FEDS Notes

May 29, 2026

Federal Reserve Discount Rate Press Releases in the 1960s and 1970s through the Lens of Monetary Policy Communications

Mark Carlson, Daben Chen, and Benjamin K. Johannsen1

Introduction

This article examines press releases from the Board of Governors of the Federal Reserve System (Board) in the 1960s and 1970s related to changes in the discount rate through the lens of monetary policy communications. As argued by Yellen (2013), we start from the premise that communications have a "distinct and special role in monetary policymaking."2 Recent academic literature has focused on the effects of monetary policy communications by analyzing changes in asset prices around the time of federal reserve communications, particularly the Federal Open Market Committee's (FOMC's) postmeeting statement, which has been released regularly starting in the 1990s. Those communications have garnered attention because they are publicly available in real time, announce specific policy decisions or views about future policy decisions, and they reference macroeconomic developments or monetary policy goals as reasons for those decisions or views. We provide examples of press releases about changes in the discount rate in the earlier period that share all of these features.

The press releases were made available to the public shortly after the decision to change the discount rate was made, and related information would appear in newspaper articles the next morning. This information had to be public because the discount rate is the rate at which the Federal Reserve lends money to commercial banks through the discount window and banks would need to know the rate they would pay when they borrowed from the Federal Reserve. Their public nature and wide availability make these press releases a potentially important form of communications in the 1960s and 1970s because the FOMC's policy decisions related to open market operations were not explicitly announced during this time.

The use of press releases to convey information on the economic factors shaping shifts in Federal Reserve policy started in the early 1960s. Reflecting the governance of the discount window, these statements were issued by the Board rather than the FOMC, but the rationale provided frequently reflected the discussions of the FOMC. The press releases and their informational content were reported in the financial press. Policymakers discussed the implications of the press releases in FOMC meetings and indicated that they thought the announcements had implications for financial conditions and, consequently, for the economy. The historical record indicates that both policymakers and market participants perceived these press releases as providing guidance about monetary policy.

The market responses to discount rate announcements have been noted by other researchers. Meltzer (2009) and Nelson (2025) cite particular discount rate announcements that communicated reasons for Federal Reserve policy actions.3 Roley and Troll (1984) and Smirlock and Yawitz (1985) conduct empirical investigations of the effect of the changes in the discount rate on financial-market prices in the 1970s and 1980s; Cook and Hahn (1988) extend that work to see if discussions of economic topics in the discount rate announcements during that period had additional effects on markets. We complement this work by discussing the evolution of the content of the discount rate announcements going back to the early 1960s and by discussing that content in the context of more-recent monetary policy communications.

The examples we provide are somewhat surprising because of what is understood to be policymakers' aversion to monetary policy communications before the 1990s. Yellen (2013) argues that before the 1990s, the Federal Reserve took an approach of "never explain," and Jefferson (2024) recounts that in the 1980s "central banking wisdom dictated that monetary policymakers should say as little as possible."4 While it is undoubtable that Federal Reserve communications have increased in transparency and informativeness since the 1990s (see Lindsey (2003) for an extensive discussion of the evolution of FOMC communications from 1975-2002), our analysis suggests that Board press releases related to the discount rate may have provided the public with meaningful information about monetary policymaking in earlier periods.5

This note proceeds as follows. First, we provide some background information on the monetary policy framework in place the 1960s and 1970s and how the discount rate fit into the Federal Reserve's toolkit. Second, we discuss how discount window press releases evolved over time to include richer communication about the motivation for the changes to the stance of policy. Third, we document that discount rate press releases were understood by both policymakers and financial market participants to be a part of the policy process. Fourth, we present the December 1968 discount window announcement as a clear example of discount window announcements as a part of the policy process. Notably, Romer and Romer (1989) identify December 1968 as a policy tightening shock.6

1. Background

In this section, we review the monetary policy framework prevailing at the time of our analysis. In the 1960s and 1970s, monetary policy was implemented by targeting conditions in money markets with the goals of stabilizing economic activity and maintaining low levels of inflation. Rather than using the federal funds rate as the main policy instrument, as is done currently, for most of this period the Federal Reserve targeted a mix of the federal funds rate, the quantity of reserves, Treasury bill rates, and dealer financing costs (Meulendyke 1998).7 Still, over this period, the FOMC increased its focus on the federal funds rate.

