FEDS Notes

Print

PrintSeptember 24, 2015

The Effects of FOMC Communications before Policy Tightening in 1994 and 20041

Ellen E. Meade, Yoshio Nozawa, Lubomir Petrasek, and Joyce K. Zickler

The ways in which the Federal Open Market Committee (FOMC or "Committee") communicates its views on economic and financial conditions, the economic outlook, and its policy intentions have evolved over time. Using information from publicly available historical policy records, we describe the Committee's communications as it approached the decisions to increase the target for the federal funds rate in February 1994 and June 2004 and we examine the effect those communications had on policy expectations in financial markets.

Tightening in 1994

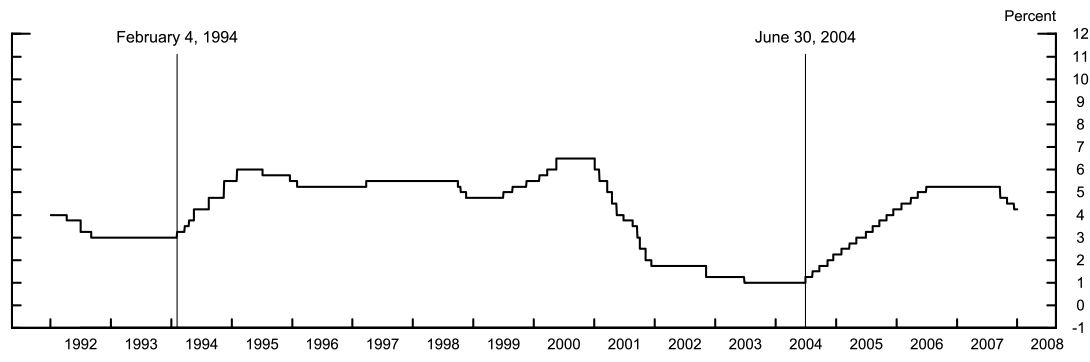

At its meeting in February 1994, the FOMC voted to increase the target federal funds rate by 25 basis points to 3.25 percent (figure 1), the first increase in the target since 1989. At that time, the Committee did not communicate actively with the public as it does today and its communication tools were very limited. For example, statements were not issued following FOMC meetings, changes in the federal funds rate target were not announced, and the minutes and directive for each FOMC meeting were not released until two days after the subsequent meeting. (The directive contains the instructions regarding the implementation of monetary policy that the FOMC issues to the Open Market Desk at the Federal Reserve Bank of New York.) The economic projections prepared by the Committee were made publicly available only twice a year, in February and July, in the Monetary Policy Report to the Congress (MPR) and the accompanying testimony by the Chair. Thus, in late December 1993 and early January 1994, the most up-to-date information on the Committee's thinking was the assessment contained in the minutes of the November meeting: "In the Committee's discussion of policy for the intermeeting period ahead, the members generally agreed that despite various indications of a pickup in economic growth, the underlying economic situation and the outlook for inflation had not changed sufficiently to warrant an adjustment in monetary policy." The November directive to the Open Market Desk indicated that the Committee would maintain the current degree of reserve restraint and had a balanced, or "symmetric," view of the likely adjustment of policy over the intermeeting period, saying that either "slightly greater" or "slightly lesser" reserve restraint might be warranted.2

