FEDS Notes

June 26, 2026

Recent Developments in Foreign Direct Investment into the U.S.

In 2025, U.S. tariffs rose sharply, contributing to record-high trade and economic policy uncertainty. Part of the motivation for the tariffs announced in April 2025 reflects a desire to spur foreign direct investment (FDI) into the United States. However, elevated policy uncertainty could work against this goal, as firms may delay investments amid ambiguity over the duration and severity of tariffs (Jinji and Inada, 2023; Bonaime, Gulen and Ion, 2018). Additionally, while tariffs can increase investment in some industries, evidence suggests they can adversely impact other industries that use tariffed goods as intermediate inputs (Moder and Spital, 2025).

Alongside these tariff-related developments, the AI boom in the U.S. has spurred massive domestic investments, especially in data center construction, which may draw in or be financed by foreign investors.

Amid these developments, this note provides a descriptive overview of how FDI into the U.S. shifted in 2025. I show that although aggregate FDI into the U.S. was resilient, this masks substantial heterogeneity across industries. Namely, FDI plunged in food manufacturing and transportation equipment manufacturing. Meanwhile, FDI surged in metal product manufacturing—due to the completion of Nippon Steel's acquisition of U.S. Steel announced in 2023—and in electrical equipment manufacturing, possibly as part of the AI boom.

Beyond these industry-level shifts, the composition of new FDI—greenfield FDI projects and cross-border mergers and acquisitions—provides additional insight. Greenfield FDI into the U.S. was down slightly from 2024 but roughly in line with 2022 and 2023. The number of foreign acquisitions of U.S. firms declined, but the value of announced deals surged, reflecting announced but not-yet-completed acquisitions of U.S. firms in the high-tech sector amid the AI boom, pointing toward substantial FDI inflows if these high-tech acquisitions are completed.

FDI in Official Statistics

We first analyze the official measures of FDI into the U.S., reported by the Bureau of Economic Analysis (BEA). This measure is available for the U.S. in aggregate, as well as by type of financing, by industry, or by source country.

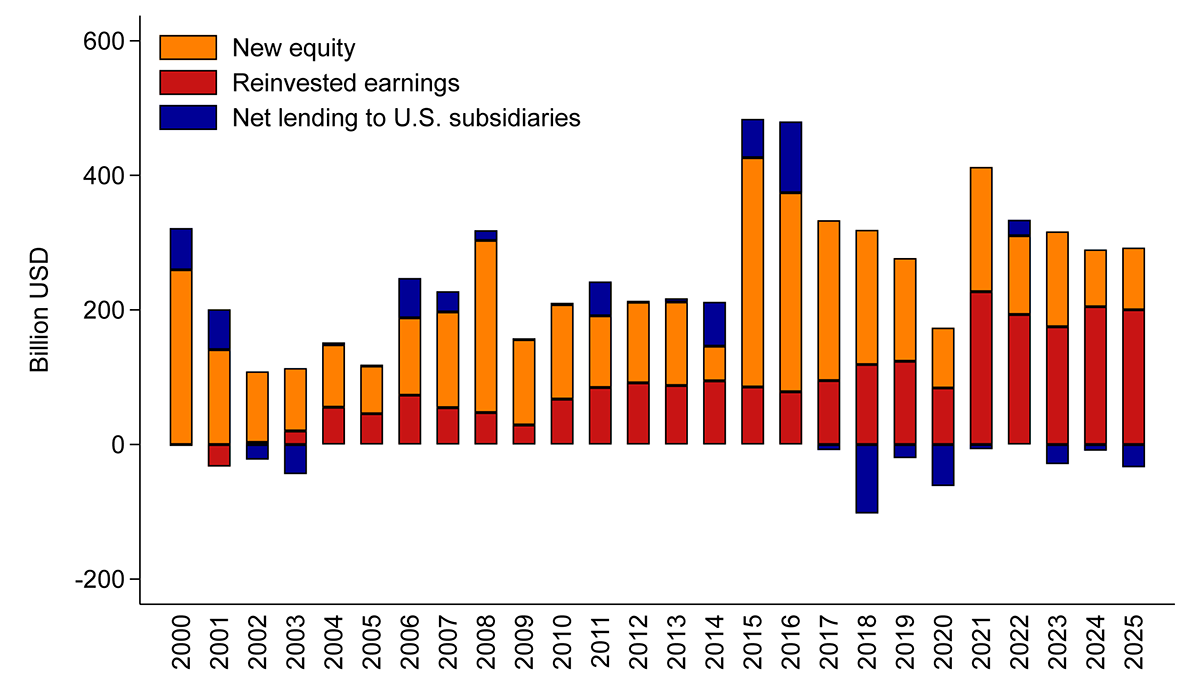

Figure 1 presents total FDI into the U.S. by the type of financing—new equity investment, reinvested earnings, and net lending from foreign parent companies to their U.S. subsidiaries. Total FDI into the U.S. was little-changed in 2025 compared to 2024—down slightly on a directional basis—and slightly lower than the preceding years.1 Any impacts from tariffs and trade uncertainty are not obvious in aggregate.

