November 14, 2014

Monetary Policy Accommodation, Risk-Taking, and Spillovers

At the Global Research Forum on International Macroeconomics and Finance, Washington, D.C.

Our panel's topic--"Monetary Policy Spillovers and Cooperation in a Global Economy"--is surely a timely one. I will offer brief introductory thoughts and then discuss some recent research by Federal Reserve Board economists that has bearing on these matters.1

The Federal Reserve's monetary policy is motivated by the dual mandate, which calls upon us to achieve stable prices and maximum sustainable employment. While these objectives are stated as domestic concerns, as a practical matter, economic and financial developments around the world can have significant effects on our own economy and vice versa. Thus, the pursuit of our mandate requires that we understand and incorporate into our policy decision-making the anticipated effects of these interconnections. And the dollar's role as the world's primary reserve, transaction, and funding currency requires us to consider global developments to help ensure our own financial stability.

Since the financial crisis, the Federal Reserve has pursued a highly accommodative monetary policy, which has had important effects on asset prices and global investment flows. With unconventional tools, the scale and scope of these effects were difficult to predict ex ante. Nor is it possible to predict with confidence how markets will react day to day as policy returns to normal. The Federal Open Market Committee (FOMC) has gone to great lengths to provide transparency about its policy intentions. Yet, since Chairman Bernanke first discussed the end of the asset purchase program in mid-2013, volatility has surprised both on the upside (the "taper tantrum") and on the downside (the actual taper and the low volatility throughout most of 2014). In my view, while market volatility will continue to ebb and flow, these fluctuations are not likely to have important implications for policy. The path of policy will depend on the progress of the economy toward fulfilment of the dual mandate.

Overall, accommodative monetary policy seems to have provided significant support for U.S. growth. And, of course, a strong U.S. economy contributes to strong growth around the globe, particularly in the emerging market economies (EMEs). But what of the so-called spillovers in the form of flows into, and out of, EMEs, whose financial sectors are small compared with global investment flows? Such spillovers could merely reflect investor responses to changing differentials between rates of return abroad and in the United States. But these spillovers could also reflect shifts in investor preferences for risk.

By design, accommodative monetary policy--whether conventional or unconventional--supports economic activity in part by creating incentives for investors to take more risk. Such risk-taking can show up in domestic financial markets, in the international investments of U.S. investors, and even, ultimately, in general risk attitudes toward foreign financial markets. Distinguishing between appropriate and excessive risk-taking is difficult, however.

I now turn to some recent research on whether there has been an increase in the riskiness of our investments abroad and whether such increases might be traced to the current low-interest rate environment. Many studies of the pre-crisis period document the pro-cyclical nature of bank lending and leverage, and the buildup of risk-taking and leverage by banks.2 It is much harder to find evidence that low interest rates have led to increased post-crisis risk-taking by U.S. banks. Growth in overall lending by U.S. banks has been modest at best. However, some pockets of increased risk-taking by banks and other investors are observable in domestic markets, such as leveraged loans. And on the international front, there has been a notable increase in syndicated loan originations.