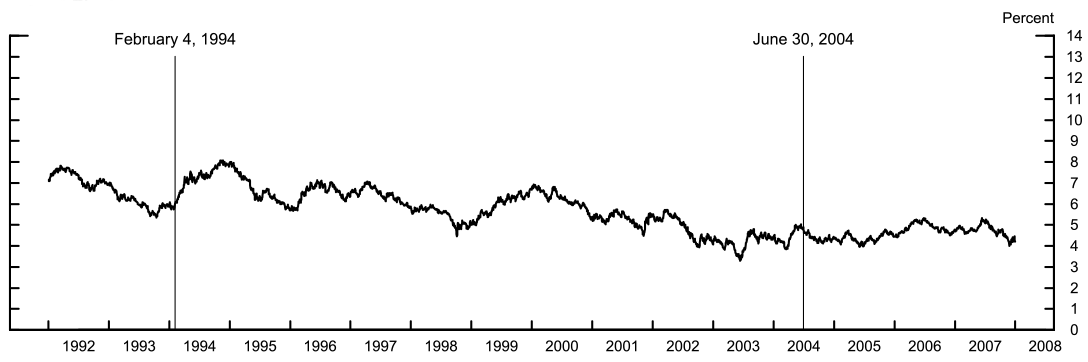

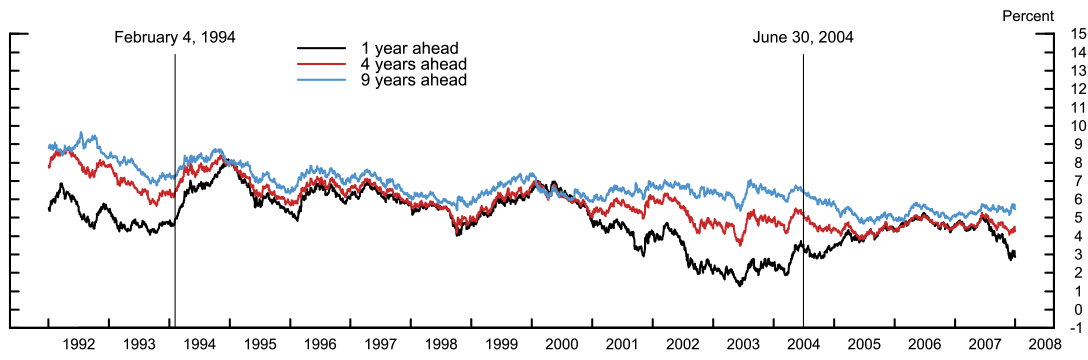

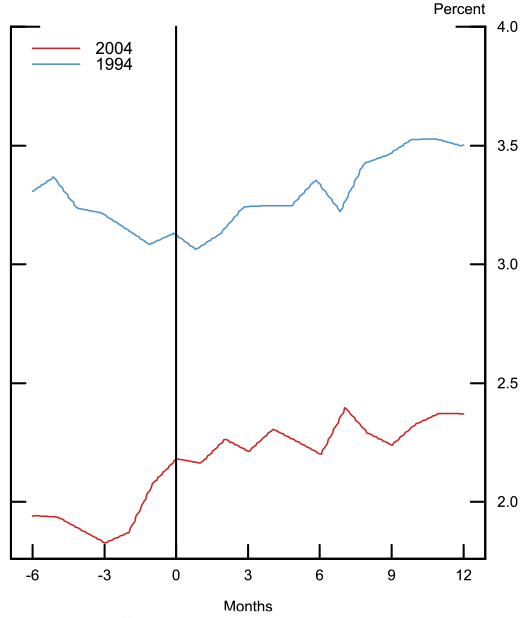

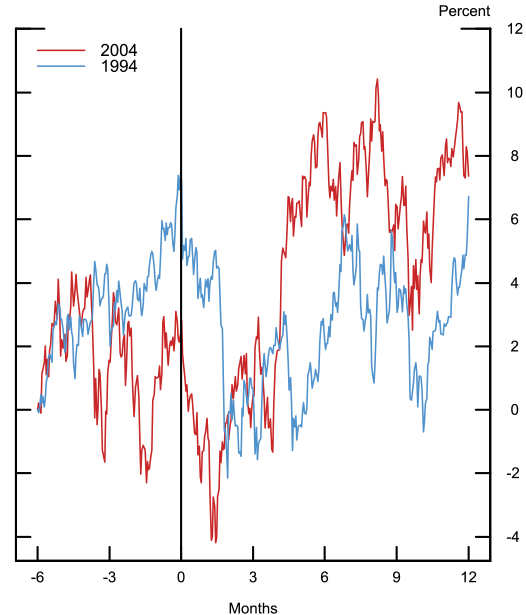

Despite the strength of incoming economic data over the fall and winter of 1993, market expectations for the federal funds rate did not increase significantly. Treasury yields and forward rates at short and longer-term maturities remained near the lower end of their recent ranges (figures 2 and 3). Data from the Blue Chip survey at the time suggest that some market participants may have underestimated the economy's momentum and resulting inflationary pressures. The Blue Chip forecast for one-year-ahead real GDP growth (figure 4) did not increase, on net, in the six months prior to the policy tightening, and expectations for consumer price inflation one-year-ahead edged down (figure 5). Accordingly, market participants generally appeared to expect that the federal funds rate would remain unchanged in the near future (figure 6).

