February 18, 2015

Financial Institutions, Financial Markets, and Financial Stability

At the Stern School of Business, New York University, New York, New York

It has now been over six years since the most acute phase of the financial crisis. Over the intervening years, market structures have evolved, and financial firms have changed their business models in important respects. Authorities around the world are implementing reforms that address the painful lessons of the crisis, while at the same time keeping the evolution of markets and firms in mind.1

Today, I will briefly summarize this sweeping reform program as it relates to large, global systemically important banks (G-SIBs), critical financial market infrastructure, and money markets. In my view, the basic agendas in these areas are, to different degrees, well developed, although a great deal of implementation remains. In contrast, I will argue that thinking about financial stability in the context of credit markets is less advanced and presents difficult challenges for supervisors. I will consider a range of factors that may address those challenges, illustrated with a discussion of recent developments in the syndicated leveraged loan market. And I will argue that the standard for regulatory intervention in the credit markets should be higher than for the other three areas.

Financial Institutions: Even before the financial crisis ended, it was clear that reforms to strengthen the most systemically important firms and their regulation and supervision needed to be the first order of business. I will mention four critical elements of that program. First, these institutions are required to hold, and now do hold, much higher levels of higher-quality capital, as measured by both risk-based ratios and a much more comprehensive leverage ratio. Under the "enhanced prudential standards" of the Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank), the fully phased-in capital requirements will be meaningfully higher for these institutions because of the greater threat their failure would pose to the financial system and to the broader economy. Second, these institutions are for the first time becoming subject to rule-based liquidity regulation, including the Liquidity Coverage Ratio, the Net Stable Funding Ratio, and liquidity stress testing.2 These innovations are in part designed to address the firms' vulnerabilities to damaging runs on their short-term financing, runs that occurred repeatedly during the crisis and clearly increased its severity. Third, we now have rigorous, forward-looking capital stress testing that recognizes the dynamic nature of the financial system and guards against the excessive optimism that can build during a credit boom.

These three reforms are well advanced and, in my view, have left the G-SIBs far stronger than they were before the crisis. Together, they significantly reduce the probability of a large bank failure. But they would leave us short of meeting the overriding objective of eliminating the too-big-to-fail conundrum without a fourth reform--a viable resolution mechanism that could handle the failure of these institutions without severe damage to the economy. Until recently, no nation has had a way of handling such failures without that degree of damage.

Authorities around the world have been working to develop an approach to resolving large financial firms that credibly imposes losses on shareholders and debt holders consistent with the basic tenets of our capitalist system, but does so in a way that protects the rest of the financial system and the real economy from severe damage. The single-point-of-entry approach developed by the Federal Deposit Insurance Corporation (FDIC) in conjunction with other U.S. supervisors is a promising innovation, especially in combination with the recent proposal of the Financial Stability Board to increase the "total loss absorbency capacity" of systemically important firms in terms of their total levels of equity and long-term debt. When fully worked out, these new regulatory regimes should permit a large, consolidated entity that owns banks or broker-dealers to continue to function even if the ultimate holding company ceases to be viable and must be recapitalized or wound down.

As I said at the outset, these reforms directed at the G-SIBs are well advanced. But much implementation remains, including, most notably, addressing cross-border issues associated with the failure of complex global firms. It will take time and continued international cooperation to complete this task.3

Infrastructure: The crisis exposed a number of important weaknesses in the infrastructure of the financial markets--what might be more plainly called the plumbing. Reforms aimed at addressing these weaknesses receive less public attention than those focused on the G-SIBs, and are in some respects less advanced in their conception and execution. But they are, in my view, of great importance.

I will mention two important sets of reforms in the U.S. context, one well advanced and the other still under development. The first concerns the triparty repurchase agreement (repo) market, which is a principal source of overnight financing for the largest securities dealers. Before the crisis, the functioning of this market was critically dependent on the extension of large volumes of discretionary intraday credit by two clearing banks. When confidence in Bear Stearns collapsed in March 2008, the vulnerability of this market and its settlement procedures in particular became very clear. Today, almost seven years later, in no small measure thanks to the leadership and persistence of the Federal Reserve Bank of New York, the triparty repo settlement process has been substantially reengineered, with reliance on discretionary intraday credit essentially eliminated.4 In addition, a smaller fraction of the market now involves the financing of lower-quality collateral, and far less of the overall funding is provided overnight and thus subject to daily rollover risk. 5 Dealers in general manage their short-term funding risk far more conservatively than before the crisis, including by carrying substantially higher levels of liquidity, in part because of the introduction of prudential liquidity standards that I mentioned earlier.

Second, as I have discussed at some length in other venues, in the run-up to the crisis, the highly opaque and fast-growing market for over-the-counter derivatives gave rise to an underappreciated and largely invisible buildup of risk, which proved a major source of instability when the crisis broke.6 In light of this experience, authorities around the world agreed in 2009 that standardized derivatives should be cleared through central counterparties (CCPs), and that noncentrally cleared derivatives should be subject to minimum margin requirements.

Central clearing holds the promise of enhancing financial stability through the netting of counterparty risks, creating greater transparency, and applying stronger and more consistent risk-management practices. But this reform program will only succeed if CCPs, in which counterparty credit risks are concentrated, are strong enough to withstand severe but plausible stress scenarios, including, for example, the failure of multiple clearing members. Achieving this degree of resiliency will require robust liquidity risk-management practices, including the maintenance of substantial buffers of liquid resources that can quickly be tapped. In addition, adequate loss absorption capacity is essential, including through substantial initial margin requirements and default funds. A framework for such requirements has been agreed upon at the international level through the Principles for Financial Market Infrastructures.7 Vigorous implementation at the national level is essential. There is also a need for greater transparency for clearing members and the public regarding the risk-management practices of CCPs, for heightened stress testing, for consideration of "skin-in-the-game" requirements, and for credible recovery and resolution plans. A great deal of work remains to be done to finalize and implement these additional reforms in all of the important CCPs around the world.

Money Markets: Money markets involve money-like investments such as commercial paper and repo. Investors in these markets include money market funds, corporations and other large holders of excess cash seeking a safe return in the short term, frequently no longer than overnight. Borrowers in money markets include banks, securities dealers and other financial companies, nonfinancial corporations, and governments. By linking investors seeking a safe return with borrowers needing short-term credit, money markets do what commercial banks have always done, but without deposit insurance and other aspects of the safety net provided for regulated depository institutions. After Lehman failed and the Reserve Fund "broke the buck," money market fund investors realized that their investments were not as safe and liquid as "money" after all. There were widespread runs in these markets, and it took a U.S. Treasury guarantee, augmented by a number of unprecedented liquidity facilities established by the Federal Reserve, to stabilize the money market fund industry and, more importantly, stave off a sudden stoppage of the flow of credit to households and businesses.

