Consumer & Community Context

Meeting Small-Dollar Consumer Credit Needs: Old and New Choices

This issue of Consumer & Community Context explores the use of small-dollar credit. It reviews traditional and new products offered by banks and nonbanks alike and considers how new data sources and technologies are used to offer these products to consumers. The discussion concludes with a look at whether and how these products may be serving consumers' needs.1

Thank you for your interest in Consumer & Community Context, a publication of the Federal Reserve Board's Division of Consumer and Community Affairs. To subscribe to future issues, email [email protected]. For past issues, visit https://www.federalreserve.gov/publications/consumer-community-context.htm.

What Is Small-Dollar Credit—and Why Do Consumers Need It?

Large loans, like mortgages and auto financing—used a few times in a lifetime—garner the most attention when it comes to consumer finance products. Yet for many consumers, short-term, small-dollar credit helps them manage day-to-day living expenses and keeps them financially afloat, particularly in times of rising prices and economic uncertainty. Consumers can use these products, which are typically offered in amounts less than $1,000, to cope with fluctuating incomes or unanticipated expenses.

The Federal Reserve's Survey of Household Economics and Decisionmaking (SHED) provides a sense of why consumers may utilize small-dollar credit.2 The SHED annually reports on the share of adults who say they would not cover a small emergency expense using cash, savings, or a credit card paid off at the next statement. The report also measures the share of adults who are unable to pay their current month's bills in full. While these metrics have shown overall improvement since the start of the survey in 2013, 37 percent of adults reported that they would have difficulty paying for a $400 emergency in 2022 (figure 1).3

Figure 1. Would not cover a $400 emergency expense completely using cash or its equivalent (by year)

Accessible Version | Return to text

Note: Among all adults.

Source: Survey of Household Economics and Decisionmaking (SHED).

The SHED data also suggest why some consumers may have trouble paying bills. While only 14 percent of consumers with "stable income" struggled to pay bills in full in the prior year, this was true of 24 percent of those whose income varied "occasionally" from month to month and 41 percent of those whose income varied "quite often." Also, the lower the income, the more closely linked these income fluctuations are to having trouble paying bills in full, especially for consumers with incomes below $50,000.

Another sign of financial stress is how often consumers incur overdraft fees on their bank accounts. Banks charge these fees to cover a withdrawal if the customer's account lacks the funds to cover the transaction. Some consumers make repeated use of overdraft protection to keep payments from being declined.4 While industry stakeholders point out that overdraft protection provides a valuable service by ensuring that payments clear, some consumer advocates assert that this is not a sustainable way for consumers who rely repeatedly on overdraft protection to meet recurring short-term credit needs.

How Do Consumers Qualify for Small-Dollar Credit?

Generally, lenders require consumers who obtain short-term credit to have a bank account in order to ensure access to consumers' funds for repayment priority. Fortunately, the share of the adult population without a bank account is quite low—6 percent in 2019, down from 14 percent in 1986—and continuing to improve.5 Still, there are differences in bank account ownership by race and ethnicity. One source shows that the share of Black adults without a bank account exceeded five times the share for White adults in 2021 (11 percent compared to 2 percent, respectively).6

In addition, lenders must assess borrowers' likelihood to repay before extending new or additional credit—typically by checking their credit score. Based on a typical range of 300 to 850, a higher credit score means to a lender that a borrower is lower risk and more likely to make on-time payments. However, there are an estimated 49 million people (nearly one in five adults) with no credit score, meaning they have no credit history in this country or have gone six-plus months without using credit. Another 59 million people have a credit score below 660, a level often classified as subprime.7 If borrowers' creditworthiness is determined primarily by a credit score, many banks' lending guidelines may categorize these applicants as too risky, leading to an increase in the cost of credit or denial of credit altogether.

What Are Some Typical Small-Dollar Credit Products?

Small-dollar credit products are offered by banks, as well as other types of finance providers, and are packaged in a variety of ways. These products range from very short-term sources of funds—often less than one week—to open-ended lines of credit, such as a credit card. Some lenders may offer these products only to customers considered low risk, while other lenders make their products available more broadly.