At their meeting in December 1993, FOMC participants discussed the best way to signal to financial markets and the public that a decision to raise rates might come soon. While some spoke of wanting a tightening decision at that meeting, Chairman Greenspan recommended that the Committee leave the target for the federal funds rate unchanged, but prepare to tighten policy early in 1994, if necessary. He also proposed that the directive remain symmetric and not signal any bias toward tightening during the intermeeting period, arguing that the decision to raise interest rates--a crucial step--should be taken by a vote of the Committee and not by the Chairman in between scheduled meetings. In response to a suggestion that the Chairman use an upcoming speaking opportunity to convey the Committee's thinking about the outlook for monetary policy, Chairman Greenspan used his testimony before the Joint Economic Committee on the Monday before the February FOMC meeting "to emphasize that monetary policy must not overstay accommodation" and that "the foundations of the economic expansion are looking increasingly well-entrenched." He went on to note that historical experience suggested that "higher price inflation tends to surface rather late in the business cycle" and that "the challenge of monetary policy is to detect such latent instabilities in time to contain them."

When the FOMC met later that week, participants generally agreed that the economy was entering 1994 with considerable forward momentum. They saw little likelihood of further progress in reducing inflation and a "distinct risk" of higher inflation if monetary policy remained very accommodative. These views were reflected in the projections prepared for the upcoming MPR. Against this backdrop, participants generally favored an increase in the target for the federal funds rate. A number argued in favor of a 50-basis-point increase in order to get out in front of inflation, but most wanted to remove the high degree of policy accommodation gradually. Committee members expressed concerns about the possibility of a large announcement effect because it had been so long since the Committee's last policy rate tightening in 1989. They decided to raise the target rate by 25 basis points, and for the first time, the Chairman issued a very brief postmeeting statement announcing the change. A fuller explanation of the Committee's views came a few weeks later in the Chairman's monetary policy testimony to the Congress.

