February 24, 2021

How Should We Think about Full Employment in the Federal Reserve's Dual Mandate?

Governor Lael Brainard

At the Ec10, Principles of Economics, Lecture, Faculty of Arts and Sciences, Harvard University, Cambridge, Massachusetts (via webcast)

I want to thank Jason Furman and David Laibson for inviting me to join your economics class. I often found it difficult in introductory economics to connect the abstract concepts in the textbooks to the real-world issues I cared about. So the one message I hope you remember from today is that economics provides powerful tools to enable you to analyze and affect the issues that matter most to you.1

With jobs down by 10 million relative to pre-pandemic levels, one issue that matters fundamentally to all of us is achieving full employment. So today I want to talk about both the Federal Reserve's responsibilities with regard to full employment and different approaches to assessing where we are relative to that goal.

The belief that the federal government has a responsibility for full employment has its roots in the Great Depression. It was given statutory expression at the end of the Second World War when policymakers and legislators feared that the millions of American soldiers returning to the labor market would face Depression-era conditions.2 In the Employment Act of 1946, the Congress directed the federal government as a whole to pursue "conditions under which there will be afforded useful employment for those able, willing, and seeking work, and to promote maximum employment, production, and purchasing power."3

The postwar policy discussion raised important issues surrounding the definition and measurement of full employment. In 1950, the Review of Economics and Statistics published a symposium titled "How Much Unemployment?" which debated the accuracy of the Census Bureau's value for unemployment.4 Dr. Palmer was a critical contributor to the symposium. Palmer was a professor at Wharton, a fellow of the American Statistical Association, a worldwide expert on manpower and labor mobility, and a consultant with the Office of Statistical Standards.5 She argued that "a single figure of unemployment, regardless of how it is defined or derived, is inadequate as a basis for selection among [policy] programs. Inherent in the phenomena being measured are so many degrees and kinds of labor force activity that no single definition or classification can adequately summate them."6

With concerns about employment again on the rise, in 1976, Senator Hubert Humphrey joined with Congressman Augustus Hawkins to sponsor legislation promoting full employment.7 An amendment to the Federal Reserve Act in 1977 specifically assigned monetary policy responsibility for promoting "the goals of maximum employment, stable prices, and moderate long-term interest rates," commonly referred to as the dual mandate.8 This amendment was followed by the Humphrey-Hawkins Full Employment and Balanced Growth Act, passed in 1978, requiring that the Federal Reserve regularly report to the Congress on how monetary policy was supporting the goals of the act.9

Congressman Hawkins was a prominent advocate of full employment, emphasizing its importance not only for providing a job to every American seeking work, but also for reducing poverty, inequality, discrimination, and crime and improving the quality of life of all people.10 A congressman from southern California, Hawkins was one of the founders of the Congressional Black Caucus and played a major role in the drafting of the Civil Rights Act of 1964. He was also an undergraduate economics major.

Hawkins's views were influenced by his experience representing the Watts neighborhood in Los Angeles, where depression levels of joblessness persisted even when the nation overall was experiencing good times. He was also influenced by the work of economists such as Robert Browne and Bernard Anderson, which highlighted the persistent disparity between Black and white employment and the connection between elevated Black unemployment and economic challenges facing Black communities.11 Hawkins emphasized that "without genuine full employment it would be impossible to eliminate racial discrimination in the provision of job opportunities."12 The Humphrey-Hawkins Act noted that "increasing job opportunities and full employment would greatly contribute to the elimination of discrimination based upon sex, age, race, color, religion, national origin, handicap, or other improper factors."13

The centrality of achieving full employment for all Americans is as pressing today as it was in 1930, 1946, and 1977. The measurement challenges highlighted by Dr. Gladys Palmer and the racial disparities highlighted by Robert Browne and Bernard Anderson are just as relevant in today's economy. And the statutory dual mandate assigned to monetary policy has ensured an unwavering, strong focus on maximum employment as well as price stability at the Federal Reserve in research and measurement no less than policymaking.

The Federal Reserve recently concluded a review of our monetary policy framework, which included extensive outreach to a broad range of people over the course of 2019. In 14 Fed Listens events in communities around the country, we heard testimonials that would have sounded strikingly familiar to Congressman Hawkins. At a time when the national headline unemployment rate was at a multidecade low, community and labor representatives and educators noted "it's always a recession" in their communities.14 They challenged whether the overall economy could be characterized as at "full employment" while unemployment remained in the double digits in their communities.

Reflecting this input, and in light of persistently below-target inflation, low equilibrium interest rates, and low sensitivity of inflation to resource utilization, we made several important changes to the monetary policy framework. Two changes have particular relevance for the employment leg of the dual mandate.15 The new framework calls for monetary policy to seek to eliminate shortfalls of employment from its maximum level, in contrast to the previous approach that called for policy to minimize deviations when employment is too high as well as too low. The new framework also defines the maximum level of employment as a broad-based and inclusive goal assessed through a wide range of indicators.

So how should we assess this broad-based and inclusive concept of maximum employment? When discussing aggregate indicators about the labor market, people tend to focus on the headline U-3 measure of the unemployment rate.16 Although the unemployment rate is a very informative aggregate indicator, it provides only one narrow measure of where the labor market is relative to maximum employment. Recalling Gladys Palmer's dictum, I would not recommend relying on any single indicator, but rather consulting a variety of indicators that together provide a holistic picture of where we are relative to full employment.

So let us start by seeing what insights we gain by disaggregating the unemployment data into different groups of workers. The unemployment rate has improved very rapidly from its peak of 14.8 percent last April to 6.3 percent today. But this number is closer to 6.8 percent when taking into account a substantial number of people on temporary layoff, who have been misclassified as "employed but on unpaid absence" but instead should be counted as unemployed." 17

Disaggregating the overall unemployment rate reveals that workers in the lowest wage quartile face Depression-era rates of unemployment of around 23 percent.18 In part, this rate likely reflects the concentration of lower-wage jobs in service industries that are strongly reliant on in-person contact, or at least in-person work, while a larger proportion of higher-wage jobs are currently being performed remotely or with reduced levels of in-person contact.