Traditionally, the least risky way for banks to offer small-dollar credit to borrowers with lower credit scores is through a secured credit card, in which the consumer puts down money upfront, say $250 or $500, and can charge up to that amount on the card. While only about 4 percent of all credit cards originated in 2021 were secured cards, over two-thirds of secured card recipients were consumers with very low credit scores or no score at all. This compares with just 7 percent of unsecured card originations going to consumers with very low credit scores or none at all. Thus, a disproportionate share of borrowers in these categories prepaid for their opportunity to obtain credit.8 For those without a credit score, using a secured card for six months can be enough for credit bureaus to calculate a score, opening the door to further opportunities to obtain credit.9

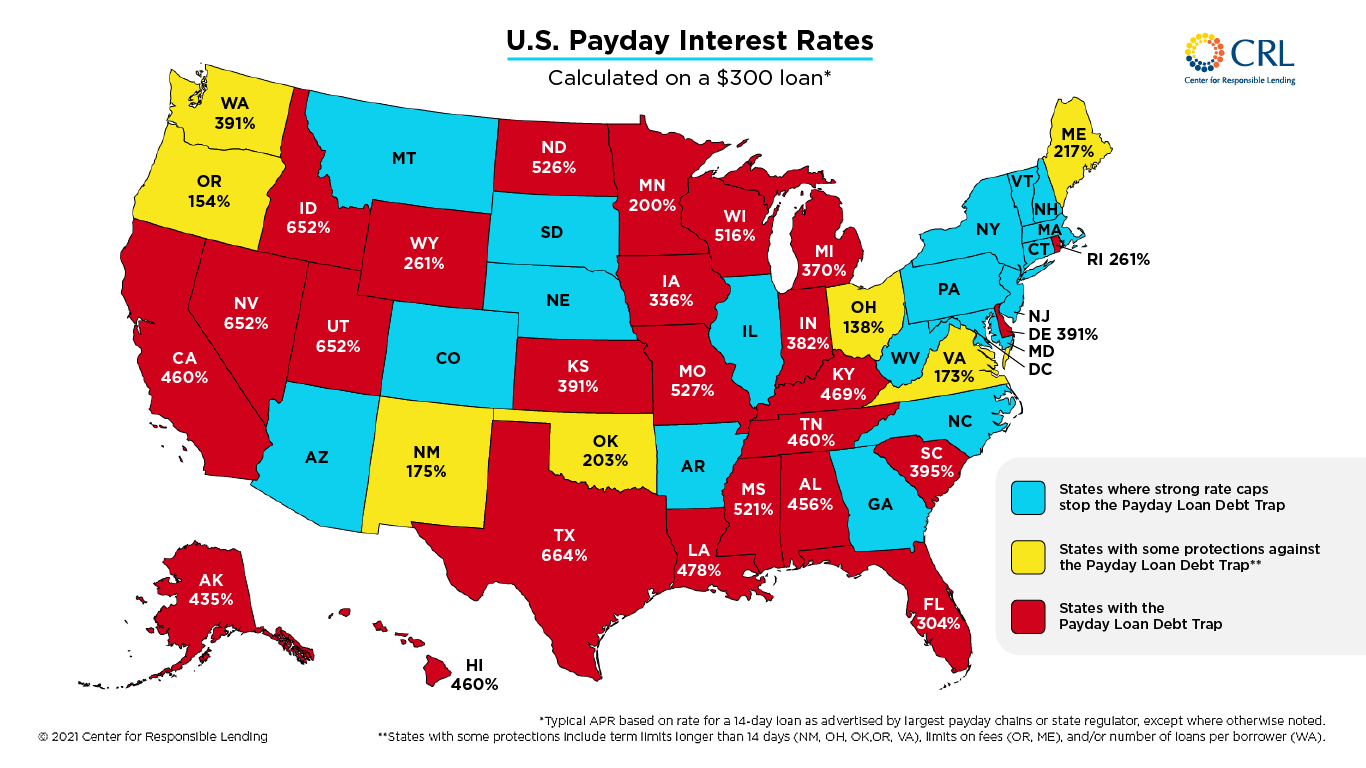

Some consumers turn to lenders outside of the banking system, such as payday lenders, though most payday lenders will only extend loans to customers who have bank accounts. Payday loans are small, unsecured loans with payments usually due in full on the borrower's next regularly scheduled paycheck, which is typically two weeks or less. Payday lenders operate both in brick-and-mortar facilities as well as online.10 About one-third of states have placed limits on the rates borrowers pay for these loans, while in the remaining states, consumers pay fees of roughly $10 to $30 per $100 borrowed. Proponents of payday loans argue that high costs are a necessary tradeoff given their convenience and accessibility, especially for those who may be unable to obtain funds from a traditional source.

