February 25, 2011

Unconventional Monetary Policy and Central Bank Communications

Vice Chair Janet L. Yellen

At the University of Chicago Booth School of Business U.S. Monetary Policy Forum, New York, New York

The U.S. Monetary Policy Forum has become an important venue for promoting an exchange of views among policymakers, academics, and financial market participants. I'm pleased to participate in this panel on lessons learned about unconventional monetary policy. In my remarks today, I'll highlight the role of central bank communications in bolstering the effectiveness of unconventional monetary policy.1 It is not my intention to provide new information about the outlook for the U.S. economy or monetary policy.

The Federal Open Market Committee (FOMC) has deployed unconventional monetary policy tools to promote economic recovery and price stability since late 2008. In particular, after the intensification of the financial crisis, conventional monetary policy became constrained by the zero lower bound on nominal interest rates. At that point, the FOMC began to provide forward guidance about the likely path of the federal funds rate, and the Federal Reserve also announced a program to buy agency debt and mortgage-backed securities (MBS). Over time, the purchase program was augmented substantially and was expanded to include longer-term Treasury securities. Furthermore, on several occasions, the FOMC has communicated to the markets about the likely longer-term trajectory of its holdings of Treasury securities, agency debt, and agency MBS.

In the remainder of my remarks, I will present some evidence regarding the effectiveness of these policy tools and discuss important similarities and differences in the transmission mechanisms through which they influence the economy. I will also present some simulations of a macroeconometric model to illustrate the importance of clear and effective communication in conjunction with the use of these unconventional policy tools.

Some General Observations

It is important to recognize at the outset that conventional and unconventional monetary policy actions bear many similarities. Forward guidance concerning the path of the federal funds rate, for example, is explicitly intended to influence market expectations concerning the future trajectory of shorter-term interest rates and thereby affect longer-term interest rates. That said, standard monetary policy actions also typically alter not just current short-term rates, but the anticipated path of short-term rates as well, influencing longer-term rates through the identical channel. In fact, central bankers have long recognized that this "expectations channel" operates most effectively when the public understands how policymakers expect economic conditions and monetary policy to evolve over time, and how the central bank would respond to any changes in the outlook.

The transmission channels through which longer-term securities purchases and conventional monetary policy affect economic conditions are also quite similar, though not identical. In particular, central bank purchases of longer-term securities work through a portfolio balance channel to depress term premiums and longer-term interest rates. The theoretical rationale for the view that longer-term yields should be directly linked to the outstanding quantity of longer-term assets in the hands of the public dates back at least to the 1950s.2

Each of these policy tools tends to generate spillovers to other financial markets, such as boosting stock prices and putting moderate downward pressure on the foreign exchange value of the dollar. My reading of the evidence, which I will briefly review, is that both unconventional policy tools--the use of forward guidance and the purchases of longer-term securities--have proven effective in easing financial conditions and hence have helped mitigate the constraint associated with the zero lower bound on the federal funds rate.

The Effectiveness of Forward Guidance

I will begin with an assessment of the FOMC's forward guidance concerning the federal funds rate, which began when the FOMC reduced its funds rate target to a range of 0 to 1/4 percentage point. In particular, the December 2008 FOMC meeting statement indicated that "economic conditions are likely to warrant exceptionally low levels of the federal funds rate for some time." Identical guidance was reiterated in January 2009, and in March 2009 the phrase "for some time" was changed to "for an extended period."

