FEDS Notes

Print

PrintFebruary 26, 2015

Where Are The Construction Workers?

Andrew Paciorek1

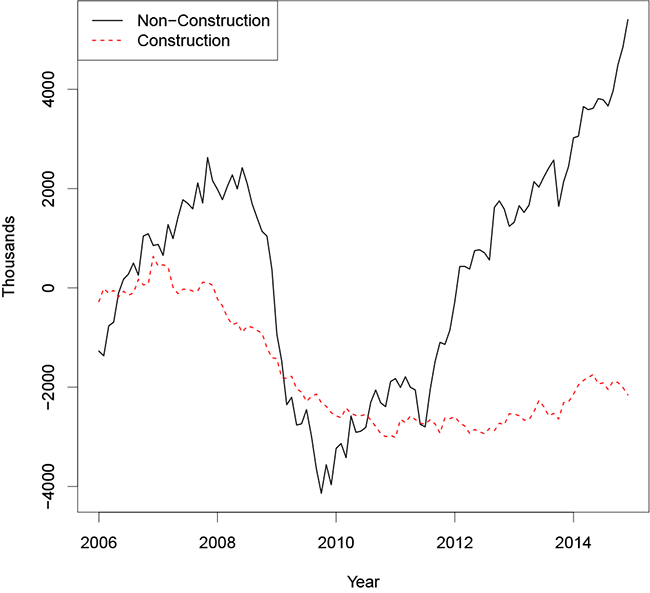

The labor market for construction workers suffered a massive shock in the wake of the housing bust, as demand for new homes dried up and firms rapidly shed workers. Employment in the construction sector fell nearly 25 percent from more than 11-1/2 million in 2006 to about 9 million in 2010. Even though the construction sector employs only about 7 percent of total employment, it accounted for about half of the economy-wide drop in employment over that period. Figure 1 shows the evolution of construction and non-construction employment, relative to their 2006 levels. Since 2010, the recovery in the construction sector has been exceptionally slow: Nine years after the bust began, construction employment has made up only about a third of its losses, even as non-construction employment has substantially exceeded its previous peak.2

The relatively weak recovery in construction employment is interesting for at least two reasons: First, construction work is a source of relatively high-wage jobs that do not require a college education, which have been in increasingly short supply as the job market becomes more polarized (Autor and Dorn 2013, e.g.).3 The housing bust appears to have exacerbated this polarization: As I discuss below, average real income has fallen by nearly 13 percent among workers who are relatively likely to be construction workers.

Second, many builders and contractors have reported difficulty finding new workers.4 The macroeconomic evidence for this story is mixed. Average wages in the construction sector have not been rising appreciably faster than for other workers. However, at the end of 2014, the average employed construction worker was working the most hours per week on record. This fact, combined with the anecdotes and survey evidence, suggests that low construction employment could be, at least in part, a symptom of a relatively tight supply of construction workers, rather than fully a consequence of low demand for new homes.

This note sheds light on these issues by looking at what happened to the construction workers who left the industry after 2006. I also examine the current labor market outcomes of people whose observable characteristics would have made them likely to be construction workers in the past. My analysis suggests that there is a sizable pool of workers who fit the profile of construction workers, at least in broad terms, but are currently out of the labor force.

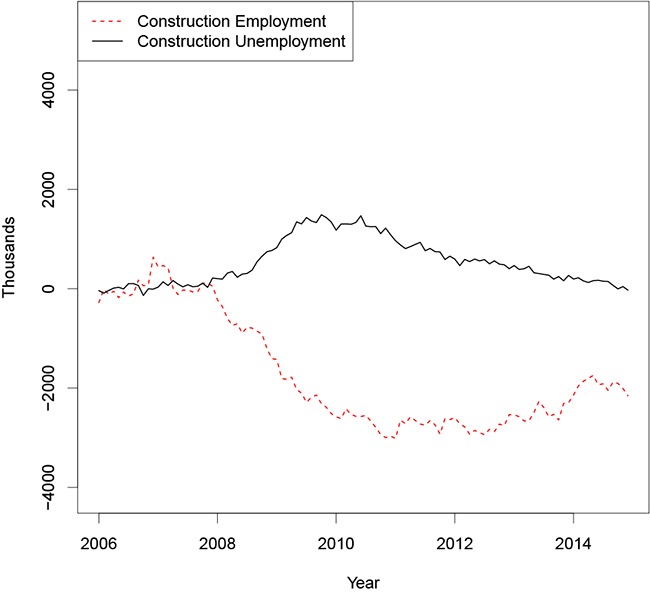

The first obvious place to look for formerly employed construction workers is among the ranks of the unemployed. Figure 2 shows that the decline in construction employment after 2007 was accompanied by a large increase in unemployed workers who reported that their most recent job was in construction. But while construction employment remains far below its 2006 level, construction unemployment has more or less returned to normal. This pattern indicates that, on net, most former construction workers must have flowed out of the sector entirely.