This experience tells us clearly that disruptions in the money markets can threaten the broader financial system. Regulation to increase the resilience of the money markets needs to reflect their systemic importance. Some important steps have been taken to address the most immediate risks--for example, through the liquidity standards for large institutions I mentioned earlier. But the risks associated with dislocations in the money markets go far beyond the large banks.

The Securities and Exchange Commission (SEC) has taken some important steps to address the money market fund issue, notably through its 2014 rule amendments.8 To address so-called repo runs, the Financial Stability Board is in the final phases of developing a framework of margin rules designed to be applied uniformly across nations for securities financing transactions involving nongovernmental securities. These minimum standards should increase the resiliency of those markets and mitigate the pressures on terms that inevitably emerge during benign periods. We expect to propose regulations implementing these rules in the United States in due course.

Credit Markets: That brings me to the credit markets, where households, businesses and governments engage in borrowing to fund their purchases and operations. These markets figured importantly in the crisis, most notoriously through securities collateralized by subprime mortgages. The story is by now well known. Lenders offered these loans to retail borrowers, often with negligible or simply fraudulent underwriting. Many of our largest financial institutions packaged the loans into marginally capitalized securitization structures that were rated highly by the credit rating agencies and thus generally viewed as suitable for purchase by a range of investors--including the most risk averse. As conditions in the housing market deteriorated, the threat of significant mortgage defaults emerged in 2007. The panic began in earnest when it became apparent that exposure to subprime mortgages was ubiquitous, from the balance sheets of key financial intermediaries and their supposedly "off balance sheet" vehicles to the investment portfolios of other institutional investors around the world. Although the total losses were initially thought to be not so large as to threaten the system, some of these toxic mortgage-backed securities (MBS) were financed with the types of short-term, confidence-sensitive funding mechanisms I have just described, which amplified the dislocations once the run in funding markets began and caused great harm to the broader economy.

As the crisis has receded, supervisors--not to mention market participants, commentators, and the general public--have eyed financial markets with a heightened sensitivity to anything that resembles the buildup of risks that occurred in the run-up to the crisis--a natural and useful exercise in pattern recognition. In that spirit, the Fed, the Office of the Comptroller of the Currency (OCC), and the FDIC have focused significant attention on the origination activities of depository institutions in the syndicated leveraged loan market, where some of the troubling patterns that were evident in subprime MBS have been observed.

These conditions prompted policymakers first to ask questions and then to act. Fed officials raised concerns publicly as early as 2011.9 The Fed, the OCC, and the FDIC issued supervisory guidance emphasizing these concerns in 2013.10 In 2014, the agencies clarified the guidance through published FAQs and began to exercise intensive supervision at the largest regulated banks emphasizing the need to improve underwriting standards and credit risk management on safety and soundness grounds.11

The case of the leveraged loan market is an interesting one, because it sits at the intersection between core financial institutions and credit markets and illustrates the challenges supervisors face in thinking about intervention in credit markets. I will turn to that market now in some detail.

