FEDS Notes

Print

PrintMay 26, 2015

The FOMC meeting minutes: An assessment of counting words and the diversity of views

Ellen E. Meade, Nicholas A. Burk, and Melanie Josselyn1

The Federal Reserve's communications with the public have evolved substantially since the early 1990s and today include: policy statements released shortly after the conclusion of monetary policy meetings; minutes of those meetings issued three weeks later; quarterly economic forecasts from the members of the Federal Reserve Board of Governors and the presidents of the Federal Reserve Banks; the Chair's press conferences four times per year; a semi-annual Monetary Policy Report that is submitted to the Congress and released to the public, along with the Chair's testimony on that report; and transcripts of monetary policy meetings published after five years. In addition, the public websites maintained by the Board and the 12 Federal Reserve Banks provide reports, testimony, speeches, and a wealth of other information on the policy and operations of the Federal Reserve System.

In this note, we focus on the minutes of Federal Open Market Committee (FOMC) meetings. Summaries of FOMC meetings have been released to the public in some form since 1936; detailed minutes like those available today have been released since 1993. Between 1993 and the end of 2004, minutes for each meeting were released after the subsequent meeting and so did not inform the public about the most recent thinking or discussions of the FOMC. In December 2004, the Committee decided to begin publishing the minutes 21 days after each FOMC meeting, shortening the publication lag by several weeks and providing the public with more timely information about policy deliberations and the rationale for policy decisions.

The minutes provide a detailed summary of the discussion at an FOMC meeting.2 Typically, an FOMC meeting begins with a staff review of foreign currency and domestic open market operations over the intermeeting period; meeting participants have the opportunity to question the staff on these market developments. Next comes the "economic go-round," which begins with several staff presentations on developments in, and prospects for, the economies of the United States and foreign countries. After asking any questions they may have on those presentations, all meeting participants--the Federal Reserve governors and the presidents of the 12 Federal Reserve Banks--discuss their views on economic developments and the outlook. Generally, Reserve Bank presidents include in their remarks commentary from industry contacts and information about recent economic developments in their Districts. In addition, four times each year, the economic go-round includes a staff summary of the economic projections submitted by FOMC participants.3

A go-round on monetary policy follows the economic go-round. A staff briefing outlines policy options and discusses several alternatives for the statement that the Committee will issue after the meeting. Following questions, the governors and Reserve Bank presidents outline their views on policy and discuss possible amendments to the language in drafts of the Committee's statement. At the conclusion of that discussion, the Committee members vote on the policy that will be followed over the period until the next FOMC meeting and on the statement that will be released shortly after the meeting is adjourned. A key feature of the governance of Federal Reserve monetary policy decisions is that, while all Reserve Bank presidents participate in the discussion at FOMC meetings, not all are voting members of the Committee. The Federal Reserve Act specifies that Committee "members"--that is, those who vote on policy--include all Federal Reserve governors, the President of the Federal Reserve Bank of New York, and four of the other 11 Federal Reserve Bank presidents who vote according to a specified rotation.

In addition to the review of financial market developments and the go-rounds on the economy and monetary policy, many FOMC meetings include discussion of a special topic. In recent years, for example, meeting participants have discussed the Federal Reserve's large-scale asset purchase programs, the forward guidance about future policy that is contained in the Committee's postmeeting statement, and the consensus statement on the Committee's longer-run goals and monetary policy strategy that was first issued in January 2012. The minutes of FOMC meetings summarize participants' discussions of such special topics as well as their comments during the regular go-rounds.

