FEDS Notes

Print

PrintDecember 18, 2015

Introducing Section 529 Plans into the U.S. Financial Accounts and Enhanced Financial Accounts

Madeline McCullers and Irina Stefanescu

Section 529 plans are tax-qualified college saving or prepaid tuition programs generally offered and administered by the states. Created as tax-advantaged savings vehicles, they were designed to encourage families to save for future college education expenses.

There are two types of 529 plans: college savings plans and prepaid tuition plans. College savings plans are savings accounts that receive federal tax benefits similar to those for Roth IRAs: Contributions are not deductible for federal tax purposes, but withdrawals, including investment earnings, are tax free as long as they are used to finance educational expenses. In addition, contributions may be tax-deductible at the state level. Prepaid tuition plans allow households to purchase tuition credits at designated institutions with after-tax dollars.

In the Financial Accounts of the United States, assets in 529 plans appear as memo items on the household balance sheet (table B.101). In addition, the assets of the plans are included (though not separately identified) in the body of the household balance sheet, as part of the totals for several of the asset categories. For example, assets in 529 college savings plans, which are predominantly invested in mutual funds, are included as part of households' direct holdings of mutual funds (line 26). The assets backing 529 prepaid tuition plans are spread over several asset categories on the household balance sheet, depending on how these assets are invested by the states managing the plans.

This Note provides some background information on 529 plans and discusses the methodology used to construct the measure of 529 plan assets reported in the Financial Accounts. The Note also introduces the state-level data on 529 plan assets that have been published in the Enhanced Financial Accounts.1

1. Background information on 529 plans

The first prepaid college savings vehicle was created in 1986 by the state of Michigan. In 1994, the U.S. Court of Appeals for the Sixth Circuit ruled that the income from the plan should not be subject to the federal income tax. Then, in 1996, the Congress enacted Section 529 of the Internal Revenue Code, establishing federal tax rules for 529 college plans. But it was not until the Economic Growth and Tax Relief Reconciliation Act of 2001 made qualified distributions tax-exempt that these plans really started to grow. 2

Generally, 529 plans are sponsored by states. Currently, all states except Wyoming have at least one 529 plan. In addition, the District of Columbia administers its own plan, and there is one nonprofit consortium of 127 private colleges administering an Independent 529 college plan. States (or administrators) can choose to sponsor one or several types of plans. Eligibility criteria in terms of residency are determined at the state level.3

Total contributions to a 529 plan may not exceed the amount necessary to finance qualified education expenses of the beneficiary.4 Some states can choose to exclude in-state 529 balances in the calculations for the eligibility of financial aid, creating a preference for in-state plans over out-of-state plans.

The allocation of 529 plan assets typically differs across the two plan types. In prepaid tuition plans, individuals pay for college tuition credits and have no control over the management of the plan assets. Instead, plan participants receive guarantees for future tuition credits, though the extent and structure of the guarantees differ by state.5 In college savings plans, investors choose among a selection of portfolios of mutual funds, which are then held in a trust established by the state. The investment returns depend on the performance of these funds. Most states hire a program manager to oversee their 529 college plans.6 In terms of marketing channels, the investors in 529 savings plans can buy shares directly from the program manager (direct-sold) or through an advisor or broker (broker-sold). The fund choices are typically diverse in terms of risk and investment strategies, e.g., money market funds, equity funds, bond funds, or age-based portfolios that shift from equities to bonds as the beneficiary approaches college age.

2. Measuring the aggregate size of 529 plans

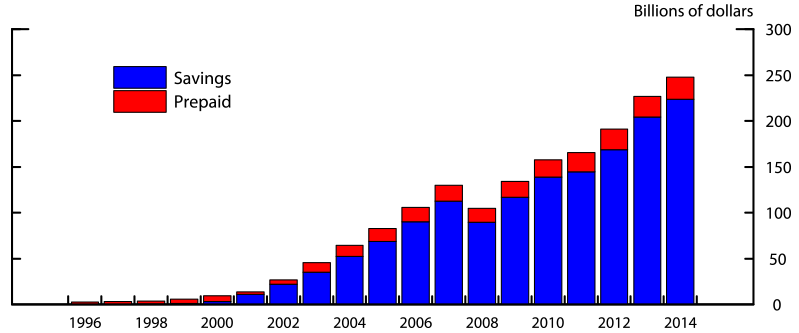

Our data on 529 plan assets come from the College Savings Plan Network (CSPN) website, which aggregates all the information that plan administrators voluntarily disclose to the public.7 We classify plans by type (prepaid versus savings) and state, using the information available on the CSPN.8 We supplement our data with additional information that we collect from the plans' annual disclosures.9 Figure 1 shows that 529 plan assets have grown substantially since 2001, when earnings on qualified distributions became tax-exempt. By the end of 2014, there were $248 billion in assets invested in 529 plans, representing a small but rapidly growing part of the household balance sheet.10 Most of the growth in 529 assets is attributable to college savings plans. As shown in Figure 1, prepaid plan assets accounted for less than 10 percent of total 529 plan assets in 2014.