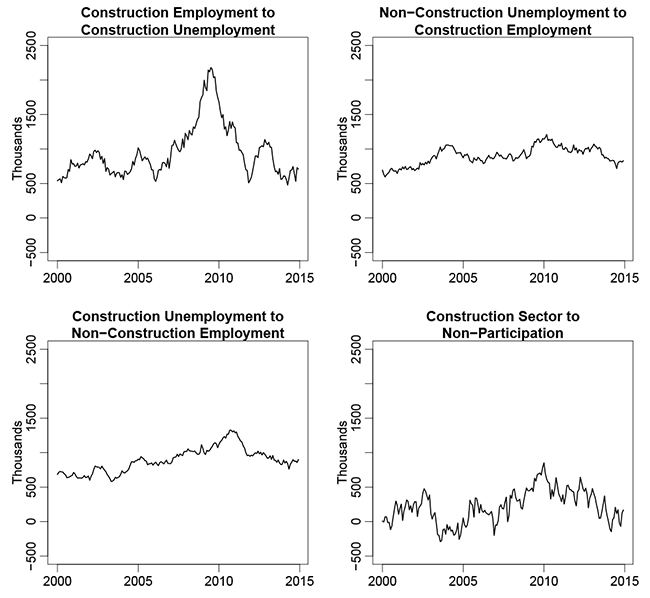

We can get a better sense of where these workers went by examining a longitudinally matched version of the CPS, which makes it possible to track most workers from month to month (Nekarda 2009). I divide all adults in the CPS sample into one of five categories: construction employment, construction unemployment, non-construction employment, non-construction unemployment, and non-participation. The four panels of figure 3 summarize the net flows across these categories that are most relevant for understanding the construction labor market from 2000 through 2014. For example, the top left panel shows the number of employed construction workers who flowed into unemployment, minus the number of unemployed construction workers who flowed into employment, over the 12 months prior to the date on the x-axis.

| Figure 3: Net Flows (12-Month Moving Sum) |

|---|

|

Source: Monthly Current Population Survey (matched sample).

Even when the industry was booming, from 2000 to 2005, between 500,000 and a million construction workers flowed into unemployment, on net, in each 12-month period, as part of the natural dynamics of the labor market. During the boom, this large net flow into unemployment was more than offset by the net flow of unemployed non-construction workers into construction employment (figure 3, top right).5 During the housing bust, however, the net number of construction workers flowing into unemployment soared to a peak of over 2 million per year. Although the flow into the industry from non-construction unemployment was actually somewhat higher in 2009 and 2010 than earlier in the decade--in part because there were simply so many more unemployed workers overall--it was nowhere near enough to offset the wave of unemployment, leading to the dramatic reduction in the size of the construction workforce shown in figures 1 and 2.

Where did the unemployed workers go? Although figure 3 shows only net flows, it is worth noting that the gross flow of unemployed construction workers back into construction employment was still very large during the housing bust, so many workers found new jobs in their old industry. But the top left panel of figure 3 makes clear that they were far outnumbered by workers flowing in the other direction. Instead, the number of unemployed construction workers shrank because they flowed out to employment in other sectors of the economy (figure 3, bottom left). This net outflow from the industry was quite large even in boom times, but roughly doubled during the bust.

In addition, a sizable number of workers flowed from the construction sector--from both employment and unemployment--out of the labor force. The bottom right panel of figure 3 shows the sum of these two net flows out of the labor force. The net flow was positive but small in the early 2000s and actually turned negative in 2004 and 2005, as construction drew workers into the labor force, on net. During the bust, however, the net flow turned sharply positive, and at the peak in 2010, nearly a million workers flowed out of the labor force. Since the bust, all four of the net flows in figure 3 have returned to roughly their pre-bust levels, which explains why construction employment is once again growing, albeit slowly, and construction unemployment is flat.