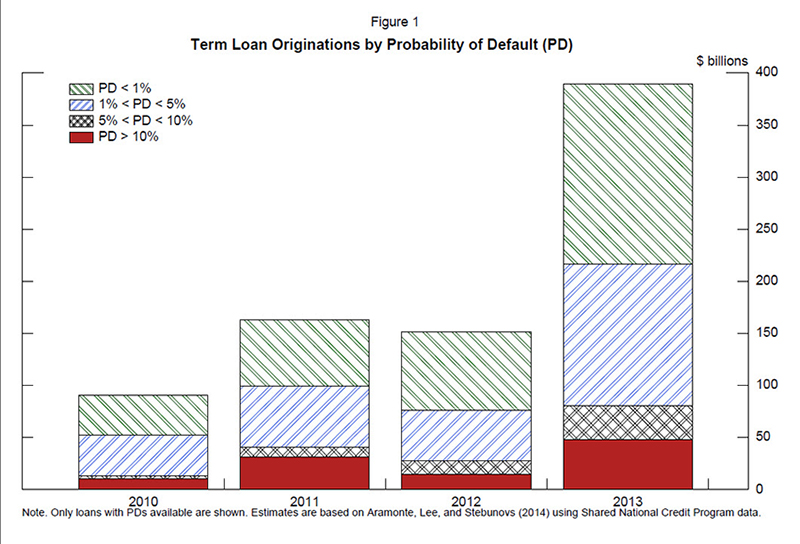

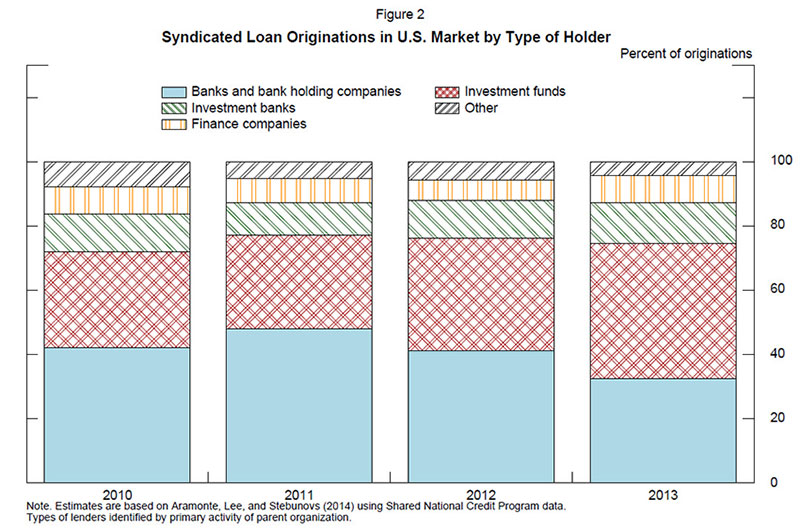

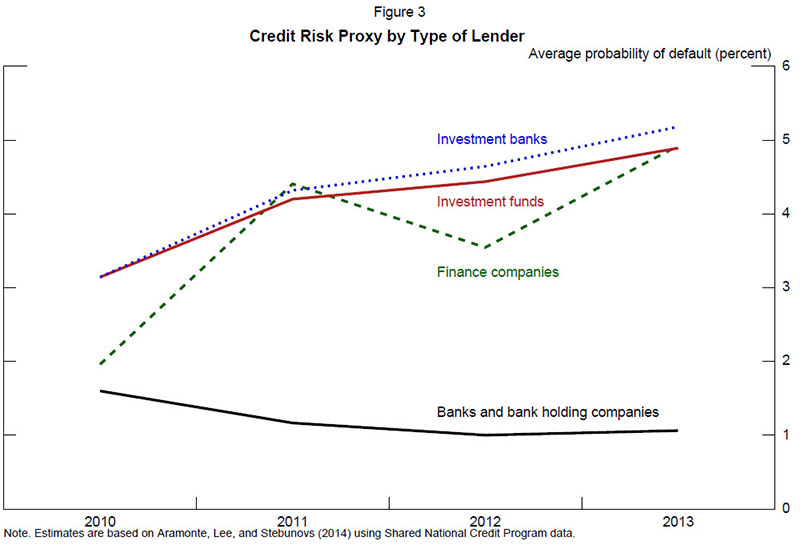

Recent research by Board staff, using a database of loans primarily to U.S. borrowers but also to some foreign borrowers, suggests that lenders have indeed originated an increased number of risky syndicated loans post-crisis, based on the assessed probability of default as reported to bank supervisors (figure 1).3 Regression results confirm that the average probability of default is significantly inversely related to U.S. long-term interest rates. This increase in riskiness of syndicated loans post-crisis has been accompanied by a shift in the composition of loan holders: An increasing share is now held not by banks but by hedge, pension, and other investment funds (figure 2). These nonbank investors also tend to hold loans with higher average credit risk (figure 3). These data suggest that a tougher regulatory environment may have made U.S.-based bank originators unable or unwilling to hold risky loans on their balance sheets. Related work by the same researchers, using a database with more-extensive coverage of loans to foreign borrowers, shows a similar pattern of increased risky loan underwriting by international lenders, an increase that is also significantly inversely related to U.S. interest rates. Together, these results suggest a potential spillover from accommodative U.S. monetary policy through increased risk-taking in syndicated loans globally, although preliminary results also indicate that investors still require extra return for this extra risk.

