FEDS Notes

Print

PrintAugust 7, 2015

How Much Student Debt is Out There?

Jesse Bricker, Meta Brown

, Simona Hannon, and Karen Pence

, Simona Hannon, and Karen Pence

As is widely known, student loan debt has expanded significantly over the past decade or so and stands at historically high levels. But how much in total do students owe? Somewhat confusingly, the Federal Reserve System produces three sets of statistics on student loans. Every quarter, total student loans are reported on the Federal Reserve Board's Consumer Credit (G.19) statistical release and the Federal Reserve Bank of New York's Quarterly Report on Household Debt and Credit (PDF) , based on the Consumer Credit Panel (CCP). And every three years, the Federal Reserve Board collects data on the assets and debts, including student loans, of a representative sample of U.S. households on the Survey of Consumer Finances (SCF) and provides both the anonymized household-level data and selected tabulations and analyses on its website.

Although these estimates do not line up exactly--an unsurprising finding given their different source data--they provide a very similar picture of the increase in student loan debt over the past decade or so. This note describes the data used in the three estimates as well as the student loan questions that each dataset is best positioned to answer.

An easy way to start thinking about the differences among the various estimates is to imagine how you might go about collecting data on student loans. Who might you collect the data from? You could ask the entities that hold or guarantee student loans, such as banks, finance companies, and the federal government, to report how much they are owed. This approach is taken in the G.19 release. You could ask a credit bureau to tabulate how much student debt is recorded in borrowers' credit records, which compile data on loan balances and payment history from loan servicers. This approach is taken in the CCP. You could ask people directly how much they owe. This approach is taken by the SCF.

Although in a perfect world student loan holders, servicers, and borrowers would report the exact same amounts, in practice this rarely happens. One reason why is that each dataset misses certain types of student loans. The G.19 data misses the private student loan holdings of some smaller financial institutions and nonprofit organizations. The CCP temporarily misses loans that have been originated but not yet reported by the servicer to credit bureaus and loans that are transferred between servicers. The SCF misses student loans for some economically independent people living at the same address--such as roommates or adult children living at home. In addition, all three datasets will be subject to some measurement error due to imperfect reporting from firms, servicers, and households.

The data sources also differ in their coverage of student loans in default. Defaulted loans represent a significant share of outstanding student loans because student debt obligations are rarely discharged through bankruptcy. Hence capturing the full student loan market entails capturing many long-defaulted loans that the borrower is still obligated to repay. The G.19 includes defaulted loans that are guaranteed by the government, but excludes private student loans (those without a government guarantee) that have been charged off by financial institutions. The CCP data are likely missing some long-defaulted government-guaranteed loans that servicers have stopped reporting on, but probably include many of the charged-off private student loans that are omitted from the G.19. In principle the SCF includes all student loans, including those in default (inferred by the fact that loan has not been deferred and is not in repayment). However, it is possible that respondents are less likely to report loans on which they have not made payments for some time.

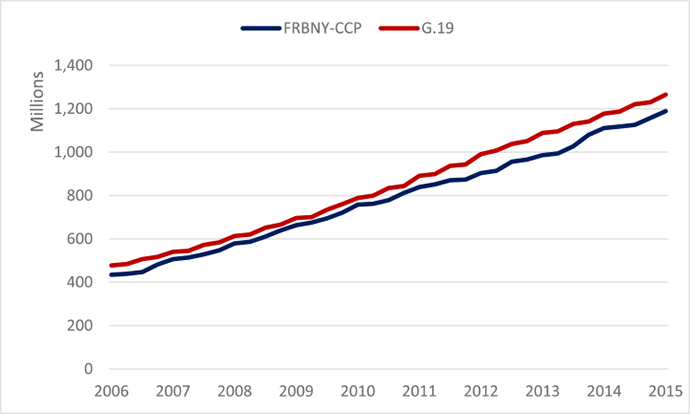

Even with these differences, though, the levels of student debt reported in the G.19 and in the CCP are quite similar over time. As shown in Figure 1, total student loan balances at the end of March 2015 were reported as $1.27 trillion in the G.19, and as $1.19 trillion in the CCP. The SCF level (not shown in Figure 1) is lower, and indicates that outstanding student loans in September 2013 were around $710 billion.