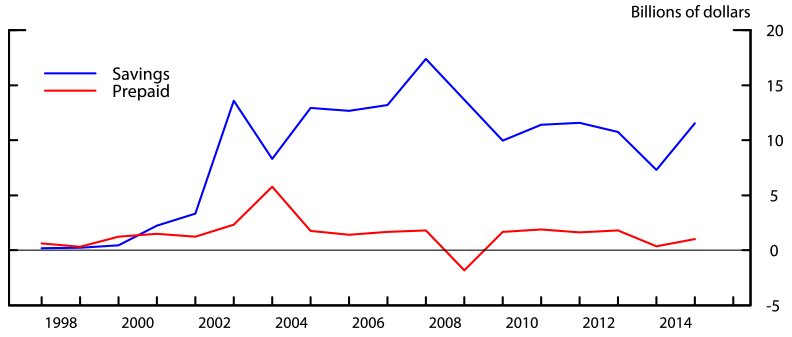

In Figure 2, we present our estimates of 529 plan flows, by plan type. In the absence of direct information on 529 college savings plan flows, we estimate flows from changes in assets and the mutual funds sector's capital gains. For 529 prepaid plans we estimate flows from changes in assets, under the presumption that these plans are guaranteed by states and that accumulated assets reflect the size of the state liability.11 The figure reveals that inflows into 529 savings plans are cyclical, peaking in the pre-dot-com and prefinancial crisis periods. Flows into 529 prepaid plans appear to be small and fairly stable, especially in the past five years.

3. 529 plans in the Enhanced Financial Accounts (EFAs)

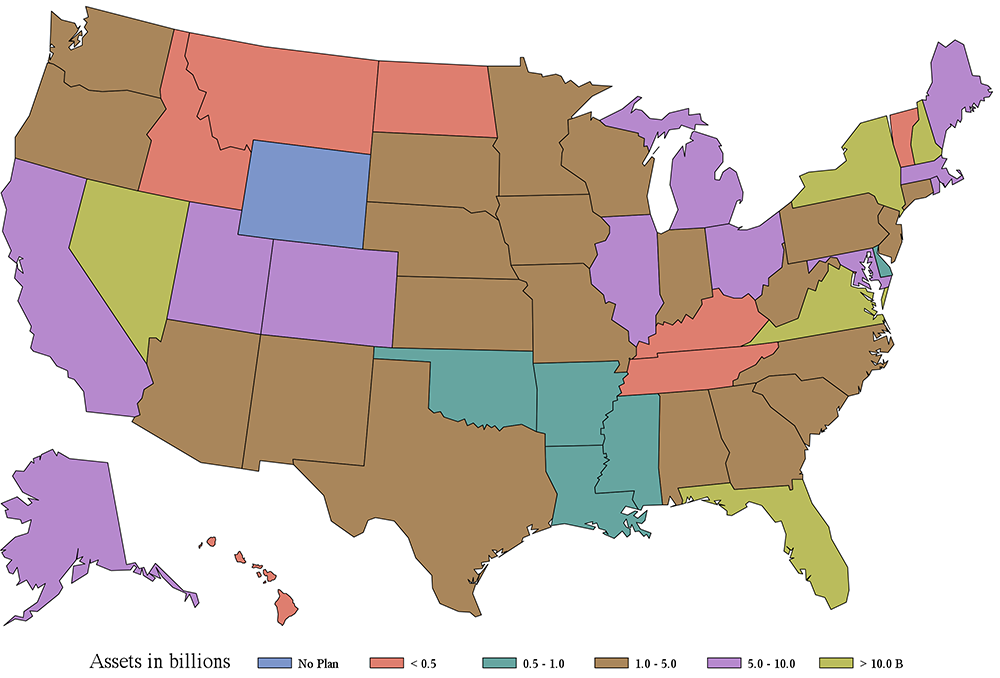

In the Enhanced Financial Accounts, we present Section 529 college plan assets by state and year from 2004 to 2014.12 An "ND" (no data) is recorded when data are not publicly available for a state or for a plan, but we are reasonably certain that the plan is still in existence.13 When a plan closes or is dissolved, we assume that the funds are redistributed to the original account owners and all assets flow out of that plan in the following quarter.14 Assets are assumed to be zero throughout the remainder of the time period.15

Figure 3 shows the distribution of total 529 plan assets across states in 2014. With more than $50 billion in assets in 2014, Virginia has the largest 529 plan, holding almost 23 percent of total 529 plan assets.16 The second-largest plan is offered by the state of New York and has $20 billion in assets; it is mostly direct-sold to New York residents.

Conclusion

Including information on 529 plans in the Financial Accounts provides additional information on the investments of the household sector. The state-level detail provided in the Enhanced Financial Accounts represents the first example of disaggregated information to be published as part of the EFA initiative. Future EFA projects will show, among other things, state-level detail on state-and-local-government pension funding. In addition, other future EFA projects will endeavor to provide more information on the asset allocations of 529 plans, the types of funds, and other details.

