February 09, 2015

"Audit the Fed" and Other Proposals

At the Catholic University of America, Columbus School of Law, Washington, D.C.

It is a pleasure and a particularly personal honor for me to speak to you today as a guest of this institution.1

I am proud to say that my grandfather, James J. Hayden, earned his doctorate of law from Catholic University and later served as dean of the law school. He was an early scholar of the regulation prompted by a technological innovation that would change the world--aviation. He was, in that sense, someone who looked to the future and wanted to be a part of it. In his years leading the law school, I hope my grandfather could also glimpse the great institution that it would become.

It has been a little more than six years since the fall of 2008, when the peak of a severe financial crisis presented the very real threat of a second Great Depression. The damage was extensive, and for some time, the recovery was frustratingly slow. But the economy has improved considerably over the past two years, and I am optimistic that that this improvement will continue. The financial system is also stronger and more resilient after improvements in regulation and oversight by the Federal Reserve and other agencies and better management by banks and other financial firms.

The Fed acted boldly during and after the financial crisis in the face of great uncertainty. The full effects of these policies will become clearer with the passage of time. Indeed, the Federal Reserve's role in the Great Depression of the 1930s is still actively debated. That said, as I will show, the evidence as of today is very strong that the Fed's actions generally succeeded and are a major reason why the U.S. economy is now outperforming those of other advanced nations. Other central banks are now embracing some of the same bold steps undertaken much earlier by the Fed.

Against that background, I am concerned about several troubling proposals that would subject monetary policy to undue political pressure and place new limits on the Fed's ability to respond to future crises. My remarks will address three such proposals. The first goes by the somewhat misleading name of "Audit the Fed," and would subject the Federal Reserve's conduct of monetary policy to unlimited congressional policy audits (not to be confused with financial audits, which are already conducted regularly.)2 The second is a proposal to require the Fed to adopt and follow a specific equation in setting monetary policy and to face immediate congressional hearings and investigation by the Government Accountability Office (GAO) whenever it deviates from the policy dictated by that equation.3 And, third, there are discussions about imposing new limitations on the Fed's long-held powers to provide liquidity during a financial crisis.

I think these proposals are misguided for three reasons.

First, they are motivated by the belief that the Fed's response during the crisis was both ineffective and outside the bounds of its traditional role and responsibilities. In fact, the Fed's actions were effective, necessary, appropriate, and very much in keeping with the traditional role of the Fed and other central banks.

Second, these proposals are based on the assertion that the Federal Reserve operates in secrecy and was not accountable for its actions during the crisis, a perspective that is in violent conflict with the facts. The Fed has been transparent, accountable, and subject to extensive oversight, especially during and since the crisis. We have also taken appropriate steps since the crisis to further enhance that transparency.

Third, and most importantly, I believe these proposals fail to anticipate the significant costs and risks of subjecting monetary policy to political pressure and constraining the Fed's ability to carry out its traditional role of providing liquidity in a crisis.

Appropriate and Effective

There is no dispute that the Fed's actions after the onset of the financial crisis were unprecedented in scale and scope.

To help stabilize the financial system and keep credit flowing to households and businesses, the Federal Reserve lent to banks through the discount window and to financial institutions and markets through numerous new broad-based lending facilities it created using emergency lending authority granted by the Congress during the Great Depression.4 In a limited number of cases, the Fed also extended liquidity support to individual institutions whose imminent failure threatened to bring down the global financial system.

At the same time, the Federal Reserve used monetary policy to help stabilize the economy. After cutting our target for the overnight interest rate on loans between banks--our usual monetary policy tool--as low as it could go, the Fed took further action using unconventional policy tools. These policies involved communication, providing "forward guidance" that the Federal Open Market Committee (FOMC) expected to keep rates low for longer than had been expected, and also purchasing large amounts of longer-term Treasury debt and other securities to put downward pressure on long-term interest rates.

While these actions were extraordinary and in some respects unprecedented, they were taken because the threats posed by the crisis were also without precedent, even in the events that led to the Great Depression.5 For the first time, cutting the Fed's policy rate to near zero proved insufficient to halt a plummeting economy; so the Fed took further action. For the first time since the Great Depression, our nation faced a financial panic so severe that the Fed's normal overnight lending to banks was not enough; so the Fed did more, using congressionally granted powers it had held but not used since the 1930s that were intended to deal with just such rare emergencies.

As the Congress considers proposals that will affect the conduct of monetary policy and the Fed's ability to respond in a crisis, I believe it is also important to recognize how effective the Fed's response has been.