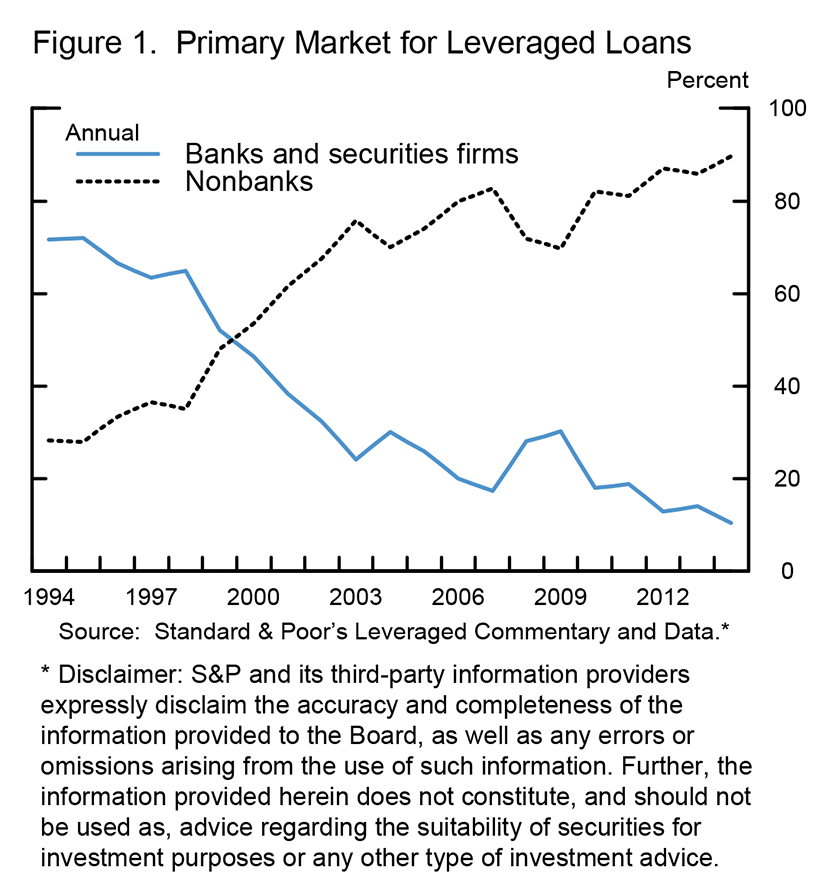

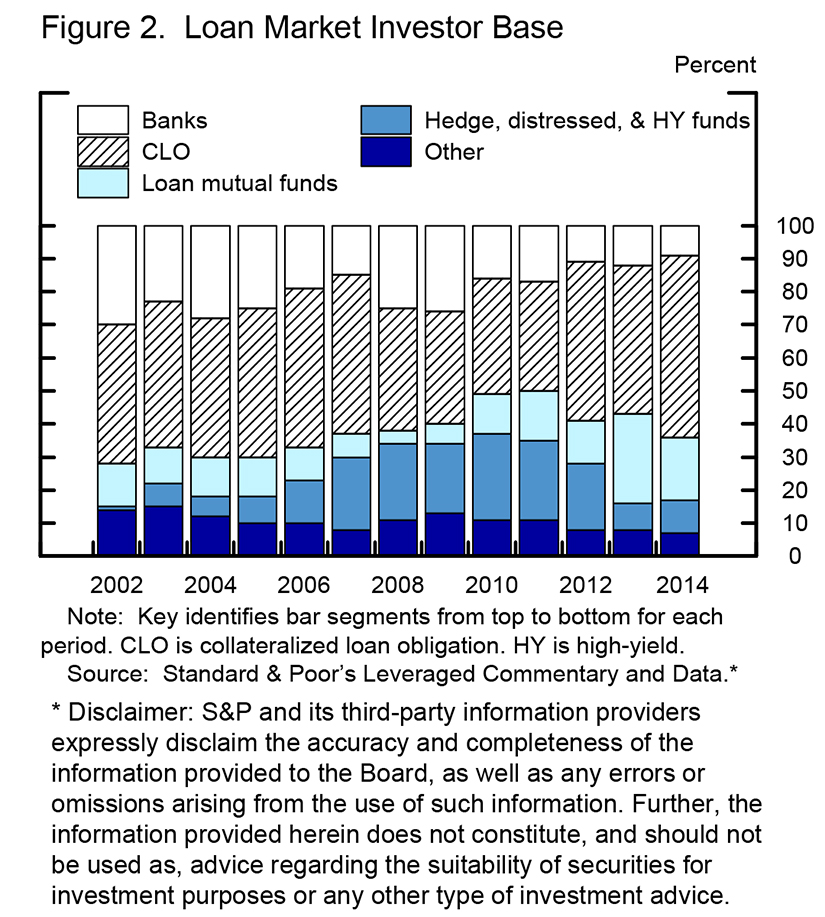

The term portions of leveraged loans are typically not held in the arranging banks' portfolios, but rather sold to a wide range of institutional investors--collateralized loan obligations (CLOs), retail loan funds, pension funds, insurance companies, hedge funds, and others (figures 1 and 2). This "originate-to-distribute" model is now dominant across a range of markets and reflects the movement over several decades of credit intermediation from portfolio lending (from the firm's perspective, the "storage business") to the capital markets (the "moving business"). This practice transfers and disperses credit and liquidity risks from the core of the financial sector to capital market investors that are willing to bear such risks for what they deem appropriate compensation. While the risks do not disappear, the system can, in principle, be safer if the ultimate institutional investors pose lower risk to the system than banks. For example, movement of credit exposure to speculative grade firms from a bank's balance sheet to a vehicle that is stably funded by sophisticated, deep-pocket institutional investors could be a net gain to financial stability. Movement of such loans to a highly leveraged, runnable vehicle beyond the regulatory perimeter could have the opposite effect.