To adjust conditions in money markets, the Federal Reserve employed four tools:

- Open market operations. Purchases and sales of Treasury securities affected the quantity of reserves in the system and could thus change the federal funds rate and Treasury bill rates. Modestly sized open market operations were conducted frequently but it could be difficult to discern shifts in monetary policy from regular seasonal fluctuations because the FOMC's directive related to open market operations was not immediately made public.

- Reserve requirements. Changing the amount of reserve that banks were required to hold against certain types of deposits affected the demand for reserves and willingness of banks to grow their deposits and lending. Adjustments in these requirements did not occur very often.

- Interest rate ceilings that banks were allowed to pay on deposits under Regulation Q. Raising or lowering these ceilings affected banks' ability to use interest rates to attract deposits and expand bank credit. The ceilings were adjusted more often than reserve requirements but not as often as changes in the discount rate.

- The discount rate that the Federal Reserve charged when making loans to banks through the discount window. The discount window was a useful marginal source of funds for banks and could influence other interest rates paid by the banks on their funding or charged on their loans.

As captured in the memoranda of discussion and minutes associated with FOMC meetings in this period, the FOMC discussed all these policy tools in relation to each other.

While the FOMC discussed the discount rate, the governance of this rate meant that it was not set by the FOMC but instead through joint actions of the Reserve Banks and the Board. Discount rate changes are initiated by the Reserve Banks who submitted requests to the Board for approval. (If there was a desire by FOMC meeting participants to change discount rates, the Board could "invite" the Reserve Banks to submit changes.) The Board would decide at its discretion whether to authorize the change. If the Board approved the request, it made a press announcement.8 There was a consensus to keep the discount rate the same across Reserve Banks, although there could be slight differences in timing of when these requests were submitted.

2. The press release regarding the change in the discount rate

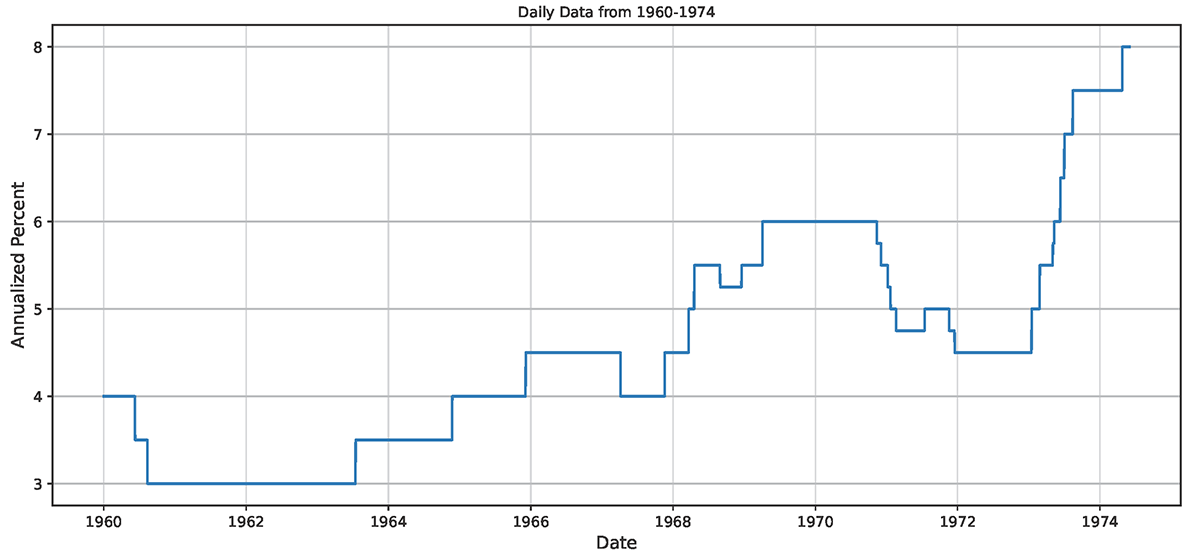

The beginning of our sample—January 1960—was about the time that one mild monetary policy easing cycle started. Our analysis period ends in July 1974, shortly before the period taken up by Lindsey (2003) and at a time around the completion of a monetary policy tightening cycle, which gives us two full monetary policy cycles to consider. The discount rate at the Federal Reserve Bank of New York during this time is shown in figure 1.

