Print

Print

Market Value Analysis: A Data-Based Approach to Understanding Urban Housing Markets

A major challenge that cities across the country face in their efforts to stabilize--and revitalize--neighborhoods is determining where and how to invest limited resources. The Market Value Analysis (MVA) approach, which provides an accurate, accessible, and in-depth portrayal of market data in urban areas, is one tool cities are using to help make decisions about resource allocation, set priorities for service delivery, and tailor intervention strategies for specific market types. The MVA approach practiced by The Reinvestment Fund (TRF) is unique in its use of cluster analysis, its spatial context (i.e., the need to not only understand what the conditions are in a given place but what they are in adjacent areas), and in its extensive field validation. Although preparing an MVA is modestly data- and labor-intensive, as the experiences of Baltimore and other cities suggest, many municipalities are finding that it is an undertaking well worth the effort.

This article provides an overview of TRF's MVA approach, discusses the process it uses to prepare an MVA and, using Baltimore as an example, highlights how the MVA approach can inform citywide strategies and decisionmaking related to neighborhood stabilization.

Overview of the MVA Approach

The MVA approach was born from former Philadelphia Mayor John Street's charge to TRF to create a data-based analysis of the city's housing market. TRF created the MVA to give public officials the basis for making informed, objective decisions about how to prioritize resources and services. By 2000, Philadelphia's population had fallen from its 1950 peak of over 2 million to just under 1.52 million.1 That population loss left Philadelphia with an estimated 30,000 vacant lots and 25,000 vacant homes, as well as 9,000 residential structures in danger of falling under their own weight.2

Many of Philadelphia's neighborhoods were scarred with decades of blight, while some showed just the beginnings of decline. Other areas manifested market strength: well-maintained homes, strong prices, a healthy mixture of residential and commercial uses, and no signs of vacancy or abandonment. Mayor Street recognized that to bring the downtown vitality to the neighborhoods, which then housed more than 95 percent of the city's population, he needed a current assessment of the relative economic health of the neighborhoods in the form of comprehensive, data-based profiles. Because city agencies did not have the data or capacity to prepare the needed profiles, Mayor Street turned to TRF to design and conduct the necessary statistical and spatial analysis. Not only would this analysis help guide the level and nature of municipal services delivered throughout the city (e.g., residential and commercial demolition, acquisition of vacant land, streetscape upgrades, housing rehabilitation), but it also would provide the basis for underwriting a $295 million bond issuance.3

Underlying the MVA is a perspective that residents of all of a city's markets are its customers--of its programs, resources, and services. Moreover, public resources are generally scarce and cannot be singularly relied upon to create a housing market where none exists. Thus, locating and building on local market strength is fundamental. Scarce public resources should be used to prepare a market for the infusion of private capital; public investment should be invested in a way that leverages private capital. Also important is the recognition that neighborhoods--the concept that many community and economic development practitioners use to describe an area--are typically not uniform districts. In fact, most neighborhoods comprise a variety of market types; therefore, governmental activity and resources should be related to the extant conditions in each of the market types, not "the neighborhood."

Since that 2001 analysis, TRF conducted two more MVAs in Philadelphia. TRF also prepared MVAs in Pittsburgh, Pennsylvania; Baltimore, Maryland; Newark and Camden, New Jersey, as well as a set of small towns throughout southern New Jersey; San Antonio, Texas; Washington, DC; Wilmington, Delaware; and most recently, Detroit, Michigan. Funding for these MVAs came from both government and philanthropy (in tandem with the public funding). In addition to their initial purposes for preparing these MVAs, many of these cities used the MVA approach as a means of targeting their federal Neighborhood Stabilization Program activities.

Preparing a Market Value Analysis

Jump to:

The MVA approach uses a variety of market indicators to analyze, validate, and understand the nature and conditions of existing housing market types throughout a city. Cities can then use this information to better target resources and services as well as tailor development and investment strategies for specific market types.

Indicators

The package of indicators for an MVA includes administrative elements and other secondary data sources. In general, these market indicators were selected because they reflect the conditions that any developer might observe when evaluating areas for investment or intervention. With some variation from city to city, the following indicators are used:

- median and variability of housing sale prices

- housing and land vacancy

- mortgage foreclosures as a percent of units (or sales)

- rate of owner occupancy

- presence of commercial land uses

- share of the rental stock that receives a subsidy

- density

Cities have wide variation in the depth and scope of their administrative databases. Some cities, like Baltimore, can provide a high-quality dataset for each indicator.

