FEDS Notes

Print

PrintJune 8, 2015

Did the Fed's Announcement of an Inflation Objective Influence Expectations?

Alan Detmeister, Daeus Jorento, Emily Massaro, and Ekaterina Peneva

Economic theory suggests that inflation expectations are a key determinant of actual inflation. In particular, without shocks from labor markets, movements in oil prices, exchange rates or idiosyncratic factors, prices should change at an average pace consistent with expectations. Indeed, empirical work attests to their importance: conditioning on long-run inflation expectations from surveys improves the accuracy of inflation forecasts.1 Thus, an important question is whether, and how, the Federal Open Market Committee (FOMC) can influence inflation expectations.

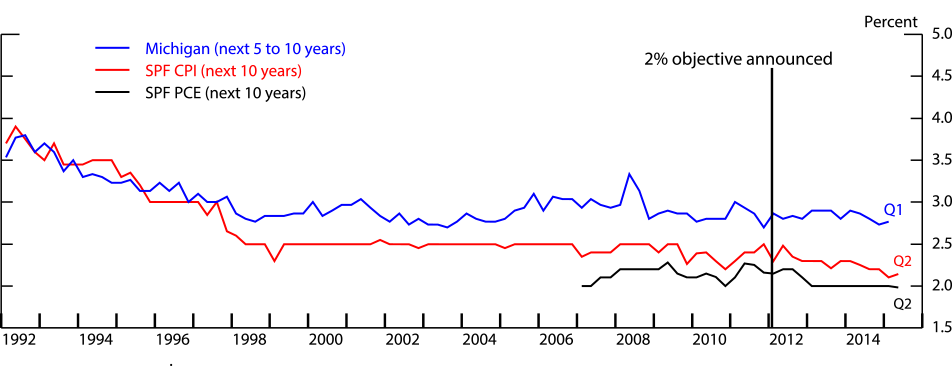

Figure 1 shows three survey measures of long-run expected inflation: the expected rate of price change during the next five to ten years from the University of Michigan's Survey of Consumers in blue; the expected average Consumer Price Index (CPI) inflation during the next ten years from the Philadelphia Fed's Survey of Professional Forecasters, or SPF, in red; and expected Personal Consumption Expenditure (PCE) price inflation during the next ten years from the SPF in black.

| Figure 1: Survey Measures of Long-Run Expected Inflation, 1992-Present |

|---|

|

Note. Median responses.

Sources: University of Michigan, Surveys of Consumers  ; Federal Reserve Bank of Philadelphia, Survey of Professional Forecaster (SPF) .

; Federal Reserve Bank of Philadelphia, Survey of Professional Forecaster (SPF) .

As can be seen from the chart, these survey measures have moved little since the late 1990s despite the recent deep recession, significant swings in commodity prices, and unprecedented monetary policy actions. The remarkable stability of these measures, however, makes it very difficult to figure out what drives them using standard time series regression techniques. For this reason, we look at how inflation expectations have changed following a single event--the FOMC's announcement of a 2 percent longer-run objective for PCE price inflation in January 2012.

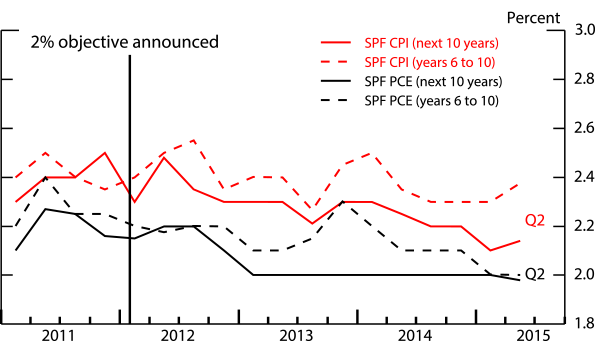

Starting with the expectations of professional forecasters, in the four quarters following FOMC's announcement, expected PCE price inflation during the next 10 years--the solid black line in figure 2--moved from about 1/4 percentage point above the FOMC's objective down to the 2 percent objective. In the two years since coming into line with the FOMC's objective, these expectations have remained at the 2 percent level.

| Figure 2: Long-Run Expected Inflation from the SPF, 2011-Present |

|---|

|

Note. Median responses.

Sources: Federal Reserve Bank of Philadelphia, Survey of Professional Forecaster (SPF) .

