FEDS Notes

May 09, 2018

Low risk as a predictor of financial crises

Jon Danielsson (London School of Economics), Marcela Valenzuela (University of Chile), and Ilknur Zer

The global crisis in 2008 blindsided every observer. We had come to believe that crises were a thing of the past. The rules and institutional structure in place protected us. The crisis proved all of this wrong.

Since then, we have been searching for ways to predict that a crisis might be under way so the policy authorities and private institutions can prepare.

One of the key tools is early warning indicators of crises, EWIs, which gained some prominence after the Asian crisis of 1998. Those in place in 2008 did not work well (Rose and Spiegel, 2009), and to rectify that, a variety of EWIs have been proposed.

At the risk of oversimplification, we can classify this work in two main categories. First group of EWIs that are purely data-driven, and based on market data indicators, such as stock prices, volatility and CDS spreads. The second category uses economic theory to guide the indicator design, looking more fundamentally at how risk emerges in the first place.

Theoretical background

Economic theory is quite clear on where we should look for indications of crisis. Both Keynes (1936) and Hayek (1960) suggest that perceptions of risk--especially when they deviate from what economic agents have come to expect--affect risk taking behavior.

Perhaps the best expression of this view is Minsky's (1977) instability hypothesis, where economic agents observing low financial risk are induced to increase risk-taking, which in turn may lead to a crisis -- the foundation of his famous dictum that "stability is destabilizing."

The recent literature reaches the same conclusion, for example Brunnermeier and Sannikov's (2014) "volatility paradox" and Bhattacharya's et. al (2015) examination of Minsky's hypothesis. Similarly, Danielsson et. al (2012) consider a general equilibrium framework with risk constraints, where up on observing low volatility, agents are endogenously incentivized to increase risk.

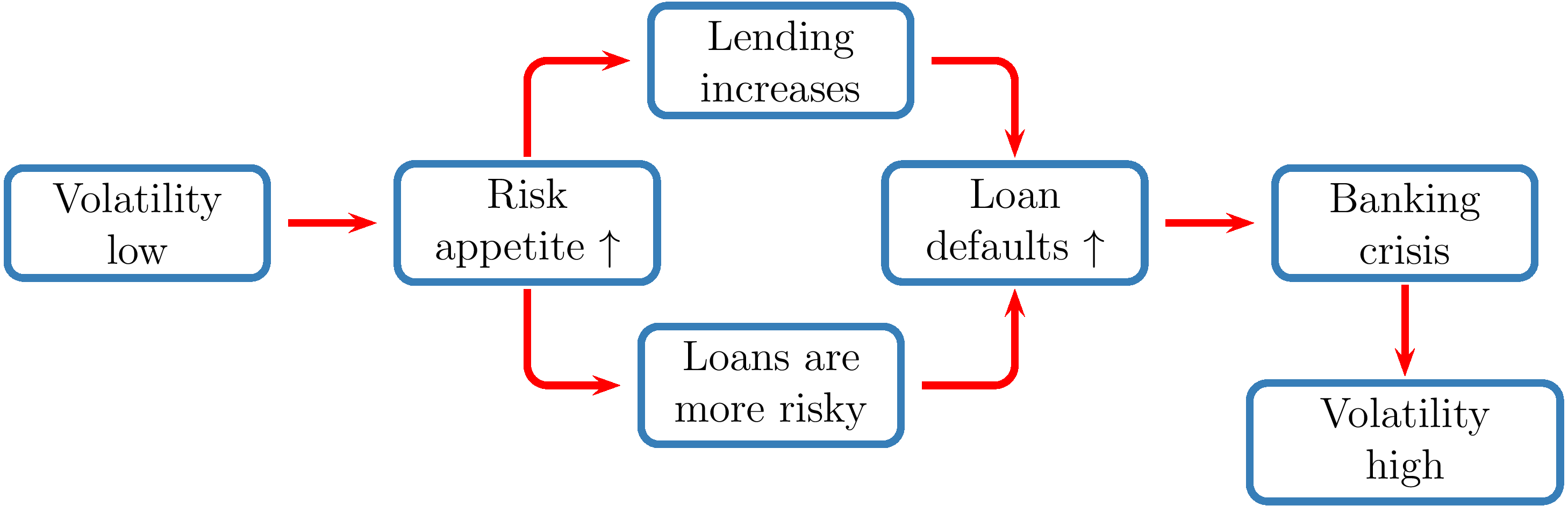

The basic mechanism for the relationship of risk to crisis can be seen in the following figure.