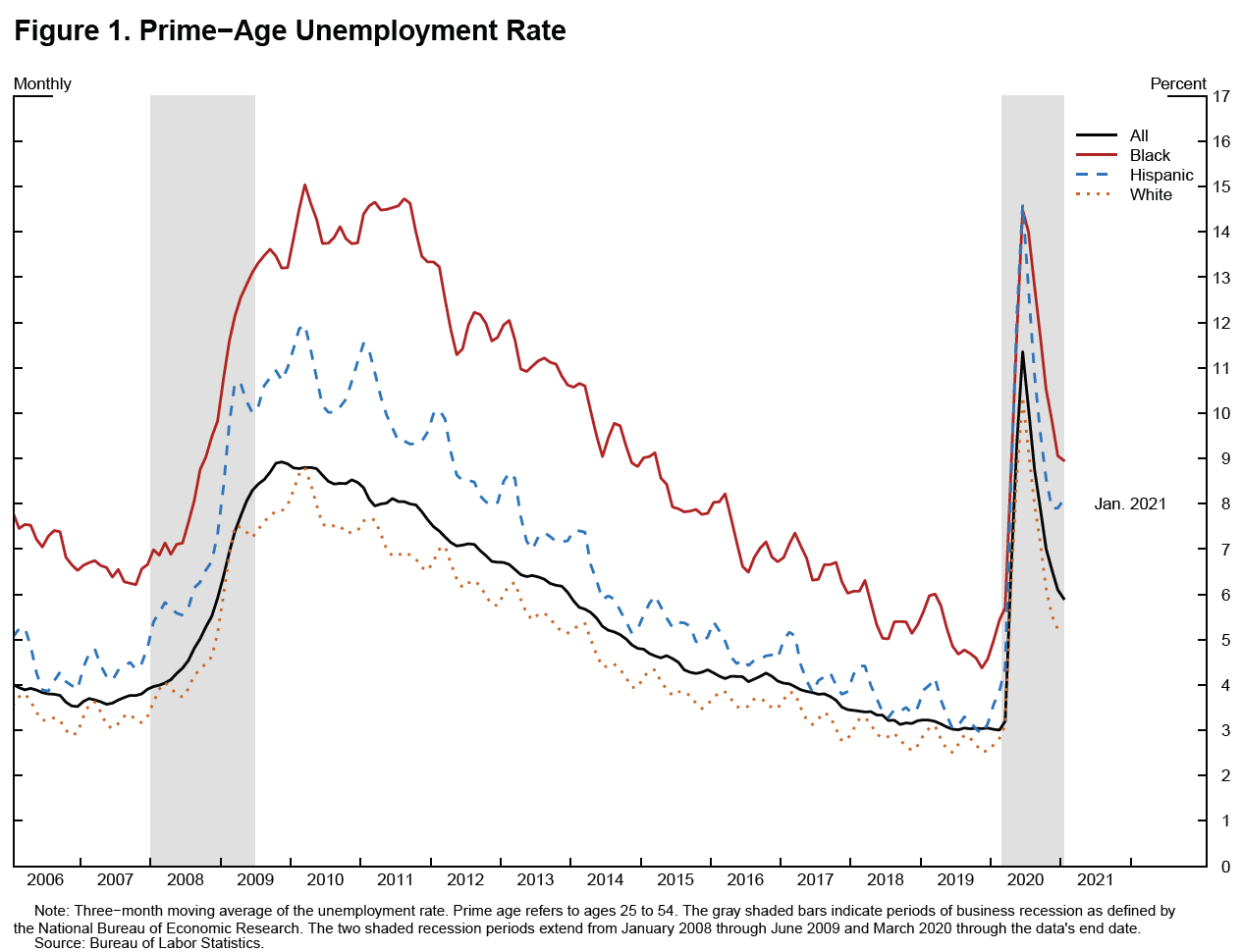

There is also important information in the disaggregation of unemployment by different racial and ethnic groups. Figure 1 shows the prime-age unemployment rate overall and on a disaggregated basis.19 There are notable persistent gaps between different racial and ethnic groups, and the sizes of those gaps tend to vary over the business cycle.

{kind=link}

For example, historically, the ratio of the Black unemployment rate to the white unemployment rate is around 2 for prime-age workers. On average, a 1 percentage point increase in the white unemployment rate is accompanied by a 2 percentage point increase in the Black unemployment rate. This gap narrows considerably the longer an expansion progresses. At the beginning of 2015, a time when many economists believed the overall unemployment rate had reached its "normal" rate, the gap between the Black and white prime-age unemployment rates stood just under 5 percentage points, roughly at its average level since 1972. By September 2019, that gap had reached a historical minimum of 1.7 percentage points, and the gap between the Hispanic and white prime-age unemployment rates had fallen to 0.3 percentage point.

The unemployment gaps between racial and ethnic groups widened again during the pandemic. Currently, for prime-age individuals, the gaps between the white unemployment rate and the Black and Hispanic unemployment rates are roughly 4 percentage points and 3 percentage points, respectively.

The unemployment rate obscures important information about people leaving and entering the workforce. Each adult in the population is classified as employed, unemployed, or not in the labor force. The unemployment rate is the number of individuals who are not currently working but are actively looking for a job, divided by the size of the labor force, which includes only those people who are either working or actively seeking work:

$$ U = {Unemployed \over Labor Force}.$$

Changes in labor force participation contain important information about the strength of the labor market that is not captured in the unemployment rate. The labor force participation rate (LFPR) is the number of individuals who are either working or are seeking work, divided by the working-age population:

$$ LFPR = {Labor Force \over Population}.$$

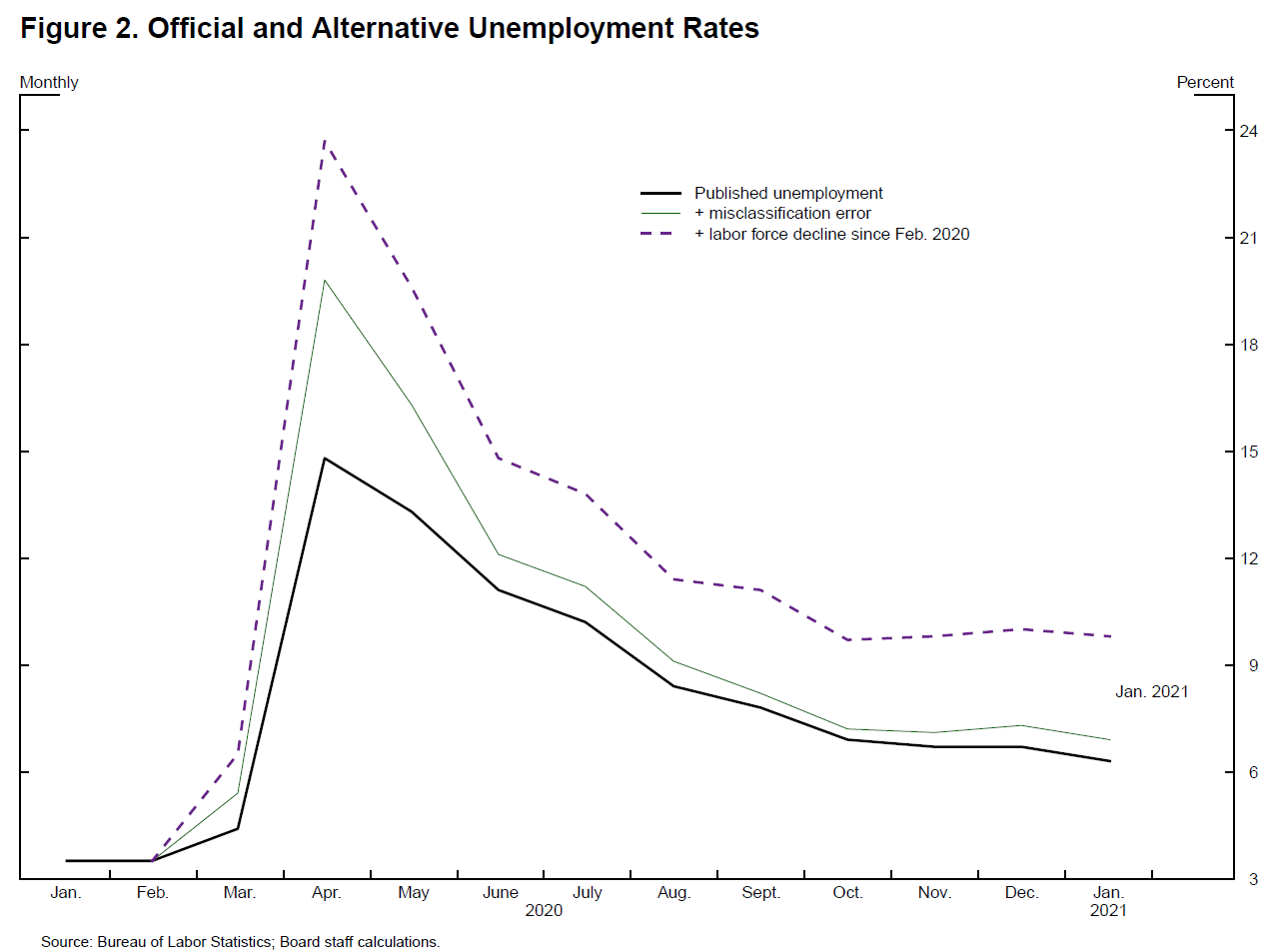

When we take into consideration the more than 4 million workers who have left the labor force since the pandemic started, as well as misclassification, the unemployment rate is close to 10 percent currently—much higher than the headline unemployment rate of 6.3 percent—and similar to the peak unemployment rate following the financial crisis. This is shown in Figure 2.