Arguably, since monetary policy has its greatest influence on inflation in the longer run, removing the initial five years from the ten year sample provides a clearer signal of the inflation rate that professional forecasters think is consistent with monetary policy. The black dashed line in figure 2 displays professional forecasters' expectations of PCE inflation in years six through ten. These expectations trended down more gradually following the announcement, and have just recently reached the FOMC's 2 percent inflation objective. 2 ,3 Turning to the CPI, expected inflation during the next 10 years--the solid red line--also declined since the announcement, though fairly gradually. Given that inflation as measured by the CPI has been slightly higher, on average, than inflation measured by PCE prices, it is no surprise that CPI expectations remain above 2 percent. In contrast to the downward movement in the other measures, expected CPI inflation in years six through ten--the red dashed line--has shown little net change.

Taken at face value, the movement in CPI and PCE price inflation expectations provide a little support for the idea that the FOMC's announced inflation objective did influence the inflation expectations of professional forecasters, who probably follow FOMC statements fairly closely.4

On the other hand, there is little evidence that households were influenced by the FOMC's announcement. As shown by the blue line in figure 1, expected inflation during the next five to ten years from the Michigan survey continued to move sideways after early 2012. It is worth noting that Michigan survey does not specify a particular price measure, and the time horizon is less explicit than in the SPF.