{kind=link}

{kind=link}

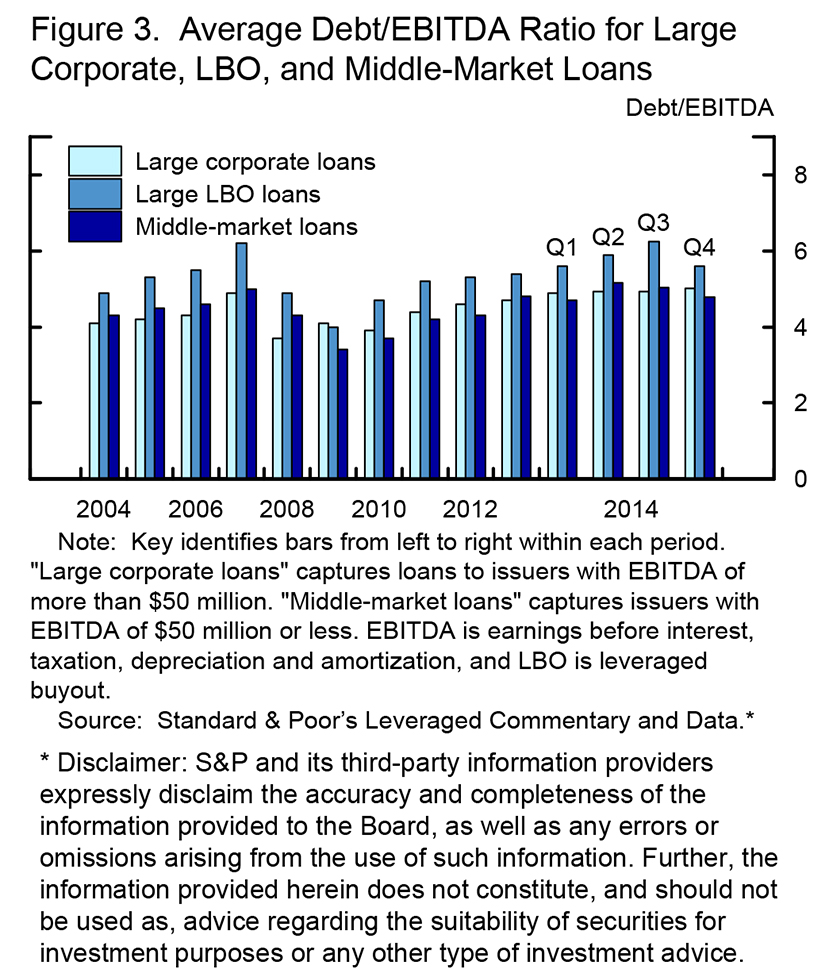

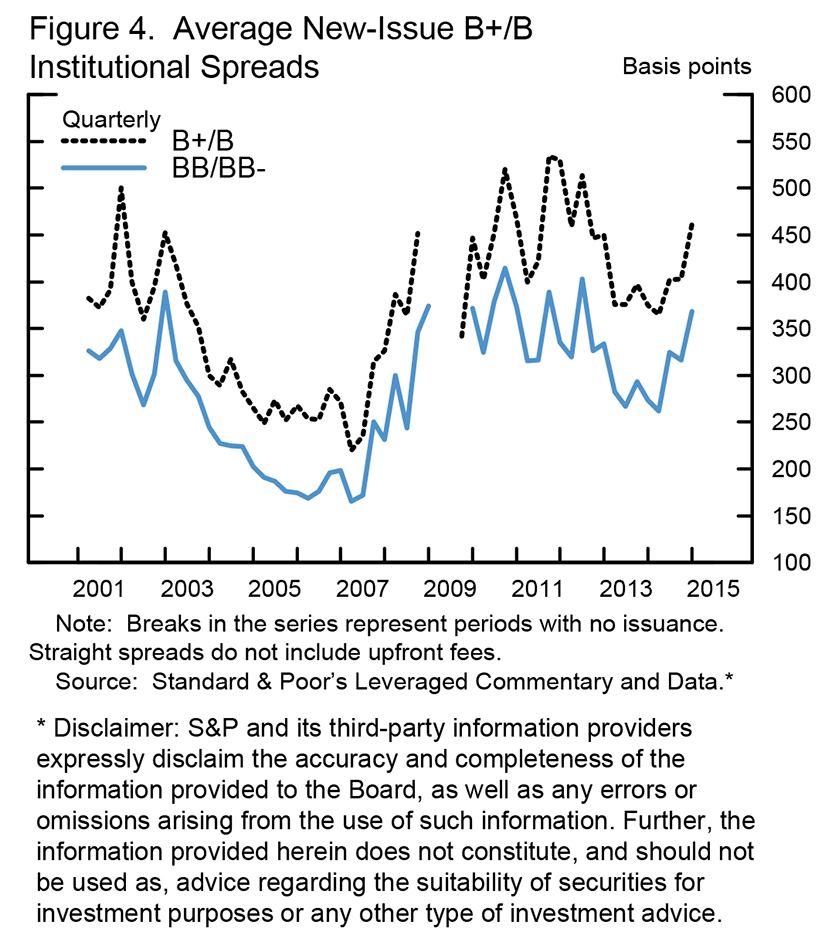

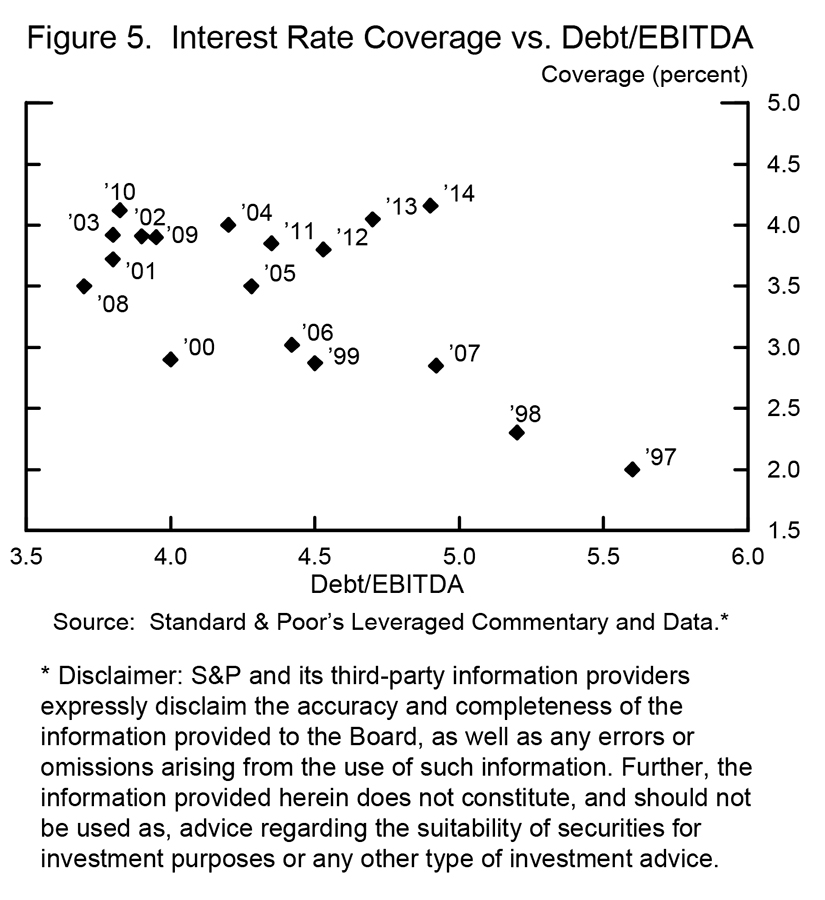

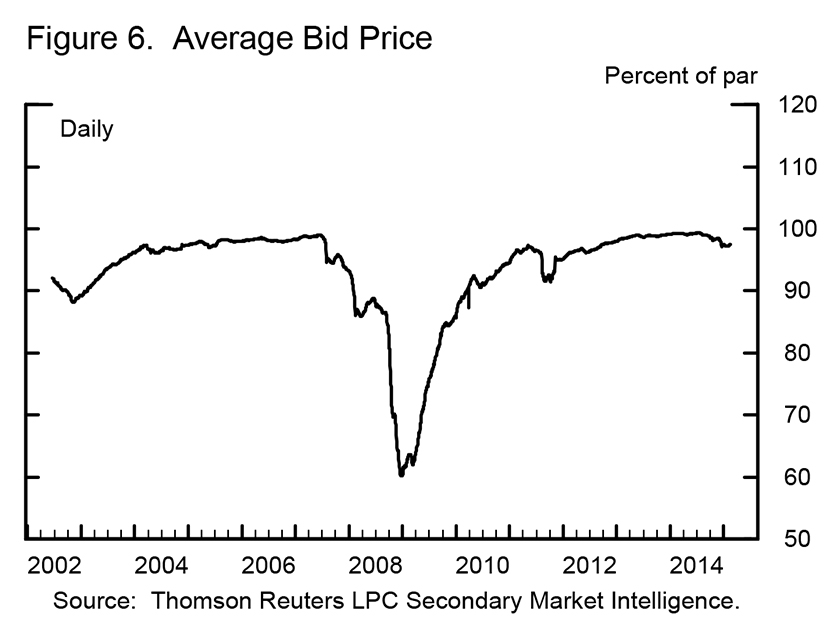

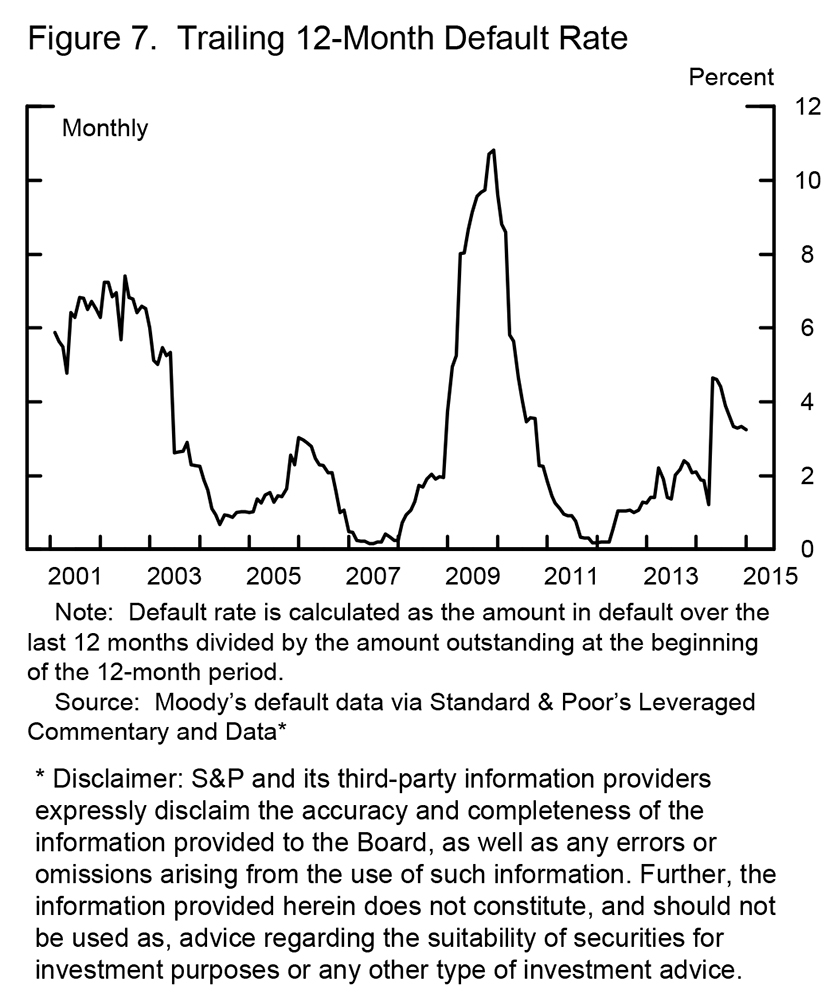

Pre-crisis conditions in leveraged finance markets were, with the benefit of hindsight, clearly in bubble territory. Deal leverage was at historically high levels (figure 3), and spreads were at historic lows (figure 4). Interest coverage ratios were quite low (figure 5). Unusually large leveraged buyouts were common. Banks entered into very large, long duration commitments to fund deals that faced significant regulatory and other requirements before they could close. Estimates vary, but when the crisis emerged and liquidity in these markets evaporated, large dealers were left holding roughly $350 billion in loans and commitments in their pipelines that they could not sell, and these positions remained on banks' balance sheets for a time. As loan values declined an unprecedented 40 percent (figure 6), there were significant mark-to-market losses on these assets, which may have contributed to doubts about the condition of institutions at the core of the system. Subsequent default rates were not outsized by historical standards, and recovery rates were in line with past averages (figure 7). Of course, the Fed's monetary policy eased financial conditions across the economy and enabled the refinancing of many of these loans at lower rates and with issuer-friendly terms.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Because leveraged loans were generally not held in investment structures that used short-term, confidence-sensitive funding, these investments were not a principal focal point of runs such as those that plagued MBS funding structures. CLOs were the largest institutional investors in leveraged loans, holding over 50 percent of loans outstanding. These structures are funded with stable capital, with both equity and debt tranches committed for several years--a longer duration than that of the underlying loans.

This picture of the pre-crisis leveraged lending market is one of a sharp decline in underwriting standards and a breakdown of risk management, resulting in a large risk buildup involving many of the G-SIBs--something the Fed and other regulators want to avoid. Leveraged loans may not have been a material cause of the crisis, and leveraged lending alone would likely not have threatened the overall health of the large institutions. But caution on the part of supervisors is certainly understandable here. It is worth remembering that the destructive potential of the subprime mortgage market was not obvious in advance and not fully reflected in real-time measures of balance sheet exposure. In light of that demonstrated uncertainty, since the crisis, supervisors have opted to react earlier and more aggressively to the buildup of risk.