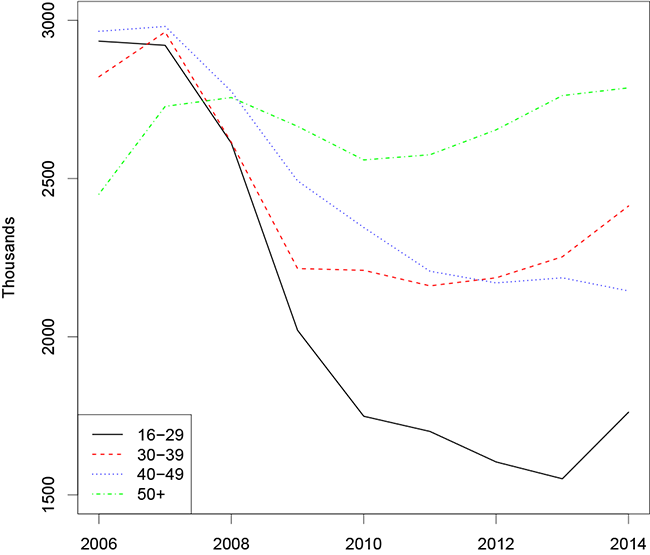

| Figure 4: Construction Employment by Age |

|---|

|

Source: Current Population Survey Annual Social and Economic Supplement.

While the flows analysis is informative, it is also useful to step back and examine the effects of these changes in flows on the stock of construction workers, for two reasons: First, while the matched CPS can be used to track former construction workers over short horizons, we do not know anything about them after more than a year or so. Second, the long duration of the housing slump means that many people who might have become construction workers never joined the sector in the first place.

This second phenomenon is indicated by the notable change in the age distribution. Figure 4 shows the stock of construction workers from the annual March CPS, broken out into four age bins. In March 2006, construction workers were roughly evenly distributed, with 2½ to 3 million workers in each of the 18-29, 30-39, 40-49, and 50-plus bins. In subsequent years, however, the number of workers in the youngest bin fell nearly in half, and there were also sizable declines in the middle two bins. In contrast, the 50-plus bin actually increased in size, on net. As a result, the average age of employed construction workers rose by more than 2½ years between 2006 and 2014, while the overall employed population aged by less than 1½ years. Since older workers typically have higher incomes, these changes in the age distribution help explain why average real income among construction workers only fell by about 3½ percent, rather than the 9 percent reduction implied had the average characteristics of construction workers remained fixed.6

The next question is what these missing young and middle-aged construction workers are doing instead. To get some traction on this question, we can examine the current labor market outcomes of the kinds of people who, given their observable characteristics, were relatively likely to be construction workers in 2006. To identify this group, I use March 2006 CPS data to estimate a logistic model where the dependent variable is an indicator for whether the adult is a construction worker, and the covariates include indicator variables for race, Hispanic ethnicity, citizenship status, educational attainment, and age. I then sort all adults according to the predicted values from this model and look at the top 20 percent.7 In 2006, about 16½ percent of this selected group actually worked in construction--versus about 5 percent of the adult population--and the group accounted for about 60 percent of total construction employment.

To examine the current outcomes of similar workers, I use the model estimated on 2006 data to predict probabilities of construction employment using subsequent years of CPS data and select the group that would have been in the top quintile in 2006. In March 2014, the selected group still accounted for about 60 percent of construction employment, but just 13-1/2 percent of the group was employed in construction, compared with 3.5 percent of the adult population.

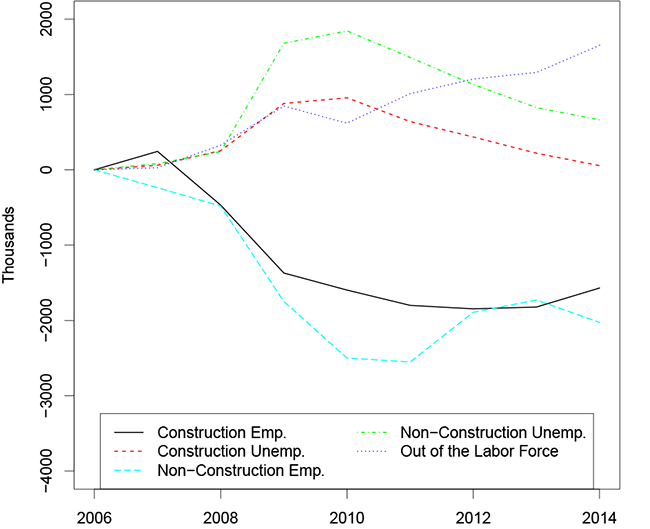

| Figure 5: Outcomes for Likely Construction Workers, Relative to 2006 |

|---|

|

Source: Current Population Survey Annual Social and Economic Supplement.