Source: Board of Governors of the Federal Reserve System (1976), Banking and Monetary Statistics, 1941-1970. Board of Governors of the Federal Reserve System (1981), Annual Statistical Digest, 1970-1979.

The first press releases associated with changes in the discount rate during this period occurred in June and August 1960.9 They were quite terse and simply noted that actions had been taken. The June press release, which was released at 4:00 p.m. eastern time on June 2, in its entirety reads:

"The Board of Governors of the Federal Reserve system today approved action by the directors of the Federal Reserve Banks of Philadelphia and San Francisco decreasing the discount rates at those Banks to 3-1/2 per cent, effective Friday, June 3, 1960. The rates previously in effect at those Banks were 4 percent."

The August 1960 press release is nearly identical.

In contrast to these terse press releases, the July 1963 press release was two pages long.10 In July of 1963, the Board raised the discount rate, an action that was the beginning of a monetary policy tightening cycle. At the outset of the press release, the Federal Reserve indicates that the purpose of raising the discount rate, and simultaneously raising the ceilings on interest rates banks could pay on deposits, was to combat the United States' balance of payments problems.

Press releases issued later in the decade focused on domestic economic conditions as reasons for policy actions. For example, in December of 1965 the Federal Reserve increased the discount rate as part of a tightening cycle to dampen credit growth and restrain inflation pressures:11

"The actions, intended not to cut back on the present pace of credit flows but to dampen mounting demands on banks for still further credit extensions that might add to inflationary pressure, were [to increase the discount rate by 50 basis points]….

With slack in manpower and productive capacity now reduced to narrow proportions, with the economy closer to full potential than at anytime in nearly a decade, and with military demands on output and manpower increasing, it was felt that excessive additions to money and credit availabilities in an effort to hold present levels of interest rates would spill over into further price increases in goods and services. Such price rises would endanger the sustainable nature of the present business expansion."

This statement reflected the conversation and points raised at the most recent FOMC meeting. For instance, according to the minutes for the November 23, 1965 meeting, the staff economic presentation indicated that:12

"The economy, stimulated in part by increased military activity, is operating closer to full potential now than at any other time in nearly a decade (statement of Mr. Koch p.20)."

FOMC members were reported in the minutes to have been concerned about credit growth and rising prices.

"Mr. Daane said, it was necessary to restrain credit expansion so as to retain a reasonable degree of price stability. Whatever set of theories of linkages between credit or money and prices one might prefer, the present and prospective situation was certainly one in which too much ease would be likely to contribute, directly or indirectly, to upward pressures on prices (p. 63)."

"Chairman Martin observed that it was necessary to make fundamental judgments at this stage. It was easy for him to make a judgment because he believed the country was in a period of creeping inflation already (p.85)."

The similarities between the economic rationales for tightening policy presented at the FOMC meeting and in the statement regarding the change in the discount rate support the idea that these press releases were conveying information about the stance of monetary policy.

Not every press release announcing a change in the discount rate was accompanied by an economic rationale. In our sample, we find that just over half of the announcements of changes in the discount rate contain a reference to economic policy goals.13 Domestic rationales for changes in the discount rate included price stability, curbing inflationary expectations or pressures, the general rise in the price level, excessive expansion in money and credit as well as supporting economic growth or economic stability. The international balance of payments and the strength of the Dollar were also mentioned as motivations for policy changes.

3. Discount rate press releases were understood as policy communications

Discount window announcements were treated as an explicit communication device regarding the stance of monetary policy, and this was well understood by policymakers and the public.

Policymakers understood that the actions and the statement had an "announcement effect" to inform markets about the policy stance and thought carefully about the impact of changes in the discount rate and of the information in the statement on perceptions and expectations of market participants. Policymakers were also aware that the announcement effects could be larger if changes in the discount rate were made in conjunction with changes in other policy tools. For instance, at some meetings participants actively discussed whether the Board should announce changes in reserve requirements in conjunction with a discount rate rise, so that a greater "announcement effect" would be achieved.14, 15 At other times, participants cited the "announcement effect" as an argument for inaction: in the summer of 1966 credit crunch, requests to change the discount rate were declined in part to avoid the possibility of a significant market reaction to any discount rate action.16

Market participants reportedly viewed discount rate changes and the accompanying statements either as news about the stance of monetary policy or as confirming developments in the stance that were guessed at based on developments in open market operations. For example, a New York Times article reported that while a 1967 reduction in the discount rate was anticipated, it "confirmed events that had already taken place in the money market" and served as a "restatement of the present trend of Federal Reserve policy" toward easier money.17