The role of the minutes and the postmeeting statement

Transcripts from FOMC meetings around the time that the Committee decided to expedite the release of the minutes shed some light on the role that policymakers see the minutes playing in their communications about monetary policy, particularly relative to the postmeeting statement that the Committee releases to the public shortly after the conclusion of each FOMC meeting. In May 2005, Reserve Bank Presidents Guynn (Atlanta) and Poole (St. Louis) noted their increasing discomfort with the fact that the statement did not reflect the widespread uncertainty that meeting participants were expressing about policy at that meeting. They wanted that range of uncertainty to be presented in the statement, "because, otherwise, the statement would not truly reflect what happened at the meeting."4 Chairman Greenspan responded that "what is in the minutes, even though they are released later, reflects what occurred before we voted on the statement. So whatever the Committee votes is the Committee's view at that point."5 At a meeting in 2006, Chairman Bernanke framed the relative roles of the statement and the minutes slightly differently, saying, "... I do not think that the minutes and the statement are perfect substitutes. The statement, after all, is much more timely, and it represents something closer to a consensus or median view of the Committee as opposed to the minutes, which try to express the range of views and discussion around the table."6 These extracts from FOMC transcripts suggest that policymakers see the minutes as providing insight about the breadth of views that the postmeeting statement does not provide.

All of the minutes released since the end of 2004 on the expedited schedule have reflected not only views expressed by Committee "members" but also those articulated by meeting "participants," a larger group that includes those Reserve Bank presidents who do not vote. The minutes' account of the economic go-round summarizes the views expressed by participants, while the section titled "Committee Policy Action" includes only the members because they are responsible for the policy decision. At times since 2008, the minutes have included participants' views on particular aspects of monetary policy when the range of views expressed by participants was broader than that expressed by the members alone.7

Another way in which the meeting minutes are informative about the diversity of views is through the use of "quantitative" or "counting" words--such as "few" or "many"--to characterize the number of members or participants aligned with a particular view. In their article on the minutes, Danker and Luecke (2005) provide a list of the quantitative words, which are shown on Table 1 ordered from largest to smallest. We add to this list two other counting words that are used with some frequency in the minutes: "some" and "a number of."

| Table 1. Quantitative words used in the FOMC minutes |

|---|

|

"all" |

| "all but one" |

| "almost all" |

| "most" |

| "many" |

| "several" |

| "few" |

| "a couple" or "two" |

|

"one" ... "another |

Source: Deborah J. Danker and Matthew M. Luecke (2005), "Background on FOMC Meeting Minutes," Federal Reserve Bulletin, Spring, pp. 175-179. |

An analysis of the "counting" words

The question we are interested in is, do the FOMC minutes present diverse perspectives and has that diversity changed over time? To find the answer, we subject the FOMC minutes released from 2005 through 2014 to some elementary text analysis and provide an assessment of the dispersion of viewpoints expressed through an examination of the quantitative words. The frequency of these counting words can be used as a measure of the range of opinion expressed at an FOMC meeting.

For the purposes of this analysis, we examined all sections of the minutes that describe policymakers' discussion at the meeting; these are, primarily, the sections on the economic and monetary policy go-rounds titled "Participants' Views on Current Conditions and the Economic Outlook" and "Committee Policy Action," respectively, although we also examined any special sections or additional paragraphs that included sentences pertaining to views expressed by participants.8

Before turning to our findings, we note a few details about our counting procedures. First, statements that represent unanimity are sometimes expressed explicitly, as in "all members judged;" at other times, statements of near unanimity are implicit, as in "participants judged" or "the Committee judged." In making the counts, we grouped these explicit and implicit statements together with statements using "all but one" and "almost all" to form a grouping that reflects a high degree of consensus.9 Second, the quantitative word "one" is sometimes used in a "one ... another" construction; when that occurred, we counted both "one" and "another" as separate views. Finally, we counted only expressions of views or opinions, and not mere discussions of a topic.