{kind=link}

A decline in participation by prime-age women is an important contributor to the overall participation decline. Some portion of the decline reflects the increase in caregiving work at home with the shutdown of schools and daycare due to COVID-19. On average over the period from November 2020 to January 2021, the fraction of prime-age respondents with children aged 6 to 17 who were out of the labor force for caregiving was about 14 percent, up 1-3/4 percentage points from a year earlier. For mothers, the fraction who were out of the labor force for caregiving was 22.8 percent, an increase of 2.4 percentage points from a year earlier, while for fathers the fraction was 2.2 percent, an increase of about 0.6 percentage point.20 If not soon reversed, the decline in the participation rate for prime‑age women could have longer-term implications for household incomes and potential growth.21

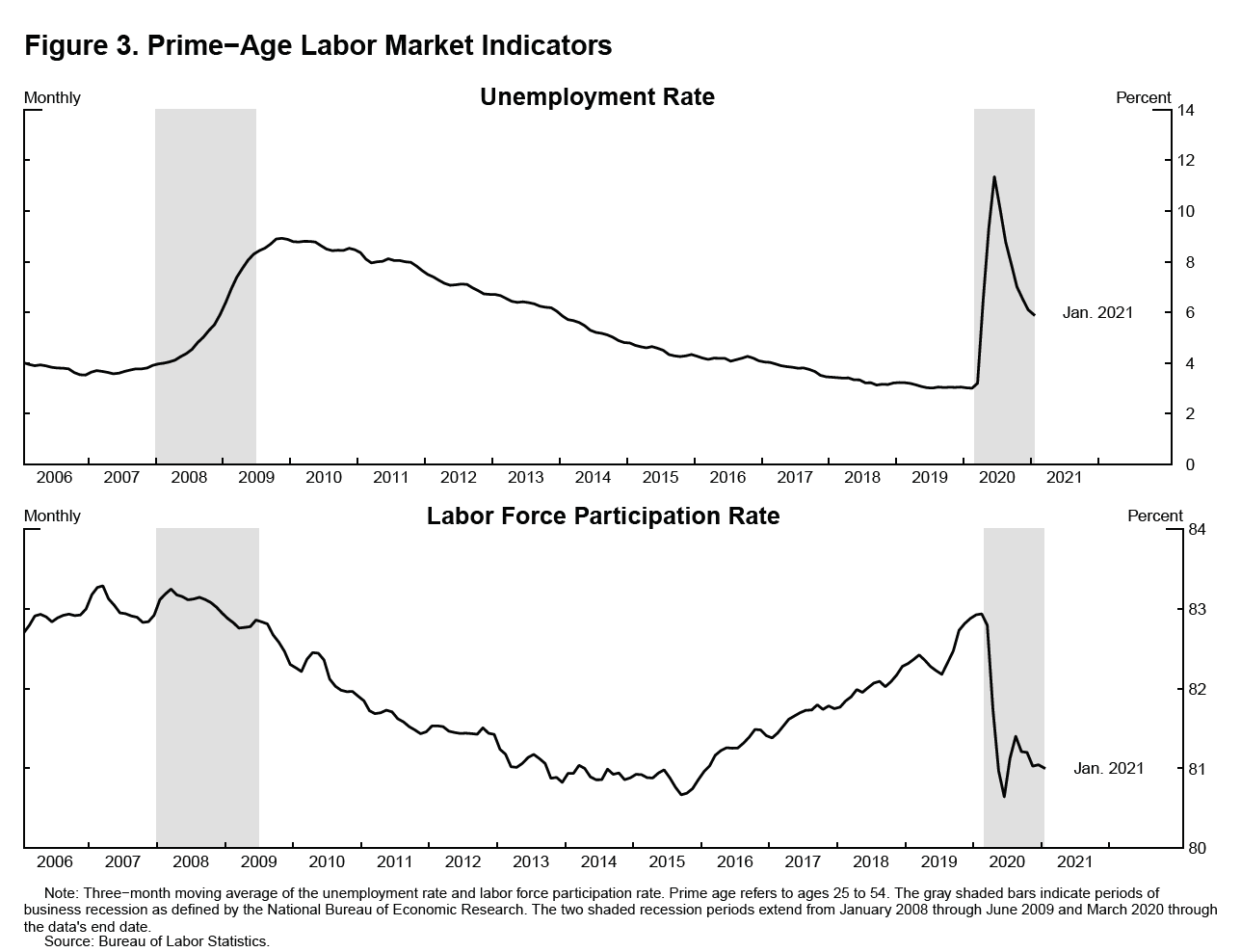

While there are long-term structural trends in participation, such as population aging, there are also cyclical dynamics that are important for our assessment of maximum employment. The two panels in figure 3 show prime-age unemployment and labor force participation over the previous recession and recovery. Following the onset of the global financial crisis, as the number of unemployed people was rising, the size of the labor force was also contracting, pushing the numerator of the unemployment rate up and the denominator down. When the unemployment rate started to decline at the end of 2010, this decline in part reflected unemployed people dropping out of the labor force through 2013. As the labor market healed further, prime-age LFPR leveled out and started to increase at the end of 2015. The subsequent seemingly modest decline in the unemployment rate from 4.3 at the end of 2015 to 3 percent at the end of 2019 was much more significant, taking into account that more than 3-1/2 million prime-age workers joined or rejoined the labor force during that period.

{kind=link}

This brings me to figure 4 and the employment-to-population (EPOP) ratio, which is the number of individuals employed divided by the working-age population:

{kind=link}

$$ EPOP = {Employed \over Population}.$$

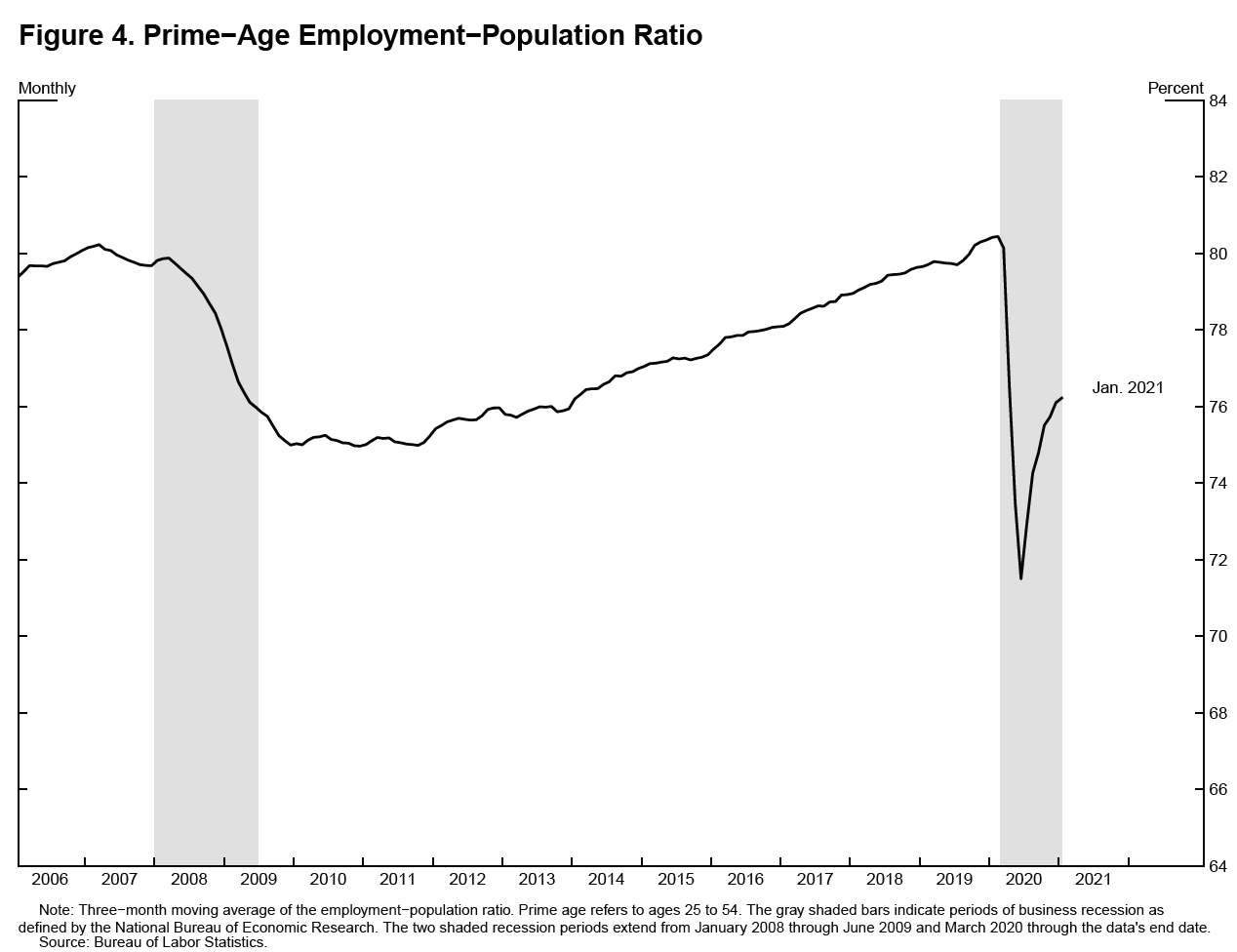

The EPOP ratio synthesizes the information contained in the unemployment rate and LFPR. For instance, as you can see in figure 4, a decline in participation almost entirely offset the decline in unemployment in 2010 and 2011, leaving the prime-age EPOP ratio essentially flat at 75 percent. The EPOP ratio then improved steadily over the subsequent seven years, moving up to 80.4 percent in late 2019.

