January 16, 2026

Economic Outlook and Monetary Policy Implementation

Vice Chair Philip N. Jefferson

At the American Institute for Economic Research, Shadow Open Market Committee, and Florida Atlantic University Conference, Boca Raton, Florida

Thank you, President Hasner, for the kind introduction. It is an honor to speak at Florida Atlantic University, and I am glad to have the chance to talk with those here from the American Institute for Economic Research and the Shadow Open Market Committee.

{kind=link}

I especially appreciate the opportunity to discuss my economic outlook at the start of the new year. It is a task made considerably easier with the gradual return of federal government data, which was disrupted by last year's lapse in funding. The lack of data reinforced two long-held beliefs for me. One, how grateful I am for the dedicated service of the statistical agencies to keep policymakers, businesses, and the public informed about the state of the economy. And, two, how important it is to have access to an array of data beyond what those agencies provide. That includes data produced by the Federal Reserve System, state governments, and a wide variety of private-sector sources. All of those data sources inform my view of the economy and help me make monetary policy decisions.

Today, I will start by sharing my outlook for the economy at the start of 2026. Next, I will discuss the implications of that outlook for the path of monetary policy. And, finally, I will discuss some recent developments in monetary policy implementation, which I know is of interest to many of you in this room. As a reminder, these views are my own and are not necessarily those of my colleagues.

{kind=link}

Economic Outlook

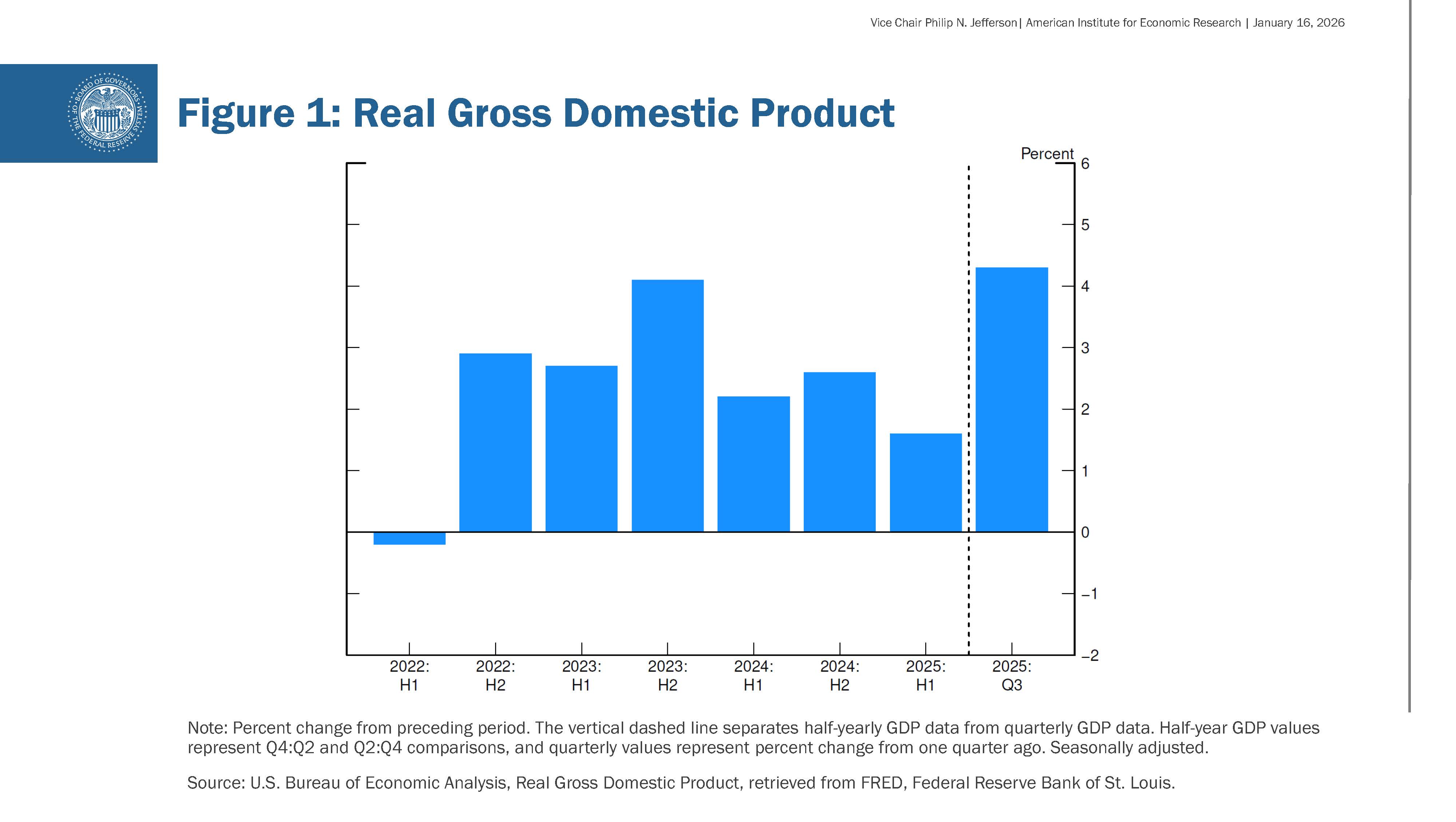

I am starting 2026 with a cautiously optimistic point of view. Conditions in the labor market appear to be stabilizing, and I see the economy as well positioned to continue to grow while inflation returns to a pathway toward our 2 percent objective. The most recent data indicate that economic activity has remained strong. In the third quarter of 2025, gross domestic product rose at an annual rate of 4.3 percent. As you can see in figure 1, that was a sharp acceleration from the first half of last year, mostly reflecting strong consumer spending and an upward swing in net exports, which can be volatile. Business investment grew at a solid rate in the third quarter, while residential investment continued to be soft. Fourth-quarter growth is likely to be restrained due to the effects of the government shutdown. Still, excluding those effects, I see the economy expanding at a solid pace of about 2 percent in the near term.

