FEDS Notes

December 20, 2019

Shining a light on the shadows: dealer funding and internalization

Marco Macchiavelli and Luke Pettit1

One of the primary functions of a broker-dealer (dealer or "firm" hereafter) is providing leverage to its clients. In this role, the dealer provides a cash loan, using the client's own securities as collateral. To finance this loan, the dealer typically rehypothecates some of these securities received as collateral in the repo markets.2 The dealer ultimately acts as a funding intermediary, using clients' collateral to raise cash from wholesale secured funding markets. Some work has been done to size and understand the workings of secured funding markets, including bilateral and triparty repo markets, and securities lending markets (Adrian et al. 2014; Baklanova et al. 2015).

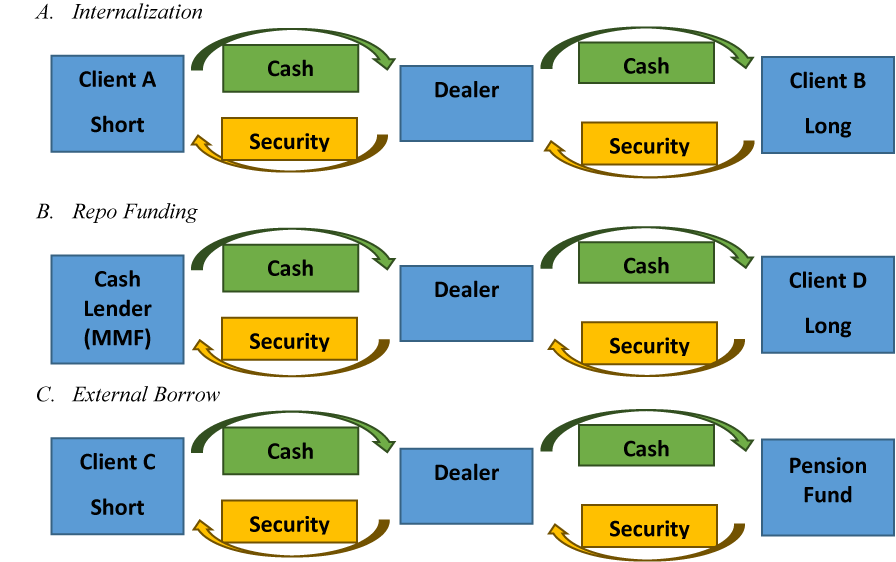

However, a largely unknown amount of funding intermediation occurs within the walls of the dealer via a practice often referred to as internalization, in which long and short positions from a dealer's client pool are matched to reduce net funding requirements. Said differently, if the dealer has two clients (or "customers") that are taking opposite positions (one long and one short) in the same security, the dealer can effectively finance the long position through the cash generated by the short position (Figure 1, panel A).3 In this note, we use new confidential supervisory data to take a first look at the practice of internalization and examine some of its implications.

The intermediation of cash and securities that a dealer cannot internalize has to occur externally: this can happen in two ways. First, when a customer takes a leveraged long position in a security that cannot be funded internally (by a customer or firm short), the dealer has to raise funding externally on behalf of the client (Figure 1, panel B). To do so, the dealer would typically pledge customer securities as collateral in the repo market. Second, the customer short positions in securities that cannot be matched internally (with customer or firm longs) have to be sourced externally. To accomplish this, the dealer typically borrows the needed security in the securities lending market, for example, from a pension fund or insurance company (Figure 1, panel C). The cash generated by the customer short serves as cash collateral for the borrowed securities.

The loss of internalization in times of stress may have significant, yet understudied, financial stability implications. Internalization is commonly used for equities. There are two potential concerns with an unexpected and sudden loss of internalization, depending on whether long or short positions are terminated. First, if the long positions originally used to cover short positions leave, the dealer has to then source these securities externally, typically via the securities lending market for equities. In normal market conditions, this does not pose a threat due to the depth of these markets. However, in times of stress it may be difficult to source large amounts of securities. The second instance occurs if short positions are closed. This may happen either because a client is migrating its positions to another dealer, or because short-sellers are closing their short positions. A significant loss of short positions means that the dealer has to find alternative sources to finance the clients' long positions that were originally funded internally. A dealer would typically obtain such financing in the repo markets. However, since internalization in equities is very large relative to the size of the repo market for equity collateral, a sudden loss of equity shorts may not be easily offset by financing through the repo market.