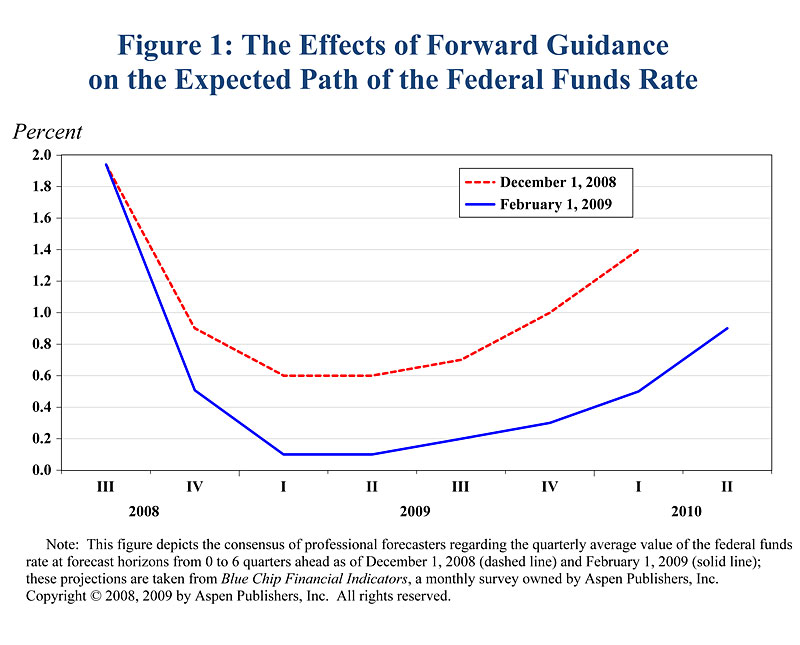

Figure 1 suggests that the provision of guidance concerning the future path of the federal funds rate likely contributed to more accommodative financial market conditions. In particular, the consensus outlook of professional forecasters regarding the path of the funds rate shifted down markedly in the Blue Chip survey published at the beginning of February 2009 (the solid line) compared with the survey published two months earlier (the dashed line).3

{kind=link}

A crucial feature of the FOMC's policy communications is that the Committee's forward guidance has been framed not as an unconditional commitment to a specific federal funds rate path, but rather as an expectation that is explicitly contingent on economic conditions. Since November 2009, the Committee has specifically indicated that the relevant economic conditions include "low rates of resource utilization, subdued inflation trends, and stable inflation expectations." An important consequence of such conditionality, serving to enhance the effectiveness of the guidance, is that incoming information about economic and financial developments has led forecasters and investors to revise their outlook for the path of the funds rate even in the absence of a change in the forward guidance language.

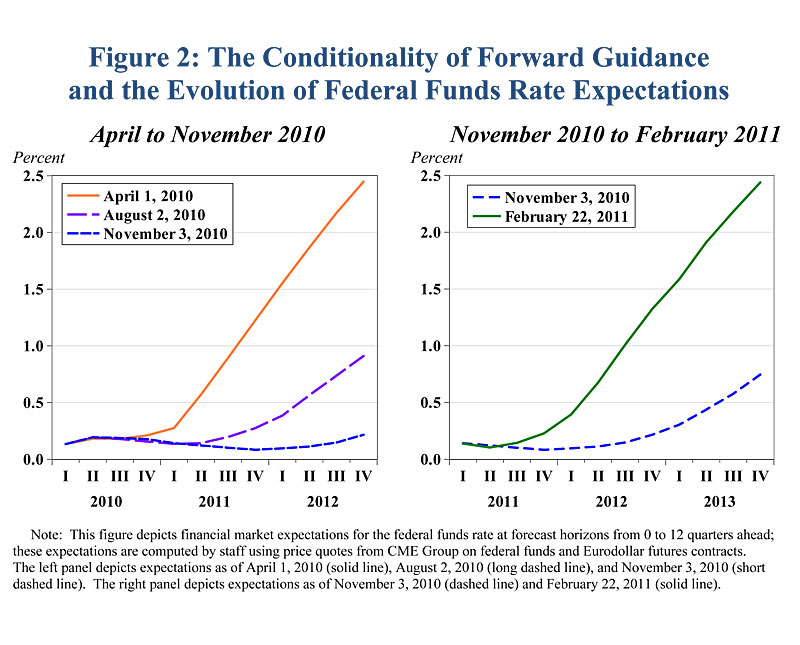

The evolution of financial market expectations concerning the funds rate path over the past year illustrates that the conditional nature of the FOMC's forward guidance allows incoming economic data to shift market views. For example, as shown in the left panel of Figure 2, the expected path of the funds rate shifted down markedly during the spring and early summer of last year in the wake of weaker readings on economic activity and prices and of some concerns about potential spillovers from developments in Europe. Those expectations shifted down somewhat further during late summer and early autumn. Conversely, as shown in the right panel, funds rate expectations have shifted upward over the past several months in response to more-positive economic news and greater confidence that a self-sustaining economic recovery may be taking hold.

