s until 2008:Q2 when the outstanding amount of domestic FABS peaked at $140 billion. Domestic FABS then contracted sharply in the second half of 2008 through 2009, reflecting a run on these relatively liquid liabilities triggered by the global financial crisis (see Foley-Fisher, Narajabad, and Verani, 2015; and Bao, David, and Han, 2015). Recent levels of domestic FABS have remained fairly stable at levels roughly equivalent to those attained in the mid-2000s.

Measuring funding agreements and FABS in the Financial Accounts

Prior to the December 2015 release of the Financial Accounts, our measurement of funding agreements was constrained by source data for the life insurance sector that did not allow us to separate funding agreements that back FABS from similar deposit-type contracts that back pension entitlements (such as guaranteed investment contracts). As a result of this data limitation, we categorized all such deposit-type contracts--including those that serve as collateral for FABS--as "pension entitlements."3 Beginning with the December 2015 release, the new data on FABS allow us to separate those funding agreements that back FABS from the deposit contracts that back pension entitlements. We also make related adjustments to the Financial Accounts to reflect the fact that funding agreements backing FABS are assets of the ABS sector or the foreign sector, depending on whether they are held by domestic or foreign SPEs.

Specifically, domestic SPEs' funding agreement purchases are shown as a new identified miscellaneous asset on the issuers of ABS sector tables, such as table L.126 in the Financial Accounts. An abbreviated version of this table is shown as Table 1 below. As a result of the new asset in line 5, total financial assets for the ABS sector (line 1) are higher by the amount of the funding agreements shown in line 5, and total liabilities, line 6, are also higher by the same amount, reflecting the accounting for the sector's domestically issued FABS.4

| Table 1.5 L.126 Issuers of Asset-Backed Securities (ABS) - Abbreviated |

|---|

| 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | |||

|---|---|---|---|---|---|---|---|---|---|---|

| 1 | FL674090005 | Total financial assets | 4641 | 4223.2 | 3377.9 | 2314.3 | 2059 | 1839 | 1543.6 | 1453.2 |

| 2 | FL674022005 | Debt securites | 435.5 | 395.9 | 153.4 | 43.7 | 29.5 | 23.7 | 24.4 | 29.9 |

| 3 | FL674023005 | Loans | 3966.3 | 3610.4 | 3075.1 | 2140.4 | 1912 | 1704.6 | 1422.3 | 1321.6 |

| 4 | FL673070003 | Trade credit | 111.7 | 95.5 | 61.3 | 51.8 | 47.6 | 41.2 | 35.7 | 31.3 |

| 5 | FL673090543 | Miscellaneous assets (funding agreements) (1) | 127.5 | 121.3 | 88.1 | 78.4 | 70 | 69.6 | 61.1 | 70.4 |

| 6 | FL674122005 | Total liabilities | 4644.1 | 4225.9 | 3380.2 | 2314.3 | 2059 | 1839 | 1543.6 | 1453.2 |

| 7 | FL674122005 | Debt securities | 4644.1 | 4225.9 | 3380.2 | 2314.3 | 2059 | 1839 | 1543.6 | 1453.2 |

| 8 | FL673169105 | Commercial paper | 643.1 | 559.3 | 293.1 | 120.2 | 96 | 87 | 79.9 | 64.8 |

| 9 | FL673163005 | Corporate bonds (net) | 4001 | 3666.6 | 3087.2 | 2194.1 | 1963 | 1752 | 1463.7 | 1388.4 |

(1) Funding agreements with life insurance companies. Return to text.

In contrast to the effect on the domestic ABS table, our new measures of the FABS activities of foreign SPEs do not result in revisions to the rest of the world sector table (F.132 and L.132, not shown), because these transactions were already captured in the Financial Accounts source data. Note that foreign SPEs' purchases of funding agreements from U.S. life insurance companies are a component of foreign direct investment in the U.S.6 Any FABS issued by these foreign SPEs that are purchased by U.S. residents are included as part of the debt securities liabilities of the rest of the world sector. FABS issued by foreign SPEs and purchased by foreign residents are not included in the Financial Accounts.