4. The December 1968 discount-rate press release

A vivid example of a press release announcing a raising of the discount rate and providing an economic rationale is from December 1968. Notably, December 1968 is one of the dates identified by Romer and Romer (1989) as involving a monetary policy tightening shock. The discount-rate press release from December 1968 included the following economic rationale for the announced policy action:

"This discount rate increase was approved in recognition of the advances that have taken place in other market interest rates in recent months and also in light of the resurgence in inflationary expectations that is impeding the restoration of economic stability. The objective of Federal Reserve policy is to foster financial conditions conducive to the reduction of inflationary pressures, with a view toward encouraging a more sustainable rate of economic expansion and attaining reasonable equilibrium in the country's balance of payments. The present action is being taken in furtherance of a policy of restraint."18

The interest rate ceilings in Regulation Q were left unchanged in December 1968. When coupled with the rise in the discount rate, the unchanged interest rate ceiling would have acted as a further restraint.

It is clear that FOMC meeting participants understood the December 1968 press release as having policy implications independent of the policy action. The December 1968 FOMC meeting included a rich discussion of communication strategies and the "announcement effect" of monetary policy actions.19 Additionally, the January 1969 FOMC meeting included a discussion of the effect of the December 1968 press release.20 Mr. Robinson, an FOMC member, noted that:

"Since our mid-December meeting, monetary restraint has caught the attention of the country – partly because of the conduct of open market operations, partly because of the discount rate action, but importantly, too, because of the contents of the press announcement of the latter (p. 69)."

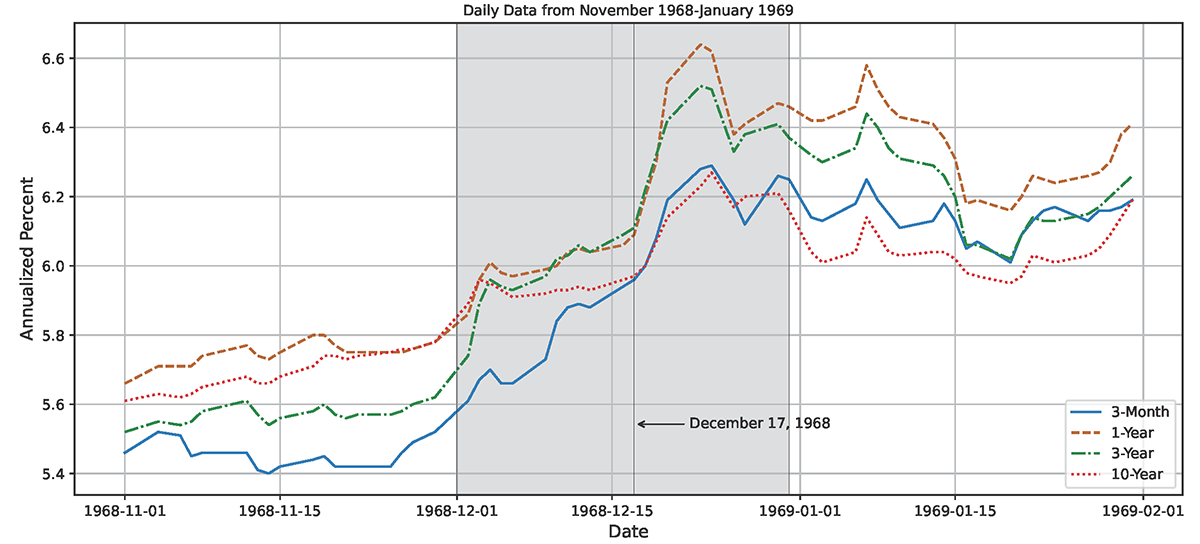

The public's understanding of discount rate press releases as monetary policy communications was also clear after the policy actions in December 1968. The discount rate action had arguably been expected, but the Board's inaction on interest rate ceilings under Regulation Q was a surprise.21 Not raising the interest rate ceilings amid a general increase in interest rates would have made it more difficult for banks to raise wholesale funds which would have restricted their ability to intermediate credit and thus tightened financial conditions. The implications of not raising the interest rate ceilings was well known so the conscious choice by the Federal Reserve to hold the ceilings in place would have clearly signaled that it was tightening policy. In the next four trading days, Treasury security prices slid, and yields rose by as much as 40 basis points (figure 2).