At the start, economic agents observe that volatility is lower than what they have come to expect. This fuels optimism, making the agents more willing to take more risk. This is manifested within the banking sector, which will both lend more than it did before and also make riskier loans. Eventually, loan defaults mount, a banking crisis ensues, at which time volatility increases sharply.

This chain of events implies that a considerable time passes between an observation of low volatility and crises. By contrast, an observation of high volatility directly results from a crisis, implying that by the time volatility peaks, it is too late to react.

The empirical data-driven literature

Most empirical literature on early warning indicators, EWIs, takes the opposite view that the likelihood of crises increases along with measured risk, typically measured by ex-post outcomes in financial markets, price movements or volatility, VIX, CDS spreads, volumes and other activity measures. Examples include SRISK (Acharya et. al 2012) and the ECB systemic risk composite indicator.

The theoretical literature suggests that such EWIs are likely to be of limited use. They signal high risk once a crisis is underway, but do not provide much in terms of ex ante prediction, limiting their usefulness.

A counterargument might be that a particular indicator gave a good warning for events of 2008, however, that is one observation with multiple degrees of freedom for optimization, calculated ex-post. It is straightforward use the benefit of hindsight to find a measure that predicts a single known crisis event in history. However, such indicators are unlikely to capture the buildup of systemic risk that leads to crises in the future.

Empirically testing the theoretical literature

Several recent papers have been guided by the theoretical literature in the design of EWIs. The most promising ones are those that link credit expansions to crises, as for example Schularick and Taylor (2012), or Baron and Xiong (2016), where over-optimism increases the likelihood of a financial crisis.

Danielsson, Valenzuela and Zer (2018) take this one step further and formally investigate the mechanism in Figure 1 above. They take a historical perspective, using data going back to 1800 were available, and 60 countries, examining the likelihood of crises as a function of volatility.