As the effects of the virus and measures to combat it took hold of the economy, the EPOP ratio plummeted last April, and, after staging a sharp but partial recovery, improvements in the prime-age EPOP ratio have moderated in recent months. A glance back at figure 3 shows that the reductions in employment last spring were accompanied by many prime-age workers leaving the labor force, and the participation rate among prime-age workers has declined further since last May. The prime-age EPOP ratio currently stands at 76.4 percent, well below the 80 percent level that was reached during each of the past two expansions.

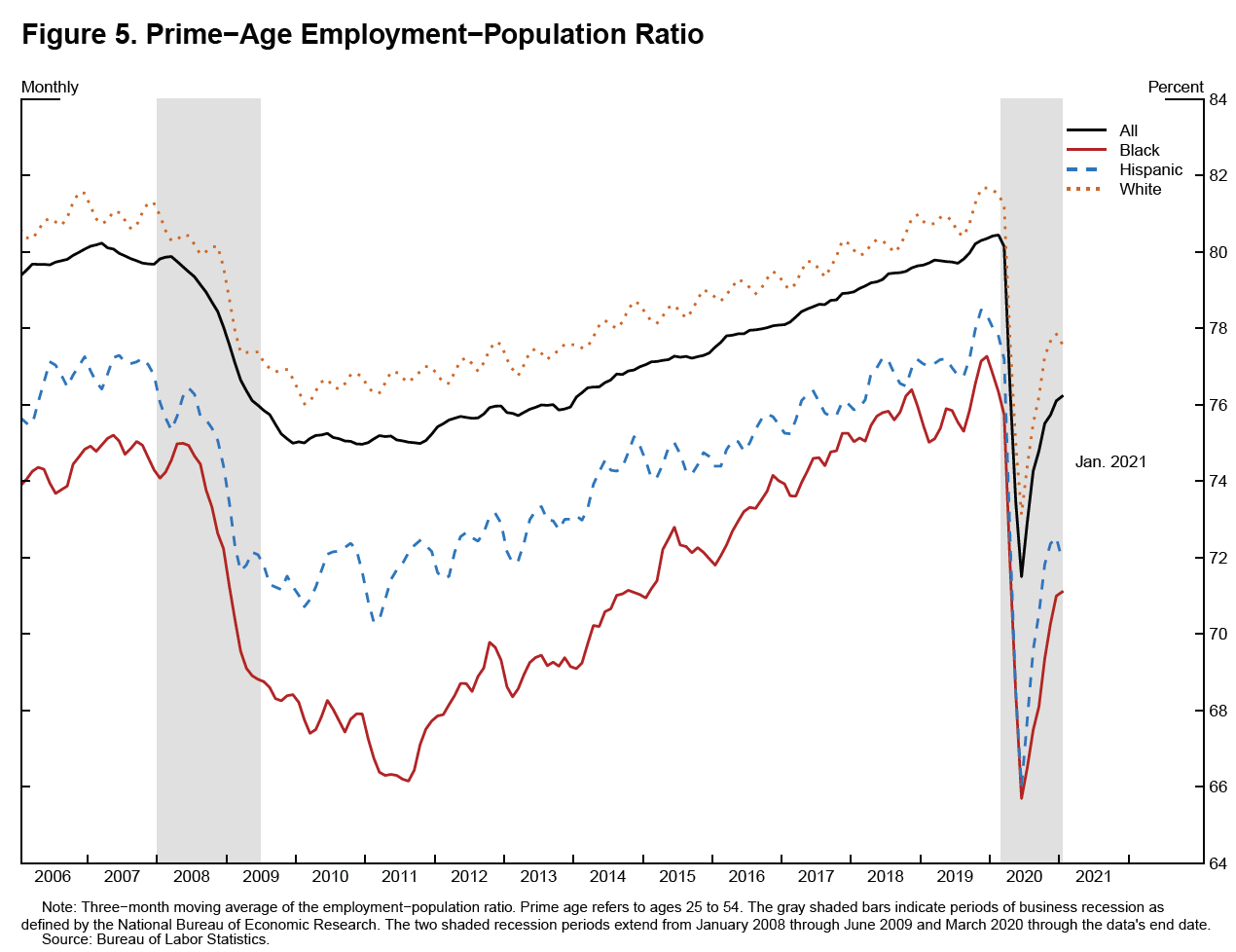

Figure 5 shows the patterns in the EPOP ratio for prime-age workers in different racial and ethnic groups.22 Following the Global Financial Crisis, the Black–white EPOP gap opened to more than 10 percentage points in mid-2011 before shrinking to under 5 percentage points as labor markets tightened further during 2018 and 2019. In contrast, the Hispanic–white EPOP gap was smaller than the Black–white gap, and it fluctuated in a much narrower range over the business cycle.

{kind=link}

During the pandemic, labor market performance as shown by the EPOP measure has been fairly similar for Black and Hispanic prime-age workers and markedly worse than for white workers. Research indicates that Black and Hispanic workers are overrepresented in industries particularly hard hit by the pandemic, such as hotels and restaurants.23 It also shows that Black and Hispanic workers are overrepresented in essential industries at lower pay, and that they are significantly less likely to be able to telework.24