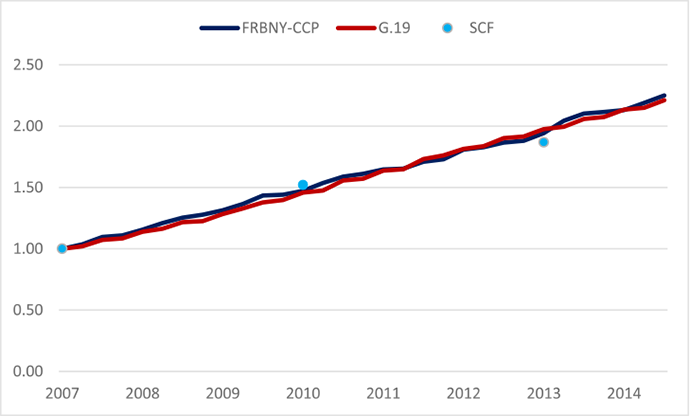

Despite these level differences between the G.19/CCP and SCF estimates, though, the three measures of total student debt have been growing at essentially the same average rate across the three data sources (Figure 2). Student loan debt as measured by the SCF increased 87 percent between 2007 and 2013, compared with a 94 percent increase in the CCP estimates for the same period and a 98 percent increase in the G.19 estimates. At an annual rate, these increases correspond to an 11 percent increase in the SCF, an 11-1/2 increase in the CCP, and a 12 percent increase in the G.19 data.

The remainder of this note describes these data sources and their strengths and limitations in more detail.

Consumer credit (G.19) release

The G.19 reports data on outstanding consumer credit held by financial institutions and other entities. "Consumer credit" is defined as loans extended to consumers--such as student loans, auto loans, and credit cards--that are not collateralized by real estate. Data are collected and reported separately by type of institution, such as depository institutions (commercial banks and thrifts), finance companies, credit unions, the federal government, nonprofit and education institutions, nonfinancial businesses, and pools of securitized assets.1 Outstanding loans are further categorized into revolving credit, which is primarily credit cards, and nonrevolving credit, which is primarily student and auto loans.

In its coverage of delinquent and defaulted loans, the G.19 follows the reporting conventions of each institution. Charged-off loans are generally excluded from the loan totals of private financial institutions, whereas the Department of Education loan totals include defaulted loans. Borrowers still have a legal responsibility to repay charged-off loans, unless the loans are discharged.2

It is difficult to calculate outstanding student loan balances from these data because commercial banks and thrifts do not separate out the student loan component of their nonrevolving credit holdings on the regulatory reports or survey data used as the basis for constructing the information presented in the G.19. Commercial banks hold about 20 percent of government-guaranteed student loans and about 40 percent of private student loans. In addition, finance companies are not required to file reports on their outstanding loans with any regulator, so the consumer credit estimates reported for this sector on the G.19--including the student loan holdings--are based on a voluntary survey.3 These estimates are measured with less precision because some finance companies do not participate in the survey.

As a result, the G.19 provides a separate estimate of outstanding student loans that is drawn, in part, from different data sources than the nonrevolving credit estimate. Comprehensive data on loans originated or guaranteed by the government are available from the Department of Education. These totals include loans originated and held by the Department of Education through the William D. Ford Direct Student Loan program and the Perkins program, as well as legacy loans originated by private financial institutions and guaranteed by the government through the discontinued Federal Family Education Loan Program.

Data on private student loans are more difficult to obtain. Due to the relatively small size of this market, most types of financial institutions are not asked to split out these loans on the regulatory reports or survey instruments that are used to construct the G.19. When the Federal Reserve Board first began providing these estimates in 2013, staff benchmarked the size of the market to estimates in a Consumer Financial Protection Bureau (CFPB) report.4 However, the Board's staff subsequently determined that this benchmark likely overstated the size of the private student loan market. In addition, the staff wanted to identify a data source that would be updated regularly to reflect changes in the private student loan marketplace.

Starting with the August 2015 G.19 release, which reports consumer credit outstanding as of the end of June 2015, the private student loan estimates are based on quarterly data provided by MeasureOne. The historical student loan data have also been revised back to the start of the series in 2006. The MeasureOne data include the holdings of the six largest current originators of student loans; three financial institutions that have stopped originating private student loans but have significant legacy portfolios; credit unions; some companies that specialize in refinancing existing student loans; and loans in publicly placed securitized pools. These data omit student loans held in the portfolios of smaller depository institutions (other than credit unions) and some finance companies, and by nonprofit and educational institutions. The Board's staff will continue to explore ways to collect data on the student loan holdings of these institutions, but believe that their share of aggregate private student loans is quite small.

In total, the G.19 estimates for student loans outstanding are now $32 billion to $95 billion lower, depending on the quarter, than the earlier estimates. The average gap between the G.19 estimates and the CCP estimates has been reduced from about $124 billion to $56 billion; in the first quarter of 2015, the gap has been reduced from $171 billion to $76 billion. The measurement issues described in this note, including the coverage of defaulted loans and servicer-reporting lags, likely only account for a portion of this remaining discrepancy, and so the extent to which the G.19 overstates or the CCP understates the true amount of student loans outstanding remains an open question at this point.

