FEDS Notes

May 08, 2026

Trade Finance Activities of U.S. Banks: What the Data Can Tell Us

Friederike Niepmann and Tim Schmidt-Eisenlohr1

Trade finance encompasses a range of financial instruments and services designed to facilitate international trade. U.S. banks are key providers of these services. This note draws on several regulatory data sources to show that trade finance supports a sizeable share of international trade, is highly concentrated in large U.S. banks, and has declined over time. Potential risks to the banking system from this activity appear small, among other things because it constitutes only a small portion of banks' overall business.

Trade Finance Instruments and Their Role in International Trade

International trade is risky and takes time. Contracts are difficult to enforce across borders, and shipping goods internationally can take weeks. These frictions create both heightened risk and greater financing needs for firms engaged in cross-border commerce. Financial intermediaries play a crucial role in helping firms navigate these challenges through the provision of trade finance (Niepmann and Schmidt-Eisenlohr, 2017a). The primary trade finance instruments provided by banks include:2

- Trade finance loans are extended to finance imports and exports, providing working capital to bridge the time gap between production or purchase and final payment.

- Letters of credit (LCs) serve as a commitment device and payment guarantee. Under a letter of credit arrangement, an exporter documents the shipment of goods. The importer's bank guarantees payment to the exporter upon presentation of these documents. This instrument substantially reduces the risk of non-payment for exporters and the risk of payment without delivery for importers.

- Documentary collections involve the importer's bank releasing shipping documents to the importer only upon payment, providing a simpler alternative to letters of credit with somewhat less protection for the parties involved.

Measuring U.S. Banks' Trade Finance Activities: Data Sources and Challenges

Measuring banks' trade finance activities presents significant challenges because data on this business line are scarce and fragmented across multiple regulatory reports. We draw on three primary data sources, each with distinct coverage and limitations:3

- Y-14 loan-level data provide information on commercial and industrial (C&I) loans with the designated purpose of "trade finance". These data have been collected since 2011 but cover only the very largest bank holding companies subject to stress testing by the Federal Reserve. In 2024, 33 institutions reported Y-14 data.

- FFIEC 009 reports contain data on banks' "trade finance claims" by country and quarter. These data have been collected since the 1980s and cover institutions with substantial international activities—a broader set than Y-14 reporters but still limited to approximately 70 institutions. The trade finance claims reported in FFIEC 009 likely encompass both letters of credit and trade finance loans. Based on the correlation with trade patterns documented in Niepmann and Schmidt-Eisenlohr (2013), these claims appear to support primarily U.S. exports rather than imports.

- Call Report data include information on commercial letters of credit as an off-balance-sheet item. These data are available for the universe of U.S. banks from the 1990s onward, though they lack the country-level detail available in the FFIEC 009 reports.

Each data source captures different aspects of trade finance activity, and none provides a complete picture. The Y-14 data offer loan-level granularity but limited institutional coverage and history. The FFIEC 009 data provide longer time series and country-level detail but combine different instrument types. The call reports offer the broadest institutional coverage but provide only aggregate figures for letters of credit without geographic breakdown. By examining all three sources together, we can develop a more comprehensive understanding of the scale and evolution of U.S. banks' trade finance business.

The Size and Concentration of Trade Finance Activities

Our analysis of these data sources reveals several findings about the current state and evolution of U.S. banks' trade finance business:

Current Volumes

As of the fourth quarter of 2024, the available data indicate that trade finance loans totaled approximately $70 billion to foreign firms and $30 billion to U.S. firms (Y-14 data).4 At the same time, total trade finance claims reached $57 billion (FFIEC 009 data), and outstanding commercial letters of credit amounted to approximately $15 billion (call report data). These figures, while substantial in absolute terms, represent a relatively small share of banks' overall balance sheets and business activities, as we discuss below.

Concentration Among Large Banks

The trade finance business is highly concentrated among the largest U.S. banking institutions. In the Y-14 data for 2024, the five largest trade finance providers account for more than 75 percent of all trade finance loans. Remarkably, 17 of the 33 institutions reporting Y-14 data—more than half—report zero trade finance loans, indicating they do not engage in this business line at all.