{kind=link}

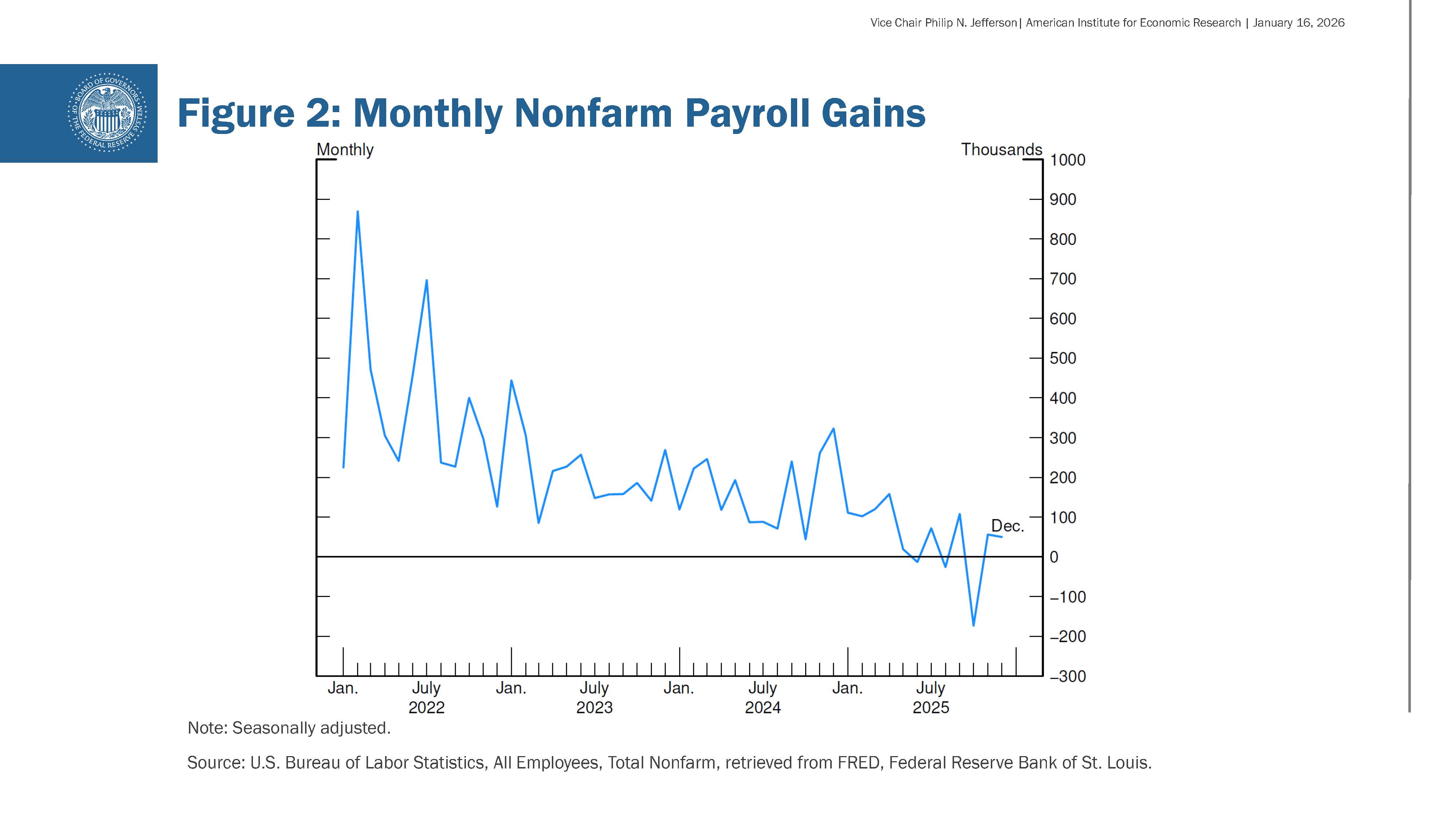

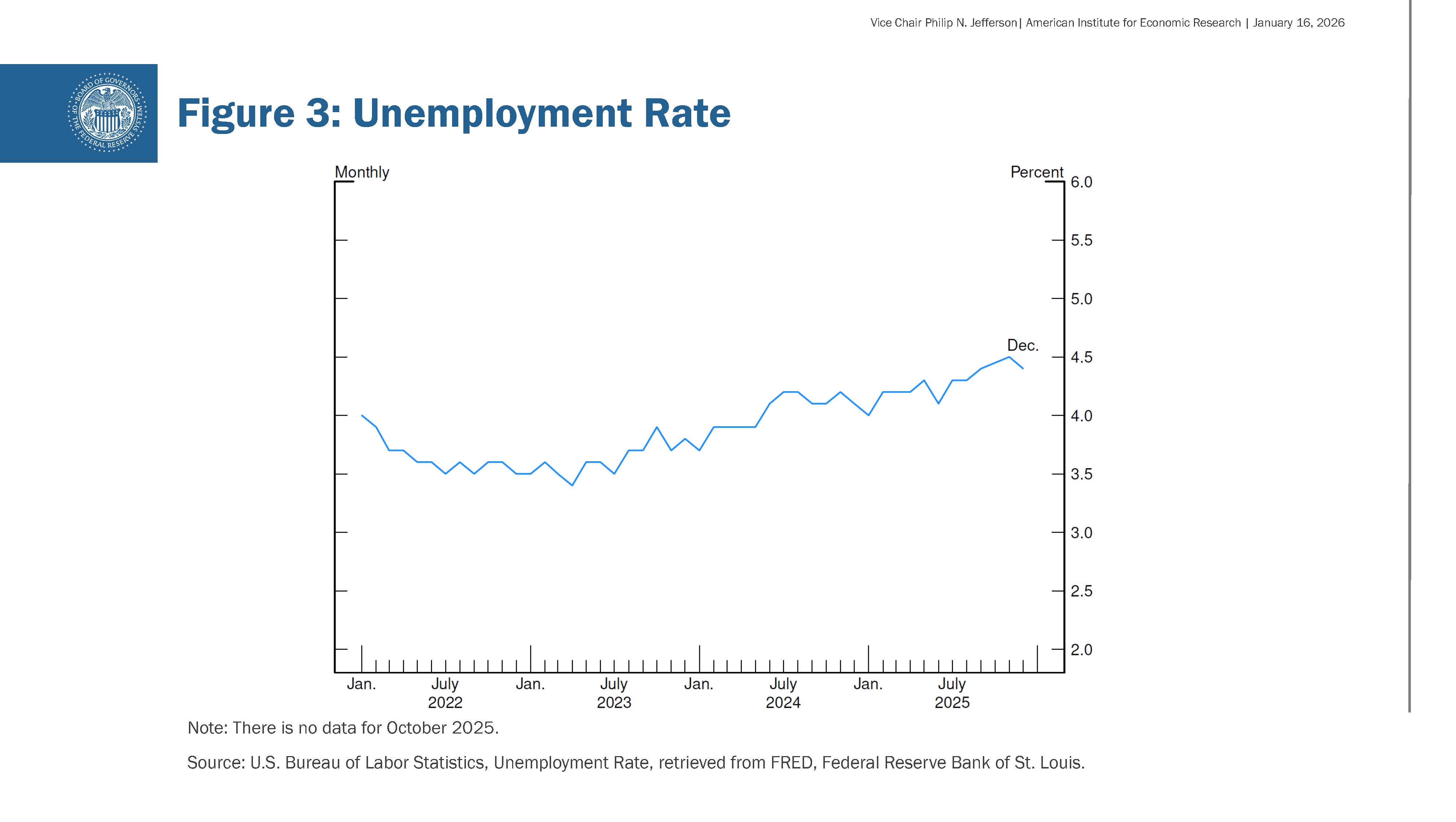

Looking at the labor market, job growth moderated last year, and the unemployment rate edged higher. In November and December, employers added about 50,000 jobs to payrolls each month, as you can see in figure 2. This came after payrolls declined in October, largely due to an unusually large number of separations from the federal government. However, even setting aside October, the broader trend last year showed slower job creation than in 2024. At least part of the slowdown in the job market reflects a decline in the growth of the labor force due to lower immigration and labor force participation. However, labor demand has softened as well. Meanwhile, the unemployment rate, shown in figure 3, ended the year at 4.4 percent, up modestly from 4.1 percent at the end of the previous year.

