May 08, 2018

Monetary Policy Influences on Global Financial Conditions and International Capital Flows

Chairman Jerome H. Powell

At "Challenges for Monetary Policy and the GFSN in an Evolving Global Economy" Eighth High-Level Conference on the International Monetary System sponsored by the International Monetary Fund and Swiss National Bank, Zurich, Switzerland

Thank you for inviting me to join you today as part of this distinguished panel.

Our subject is the relationship between "center country" monetary policy and global financial conditions, and the policy implications of that relationship both for the center country and for other countries affected. This broad topic has been the subject of a great deal of research and discussion in recent years. Today I will focus in particular on the role of U.S. monetary policy in driving global financial conditions and capital flows. To preview my conclusions, I will argue that, while global factors play an important role in influencing domestic financial conditions, the role of U.S. monetary policy is often exaggerated. And while financial globalization does pose some challenges for monetary policy, efforts to build stronger and more transparent policy frameworks and a more resilient financial system can reduce the adverse consequences of external shocks.

The well-known Mundell-Fleming "trilemma" states that it is not possible to have all three of the following things: free capital mobility, a fixed exchange rate, and the ability to pursue an independent monetary policy. The trilemma does not say that a flexible exchange rate will always fully insulate domestic economic conditions from external shocks.1 And, indeed, that is not the case. We have seen that integration of global capital markets can make for difficult tradeoffs for some economies, whether they have fixed or floating exchange rate regimes.