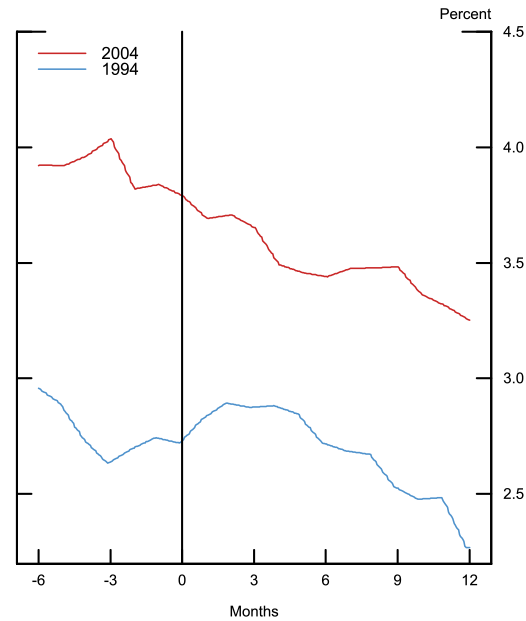

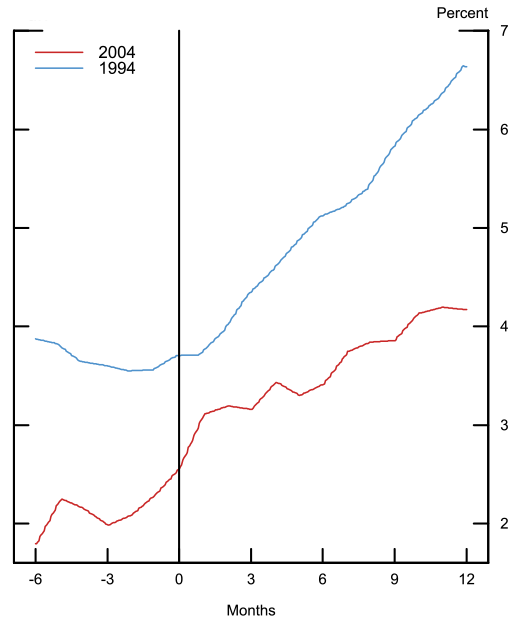

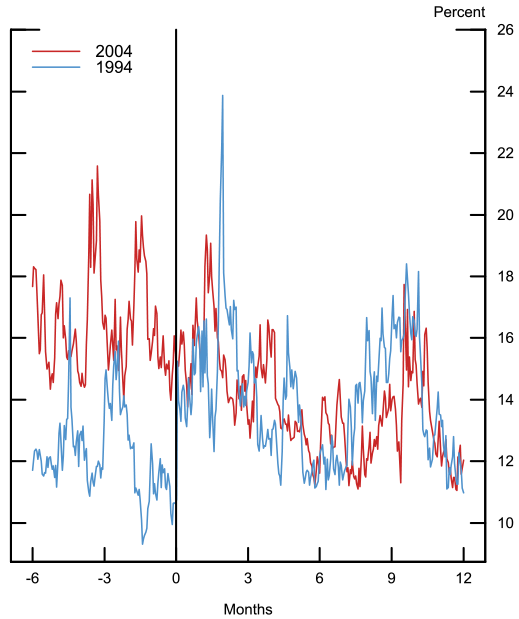

The tightening, as well as the release of Chairman Greenspan's brief statement announcing the decision following the FOMC meeting, were not anticipated by the public, leading to a sharp run-up in interest rates and a temporary increase in financial market volatility. As shown in figure 7, the 10-year nominal Treasury yield increased 14 basis points on the day of the announcement, and about 200 basis points over the next nine months. Meanwhile, the yield curve flattened as short-term rates rose even more sharply (figure 3). Several factors may account for the sharp rise in Treasury yields. The tightening came sooner than investors had anticipated. Moreover, the expected path of the federal funds rate over the coming year implied by futures market quotes right before the tightening--111 basis points--substantially underestimated the subsequent tightening--300 basis points. The more-rapid pace of tightening occurred in response to data releases over several months that repeatedly led to a marking up of expectations for economic growth and inflation (figures 4 and 5) and, in turn, called for a higher level of yields. There was also a significant rise in uncertainty about the paths of interest rates, as indicated by the widening of confidence intervals on the federal funds rate in figure 8.

| Figure 8: 6-Month-Ahead 90% Confidence Intervals on the Federal Funds Rate |

|---|

|

Note: The confidence interval is estimated using Eurodollar futures options.

Source: CME, CBOT with permission from CME Group, Inc.