Level of Analysis

Although census tracts and census block groups both provide data by fixed geographic area, the block group--the entity into which a census tract is divided--is the most appropriate level for this analysis. Census tracts are spatially much larger than block groups and their populations range from 2,500 to 8,000 people, whereas block group populations range from only 600 to 3,000.4 Thus, the census block group is small enough that the differences that may be observed as you walk through a community can be detected, while large enough that the estimates are reasonably stable because they are based on larger numbers of data points (e.g., housing units, foreclosures, residential sale transactions).

Process

The MVA process requires acquiring and evaluating each indicator's accuracy, which is usually accomplished by preparing block group maps of each indicator. The maps are then subjected to an on-site inspection and vetted through interviews and/or focus groups with local subject-matter experts (SMEs).5

Once the variables are deemed acceptable, they are subjected to a cluster analysis, which is a statistical procedure that creates homogeneous groupings of cases (i.e., block groups). Each group shares a common constellation of characteristics. The groupings are generally designed to maximize the similarity of cases within groups and maximize the differences across groups. Indicators are put on the same scale, typically through a transformation (e.g., z-score). The cluster analysis does not require an a priori decision about what level of any indicator is more or less desirable (e.g., owner occupancy is good and rental occupancy is bad). It is the constellation of characteristics as revealed by the statistical analysis that helps to define the market categories.

The results of the cluster analysis are then mapped and subject to field inspection and SME review. Typically, the field inspection is accomplished by preparing maps and then driving throughout the city with an eye toward understanding whether the map comports with what is observed in the field. Observations focus on whether the appearance of any given market type is similar, regardless of where in the city that given market type is found. Additionally, the degree to which any changes observed from block to block are appropriately reflected on the map are also noted. Experience suggests that field validation takes anywhere from three to five (or more) days depending upon the city's size and complexity of its markets.6

TRF's experience is that the validation and modeling process is iterative. Typically, the first statistical solutions do not adequately match with field observations or the review of local SMEs, and this makes some re-modeling, re-mapping, and re-inspection necessary. Some cities have taken the added step of preparing a set of overlays of data reflecting a variety of things like (1) local assets (e.g., large employers, colleges, hospitals, transportation hubs); (2) crime hot spots; (3) social and human service need indicia; (4) history of the city's housing or infrastructure investments; and (5) demographic characteristics and changes.

The Baltimore Experience: Uncovering the Dimensions of Market Vitality and Distress

Jump to:

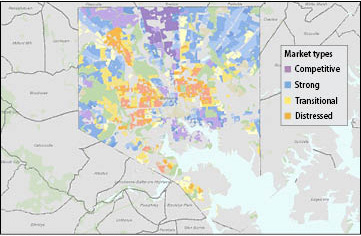

TRF completed two MVAs (2005 and 2008) for Baltimore and is now working on a third for the city.7 The 2008 MVA was based on the following indicators: (1) median sale price; (2) housing density; (3) tenure; (4) foreclosure filings as a percent of owner-occupied properties; (5) vacant lots and vacant housing; (6) percent of rental units with a subsidy; (7) mixture of commercial and residential uses; and (8) density. Representatives of Baltimore's Housing and Planning departments were the main SMEs, and those who would be responsible for implementing programs based on the MVA. The resulting 2008 Baltimore MVA is displayed in figure 1. The constellation of characteristics for each market type is displayed in table 1.

| Market | Distribution summary | Analysis variables | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Block groups | Housing units | % of city housing units | Foreclosures 2006-07 as % of all owner-occupied units | Owner-occupied housing units, % | Vacant housing notices as % of all housing units | Vacant lots as % of all parcels | Occupied single-family units as % of all units | Housing units per acre | Commercial land use area as % total block group area | Section 8 units 2008 as % of all rental units | Median 2006-07 sales price | |