{kind=link}

{kind=link}

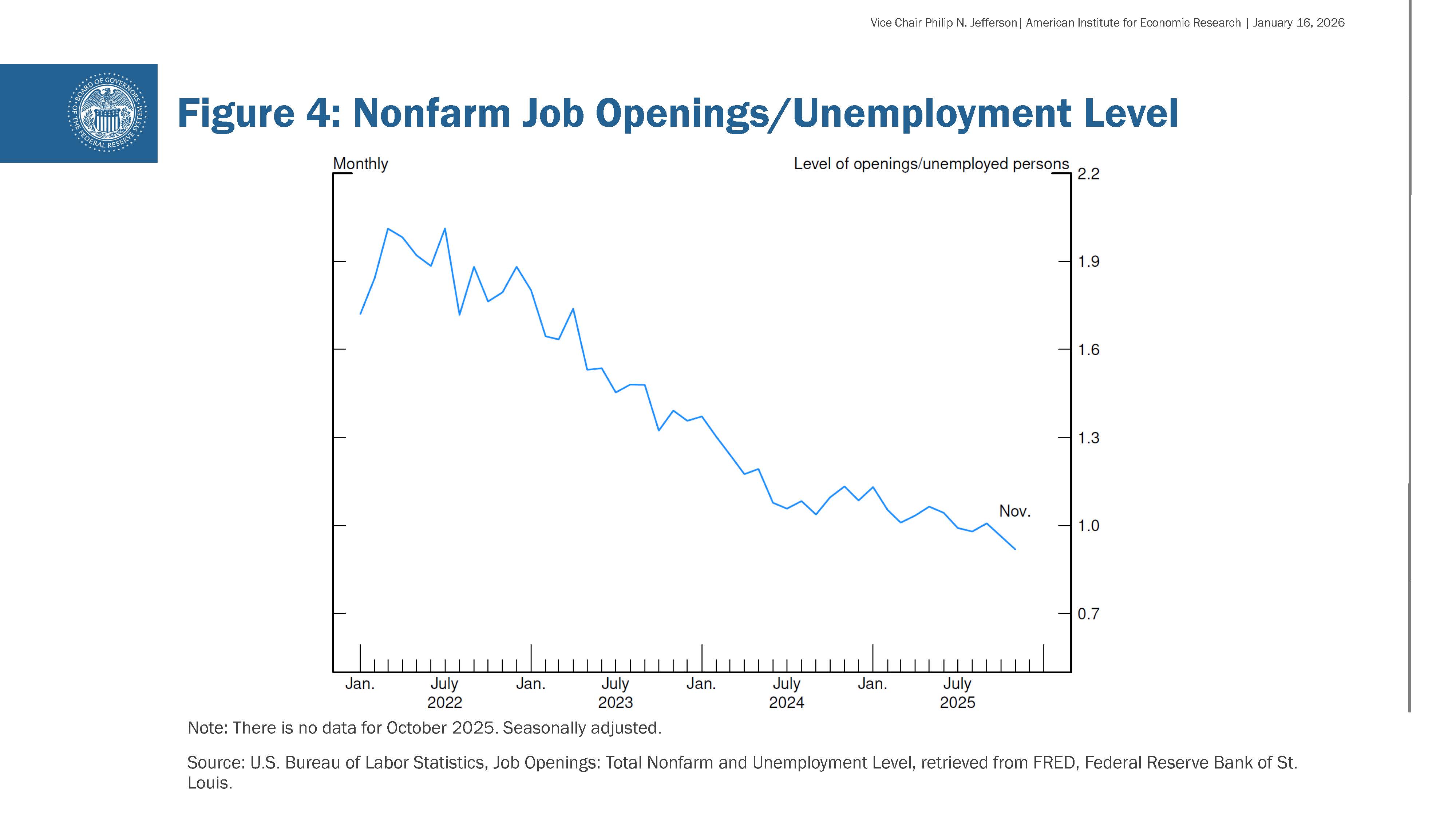

That said, the labor market is not deteriorating rapidly, as layoffs remain low; however, hiring remains low as well. Figure 4 shows that there were 0.9 available jobs in November for every unemployed American seeking work. While that level is normally consistent with a solid labor market, the ratio is considerably lower than a few years ago, when labor market conditions were much tighter early in the pandemic recovery. In this less dynamic and somewhat softer labor market, the downside risks to employment appear to have risen. My baseline, however, is for the unemployment rate to hold steady throughout this year.