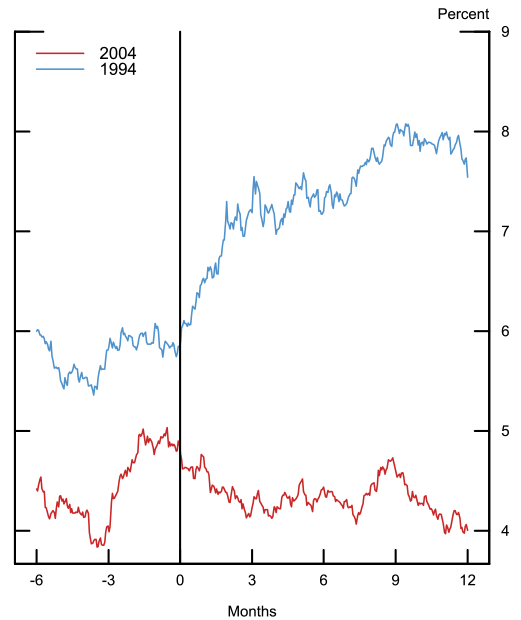

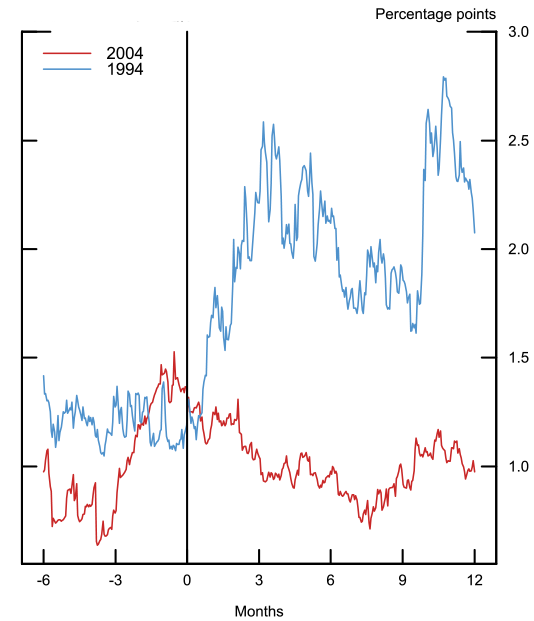

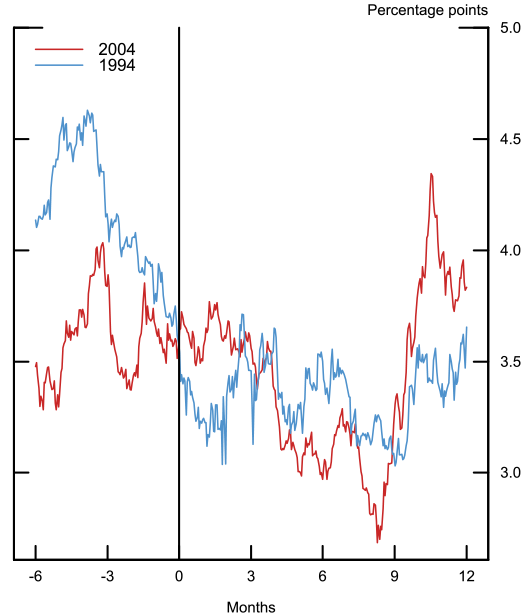

In contrast to interest rates, stock prices stabilized quickly after an initial negative reaction, and fully recovered their losses later in the tightening cycle (figure 9), likely because the economy strengthened. Measures of the implied volatility of stock prices initially increased, but reverted to normal levels after several months (figure 10). Corporate yield spreads, particularly those faced by lower-tier issuers, also narrowed (figure 11), consistent with investors judging that the economic outlook was improving.

| Figure 11: High-yield Corporate Bond Spreads |

|---|

|

Source: Bloomberg, Federal Reserve Bank of New York, staff estimates.

Tightening in 2004

By the time of the June 2004 FOMC meeting, the Committee was routinely issuing postmeeting statements. However, the minutes and directive for each FOMC meeting were still not released until two days after the subsequent meeting. As a result, the postmeeting statements garnered significant attention in financial markets. The statements at the time provided an indication of the Committee's view about risks to the outlook for economic growth and inflation--the "balance of risks." In addition, the Committee had also begun to use a time-dependent form of forward guidance about the likely stance of policy. For instance, the August 2003 postmeeting statement stated that policy accommodation could be maintained "for a considerable period;" in January 2004, that forward guidance was changed to indicate that the Committee thought it could be "patient in removing" monetary policy accommodation. Thus, the Committee used a sequence of changes in the balance of risks and forward guidance language in the months leading up to the June 2004 tightening to signal that its assessment of the economy was evolving and that it was getting closer to raising its target for the federal funds rate.

Over the months leading up to the tightening in June 2004, financial market expectations for the timing of the first increase in and the subsequent path for the target federal funds rate shifted noticeably in response to the receipt of economic data and FOMC communications. During the late summer and fall of 2003, core PCE inflation had slipped to 1¼ percent and the Committee had noted in its postmeeting statements the risk that inflation could become "undesirably low" as its "predominant concern for the foreseeable future." By December 2003, the risks of further disinflation had come down, and the Committee stated that the risk of a fall in inflation was "almost equal" to that of a rise. At the March 2004 meeting, the Committee decided to retain its assessment that the risks to economic growth were "roughly equal" and the risks to inflation were "almost equal" even though some participants noted that rising energy and commodity prices along with reports of pricing power in some sectors suggested that the risks to inflation had become more balanced, because many Committee members continued to believe that slack in labor and output markets would keep inflation low. At the meeting, Chairman Greenspan talked about how a move to full balance in describing the risks to inflation would be consistent with "continuing to adjust our statements meeting by meeting and fostering a momentum that might enable us at the appropriate time to tighten with minimum effect on rates." However, he argued that, although it was "a very close call," he wanted to "avoid creating momentum toward a policy action if, indeed, the economic expansion was slowing down."

Financial markets read the Committee's assessment of the economy in its March statement as having a soft cast. However, by May, a strong employment report, higher core CPI inflation, and some signs of a pickup in labor compensation led to rapidly shifting expectations, both among policymakers and in financial markets. Near-term inflation expectations had been rising (figure 5), although longer-run measures of inflation expectations remained stable. Bonds sold off in response to heightened prospects for policy tightening and interest rates moved up noticeably (figures 2 and 3).

