IFDP Notes

Print

PrintJuly 20, 2015

Do financial market frictions affect executive compensation?

Bo Sun

1. Introduction

Transaction costs for investors trading in the U.S. stock market have declined significantly over the past 30 years: For example, the bid-ask spreads on Dow Jones stocks dropped from over 0.7% in 1980 to 0.2% in the 2000s, and the average brokerage commissions on listed stocks fell from 13 cents per share in 1980 to 4 cents per share in the 2000s.1 There has been a debate over the effect of such changes on asset prices and financial stability. On the one hand, a lower transaction cost enhances trading and promotes market efficiency. On the other hand, an easy transaction makes the financial market less stable and may have a detrimental effect on the macroeconomy. The proponents of the "Tobin tax," for example, tend to emphasize the latter view.2

One recent development in the corporate finance literature is the emphasis on the "feedback" effect.3 This literature challenges the traditional view of the financial market as merely a mirror image of real economic activities, emphasizing that activities in the financial market reveal information and affect (thus "feed back into") the behavior of firms and other economic actors. In light of this view, one natural question is: how does the decline in transaction costs in the financial market affect the real activity?

2. A model of CEO compensation and transaction costs

In Lin, Liu, and Sun (2015), we ask this question in the context of CEO compensation.4 Compensation policy, characterized by CEO pay-for-performance, is one of the most important factors in a company's success, shaping how well executives run the company. One important observation from our empirical study, detailed below, is that reducing transaction costs in the financial market lowers the degree of executive pay-for-performance, that is, the response in executive pay to firm performance. In a model of managerial compensation with informed trading in the stock market, we show that stock market participants' information acquisition in the financial market can substitute out part of incentive pay in executive compensation.5 The reason is that easier and cheaper transactions encourage market participants to acquire information and improve the informational efficiency of stock prices, which allows prices to better guide managers in their real decisions, such as investments and acquisitions, rendering incentive compensation less necessary as a means to achieve optimal decisions. The general idea that the market provides useful information to economic actors goes back to Hayek (1945): Prices aggregate diverse pieces of information gathered by many market participants and convey information that is not otherwise available to real decision-makers, and corporate decision-makers such as managers can learn new information from stock price movements and use it to guide their decisions. Reductions in transaction costs, which encourage trading and enhance the feedback effect, will therefore reduce the necessity to provide direct incentives in compensation.