{kind=link}

Down the road, once the recovery is well established and the appropriate time for beginning to firm the stance of policy appears to be drawing near, the FOMC will naturally need to adjust its "extended period" guidance and develop an alternative communications strategy to shape market expectations about the policy outlook. However, if there were an unexpected faltering of the recovery or a substantial widening of downside risks to economic activity and inflation, the forward guidance now in place might well be sufficient to facilitate an outward shift in the expected path of the funds rate, just as we saw over the course of last year.

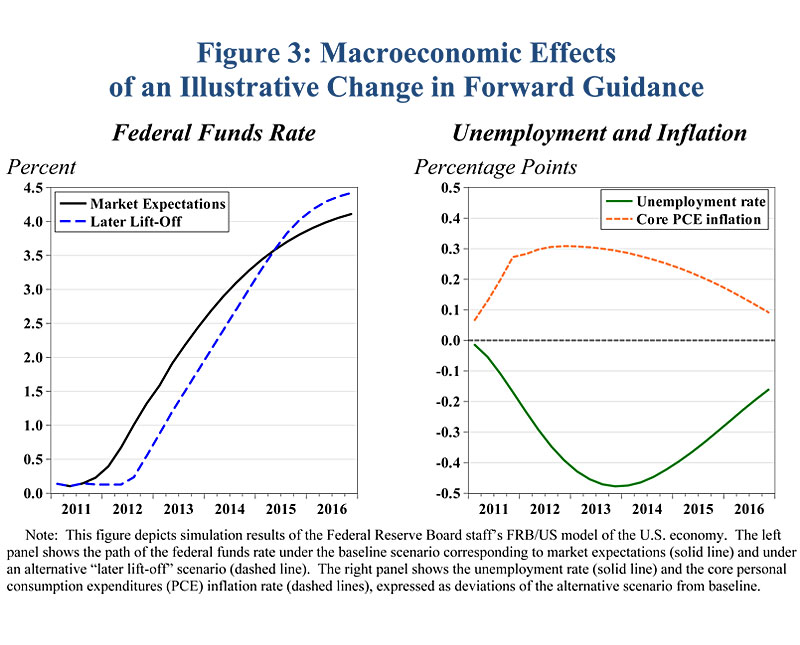

If financial market participants appeared to be expecting policy firming to begin somewhat sooner than policymakers considered desirable or appropriate under such circumstances, the language of the forward guidance could be adjusted to shift expectations toward the somewhat longer horizon over which the Committee expected the federal funds rate to remain extraordinarily low. Figure 3 illustrates the potential for such a change in forward guidance to support economic activity. In the left panel, the dashed line denotes the baseline path for the federal funds rate as embedded in current financial market data, while the solid line corresponds to an alternative path in which the initiation of policy firming is postponed by one year. If policymakers viewed that alternative path as appropriate and market participants came to share that view, then financial conditions would become significantly more accommodative, even in the absence of any change in the current level of the funds rate. As shown in the right panel, a simulation of the FRB/US model--a macroeconometric model developed and maintained at the Federal Reserve Board--indicates that such a shift in policy expectations would be associated with a lower trajectory for the unemployment rate (solid line) and a somewhat higher path of core inflation (dashed line) over coming years.

{kind=link}

The Effectiveness of Asset Purchases

I will now turn to an assessment of the FOMC's program of longer-term securities purchases. Both theory and empirical evidence suggest that asset prices and yields are affected not only by current securities purchases but also, importantly, by market expectations concerning future FOMC securities holdings. This observation implies that central bank communications pertaining to any important feature of the path of the Federal Reserve's balance sheet should influence financial conditions.