| A | 12 | 7,071 | 2.40 | 0.87 | 67.42 | 0.01 | 0.00 | 98.65 | 6.22 | 2.05 | 4.10 | $615,915 |

| B | 63 | 33,584 | 11.41 | 1.98 | 51.21 | 0.92 | 0.04 | 93.90 | 19.43 | 0.36 | 1.56 | $293,598 |

| C | 30 | 16,261 | 5.52 | 3.37 | 45.19 | 2.45 | 0.48 | 91.93 | 17.19 | 18.77 | 2.22 | $244,309 |

| D | 117 | 51,865 | 17.61 | 4.50 | 58.60 | 1.69 | 0.46 | 93.91 | 11.31 | 0.00 | 8.51 | $161,447 |

| E | 72 | 37,488 | 12.73 | 4.33 | 54.30 | 1.68 | 0.25 | 93.57 | 10.86 | 4.71 | 7.55 | $153,311 |

| F | 59 | 24,700 | 8.39 | 5.45 | 50.09 | 5.72 | 0.75 | 87.54 | 14.63 | 18.79 | 16.37 | $97,409 |

| G | 118 | 45,714 | 15.53 | 5.75 | 51.93 | 6.09 | 1.01 | 87.63 | 15.52 | 0.07 | 17.37 | $80,315 |

| H | 89 | 29,374 | 9.98 | 6.53 | 34.84 | 24.01 | 5.24 | 66.85 | 15.91 | 8.50 | 11.07 | $40,409 |

| I | 85 | 25,786 | 8.76 | 6.72 | 33.40 | 27.28 | 4.91 | 63.18 | 18.56 | 0.00 | 10.30 | $36,119 |

| Block group average | 5.03 | 48.02 | 9.69 | 2.10 | 83.87 | 14.89 | 4.35 | 10.26 | $130,712 | |||

What the City's 2008 MVA Revealed

One of the 2008 MVA's key contributions to Baltimore's strategy development was the recognition of the spatial arrangement of market types:

- Stronger markets, displayed in the blue and purple ranges, can often operate as nodes of strength upon which interventions in markets that manifest early signs of blight can be based.

- Large areas of distress dictate larger-scale interventions because the degree of blighting influences is so great that minor interventions (e.g., a small number of scattered site housing rehabilitations) are not likely to promote market change.

- Yellow markets (labeled in some cities as "transitional markets") draw attention, especially when adjacent to more stable (blue) markets because, in Baltimore, they may be being undermined by high levels of financial distress as evidenced by elevated foreclosure levels. That which is destabilizing the yellow markets may threaten the blue areas.

Baltimore is also unique, compared to some other cities, in the degree to which it has made the data and results of its MVAs available to the public.8 One of Baltimore's efforts to inform the public describes the MVA as follows:

Baltimore's housing market typology was developed to assist the City strategically match available public resources to neighborhood housing market conditions; the housing market typology was a key tool used in LIVE EARN PLAY LEARN, the City's 2006 Comprehensive Master Plan. The typology informs neighborhood planning efforts by helping neighborhood residents understand the housing market forces impacting their communities. The financial and resource tools the City uses to intervene in the housing market are applied appropriately to the conditions in the neighborhoods. Some tools, such as demolition, may be necessary in distressed markets to bring about change in whole blocks yet may be applied more selectively in stable markets on properties that may lead to destabilization in the future.9How Baltimore Is Using the MVA to Aid Revitalization Efforts

Encouraging Collaborative Solutions

According to current and former officials of the City of Baltimore,10 the MVA approach is an accurate and useful diagnostic of localized market conditions. A diagnostic is not an answer, but it provides the basis for government and nongovernment experts to collaborate to create a set of solutions tailored for Baltimore. Thus, to inform local discourse and municipal action, Baltimore made its MVAs available to the public.11 The city also took steps to share the information more broadly--for example, by submitting its 2005 MVA for publication in the ESRI Map Book Gallery, a tool intended for use primarily by GIS professionals around the world.12

Informing Planning and Development

In addition, the MVA approach helped change the city's development mindset, which had previously been targeted based on level of need. As time passed and resources became increasingly scarce, MVA helped the city to understand government resources as a catalyst to be targeted where there was market strength upon which to build. As a result, targeting resources to market conditions became a critical component of the city's effort.13

That mindset was affirmed in city's comprehensive and area master plans. The first Baltimore MVA, completed in 2005, formed a critical information overlay in those plans. Planners and other government officials created a set of responses to each of the different market types and conditions.

The MVA served as the information base for multiple city agencies, nonprofit housing and community development organizations, and foundations to develop a unified set of strategies for Baltimore's neighborhoods. For example, Baltimore's Vacants to Value program, designed to encourage the rehabilitation of more than 1,000 vacant housing units across the city, had targeting and resource prescriptions tied to the MVA market conditions (the Vacants to Value program is described elsewhere in this compilation in the article by Janes and Davis).14

Additionally, Baltimore used the MVA as a measure of market demand in its cooperative forecast for transportation planning. For the same reason, the city also used it in much of its transit-oriented development strategic planning efforts.

Moreover, city departments including Planning and Housing adopted the MVA approach in order to tailor the level and nature of municipal action, zoning, code enforcement, demolition, and other interventions. These departments also began incorporating the MVA in their Notices of Funding Availability.

Lastly, as testament to the MVA's value to its housing and community development efforts, one former city official noted that during transition discussions between Mayors O'Malley, Dixon, and Rawlings-Blake, the transition committees encouraged continued use of the MVA as a tool to assist city efforts.