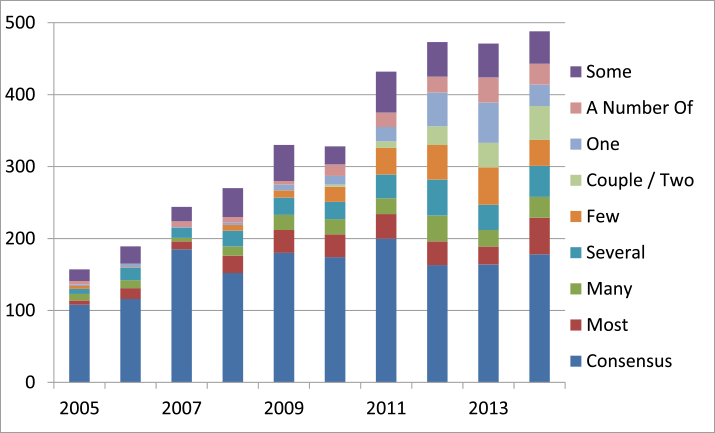

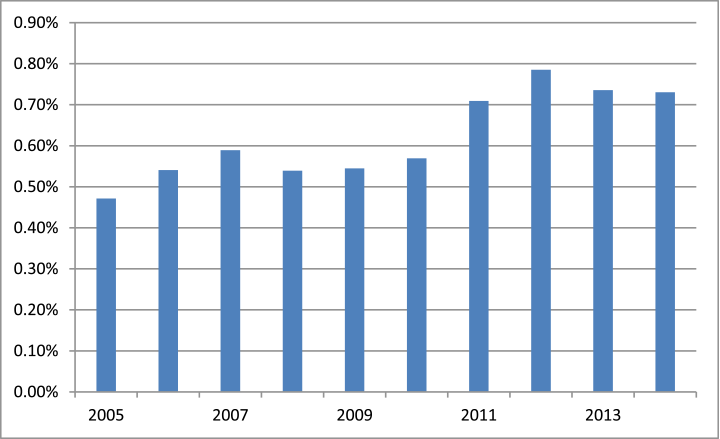

It is important to note that the FOMC minutes have gotten considerably longer over time. In 2005, the first year that the minutes were released on their current, expedited schedule, the average length per meeting was just under 4200 words.10 By 2014, the word count had risen to around 8350, with the bulk of this rise occurring between 2005 and 2009. The total annual frequency of the counting words from participants' and members' paragraphs of the minutes has risen over time as well, particularly since about 2011 (chart 1). Interestingly, the counting words have risen as a share in the total number of words (chart 2), pointing either to a greater diversity of viewpoints or to more complete reporting of the diversity of views.

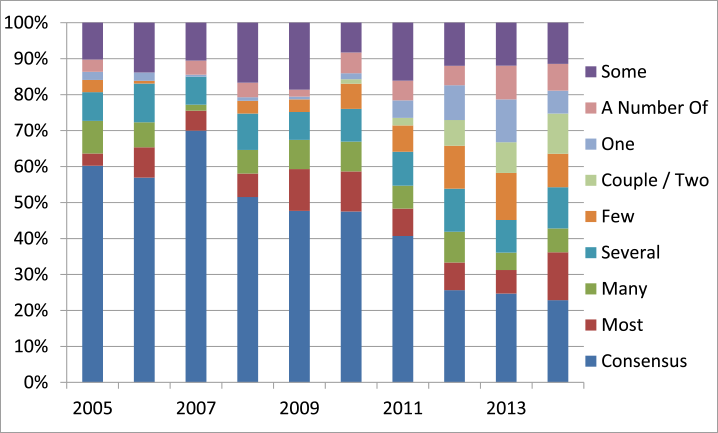

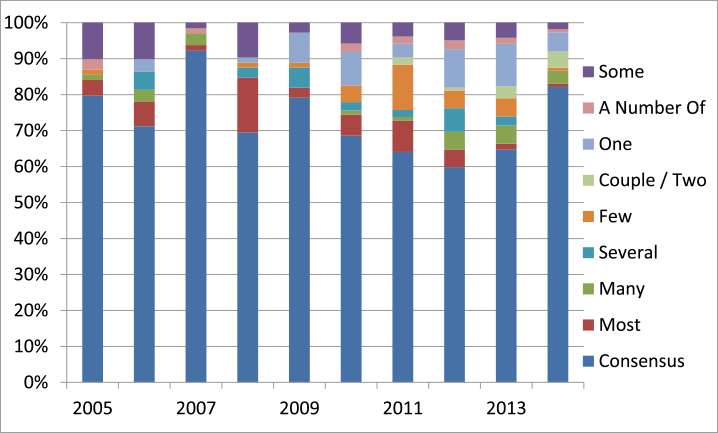

The total number of paragraphs that reflect views expressed by members is substantially smaller than the total number of paragraphs describing participants' views--sometimes substantially so. Thus, it is not surprising that the total count for the quantitative words is higher for participants' paragraphs than for members' paragraphs (not shown). Since 2007, the quantitative words in participants' paragraphs of the minutes have accounted for about 75 to 80 percent of all quantitative words used.