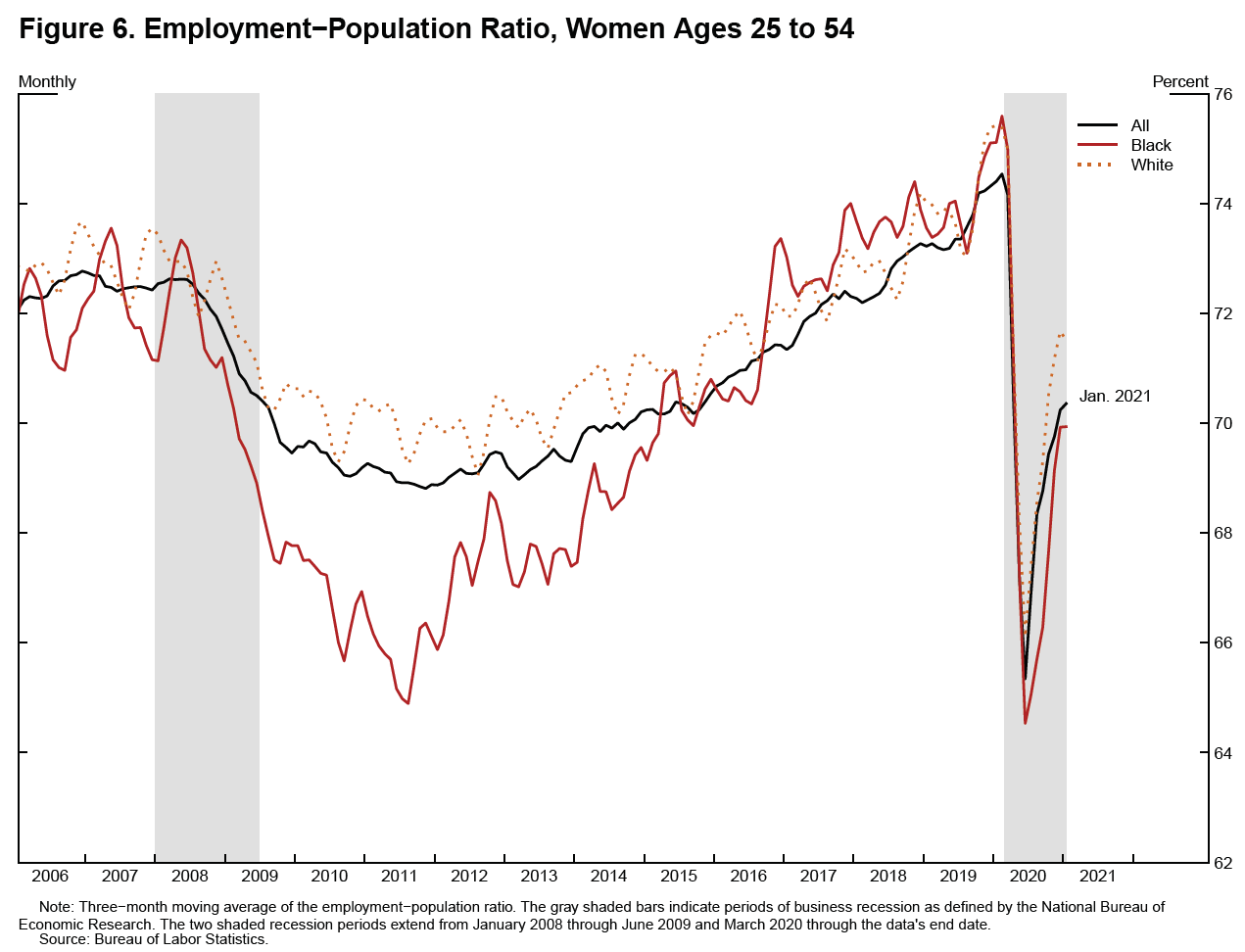

Figure 6 shows one more EPOP snapshot, this time for prime-age women overall, as well as for Black and white subgroups. Following the financial crisis, a gap opened up between the prime-age EPOP ratios for Black and white women. That gap closed in 2015, and employment for both groups surged over the next four years. Between January 2015 and February 2020, the EPOP ratios for white and Black prime-age women each increased roughly 5 percentage points, reaching historical highs in the months just before the onset of the pandemic. As the pandemic took hold in the subsequent months, once again a gap opened up between the EPOP ratios for white and Black women, though the current gap of roughly 2 percentage points is not as large as in the previous downturn.

{kind=link}

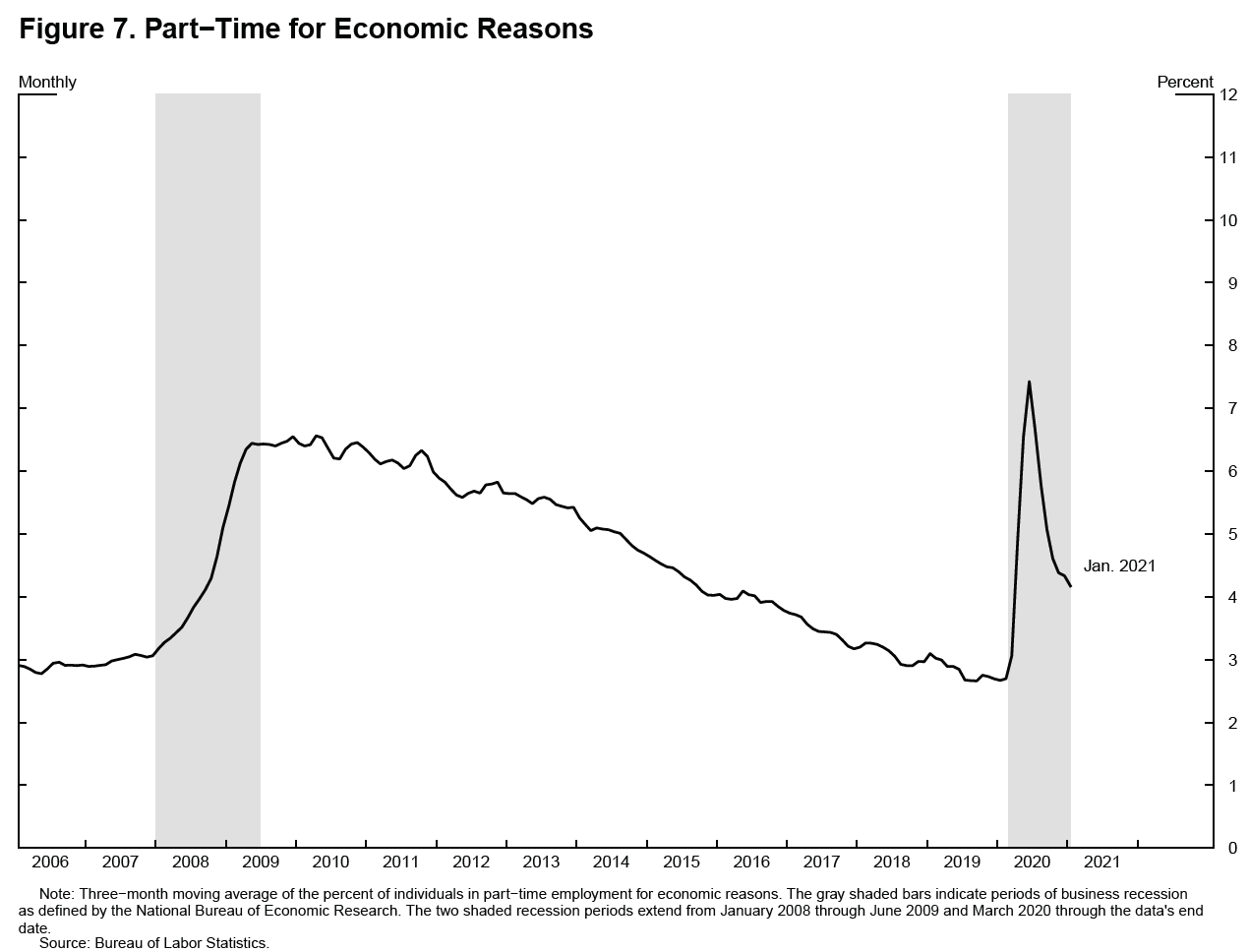

While the EPOP ratio is a strong indicator of the extensive margin in the labor market, or how many people are working, there is also important information in the intensive margin—that is, how much work each person is doing. The part-time for economic reasons (PTER) indicator shown in figure 7 measures those who are working part time because they are unable to find a full-time job or whose hours have been reduced and who would prefer full-time employment.25 This indicator is an important measure of labor market slack, which tends to jump rapidly during recessions and improve more slowly than headline unemployment during recoveries. PTER jumped during the financial crisis as workers who were unable to secure full-time employment moved to part-time work, accounting for more than half of the increase in involuntary part-time work during 2008.26

{kind=link}

Today there are 6.0 million people working part time who would prefer full-time work, up 1.6 million relative to the pre-COVID level. The Bureau of Labor Statistics has six alternative measures of labor underutilization, the most expansive of which is the U-6 measures, which adds to the headline unemployment rate those employed part time for economic reasons, along with all persons marginally attached to the labor force as a percentage of the civilian labor force. The U-6 measure stood at 11.1 percent in January.27