A drawback of payday loans is the mismatch that can arise between the loan's terms and a borrower's needs. Research finds that many borrowers of payday loans face ongoing financial challenges and may struggle to fully repay their loans in just one to two weeks.11 In response, some consumers roll over loans as they become due or take out new ones to make ends meet. With these rollovers, combined with high interest rates and additional fees, they find themselves caught in a debt cycle. While not every borrower will get trapped, three-quarters of the fees received by payday lenders come from borrowers taking out 10 or more loans a year.12 Consumer advocates have raised the concern that the business model relies on borrowers who are unable to use the product as it is advertised.

What's New in the Small-Dollar Credit Market?

In recent years, nonbank financial technology ("fintech") companies have emerged, aiming to provide consumers with short-term credit through offerings like credit cards, installment loans, or debt refinancing. To qualify applicants, some fintech firms go beyond credit scores to consider applicants' financial information, such as deposit account records and rent payments, or other factors like education levels or cellphone analytics (table 1). Fintech lenders maintain that this use of "alternative data" can qualify borrowers who may not otherwise have access to small-dollar credit. There is evidence to suggest that some use of alternative data has led to higher approval rates and lower interest rates for low-score applicants. However, there are concerns about what types of alternative data, especially certain nonfinancial information, are fair to use. This is particularly the case if these considerations are not disclosed to the borrower and are highly correlated with classes protected by fair lending laws, such as race, ethnicity, sex or gender, or national origin.13

Table 1. Examples of alternative data types

| Financial or payment-related data | Nonfinancial data |

|---|---|

| Data on inflows and outflows from checking accounts ("cash flow"), such as paycheck deposits and bill payments | Applicant's job and/or industry, highest education level attained, and institution attended |

| Rent, utility, and telecom payments | Cellphone usage analytics, such as the type of phone the borrower owns |

| Underlying credit report history (details on payments and balances) | Types of goods or services purchased |

Perhaps spurred by this competition, some large banks have waded into the market in recent years to offer some new small-dollar credit products. These are typically installment loans with standardized features, including lower costs, flat fees, and spread-out payments (i.e., a customer may pay a $15 fee to borrow $300, repaid over four installments, a fraction of the cost to borrow the same amount in a single-payment payday loan).14 Meanwhile, some of these large banks are addressing the demand for small-dollar credit by introducing new line-of-credit products in which they agree to a preset borrowing limit that customers can tap into at any time. Overall, these types of products have the potential to meet the short-term credit needs of many borrowers with more manageable costs and terms than other options.15

Factors other than competition from nonbanks may be spurring banks to offer these products as well. First, banks offer these products only to their own customers, and much of the approval process is automated and handled online, making them economical for banks to offer. Second, they provide the ability to tap into, and efficiently process, large amounts of data on the inflows and outflows of money ("cash flow data") from their customers' accounts. Banks can then use this information—either exclusively or in conjunction with credit scores—to weigh risk and decide whether to approve credit to borrowers. A few simple metrics from depositors' checking accounts, such as the age of the account, the balance, the trend of the balance, the presence of regular automatic deposits, and the absence of negative balances, are enough for some banks and fintech firms to make a safe, informed lending decision.

Are These Emerging Products Expanding the Availability of Small-Dollar Credit?

Without detailed information on personal characteristics of borrowers, their credit scores, and other factors, it is difficult to determine whether new credit products are expanding the availability and affordability of small-dollar credit. It is reasonable to assume, given their target audiences, that many of these products specifically serve consumers with low or no credit scores—categories of consumers who, as noted above, have a greater need for, but fewer options to obtain, small-dollar credit. Indeed, some banks that recently entered this space are not considering credit scores and are underwriting credit based solely on cash flow data.

On the other hand, new products and approval methods may not always expand the ranks of consumers who are approved for credit. This is in part because some fintech firms' business models focus on refinancing the debt of consumers who already have credit. Meanwhile, some banks approve fewer than half of their customers who apply for their short-term credit products.

Many consumers are likely to continue to turn to small-dollar credit to manage their household finances. As described here, more product choices are available to consumers than ever before, and new products will likely appear in the marketplace. What will matter even more than the sheer number of available products, however, is whether these options are more accessible, affordable, and safer for both small-dollar credit providers and consumers than what came before.

Footnotes

The views expressed here are those of the authors and do not necessarily reflect the position of the Federal Reserve Board or the Federal Reserve System.