{kind=link}

{kind=link}

{kind=link}

Another area in which to look for links between low interest rates and risk-taking is in cross-border securities purchases. The role of low interest rates in advanced economies in encouraging capital flows to EMEs where returns are higher has been a familiar theme.4 And recent studies have found that asset prices in EMEs do respond systematically to U.S. monetary policy shocks.5

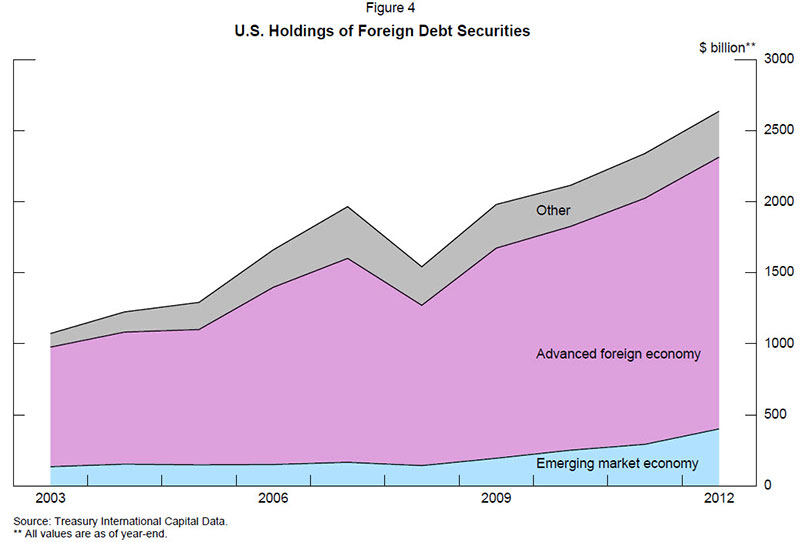

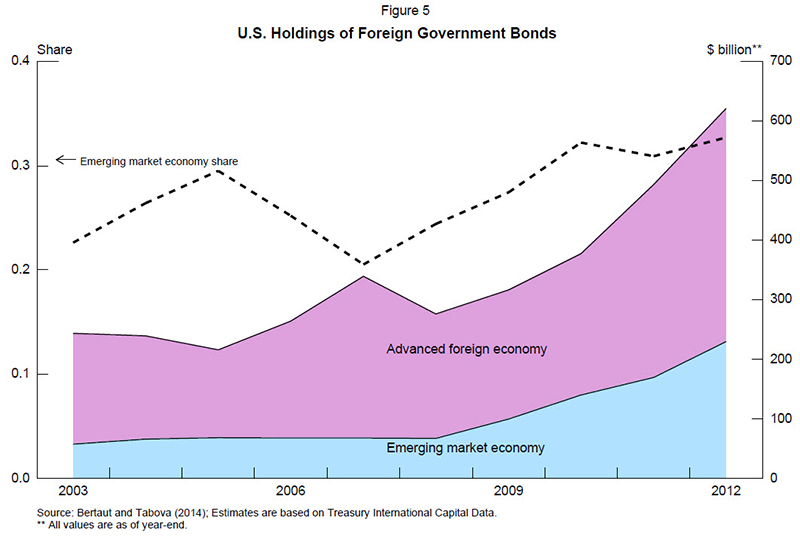

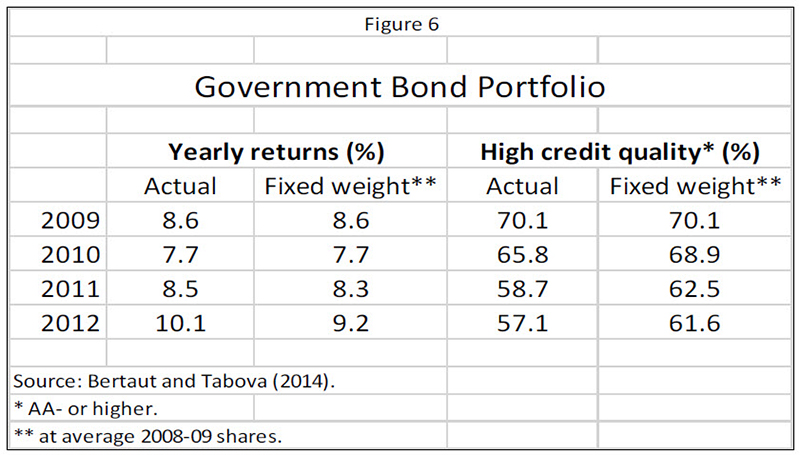

For evidence of increased risk-taking in cross-border investment, let's look at the composition of U.S. investors' foreign bond portfolios. Although emerging market bonds remain a relatively small proportion of the aggregate U.S. cross-border bond portfolio (figure 4), within foreign government bonds, U.S. investors have modestly shifted their portfolio shares toward higher-yielding bonds of emerging market sovereigns (figure 5). Ex post, these portfolio reallocations delivered a higher return to U.S. investors on this part of their portfolio relative to what they would have