{kind=link}

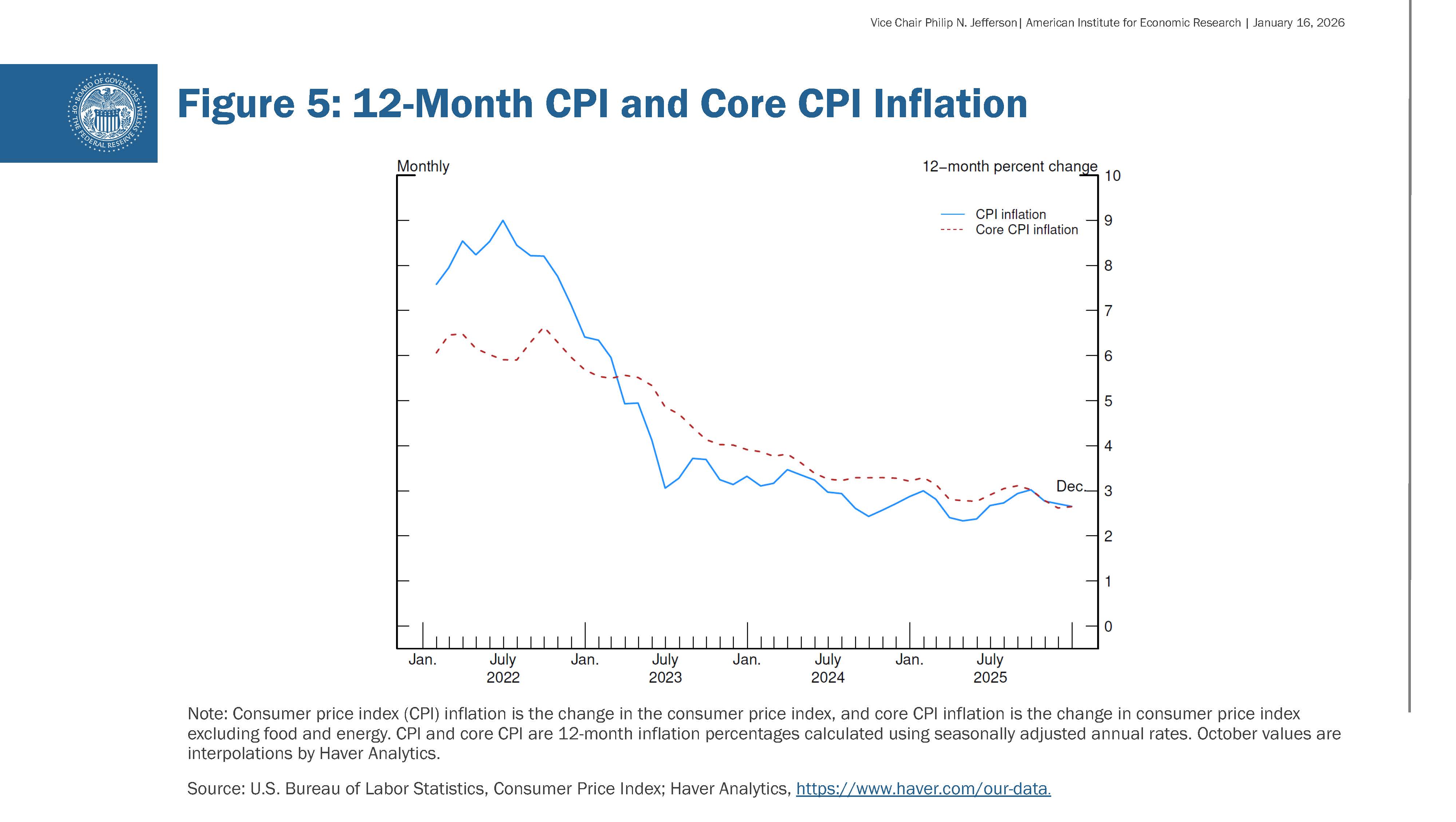

Considering the other part of our dual mandate, inflation remains somewhat elevated from our 2 percent goal. As you know, the Federal Open Market Committee (FOMC) targets the rate of increase in the personal consumption expenditures (PCE) price index; however, due to the government shutdown, the most recent available PCE price data are for September 2025. For this reason, I find it informative to review consumer price index (CPI) data to get a timelier sense of the direction of inflation, even if it does not directly translate to our inflation target. Over the longer term, both CPI and PCE measures tell a similar story. Data released earlier this week showed that the CPI rose 2.7 percent over the 12 months ending in December, the same rate as November. Core CPI, which excludes food and energy prices, rose 2.6 percent, also matching November's reading. You can see in figure 5 that both headline and core measures of inflation have eased significantly from their highs in mid-2022. However, that progress slowed over the past year or so, and inflation remains at a level that is above readings consistent with our inflation target.