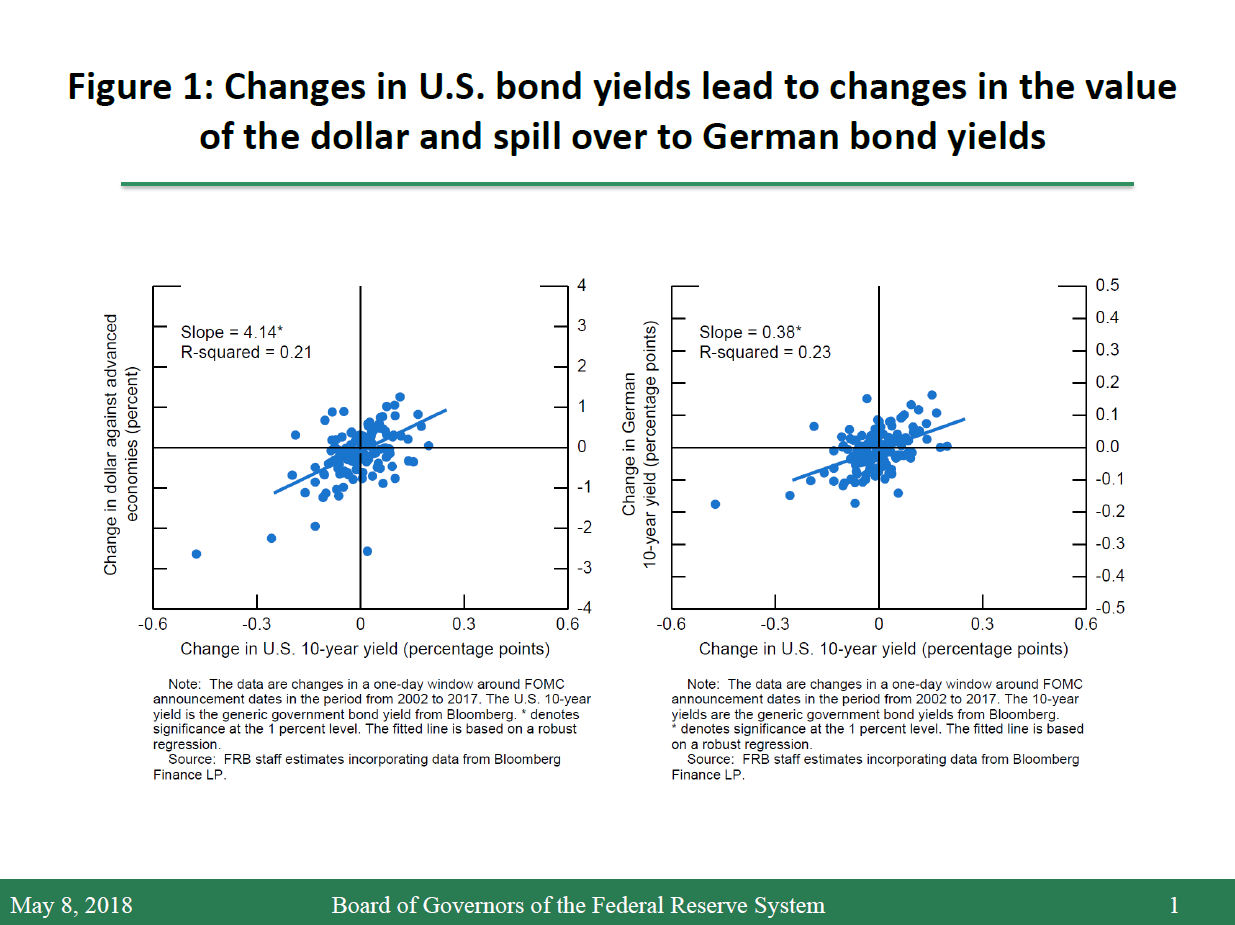

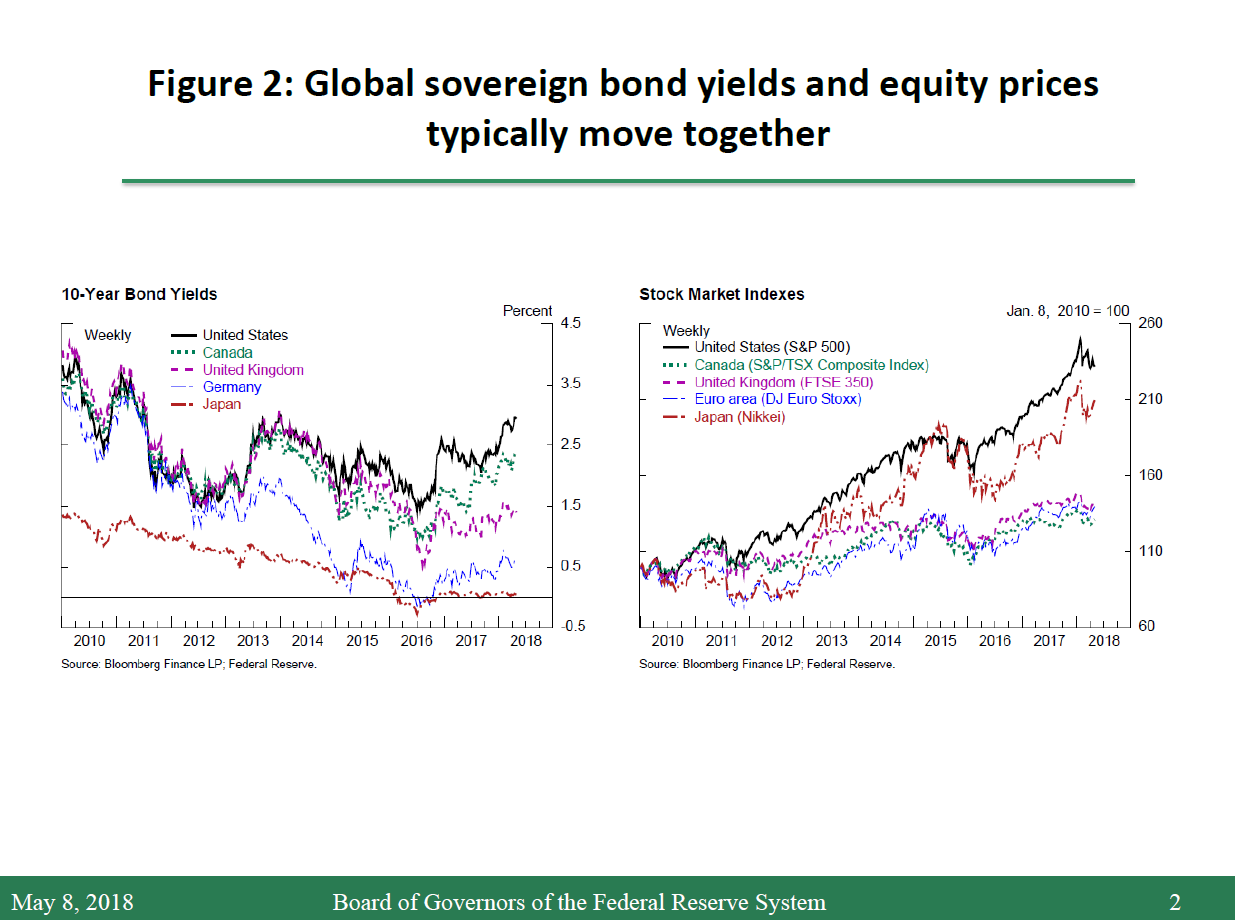

Since the Fed is the central bank of the world's largest economy and issuer of the world's most widely used reserve currency, it is to be expected that the Fed's policy actions will spill over to other economies. To illustrate this point, the scatterplot on the left side of figure 1 focuses on movements in interest rates and exchange rates following Federal Reserve policy announcements. As you can see, changes in U.S. interest rates after Fed policy actions (shown on the horizontal axis) lead to corresponding changes in the value of the dollar (shown on the vertical axis). And because of the dollar's widespread use around the world, these changes in the dollar affect financial conditions abroad. Fed policy-related movements in U.S. bond yields also tend to spill over to bond yields abroad, such as the German yields shown in the scatterplot on the right. Such spillovers are to be expected in a world of highly integrated financial markets.2 As figure 2 shows, bond yields (left) and equity prices (right) around the world typically move together fairly closely.