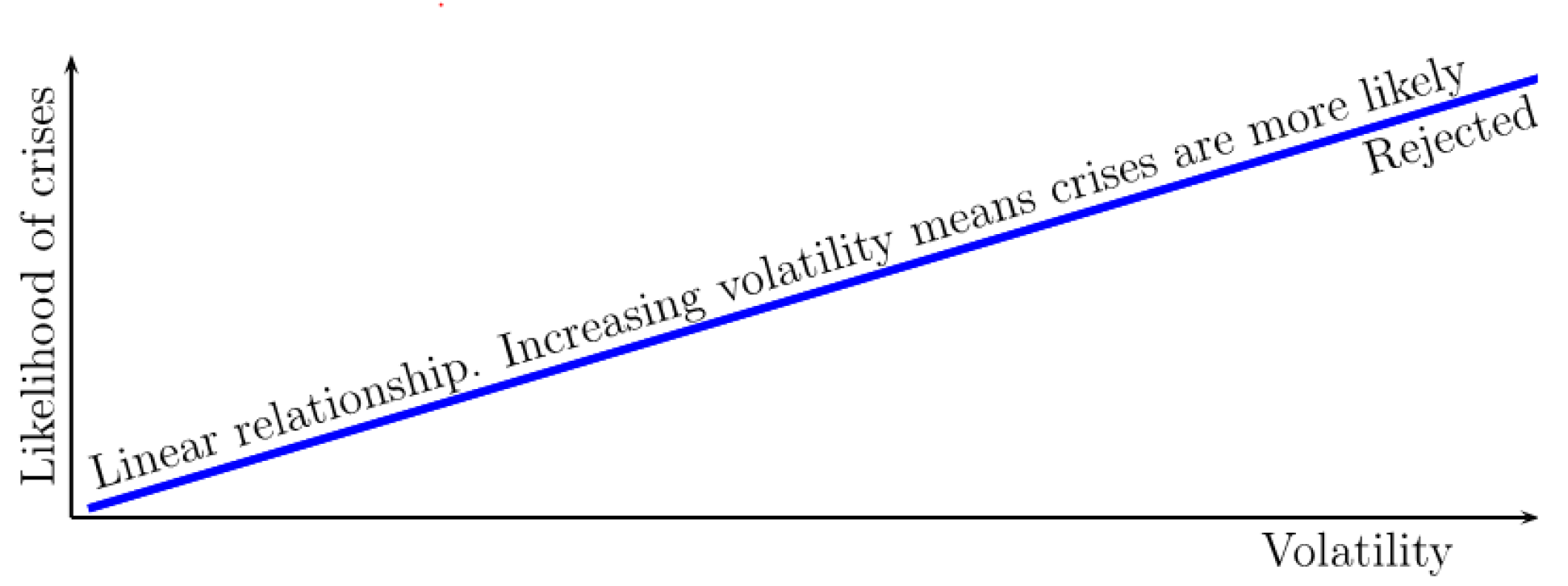

To start with, they investigate the relationship between current volatility and the likelihood of future crisis -- what could be called the linear volatility-crisis view, as seen in the next figure. This is rejected by the data. When coupled with macroeconomic variables to capture the state of the economy, volatility itself is not a significant predictor of crises.

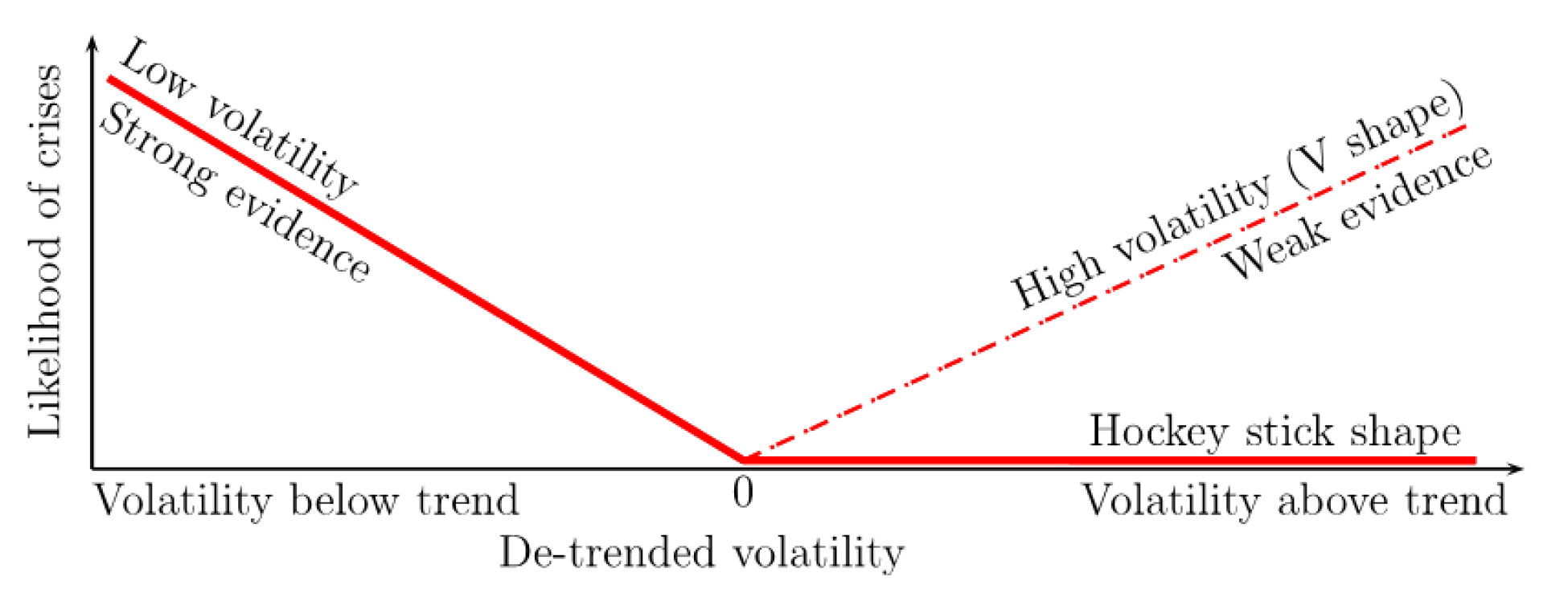

However, by decomposing volatility into trend, and deviations from trend, a different picture emerges. The reason is that economic agents see the trend as "usual/expected" volatility, and when it deviates from the trend, risk-taking behavior is affected.

That leaves two forms of volatility -- low volatility, when it is below trend, and high volatility when above the trend. The relationship between low and high volatilities and the likelihood of crises can be seen in the following Figure.