The top chart displays an example of internalization. The securities shorted by Client A (in the yellow box) come from Client B's long positions; similarly, the cash margin of Client A (in the green box) finances Client B's cash loan—called a margin loan. In the middle chart, Client D's leveraged long positions are financed by the dealer through a margin loan, which in turn the dealer funds on the repo market—raising cash from a money market fund (MMF) against the pledge of collateral. Finally, in the bottom chart Client C's short positions are covered by borrowing the securities externally, for instance from a pension fund.

Even though internalization occurs in most collateral classes (Treasuries, agencies, corporate debt and equities), it is predominantly relevant in the equity space. For the average dealer in the equity space, about 40% of customer shorts are covered internally, mainly via customer longs, while 50% are covered externally, namely by borrowing the security via securities borrowing or reverse repos. The remaining 10% is covered via collateral swaps and unsettled positions.4 As noted above, customer shorts are a funding source for the dealers; this is especially true in equities. During our 2016-2018 sample period, equity customer shorts are larger than the total secured funding raised via both repos (triparty and bilateral) and securities lending with equity collateral. While recent work has looked at the stability of repo and securities lending markets, little is known about the stability of funding generated via internalization. In addition, while the Liquidity Coverage Ratio (LCR) takes into account the potential cash outflows generated by clients closing short positions, we do not know how the hypothetical run-off rates set out by the LCR compare with the actual run-off rates in a stress scenario. Due to the size of equity customer shorts relative to the size of funding secured by equities, it is all the more important to understand the behavior of customer shorts in times of stress. In times of acute stress, a runoff of customer shorts could create a liquidity shortfall due to their significant role in generating funds.

In the remainder of this note, we introduce background information on internalization, present the dataset, and conclude with some summary statistics.

Background

To illustrate the concept of internalization, a brief explanation of the mechanics behind trade execution is warranted. In order to gain short exposure to a security, an investor needs to source the underlying security before it can sell it short into the market. This process is often facilitated by a dealer, which acquires the to-be-shorted security on behalf of the investor, allowing them to sell short.

Dealers typically facilitate this process in one of several ways. First, the dealer can borrow the security from a third party via the bilateral repo market or the securities lending market. Second, the dealer can source the security outright, by simply purchasing it in the market. Finally, the dealer can use internalization, that is, use existing securities of either a client or the dealer itself. In this case, the dealer matches clients who wish to short a security either with other clients who have long positions in the same security or with the dealer's own inventory positions.

Developing this concept further, in the first two options, the dealer uses the client's cash margin to borrow the security that the client wants to short. The third option, internalization, only requires that an unencumbered security exist in the dealer's own inventory or its pool of client long positions. This approach leaves the cash (which would have been used to purchase the security or as collateral for borrowing it) free for other purposes, such as providing leverage via margin loans.

Ultimately, internalization lessens the net funding requirements for dealers and lowers the client's cost of shorting securities. Each time a dealer can match client longs with client shorts, it bypasses the need to source the security for the short position externally or to finance the security for the long position externally.

Implications for dealers

Internalization is not without its drawbacks, and there are risks inherent to this form of intermediation. Unlike matched book repo, internal secured financing is essentially without tenor and is at the whim of client behavior. Given that short sales generate funding, dealers rely on these positions to fund credit extension (primarily margin loans to provide leverage). As such, dealers are vulnerable to funding shortfalls if clients leave asymmetrically or they rapidly change their net positioning. Anecdotally, this dynamic is said to have occurred during the crisis at several large dealers as clients shifted their profitable positions (shorts) from firms facing financial pressures. All else equal, clients' growing use of multiple prime brokerage relationships ("multi-priming") has probably increased their ability to run from dealers in this manner.

Data

We use confidential FR 2052a data, which is collected by the Federal Reserve to assess the liquidity profile of LISCC firms, and to monitor compliance with the LCR Rule. U.S. firms with $50 billion or more in total consolidated assets must report data for all of their domestic and international operations. Foreign Banking Organizations (FBOs) with U.S. assets of $50 billion or more must report data only for their consolidated U.S. operations. Starting in 2016, U.S. firms with $700 billion or more in total consolidated assets or $10 trillion or more in assets under custody and FBOs identified as LISCC firms have had to submit a report for each business day. We conduct our analysis at the consolidated level for each bank holding company (BHC), because we want to factor our internal transactions between subsidiaries of the same BHC.5 Our sample period goes from July 2016 to January 2019.