Figure 5 shows the evolution of labor market outcomes for this group of relatively high-probability construction workers.8 Relative to 2006, almost 2 million fewer were actually employed as construction workers by 2011. There was an even bigger decline in non-construction employment, although a modest rebound began in 2012. Meanwhile, construction unemployment among likely construction workers first rose by up to 1 million but has since fallen back close to its 2006 level. Unemployment in other sectors shows a similar pattern but remained somewhat elevated in 2014. However, the largest increase has been among labor force non-participants, of whom there were roughly 2 million more in 2014 than in 2006.9

The chart thus indicates that there is a large and growing group of workers who, based on their observable characteristics, would have been relatively likely to be construction workers in 2006 but are instead out of the labor force. This result is particularly striking because few people that I identify as likely construction workers are over the age of 60, and at most a quarter of the increase can be explained by increases in school or college attendance. As a result, the average real income among relatively high-probability construction workers has fallen by about 13 percent, compared with declines of 3 percent among employed construction workers and 4 percent among all adults, employed or not.

It seems there are many underemployed workers who appear to be relatively good candidates for construction employment, at least on the basis of these basic characteristics. In particular, there may be a large pool of people who would find construction work attractive but did not enter the industry during the bust years. The open question is how difficult it will be to draw these people into the sector if demand for new homes picks up. These potential workers may require more training to compensate for "lost" on-the-job training during the bust years. Alternatively, if labor supply decisions are "sticky", underemployment among relatively high-probability construction workers--mostly non-college educated men--could be more persistent, regardless of the training available. This conjecture suggests an important topic for future research.

Bibliography

Autor, David H. and David Dorn (2013). "The Growth of Low-Skill Service Jobs and the Polarization of the U.S. Labor Market", American Economic Review, 103 (5), pp. 1553-1597.

Blinder, Alan (1973). "Wage Discrimination: Reduced Form and Structural Estimates", Journal of Human Resources, 8 (4), pp. 436-455.

Emrath, Paul (2014). "Builders See Shortages of Labor and--Especially--Subcontractors". See http://www.nahb.org/generic.aspx?sectionID=734&genericContentID=231854&channelID=311.

Nekarda, Christopher J. (2009). "A Longitudinal Analysis of the Current Population Survey: Assessing the Cyclical Bias of Geographic Mobility". See http://chrisnekarda.com/2009/05/a-longitudinal-analysis-of-the-current-population-survey/

Oaxaca, Ronald (1973). "Male-Female Wage Differentials in Urban Labor Markets", International Economic Review, 14 (3), pp. 693-709.

1. I am grateful to Chris Nekarda for assistance with the longitudinal CPS data and to Chris, Stephanie Aaronson, Tomaz Cajner, Steve Laufer, Paul Lengermann, and Michael Palumbo for thoughtful comments. Any errors are my own. Return to text

2. This paragraph refers to monthly employment figures from the Current Population Survey (CPS). Construction employment is lower in the payroll survey because many construction workers are self-employed, and hence not covered by the survey, but the qualitative patterns described here are the same. Return to text

3. In March 2014, the average annual income for construction workers without a college degree was about $40,500, compared with $34,500 for non-college educated workers in other industries. Return to text

4. For example, Emrath (2014) discusses recent evidence from a National Assocation of Homebuilders survey. Return to text

5. Since the CPS asks unemployed workers for their most recent industry of employment, it is possible that many of the unemployed non-construction workers flowing into construction employment were in fact construction workers at some previous point. Return to text

6. This result draws on a Oaxaca-Blinder decomposition (Blinder 1973; Oaxaca 1973). The included covariates are sex, race, Hispanic ethnicity, citizenship status, education, and age. Return to text

7. Given the prevailing likelihoods of construction employment, the selected group is entirely male and largely non-college educated. They are also somewhat younger, more Hispanic, and less likely to be U.S. citizens than the general adult population. The interpretation of the results for this group is not sensitive to reasonable alternative cutoffs. Return to text

8. Note that the lines do not sum to zero within a given year because changes in the characteristics of the population--aging, for example--imply that progressively fewer people meet the cutoff implied by the 2006 estimates. Indeed, there were roughly 1.2 million fewer likely construction workers in 2014 than in 2006, even though there were 20 million more adults in the country. Return to text

9. Non-participation among this group also rose during the early 2000s, but the increase has been appreciably steeper since 2006. Return to text

Please cite as:

Paciorek, Andrew D. (2015). "Where Are The Construction Workers?" FEDS Notes. Washington: Board of Governors of the Federal Reserve System, February 26, 2015. https://doi.org/10.17016/2380-7172.1499

Disclaimer: FEDS Notes are articles in which Board economists offer their own views and present analysis on a range of topics in economics and finance. These articles are shorter and less technically oriented than FEDS Working Papers.