3. Empirical analysis

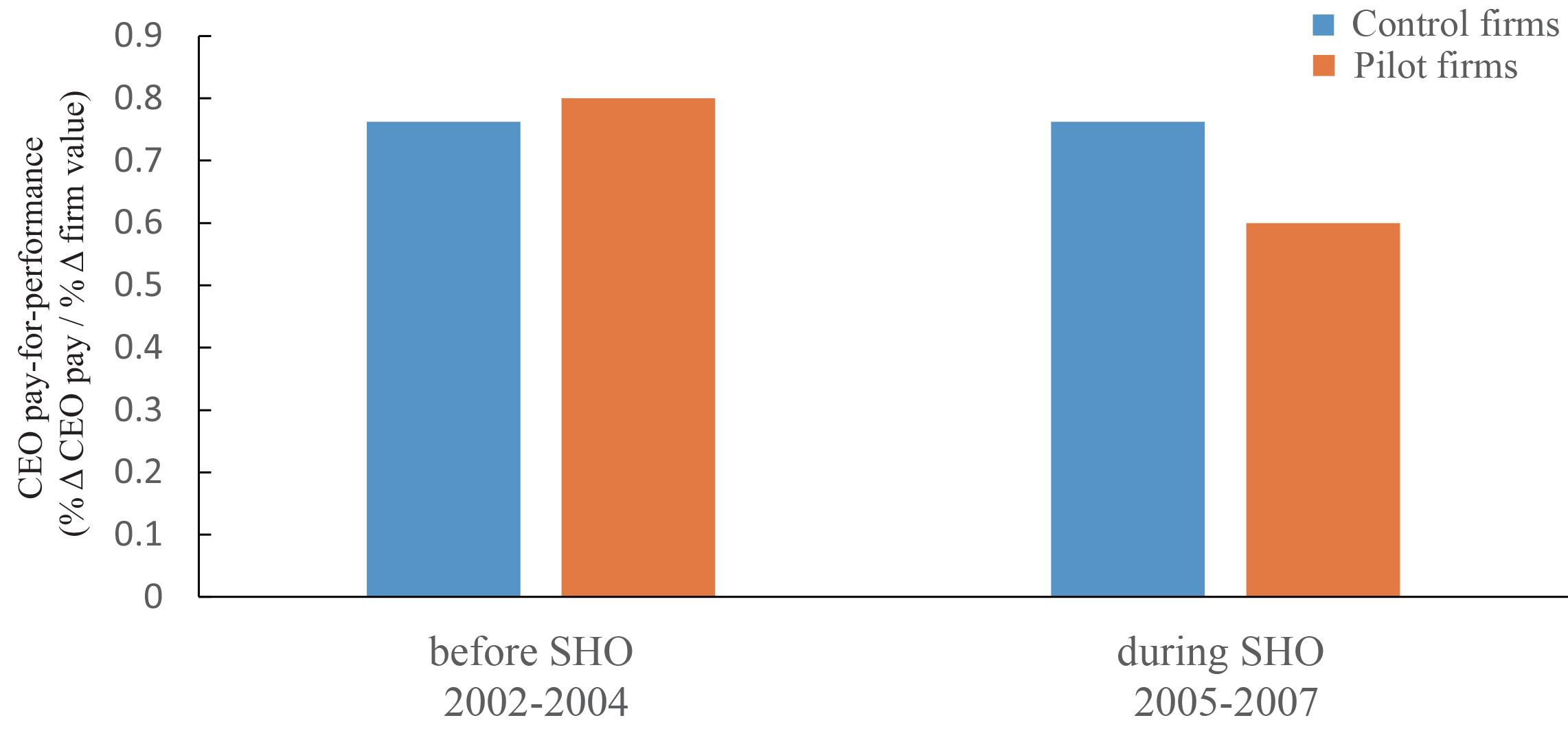

Empirically, we exploit two quasi-natural experiments that help us identify the effect of declines in transaction costs on CEO compensation structure. The first experiment, called the "Regulation SHO" program, took place when the U.S. Securities and Exchange Commission (SEC) removed the short-sale restriction ("uptick rule") for a randomly selected set of pilot firms from May 2005 to August 2007.6 We highlight the change in managerial pay-for-performance in response to the Regulation SHO program in Figure 1. Managerial pay-for-performance (indicated on the vertical axis in Figure 1) is measured using the scaled wealth-performance sensitivity (WPS), which is the percent change in CEO wealth for a one percent change in firm value; CEO wealth is approximated by the value of an executive's existing equity portfolio, including both new and existing grants.7 We can see in Figure 1 that executive pay in pilot firms (for which the short-sale constraint was removed) became less responsive to firm performance during the experiment, while the rest of the firms (shown as "control firms") barely changed their pay structure.

To see this change more clearly, we employ a difference-in-difference methodology using the following regression to study the change in managerial pay-for-performance in pilot firms due to the relaxation of the short-sale constraint compared to that in control firms:

| Figure 1: Average effect of Reg SHO on CEO Pay |

|---|

|

Notes: Pilot firms are those randomly selected firms for which short-sale constraints were removed during Regulation SHO. Control firms are the rest of the Russell 3000 firms.

βi,t = α i+ αt + a1·Ipilot x Iduring + a2·Xi,t-1 + εi,t,

where βi,t is managerial pay-for-performance measured using WPS, αi is a dummy for the firm fixed effect, αt is a dummy for the year fixed effect, Ipilot is a firm dummy that equals 1 for the Regulation SHO pilot firms and 0 for the other firms, Iduring is a year dummy that equals 1 for the three years during the program and 0 for the three years before the program, and Xi,t-1 denotes control variables including institutional ownership ratio and stock return volatility.

Estimation of Equation 1 yields that a1 is negative at a significant level of 1%, suggesting that pilot firms experienced a reduction in managerial incentives in compensation during the program, relative to control firms. The economic magnitude is also sizable. The point estimate of a1 is -0.195, implying that in response to a one percent change in firm value, the response of pay in pilot firms is roughly 0.2 percentage points less than in control firms during the Regulation SHO. That is, for a one percent increase in firm value, the CEOs in pilot firms gain $14,200 less (on average) than the CEOs in control firms during the experiment.8

The second experiment that effectively reduced transaction costs, called "decimalization," occurred when the U.S. stock market reduced the minimum tick size (i.e., minimum stock price movement) from 1/16 dollar to one cent in 2001. We also find declines in CEO pay-for-performance after decimalization, especially in firms for which information from the stock market is likely to be useful.

4. Conclusion

Our research offers insights for the current debate on financial-stability regulation. The conventional wisdom is that if the stock market is more strongly regulated and stabilized, managers have less incentive to take large risks, as the upside gain becomes limited. Our study cautions that directly applying this conventional wisdom to policymaking may overlook the increasingly important role of the stock market as an information provider. Trading frictions induced by regulations in the stock market may reduce speculative trading activities and may help stabilize market prices, but they may also reduce the benefits of information produced in the stock market in limiting managerial risk-taking. The real effect of the information contained in stock prices calls for more studies on the costs and benefits of financial market regulations.