Note: The debt series is shown on a directional basis.

Source: Bureau of Economic Analysis, International Transactions, via Haver, as of June 24, 2026.

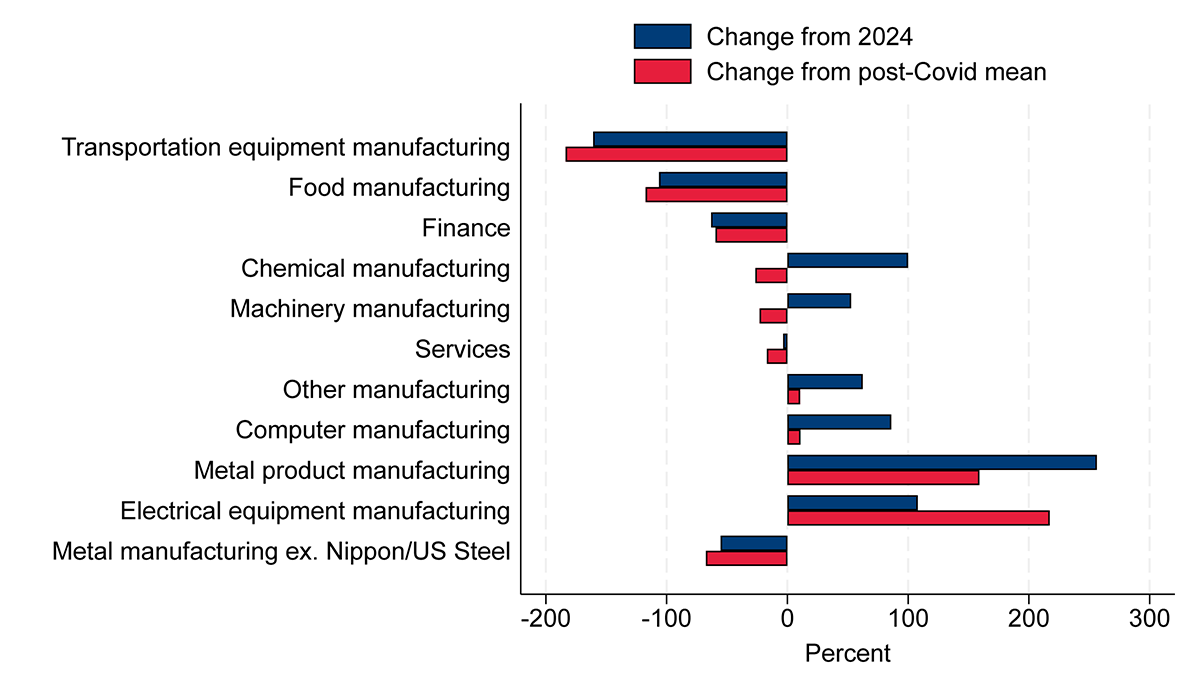

However, this aggregate result masks substantial heterogeneity across industries. Figure 2 reports the percent change in inward FDI by industry, compared to either 2024 or a baseline of average FDI over 2021-2024 (the post-Covid, pre-tariff period). Inward FDI in food manufacturing and transportation equipment manufacturing (primarily automotives) plummeted. Meanwhile, FDI surged in metal product manufacturing—entirely due to the completion of Nippon Steel's $14.2 billion acquisition of U.S. Steel, which was initiated in 2023. Excluding this deal, FDI into metal product manufacturing would have declined by about 60 percent. FDI also rose in electrical equipment, appliance and component manufacturing, which may reflect demand for electrical equipment as part of data center construction.

Note: Key identifies in order from top to bottom.

Source: Bureau of Economic Analysis, International Transactions, via Haver, as of June 24, 2026.

New FDI into the U.S.