{kind=link}

{kind=link}

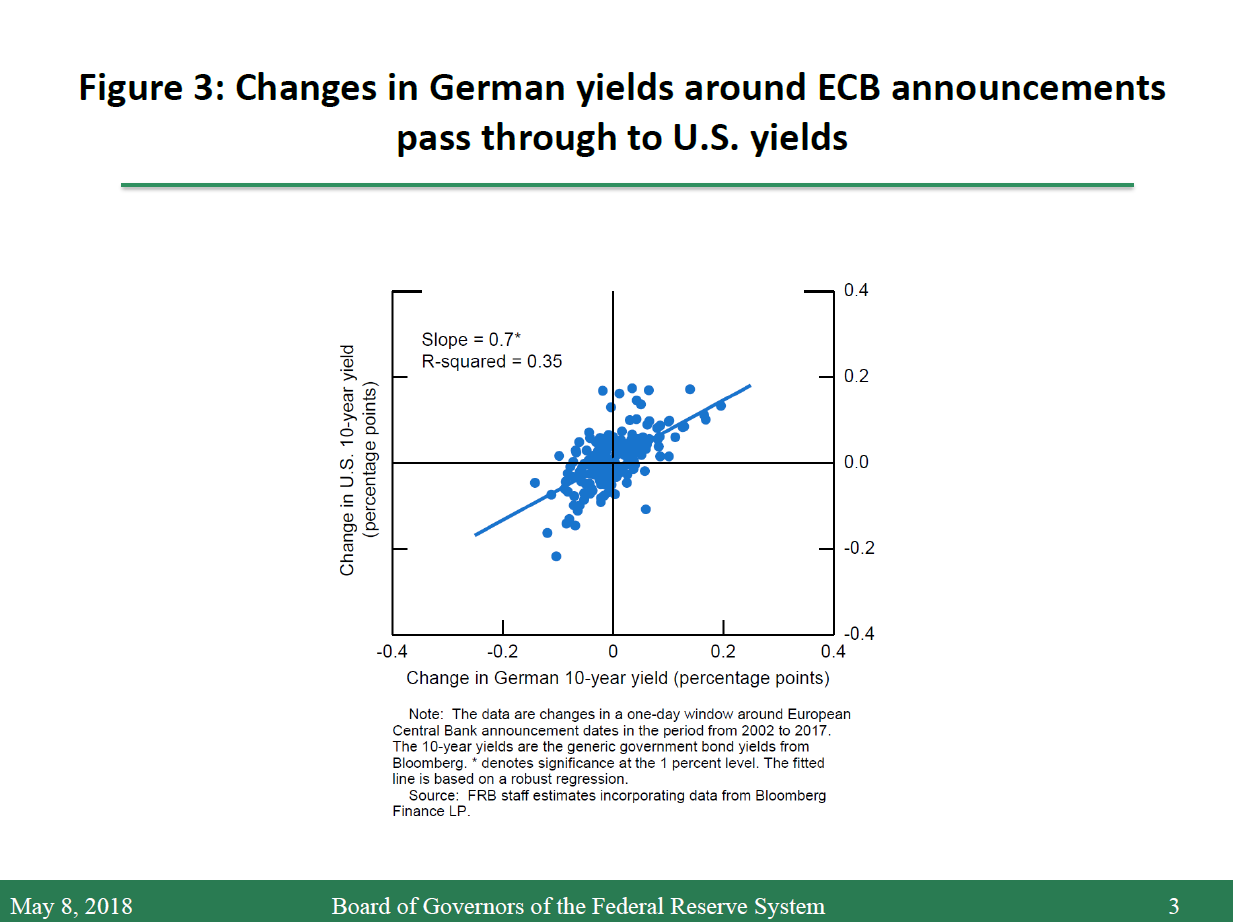

But the influence of U.S. monetary policy on global financial conditions should not be overstated. The Federal Reserve is not the only central bank whose actions affect global financial markets. In fact, the United States is the recipient as well as the originator of monetary policy spillovers. For example, as seen in figure 3, changes in German yields after European Central Bank policy decisions also pass through to U.S. yields.3 More broadly, it is notable that although the Fed has raised its target interest rate six times since December 2015 and has begun to shrink its balance sheet, overall U.S. domestic financial conditions have gotten looser, in part due to improving global conditions and central bank policy abroad.