Our new treatment of funding agreements backing securities resulted in changes to the life insurance sector table (L.116), shown in abbreviated form as table 2 below.7 As noted above, prior to the December 2015 release of the Financial Accounts, these funding agreements were included with pension entitlements liabilities, line 15, along with all other deposit-type contracts.8 The new treatment lowers pension entitlements by the amount of funding agreements purchased by both domestic and foreign SPEs.9 Domestic SPEs' funding agreement purchases are now shown as a separately identified miscellaneous liability category, "funding agreements backing securities," line 20 of Table 2, while those purchased by foreign SPEs are included as part of foreign direct investment in the U.S., line 17 (as they were before the accounting change).10

| Table 2. L.116 Life Insurance Companies - Abbreviated |

|---|

| 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | |||

|---|---|---|---|---|---|---|---|---|---|---|

| 1 | FL544090005 | Total financial assets | 4949.7 | 4514.4 | 4823.9 | 5167.8 | 5340.1 | 5614.7 | 5977.3 | 6227.1 |

| 2 | FL543020005 | Checkable deposits and currency | 58.3 | 82.8 | 50.7 | 51.7 | 53.7 | 56.4 | 47.2 | 50.8 |

| 3 | FL543034073 | Money market fund shares | 21.6 | 39.2 | 33.7 | 21 | 28.8 | 27.5 | 21.6 | 27.7 |

| 4 | FL542051073 | Security repurchase agreements | 2.7 | 8 | 10.2 | 10.9 | 6.1 | 8.2 | 2.9 | 3.4 |

| 5 | FL544022005 | Debt securities | 2399.2 | 2374.3 | 2555.6 | 2716 | 2818.5 | 2879.1 | 2934.2 | 3004.3 |

| 6 | FL544023005 | Loans | 472 | 508.5 | 467.1 | 458.2 | 481.1 | 494.8 | 517.1 | 546.6 |

| 7 | LM543064105 | Corporate equities | 1464.6 | 1001.7 | 1208.5 | 1371.6 | 1355.5 | 1502.7 | 1743.4 | 1798.4 |

| 8 | LM543064205 | Mutual fund shares | 188.4 | 121 | 140.8 | 186.7 | 184.8 | 201.7 | 235.8 | 246.4 |

| 9 | FL543092073 | U.S. direct investment abroad | 25.6 | 25 | 28.9 | 46.3 | 54.2 | 69.1 | 72.2 | 72.8 |

| 10 | FL543090005 | Miscellaneous assets | 317.3 | 354 | 328.7 | 305.6 | 357.4 | 375.2 | 403 | 476.6 |

| 11 | FL544190005 | Total liabilities | 4661.7 | 4265 | 4532.3 | 4844.3 | 5002.2 | 5248.8 | 5602.8 | 5828.1 |

| 12 | FL542151073 | Security repurchase agreements | 20.2 | 12.9 | 12.4 | 10.3 | 12.1 | 14.4 | 20.9 | 21.9 |

| 13 | FL543169373 | Loans (other loans and advances) | 28.7 | 54.9 | 48.3 | 45.1 | 46.8 | 51.6 | 59.4 | 71.8 |

| 14 | FL543140005 | Life insurance reserves | 1156.1 | 1133.4 | 1194.5 | 1229.9 | 1302.3 | 1309 | 1366.3 | 1426.1 |

| 15 | FL543150005 | Pension entitlements | 2102 | 1848.9 | 1994.7 | 2205.8 | 2256.2 | 2442.9 | 2716.9 | 2809.8 |

| 16 | FL543178073 | Taxes payable (net) | -4.7 | -24.4 | -31.4 | -28.8 | -23.6 | -28.3 | -30.5 | -32.4 |

| 17 | FL543192073 | Foreign direct investment in U.S. | 68.7 | 60.3 | 69.4 | 84.3 | 103.6 | 105.3 | 88.1 | 101.4 |

| 18 | FL543190005 | Miscellaneous liabilities | 1290.7 | 1178.9 | 1244.3 | 1297.8 | 1304.7 | 1353.9 | 1381.8 | 1429.6 |

| 19 | FL543194733 | Investment by parent companies | 43.7 | 31.2 | 40.5 | 62.7 | 72 | 17.2 | 10.7 | 11.5 |

| 20 | FL673090543 | Funding agreements backing securities (1) | 127.5 | 121.3 | 88.1 | 78.4 | 70 | 69.6 | 61.1 | 70.4 |

| 21 | FL543195005 | Other reserves | 247.6 | 265.2 | 273.6 | 290.7 | 305.5 | 303.7 | 304.2 | 310 |

| 22 | FL593095005 | Unallocated insurance contracts | 587.6 | 448.9 | 587 | 617.5 | 623.4 | 640 | 655.7 | 667.8 |

| 23 | FL543193005 | Other | 284.2 | 312.3 | 255.1 | 248.4 | 233.8 | 323.4 | 350.1 | 370 |

(1) Equal to funding agreement-backed securities (FABS) issued by domestic issuers of asset-backed securities. Return to text.