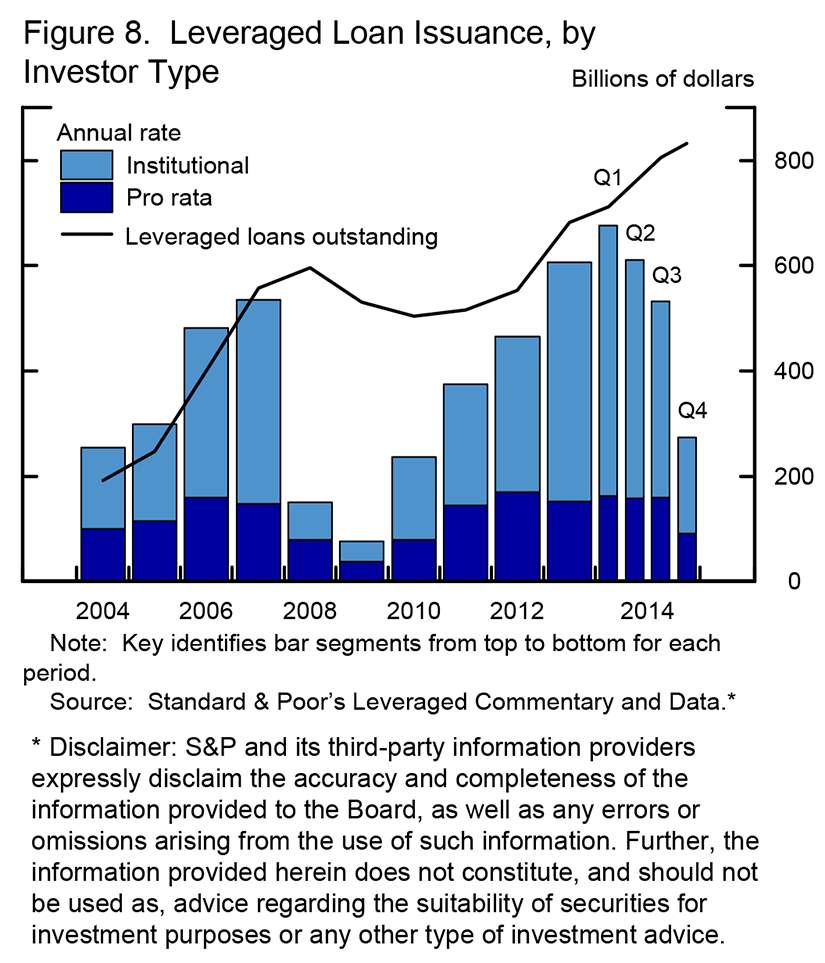

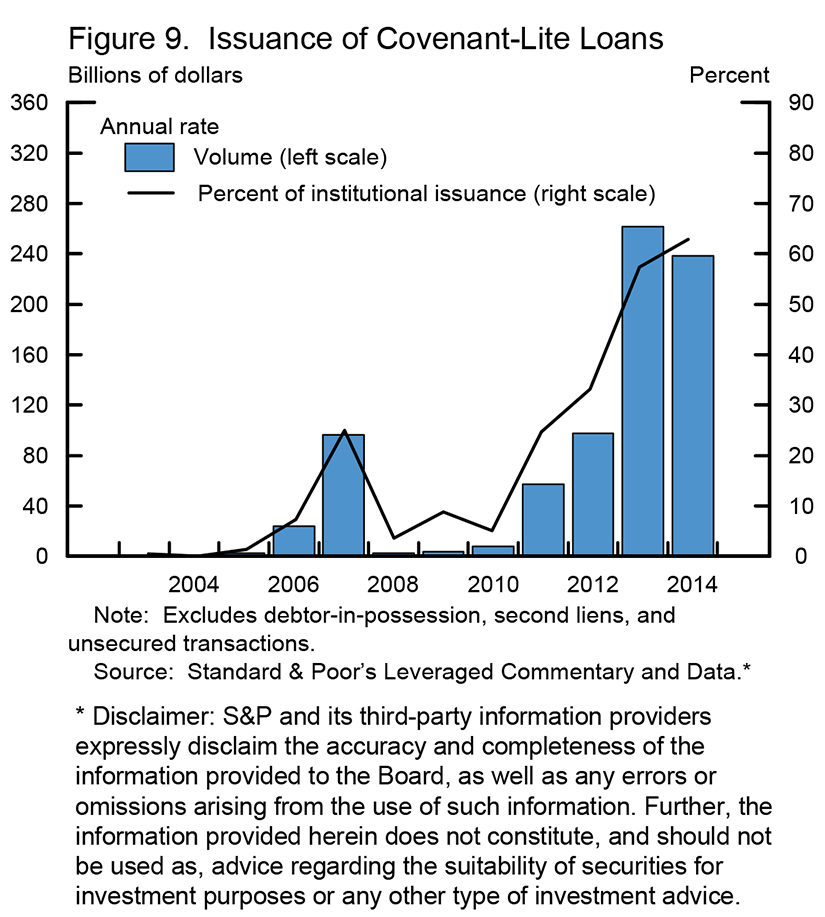

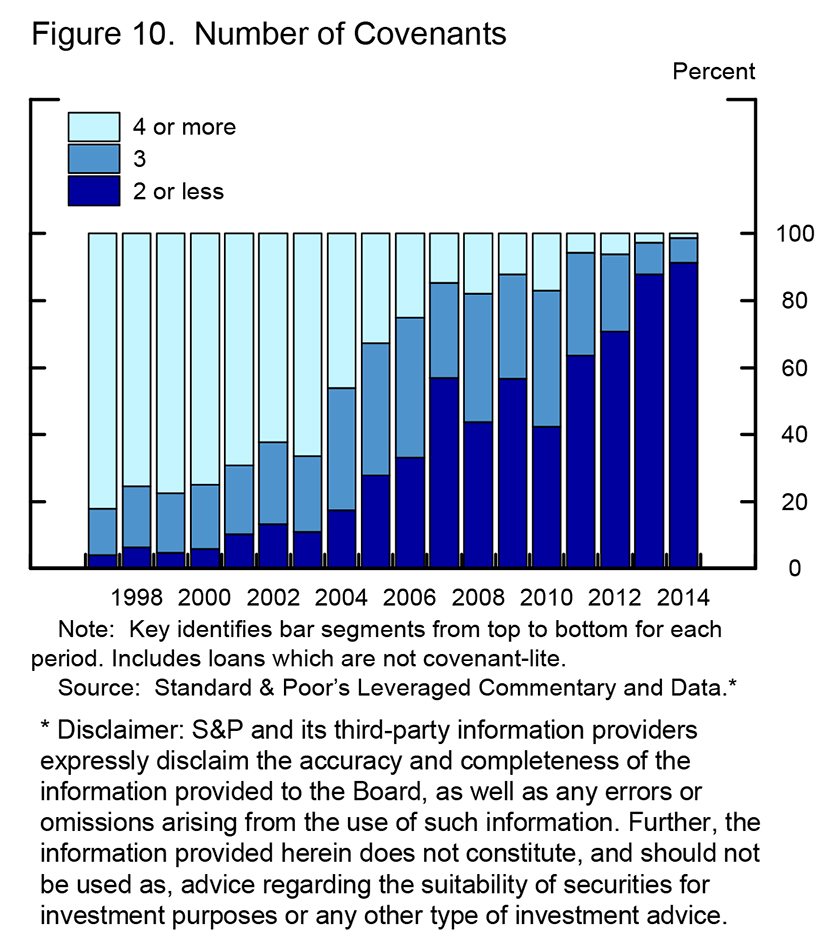

Let's now turn to post-crisis market conditions, which exhibit both similarities and differences compared with the pre-crisis period. Borrowing through leveraged loans by speculative-grade companies has been brisk since 2010, with about $800 billion of institutional loans now outstanding (figure 8). Over much of the post-crisis low interest rate period, demand for higher-yielding assets has been very strong, often outstripping supply. Price and nonprice terms in the syndicated leveraged loan market have been highly favorable to borrowers, as credit spreads declined, albeit not to particularly low levels (figure 4), and leverage multiples increased (figure 3). The share of loan agreements that lack traditional maintenance covenants increased to historic highs (figures 9 and 10).12

{kind=link}

{kind=link}

{kind=link}

CLOs and other stably funded investors continue to be the primary owners of leveraged loans. But in recent years, mutual funds that invest in fixed income assets have seen large inflows and have become more significant investors in this market. Some of these funds, including those holding syndicated leveraged loans and high-yield bonds, provide investors with what is called "liquidity transformation"--providing daily liquidity even when the underlying assets are relatively illiquid. The risk is that, in the event of a shock or a panic, investors will demand all of their money back at the exact time when the liquidity of the already illiquid underlying assets deteriorates even further. Investors may not anticipate or recognize this problem until it is too late--the so-called liquidity illusion.