The analysis above focuses on official measures of FDI. However, overall FDI includes reinvested earnings and net lending between parents and affiliates, which may be less responsive to recent developments than new equity-based investments (Tabova, 2020). New FDI consists of greenfield FDI—investments in new facilities or projects—and cross-border acquisitions. While cross-border acquisitions are the primary form of new FDI for the U.S., greenfield FDI draws greater attention for new investment and production.

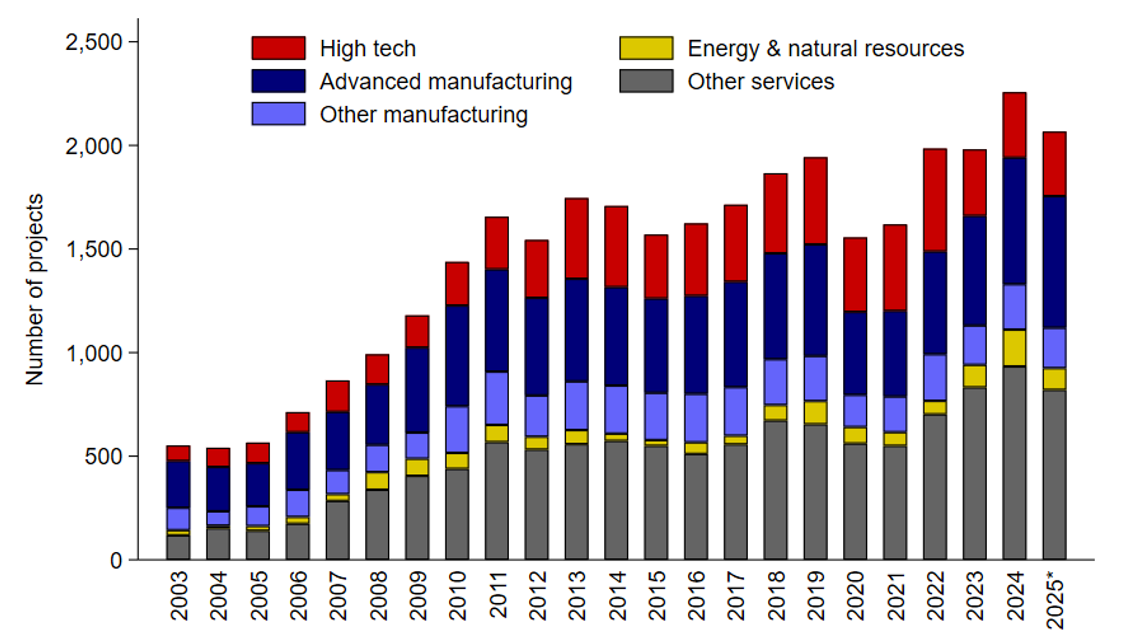

Figure 3 presents the number of greenfield FDI projects announced in each year, grouped into five sectors: high tech, advanced manufacturing, other manufacturing, energy and natural resource extraction, and other services. These data come from fDi Markets, a service of the Financial Times.2

Note: Counts for 2025 are preliminary and may be revised up slightly. Key identifies in order from top to bottom.

Source: fDi Markets, as of April 2026.

The number of greenfield FDI announcements decreased in 2025 relative to 2024, although it remains slightly above the levels of 2022 and 2023. These tabulations display no notable shifts across sectors, nor any obvious foreign participation in the U.S. AI boom via greenfield investment. This lack of heterogeneity is remarkable compared to the more dramatic shifts in overall FDI by industry in Figure 2.