At the May 2004 meeting, policymakers revised the statement language to indicate that the risks to price stability had "moved into balance." In addition, they replaced the forward guidance language indicating that the Committee would be "patient in removing" policy accommodation with "the Committee believes that policy accommodation can be removed at a pace that is likely to be measured." In discussing how to position the Committee to move at an upcoming meeting, several participants wanted to send a signal that, while the Committee might want to start to tighten early, it intended to be gradual; a number of them specifically mentioned that they wanted to avoid having financial markets assume that the Committee might be as aggressive as it had been during the 199495 tightening cycle. Several also noted that the sentence describing their expected policy path would indicate that inflation was still relatively low and resource slack remained, and it would therefore lend support to the expectation of a gradual pace of tightening. The use of the words "likely to be measured" seemed to satisfy those who wanted the flexibility to move more aggressively, if needed, particularly if the outlook for inflation worsened.

The replacement of the sentence in the statement that the Committee could be "patient" in removing policy accommodation with new guidance that accommodation could be removed at a "measured pace" did not lead to a significant reaction in financial markets. However, a subsequent series of economic releases showing strong gains in employment and spending caused investors to anticipate that policy tightening would begin with an increase of 25 basis points in the target federal funds rate at the June meeting and would be followed by similar increases at each of the remaining four meetings of the year. Measures of interest rate uncertainty (figure 8) also moved up noticeably.

At the June 2004 meeting, most participants agreed that the Committee needed to move policy back to neutral over a period of time, but a few indicated that they preferred removing any characterization of possible future policy actions from the postmeeting statement. Two members expressed reservations about retaining the "measured pace" language because it was likely to imply a steady tightening path of 25 basis points each meeting and might result in the Committee falling behind the curve as inflation rose. However, most viewed the addition of the sentence stating that "nonetheless, the Committee will respond to changes in economic prospects as needed to fulfill its obligation to maintain price stability" as providing scope for adjusting the path for the funds rate in response to incoming economic information and their interpretation of its implications for economic activity and inflation.

In part because of the change in the forward guidance in May, the market reaction to the June 2004 FOMC action was much more muted than the response to the tightening in February 1994. The 10-year Treasury yield in fact decreased 8 basis points on the day of the initial target rate increase (figure 7), and interest rates declined further across the term structure over subsequent months (figure 3). Standard measures of volatility and liquidity in the Treasury securities market held fairly steady at typical levels, and the confidence interval on the federal funds rate narrowed (figure 8), indicating that interest rate uncertainty decreased. Equity prices initially declined (figure 9), but quickly recovered amid declines in equity market volatility (figure 10). Corporate bond spreads narrowed (figure 11) and inflation expectations stabilized (figure 5).

Conclusion

The policy record shows that the FOMC's decisions about the appropriate time to begin to remove policy accommodation in February 1994 and June 2004 depended importantly on the evolution of policymakers' outlook for real economic activity, labor market conditions, and inflation. However, at the time of the February 1994 tightening, the Committee's policy communications with the public were limited and were not timely, and financial markets did not fully anticipate the Committee's decision. By the time of the June 2004 tightening, the Committee's policy communications had expanded significantly--in particular, the postmeeting statements that included assessments of the balance of risks and forward guidance were important in shaping investor expectations by signaling the Committee's assessment of how economic conditions were evolving and its thinking about when to raise the federal funds rate target.

1. The authors thank Bill English and Steve Meyer for comments, and Edward Atkinson, Eric Horton, and Blake Phillips for research assistance. Return to text

2. The directive specified the Committee's short-term operating objective in terms of a "degree of pressure on reserve positions." It also provided the Committee's inclination toward modifying policy over the intermeeting period--the "bias" or "tilt." Return to text

Please cite as:

Meade, Ellen E., Yoshio Nozawa, Lubomir Petrasek, and Joyce K. Zickler (2015). "The Effects of FOMC Communications before Policy Tightening in 1994 and 2004," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, September 24, 2015. https://doi.org/10.17016/2380-7172.1559

Disclaimer: FEDS Notes are articles in which Board economists offer their own views and present analysis on a range of topics in economics and finance. These articles are shorter and less technically oriented than FEDS Working Papers.