{kind=link}

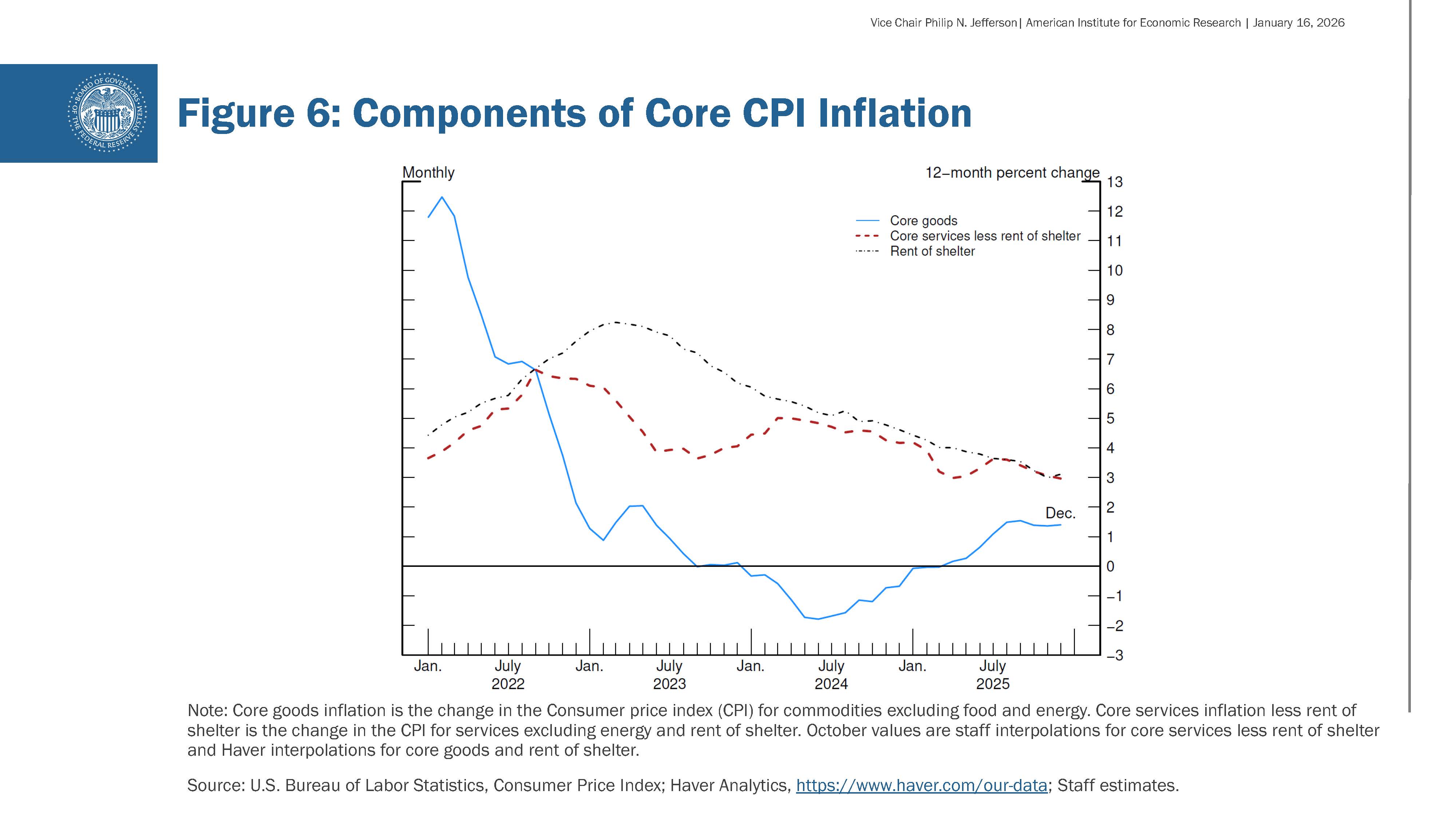

Looking at the subcomponents of core CPI, shown in figure 6, we can see why there has been a slowdown in the pace of disinflation. Over the past year, we have seen further notable declines in services inflation—rent of shelter as well as other non-energy services—but these have been offset by an increase in core goods price inflation. Looking at the three buckets separately, shelter inflation, shown by the black dot-dashed line, has continued to decline, and core services inflation excluding shelter, the red dashed line, has also been on a downward trend, albeit on a somewhat bumpier path. Those readings are consistent with overall inflation moving back toward our target. What is inconsistent with a return to 2 percent inflation is the rise in core good prices. Following very high readings during the pandemic, goods inflation fell sharply, reaching its pre-pandemic range in 2023, and fluctuated roughly in that range until 2025. Last year, core goods price inflation picked up markedly, to 1.4 percent over the 12 months ending in December 2025, at least in part reflecting increased tariffs filtering through to certain goods prices.