Chart 3 provides the share of each counting word in the total for participants (upper panel) and members (lower panel) for each year. Highly consensual statements (shown as "consensus") comprised nearly 60 percent of participants' paragraphs in 2005, compared with about 25 percent in 2014. Members' paragraphs have a higher proportion of "consensus" statements, which is to be expected in light of the role that the Committee's statement and the discussion of it plays in the members' paragraphs. In 2014, "consensus" statements constituted 80 percent of members' paragraphs, although for several years prior the share was somewhat lower--generally between 60 and 70 percent. A wider diversity of opinion among participants and members might be expected in the aftermath of the financial crisis given that, after the Committee reduced the target for the federal funds rates to nearly zero in December 2008, the Federal Reserve began using nontraditional monetary policy--namely, large-scale asset purchases and forward guidance--to provide additional stimulus to the economy. These nontraditional monetary policies were less familiar and were therefore less well understood. Policymakers debated their efficacy and costs and spent a great deal of time at FOMC meetings discussing the implications and effects of them. In addition, the greater diversity of viewpoints could reflect a changing composition of policymakers with different opinions.11

In conclusion, the FOMC meeting minutes are a key means for informing the Congress and the public about the full range of policymaker opinion and debate about monetary policy issues, and thus help ensure that the Federal Reserve is accountable to the Congress and the public. Since 2005, the minutes have gotten considerably longer. Our analysis of the quantitative words used in the minutes indicates that the meeting minutes capture a wide diversity of viewpoints expressed by FOMC policymakers and that this diversity appears to have increased over time, particularly since the financial crisis.

1. The authors thank Bill English, Thomas Laubach, Steve Meyer, and Bob Tetlow for comments. Return to text

2. For a more detailed discussion of what happens at an FOMC meeting, see the speech "Come with Me to the FOMC" that Governor Elizabeth A. Duke gave to the Money Marketeers of New York University in October 2010. Return to text

3. These projections have been collected since October 2007. Tables and charts of the projections are released to the public prior to the Chair's press conference and a detailed analysis is released three weeks later in the "Summary of Economic Projections" section of the minutes for the relevant FOMC meetings. Return to text

4. President Poole, Transcript of FOMC meeting, May 3, 2005, p. 86. Return to text

5. Chairman Greenspan, Transcript of FOMC meeting, May 3, 2005, p. 86. Return to text

6. Chairman Bernanke, Transcript of FOMC meeting, March 27-28, 2006, p. 140. Return to text

7. For example, in the minutes of the January 2013 meeting, there were three paragraphs at the end of the economic go-round section on the benefits and costs of the Committee's open-ended asset purchase program, the pace of asset purchases, and the economic thresholds in the Committee's forward guidance. On some occasions, there have been separate sections in the minutes pertaining to a discussion of aspects of monetary policy; see, for example, the section titled "Policy Planning" in the minutes of the October 2013 meeting which relates participants' views on the strategy and tactics of future policy. Return to text

8. The "Committee Policy Action" section reflects views expressed by members; it does not reflect views expressed only by those participants who are not voting members. Return to text

9. We also included statements using the construct "participants generally judged..." or "members generally judged..." in this grouping. Return to text

10. The word counts and other analysis in this section include scheduled meetings and exclude video conference (unscheduled) meetings. The minutes of the first meeting in a year are significantly longer than subsequent meetings owing to discussion of procedural matters. Return to text

11. For example, since the beginning of 2005, there has been considerable turnover among Federal Reserve governors: Six governors appointed prior to 2005 resigned and, of the 12 governors appointed since 2005, only five of them remain.Return to text

Please cite as:

Meade, Ellen E., Nicholas A. Burk, and Melanie Josselyn (2015). "The FOMC Meeting Minutes: An Assessment of Counting Words and the Diversity of Views," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, May 26, 2015. https://doi.org/10.17016/2380-7172.2048

Disclaimer: FEDS Notes are articles in which Board economists offer their own views and present analysis on a range of topics in economics and finance. These articles are shorter and less technically oriented than FEDS Working Papers.