Quarterly Report on Household Debt and Credit

The Quarterly Report on Household Debt and Credit is based on the Federal Reserve Bank of New York Consumer Credit Panel.5 This dataset consists of the anonymized Equifax credit bureau records of a 5 percent random sample of U.S. individuals with credit files, as well as those of all of their household members. The data contain timely and detailed information on each person's debts, including the account balance, scheduled monthly payment, and loan performance. Data are collected at a quarterly frequency from the start of 1999 through the most recent quarter, on an ongoing basis. The sampling frame produces U.S.-representative data at each cross section, and yet individuals and households can be followed over time. With these data, researchers can explore topics such as the distribution of debt across borrowers and the relationships between different types of debt and delinquencies.6 Such rich analyses of the distribution and dynamics of debt are not possible with the aggregated institution-level data used in the G.19.

The data have two limitations from the perspective of student loan measurement. First, credit bureau records do not distinguish between government-guaranteed and private student loans. Second, although the records include information on which loans share the same (anonymized) servicer, they do not identify the financial institution, or even type of financial institution, that holds the loan. Thus the data cannot be aggregated to construct an estimate of outstanding private student loans, or of student loans held by a particular part of the financial sector.

When a student loan is originated or transferred to a new servicer, it takes time for the new servicer to incorporate the information into its system and begin reporting the information to credit bureaus. Typical reporting delays are one or two months, and so, for example, we find that loans originated in the second half of a given quarter most often do not appear in the CCP until the following quarter. Similar delays characterize some servicer transfers.7 Therefore, while almost all student loans are reflected in the credit bureau data by the end of the quarter following the actual quarter of origination, at any given point in time some small fraction of loans will be missing. Occasionally, a servicer may also report information on student loans only to one of the three major credit bureaus.8

Loans will still be included in credit bureau data after financial institutions have charged off the loans. Indeed, a key function of credit bureaus is to contain information on delinquent accounts. However, servicers may stop reporting data on loans that have been delinquent for an extended period of time, and some student loans that have been delinquent for extremely long periods of time may never have been reported to credit bureaus.9

Survey of Consumer Finances (SCF)

The SCF is a triennial cross-sectional survey sponsored by the Federal Reserve Board. These data provide the most comprehensive microeconomic data available on assets and liabilities of U.S. families, and also include detailed income and demographic information for these families. Credit bureau files contain very little demographic information on the borrower (although information on the demographic characteristics of the borrower's zip code is available), and no information on household income or assets. For their part, data from the G.19, which are based on aggregated figures from lenders, contain no information about individual-borrower characteristics. In contrast, SCF data can be used to compare student loan debt across different types of families, and in the context of the assets and resources that the family has to repay the loan.10

The SCF data are representative of U.S. families in the survey year. A "family" in the SCF is defined as the economic core of the sampled household, roughly speaking the person whose name is on the deed or lease at the surveyed address, and all people at that address whose finances are intertwined with those of that person. The published SCF statistics refer only to the debts and assets of this economic core.11 Thus, student loan information is not collected for members of the household that are outside of the household economic core. It is likely that most of the student loans of these non-core household members are included in G.19 and CCP statistics.12

The SCF sampling frame is another way that the SCF estimates will differ from the G.19 and CCP. A sampling frame is a list of all eligible housing units for a survey, and the frame for the SCF excludes institutional residences, including college dorms. As a result, any financially independent college student residing in a college dorm is excluded from the survey. In principle, though, the student loans of a financially dependent household member who is temporarily residing in a college dorm will be included in the statistics if her parents (or other adult with whom she has intertwined finances) are selected to participate in the SCF.13

Due to these considerations, the aggregate amount of student loan debt captured in the SCF will be lower than that captured in either the G.19 or the CCP. Thus, the differences between the SCF and CCP and G.19 aggregate levels suggests that a considerable portion of aggregate student loan debt is held by individuals outside of the economic core of a household. However, the fact that the SCF, G.19, and CCP have grown at the same rate, as shown earlier, suggests that the student loan balances of individuals inside and outside of the economic core have grown at the same pace.

A major strength of the SCF is the comprehensive information that it includes on student loans, which allows researchers to explore the role of student loans in family finances. The survey captures detailed information on up to six education loans owed by the family, and summary information for any further education loans. The details allow data users to understand when each loan was taken out, the amount that was originally borrowed, the current account balance, whether payments are currently being made on the loan, whether the payments are deferred, the amount of each loan payment, the interest rate on the loan, and the institution at which the loan is held. It is often the case that families are surveyed many years after their education loans were originally taken out, in which case the original set of education loans have been consolidated into one loan. If so, the survey captures the details of the consolidated loan.