{kind=link}

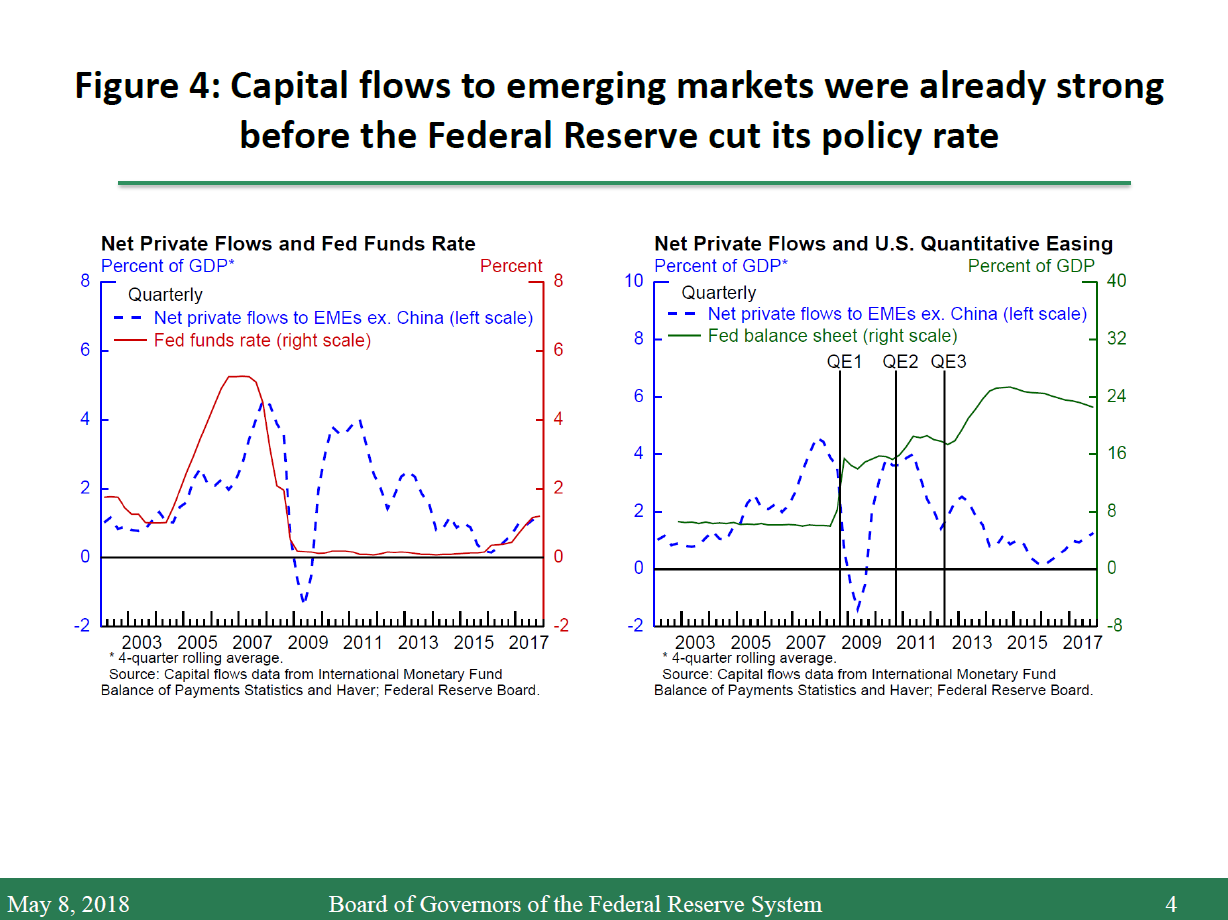

Much of the discussion of the spillovers of U.S. monetary policy focuses on their effects on financial conditions in emerging market economies (EMEs). Some observers have attributed the movements in international capital flowing to EMEs since the Global Financial Crisis primarily to monetary stimulus by the Fed and other advanced-economy central banks.4 The data do not seem to me to fit this narrative particularly well. As illustrated by the blue dashed line in the left panel of figure 4, capital flows to EMEs were already very strong before the Global Financial Crisis, when the federal funds rate was comparatively high. The subsequent surge in capital flows in 2009, as the crisis was abating, largely reflects a rebound from the capital flow interruption during the crisis itself, though highly accommodative monetary policies in advanced economies doubtless also played a role. Moreover, capital flows to EMEs started to ease after 2011, a period when the Federal Reserve continued to add accommodation and reduce yields through increases in its balance sheet, as shown in the right panel. And, more recently, capital flows to EMEs have picked up again despite the fact that the Fed has been removing accommodation since 2015.