References:

Gallin, Joshua, and Paul Smith (2014). "Enhanced Financial Accounts," Finance and Economics Discussion Series Note, Washington: Board of Governors of the Federal Reserve System, 2014-08-01.

1. The Enhanced Financial Accounts initiative is a long-term effort to augment the Financial Accounts with a more detailed picture of financial intermediation and interconnections, including supplementary information that offers finer detail, new types of activities, higher-frequency data, and more-disaggregated data (see Gallin and Smith, 2014). Return to text

2. If not used for educational purposes, the withdrawals are subject to a 10 percent penalty. Return to text

3. Many plans do not require residency for opening a 529 college plan account. Return to text

4. 529 plans typically impose lifetime contribution limits, currently varying from $235,000 and $400,000. In addition, there may be federal gift tax implications for contributions in excess of $14,000 per year on behalf of a single beneficiary. There is no limit on the number of accounts by state or by beneficiary. Return to text

5. Recent developments in some states suggest that prepaid plans may not always be fully guaranteed. See for example http://www.nytimes.com/2011/04/02/your-money/paying-for-college/02money.html?_r=0. A summary of state prepaid tuition guarantees can be found at: http://www.savingforcollege.com/compare_529_plans/index.php?plan_question_ids[]=14&plan_question_ids[]=112&plan_question_ids[]=113&mode=Compare&page=compare_plan_questions&plan_type_id=. Return to text

6. According to Morningstar, the top program managers are American Funds, Ascensus, TIAA Tuition Financing, Fidelity Investments, and T. Rowe Price Associates. Return to text

7. We downloaded the data from http://www.collegesavings.org/  . National totals are created using a combination of semiannual aggregates from 1996 to 2001 provided by the CSPN and semiannual state assets from 2002 to 2015:Q2 found on the CSPN website. We are grateful to Chris Hunter for providing us with aggregate data from 1996 to 2001, years for which data are not publicly reported at the state level. Return to text

. National totals are created using a combination of semiannual aggregates from 1996 to 2001 provided by the CSPN and semiannual state assets from 2002 to 2015:Q2 found on the CSPN website. We are grateful to Chris Hunter for providing us with aggregate data from 1996 to 2001, years for which data are not publicly reported at the state level. Return to text

8. CSPN data collection methodology changed in 2009 and data are now presented at the more granular plan level (rather than by state and plan type). Assets are not collected in 2009:Q2. At the state level, we generate a staff estimate for assets and flows in 2009:Q2 using data points in 2008:Q4 and 2009:Q4. Return to text

9. In several cases, we clarified and confirmed the data in conversations with plan representatives. Return to text

10. For comparison, total mutual fund assets (line 26) were $7.8 trillion as of 2014:Q4. Return to text

11. Most states guarantee that the funds accumulated in prepaid plans will keep pace with tuition. Some states back their prepaid tuition plans by the full faith and credit of the state, meaning that if the program should find itself in financial difficulty, the state will step in to provide the necessary funding. See http://www.finra.org/investors/529-prepaid-tuition-plans . However, as discussed earlier, there is some variation across states. Return to text

12. The topline totals shown in the state-level EFA tables are identical to the national aggregates shown in the Financial Accounts of the United States. However, they are not necessarily the sum of assets across states-level assets due to interpolated values for missing plan data. Return to text

13. For example, assets in the Ohio prepaid plan are reported as "ND" from 2009 to 2012. According to conversations held with a CollegeAdvantage representative and postings on Savingsforcollege.com, the guaranteed savings plan was closed to new enrollment in 2004. However, it currently retains assets from previous investors. Therefore, we treat these data as missing rather than as a plan closing. At the state level, these assets are left as "ND." For the national accounts, a staff estimate is created for this plan from 2009 to 2013:Q2. Return to text

14. We use external informational to confirm that the plan is conclusively closed. In these instances, we treat the plan as closed and balances distributed to the account owners in the quarter following the last instance of reported assets, independent of whether the plan is legally closed at a different date. New Mexico and Colorado prepaid plan both fall under these rules. Return to text

15. Tennessee closed its savings plan in 2007 and partnered with Georgia's savings plan from 2008 through 2012. In 2013, it opened a new plan only for Tennessee residents. Wyoming savings plan was also terminated in 2006. Similarly, Colorado prepaid plan was closed to new investors in 2002, and stopped reporting data in 2009. The last reported assets for the New Mexico prepaid plan are in 2005:Q2. Return to text

16. The large market share comes from an early and long-term partnership with American Funds. The advisor-sold College America Fund offered by Virginia is sold at the national level. Return to text

Please cite as:

McCullers, Madeline and Irina Stefanescu (2015). "Introducing Section 529 Plans into the U.S. Financial Accounts and Enhanced Financial Accounts," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, December 18, 2015. https://doi.org/10.17016/2380-7172.1673

Disclaimer: FEDS Notes are articles in which Board economists offer their own views and present analysis on a range of topics in economics and finance. These articles are shorter and less technically oriented than FEDS Working Papers.