The variables of interest are Customer Shorts and Firm Shorts, broken down by collateral type and source. Customer Short refers to a transaction where the reporting entity's customer sells a security it does not own, and the entity subsequently obtains the same security from an internal or external source to make delivery into the sale. External refers to a transaction with a counterparty that falls outside the scope of consolidation for the reporting entity. Internal refers to securities sourced from within the scope of consolidation of the reporting entity. External sourcing could occur via cash transactions (securities borrowing or reverse repo) and non-cash transactions (collateral swap); internal sourcing can come from firm longs (through the firm's own inventories), customer longs (collateral held in customer accounts at the firm), or firm longs with an associated derivative (whose market risk is hedged via derivatives); finally, the short position could still be uncovered, namely the sourcing still needs to occur. Similarly, Firm Short refers to a transaction where the reporting entity sells a security it does not own, and the entity subsequently obtains the same security from an internal or external source to make delivery into the sale. The possible sources for delivery into the sale (external, internal, or uncovered) are the same as for Customer Shorts.

Summary Statistics

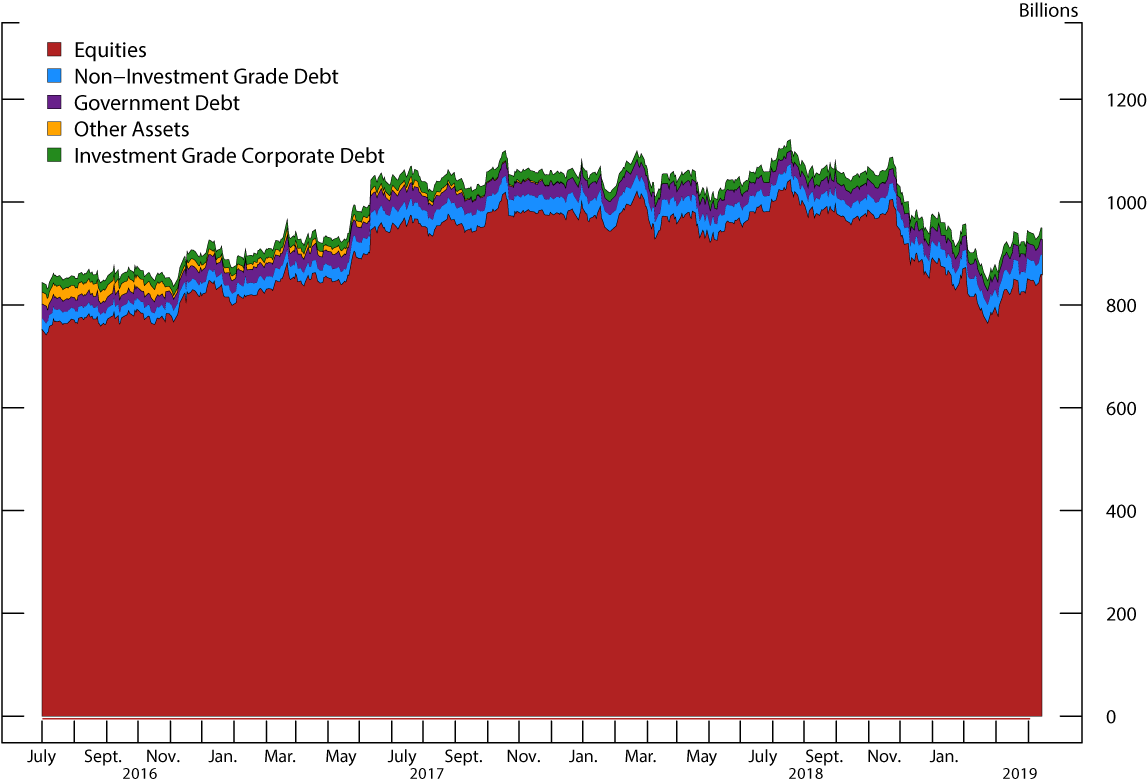

As shown in Figure 2, short positions in equities are much larger than those in any other collateral type. Table 1 displays how the average dealer in our sample covers its customer shorts in the July 2016 to January 2019 period, for each collateral type. For Treasury securities, on average 49% of customer shorts are sourced externally, by borrowing the securities. In contrast, 44% of customer shorts are sourced internally: 30% through clients taking the opposite (long) position, and 14% through the firm's long position. In the agency space, internalization makes up a larger share of customer shorts: external sourcing accounts for 37%, firm longs 33%, and customer longs 26%--hence internal sourcing accounts for 59% of customer shorts.