{kind=link}

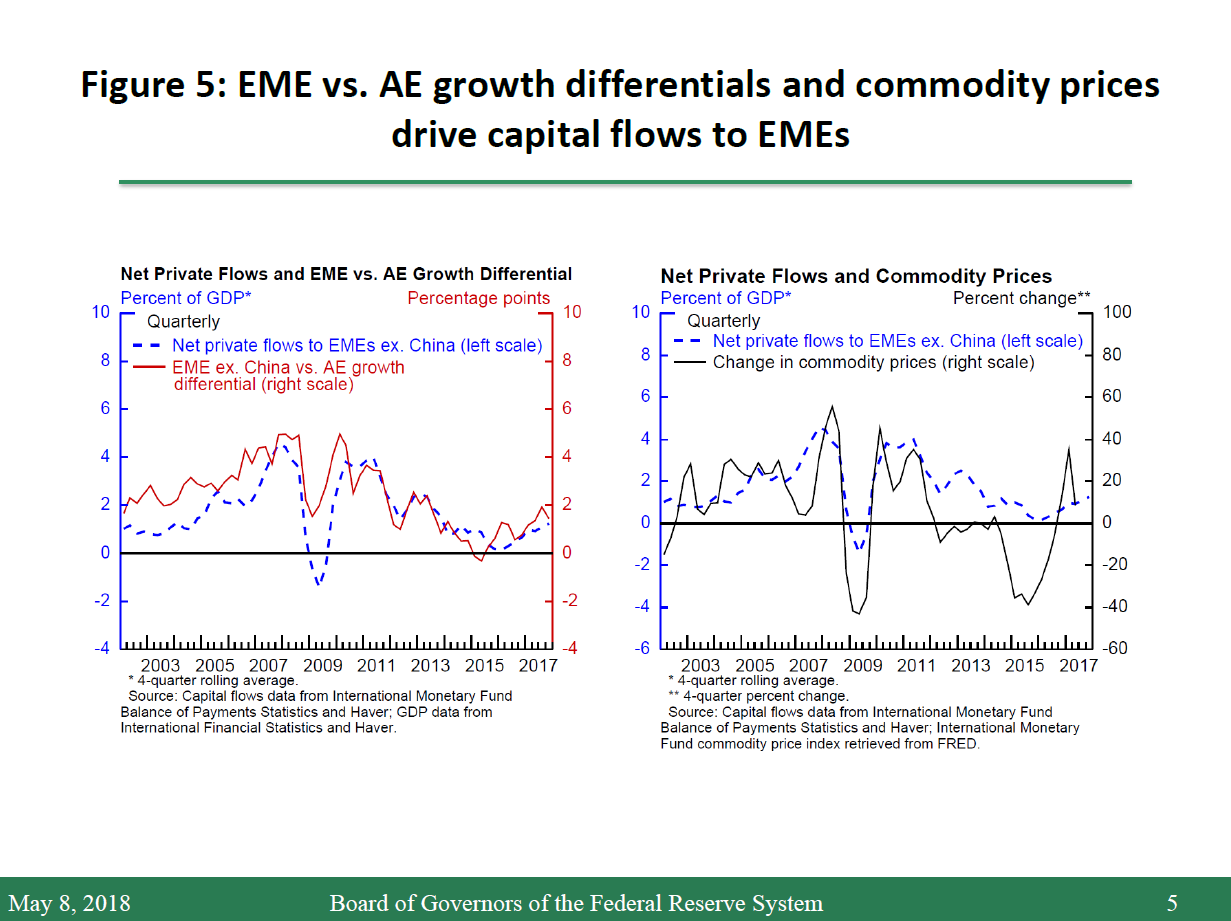

If U.S. monetary policy is not the major determinant, what other factors have been driving EME capital flows? One prominent factor has been growth differentials between EMEs and advanced economies. In figure 5, the left panel shows that capital inflows to EMEs picked up post-crisis, in line with the widening of this growth differential, while the slowdown in inflows after 2011 coincides with its narrowing. Another related determinant has been commodity prices, as shown in the right panel. The pickup in both global growth and commodity prices over the past couple of years explains a good part of the recent recovery of capital flows to EMEs.5