In principle, capturing the institution of the loan should allow the SCF to separate private loans from federal loans. However, our analysis of these reported institutions indicates that the respondent often reports the loan servicer, rather than the originator of the loan. As result, in practice, the SCF cannot distinguish federal from private student loans.

Conclusion

The large and sustained increase in student loan balances over the past decade or so has raised concerns that student loan borrowers are incurring debt burdens that will be difficult to repay and will hinder their ability to achieve life goals such as purchasing homes, starting families, investing in small businesses, or retiring from the workforce. In order to understand better the causes and implications of the increase in student debt, the Federal Reserve System has embarked on initiatives to increase the information that it provides to the public on student loans. These initiatives include the launch of the Quarterly Report on Household Debt and Credit in 2010; the addition of a separate student loan category on the G.19 in 2013; numerous briefings and blogs using the CCP data; a conference on student loan measurement at the New York Fed in March 2015; the revision of the G.19 student loan total with improved source data in August 2015; and the addition of revised and expanded questions on student loans in the 2016 SCF. By providing more background information on these data sources in this note, we hope to spark more research and discussion on these important student loan policy issues.

1. For more information on the data reported on the G.19, please see: http://www.federalreserve.gov/releases/g19/about.htm. Return to text

2. Government-guaranteed student loans can be discharged if the borrower dies or becomes permanently disabled; if the borrower's school closes its doors before the student finishes his or her education; or, in rare cases, via an undue hardship clause in bankruptcy. Return to text

3. We thank the finance companies who respond to this survey. Return to text

4. Following the report publication, the CFPB reported a subsequent estimate for the private student loan market for 2013:Q2, which the Board's staff also incorporated into the estimates. Return to text

5. See Donghoon Lee and Wilbert van der Klaauw, An Introduction to the FRBNY Consumer Credit Panel, Staff Report #479, November 2010, for more background information on the data. Return to text

6. See, for example, Andrew Haughwout, Donghoon Lee, Joelle Scally, and Wilbert van der Klaauw, Student Loan Borrowing and Repayment Trends, 2015 (PDF) , April 16, 2015. Return to text

7. Typically, it takes more time for the new servicer to add the account and begin reporting its data to the credit bureaus than for the old servicer to drop the account from its reporting file. While many servicer pairs accomplish this transition within the quarter of the transfer, some do not. As a result, we find that servicer transfer can cause some accounts to go unreported temporarily. Return to text

8. We are aware of instances of this practice in the early years of the panel. The Higher Education Opportunity Act of 2008 and the 1998 Amendments to the Higher Education Act of 1965 require that "For the purpose of promoting responsible repayment of loans covered by Federal loan insurance pursuant to this part or covered by a guaranty agreement pursuant to section 428, the Secretary, each guaranty agency, eligible lender, and subsequent holder shall enter into agreements with consumer reporting agencies (credit bureau organizations) to exchange information concerning student borrowers." The similarity of the student loan aggregates reported in the G.19, in the CCP, and by TransUnion, http://transunioninsights.com/studentloans, suggests that this practice is a more minor concern today. Return to text

9. Student loan reporting to credit bureaus before 2003 appears, based on non-CCP sources, to have been less reliable. In 2003, pressure from outside groups appears to have spurred servicers to improve their reporting. However, loans that were severely delinquent before 2003 may not have been reported then, and may have since been forgotten as long-delinquent and unrecoverable. Return to text

10. Box 14 in Bricker, Dettling, Henriques, Hsu, Moore, Sabelhaus, Thompson, and Windle (PDF) (2014) contains one such analysis based on the data from the 2013 survey. Return to text

11. The core is typically the economically dominant single person or couple in the household, plus all other people in the household that are economically interdependent with that single person or couple. In this way, a young adult who is renting a house with roommates will be included in the economic core, but her roommates likely will not be. Likewise, an adult child living at home with her parents but with otherwise independent finances will not be included in the family. Return to text

12. Brown, Haughwout, Lee, and van der Klaauw (2015) provide a detailed comparison of student (and other) debt measurement, levels, and trends in the SCF and CCP. Henriques and Hsu (PDF) (2014) do the same for asset and debt patterns in the SCF and Flow of Funds Accounts (FFA), offering a long history of the relationship between SCF and G.19 debt measures. Return to text

13. The main family respondent is ultimately allowed to decide if a family member temporarily away from home will be included in the household. Return to text

Please cite as:

Bricker, Jesse, Meta Brown, Simona Hannon, and Karen Pence (2015). "How Much Student Debt is Out There?" FEDS Notes. Washington: Board of Governors of the Federal Reserve System, August 07, 2015. https://doi.org/10.17016/2380-7172.1576

Disclaimer: FEDS Notes are articles in which Board economists offer their own views and present analysis on a range of topics in economics and finance. These articles are shorter and less technically oriented than FEDS Working Papers.