FEDS Notes

Print

PrintMay 2, 2016

The Role of Global Supply Chains in the Transmission of Shocks: Firm-Level Evidence from the 2011 Tōhoku Earthquake

Christoph E. Boehm, Aaron Flaaen, and Nitya Pandalai-Nayar

The April 2016 Kumamoto earthquake in southwest Japan has sent ripple effects through global supply chains. Toyota, Honda and Sony halted most Japanese production following the quake, and more recently General Motors announced production stoppages at four North American plants, citing parts shortages. Such far-reaching consequences of natural disasters are not without precedent: just five years earlier, the March 2011 Tōhoku earthquake had even more disruptive effects. Manufacturing plants in a diverse set of countries were affected, and the consensus view was that this Japanese-based disaster shaved off nearly 0.5 percentage point from U.S. second-quarter GDP in 2011.1

Though tragic, such natural disasters offer a rare glimpse into the nature of modern supply chain linkages. Generally, disentangling the various explanations for firm-level outcomes is a challenging task, as most explanatory variables are correlated with possibly confounding developments. Unlike scientists, economists generally do not have access to controlled experimental environments for the study of any particular mechanism. In a recent paper, (Boehm, Flaaen, and Pandalai-Nayar 2015) we use the 2011 Tōhoku earthquake as a natural experiment to provide new evidence for the role of intermediate input trade and multinational firms in the cross-country transmission of shocks.

The 2011 Tōhoku Earthquake: Effects on Japanese & U.S. Industrial Output

The 2011 Tōhoku event was in fact a triple disaster beginning on March 11, 2011 with an earthquake that measured 9.0 on the moment magnitude scale -- the fourth largest earthquake ever recorded. Perhaps more damaging than the earthquake itself was the subsequent tsunami, which inundated entire towns and coastal fishing villages across Northeast Japan. Finally, the partial meltdown of the nuclear reactor near Fukushima had a devastating effect on that region, and the precautionary shut-down of all nuclear power plants in the country resulted in severe power outages that persisted for months.

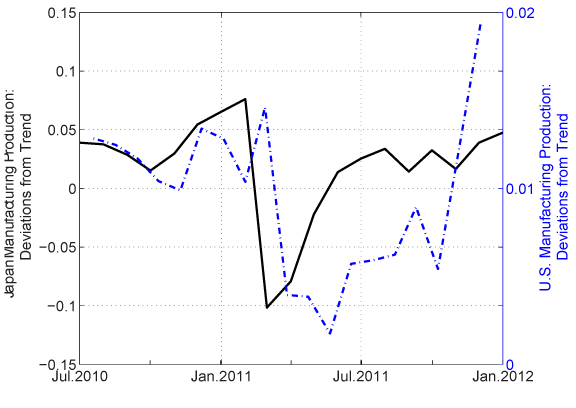

In addition to the human tragedy caused by the cumulative effect of these disasters, there were severe consequences for Japanese industrial production. Manufacturing output fell by roughly 15 percent in the month of March (see Figure 1, left scale), only recovering to pre-shock levels five months later in August. As expected, U.S. imports from Japan fell dramatically as well, though the large drop was recorded in April 2011, reflecting the several weeks of travel time for goods to reach the United States. More surprising is the effect of this shock on the U.S. economy, as measured by the deviations from trend in U.S. manufacturing output during this time. U.S. manufacturing output fell by about one percent in the month of April (see Figure 1, right scale) and remained significantly below prior levels for roughly six months following the Tōhoku event.

| Figure 1: Manufacturing Production in Japan and the U.S.: Months Surrounding the 2011 Tōhoku Earthquake |

|---|

|

Source: Boehm, Flaaen, and Pandalai Nayar (2015)

Firm-Level Effects: Exposure to Japan and the Elasticity of Substitution

What were the mechanisms behind the transmission of this shock to the U.S. economy? To answer this question, we use confidential firm-level microdata from the U.S. Census Bureau, complemented by new identifiers of cross-country firm ownership. The Census Bureau data on firm-level trade is particularly valuable in our context. Because trade is recorded at the level of individual transactions, the data can be aggregated into weekly or monthly time series. Such high-frequency data is necessary to identify the effects of this short-lived disruption.