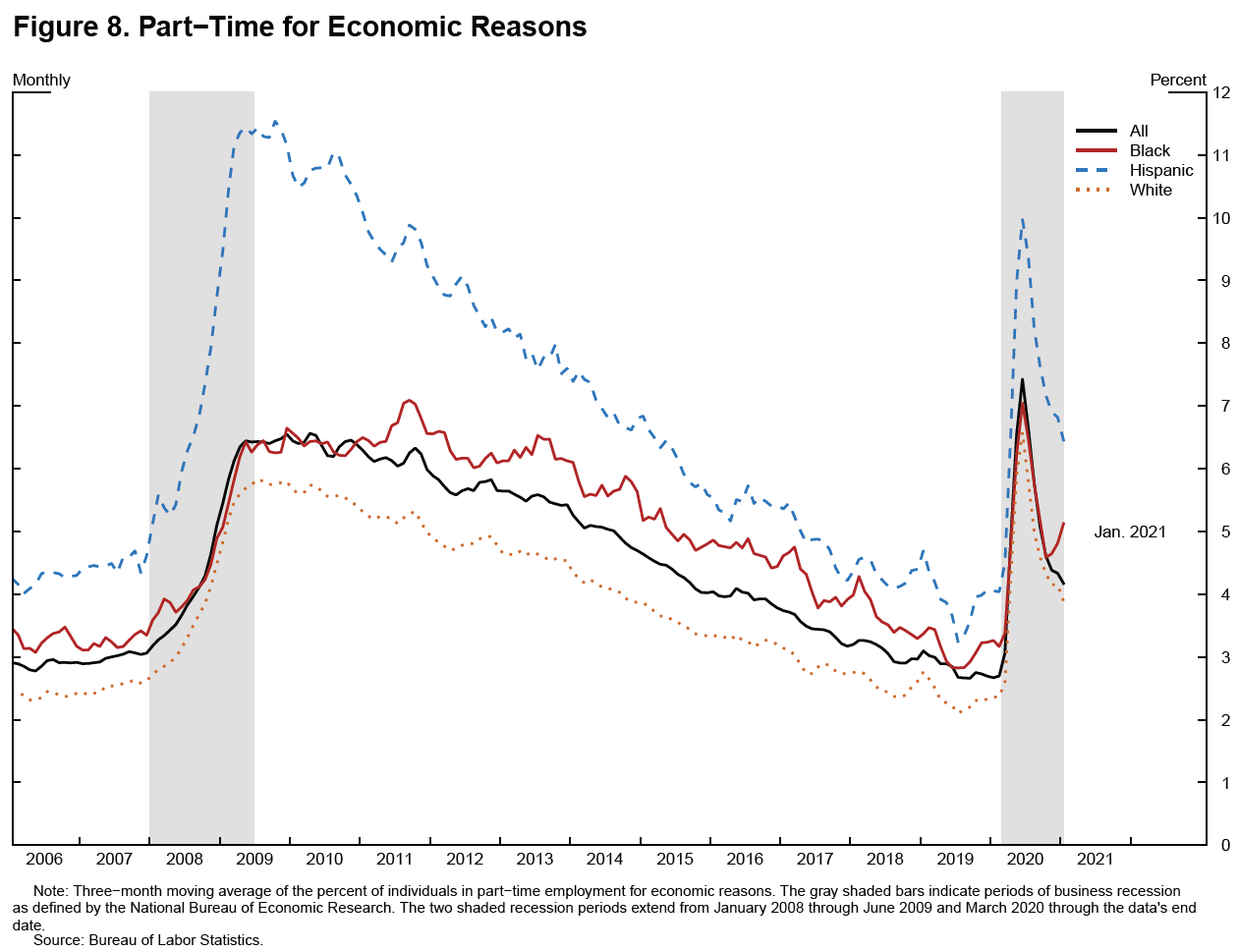

Figure 8 shows the large amount of cyclical variation across PTER for several racial and ethnic groups. The incidence of involuntary part-time work was especially notable for Hispanic workers at the trough of the Great Recession, nearing 12 percent of employment and almost double its rate before the recession. This gap between Hispanic and white PTER narrowed substantially during the recovery and fell to just above 1 percentage point in the summer of 2019. Research indicates that gaps in involuntary part-time employment rates remain for Blacks, as well as Hispanics, relative to whites after controlling for age, education, marital status, and state of residence, although education and occupation can explain a portion of the gap for Hispanics.28

{kind=link}

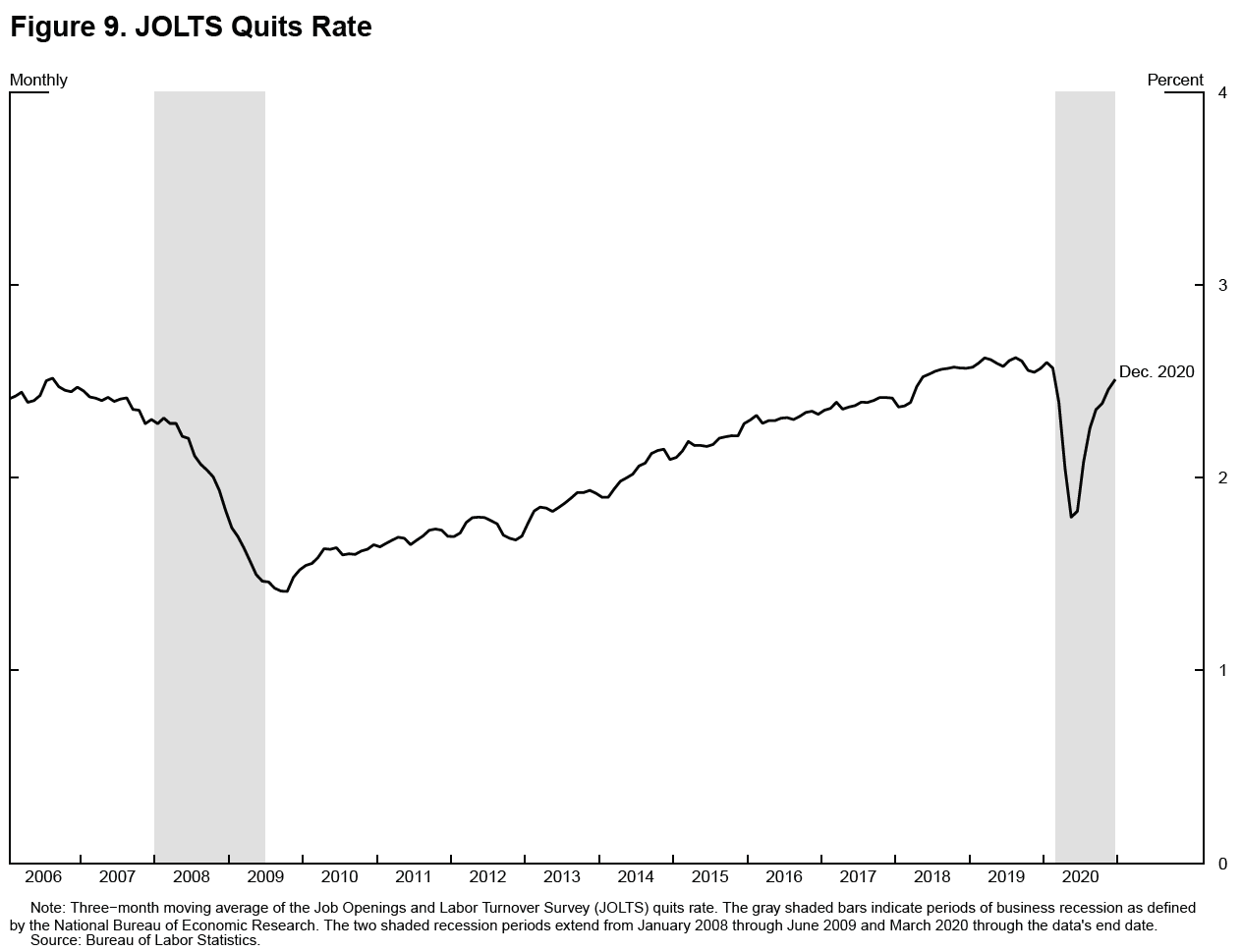

Before concluding, I would like to point to two other labor market indicators that provide useful evidence of the extent of labor market slack. The quits rate, shown in figure 9, is a measure of voluntary separations that provides information about how confident people are that they will be successful in finding a new job they prefer and, relatedly, of how aggressively firms are pursuing talent.29 Research indicates that the quits rate and wage growth are highly correlated, suggesting that these voluntary job-to-job transitions reflect individuals moving up a "job ladder" to higher-paying jobs.30 The quits rate fell rapidly during the 2008 recession as workers' options became more limited, then recovered slowly, only surpassing its pre–financial crisis level of roughly 2.5 percent in 2018. In contrast, the bounceback from the pandemic trough has been much more robust, with quits already reaching 2.6 percent in December. As undergraduates, the quits rate may soon become relevant to you, as research indicates that job-to-job transitions are most frequent for young workers and that this measure has trended down in recent decades.31