With respect to monetary policy, the unconventional policies were designed to stimulate the economy in the same way as traditional monetary policy, by lowering interest rates. These actions helped deliver highly accommodative policy, which was essential given the depth of the recession. Without these steps, the slump in the labor market and the broader economy surely would have been even deeper and more prolonged, and the low wage and price inflation we are still experiencing might have turned into outright deflation.

Critics warned that these policies would unleash uncontrollable inflation, fail to stimulate demand, and court other known and unknown risks. After I joined the Federal Reserve Board in May 2012, I too expressed doubts about the efficacy and risks of further asset purchases. But let's let the data speak: The evidence so far is clear that the benefits of these policies have been substantial, and that the risks have not materialized. Inflation has continued to run well below the Committee's 2 percent objective. Indeed, some argue today that low inflation should cause the Committee to hold off from raising interest rates. As I noted at the outset, due in part to the Fed's effective response to the crisis, the recovery in the United States has been stronger than that of other advanced economies, with more rapid job creation, lower unemployment, and faster growth. That is one reason why a number of central banks around the world have adopted forward guidance and asset purchase programs similar to the policies adopted by the Fed.6

The Federal Reserve's lending in the crisis was also successful. There is little dispute today that the crisis threatened a global financial collapse and depression, and that these liquidity policies were instrumental in arresting the crisis.

Warnings about the Fed's lending also have not been borne out. Critics claimed the Fed had been reckless, throwing money ineffectively at problems and making loans to uncreditworthy borrowers. On the contrary, the Fed's lending was targeted to institutions, markets, and sectors that proved central to arresting the crisis. Loans were extended based on the same terms that the Federal Reserve has always applied—the borrowers must be solvent, the loans must be secured, and an appropriate interest rate must be charged. As a result, every single loan we made was repaid in full, on time, with interest.7

Traditional Oversight of the Federal Reserve Was Extensive and Effective

The Federal Reserve, like other parts of our democratic system of government, must be accountable to the public and its elected representatives. Given the scale of the Fed's actions during the Crisis, it has been not only appropriate but essential that these actions be transparent to the public and subject to close and careful scrutiny by the Congress. And that is exactly what happened. So it is jarring to hear it asserted that the Fed carries out its duties in secret and is unaccountable to the public and its elected representatives. The Federal Reserve is highly transparent and accountable to the public and to the Congress.

First, the Fed does not set its own goals for monetary policy. Congress assigned us the goals of price stability and maximum employment--that is, the highest level of employment achievable without threatening price stability. Federal Reserve Board members are nominated by the President and must be confirmed by the Senate. The Chair of the Fed appears before both the House and Senate oversight committees twice every year to report on monetary policy, and, in practice, to respond to questions about anything and everything related to the Fed's activities. The Chair and other Board members routinely make additional appearances before the Congress and meet frequently with members.

More generally, the Fed is open and transparent in its operations, including those related to monetary policy, accounting for itself in timely postmeeting FOMC statements, minutes, broadcast press conferences, and speeches.8 Details about the Fed's balance sheet are on the public record; in fact, every security owned by the Fed is identified individually on the website of the Federal Reserve Bank of New York.9 The FOMC's plans to normalize the balance sheet have been the subject of exhaustive discussion--in FOMC meetings, in speeches by policymakers, and among the many journalists and academics who analyze and discuss Fed policies. Last September, the FOMC published its Normalization Principles, which set forth its plans to reduce the balance sheet to a more normal level over time.10

The Fed's financial statements are also a matter of public record, and are audited annually by independent, outside auditors under the watchful eye of the Fed's independent Inspector General.11 I am well aware of this because I chair the committees that have oversight responsibility for the audits of the Board and the Reserve Banks. I worked for many years in the financial markets, and I can tell you that the Federal Reserve's financial statements, though they contain very large numbers, are relatively straightforward--much simpler than those of a typical regional bank.

The Fed's operations, including its role regulating and supervising banks, are subject to extensive review by the GAO. If you visit the GAO's website, you'll find more than 70 reports since the crisis that are wholly or partly dedicated to reviewing the Fed's operations, including the emergency lending facilities I mentioned earlier.12 The GAO works closely with the Fed's Office of Inspector General, which is involved in both financial audits and other oversight of our operations.