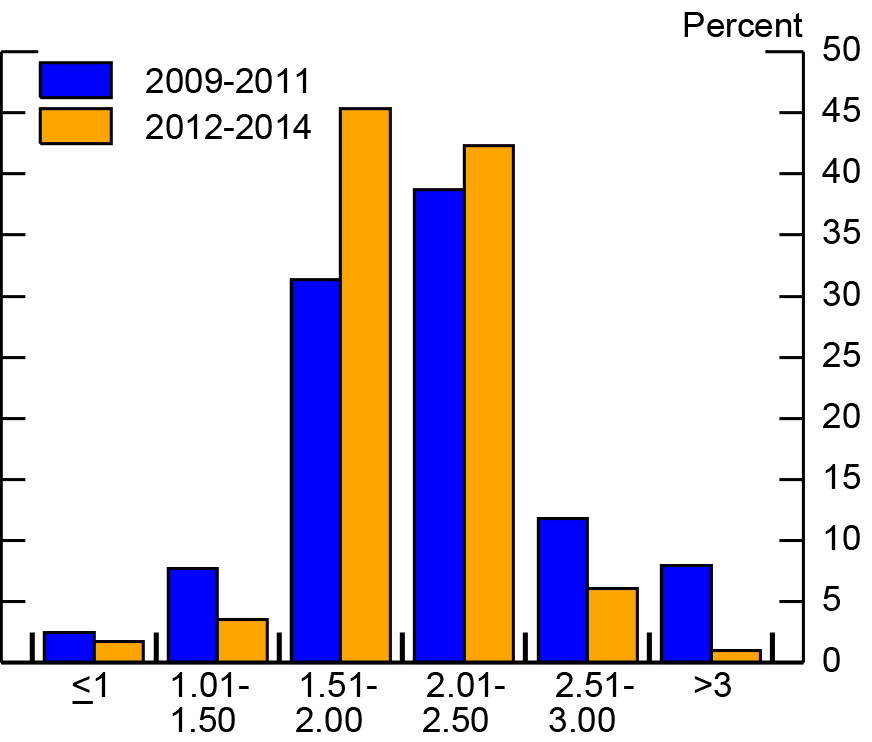

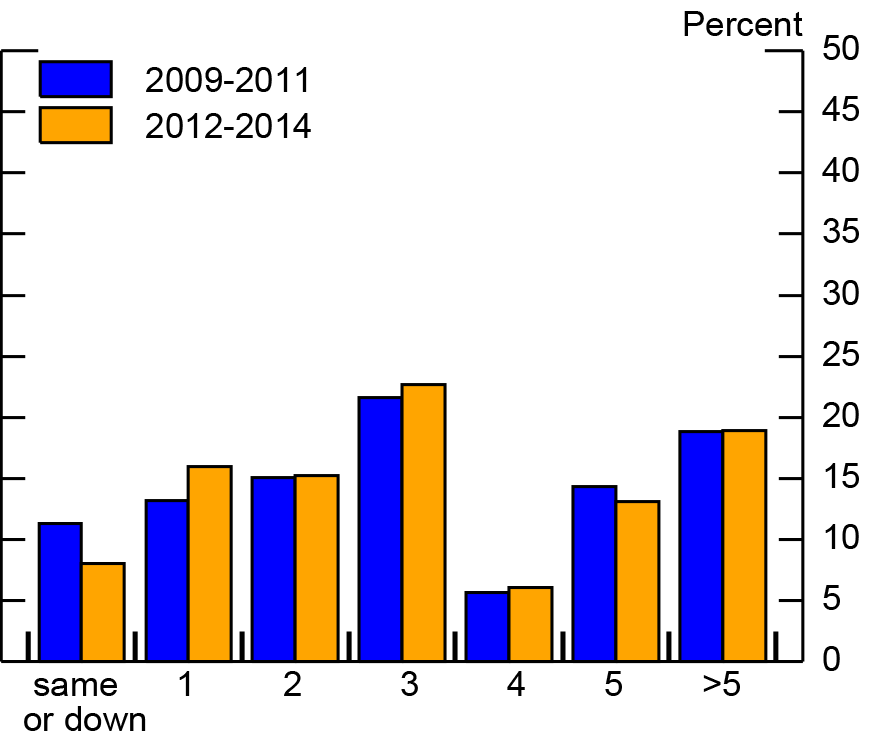

Examining individual responses from the SPF and Michigan survey provides further support for the idea that professional forecasters were influenced by the FOMC's announcement, but households were not. As can be seen by comparing the blue and orange bars in figure 3, the expectations of professional forecasters of PCE price inflation during the next 10 years became more concentrated around 2 percent in the three years following the FOMC's January 2012 announcement compared to the three years prior to the announcement. Both professional forecasters with very low inflation expectations and very high inflation expectations have become less common, and the standard deviation of across participants' responses declined from an average of 0.62 percentage points in the surveys during three years prior to the announcement to 0.40 percentage points in the surveys during the three years since. 5 By contrast, the distribution of long-run Michigan inflation expectations--figure 4--reveals little if any change in consumer inflation expectations following the announcement of a longer-run inflation objective.

| Figure 3: Distribution of SPF Expectations for 10-year PCE Inflation |

|---|

|

Sources: Authors' calculations using data from Federal Reserve Bank of Philadelphia, Survey of Professional Forecaster (SPF)

| Figure 4: Distribution of Michigan Expectations for 5- to 10-Year Inflation |

|---|

|

Sources: Authors' calculations using data from University of Michigan, Surveys of Consumers .

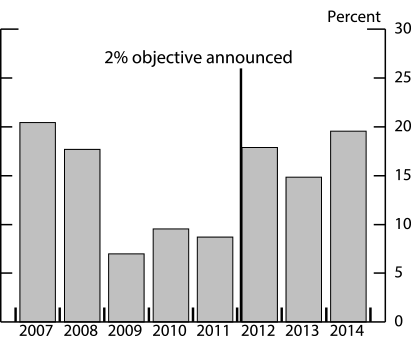

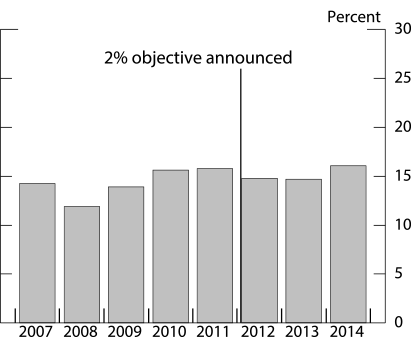

As yet another way of describing how longer-term inflation expectations have changed over time, the next two figures plot annual time series of the fraction of SPF and Michigan survey respondents with a long-term inflation expectation of 2 percent. The average share of professional forecasters who expected exactly 2 percent PCE inflation during the next 10 years--figure 5--rose noticeably from the three years prior to the three years following the FOMC's announcement, though the share after the announcement is no higher than it was in 2007 and 2008. This increase in the share is statistically significant.6 At the same time, the average share of consumers in the Michigan survey who expected 2 percent inflation over the longer term--figure 6--changed little, with the difference being neither economically nor statistically significant.7

| Figure 5: Share of SPF Respondents Who Expect Exactly 2 Percent PCE Inflation Over the Next 10 Years |

|---|

|

Sources: Authors' calculations using data from Federal Reserve Bank of Philadelphia, Survey of Professional Forecaster (SPF) .

| Figure 6: Share of Michigan Survey Respondents Who Expect 2 Percent Inflation Over the Next 5 to 10 Years |

|---|

|

Sources: Authors' calculations using data from University of Michigan, Surveys of Consumers .