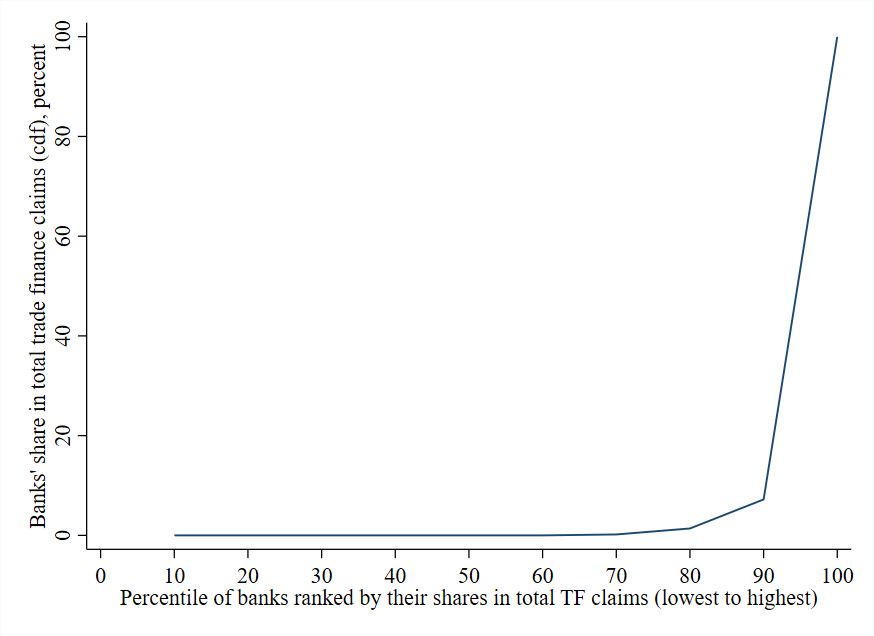

The FFIEC 009 data show an even higher degree of concentration: the largest five banks account for more than 87 percent of reported trade finance claims, and 40 of the 70 reporting institutions have zero trade finance claims in that data. Figure 1 illustrates this concentration, showing the distribution of trade finance claims across banks in the form of the cumulative distribution function. The x-axis has banks ranked by their shares of total claims and grouped into deciles. The y-axis shows the share in total trade finance claims that the banks in each decile account for. Banks in the highest decile of share in trade finance claims account for 90 percent of the U.S. banks' total trade finance claims.

Source: FFIEC009, staff calculations.

The call report data, which cover the universe of U.S. banks, reveal that approximately 90 percent of all banks report zero commercial letters of credit. This extreme concentration reflects both economies of scale in trade finance operations—which require specialized expertise and international networks—and the fact that smaller banks may serve fewer customers engaged in international trade.