{kind=link}

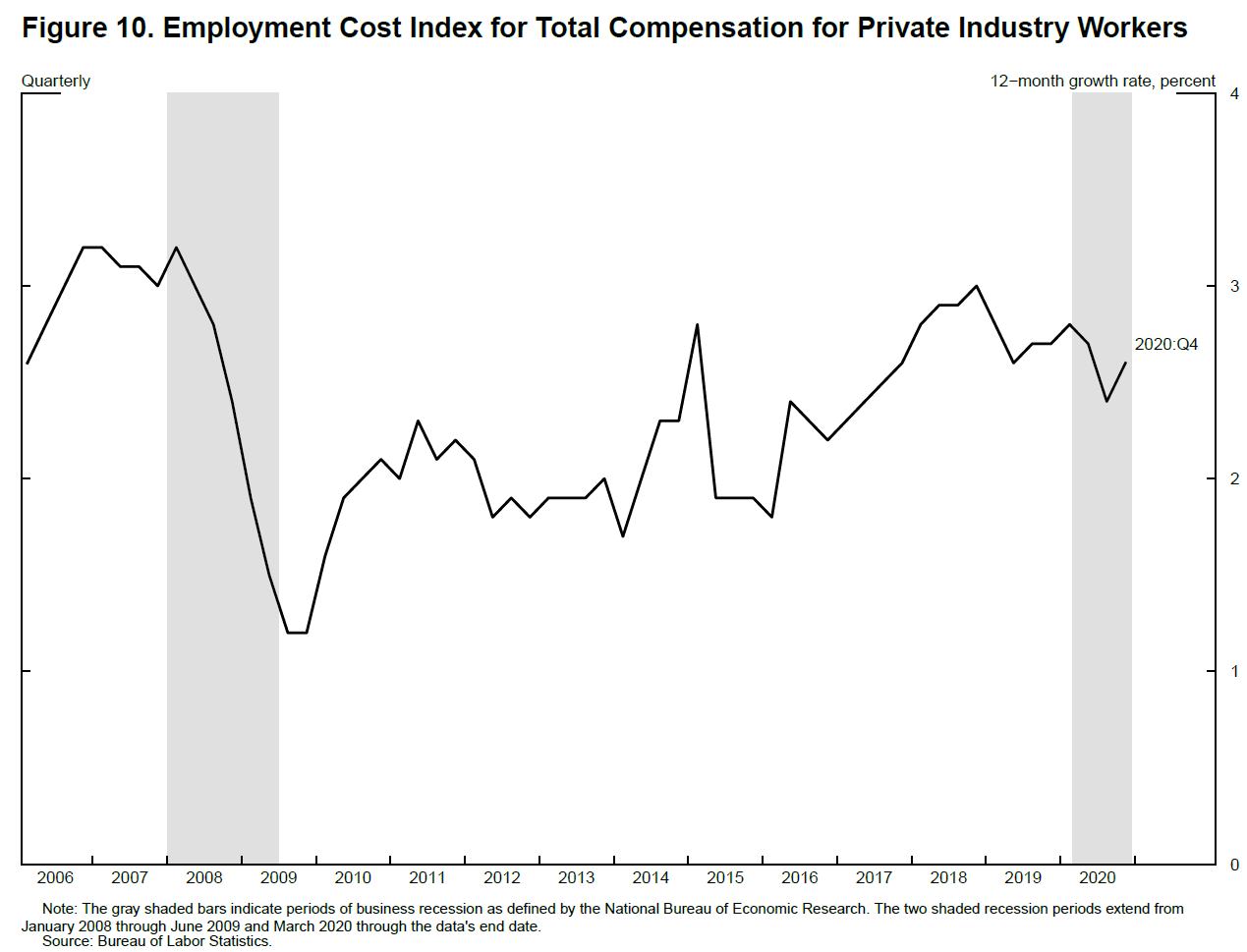

Finally, measures of compensation are closely monitored for evidence on labor market slack. Figure 10 shows the 12-month growth rate of the employment cost index for total compensation for private industry workers (ECI). Just as quits fell during the Great Recession, so did the ECI. About two years after the onset of the financial crisis, the ECI moved up slightly in 2010 and then remained essentially flat at an annual growth rate of 2 percent over a five-year period between 2010 and 2015. There was a pickup of the ECI at the end of 2015, which coincided with the turning point in the prime-age LFPR. Even so, the growth rate of the ECI did not return to the levels experienced before 2008.

{kind=link}

Unlike the other indicators I have discussed, the pandemic appears to have made fairly little imprint on the ECI. The ECI declined slightly over the second and third quarters of 2020 and moved up in the fourth quarter. It is difficult to draw any firm conclusions from these developments; while the ECI is not as susceptible to composition effects as some other measures, smaller composition effects are still possible.32

So, what conclusions can we draw from this high-level overview of a variety of labor market indicators, their current readings, and their performance in the previous expansion? First, the headline unemployment rate by itself can obscure important dimensions of labor market slack, so it is important to heed Dr. Palmer's dictum and consult a broad set of aggregated and disaggregated measures. Second, groups that have faced the greatest challenges often make important labor market gains late in an expansion, consistent with Augustus Hawkins's emphasis on the importance of full employment for all Americans.

So where does this leave us today? Jobs are still down by 10 million relative to pre-COVID levels, and COVID has disproportionately harmed certain sectors, groups of workers, businesses, and states and localities, leading to a K-shaped recovery. The fiscal support that is enacted and expected will provide assistance to vulnerable households, small businesses, and localities and a significant boost to activity when vaccinations are sufficiently widespread to support a reopening of in-person services. Monetary policy will continue to provide support by keeping borrowing costs for households and businesses low.

The assessment of shortfalls from broad-based and inclusive maximum employment will be a critical guidepost for monetary policy, alongside indicators of realized and expected inflation. The Federal Open Market Committee has said it expects the policy rate to remain in the current target range until labor market conditions have reached levels consistent with the Committee's assessments of maximum employment and inflation has risen to 2 percent and is on track to moderately exceed 2 percent for some time. It has noted that asset purchases will continue at least at the current pace until substantial further progress has been made toward the maximum-employment and inflation goals.

In assessing substantial further progress, I will be looking for sustained improvements in realized and expected inflation and examining a range of indicators to assess shortfalls from maximum employment. I will be looking for indicators that show the healing in the labor market is broad based, rather than focusing on the narrow aggregate U-3 unemployment rate, in light of the significant decline in labor force participation since the spread of COVID and the extremely elevated unemployment rate for workers in the lowest wage quartile.

For nearly four decades, monetary policy was guided by a strong presumption that accommodation should be reduced preemptively when the unemployment rate nears its normal rate in anticipation that high inflation would otherwise soon follow. But changes in economic relationships over the past decade have led trend inflation to run persistently somewhat below target and inflation to be relatively insensitive to resource utilization. With these changes, our new monetary policy framework recognizes that removing accommodation preemptively as headline unemployment reaches low levels in anticipation of inflationary pressures that may not materialize may result in an unwarranted loss of opportunity for many Americans. It may curtail progress for racial and ethnic groups that have faced systemic challenges in the labor force, which is particularly salient in light of recent research indicating that additional labor market tightening is especially beneficial for these groups when it occurs in already tight labor markets, compared with earlier in the labor market cycle.33 Instead, the shortfalls approach means that the labor market will be able to continue to improve absent high inflationary pressures or an unmooring of inflation expectations to the upside.

Inflation remains very low, and although various measures of inflation expectations have picked up recently, they remain within their recent historical ranges. PCE (personal consumption expenditures) inflation may temporarily rise to or above 2 percent on a 12-month basis in a few months when the low March and April price readings from last year fall out of the 12-month calculation, and we could see transitory inflationary pressures reflecting imbalances if there is a surge of demand that outstrips supply in certain sectors when the economy opens back up. While I will carefully monitor inflation expectations, it will be important to see a sustained improvement in actual inflation to meet our average inflation goal.

Today the economy remains far from our goals in terms of both employment and inflation, and it will take some time to achieve substantial further progress. I look forward to the time when this K-shaped recovery becomes a broad-based and inclusive recovery and when vaccinations are widespread, the services sector springs back to life, and all Americans enjoy the benefits of full employment. I cannot think of a more meaningful time to be studying economics or a more important time to be thinking about the different ways to assess our shared goal of full employment.