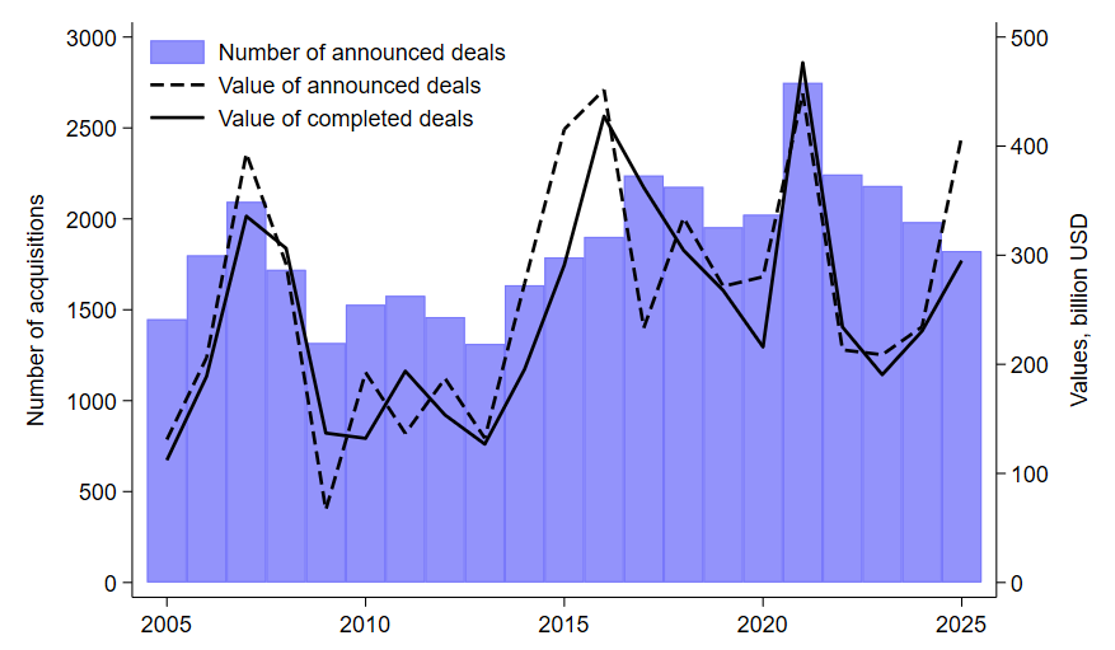

Greenfield FDI is a small portion of total FDI into the U.S. The vast majority of new FDI consists of foreign acquisitions of U.S. firms—shown in Figure 4, based on data from LSEG Data and Analytics. In 2025, the number of foreign acquisitions of U.S. firms declined to its lowest level since 2015. However, the value of completed deals rose moderately, and the value of announced deals surged, suggesting a pipeline of major transactions to be completed in 2026 and 2027.

Note: The totals exclude withdrawn deals, recapitalizations, repurchases, spinoffs, self-tenders, and exchange offers.

Source: LSEG Data and Analytics, as of April 3, 2026.