To conclude, the data suggest that the FOMC's announcement of an explicit inflation objective had some effect on professional forecasters' long-run inflation expectations, but not on households' expectations. Admittedly, inflation expectations of professional forecasters did not immediately jump to the FOMC's objective, so it is not clear just how much of change in professional forecasters' expectations can be attributed to the FOMC's announcement versus other factors, such as a general reduction in uncertainty as economic conditions improved and actual inflation remained moderate. That said, given that the decline in the SPF inflation expectations, the tightening of the distribution, and the increase in the share expecting exactly 2 percent inflation started around the time of the announcement, it is likely the FOMC's announcement influenced the views of professional forecasters. We cannot say the FOMC's announcement had the same influence on households.

References:

Binder, Carola, "Fed Speak on Main Street," working paper (2014).

Clark, Todd E., and Taeyoung Doh, "Evaluating Alternative Models of Trend Inflation," International Journal of Forecasting, Volume 30, Issue 3 (2014), 426-448.

Faust, Jon, and Jonathan H. Wright, "Forecasting Inflation," in G. Elliott and A. Timmerman (Eds.) Handbook of Economic Forecasting, volume 2A. Amsterdam: North Holland (2013).

Nechio, Fernanda, "Have Long-term Inflation Expectations Declined?" Federal Reserve Bank of San Francisco Economic Letter, no. 2015-11 (2015).

Zaman, Saeed, "Improving Inflation Forecasts in the Medium to Long Term," Federal Reserve Bank of Cleveland Economic Commentary, no. 2013-16. November 16 (2013)

1. This may be because long-run inflation expectations proxy quite well for the trend in inflation. Including a measure of the trend improves the quality of inflation predictions. See, among others, Faust and Wright (2013), Clark and Doh (2014), and Zaman (2013). Return to text

2. The figure starts in 2011, the time when the SPF implemented a check to confirm that respondents' expectations for inflation 6 to 10 years ahead were consistent with their answers about expected inflation during the next 5 and the next 10 years. In order to use longer sample period we focus on SPF expectations for 10-year PCE inflation in the rest of the analysis. Return to text

3. Nechio (2015) finds that the decline in expected PCE inflation in years six through ten in the SPF survey is primarily driven by revised expectations from forecasters who overestimated inflation in the aftermath of the Great Recession. Return to text

4. In addition, in the second quarter of 2012, the SPF panelists were explicitly told that on January 25th, 2012 the FOMC had reached a broad agreement on some principles regarding its long-run goals, including that "The committee judges that inflation at the rate of 2 percent, as measured by the annual change in the price index for personal consumption expenditures, is most consistent over the longer run with the Federal Reserve's statutory mandate" In the same quarter, the Philadelphia Fed's survey of Professional Forecasters included a special question which asked the panelists "...whether their long-run forecast for inflation in the price index for personal consumption expenditures (PCE) differs in an economically meaningful way from the FOMC's longer-run goal for inflation of 2 percent." About three-quarters of the panelists who answered the special question indicated that their long-run forecasts for PCE inflation did not differ from the FOMC's goal in an economically meaningful way. The rest thought that inflation in the long run will exceed 2 percent and the FOMC will not achieve its goal. Return to text

5. Statistical tests strongly reject the equality of the variances in the responses of professional forecasters across the two periods. A similar narrowing of the distribution is observed for PCE inflation in years 6 to 10 (not shown). Relatedly, the differences between the upper and lower quartiles for all SPF-based measures of longer-run expected inflation (not shown) have declined noticeably since 2012, with the interquartile ranges for the 10-year and six-to-ten-year forward measures of expected PCE inflation narrowing to historically low levels. Return to text

6. We tested for difference in means between the two three-year periods, prior and following the FOMC's inflation objective announcement. The errors were corrected for heteroskedasticity and autocorrelations using a Newey-West procedure with 1 lag (the results were not sensitive to using 4 lags). Return to text

7. Based on analysis of Michigan survey micro data, Binder (2014) concludes that the announcement of an inflation objective has not reached the general public and inflation expectations of consumers are weakly anchored. Return to text

Please cite as:

Detmeister, Alan K., Daeus Jorento, Emily Massaro, and Ekaterina V. Peneva (2015). "Did the Fed's Announcement of an Inflation Objective Influence Expectations?" FEDS Notes. Washington: Board of Governors of the Federal Reserve System, June 08, 2015. https://doi.org/10.17016/2380-7172.1550

Disclaimer: FEDS Notes are articles in which Board economists offer their own views and present analysis on a range of topics in economics and finance. These articles are shorter and less technically oriented than FEDS Working Papers.