Table 1: Summary Statistics on Sourcing Methods for Customer Shorts

This Table displays the average share of customer shorts that are sourced in a certain way (customer longs, firm longs, external borrows, collateral swaps, and unsettled positions), broken down by collateral type (Treasuries, agencies, investment-grade corporate bonds, high-yield corporate bonds, and equities), between July 2016 and January 2019. Sourcing via customer longs and firm longs is referred to as internalization.

| Method | Collateral Type: | ||||

|---|---|---|---|---|---|

| Treasuries | Agencies | Corporate Bonds, IG | Corporate Bonds, HY | Equities | |

| Customer Longs | 30% | 26% | 20% | 22% | 31% |

| Firm Longs | 14% | 33% | 5% | 5% | 7% |

| External Borrows | 49% | 37% | 68% | 65% | 51% |

| Collateral Swaps | 6% | 1% | 6% | 6% | 10% |

| Unsettled | 1% | 3% | 2% | 1% | 2% |

Source: FR 2052A.

For corporate debt, internalization is used to source a much smaller share – about one-quarter – of customer shorts. Across both investment grade and high yield, about two-thirds of customer shorts are sourced externally through security borrowing (and reverse repos). Within the internal coverage of customer shorts, about 20% comes from customer longs and 5% from firm longs.

Finally, equities have the largest share of customer shorts covered internally by customer longs, at 31%. The other part of internal coverage, via firm longs, represents 7%. External sourcing is still the most common vehicle for covering customer shorts, at 51%. The remainder is almost covered by swaps, at 10%, and unsettled positions at 2%.

While these shares are informative about the business model of dealers, they do not convey the relative depth of the internal market relative to the overall external market. This is important because if the dealer can no longer source a security internally, it may have to borrow it externally; similarly, when a dealer cannot fund a long position internally, it has to do so externally via the repo market. Problems may arise when the internal market is quite large compared to the external market and, as a result, the external market may not smoothly absorb a significant loss of internalization.

Relative size of internal and external markets

To shed light on these issues, in Table 2 we compare the size of customer shorts with the size of external sources of securities (dealers' reverse repos and sec borrowing) and external sources of cash (dealers' repos and sec lending).

Treasury collateral. Internal sources of long positions to cover customer shorts in Treasuries are small compared to the size of the dealer's total sourcing of Treasuries (sec borrowing plus reverse repos). Customer longs to cover customer shorts (CLCS) are just 0.4% of the average dealer's total sourcing of Treasuries (see Table 2). The external market for sourcing Treasuries is very deep and can seamlessly accommodate a loss of internalization.

Agency collateral (excluding Ginnie Mae). Internalization as a share of total sourcing of securities is similarly small, representing 0.4% of agency securities in (sec borrowing plus reverse repos).

Corporate collateral. A loss of internalization is unlikely to have a significant impact. The size of customer longs to cover customer shorts (CLCS) is around 3% of corporate debt securities in; in addition, firm long positions to accommodate customer shorts represent 2% of total external sources of corporate collateral.