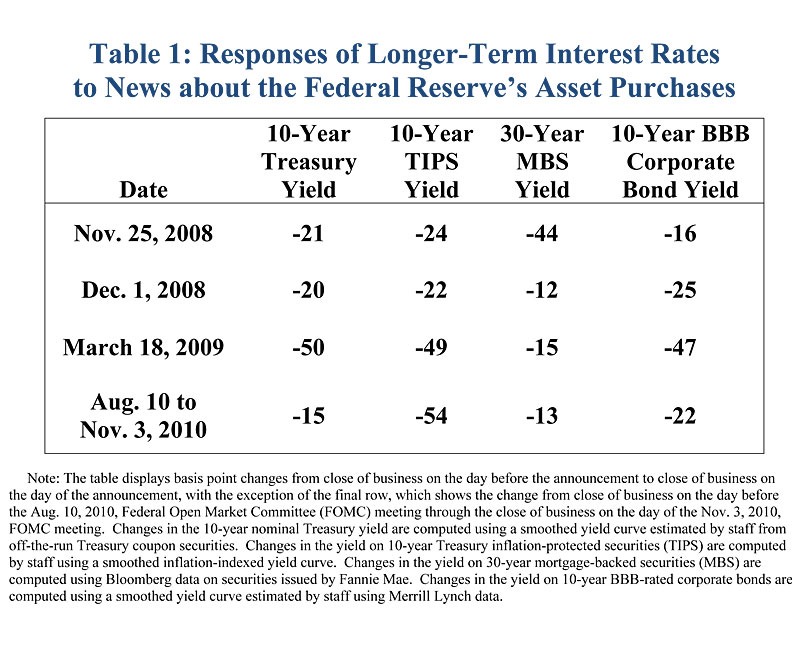

Event studies can therefore be helpful in gauging the financial market effects of such communications.4 For example, table 1 reports the response of selected financial variables on several key dates associated with the FOMC's purchases of longer-term securities. In late November 2008, the Federal Reserve announced that it would purchase up to $600 billion in agency MBS and agency debt, and Chairman Bernanke provided further details in a speech one week later. On March 18, 2009, the FOMC announced that the program would be expanded by an additional $850 billion in purchases of agency securities and by $300 billion in purchases of longer-term Treasury securities. Evidently, each of those communications was associated with substantial declines in longer-term nominal and real Treasury yields and in rates on agency MBS and corporate debt.

{kind=link}

Last August, the FOMC announced that it would begin reinvesting principal payments on agency MBS and agency debt into longer-term Treasury securities, and over the subsequent couple of months or so, the public remarks of Federal Reserve officials made note of the possibility of a further expansion of the portfolio. Consequently, when the Committee announced in early November that it intended to purchase an additional $600 billion in longer-term Treasury securities, that decision was largely anticipated by financial market participants, and it occasioned only minimal market response. However, taken together the movements in longer-term interest rates that occurred between the August and November FOMC meetings are strikingly similar to those on the prior announcement dates shown in the table, bolstering the judgment that these securities purchases contribute to more accommodative financial conditions.