received if they had left portfolio compositions unchanged at the average shares in 2008 and 2009, but at a cost to the portfolio's credit quality (figure 6). Regression results confirm that in choosing among foreign government bonds, U.S. investors have put more weight on returns since the crisis.6

{kind=link}

{kind=link}

{kind=link}

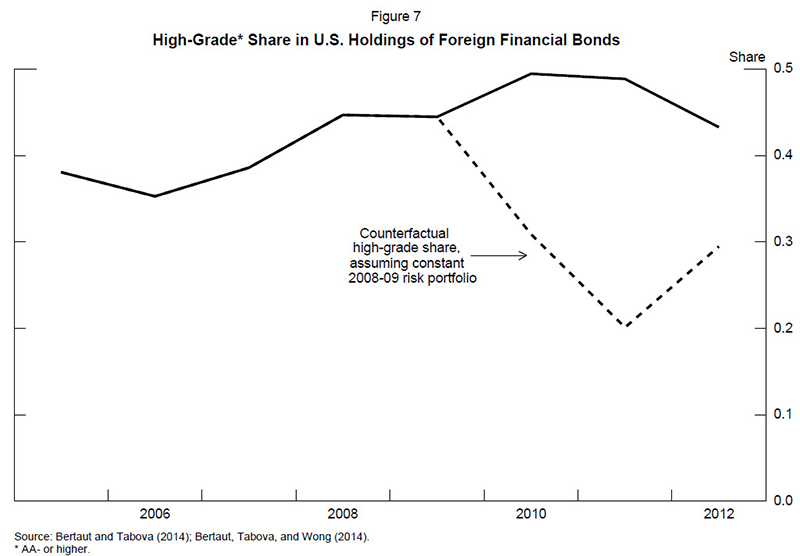

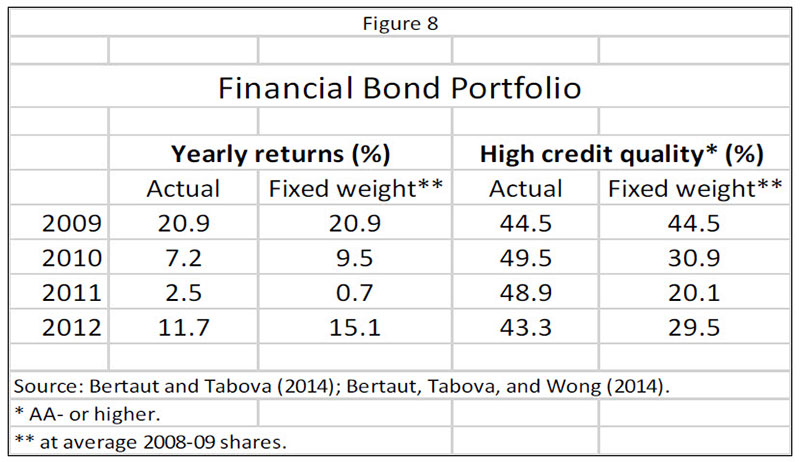

But search for higher returns has not been the only motivation for international investors post-crisis: Demand for liquid high-grade "safe" or money-like assets has also increased from foreign official investors for investment of foreign exchange reserves, from pension funds and other institutions who face portfolio allocation constraints or regulatory requirements, and from investment strategies requiring cash-like assets for margining and other collateral purposes. Some shift to safe assets is also seen in U.S. portfolios: U.S. investors actively rebalanced their holdings of foreign financial sector bonds toward those with higher credit ratings, but at some cost in returns (figure 7; figure 8).7