Table 2: Summary Statistics on the Relative Size of Internal and External Markets

This Table displays the average share of customer shorts that are sourced in a certain way (customer longs, firm longs, external borrows) relative to the size of the dealer's securities in (reverse repos plus sec borrowing), broken down by collateral type (Treasuries, agencies, investment-grade corporate bonds, high-yield corporate bonds, and equities). Sec In refers to securities in. CLCS refers to customer longs to cover customer shorts, FLCS to firms long to cover customer shorts, and EBCS is external borrowing to cover customer shorts. The second-to-last row displays the share of total customer shorts relative to total securities in (CS/Sec In), broken down by collateral type. Finally, the last row displays the share of the total customer shorts relative to total securities out (CS/Sec Out), broken down by collateral type. Securities out is the sum of repos and securities lending backed by the respective collateral type. The sample period goes from July 2016 to January 2019.

| Method: | Collateral Type: | ||||

|---|---|---|---|---|---|

| Treasuries | Agencies | Corporate Bonds, IG | Corporate Bonds, HY | Equities | |

| CLCS/Sec In | 0.40% | 0.30% | 3% | 5% | 35% |

| FLCS/Sec In | 0.10% | 0.10% | 2% | 2% | 16% |

| EBCS/Sec In | 1% | 1% | 29% | 34% | 56% |

| CS/Sec In | 1.60% | 1.50% | 40% | 46% | 155% |

| CS/Sec Out | 2.60% | 1.60% | 34% | 49% | 210% |

Source: FR 2052A.

Equity collateral. A significantly different picture emerges here, where a loss of internalization could have a more pronounced impact on the market. For the average dealer, customer longs to cover customer shorts (CLCS) are 35% of total equity securities in; also, firm longs to cover customer shorts (FLCS) are on average 16% of total external sources of equity securities. Finally, 56% of total equity securities in are on average used to meet customer shorts. Altogether, due to the high degree of internalization, total equity customer short positions are 155% of total equity securities in; in other words, a lot of the customer short positions do not rely on external sourcing, but are instead covered internally. A sudden departure of customer long positions may result in a loss of internalization, requiring the dealer to either take the long position itself, or to significantly increase the amount of external borrowings. Since dealers may be reluctant to take significant long positions exactly at the same time as the market is betting on a downward correction, they would likely need to borrow a large amount of securities externally.

Customer shorts are a source of funding for the dealer (see Figure 1). Due to the large short base in the equity space, less external funding backed by equities is needed; specifically, customer shorts are about twice as large (210%) as the sum of equity repos and equity securities lending for the average dealer (see Table 2). As a result, were a significant amount of short positions to leave, the dealer would have to drastically increase its sources of external funding secured by equity collateral from a market that is not very deep compared to this potential demand for secured funding. In other collateral types, the relative size of customer shorts to total external secured funding (repos and sec lending) is much smaller: it is 3% and 2% in treasuries and agencies, respectively, and about 40% in the corporate debt space.

References

Adrian, Tobias, Brian Begalle, Adam Copeland, and Antoine Martin (2014). "Repo and Securities Lending", Risk Topography: Systemic Risk and Macro Modeling, University of Chicago Press.

Baklanova, Viktoria, Adam Copeland, and Rebecca McCaughrin (2015). "Reference Guide to U.S. Repo and Securities Lending Markets", Federal Reserve Bank of New York Staff Reports, no. 740.

1. Board of Governors of the Federal Reserve System. The view in this document are those of the authors and do not necessarily reflect those of the Federal Reserve System, or any of its staff. Return to text

2. Rehypothecation refers to the reuse of securities received as collateral from clients. Often, dealers repledge these securities on the repo market to raise cash against them. Return to text

3. In addition to customer shorts funding customer longs, the dealer could finance a customer's long position by taking the short position itself. Therefore, internalization can generally occur by matching customer longs with either customer shorts or firm shorts. Return to text

4. Collateral swaps are transactions where non-cash assets are exchanged at inception and returned at a final date. Unsettled positions refer to the purchase of securities that have been executed, but not yet settled. Return to text

5. Our dataset contains a total of 16 BHCs: Bank of America, BNY Mellon, Barclays USA, Citigroup, Credit Suisse USA, Goldman Sachs, JP Morgan, Morgan Stanley, MUFG USA, Mizuho USA, Societe' Generale USA, Bank of Nova Scotia USA, Toronto Dominion USA, UBS USA, and Wells Fargo. Return to text

Macchiavelli, Marco, and Luke Pettit (2019). "Shining a light on the shadows: dealer funding and internalization.," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, December 20, 2019, https://doi.org/10.17016/2380-7172.2419.

Disclaimer: FEDS Notes are articles in which Board staff offer their own views and present analysis on a range of topics in economics and finance. These articles are shorter and less technically oriented than FEDS Working Papers and IFDP papers.