{kind=link}

While some upside risks remain, moving forward I expect to see inflation return to a sustainable path back to our 2 percent target. It is a reasonable base case that the effects of tariffs on inflation will not be long-lasting—effectively, a one-time shift in the price level. My view that inflation will resume a path toward our goal is consistent with near-term measures of inflation expectations declining from their peaks last year, as reflected in both market- and survey-based measures. And most measures of longer-term expectations remain consistent with our 2 percent inflation goal.

Monetary Policy

Although I am cautiously optimistic about the path ahead, as a monetary policymaker, I do confront a challenging situation. With the downside risks to employment having risen last year, I viewed the balance of risks as having shifted. As a result, I supported the FOMC's decisions to reduce the policy interest rate last year. I viewed that as the right step to balance the upside risk of persistent above-target inflation and the downside risk of a deteriorating labor market. This policy stance puts the economy in a good position moving forward.

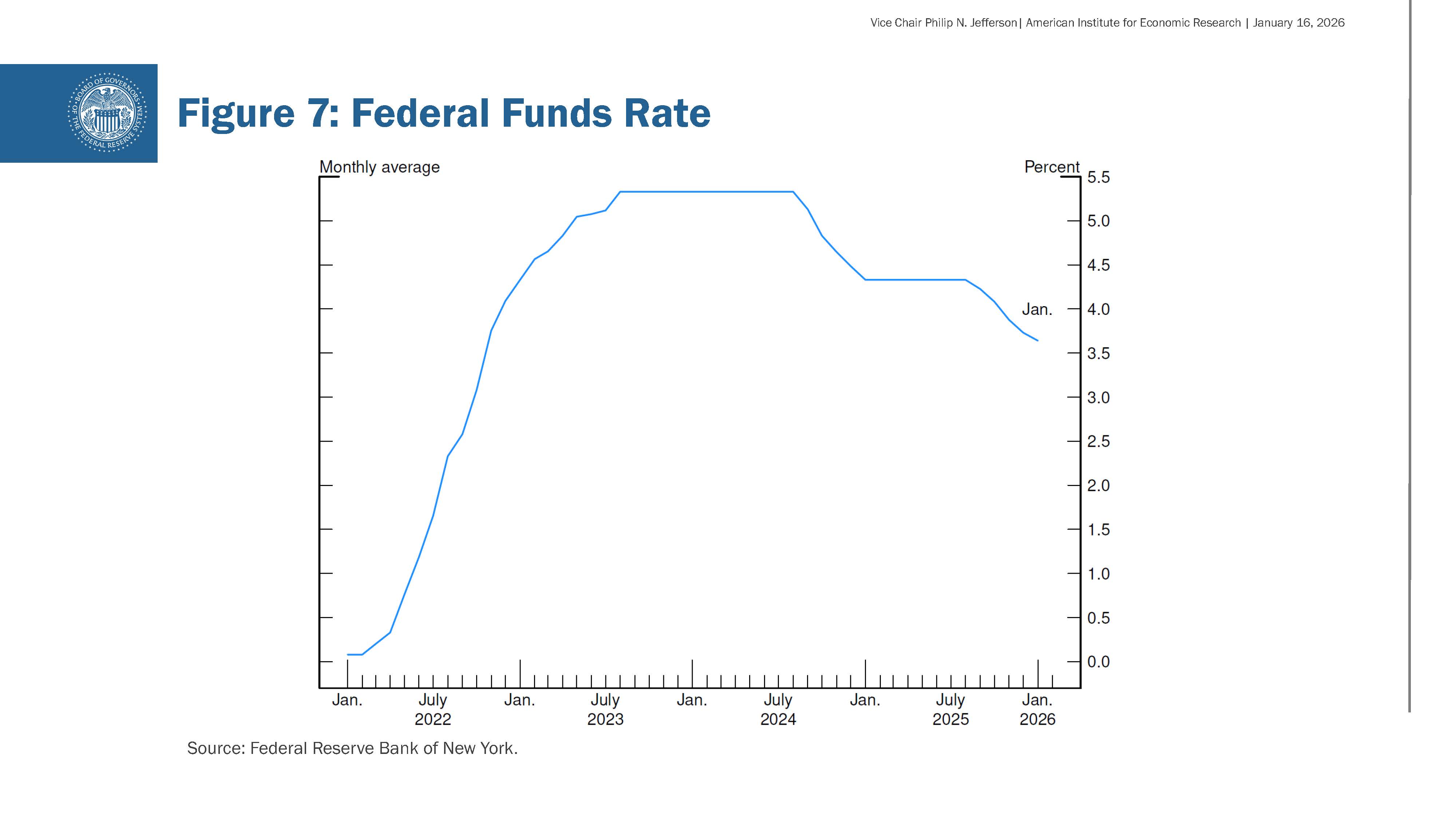

As shown in figure 7, since the middle of 2024, the Committee has reduced the policy rate by 1.75 percentage points. In my view, those moves have brought the federal funds rate into a range consistent with the neutral rate — a rate that neither stimulates nor restricts economic activity. I look forward to our upcoming policy meeting, which will be held in less than two weeks. While I do not want to prejudge the decision that will take place there, in my view, the current policy stance leaves us well positioned to determine the extent and timing of additional adjustments to our policy rate based on the incoming data, the evolving outlook, and the balance of risks.