A Declining Business Line

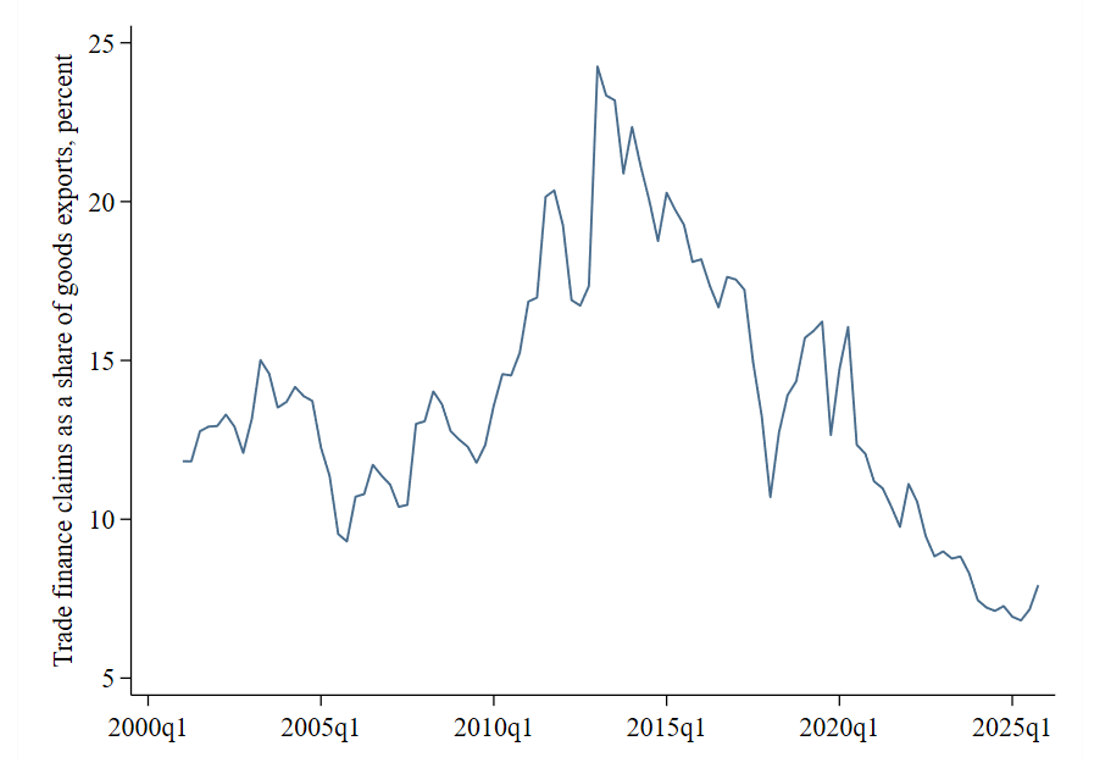

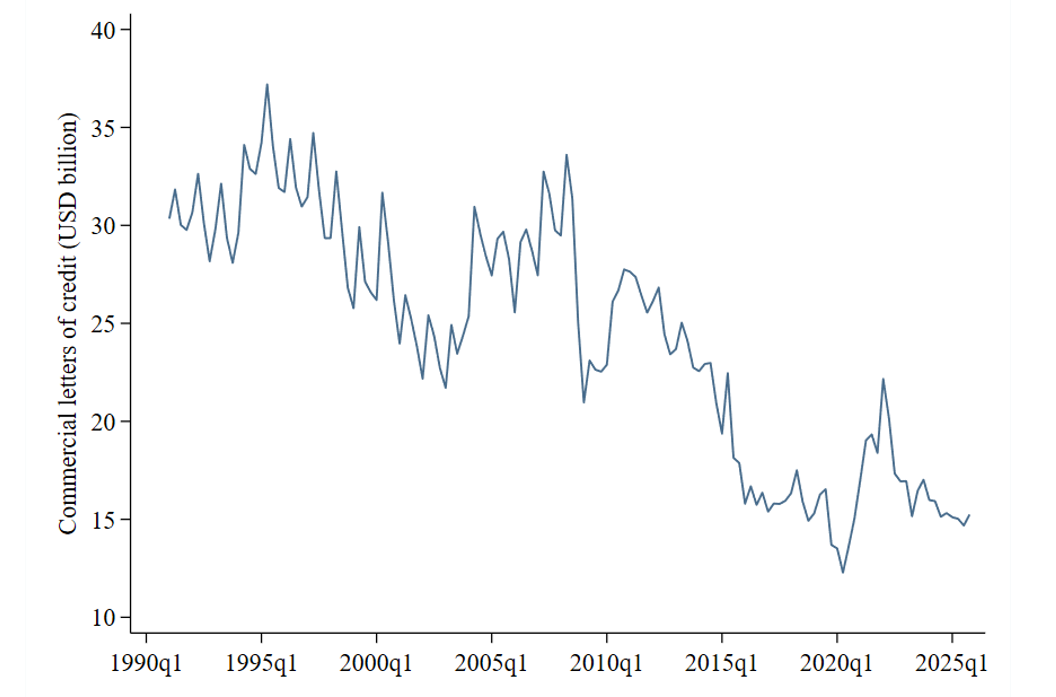

The FFIEC009 and call report data consistently show a decline in trade finance activity over the past decade. Figure 2 displays the longer time series available from FFIEC 009, revealing that trade finance claims as a share of U.S. goods exports have fallen substantially since 2014.5 Figure 3 presents the evolution of commercial letter-of-credit volumes from the call report data. It shows a general downward trend since the GFC, including over the past decade, although letter-of-credit volumes jumped during the Covid pandemic.

Source: FFIEC009, U.S. Census Bureau, staff calculations.

Source: FFIEC 031, staff calculations.

Based on 2013 data from SWIFT analyzed in Niepmann and Schmidt-Eisenlohr (2017a), letters of credit were used for approximately 7.6 percent of U.S. exports (around $43 billion quarterly) and 1.8 percent of U.S. imports (around $12 billion quarterly). Acknowledging the decline in the use of traditional trade finance instruments, we estimate that the quarterly volume of letters of credit supporting U.S. trade in 2024 was approximately $15-25 billion for exports and $6-10 billion for imports.6

Several factors may explain this decline in trade finance activity, even as a share of exports. Stricter anti-money-laundering regulations have increased the compliance costs of conducting business internationally, including trade finance. A key aspect is the retreat of correspondent banking relationships, which letters of credit depend on (Rice, von Peter, Boar, 2020). Additionally, the growth of global value chains and intra-firm trade may have reduced the need for letters of credit, as risk is smaller within multinational groups or well-established supply chains.7

Small Relative to Overall Bank Business

For the vast majority of banks engaged in trade finance, this activity represents a small share of their overall business. Thus, any issues in this business segment have only limited effects on banks' financial conditions. In the Y-14 data for 2024, trade finance loans constitute only 3.25 percent of total C&I loans and just 0.4 percent of total assets for reporting institutions. Even for the top 20 percent of banks in terms of trade finance activity, these loans represent less than 4 percent of total assets.