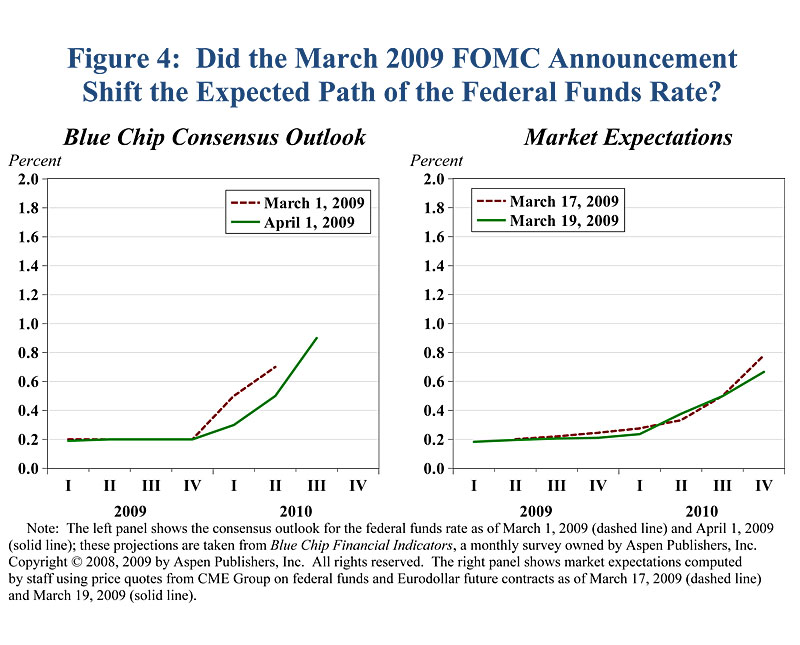

One complication that arises in evaluating the contribution of portfolio balance effects to the observed movements in longer-term rates is that news about large-scale asset purchases may also influence investors' perceptions regarding the likely path of short-term interest rates. Such effects may not have been very important, however, when the FOMC announced the expansion of its securities purchases in March 2009. As shown in figure 4, that announcement appeared to have only modest effects on the outlook of professional forecasters (left panel) and investors (right panel) regarding the likely trajectory of the federal funds rate. Thus, the substantial decline in longer-term yields following this announcement appears to have mainly reflected the effect of the purchases in pushing down term premiums rather than a shift in the expected path of the funds rate.5 This evidence suggests that the portfolio balance channel of influence is not only operative but also fairly large.

{kind=link}

That said, as we saw in figure 2, the expected path of the federal funds rate does appear to have flattened for a time during the late summer and early autumn of last year. Even allowing for that change in near-term policy expectations, however, it seems reasonable to conclude that the announcement of additional securities purchases mainly affected financial conditions through the portfolio balance channel.

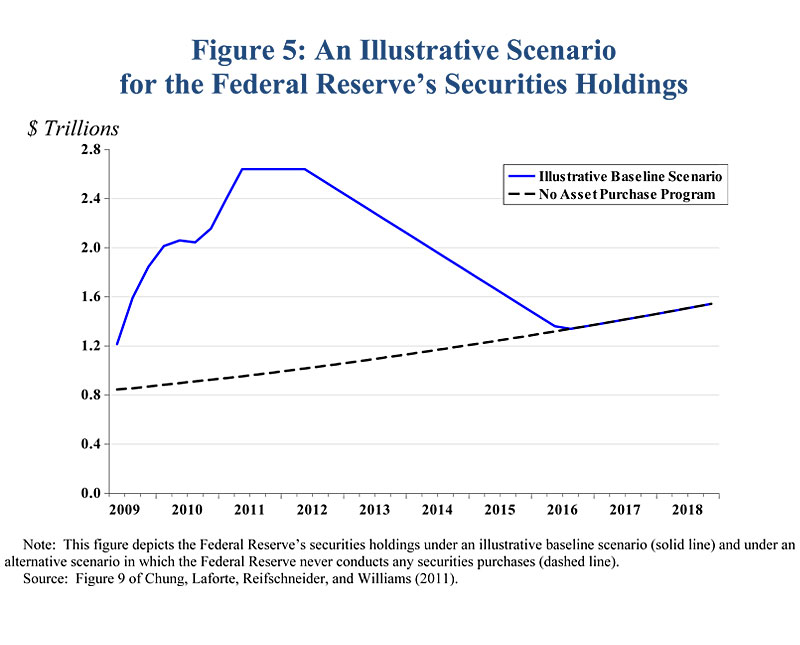

To assess the macroeconomic effects of the Fed's large-scale asset purchase program, I would like to highlight some findings from a recent study by four Federal Reserve System economists.6 As shown in figure 5, the authors constructed an illustrative baseline trajectory for the Federal Reserve's securities holdings over the course of this decade (solid line) as well as an alternative trajectory corresponding to a counterfactual scenario in which the FOMC never decided to initiate any securities purchases (dashed line).