{kind=link}

{kind=link}

Taken together, developments in U.S. bond portfolios do not indicate a worrisome pickup in risk-taking in external investments. But it is important to recognize that portfolio reallocations that seem relatively small for U.S. investors can loom large from the perspective of the foreign recipients of these flows. At roughly $400 billion at the end of 2012, emerging market bonds accounted for a tiny fraction of the roughly $25 trillion in bonds held by U.S. investors. But to the recipient countries, these holdings can account for a large fraction of their bond markets. Even relatively small changes in these U.S. holdings can generate large asset price responses, as was certainly the case in the summer of 2013. Likewise, a reassessment of risk-return tradeoffs could disrupt financing for projects that are dependent on the willingness of investors to participate in global syndicated loan markets.

We take the consequences of such spillovers seriously, and the Federal Reserve is intent on communicating its policy intentions as clearly as possible in order to reduce the likelihood of future disruptions to markets. We will continue to monitor investor behavior closely, both domestically and internationally.

1. The views expressed herein are my own and not necessarily those of other FOMC participants. Return to text

2. See Tobias Adrian and Hyun Song Shin (2010), "Liquidity and Leverage," Journal of Financial Intermediation, vol. 19 (July), pp. 418-37; Valentina Bruno and Hyun Song Shin (2013), "Capital Flows, Cross-Border Banking, and Global Liquidity," NBER Working Paper Series 19038 (Cambridge, Mass.: National Bureau of Economic Research, May); and Valentina Bruno and Hyun Song Shin (2013), "Capital Flows and the Risk-Taking Channel of Monetary Policy," NBER Working Paper Series 18942 (Cambridge, Mass.: National Bureau of Economic Research, April). Return to text

3. See Sirio Aramonte, Seung Jung Lee, and Viktors Stebunovs (2014), "Risk-Taking and Low Longer-Term Interest Rates: Evidence from the U.S. Syndicated Loan Market (PDF)," paper presented at the 14th Annual Bank Research Conference sponsored by the Federal Deposit Insurance Corporation's Center for Financial Research and the Journal of Financial Services Research, held in Arlington, Va., September 18-19, and Seung Jung Lee, Lucy Qian Liu, and Viktors Stebunovs (2014), "Risk-Taking and Interest Rates: Evidence from Decades in the Global Syndicated Loan Market," unpublished paper, Board of Governors of the Federal Reserve System. Return to text

4. See Jerome H. Powell (2013), "Advanced Economy Monetary Policy and Emerging Market Economies," speech delivered at the Federal Reserve Bank of San Francisco 2013 Asia Economic Policy Conference, San Francisco, November 4. Return to text

5. See Shaghil Ahmed and Andrei Zlate (2013), "Capital Flows to Emerging Market Economies: A Brave New World?" International Finance Discussion Papers 1081 (Washington: Board of Governors of the Federal Reserve System, June); David Bowman, Juan M. Londono, and Horacio Sapriza (2014), "U.S. Unconventional Monetary Policy and Transmission to Emerging Market Economies," International Finance Discussion Papers 1109 (Washington: Board of Governors of the Federal Reserve System, June); and Marcel Fratzscher, Marco Lo Duca, and Roland Straub (2013), "On the International Spillovers of U.S. Quantitative Easing (PDF)," ECB Working Paper Series 1557 (Frankfurt, Germany: European Central Bank, June). Return to text

6. See Carol Bertaut and Alexandra Tabova (2014), "Reach for Yield versus Search for Safety," unpublished paper, Board of Governors of the Federal Reserve System. Return to text

7. See Carol Bertaut, Alexandra Tabova, and Vivian Wong (2014), "The Replacement of Safe Assets: Evidence from the U.S. Bond Portfolio (PDF)," International Finance Discussion Papers 1123 (Washington: Board of Governors of the Federal Reserve System, October). Return to text