{kind=link}

Monetary Policy Implementation

Now, let me turn to monetary policy implementation. I'll begin with a bit of history to provide a backdrop for recent developments.

{kind=link}

In January 2019, following many years of successful implementation along with extensive deliberations, the FOMC formally adopted its ample-reserves implementation framework.1 Some key advantages of this framework include successful control of the policy rate in a variety of conditions and effective transmission to other money market rates and broader financial conditions. The FOMC defined this framework as one where "control over the level of the federal funds rate and other short-term interest rates is exercised primarily through the setting of the Federal Reserve's administered rates, and in which active management of the supply of reserves is not required."2 Therefore, the supply of reserves needs to be sufficiently large to meet the demand for reserves on most days.

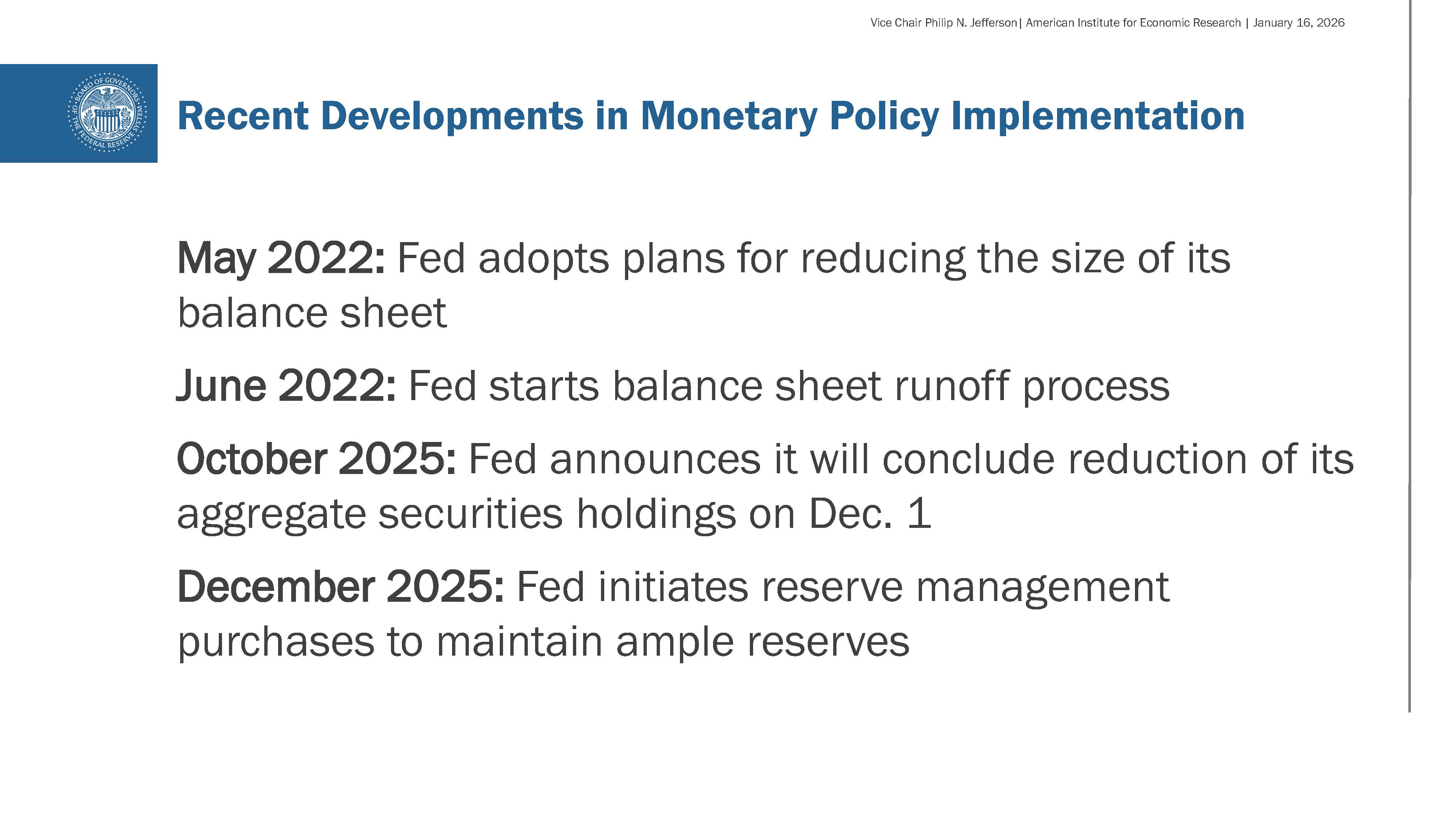

Against this backdrop, I'll now discuss recent developments in monetary policy implementation. As of December 2025, the FOMC concluded the process of reducing the size of the Fed's balance sheet that began in mid-2022 by halting the reduction of the Fed's asset holdings. During this process, we successfully reduced our securities holdings by about $2.2 trillion. This asset runoff affected not only our assets, but also our liabilities such as the reserves in the banking system and the level of overnight reverse repurchase agreement (repo) operation balances.