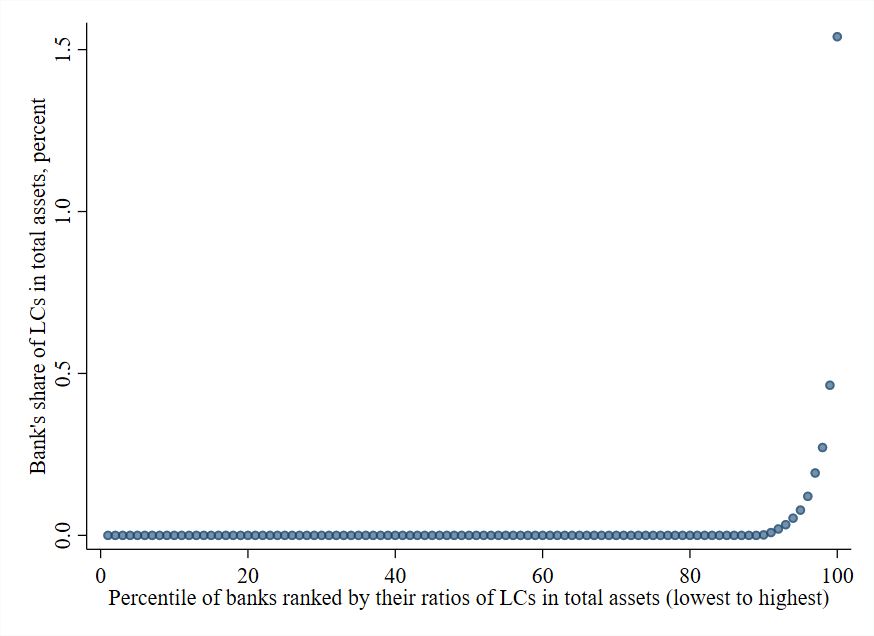

The call report data for 2024, plotted in figure 4, confirm this pattern. The chart shows the average ratio of letters of credit over total assets for banks in each percentile of the ratio's distribution. For most banks that report any commercial letters of credit, the total amount of letters of credit is below 0.5 percent of their total assets.

Source: FFIEC031, staff calculations.

But figure 4 also suggests that there are a few exceptions. For a small number of banks with total assets below $25 billion, trade finance represents a more significant share of business activity. These institutions may have developed specialized expertise or serve client bases particularly concentrated in import and export activities. For these banks, risks related to trade finance could have a more material impact on their balance sheets, though their small size limits systemic effects.

Implications for Financial Stability

Several characteristics of U.S. banks' trade finance business suggest that direct financial stability risks from this business line are generally limited. First, even for the largest trade finance providers, this business represents a small fraction of total assets and lending. Second, trade finance instruments are generally short-term, often maturing within 90 to 180 days. This short duration limits the accumulation of risk and reduces exposure to prolonged economic deterioration. Third, letters of credit and many trade finance loans are secured by the underlying goods being shipped or by other collateral. Documentary requirements provide incentives for importers to pay, and trade insurance can transfer credit risk away from exporters, making the underlying bank loans safer. Letters of credit can also be underwritten by national or multinational organizations like the U.S. Export-Import Bank and the World Bank's International Finance Corporation. Finally, the extreme concentration of trade finance among the very largest banks—institutions with diversified business models, substantial capital buffers, and sophisticated risk management—should further limit systemic risk.

The most significant risk to banks from trade-related developments likely comes not from direct trade finance exposures but from their broader lending to firms engaged in international trade. When U.S. firms lose export markets due to greater international competition or face increased input costs from tariffs, the resulting stress can propagate through banks' commercial loan portfolios more broadly.8 When banks are exposed to firms affected by trade shocks or trade policy uncertainty, they contract lending overall, amplifying effects on the real economy. As trade policy uncertainty has increased in recent years, understanding these indirect channels of transmission from trade shocks to the financial sector has become increasingly relevant.9

References

Ahn, JaeBin, and Miguel Sarmiento, 2019. "Estimating the direct impact of bank liquidity shocks on the real economy: Evidence from letter‐of‐credit import transactions in Colombia. "Review of International Economics" 27.5: 1510-1536.