1. I am grateful to Kurt Lewis, Mark Carlson, Christopher Nekarda, Edward Nelson, Ivan Vidangos, and Nicholas Zevanove of the Federal Reserve Board for their assistance in preparing these materials. These remarks represent my own views, which do not necessarily represent those of the Federal Reserve Board or the Federal Open Market Committee. Return to text

2. From 1930 to 1940, the unemployment rate averaged 18 percent by one estimate. See G.J. Santoni (1986), "The Employment Act of 1946: Some History Notes," Review (Federal Reserve Bank of St. Louis), vol. 68 (November), pp. 5–16. Return to text

3. The language of the act (quoted text in section 2) is available through FRASER on the Federal Reserve Bank of St. Louis website at https://fraser.stlouisfed.org/title/employment-act-1946-1099. In 1945, the staff at the Federal Reserve Board wrote a series of Postwar Economic Studies on the economic effects of demobilization. The first study notes that "jobs are the main channel through which national welfare reaches the individual." See Emanuel Alexandrovich Goldenweiser (1945), "Jobs," in Frank R. Garfield, Emanuel Alexandrovich Goldenweiser, Everett Einar Hagen, and Board of Governors of the Federal Reserve System, eds., Jobs, Production, and Living Standards (Baltimore: Waverly Press), p. 1. Return to text

4. For an introduction to the symposium, see Seymour E. Harris (1950), "Introduction," Review of Economics and Statistics, vol. 32 (February), p. 49. Return to text

5. See Gertrude Bancroft McNally (1967), "Gladys L. Palmer, 1895–1967," American Statistician, vol. 21 (December), p. 35. Return to text

6. See Gladys L. Palmer (1950), "Unemployment Statistics as a Basis for Employment Policy," Review of Economics and Statistics, vol. 32 (February), pp. 70–74 (quoted text on p. 70). Return to text

7. For a discussion of the evolution of the Federal Reserve's statutory responsibilities, see Ben S. Bernanke (2013), "A Century of U.S. Central Banking: Goals, Frameworks, Accountability," speech delivered at "The First 100 Years of the Federal Reserve: The Policy Record, Lessons Learned, and Prospects for the Future," a conference sponsored by the National Bureau of Economic Research, Cambridge, Mass., July 10. Return to text

8. As noted by Frederic Mishkin, "Because long-term interest rates can remain low only in a stable macroeconomic environment, these goals are often referred to as the dual mandate; that is, the Federal Reserve seeks to promote the two coequal objectives of maximum employment and price stability." See Frederic S. Mishkin (2007) "Monetary Policy and the Dual Mandate," speech delivered at Bridgewater College, Bridgewater, Va., April 10 (quoted text in paragraph 3). Return to text

9. A few other central banks have an explicit employment mandate that has the same weight as their price-stability mandate, such as the Reserve Bank of Australia and the Reserve Bank of New Zealand. For most central banks, price stability is the single objective of monetary policy (Bank of Canada, Riksbank, and Bank of Japan) or the priority objective (for example, European Central Bank and Bank of England). Economic research suggests that inflation outcomes have been as good, or better, in the United States compared with jurisdictions in which employment either is not a monetary policy objective or is subordinate to price stability. See Eric S. Rosengren (2014), "Should Full Employment Be a Mandate for Central Banks?" Journal of Money, Credit and Banking, vol. 46, suppl. 2 (October), pp. 169–82. Return to text

10. See Helen Lachs Ginsburg (2012), "Historical Amnesia: The Humphrey-Hawkins Act, Full Employment and Employment as a Right," Review of Black Political Economy, vol. 39 (October), pp.121–36. Return to text

11. See Bernard E. Anderson (2008), "Robert Browne and Full Employment," Review of Black Political Economy, vol. 35 (January), pp. 91–101. Return to text

12. See Augustus F. Hawkins (1975), "Full Employment to Meet America's Needs," Challenge, vol. 18 (November/December), pp. 20–28. Return to text

13. The complete original language of the act (quoted text in section 2B (4)) is available through FRASER on the Federal Reserve Bank of St. Louis website at https://fraser.stlouisfed.org/title/full-employment-balanced-growth-act-humphrey-hawkins-act-1034. Return to text

14. See Board of Governors of the Federal Reserve System (2020), Fed Listens: Perspectives from the Public (PDF) (Washington: Board of Governors, June). Return to text

15. See Lael Brainard (2021), "Full Employment in the New Monetary Policy Framework," speech delivered at the Inaugural Mike McCracken Lecture on Full Employment, sponsored by the Canadian Association for Business Economics (via webcast), January 13. Return to text

16. This measure is the number of unemployed persons divided by the size of the labor force. People in both categories must be 16 years of age or older. Return to text

17. Since March 2020, the Bureau of Labor Statistics (BLS) has instructed its household survey interviewers to classify employed persons who are absent from work due to temporary, pandemic-related business closures or cutbacks as being unemployed on temporary layoff. During this period, however, some workers affected by the pandemic who should have been classified as unemployed on temporary layoff were instead misclassified as employed but not at work. Each month, the BLS provides an estimate of the likely size of this effect on the unemployment rate. More information is available on the BLS website at https://www.bls.gov/covid19/employment-situation-covid19-faq-january-2021.htm. Return to text

18. For more information on this analysis, see the box "Disparities in Job Loss during the Pandemic" in Board of Governors of the Federal Reserve System (2021), Monetary Policy Report (Washington: Board of Governors, February), pp. 12–14. Return to text

19. Prime age refers to ages 25 to 54. I focus on this age range because of how important those working years are for individuals' overall careers and because labor market metrics calculated over workers in this age range help control for the aging of the population. Return to text

20. The percentages are staff calculations based on the microdata from the January Current Population Survey. For more information on this analysis, see the box "Disparities in Job Loss during the Pandemic" in Board of Governors, Monetary Policy Report, pp. 12–14, in note 19. Return to text

21. See Olivia Lofton, Nicolas Petrosky-Nadeau, and Lily Seitelman (2021) "Parents in a Pandemic Labor Market," Federal Reserve Bank of San Francisco Working Paper 2021-04. (February) (2020), and Lael Brainard, "Achieving a Broad-Based and Inclusive Recovery," speech delivered at "Post-COVID—Policy Challenges for the Global Economy," Society of Professional Economists Annual Online Conference, October 21. Return to text

22. The Bureau of Labor Statistics makes disaggregated EPOP data from the Current Population Survey available through online tools found on the bureau's website at https://www.bls.gov/data. Return to text

23. See Connor Maxwell and Danyelle Solomon (2020), "The Economic Fallout of the Coronavirus for People of Color," Center for American Progress, April 14. Return to text

24. See Hye Jin Rho, Hayley Brown, and Shawn Fremstad (2020), A Basic Demographic Profile of Workers in Frontline Industries (PDF) (Washington: Center for Economic and Policy Research, April). Return to text

25. According to the Bureau of Labor Statistics, this category includes people who gave an economic reason when asked why they worked 1 to 34 hours during the survey's reference week. Their usual hours of work may be either full or part time. Economic reasons include the following: slack work, unfavorable business conditions, inability to find full-time work, and seasonal declines in demand. People who usually work part time and were at work part time during the reference week must indicate that they want and are available for full-time work to be classified as part time for economic reasons. Return to text

26. For more information, see Tomaz Cajner, Dennis Mawhirter, Christopher Nekarda, and David Ratner (2014), "Why Is Involuntary Part-Time Work Elevated?" FEDS Notes (Washington: Board of Governors of the Federal Reserve System, April 14). Return to text

27. Persons marginally attached to the labor force are those who currently are neither working nor looking for work but indicate that they want and are available for a job and have looked for work sometime in the past 12 months. Return to text

28. See Tomaz Cajner, Tyler Radler, David Ratner, and Ivan Vidangos (2017), "Racial Gaps in Labor Market Outcomes in the Last Four Decades and over the Business Cycle (PDF)," Finance and Economics Discussion Series 2017-071 (Washington: Board of Governors of the Federal Reserve System, June). Return to text

29. See the Job Openings and Labor Turnover Survey, which can be found on the Bureau of Labor Statistics website at https://www.bls.gov/jlt/home.htm. Return to text

30. See R. Jason Faberman and Alejandro Justiniano (2015), "Job Switching and Wage Growth," Chicago Fed Letter 337 (Chicago: Federal Reserve Bank of Chicago). Return to text

31. For evidence that job-to-job transition is utilized most when young, and that job dynamism for the young has declined, see Canyon Bosler and Nicolas Petrosky-Nadeau (2016), "Job-to-Job Transitions in an Evolving Labor Market," FRBSF Economic Letter 2016-34 (San Francisco: Federal Reserve Bank of San Francisco, November). Return to text

32. For example, the ECI data are assembled at an industry-occupation level of granularity. If at the outset of the pandemic, firms in a particular industry laid off their newest, lowest-paid staff in a particular occupational category first, the compositional change could lead compensation in that industry and occupation to increase on average. Return to text

33. See Stephanie R. Aaronson, Mary C. Daly, William L. Wascher, and David W. Wilcox (2019), "Okun Revisited: Who Benefits Most from a Strong Economy? (PDF)" Brookings Papers on Economic Activity, Spring, pp. 333–75. Return to text