The extensive oversight I describe intensified--appropriately so--as the Federal Reserve responded to the financial crisis. Our lending facilities were also the subject of review by the Fed's Inspector General, the Special Inspector General for the Troubled Asset Relief Program, the Congressional Oversight Panel, the Financial Crisis Inquiry Commission established by the Congress, and numerous congressional hearings and reviews.

The Fed's actions were also fully transparent. As always, monetary policy decisions were debated and voted on by the FOMC and announced immediately, with detailed explanations provided in the minutes of these deliberations. The Fed provided public guidance on its plans to purchase assets and made those purchases in open, competitive transactions that were disclosed as soon as they occurred.

The terms and conditions for every lending facility were publicly disclosed. The amounts lent under each program were published on the Fed's weekly balance sheet report. The Fed created a website and issued a monthly report to the Congress disclosing details on all loans, such as the quantity and quality of collateral posted by borrowers.13

The Significant Costs of Restrictions on the Fed's Independence

As I said at the outset, I believe these proposals under consideration by the Congress fail to anticipate the significant costs and risks of subjecting the Fed's conduct of monetary policy to political pressure and of limiting the ability of the Fed to execute its traditional role of keeping credit flowing to American households and businesses in a financial crisis.

Let me first address "Audit the Fed," which would repeal a narrow but critical exemption, adopted by the Congress in 1978, to limit GAO policy reviews of the Fed's conduct of monetary policy. The Congress granted this exemption because the costs of involving the GAO in monetary policy, including the substantial risk of political interference, far outweigh the potential benefits.

It is important to note that GAO investigations are not the financial audits that many assume them to be. They extend beyond mere accounting to examine strategy, judgments and day-to-day decisionmaking. Indeed, by statute, the GAO is charged with making recommendations to Congress about the areas they have reviewed. This could put the GAO in the position of reviewing the FOMC's policy decisions and recommending its own course for monetary policy.

With these features in mind, the potential benefits of GAO policy audits would be small, even before considering the potential costs. Unlike the programs that are typically the subject of GAO policy audits, such as procurement decisions that may be brought to light only by the GAO's attention, monetary policy decisions occur with all of the world watching. They are announced immediately, described in an FOMC statement, often elaborated on in a press conference, and the subject of endless same-day-analysis and debate.

With all of this transparency and analysis, very little would be revealed by GAO policy audits that would help evaluate the effectiveness of monetary policy. The benefits of frequent GAO policy audits would also be low because the effects of monetary policy are felt with a considerable time lag and are often only clear years later.

Audit the Fed also risks inserting the Congress directly into monetary policy decisionmaking, reversing decades of deliberate effort by the Congress to insulate the Fed from political pressure in carrying out its day-to-day duties. Indeed, some advocates of the bill have expressed support for complete elimination of the Federal Reserve. Long experience, in the United States and in other advanced economies, has demonstrated that monetary policy is most successful when decisions are rendered independent of influence by elected officials. As recent U.S. history has shown, elected officials have often pushed for easier policies that serve short-term political interests, at the expense of higher inflation and damage to the long-term health and stability of the economy.14

After World War II and as recently as the early 1970s, political pressures likely influenced Federal Reserve decisionmaking in a way which helped cause excessive inflation and related bouts of economic weakness. In 1977, as what came to be called the Great Inflation neared its peak, the Congress passed legislation that spelled out the goals for monetary policy--maximum employment and stable prices--but left it to the Fed to precisely define those goals and the means by which they would be achieved.15 To preserve the Fed's independence in implementing policy to reach these goals, the Congress exempted monetary policy from the GAO investigations it was then authorizing for other Fed operations.

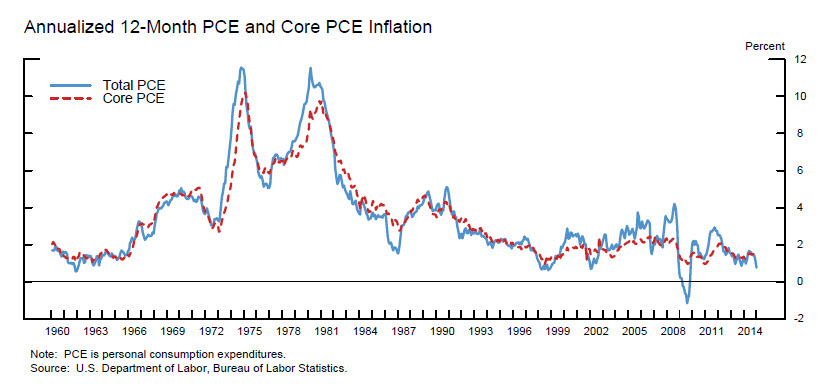

This independence has served the nation well. Over the 20 years or so prior to the crisis, the Federal Reserve was able to maintain low and stable inflation, and recessions were brief and mild.16 That is not to say that the Fed got everything just right during this period. But it seems to me that any pre-crisis shortcomings were in regulation and supervision by the Fed and other agencies, rather than in monetary policy.