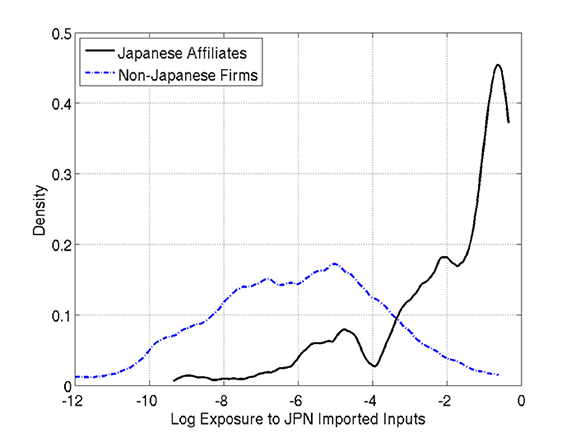

As a first step in understanding the role that intermediate inputs from Japan played in the transmission of this shock to the United States, we plot in Figure 2 a measure of the pre-shock exposure of firms to Japanese inputs. The x-axis of Figure 2 displays this measure of exposure in log form, where a value of zero corresponds to a firm with 100 percent of its inputs originating in Japan; the y-axis measures the relative frequency (density) of a given exposure value. We report these distributions of exposure across two groups of firms: one corresponding to the U.S. affiliates of Japanese multinationals, and another corresponding to non-Japanese multinationals.

| Figure 2: Density of Firm Exposure to Japanese Inputs: Japanese Multinationals and Other Firms |

|---|

|

Source: Boehm, Flaaen, and Pandalai Nayar (2015)

As is evident from the solid black line of the figure, U.S. manufacturing affiliates of Japanese multinationals are -- almost universally -- highly dependent on inputs from Japan. On average, these inputs comprise almost one-quarter of the cost share in these firms' U.S. production, and the large majority (86 percent) is purchased intra-firm. On the other hand, the dashed blue line of Figure 2 indicates that it is relatively uncommon for a non-Japanese affiliate to display substantial exposure to Japanese inputs.

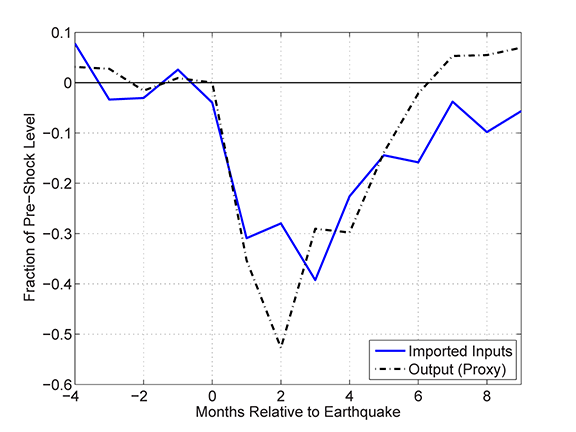

Given these large differences in exposure we focus on the Japanese-owned firms and estimate the impacts on imported inputs and output for these firms relative to a control group. To do so, we implement a dynamic treatment effects specification in which a firm is defined as being treated if it is owned by a Japanese parent company. The results, shown in Figure 3, demonstrate that these firms suffered large drops in U.S. output in the months following the shock, roughly one-for-one with the fall in (total) imported inputs.

| Figure 3: Relative Imported Inputs and Output (Proxy) of Japanese Affiliates in the United States |

|---|

|

Source: Boehm, Flaaen, and Pandalai Nayar (2015)

These results can be interpreted through the lens of a standard (constant elasticity of substitution) production function used by economists in a large variety of models. A critical parameter of this function is the elasticity of substitution across inputs, which captures the extent to which a firm can modify the mix of inputs (across different products, suppliers, etc.) in order to produce its output. For example, a temporary disruption in oil production affecting a single small country is unlikely to seriously impact U.S. firms since oil is a global commodity with many alternate suppliers -- in this case the elasticity would be relatively high. In contrast, specialized firm-specific inputs have fewer alternative sources, and hence disruptions to the supply of these inputs may exhibit greater spillover effects.

As Figure 3 shows, the shock to imported intermediates passed directly to these firms' operations in the U.S. There is virtually no scope for substitution to other inputs at this short notice. A likely explanation for this low elasticity is that the intermediates sourced from Japan are highly specialized. The high percentage of intra-firm transactions is consistent with this interpretation, as one would expect that parts produced within the firm embody a higher degree of firm-specific knowledge than parts purchased from other suppliers. Returning to the Census data, we develop a more general production structure and find firm-level elasticity estimates that are similarly low, consistent with the stylized evidence from Figure 3.2 These estimates are considerably lower than those typically used by economists to evaluate the cross-country transmission of shocks via international trade.