{kind=link}

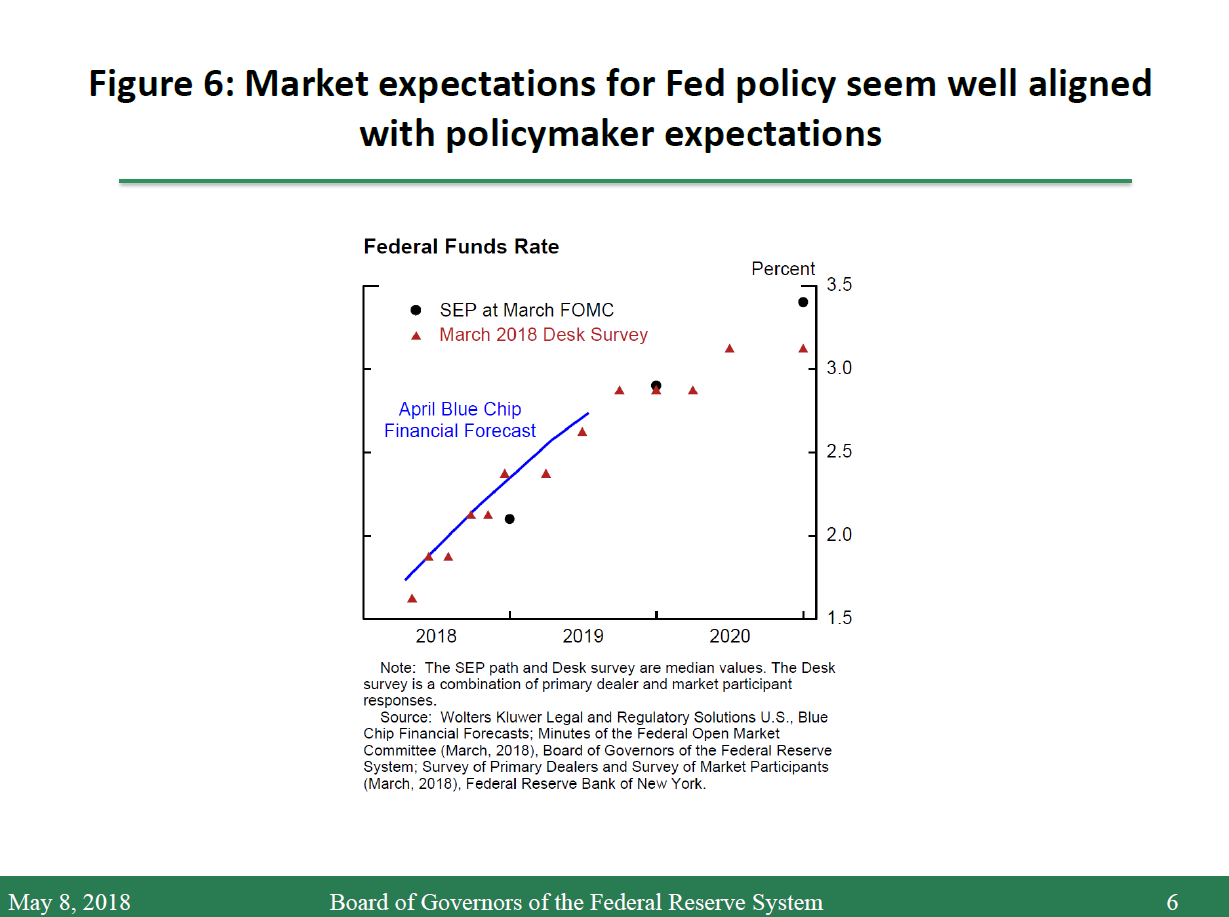

Monetary stimulus by the Fed and other advanced-economy central banks played a relatively limited role in the surge of capital flows to EMEs in recent years. There is good reason to think that the normalization of monetary policies in advanced economies should continue to prove manageable for EMEs. Fed policy normalization has proceeded without disruption to financial markets, and market participants' expectations for policy (the red symbols in figure 6) seem reasonably well aligned with policymakers' expectations in the Summary of Economic Projections (the black dots), suggesting that markets should not be surprised by our actions if the economy evolves in line with expectations.