And there are other costs from subjecting monetary policy to GAO investigations. Frequent GAO investigations would likely inhibit the debate and flow of information and ideas at FOMC meetings among staff and policymakers, which would lead to poorer decisions. Market participants would have to wonder whether the FOMC would react to GAO criticism, and they could lose confidence in the Fed's independence, reducing its credibility.

To those who may doubt that GAO investigations would be used by the Congress to try to influence monetary policy, let me briefly describe another proposal which envisions exactly that. This bill would require the FOMC to carry out monetary policy according to a simple equation and require immediate congressional hearings and a GAO audit whenever monetary policy deviates from this equation.17 Simple policy rules of this nature are used by the FOMC and by central banks around the world as a guide to policy. No central bank applies them in such a mechanical fashion, and there is very little support among economists for doing so.18 Based on my own experience in business, in government service, and in life, I doubt that important decisions can be reduced ultimately to such an equation. The most such a rule might do is get you 80 percent of the way there; that last 20 percent makes all the difference.

Finally, there has been discussion in the Congress of imposing new restrictions on the ability of the Fed to respond as it did with liquidity facilities during the financial crisis. Although I am not aware of a specific bill at this point, the idea is to limit the Fed's authority under section 13(3) of the Federal Reserve Act, under which the Fed is empowered to lend "in unusual and exigent circumstances" to firms beyond banks for the purpose of containing a financial crisis.

The Fed used this emergency lending authority to provide liquidity in the face of a systemwide panic that threatened the financial system. As the crisis receded, the Congress took two related actions. First, it gave the regulators what they had badly needed during the crisis, which was a means of resolving the largest financial institutions without threatening the financial system. Second, the Congress prohibited emergency loans to individual firms but retained the Fed's ability to establish broadly available lending programs during a crisis, with the prior approval of the Secretary of the Treasury and timely notification of the Congress.

This tradeoff came after extensive consultation between the Congress and the Federal Reserve. And I believe that it struck a reasonable balance. I also believe it would be a mistake to go further and impose additional restrictions. One of the lessons of the crisis is that the financial system evolves so quickly that it is difficult to predict where threats will emerge and what actions may be needed in the future to respond. Because we cannot anticipate what may be needed in the future, the Congress should preserve the ability of the Fed to respond flexibly and nimbly to future emergencies. Further restricting or eliminating the Fed's emergency lending authority will not prevent future crises, but it will hinder the Fed's ability to limit the harm from those crises for families and businesses.

Conclusion

In our democratic system, the Federal Reserve owes the public and the Congress a high degree of transparency and accountability. The Congress has wisely given the Fed the tools it needs to implement monetary policy and respond to future crises as well as crucial independence to do its work free from short-term political influence. I would urge caution regarding current proposals that threaten just such political influence and place restrictions on the very tools that so recently proved essential in preventing a new depression. Congressional oversight of the Federal Reserve, including its conduct of monetary policy, is extensive, but no doubt could be improved in ways that do not threaten the Fed's effectiveness. I would welcome discussions with the Congress about ways to aid its important oversight of monetary policy. There may be differing views of how Congress can best carry out this responsibility, but there can be no disagreement about the purpose of such oversight, which is to help the Federal Reserve succeed in promoting a healthy economy and a strong and stable financial system. Those are the goals Congress assigned the Federal Reserve a century ago, and I am optimistic that Congress and the Fed will continue to work together to pursue them on behalf of the American people.