Our results also indicate that these Japanese affiliates reduced their expenditures on non-Japanese inputs in line with the fall in Japanese inputs. This implies that other firms in the U.S. economy -- upstream or downstream from the Japanese affiliates -- suffered from the shock even without direct input exposure to Japan. Such network effects can propagate the shock throughout the economy, and therefore both amplify and extend its consequences (see Carvalho 2014). A related paper (Carvalho et al. 2014) documents that such propagation of the shock to upstream and downstream firms via these network linkages did indeed occur in Japan following the Tōhoku event.

General Lessons: Beyond the Tōhoku Earthquake

Because our results are specific to one natural experiment, care must be taken when generalizing our findings to alternative situations. For example, if firms had held larger material inventories, a disruption to U.S. output would have been less likely. Consistent with the wide adoption of so-called "just-in-time" production, the average manufacturing firm in our sample around the Tōhoku event held just over three weeks of materials inventories. And because this is an average across all inputs of the firm, there were likely many individual parts with much shorter supplies. The fact that the Kumamoto earthquake again triggered production disruptions indicates that firms did not hold large inventories in April 2016 either. Yet, it is clear that inventories can in principle safeguard against supply shortages.

Second, the parameter we estimate is meant to capture the complicated technological and contractual features that govern the substitutability of materials from existing suppliers with similar materials from alternative sources. As argued by economists dating back to Samuelson (1947), this parameter is necessarily tied to a particular time horizon. In models in which researchers study longer-run phenomena, larger values of this elasticity are likely. Finally, several studies reveal that the elasticity of substitution is a critically important parameter in international business cycle models. Heathcote and Perri (2002) and Johnson (2014) demonstrate that such models better fit the data when the elasticity of substitution is low. We find these theoretical results reassuring as they suggest that our estimates are indeed externally valid at business cycle frequencies.

As economists struggle to understand the determinants of a high and growing degree of synchronization across advanced economies, rigid supply chains -- particularly in multinational firms -- appear to be an important feature worth further study. Although the full effects of the Kumamoto earthquake on global production is likely to be more modest than the more devastating Tōhoku earthquake/tsunami, the lesson it provides for the nature of global supply chains appears to be the same.

Disclaimer: Any opinions and conclusions expressed herein are those of the authors and do not necessarily represent the views of the U.S. Census Bureau. All results have been reviewed to ensure that no confidential information is disclosed.

References

Boehm, Christoph E., Aaron Flaaen, and Nitya Pandalai-Nayar. 2015. "Input Linkages and the Transmission of Shocks: Firm-Level Evidence from the 2011 Tōhoku Earthquake." Finance and Economics Discussion Series 2015-094. Washington: Board of Governors of the Federal Reserve System.

Carvalho, Vasco M. 2014. "From Micro to Macro via Production Networks." Journal of Economic Perspectives, 28(4): 23-48.

Carvalho, Vasco M., Makoto Nirei, and Yukiko U. Sato. 2014. "Supply Chain Disruptions: Evidence from the Great East Japan Earthquake." Working paper.

Cox, Jeff (2015, May 5) "U.S. economy damaged more than thought by Japan quake." CNBC. Retrieved from http:/www.cnbc.com

Heathcote, Jonathan and Fabrizio Perri. 2002. "Financial Autarky and International Business Cycles." Journal of Monetary Economics 49. 601-627.

Johnson, Robert C. 2014. "Trade in Intermediate Inputs and Business Cycle Comovement." American Economic Journal: Macroeconomics 6(4) 39-83.

Samuelson, Paul A. 1947. The Foundations of Economic Analysis. Cambridge, Massachusetts: Harvard University Press.

1. See Cox (2011) for a summary of the various estimated effects of the 2011 Japanese earthquake/tsunami on U.S. GDP. Return to text

2. The estimates for non-Japanese firms are slightly higher than those for the Japanese affiliates, but still much lower than traditional estimates used by economists. Return to text

Please cite this note as:

Boehm, Christoph E., Aaron Flaaen, and Nitya Pandalai-Nayar (2016). "The Role of Global Supply Chains in the Transmission of Shocks: Firm-Level Evidence from the 2011 Tōhoku Earthquake," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, May 2, 2016, http://dx.doi.org/10.17016/2380-7172.1765.

Disclaimer: FEDS Notes are articles in which Board economists offer their own views and present analysis on a range of topics in economics and finance. These articles are shorter and less technically oriented than FEDS Working Papers.