{kind=link}

The baseline incorporates the first round of asset purchases--which brought the Federal Reserve's securities holdings to a little more than $2 trillion. It embeds an assumption that the FOMC will complete the purchases announced last November so that the balance sheet expands to about $2.6 trillion by the middle of this year. From that point forward, the authors assume that the overall size of the portfolio will remain unchanged until mid-2012 and then shrink gradually at a rate sufficient to return it to its pre-crisis trend line by mid-2016, whereupon the Federal Reserve resumes expanding its holdings at the trend rate. Full convergence of the composition of the portfolio is not complete until 2017, however, as the average maturity of the portfolio is still somewhat elevated in 2016. It should also be noted that the trend line itself rises gradually over time as a consequence of steady growth in demand for U.S. currency.

Of course, the baseline trajectory is purely illustrative: The actual evolution of the Federal Reserve's balance sheet will depend on the decisions that the FOMC will make in light of economic and financial developments. Nonetheless, the overall characteristics of this assumed trajectory seem broadly consistent with the sense of the Committee's discussions last spring. In particular, as reported in the minutes of the April 2010 FOMC meeting, most Committee participants expressed a preference for renormalizing the size and composition of the Federal Reserve's balance sheet over a period of about five years that would commence following the initiation of policy firming.

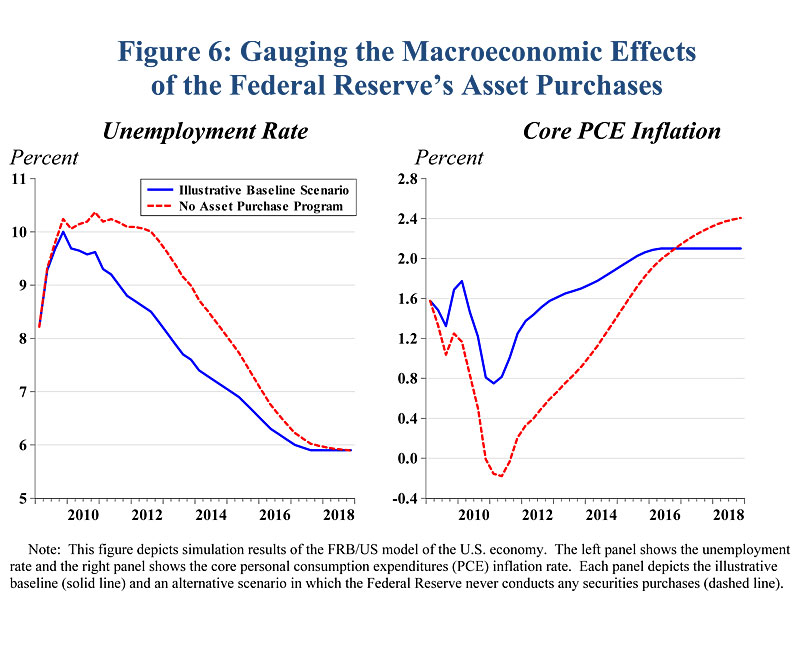

Figure 6 shows the results of simulations of the FRB/US model to gauge the effect of these asset purchases on the unemployment rate and core personal consumption expenditures (PCE) inflation. For this purpose, the baseline path (denoted by the dashed line in each panel) is constructed using historical data in conjunction with the latest set of consensus projections from the Survey of Professional Forecasters conducted by the Federal Reserve Bank of Philadelphia. Then the staff model is used to simulate the counterfactual scenario in which the FOMC never conducts any asset purchases (denoted by the solid line in each panel).7 The pace of recovery under the baseline scenario is expected to be painfully slow. But the counterfactual scenario suggests that conditions would have been even worse in the absence of the Federal Reserve's securities purchases: The unemployment rate would have remained persistently above 10 percent, and core inflation would have fallen below zero this year. Of course, considerable uncertainty surrounds those estimates, but they nonetheless suggest that the benefits of the asset purchase programs probably have been sizeable.