Antras, Pol, and C. Fritz Foley. "Poultry in motion: a study of international trade finance practices." Journal of Political Economy 123, no. 4 (2015): 853-901.

Benguria, Felipe, Alvaro Garcia-Marin, and Tim Schmidt-Eisenlohr. "Trade Credit and Relationships." Journal of Financial Economics (forthcoming).

Correa, Ricardo, Julian di Giovanni, Linda Goldberg, and Camelia Minoiu. 2024. "Trade Uncertainty and U.S. Bank Lending." Federal Reserve Bank of New York Staff Reports.

Federico, Stefano, Fadi Hassan, and Veronica Rappoport. 2023. "Trade Shocks and Credit Reallocation." Journal of Political Economy 131(7): 1836-1879.

Niepmann, Friederike, and Tim Schmidt-Eisenlohr. 2013. "International Trade, Risk, and the Role of Banks." New York Fed Staff Report No. 633.

Niepmann, Friederike, and Tim Schmidt-Eisenlohr. 2017a. "International Trade, Risk, and the Role of Banks." Journal of International Economics 107: 111-126.

Niepmann, Friederike, and Tim Schmidt-Eisenlohr. 2017b. "No Guarantees, No Trade: How Bank Affect Export Patterns." Journal of International Economics 108: 338-350.

1. The views expressed in this note are those of the authors and do not necessarily reflect the position of the Board of Governors of the Federal Reserve System or the Federal Reserve System. Return to text

2. This note focuses on bank-provided trade finance. It does not cover instruments more commonly provided by specialized non-bank financial firms, which include: Trade credit insurance protects businesses from financial losses due to unpaid invoices or debts, transferring the credit risk to an insurance provider. Forfaiting and factoring involve the sale of accounts receivables, such as export invoices, to a specialized finance firm at a discount. Selling accounts receivables allows exporters to obtain immediate cash instead of waiting for payment. Return to text

3. Below we also discuss results from Niepmann and Schmidt-Eisenlohr (2017a), who use information on SWIFT messages associated with letters of credit and documentary collections. These data are no longer available to us. Return to text

4. The Y-14 estimates may represent a lower bound for U.S. banks' trade finance loans. For our estimates, we sum all loans in the Y-14 data to which banks assign the purpose "trade finance". However, there is a sizable fraction of loans that is assigned the purpose "working capital". Working capital loans are fungible and can be used for both domestic and international transactions. To the extent that working capital loans are used to finance international trade, we may underestimate the total value of bank loans supporting this activity. Return to text

5. Figure 2 plots total trade finance claims only from the year 2000 onward because of breaks in the series prior to 2000. Return to text

6. These numbers are estimated as follows: 1.8 percent of 2013 imports equal $12.4 billion and 7.6 percent of 2013 exports equal $43.3 billion. Trade finance claims by U.S. banks declined to 37.5 percent of their 2013 level in the FFIEC009 data and to 64 percent of their 2013 level in the FFIEC 031 data. Applying these declines to 2024 quarterly U.S. exports and imports, we estimate letter of credit provision of $15-25 billion for exports and $6-10 billion for imports. Return to text

7. Still, letters of credit facilitate billions of dollars in international commerce and continue to play an important role in the creation of new trade relationships (Antràs and Foley (2015) and Benguria et al. (forthcoming)). Return to text

8. Recent research supports this concern. Federico, Hassan, and Rappoport (2023) show that Italian banks contracted lending after China's accession to the WTO through increases in loan losses from firms facing heightened export competition. Correa et al. (2024) find that during the 2018-2019 China-U.S. trade war, U.S. banks extending loans to firms facing trade uncertainty reduced their overall lending in a "wait and see" approach. Return to text

9. Another strand of the literature studies the reverse causal direction, namely the effect of financial shocks on international trade. For example, Ahn and Sarmiento (2019) and Niepmann and Schmidt-Eisenlohr (2017b) show that reductions in the supply of letters of credit reduce imports and exports. Return to text

Niepmann, Friederike, and Tim Schmidt-Eisenlohr (2026). "Trade Finance Activities of U.S. Banks: What the Data Can Tell Us," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, May 08, 2026, https://doi.org/10.17016/2380-7172.4052.

Disclaimer: FEDS Notes are articles in which Board staff offer their own views and present analysis on a range of topics in economics and finance. These articles are shorter and less technically oriented than FEDS Working Papers and IFDP papers.