1. The staff contact for this issue is Dan Gorin and for the Consumer & Community Context series is John Rodier. Kim Wilson and Alicia Lloro provided research and analysis on this topic. Barbara Lipman and Pamela Wilson provided editorial support. Return to text

2. Survey of Household Economics and Decisionmaking, https://www.federalreserve.gov/consumerscommunities/shed.htm. Return to text

3. Federal Reserve Board, Economic Well-Being of U.S. Households in 2022 (May 2023), https://www.federalreserve.gov/publications/files/2022-report-economic-well-being-us-households-202305.pdf, page 32. Return to text

4. Bankrate.com reported that the average overdraft fee in 2022 was $29.80, down slightly from the record high average of $33.58 in 2021. See https://www.bankrate.com/banking/checking/checking-account-survey/. For more details on the prevalence and use of overdraft fees, see this 2022 GAO report: https://www.gao.gov/assets/730/722124.pdf or this 2017 Pew brief: https://www.pewtrusts.org/en/research-and-analysis/issue-briefs/2017/12/overdraft-does-not-meet-the-needs-of-most-consumers. Return to text

5. Federal Reserve Board, Survey of Consumer Finances, 1989–2019, https://www.federalreserve.gov/econres/scfindex.htm. Return to text

6. 2021 FDIC National Survey of Unbanked and Underbanked Households, https://www.fdic.gov/analysis/household-survey/2021report.pdf. Return to text

7. Other ranges may be used depending on the credit provider. FICO and credit status data from Oliver Wyman, Financial Inclusion and Access to Credit, January 2022, https://images.go.experian.com/Web/ExperianInformationSolutionsInc/%7B63ec9888-37ea-405c-b39d-7492de9143ce%7D_FINALExperian_report_14_01.pdf. Return to text

8. Credit card statistics here come from Y-14 reports. These reports track credit card activity of the 16 largest banks that represent about two-thirds of all credit card activity in the United States. Return to text

9. FICO notes three requirements to be scored: (1) at least one account opened for six months or more, (2) at least one account that is reported to the credit bureaus in the prior six months, and (3) no indication that there is a deceased person tied to the credit report. See https://www.myfico.com/credit-education/faq/scores/fico-score-requirements. Return to text

10. For a geographic distribution of average payday lender fees by state, see this map from the Center for Responsible Lending: https://www.responsiblelending.org/sites/default/files/uploads/images/payday_rate_cap_map_feb2021.png. Prior to 2013, a small number of large banks offered a similar deposit advance product with fees ranging from $5 to $10 per $100 borrowed. Only one large bank is known to still offer this product and that institution has protections in place to limit rollover and the compounding of fees. Return to text

{kind=link}

11. For more details on payday lending, see this 2014 CFPB report: https://www.consumerfinance.gov/about-us/newsroom/cfpb-finds-four-out-of-five-payday-loans-are-rolled-over-or-renewed/ or this 2022 CFPB study: https://www.consumerfinance.gov/about-us/newsroom/cfpb-finds-payday-borrowers-continue-to-pay-significant-rollover-fees-despite-state-level-protections-and-payment-plans/. Return to text

12. CFPB Data Point: Payday Lending, March 2014, https://files.consumerfinance.gov/f/201403_cfpb_report_payday-lending.pdf. Return to text

13. FinRegLab: The Use of Cash-Flow Data in Underwriting Credit: Market Context and Policy Analysis, February 2020, https://finreglab.org/wp-content/uploads/2020/03/FinRegLab_Cash-Flow-Data-in-Underwriting-Credit_Market-Context-Policy-Analysis.pdf. Return to text

14. OCC Bulletin 2018-14, "Installment Lending: Core Lending Principles for Short-Term, Small-Dollar Installment Lending," https://www.occ.gov/static/rescinded-bulletins/bulletin-2018-14.pdf. This single-agency guidance was later replaced by similar interagency guidance. Pew: Fourth Major Bank Launches Small-Loan Program, https://www.pewtrusts.org/en/research-and-analysis/articles/2022/11/16/fourth-major-bank-launches-small-loan-program. Return to text

15. For further details on the preferred structures and features of these types of products, see "Interagency Lending Principles for Offering Responsible Small-Dollar Loans," May 2020, https://www.federalreserve.gov/newsevents/pressreleases/files/bcreg20200520a1.pdf. Return to text