{kind=link}

My final observation concerning the FOMC's asset purchase program pertains to the importance of clear and effective communications in the years ahead. As I noted earlier, both theory and empirical evidence suggest that market prices and yields at any particular time reflect both the Federal Reserve's current securities holdings and also markets participants' expectations for its future holdings. Consequently, a shift in expectations concerning the trajectory of the Federal Reserve's balance sheet could have an important effect on financial conditions going forward.

In particular, financial conditions depend on market expectations not only concerning the amount of the FOMC's purchases but also concerning the anticipated timing and pace of the eventual unwinding of those holdings. For example, financial conditions would likely tighten immediately if market participants came to expect a more rapid renormalization of the Federal Reserve's balance sheet. In contrast, if market participants were to anticipate a more gradual renormalization, financial conditions would likely become more stimulative.

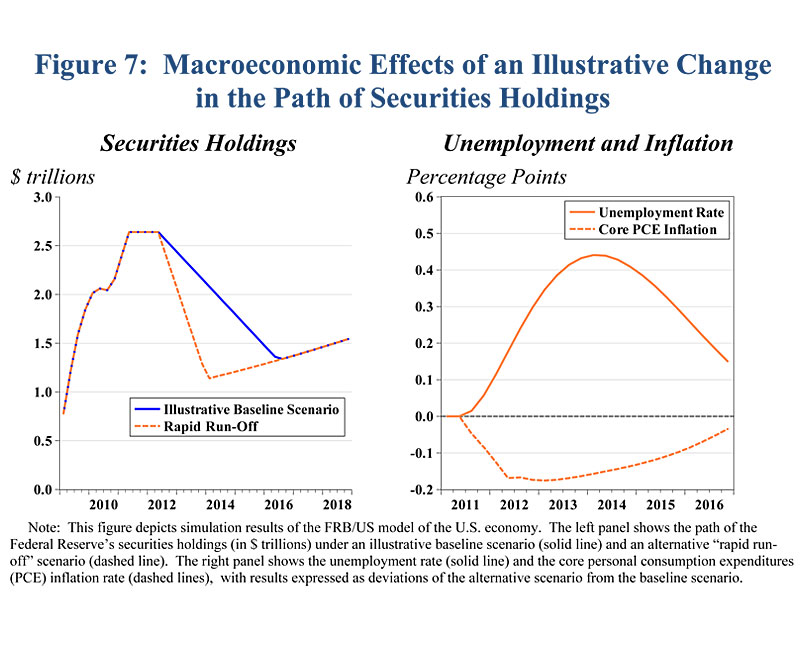

To illustrate the potential importance of such changes in expectations, figure 7 depicts a scenario in which markets come to anticipate that the Federal Reserve will shrink its balance sheet more rapidly than in the baseline scenario. The left panel shows the assumed contour of an expected acceleration of asset sales that would renormalize the overall size of the portfolio within about two years (solid line), roughly twice as fast as under the baseline scenario (dashed line). The announcement of such a strategy would cause a substantial rise in term premiums relative to the baseline scenario, and, assuming no offsetting change in the path of the federal funds rate, the resulting higher level of long-term interest rates would damp aggregate spending. The right panel depicts the macroeconomic effects of the more rapid runoff of the balance sheet in terms of deviations from the baseline scenario: The unemployment rate (solid line) is significantly higher, and core PCE inflation (dashed line) is somewhat lower.

{kind=link}

Conclusion

In conclusion, I believe that both forward guidance and large-scale asset purchases have been effective tools for providing additional monetary accommodation under circumstances in which conventional monetary policy has been constrained by the zero lower bound on the federal funds rate. My colleagues on the FOMC and I are regularly reviewing the asset purchase program in light of incoming information, and we will adjust the program as needed to promote our statutory mandate of maximum employment and stable prices. Recognizing the importance of market expectations to the effectiveness of unconventional policies, the Committee will continue to seek ways to enhance the clarity and effectiveness of our monetary policy communications.