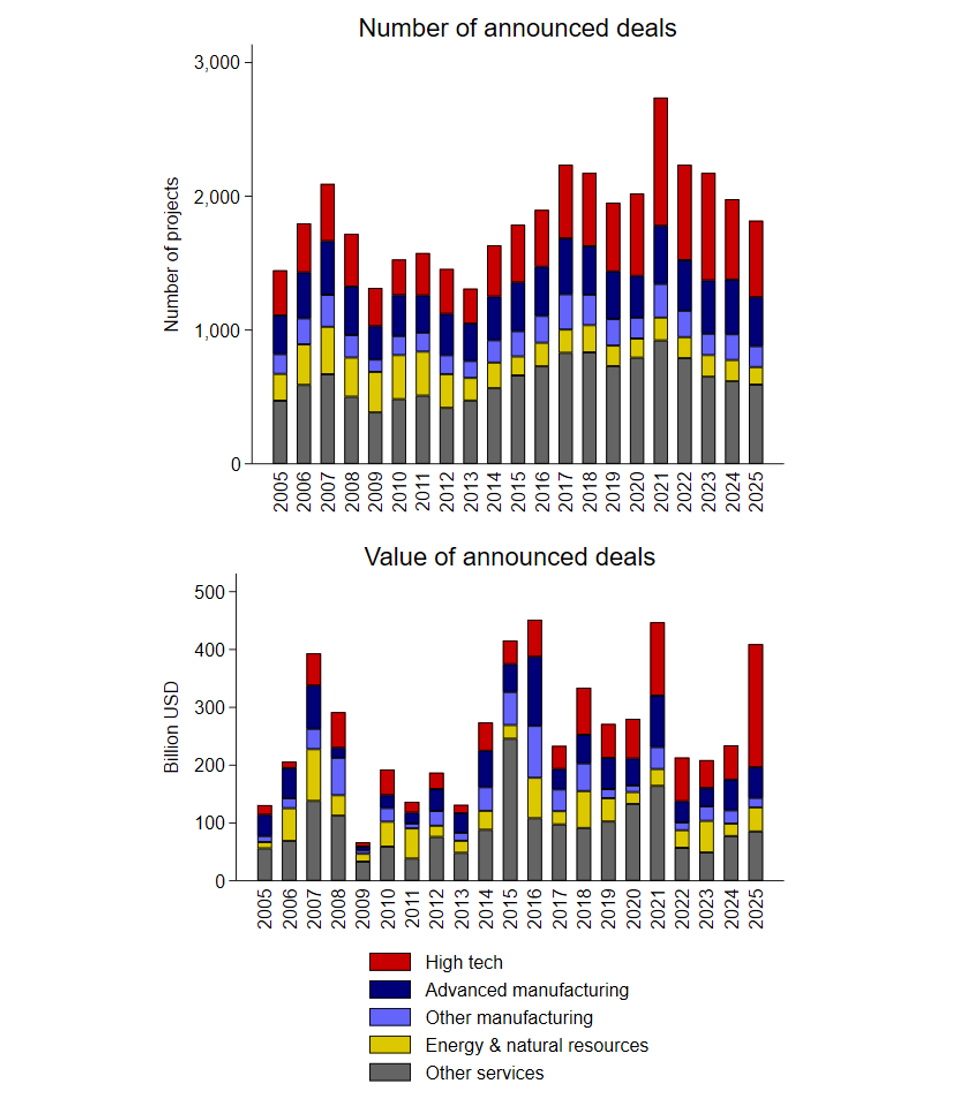

To understand the driving forces behind these developments, Figure 5 presents the number and value of announced deals by sector of the U.S. target firm, using similarly defined sectors as in Figure 3. The modest decline in the number of deals is broadly similar across sectors. However, the right panel reveals that the surge in the value of announced deals almost entirely reflects the high-tech sector. In 2025, the value of announced foreign acquisitions of U.S. high-tech companies jumped to $213 billion, comparable to the $219 billion average of total acquisitions announced in 2022-2024.

Note: The totals exclude withdrawn deals, recapitalizations, repurchases, spinoffs, self-tenders, exchange offers, and acquisitions of government and agency entities. Key identifies in order from top to bottom.

Source: LSEG Data and Analytics, as of April 2026, aggregated by announcement date.

These new announcements primarily reflect foreign investment in the U.S. AI boom via cross-border M&A, especially through mega-deals and large deals. However, these deals typically require some time for approval, and they will not appear in official FDI statistics until their completion in 2026 or 2027. This also confirms that foreign participation in the U.S. AI boom primarily comes through acquisitions of U.S. companies in the high-tech sector, rather than through greenfield investment.

Conclusions

In aggregate, foreign direct investment into the U.S. appeared resilient in 2025, with limited visible impacts from tariffs or trade policy uncertainty. However, this aggregate resilience conceals substantial heterogeneity, with divergent responses across manufacturing industries. Whether these industry-specific patterns persist or change as the tariff environment shifts merits future monitoring, especially the responses of investment in tariff-impacted industries.

The number of new foreign investments in the U.S.—either for greenfield FDI or cross-border acquisitions—decreased modestly in 2025. While the value of announced foreign acquisitions of U.S. companies surged, this entirely reflects foreign investment into the U.S. AI boom and associated high-tech firms. Whether these large foreign acquisitions of U.S. high-tech firms are completed successfully will be an important determinant of total FDI into the U.S. in 2026.

References

Bonaime, Alice, Huseyin Gulen, and Mihai Ion (2018). "Does policy uncertainty affect mergers and acquisitions?" Journal of Financial Economics 129(3), https://doi.org/10.1016/j.jfineco.2018.05.007.

Jinji, Naoto, and Mitsuo Inada (2023). "The impact of policy uncertainty on foreign direct investment: Micro-evidence from Japan's international investment agreements." Review of International Economics 32(3), https://doi.org/10.1111/roie.12710.

Moder, Isabella, and Tajda Spital (2025). "The Protectionist Gamble: How Tariffs Shape Greenfield Foreign Direct Investment." ECB Working Paper no. 2025/3144, https://dx.doi.org/10.2139/ssrn.5710183.

Tabova, Alexandra (2020). "What Happened to Foreign Direct Investment in the United States?" FEDS Notes. Washington: Board of Governors of the Federal Reserve System.

1. On an asset-liability basis, FDI into the U.S. rose by a quarter in 2025. However, that almost entirely reflects U.S. multinational parent companies borrowing from their foreign subsidiaries, which on a directional basis is more appropriately treated as a decrease in outward FDI. Return to text

2. The fDi Markets greenfield FDI data used in this analysis were received in April 2026. These data are prone to revision as additional project information is collected, so the 2025 numbers may be revised up slightly. Return to text

Kallen, Cody (2026). "Recent Developments in Foreign Direct Investment into the U.S.," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, June 26, 2026, https://doi.org/10.17016/2380-7172.4099.

Disclaimer: FEDS Notes are articles in which Board staff offer their own views and present analysis on a range of topics in economics and finance. These articles are shorter and less technically oriented than FEDS Working Papers and IFDP papers.