Note: The figure show Treasury yields for 3-month, 1-year, 3-year, and 10-year maturities. The shaded area represents the period of December 1968.

Source: Federal Reserve Board via FRED (Federal Reserve Bank of St. Louis).

The announcements also appear to have made markets more attentive to other Federal Reserve actions for some time. For example, one newspaper article suggested paying closer attention to the open market operations, which would "provide the best gauge" of whether the Federal Reserve was indeed embracing such sharp policy shifts.22 Another article suggested markets were expecting Federal Reserve to tighten policy with other tools because "it's very seldom that raising the discount rate alone will do it."23 In this example, we see that the discount rate action, even when it was anticipated, could send an important signal regarding policy stance to markets by including a rationale in the announcement and coordinating with other policy tools.

Romer and Romer (1989) used the "Record of Policy Actions" (the predecessor of the modern FOMC meeting minutes) and the minutes (third-person edited transcript) of the FOMC meeting to identify December 1968 as the date of a monetary policy tightening shock. To be a monetary policy tightening shock, Romer and Romer (1989) required that the historical record indicates that Federal Reserve desired to restrain economic activity in order to reduce inflation. While the "Record of Policy Actions" and the minutes of the December 1968 FOMC meeting were released to the public with a delay, the December 1968 press release announcing the increase in the discount rate was available on the same day as the FOMC meeting. That press release is clear in relaying the Committee's desire for a "policy of restraint" to reduce inflationary pressures.24

5. Conclusion

The press releases related to changes in the discount rate suggest that they are part of Federal Reserve's history of providing markets with information about changes in the stance of monetary policy. While these were officially press releases issued by the Board rather than by the FOMC, it appears that these statements articulated economic rationale for changes in the stance of policy that drew on discussions at FOMC meetings. It also appears to have been understood by financial market participants that these statements provided information about the factors that shaped monetary policy. Consequently, as can be seen by developments in December 1968, these press releases seem to have played an important role in transmitting shifts in monetary policy to financial markets.

References

Cook, Timothy and Thomas Hahn (1988), "The Information Content of Discount Rate Announcements and Their Effect on Market Interest Rates," Journal of Money, Credit and Banking, vol. 20, no. 2, May, pp. 167-180.

Danker, Deborah J. and Matthew M. Luecke (2005), "Background on FOMC Meeting Minutes (PDF)," Federal Reserve Bulletin, Spring, pp. 175-179.

Jefferson, Phillip N. (2024), "Communicating about Monetary Policy," speech delivered at "Central Bank Communications: Theory and Practice," a conference hosted by the Federal Reserve Bank of Cleveland, Cleveland, Ohio, May 13.

Lindsey, David (2003), "A Modern History of FOMC Communication: 1975-2002 (PDF)," memorandum to the FOMC, June 24.

Meltzer, Alan H. (2009), A History of the Federal Reserve, vol. 2, book 1, The University of Chicago Press, Chicago, IL.

Meulendyke, Ann-Marie (1998), "U.S. Monetary Policy and Financial Markets," Federal Reserve Bank of New York, New York.

Nelson, Edward (2025), "A Look Back at 'Look Through'," Finance and Economics Discussion Series 2025-37, Washington: Board of Governors of the Federal Reserve System.

Roley, V. Vance and Rick Troll (1984), "The Impact of Discount Rate Changes on Market Interest Rates," Federal Reserve Bank of Kansas City Economic Review, vol. 69, January, pp. 27-39.

Romer, Christina and David Romer (1989), "Does Monetary Policy Matter? A New Test in the Spirit of Friedman and Schwartz," NBER Macroeconomics Annual, Volume 4, pp. 121-170.

Smirlock, Michael and Jess Yawitz (1985), "Asset Returns, Discount Rate Changes, and Market Efficiency," The Journal of Finance, vol. XL, no. 4, September, pp.1141-1158.

Yellen, Janet L. (2013), "Communication in Monetary Policy," speech delivered at the Society of American Business Editors and Writers 50th Anniversary Conference, Washington, D.C., April 4.