References

Blue Chip Financial Forecasts: Top Analysts' Forecasts of U.S. and Foreign Interest Rates, Currency Values, and the Factors That Influence Them (2008 and 2009). New York: Aspen Publishers, monthly, http://www.aspenpublishers.com/blue-chip-publications.htm.

Chung, Hess, Jean-Philippe Laforte, David Reifschneider, and John C. Williams (2011). "Have We Underestimated the Likelihood and Severity of Zero Lower Bound Events? (567 KB PDF)" Working Paper series 2011-01. San Francisco: Federal Reserve Bank of San Francisco, January.

Culbertson, John M. (1957). "The Term Structure of Interest Rates," Quarterly Journal of Economics, vol. 71 (November), pp. 485-517.

D'Amico, Stefania, and Thomas B. King (2010). "Flow and Stock Effects of Large-Scale Treasury Purchases," Finance and Economics Discussion Series 2010-52. Washington: Board of Governors of the Federal Reserve System, September.

Gagnon, Joseph, Matthew Raskin, Julie Remache, and Brian Sack (2010). "Large-Scale Asset Purchases by the Federal Reserve: Did They Work?" Federal Reserve Bank of New York Staff Reports441. New York: Federal Reserve Bank of New York, March.

Hamilton, James D., and Jing (Cynthia) Wu (2011). "The Effectiveness of Alternative Monetary Policy Tools in a Zero Lower Bound Environment (877 KB PDF)," working paper. San Diego: University of California, San Diego, February.

Joyce, Michael, Ana Lasaosa, Ibrahim Stevens, and Matthew Tong (2010). "The Financial Market Impact of Quantitative Easing (748 KB PDF)," Working Paper 393. London: Bank of England, July (revised August).

Modigliani, Franco, and Richard Sutch (1966). "Innovations in Interest Rate Policy," American Economic Review, vol. 56 (March), pp. 178-97.

Tobin, James (1958). "Liquidity Preference as Behavior towards Risk," Review of Economic Studies, vol. 25 (February), pp. 65-86.

Vayanos, Dimitri, and Jean-Luc Vila (2009). "A Preferred-Habitat Model of the Term Structure of Interest Rates," NBER Working Paper Series 15487. Cambridge, Mass.: National Bureau of Economic Research, November.

1. These remarks solely reflect my own views and not necessarily those of any other member of the Federal Open Market Committee. I appreciate assistance from the members of the Board staff--including William English, Yuriy Kitsul, Jean-Philippe Laforte, Andrew Levin, David Reifschneider, and David Wilcox--who contributed to the preparation of these remarks. Return to text

2. Early examples include Culbertson (1957), Tobin (1958), and Modigliani and Sutch (1966). More recently, Vayanos and Vila (2009) study a preferred-habitat model in which short- and long-term assets are imperfect substitutes in investors' portfolios and the effect of arbitrageurs is limited by their risk aversion or other market frictions such as capital constraints. Return to text

3. See Blue Chip Financial Forecasts (2008, 2009). Return to text

4. A burgeoning literature focuses on the experience with asset purchase programs of the Federal Reserve and other central banks; for example, see D'Amico and King (2010); Gagnon and others (2010); Hamilton and Wu (2010); and Joyce and others (2010). Return to text

5. As noted earlier, in the March 2009 FOMC statement, the Committee did modify its forward guidance by indicating that exceptionally low levels of the federal funds rate would likely be warranted "for an extended period" (rather than "for some time", as in the December 2008 and January 2009 FOMC statements), but that modification does not appear to have substantially influenced professional forecasters' expectations about the near-term path of the federal funds rate. To the extent that the expanded asset purchases were expected to strengthen the economic recovery, the change in the forward guidance may have helped clarify that the FOMC did not intend to offset that effect by accelerating the initiation of policy firming; consequently, expectations for the trajectory of the federal funds rate were little changed on balance. Return to text

6. See Chung and others (2011). Return to text

7. Because the latest release of the Survey of Professional Forecasters provided forecasts of the unemployment rate only through 2014, the authors extrapolated the forecasts through 2018 using the extended consensus forecasts reported in the October 2010 Blue Chip survey. Return to text