{kind=link}

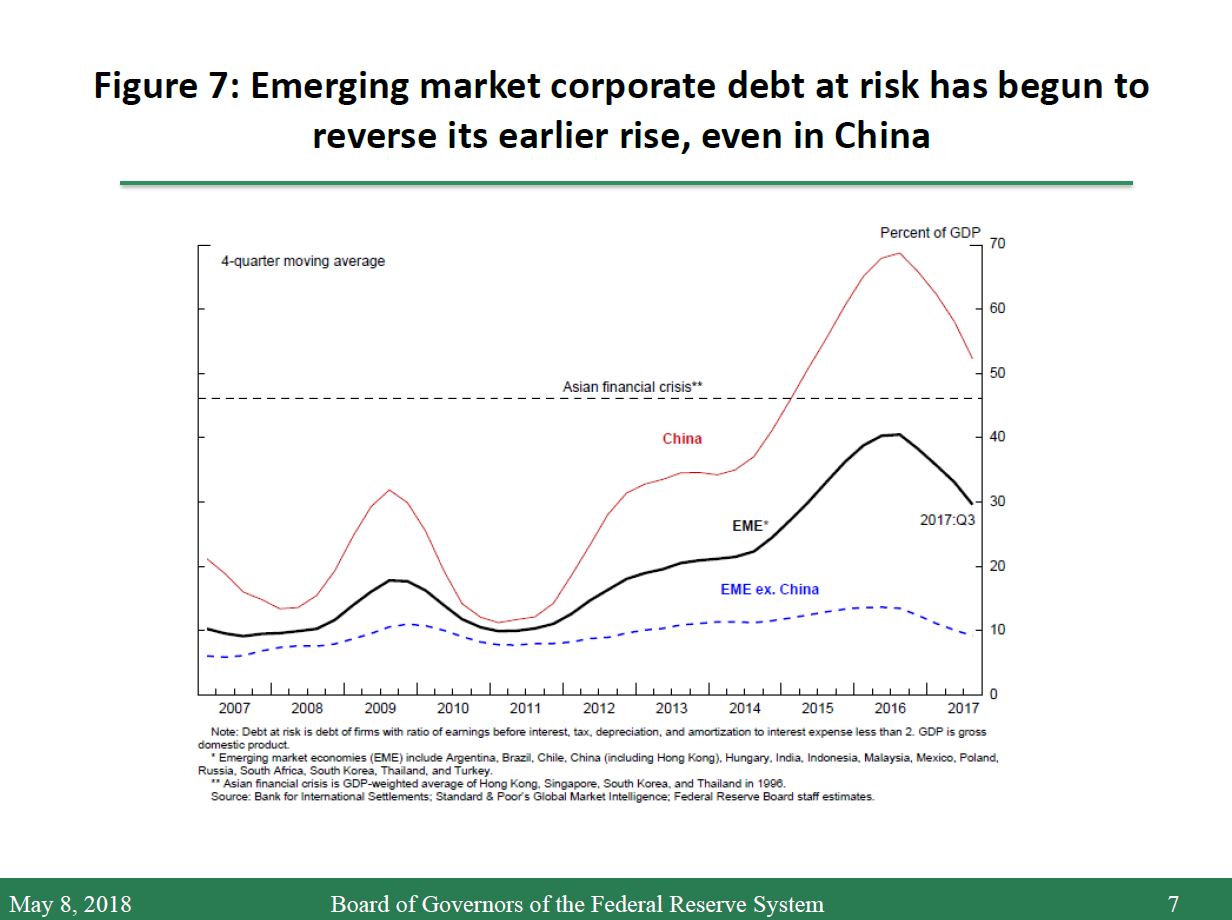

It also bears emphasizing that the EMEs themselves have made considerable progress in reducing vulnerabilities since the crisis-prone 1980s and 1990s. Many EMEs have substantially improved their fiscal and monetary policy frameworks while adopting more flexible exchange rates, a policy that recent research shows provides better insulation from external financial shocks.6 Corporate debt at risk--the debt of firms with limited debt service capacity--has been rising in EMEs, as shown in figure 7.7 But this rise has been relatively limited outside of China and has begun to reverse as stronger global growth has pushed up earnings.

{kind=link}

All that said, I do not dismiss the prospective risks emanating from global policy normalization. Some investors and institutions may not be well positioned for a rise in interest rates, even one that markets broadly anticipate. And, of course, future economic conditions may surprise us, as they often do.

Moreover, the linkages among monetary policy, asset prices, and the mood of global financial markets are not fully understood. Some observers have argued that U.S. monetary policy also influences capital flows through its effects on global risk sentiment, with looser policy leading to more positive sentiment in markets and tighter policy depressing sentiment.8 While those channels may well operate, research at both the Fed and the IMF suggests that actions by major central banks account for only a relatively small fraction of global financial volatility and capital flow movements.9

Nevertheless, risk sentiment will bear close watching as normalization proceeds around the world. What can the Federal Reserve do to foster continued financial stability and economic growth as normalization proceeds? We will communicate our policy strategy as clearly and transparently as possible to help align expectations and avoid market disruptions. And we will continue to help build resilience in the financial system and support global efforts to do the same.

References

Adrian, Tobias, Daniel Stackman, and Erik Vogt (2017). "Global Price of Risk and Stabilization Policies (PDF)," paper presented at "Eighteenth Jacques Polak Annual Research Conference: The Global Financial Cycle," sponsored by the International Monetary Fund, Washington, November 2-3. Washington: IMF.

Ahmed, Shaghil, and Andrei Zlate (2014). "Capital Flows to Emerging Market Economies: A Brave New World?" Journal of International Money and Finance, vol. 48 (November), pp. 221-48.

Bems, Rudolfs, Luis Catao, Zsoka Koczan, Weicheng Lian, and Marcos Poplawski-Ribeiro (2016). "Understanding the Slowdown in Capital Flows to Emerging Markets," chapter 2 in World Economic Outlook: Too Slow for Too Long. Washington: International Monetary Fund, April, pp. 63-99.

Cerutti, Eugenio, Stijn Claessens, and Andrew Rose (2017). "How Important Is the Global Financial Cycle? Evidence from Capital Flows," IMF Working Paper 17/193. Washington: International Monetary Fund, September.

Chari, Anusha, Karlye Dilts Stedman, and Christian Lundblad (2017). "Taper Tantrums: QE, Its Aftermath, and Emerging Market Capital Flows," NBER Working Paper Series 23474. Cambridge, Mass.: National Bureau of Economic Research, June.

Clark, John, Nathan Converse, Brahima Coulibaly, and Steve Kamin (2016). "Emerging Market Capital Flows and U.S. Monetary Policy," IFDP Notes. Washington: Board of Governors of the Federal Reserve System, October 18.

Curcuru, Stephanie, Michiel De Pooter, and George Eckerd (2018). "Measuring Monetary Policy Spillovers between U.S. and German Bond Yields (PDF)," International Finance Discussion Papers 1226. Washington: Board of Governors of the Federal Reserve System, April.

Fratzscher, Marcel (2012). "Capital Flows, Push Versus Pull Factors and the Global Financial Crisis," Journal of International Economics, vol. 88 (2), pp. 341-56.

Ghosh, Atish R., Jun Kim, Mahvash S. Qureshi, and Juan Zalduendo (2012). "Surges (PDF)," IMF Working Paper WP/12/22. Washington: International Monetary Fund, January.