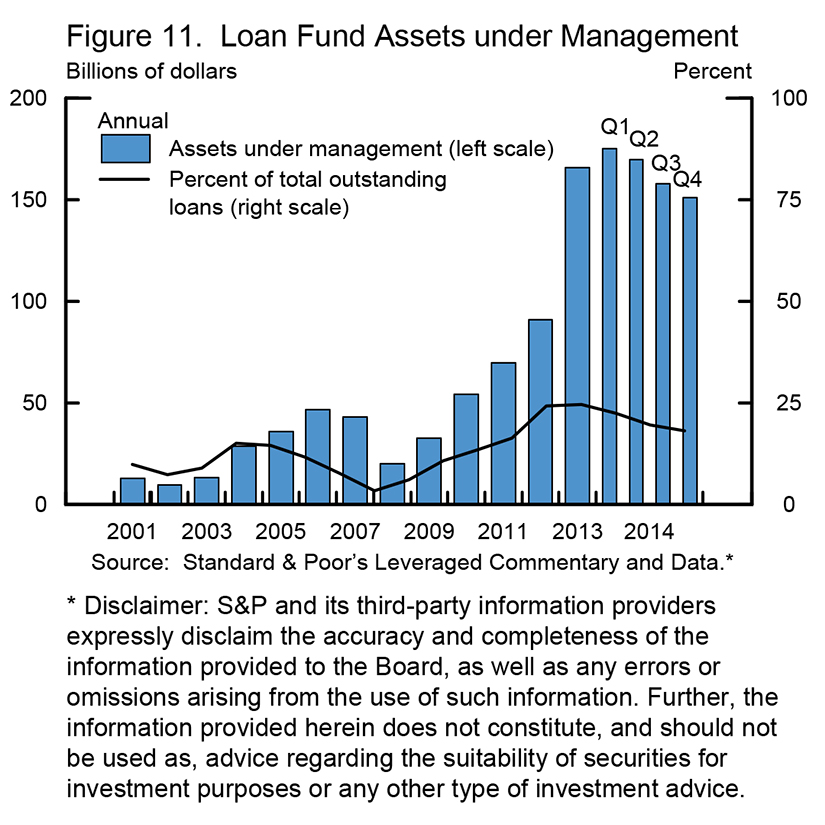

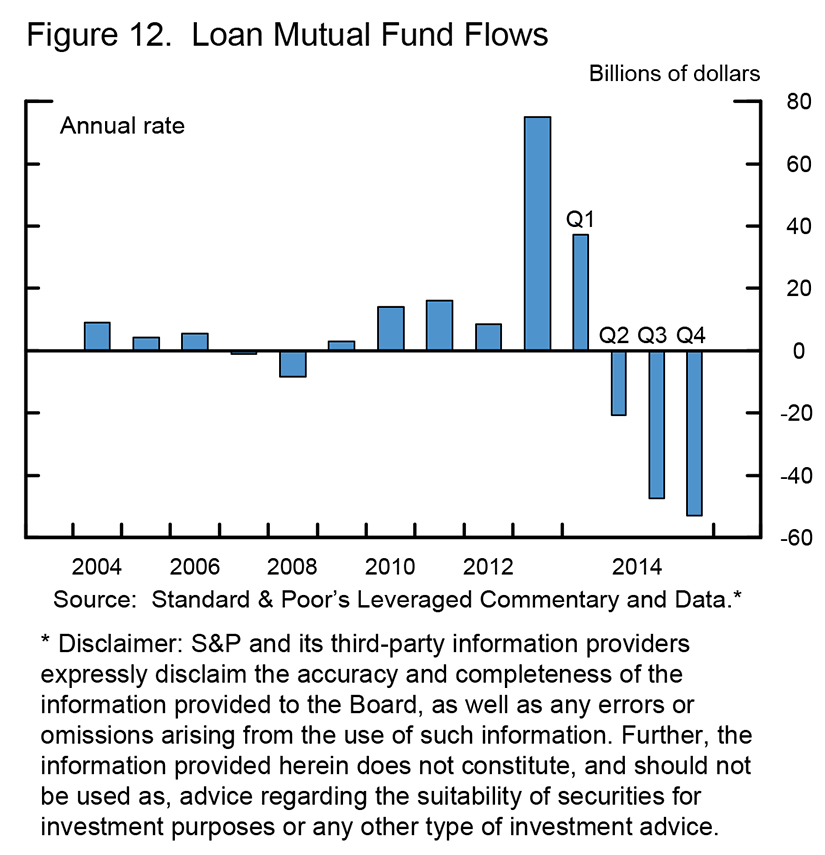

Bank loan funds, which attract retail investors and offer daily liquidity, now total about $150 billion, or 20 percent of institutional leveraged loans outstanding (figure 11). The liquidity transformation provided by these funds has not created problems so far despite recent outflows from bank loan funds, but supervisors and market participants have raised valid concerns that stressful times could well bring large-scale redemptions and threaten runs (figure 12). Chair Mary Jo White has made liquidity concerns regarding open-ended mutual funds a priority for the SEC.13

{kind=link}

{kind=link}

While it is possible to observe the characteristics of cash market investments, it is far more challenging to assess comparable positions in the derivatives and secured lending markets. Investors may take highly leveraged positions in leveraged loans through total return swaps and secured funding transactions, and a substantial buildup of these positions could present run and fire-sale risks if asset values started to fall. Today, the evidence suggests that such positions are fairly limited, but challenges in measurement and data make it hard to get a clear picture.

While some of these conditions evoke the pre-crisis bubble period and thus raise red flags, there are important differences as well. The large institutions that arrange these loans have significantly reduced both the size and duration of their leveraged loan commitments (figure 13). Thus, they are not exposed to the large "pipeline risk" they faced as the crisis broke. In addition, banks now routinely limit their risk by including "flex" provisions that, among other things, enable them to increase the interest rate on a loan offered for sale by 150 basis points or more, at the borrower's expense. So far, we have not seen the very large transactions of the pre-crisis period. In these and other respects, the leveraged finance markets have evolved, probably because of supervision as well as lessons learned by the banks themselves. Given these changes, banks at the core of our financial system seem less likely to experience stress should conditions in leveraged lending deteriorate. Of course, the guidance now stands in the way of a return to pre-crisis conditions.

{kind=link}

Let's now step back from the leveraged loan market to ask the broader question of how supervisors should address a clear deterioration of credit market conditions. I will consider three factors that are often discussed in considering the broader question of when and how to intervene in the credit markets to promote financial stability through institution-specific supervisory policy.14

First, do conditions present a threat to the safety and soundness of financial institutions at the core of the system?

It hardly needs saying that we must to be alert to the buildup of risks in the credit markets that could undermine the safety, soundness, or solvency of the G-SIBs or the broader system. If deterioration in one or more of the key credit markets would credibly raise such threats, the Fed and the other supervisors should react preemptively. An object lesson in this regard is the damage done by the accumulation of excessive exposures to high-risk MBS and other mortgage-related assets in the years leading up to the crisis. The originate-to-distribute model of mortgage lending on its face promised a social-welfare-enhancing distribution of mortgage credit risk away from banks and toward stable capital market investors. But the banks remained profoundly exposed through contractual putback rights, mortgage and MBS litigation, residual balance sheet holdings, and implicit support to sponsored investment vehicles.

Since the crisis, there have been significant and eminently justified legislative and regulatory actions to assure that mortgage originators follow minimum underwriting standards and that banks are better protected from exposure to high-risk mortgages. These efforts include the Dodd-Frank risk retention rules and ability-to-pay standards, much higher capital and liquidity requirements, stricter accounting rules that limit off-balance-sheet treatment for sponsored vehicles, and a much greater supervisory focus on litigation and reputational risk.

Second, is there use of run-prone financing by other investors that can lead to damaging fire sales?

Supervisors should be highly alert to the reemergence in the markets--that is, not on the balance sheets of the large banks--of structures that are prone to runs and damaging fire sales triggered by sharp declines in asset values. As I mentioned earlier, two different features can create vulnerability to runs and fire-sale risk. The first involves funding of volatile assets with high leverage that includes short-term, confidence sensitive debt. These structures were widely used before the crisis in the funding of MBS. The second involves "liquidity transformation," in which the investment structure provides investors daily liquidity, but the underlying assets are far less liquid and prone to becoming quite illiquid in times of stress. Either or both of these features can be replicated in the derivatives or securities lending markets, which provide less visibility to market participants and supervisors. Financial markets evolve constantly in response to market conditions, financial engineering, and regulation. It will be important to keep up with trends in these markets that may give rise to this threat.

Third, if left unaddressed, is it likely that conditions will risk meaningful damage to the real economy when the credit cycle turns?