1. Mark Carlson ([email protected]) and Benjamin K. Johannsen ([email protected]) are with the Board of Governors of the Federal Reserve System. Daben Chen ([email protected]) is with Duke University and was an intern at the Board of Governors of the Federal Reserve System when much of the work on this project was done. The views expressed here are those of the authors and do not necessarily reflect to the views of the Board of Governors, the FOMC, or anyone else. The authors thank Ed Nelson for helpful comments. Return to text

2. See Janet L. Yellen (2013), "Communication in Monetary Policy," speech delivered at the Society of American Business Editors and Writers 50th Anniversary Conference, Washington, D.C., April 4. Return to text

3. See page 439 in Meltzer (2009) and page 16 in Nelson (2025). Return to text

4. See Phillip N. Jefferson (2024), "Communicating about Monetary Policy," speech delivered at "Central Bank Communications: Theory and Practice," a conference hosted by the Federal Reserve Bank of Cleveland, Cleveland, Ohio, May 13. Return to text

5. David Lindsey (2003), "A Modern History of FOMC Communication: 1975-2002 (PDF)," memorandum to the FOMC, June 24. Return to text

6. Christina Romer and David Romer (1989), "Does Monetary Policy Matter? A New Test in the Spirit of Friedman and Schwartz," NBER Macroeconomics Annual, Volume 4, pp. 121-170. Return to text

7. Ann-Marie Meulendyke (1998), "U.S. Monetary Policy and Financial Markets," Federal Reserve Bank of New York, New York. Return to text

8. Related press releases are available on FRASER (Federal Reserve Bank of St. Louis). Return to text

9. See the Board's press release issued on June 2, 1960, available via FRASER. See the Board's press release issued on August 12, 1960, available via FRASER. Return to text

10. See the Board's press release issued on July 16, 1963, available via FRASER. Return to text

11. See the Board's press release issued on December 6, 1965, available via FRASER. Return to text

12. See the FOMC Meeting Minutes from November 23, 1965 (PDF), available on the Board's website. Return to text

13. Not all Reserve Banks changed the rates on the same day. Typically, the initial change would involve several Reserve Banks and the rest would change their rates over the next few days. Only the initial change involved an extended statement detailing the economic rationale. The statements associated with subsequent changes were short and only indicated that the rates had been changed. When calculating the proportion of statements that included an economic rationale, we only consider initial statements. Return to text

14. FOMC Memorandum of Discussion, Dec. 17, 1968 (PDF), p. 3, available on the Board's website. Return to text

15. FOMC Memorandum of Discussion, Apr. 1, 1969 (PDF), p. 36, available on the Board's website. Return to text

16. Annual Report of the Board of Governors of the Federal Reserve System, 1966, p. 95, available via FRASER. Return to text

17. H. Erich Heinemann (1967), "Making credit easy: Reserve's reduction in discount rate held important but not new policy," New York Times, April 8, p. F38. Return to text

18. See the Board's press release from December 17, 1968, available via FRASER. Return to text

19. FOMC Memorandum of Discussion, Dec. 17, 1968 (PDF), p 3, 62, 80, 84, available on the Board's website. Return to text

20. FOMC Memorandum of Discussion, Jan. 14, 1969 (PDF), available on the Board's website. Return to text

21. Expectations for the changes are described by Janssen, Richard. "Discount Rate Boost Likely to be Studied Today by Reserve Open Market Committee" Wall Street Journal, Dec 17, 1968, p. 3. Return to text

22. Wall Street Journal, "Discounting Inflation", Dec. 19, 1968, p. 18. Return to text

23. Wall Street Journal, "Discount Rate is Raised to 5-1/2% Today from 5-1/4%; Reserve Board Calls Boost Anti-Inflationary Move," Dec. 18, 1968, p. 3. Return to text

24. For a discussion of the release schedule for the "Record of Policy Actions" and the minutes of FOMC meetings, see Deborah J. Danker and Matthew M. Luecke (2005), "Background on FOMC Meeting Minutes (PDF)," Federal Reserve Bulletin, Spring, pp. 175-179. Return to text

Carlson, Mark, Daben Chen, and Benjamin K. Johannsen (2026). "Federal Reserve Discount Rate Press Releases in the 1960s and 1970s through the Lens of Monetary Policy Communications," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, May 29, 2026, https://doi.org/10.17016/2380-7172.4053.

Disclaimer: FEDS Notes are articles in which Board staff offer their own views and present analysis on a range of topics in economics and finance. These articles are shorter and less technically oriented than FEDS Working Papers and IFDP papers.