International Monetary Fund (2017). "Are Countries Losing Control of Domestic Financial Conditions?" chapter 3 in Global Financial Stability Report: Getting the Policy Mix Right. Washington: IMF, April, pp. 83-108.

-------- (2018). "A Bumpy Road Ahead," chapter 1 in Global Financial Stability Report: A Bumpy Road Ahead. Washington: IMF, April, pp. 1-55.

Koepke, Robin (2015). "What Drives Capital Flows to Emerging Markets? A Survey of the Empirical Literature," IIF Working Paper. Washington: Institute of International Finance, April.

Klein, Michael, and Jay Shambaugh (2013). "Is There a Dilemma with the Trilemma?" Centre for Economic Policy Research, Vox, September 27.

Londono, Juan M., and Beth Anne Wilson (2018). "Understanding Global Volatility," IFDP Notes. Washington: Board of Governors of the Federal Reserve System, January 19.

Miranda-Agrippino, Silvia, and Helene Rey (2015). "U.S. Monetary Policy and the Global Financial Cycle," NBER Working Paper Series 21722. Cambridge, Mass.: National Bureau of Economic Research, November (revised February 2018).

Obstfeld, Maurice (2015). "Trilemmas and Trade-offs: Living with Financial Globalisation (PDF)," BIS Working Papers 480. Basel, Switzerland: Bank for International Settlements, January.

Obstfeld, Maurice, Jonathan D. Ostry, and Mahvash S. Qureshi (2017). "A Tie That Binds: Revisiting the Trilemma in Emerging Market Economies," IMF Working Paper WP/17/130. Washington: International Monetary Fund, June.

Pomerleano, Michael (1998). "Corporate Finance Lessons from the East Asian Crisis (PDF)," Viewpoint: Public Policy for the Private Sector, Note 155. Washington: World Bank Group, October.

Powell, Jerome H. (2017). "Prospects for Emerging Market Economies in a Normalizing Global Economy," speech delivered at the 2017 Annual Membership Meeting of the Institute of International Finance, Washington, October 12.

Rajan, Raghuram (2014). "Competitive Monetary Easing--Is It Yesterday Once More?" speech delivered at the Brookings Institution, Washington, April 10.

Rey, Helene (2015). "Dilemma Not Trilemma: The Global Financial Cycle and Monetary Policy Independence," NBER Working Paper Series 21162. Cambridge, Mass.: National Bureau of Economic Research, May (revised February 2018).

Wheatley, Jonathan, and Peter Garnham (2010). "Brazil in 'Currency War' Alert," Financial Times, September 27.

1. See, for example, Klein and Shambaugh (2013) and Obstfeld (2015). Return to text

2. See, for example, Adrian and others (2017) and the IMF's most recent Global Financial Stability Report (2018) for discussion of the transmission of global risk shocks to domestic macroeconomic conditions. Return to text

3. Curcuru, De Pooter, and Eckerd (2018) find that about half of the movement in German bund yields in a window following ECB monetary policy announcements spills over to U.S. Treasury yields, roughly the same magnitude as the spillover of movements in U.S Treasury yields to German bund yields following Federal Reserve policy announcements. Return to text

4. See, for example, Wheatley and Garnham (2010) and Rajan (2014). Return to text

5. Studies looking at the determinants of EME capital flows include Chari and others (2017), Clark and others (2016), Bems and others (2016), Koepke (2015), Ahmed and Zlate (2014), Fratzscher (2012), and Ghosh and others (2012). These papers generally conclude that many factors, including both "pull" and "push," affect EME capital flows. Return to text

6. See, for example, Obstfeld, Ostry, and Qureshi (2017). The results in IMF (2017) also indicate that while global financial conditions explain a significant portion of countries' domestic financial conditions, domestic monetary policy changes also play an important role in economies with flexible exchange rates. Return to text

7. The interest coverage ratio (ICR) is the ratio of earnings before interest, tax, depreciation, and amortization to interest expense. A value of 2 or less is typically associated with an increased likelihood of distress. For example, just before the Asian financial crisis, firms in Korea, Thailand, and Indonesia had an average ICR of 2; see Pomerleano (1998).

For more on evolution of EME debt at risk and vulnerabilities, see Powell (2017). Return to text

8. Rey (2015); Miranda-Agrippino and Rey (2015). Return to text

9. For example, Londono and Wilson (2018) find that U.S. monetary policy variables account for only roughly 10 percent of the six-month ahead forecast error variance of the VIX. In fact, in their study, non-U.S. global factors (non-U.S industrial production, a global Economic Policy Uncertainty Index, and the expected probability of recessions outside of the United States) explain nearly as much of the VIX forecast error variance as U.S. monetary policy and other U.S. variables combined. In addition, Cerutti, Claessens, and Rose (2017) find that directly observed variables in "center" countries (including VIX), as well as unobserved common dynamic factors extracted from actual capital flows, together rarely explain more than one-fourth of the variation in most types of capital flows. Return to text