The slope of the curve, which translates into regression coefficients in a statistical model indicates the strength of the relationship. The higher the slope in absolute terms, the more likely a crisis becomes as volatility moves away from its trend. Danielsson, Valenzuela and Zer (2018) find strong evidence for low volatility but only weak evidence for high volatility causing crises.

The economic impact is the highest if the economy stays in the low volatility environment for five years: a 1% decrease in volatility below its trend translates to a 1.01% increase in the probability of a crisis.

They also show that the chain of causality in Figure 1 above, with low volatility leading to increased lending and excessive risk, holds empirically.

Volatility as an early warning indicator

These results suggest that volatility would not be a good crisis indicator. It might tell policymakers that a crisis is under way, but we suspect that they will know that anyways.

A standard way to evaluate the quality of EWIs is the area under the receiving operating curve (AUROC). An AUROC of 0.5 means that an EWI is no better than random noise, while a value of 1.0 implies perfect predictability.

Low volatility has an AUROC value of 76%, with a 95% confidence interval of [72%, 80%]. This means that it provides a reliable signal to policymakers for the incidence of future crisis.

Conclusion

Within the post-2008 crisis macroprudential agenda, policymakers are actively searching for signals of future financial and economic instability and developing policy tools to mitigate the most unfortunate outcomes.

Most EWI of crises are founded on ex-post market data, typically volatility in some form or another, where increasing volatility indicates the financial system has become more risky, and a crisis is therefore more likely.

However, an observation of high risk is the consequence of a stress event where financial instructions are in difficulties, not the cause.

It will be more fruitful to search for EWIs amongst the fundamental drivers of financial instability. A major cause of financial crises is excessive risk-taking by economic agents. When they perceive a low risk environment, they are endogenously incentivized to take more risk, which ultimately culminates in a crisis.

This view has been expressed by policymakers:

"Volatility in markets is at low levels...to the extent that low levels of volatility may induce risk-taking behavior...is a concern to me and to the Committee."

Former Federal Reserve Former Chair Janet Yellen. 2014

The data confirms this view. An observation of low risk is a significant crises predictor and suitable for an EWI.

The policy authorities and private institutions would consequently benefit from using low volatility as a crisis indicator since an observation of current low volatility implies that a future crisis is more likely.

Bibliography

Acharya, Viral, Robert Engle and Matthew Richardson (2012), "Capital shortfall: A new approach to ranking and regulating systemic risks" VoxEU, 14 March. https://voxeu.org/article/capital-shortfall-new-approach-ranking-and-regulating-systemic-risks

Baron, M. and W. Xiong (2017). Credit expansion and neglected crash risk. Quarterly Journal of Economics 132, 713-764.

Bhattacharya, S., C. Goodhart, D. Tsomocos, and A. Vardoulakis (2015). A reconsideration of Minsky's financial instability hypothesis. Journal Money Credit and Banking 47, 931–973.

Brunnermeier, M. and Y. Sannikov (2014). A macroeconomic model with a financial sector. American Economic Review 104, 379–421.

Danielsson, J., H. S. Shin, and J.-P. Zigrand (2012). Procyclical leverage and endogenous risk. Working Paper, Princeton University.

Daníelsson, J., M. Valenzuela, and I. Zer (2018,). Learning from history: Volatility and financial crises. Review of Financial Studies, Forthcoming. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2872651

Hayek, F. (1960). The Constitution of Liberty. Routledge.

Keynes, J. M. (1936). The General Theory of Interest, Employment and Money. London: Macmillan.

Minsky, H. (1977). The financial instability hypothesis: An interpretation of Keynes and an alternative to "standard" theory. Nebraska Journal of Economics and Business 16, 5–16.

Rose, Andrew and Mark Spiegel (2009) "Could an early warning system have predicted the crisis?" 03 August. https://voxeu.org/article/could-early-warning-system-have-predicted-crisis

Schularick, Moritz and Alan Taylor (2012) "Credit Booms Gone Bust: Monetary Policy, Leverage Cycles, and Financial Crises, 1870-2008". American Economic Review, 102, 1029-1061.

Danielsson, Jon, Marcela Valenzuela, and Ilknur Zer (2018). "Low risk as a predictor of financial crises," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, May 9, 2018, https://doi.org/10.17016/2380-7172.2169.

Disclaimer: FEDS Notes are articles in which Board staff offer their own views and present analysis on a range of topics in economics and finance. These articles are shorter and less technically oriented than FEDS Working Papers and IFDP papers.