1. The views expressed here are my own and not necessarily those of other members of the Federal Open Market Committee. Return to text

2. See Federal Reserve Transparency Act of 2015, H.R. 24, 114 Cong. (2015); and Federal Reserve Transparency Act of 2015, S. 264, 114 Cong. (2015). Return to text

3. See Federal Reserve Transparency Act of 2015 in note 2. Return to text

4. See Banking Act of 1935, ch. 614, 49 Stat. 684 (1935). Return to text

5. See Ben S. Bernanke (2010), statement before the Financial Crisis Inquiry Commission, Washington, D.C., September 2; and Ben Bernanke (2009), closed session (PDF) of the Financial Crisis Inquiry Commission, Washington, D.C., November 17. Return to text

6. On the effectiveness of the Fed’s unconventional monetary policy, see Eric M. Engen, Thomas T. Laubach, and David Reifschneider (2015), "The Macroeconomic Effects of the Federal Reserve’s Unconventional Monetary Policy Actions (PDF)," Finance and Economic Discussion Series 2015-005 (Washington: Board of Governors of the Federal Reserve System, January); Joseph Gagnon, Matthew Raskin, Julie Remache, and Brian Sack (2011), "The Financial Market Effects of the Federal Reserve's Large-Scale Asset Purchases," International Journal of Central Banking, vol. 7 (March), pp. 3-43; Stefania D'Amico and Thomas B. King (2013), "Flow and Stock Effects of Large-Scale Treasury Purchases: Evidence on the Importance of Local Supply," Journal of Money, Credit and Banking, vol. 44 (February, issue supplement s1), pp. 3-46. Return to text

7. On the effectiveness of the Fed's emergency lending, see Sean D. Campbell, Daniel M. Covitz, William R. Nelson, and Karen M. Pence (2011), "Securitization Markets and Central Banking: An Evaluation of the Term Asset-Backed Securities Loan Facility," Journal of Finance, vol. 68 (April), pp. 715-37; and Tao Wu (2011), "The U.S. Money Market and the Term Auction Facility in the Financial Crisis of 2007-2009," Review of Economics and Statistics, vol. 93 (May), pp. 617-31. Return to text

8. For example, see Statistical Release H.6, "Money Stock Measures," on the Board's website. Return to text

9. See the Federal Reserve Bank of New York's webpage "System Open Market Account Holdings" . Return to text

10. See Board of Governors of the Federal Reserve System (2014), "Federal Reserve Issues FOMC Statement on Policy Normalization Principles and Plans," press release, September 17. Return to text

11. See "Federal Reserve System Audited Annual Financial Statements" on the Board's website. Return to text

12. The reports are available on the GAO's website. Return to text

13. See "Credit and Liquidity Programs and the Balance Sheet" on the Board's website. Return to text

14. The seminal research establishing a link between central bank independence and macroeconomic performance is Alberto Alesina and Lawrence H. Summers (1993), "Central Bank Independence and Macroeconomic Performance: Some Comparative Evidence," Journal of Money, Credit and Banking, vol. 25 (May), pp. 151-62. More recent research finds the relationship to be less solid, however, in part because independent central banks have in several cases been instituted precisely because economic performance has been subpar; for example, see Christopher Crowe and Ellen E. Meade (2007), "The Evolution of Central Bank Governance around the World," Journal of Economic Perspectives, vol. 21 (4), pp. 69-90; Christopher Crowe and Ellen E. Meade (2008), "Central Bank Independence and Transparency: Evolution and Effectiveness," European Journal of Political Economy, vol. 24 (4), pp. 763-77; and N. Nergiz Dincer and Barry Eichengreen (2014), "Central Bank Transparency and Independence: Updates and New Measures," International Journal of Central Banking, vol. 10 (1), pp. 189-259. Return to text

15. See Robert J. Samuelson (2008), The Great Inflation and Its Aftermath: The Transformation of America's Economy, Politics, and Society (New York: Random House). Return to text

16. See the figure "Annualized 12-Month PCE and Core PCE Inflation" that shows inflation and core inflation over time. Return to text

{kind=link}

17. See Federal Reserve Transparency Act of 2015 in note 2. Return to text

18. As part of its ongoing Initiative on Global Markets (IGM) poll, the University of Chicago, Booth School of Business, asked 44 prominent economists to respond to the following statement: "Legislation introduced in Congress would require the Federal Reserve to "submit to the appropriate congressional committees…a Directive Policy Rule," which shall describe "the strategy or rule of the Federal Open Market Committee for the systematic quantitative adjustment of the Policy Instrument Target to respond to a change in the Intermediate Policy Inputs." Should the Fed deviate from the rule, the Fed Chair would have to "testify before the appropriate congressional committees as to why the [rule]…is not in compliance." Enacting this provision would improve monetary policy outcomes in the U.S." None of the participants agreed with the statement, and almost all disagreed or strongly disagreed. The results of the poll are available on the Booth School's IGM Forum website at www.igmchicago.org/igm-economic-experts-panel/poll-results?SurveyID=SV_doNZ9FbNq7tDi97. Return to text