At the beginning of balance sheet runoff in 2022, reserves were at an abundant level of around $3.5 trillion. As the balance sheet shrank over the next few years, the federal funds rate remained about 7 basis points below the interest on reserve balances (IORB) rate for most of this period. The decline in the level of reserves from an abundant level toward an ample level exerted upward pressure on money market rates in recent months. As the level of reserves declined, repo rates started to increase and became more volatile. We began to see intensified rate pressures, especially on tax payment days and Treasury securities settlement days, when large flows into the Treasury General Account (TGA), another liability of the Fed, led to corresponding declines in the amount of reserves in the banking system. The federal funds rate started to move up steadily in its target range, and it now stands at 1 basis point below the IORB rate. These and other indicators of tightening money market conditions were what we expected to see as reserves declined toward the range of ample reserves.

It is important to note that while ending the asset runoff slows down the decline in reserves, it does not completely halt this process. Even when the Fed's assets remain constant, trend growth in non-reserve liabilities, particularly currency in circulation, will continue to absorb reserves over time. There is also significant cyclical variation in the supply of reserve balances, reflecting seasonal changes in the TGA and other factors. Furthermore, the demand for reserves is not static but rather dynamic, influenced by various factors including economic growth and changes in the financial system. Consequently, to maintain an ample reserves level—a key operational objective of our current monetary policy implementation framework—the FOMC must expand its balance sheet commensurately with the public's demand for its liabilities. This necessitates a nuanced and forward-looking approach to balance sheet management that considers both cyclical and structural factors affecting the demand for and supply of reserves.

With the level of bank reserves judged to have declined to an ample level, the FOMC initiated reserve management purchases in December 2025. This was the crucial next step in balance sheet management to maintain ample reserves and ensure effective interest rate control, as consistent with the plan we adopted in May 2022.3

It is important to note that reserve management purchases are not quantitative easing (QE). Each process has a distinct purpose, with different goals and economic implications. QE represents a monetary policy tool deployed when the federal funds rate is constrained by the effective lower bound. The primary objective of QE is to provide economic stimulus by exerting downward pressure on long-term interest rates. This has been achieved typically through large-scale purchases of longer-term Treasury securities and agency mortgage-backed securities. These purchases are intended to influence the yield curve and broader financial conditions by removing duration risk held by the public for a given setting of short-term interest rate policy.

In contrast, reserve management purchases involve the acquisition of Treasury bills and other short-term Treasury securities in a manner that further normalizes the average maturity of the Federal Reserve's asset holdings. They help implement the short-term interest rate policy decided on by the Committee but do not alter broader financial conditions. These routine purchases are conducted to maintain ample reserves and ensure effective control over short-term interest rates. The pace and size of these purchases are calibrated to meet demand for reserve balances and to adjust reserve supply as other items on the liabilities side of our balance sheet grow over time. These purchases do not have any implications for the stance of monetary policy.

As detailed in the statement released by the Federal Reserve Bank of New York at the conclusion of our December 2025 FOMC meeting, reserve management purchases will be front-loaded for the first few months to alleviate potential near-term pressures in money markets.4 Thereafter, we expect the pace of reserve management purchases to decline, though the actual size will depend on seasonal fluctuations in non-reserve liabilities and market conditions. In the end, the size of our balance sheet will be determined by the public's demand for our liabilities in our ample-reserves regime.

Before concluding, let me also emphasize that in our ample-reserves regime, standing repo operations are a critical tool that helps provide a ceiling on money market rates. By doing so, these operations ensure that the federal funds rate remains within its target range, even on days of elevated pressures in money markets. Consistent with this view, the FOMC eliminated the aggregate limit on standing repo operations in December 2025.5 These operations are intended to support monetary policy implementation and smooth market functioning, and they should be used by our counterparties when deemed economically sensible. This is indeed what we saw over the 2025 year-end period. There was notable upward pressure on repo rates amid substantial net Treasury settlements, as widely expected. Usage increased at the Fed's standing repo operations on year-end as market repo rates increased substantially. Despite the elevated levels of repo rates, trading conditions remained orderly in money markets. I am pleased to see increased usage of our standing repo operations when it becomes economically sensible to do so.

Conclusion

To conclude, I will reiterate that I am cautiously optimistic about the path of the economy while acknowledging that we face risks to both sides of our dual mandate. Consequently, I will continue to watch incoming data carefully so that we can set policy to achieve our mandated goals: maximum employment and stable prices. A critical aspect of achieving these goals is ensuring that the Fed can efficiently and smoothly implement monetary policy decisions. We have taken the necessary steps to ensure that capability and will continue to do so.

Once again, it has been an honor to be here. Thank you for the opportunity to speak with you, and I look forward to our discussion.

{kind=link}

1. For more details, see the minutes of the November 2018, December 2018, and January 2019 FOMC meetings, which are available on the Board's website at https://www.federalreserve.gov/monetarypolicy/fomc_historical_year.htm. Return to text

2. See Board of Governors of the Federal Reserve System (2019), "Statement Regarding Monetary Policy Implementation and Balance Sheet Normalization," press release, January 30. Return to text

3. See Board of Governors of the Federal Reserve System (2022), "Plans for Reducing the Size of the Federal Reserve's Balance Sheet," press release, May 4. Return to text

4. See Federal Reserve Bank of New York (2025), "Statement Regarding Reserve Management Purchases Operations," statement, December 10. Return to text

5. See Federal Reserve Bank of New York (2025), "Statement Regarding Standing Overnight Repo Operations," statement, December 10. Return to text