References

Amihud, Y., and Mendelson, H. 1992. Transaction tax and stock values. In Lehn, K., and Kamphuis, Jr. R. W. (Eds.) Modernizing U.S. Securities Regulations. New York, N.Y.: Irwin Professional Publishing.

Bond, P., Edmans, A., and Goldstein, I. 2012. The real effects of financial markets. Annual Review of Financial Economics, 4, 339-360.

Cutler, D. M., Poterba, J. M., and Summers, L. H. 1990. Speculative dynamics and the role of feedback traders. American Economic Review, 80, 63-68.

. 1991. Speculative dynamics. Review of Economic Studies, 58, 529-546.

De Long, J. B., Shleifer, A., Summers, L. H., and Waldmann, R. J. 1990a. Positive feedback investment strategies and destabilizing rational speculation. Journal of Finance, 45, 379-395.

. 1990b. Noise trader risk in financial markets. Journal of Political Economy, 98, 703-738.

Edmans, A., Gabaix, X., and Landier, A. 2009. A multiplicative model of optimal CEO incentives in market equilibrium. Review of Financial Studies, 22, 4881-4917.

Friedman, M. 1953. The case for flexible exchange rates. In: Essays in positive economics. Chicago: University of Chicago Press.

Fu, Y., Qian, W. L., and Yeung, B. Y. 2015. Speculative investors and transactions tax: Evidence from the housing market. Forthcoming in Management Science.

Goldstein, M. A., Eugene Kandel, P. I., and Wiener, Z. 2009. Brokerage commissions and institutional trading patterns. Review of Financial Studies, 22, 5175-5212

Hayek, F. 1945. The use of knowledge in society. American Economic Review, 35, 519-530.

Hau, H. 2006. The role of transaction costs for financial volatility: Evidence from the Paris bourse. Journal of the European Economic Association, 4, 862-890.

Jones, C. M. 2002. A century of stock market liquidity and trading costs. Available at SSRN 313681.

Lin, T. C., Liu, Q., and Sun, B. 2015. Contracting with Feedback. International Finance Discussion Paper, 2015-48.

Schwert, G. W., and Seguin, P. J. 1993. Securities transaction taxes: An overview of costs, benefits and unresolved Questions. Financial Analysts Journal, 49, 27-35.

Shleifer, A., and Summers, L. H. 1990. The noise trader approach to finance. Journal of Economic Perspectives, 4, 19-33.

Stiglitz, J. E. 1989. Using tax policy to curb speculative short-term trading. Journal of Financial Services Research, 3, 101-115.

Summers, L. H., and V. P. Summers. 1989. When financial markets work too well: A cautious case for a securities transaction tax. Journal of Financial Services Research, 3, 261-286.

Tobin, J. 1978. A proposal for international monetary reform. Eastern Economics Journal, 4, 153-159.

1. See Figure 1 in Jones (2002) and Figure 1 in Goldstein et al. (2009). Return to text

2. For the former view, see, for example, Friedman (1953), Hau (2006), and Fu et al. (2015). For the latter view, see Tobin (1978), Stiglitz (1989), Summers and Summers (1989), Cutler et al. (1990, 1991), DeLong et al. (1990a, Return to text

1990b), Shleifer and Summers (1990), Amihud and Mendelson (1992), and Schwert and Seguin (1993).

3. See Bond, Edmans, and Goldstein (2012) for a review. Return to text

4. See more details in Lin, Liu, and Sun, "Contracting with Feedback," International Finance Discussion Paper 2015-48. Return to text

5. In our model, an endogenous response of financial-market speculators to executive pay generates an additional mechanism that amplifies the effects of changing market conditions on managerial pay. That is, a weak-powered compensation leads to increased uncertainty in firm value, which raises the expected return from learning and hence incentivizes information acquisition in the financial market. To take advantage of this incentivizing effect, shareholders optimally further reduce incentive pay in executive pay. Return to text

6. The uptick rule is a trading restriction that short selling a stock is only allowed on an uptick. For the rule to be satisfied, the short must be either at a price above the last traded price of the security, or at the last traded price when the most recent movement between traded prices was upward. Return to text

7. The WPS is constructed and explained in detail in Edmans, Gabaix, and Landier (2009). Return to text

8. This back-of-the-envelope calculation is based on an average CEO compensation of $7.1 million during the 2005-2007 period in ExecuComp dataset, which yields an estimated CEO pay difference of $14,200 ($7.1million x 0.2%) between pilot and control firms. Return to text

Please cite as:

Sun, Bo (2015). "Do Financial Market Frictions Affect Executive Compensation?" IFDP Notes. Washington: Board of Governors of the Federal Reserve System, July 20, 2015. https://doi.org/10.17016/2573-2129.11

Disclaimer: IFDP Notes are articles in which Board economists offer their own views and present analysis on a range of topics in economics and finance. These articles are shorter and less technically oriented than IFDP Working Papers.