Future enhancements to FABS data

In addition to the domestic and foreign FABS data that are now included in the Financial Accounts, Federal Reserve Board staff also anticipate publishing more detailed and higher frequency FABS data as part of the Enhanced Financial Accounts initiative in the coming months.11 When those data are released, an accompanying FEDS Note will provide additional information on different types of FABS and the role of FABS in the recent financial crisis.

References:

Bao, Jack, Josh David, and Song Han (2015). "The Runnables," FEDS Notes 2015-09-03. Board of Governors of the Federal Reserve System (U.S.).

Foley-Fisher, Nathan C., Borghan Narajabad, and Stephane H. Verani (2015). "Self-fulfilling Runs: Evidence from the U.S. Life Insurance Industry," Finance and Economics Discussion Series 2015-032. Board of Governors of the Federal Reserve System (U.S).

Gallin, Joshua and Paul Smith (2014). "Enhanced Financial Accounts," FEDS Notes 2014-08-01. Board of Governors of the Federal Reserve System (U.S.).

1. The views expressed herein are those of the authors and do not necessarily reflect those of the Federal Reserve Board or its staff. We thank Marco Cagetti, Paul Smith, and Stephane Verani for their helpful comments. Return to text

2. This change to the accounting for funding agreement-backed securities in the Financial Accounts is made possible by newly available Federal Reserve Board staff estimates of the outstanding amount of FABS based on data collected from Bloomberg Finance LP and Moody's ABCP Program Index. See Foley-Fisher, Narajabad, and Verani (2015) for additional information on the construction of the dataset. Return to text

3. Some pension entitlements liabilities of the life insurance sector, including certain funding agreements, are held as unallocated insurance contract assets of the pension sectors, while others, such as individual annuities, are directly held assets of households Return to text

4. While FABs can be issued as both bonds and commercial paper (FABCP), only the corporate bond line is revised up by this change because the commercial paper data for the ABS sector already included FABCP issued domestically. Return to text

5. The first column shows the series mnemonics associated with each displayed Financial Accounts series. These mnemonics can be used to locate series for download in the Federal Reserve Board's Data Download Program (DDP). Return to text

6. Although funding agreements purchased by foreign SPEs are not shown separately on the rest of the world sector tables in the Financial Accounts, a separate time series is available for download through the Federal Reserve Board's DDP as series FL263090545.Q. Return to text

7. While not shown on tables in the Financial Accounts, a separate time series for all funding agreements sold by life insurance companies to SPEs is available for download through the Federal Reserve Board's DDP as series FL543190543.Q. Return to text

8. In addition to removing funding agreements purchased by SPEs from pension entitlements, we also removed funding agreements purchased by the Federal Home Loan Banks (FHLB). The FHLB funding agreements were already separately identified in the Financial Accounts FHLB advances (line 13 of table 3). This correction lowered pension entitlements and raised miscellaneous liabilities, the residual liability category for the life-insurance sector. Return to text

9. The exclusion of the funding agreements that back FABS from the pension entitlements liabilities of the life insurance sector also reduces household sector assets by lowering their pension entitlement holdings. However, the decline in household assets due to lower pension entitlements is partially offset by an increase in household sector holdings of corporate bonds stemming from the new domestic FABS issuance. On net, the new accounting for FABS resulted in a downward revision to household net worth that is equal to the value of foreign FABS outstanding from 1997:Q3 onward. Return to text

10. In addition to publishing the Financial Accounts, the Federal Reserve Board also prepares other data submissions to international statistical organizations based on the reporting guidelines from the System of National Accounts (2008 SNA). In accordance with the SNA guidelines, funding agreements purchased by domestic SPEs are recorded in the "currency and deposits" instrument category for these international data submissions rather than in miscellaneous claims as in the Financial Accounts. Return to text

11. See Gallin and Smith (2014) for additional information on the Enhanced Financial Accounts initiative. Return to text

Please cite this note as:

Holmquist, Elizabeth B., and Maria G. Perozek (2016). "Funding Agreement-Backed Securities in the Financial Accounts of the United States," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, March 3, 2016, http://dx.doi.org/10.17016/2380-7172.1696.

Disclaimer: FEDS Notes are articles in which Board economists offer their own views and present analysis on a range of topics in economics and finance. These articles are shorter and less technically oriented than FEDS Working Papers.