Although Baltimore, like many cities, will still face challenges in revitalizing its neighborhoods for years to come, data from the MVAs have already made valuable contributions to the city's efforts. In addition to helping the city better understand the unique dynamics of its real estate markets, the MVA approach has helped Baltimore set priorities for service delivery and intervention according to market type as well as design strategies that are tailored for specifically for those markets.

About the Author

Ira Goldstein, PhD, is a nationally recognized expert on housing-related policy issues and director of Policy Solutions at The Reinvestment Fund. In addition to his work on the Market Value Analysis, Dr. Goldstein has done extensive analyses of the foreclosure crises in several cities and states, and has worked with federal and state agencies to uncover unfair and discriminatory lending and foreclosure practices. Dr. Goldstein recently completed a term on the Consumer Advisory Council of the Federal Reserve Board and serves on the board of directors of the Hope LoanPort.

1. Annual estimates of the population of Philadelphia prepared by the U.S. Census Bureau show that Philadelphia's population stabilized at 1.51 million in 2002 and grew slowly throughout the rest of the decade. See www.census.gov/popest/eval-estimates/eval-est2010.html. Return to text

2. See Rob Gurwitt (2002), "Betting on the Bulldozer," Governing Magazine (July), www.governing.com/topics/transportation-infrastructure/Betting-Bulldozer.html  . Return to text

. Return to text

3. Many articles and reviews document the history and accomplishments of Mayor Street's effort. Gurwitt (see note 2) provides a good overview and comment on the plan by a variety of local and national community and economic development experts. For some perspective on the early results of the program, see Stephen J. McGovern (2006), "Philadelphia's Neighborhood Transformation Initiative: A Case Study of Mayoral Leadership, Bold Planning, and Conflict," Housing Policy Debate, vol. 17 (3). Return to text

4. For a fuller discussion of census tracts and block groups, see the U.S. Census Bureau's Geographic Areas Reference Manual, www.census.gov/geo/www/garm.html. Return to text

5. Subject matter experts in the MVA process are usually representatives of the local housing department or planning commission. Oftentimes, TRF will rely on the review of local real estate professionals or community development practitioners. Return to text

6. Some things are more easily observed during fieldwork than others. For example, deferred maintenance is easily observed. High levels of foreclosure, however, are not always easily observed. Return to text

7. Baltimore had previously created its own typology, but found it less than fully optimal for its purposes. The city approached TRF to create its MVA because it was based on a larger and more appropriate set of market indicators and used more sophisticated spatial and statistical techniques. Return to text

8. See www.baltimorecity.gov/LinkClick.aspx?fileticket=_ezq6oAMe6M%3d&tabid=1039&mid=1838. Return to text

9. See www.baltimorecity.gov/Government/AgenciesDepartments/Planning/MasterPlansMapsPublications/HousingMarketTypology.aspx. Return to text

10. Reports on how the city is using the MVA approach come from interviews with current and former city officials as well as a review of numerous city documents (as referenced herein). We wish to especially thank former Baltimore City Planning Department officials Peter G. Conrad (director, Local Planning Assistance, Maryland Department of Planning) and Seema Iyer (associate director, Jacob France Institute at the University of Baltimore Merrick School of Business). We also thank Kurt Sommer (director, Baltimore Integration Partnership and former Baltimore city official). Return to text

11. For example, information from the 2008 MVA is available at www.baltimorecity.gov/LinkClick.aspx?fileticket=i-Vzm72_LZU%3d&tabid=1039&mid=1838. Return to text

12. See ESRI Map Book, vol. 23, at www.esri.com/mapmuseum/mapbook_gallery/volume23/sustainabledev2.html. Return to text

13. Targeting municipal resources is not a totally unique idea. For example, the City of Richmond developed its Neighborhoods in Bloom (NIB) program in which CDBG resources were targeted based on a variety of objective housing and social criteria. Reviews of NIB demonstrated that the approach yielded significantly better outcomes than the more typical approach to dividing resources evenly across a city in a manner that was never sufficient to bring forth positive change. A program description of NIB, prepared by Carolina Reid (2006), can be found on the Federal Reserve Bank of San Francisco's website at www.frbsf.org/publications/community/investments/0602/neighborhoods.pdf . A systematic analysis of NIB's accomplishments, prepared by John Accordino, George Galster, and Peter Tatian (2005), can be found at www.community-wealth.org/_pdfs/articles-publications/cdcs/report-accordino-et-al2.pdf . Return to text

14. See Housing Authority of Baltimore (2010), "Mayor Announces 'Vacants to Value' Plan to Reduce Blight," press release, November 3, www.baltimorehousing.org/wgo_detail.aspx?id=417 . Return to text