A positive answer on either of the first two questions should raise red flags for supervisors. Let's say, for the sake of argument, that the answers to these questions were negative. One might still try to make the case for supervisory intervention into the credit markets to avoid the risk of meaningful damage to the economy down the road. History shows that excesses that occur at the height of a credit boom can result in substantial losses not just to financial firms and market investors, but also to households and businesses, when that boom turns to bust.15

The question of whether to "lean against" the credit cycle through supervisory policy--and when, and with what tools--is a difficult one.16 An important threshold question is whether supervisors will be able to correctly and in a timely manner identify "dangerous" conditions in credit markets, without too many false positives and without unnecessarily limiting credit availability by interfering with market forces. Interesting recent research seeks to identify observable variables that could be used to monitor credit conditions and detect trends that could threaten the performance of the real economy in the future.17 This research is promising, and it could be used by supervisors to inform their thinking as it develops further. In the meantime, unless there is a plausible threat to the core of the system or potential for damaging fire sales, I would set a high bar for supervisory interventions to lean against the credit cycle. Such interventions would almost surely interfere with the traditional function of capital markets in allocating capital to productive uses and dispersing risk to the investors who willingly choose to bear it.

Finally, another issue to consider when contemplating such intervention is that, particularly in the United States, activity is free to migrate outside the commercial banking system into less regulated entities. As supervisory scrutiny has increased in recent years, a growing number of nonbanks have become involved in the distribution of leveraged loans. Migration of this activity could be either a net positive or a net negative for financial stability, depending on whether it actually transfers risk irrevocably from the core of the financial system, and whether the institutions to which activity migrates rely on funding that is stable and robust to fire sale dynamics.

Conclusion

To wrap up, I believe that sustaining financial stability requires supervisors to consider financial markets, in addition to financial institutions and infrastructure. That is most obviously so when conditions threaten the safety and soundness of the financial system through leverage, liquidity transformation, or deterioration of credit underwriting or other risk-management standards. At the same time, financial stability need not seek to eliminate all risks. We need to learn, but not overlearn, the lessons of the crisis. I believe there should be a high bar for "leaning against the credit cycle" in the absence of credible threats to the core or the reemergence of run-prone funding structures. In my view, the Fed and other prudential and market regulators should resist interfering with the role of markets in allocating capital to issuers and risk to investors unless the case for doing so is strong and the available tools can achieve the objective in a targeted manner and with a high degree of confidence.

1. The views expressed here are my own and not necessarily those of others in the Federal Reserve System. Return to text

2. For more information, see Daniel K. Tarullo (2014), "Liquidity Regulation," speech delivered at the Clearing House 2014 Annual Conference, New York, November 20. Return to text

3. For a more complete treatment of these issues, see Daniel K. Tarullo (2015), "Advancing Macroprudential Policy Objectives," speech delivered at "Evaluating Macroprudential Tools: Complementarities and Conflicts," a conference cosponsored by the Office of Financial Research and the Financial Stability Oversight Council, held in Arlington, Va., January 30. Return to text

4. For more on this topic, see William C. Dudley (2014), "Welcoming Remarks at Workshop on the Risks of Wholesale Funding ," speech delivered at "Workshop on the Risks of Wholesale Funding," sponsored by the Federal Reserve Bank of New York, New York, August 13. Return to text

5. There have also been reforms to the money market funds that provide most of the funding in this market, as discussed later. Return to text

6. See Jerome H. Powell (2013), "OTC Market Infrastructure Reform: Opportunities and Challenges," speech delivered at the Clearing House 2013 Annual Meeting, New York, November 21; and Jerome H. Powell (2014), "A Financial System Perspective on Central Clearing of Derivatives," speech delivered at "The New International Financial System: Analyzing the Cumulative Impact of Regulatory Reform," a conference cosponsored by the Federal Reserve Bank of Chicago and the Bank of England, Chicago, November 6. Return to text

7. See Committee on Payment and Settlement Systems and Technical Committee of the International Organization of Securities Commissions (2012), Principles for Financial Market Infrastructures (PDF) (Basel, Switzerland: Bank for International Settlements and International Organization of Securities Commissions, April). Return to text

8. The 2014 SEC rule amendments are available at www.sec.gov/rules/final/2014/33-9616.pdf. Return to text

9. See, for example, Janet L. Yellen (2011), "Assessing Potential Financial Imbalances in an Era of Accommodative Monetary Policy," speech delivered at "Real and Financial Linkage and Monetary Policy," an international conference sponsored by the Bank of Japan, June 1. Return to text

10. See Board of Governors of the Federal Reserve System, Federal Deposit Insurance Corporation, and Office of the Comptroller of the Currency (2013), "Interagency Guidance on Leveraged Lending (PDF)," March 13. Return to text

11. Along with the Shared National Credit results, the Fed, along with the OCC and the FDIC, released on November 7, 2014, an FAQ document (PDF) regarding the guidance. Also see Board of Governors of the Federal Reserve System, Federal Deposit Insurance Corporation, and Office of the Comptroller of the Currency (2014), "Credit Risk in the Shared National Credit Portfolio Is High; Leveraged Lending Remains a Concern," joint press release, November 7.

The guidance covers a wide range of risk-management issues and generally aims tighter scrutiny at deals with leverage over six times pre-tax cash flow, or with forecast debt paydown of less than 50 percent over a five-to-seven-year period; differences across industries and companies are also to be taken into consideration. Return to text

12. Highly accommodative monetary policy, while far from the only cause of ebullient credit market conditions, is designed to support economic activity by creating incentives to take credit and duration risk. See Ben S. Bernanke (2013), "Semiannual Monetary Policy Report to the Congress," statement before the Committee on Banking, Housing, and Urban Affairs, U.S. Senate, February 26. Return to text

13. See Mary Jo White (2014), "Enhancing Risk Monitoring and Regulatory Safeguards for the Asset Management Industry," speech at the New York Times DealBook Opportunities for Tomorrow Conference, New York, December 11. Return to text

14. This approach is consistent with the financial stability framework in Adrian, Covitz, and Liang (2013), and emphasizes the importance of leverage, maturity transformation, and common risks and behaviors in the financial system that can amplify credit losses and harm the real economy. See Tobias Adrian, Daniel Covitz, and Nellie Liang (2013), "Financial Stability Monitoring," Finance and Economics Discussion Series 2013-21 (Washington: Board of Governors of the Federal Reserve System). Return to text

15. See, for example, Moritz Schularick and Alan M. Taylor (2012), "Credit Booms Gone Bust: Monetary Policy, Leverage Cycles, and Financial Crises, 1870-2008," American Economic Review, vol. 102 (2), pp. 1029-61. Return to text

16. The U.S. banking agencies, following the lead of the Basel Committee on Banking Supervision, created a countercyclical capital buffer that could be activated during periods of excess aggregate credit growth. The Basel proposal can both "lean against the cycle" and create a capital cushion to absorb losses from the likely increase in defaults. Return to text

17. See Robin Greenwood and Samuel G. Hanson (2013), "Issuer Quality and Corporate Bond Returns," Review of Financial Studies, vol. 26 (June), pp. 1483-525; and David López-Salido, Jeremy C. Stein, and Egon Zakrajšek (2014), "Credit-Market Sentiment and the Business Cycle (PDF)," slide presentation. Return to text