Speech

May 04, 2018

Original remarks as prepared for delivery

Liquidity Regulation and the Size of the Fed's Balance Sheet

Vice Chairman for Supervision Randal K. Quarles

At "Currencies, Capital, and Central Bank Balances: A Policy Conference," a Hoover Institution Monetary Policy Conference, Stanford University, Stanford, California

Thank you very much to the Hoover Institution for hosting this important conference and to John Taylor for inviting me to participate.1 In my capacity as both the Vice Chairman for Supervision at the Board of Governors and a member of the Federal Open Market Committee (FOMC), part of my job is to consider the intersection of regulatory and monetary policy issues, the subject of my discussion today. This topic is a very complex and dynamic nexus, especially as regulation and the implementation of monetary policy continue to evolve.

One important issue for policymakers, and the one that I will spend some time reflecting on today, is how post-crisis financial regulation, through its incentives for bank behavior, may influence the size of the Federal Reserve's balance sheet in the long run. Such a topic is admittedly difficult to address in the time we have today, so I will focus on a particular component of the regulation--the Liquidity Coverage Ratio (LCR)--and its link to banks' demand for U.S. central bank reserve balances. Besides illuminating this particular issue, I hope my discussion will help illustrate the complexities associated with the interconnection of regulatory and monetary policy issues in general. Also, let me emphasize at the outset that I will be touching on some issues that the Board and the FOMC are in the process of observing and evaluating and, in some cases, may be far from reaching any final decisions on. As such, my thoughts on these issues are my own and are likely to evolve, benefiting from further discussion and our continued monitoring of bank behavior and financial markets over time.

Monetary Policy and the Efficiency of the Financial System

Before I delve into the more complicated subject of how one type of bank regulation affects the Fed's balance sheet, let me say a few words about financial regulation and how it relates to monetary policy more generally. As I have said previously, I view promoting the safety, soundness, and efficiency of the financial system as one of the most important roles of the Board. So how is efficiency of the financial system connected to monetary policy? To put it in the simplest fashion, to the extent that the efficiency of the financial system is improved, it will improve the transmission of monetary policy to the real economy.

Improving efficiency of the financial system is not an isolated goal. The task is to enhance efficiency while maintaining the system's resiliency. Take, for example, the Board's two most recent and material proposals, the stress capital buffer and the enhanced supplementary leverage ratio (eSLR). The proposal to modify the eSLR, in particular, initially raised questions in the minds of some as to whether it would reduce the ability of the banking system to weather shocks. A closer look at the proposal shows that the opposite is true. The proposed change simply restores the original intent of leverage requirements as a backstop measure to risk-based capital requirements. As we have seen, a leverage requirement that is too high favors high-risk activities and disincentivizes low-risk activities.

We had initially calibrated the leverage ratio at a level that caused it to be the binding constraint for a number of our largest banks. As a result, those banks had an incentive to add risk rather than reduce risk in their portfolios because the capital cost of each additional asset was the same whether it was risky or safe, and the riskier assets would produce the higher return. The proposed recalibration eliminates this incentive by returning this leverage ratio to a level that is a backstop rather than the driver of decisions at the margin. Yet, because of the complex way our capital regulations work together--with risk-based constraints and stress tests regulating capital at both the operating and holding company levels--this improvement in incentives is obtained with virtually no change in the overall capital requirements of the affected firms. Federal Reserve staff estimate the proposal would potentially reduce capital requirements across the eight large banks subject to the proposal by $400 million, or 0.04 percent of the $955 billion in capital these banks held as of September 2017.2 So this recalibration is a win-win: a material realignment of incentives to reduce a regulatory encouragement to take on risk at a time when we want to encourage prudent behavior without any material capital reduction or cost to the system's resiliency. Taken together, I believe these new rules will maintain the resiliency of the financial system and make our regulation simpler and more risk sensitive.

Liquidity Regulations

Let me now back up to the time just before the financial crisis and briefly describe why liquidity regulations are necessary for banks. Banking organizations play a vital role in the economy in serving the financial needs of U.S. households and businesses. They perform this function in part through the mechanism of maturity transformation--that is, taking in short-term deposits, thereby making a form of short-term, liquid investments available to households and businesses, while providing longer-term credit to these same entities. This role, however, makes banking firms vulnerable to the potential for rapid, broad-based outflows of their funding (a so-called run), and these institutions must therefore balance the extent of their profitable maturity transformation against the associated liquidity risks.3 Leading up to the 2007-09 financial crisis, some large firms were overly reliant on certain types of short-term funding and overly confident in their ability to replenish their funding when it came due. Thus, during the crisis, some large banks did not have sufficient liquidity, and liquidity risk management at a broader set of institutions proved inadequate at anticipating and compensating for potential outflows, especially when those outflows occurred on a rapid basis.4

In the wake of the crisis, a combination of regulatory reforms and stronger supervision was needed to promote increased resilience in the financial sector. With regard to liquidity, the prudential regulations and supervisory programs implemented by the U.S. banking agencies have resulted in significant improvements in the liquidity positions and in the risk management of our largest institutions. And, working closely with other jurisdictions, we have also implemented global liquidity standards for the first time. These standards seek to limit the effect of short-term outflows and extended overall funding mismatches, thus improving banks' liquidity resilience.

One particular liquidity requirement for large banking organizations is the LCR, which the U.S. federal banking agencies adopted in 2014.5 The LCR rule requires covered firms to hold sufficient high-quality liquid assets (HQLA)--in terms of both quantity and quality--to cover potential outflows over a 30-day period of liquidity stress. The LCR rule allows firms to meet this requirement with a range of cash and securities and does not apply a haircut to reserve balances or Treasury securities based on the estimated liquidity value of those instruments in times of stress. Further, firms are required to demonstrate that they can monetize HQLA in a stress event without adversely affecting the firm's reputation or franchise.

The rules have resulted in some changes in the behavior of large banks and in market dynamics. Large banks have adjusted their funding profiles by shifting to more stable funding sources. Indeed, taken together, the covered banks have reduced their reliance on short-term wholesale funding from about 50 percent of total assets in the years before the financial crisis to about 30 percent in recent years, and they have also reduced their reliance on contingent funding sources. Meanwhile, covered banks have also adjusted their asset profiles, materially increasing their holdings of cash and other highly liquid assets. In fact, these banks' holdings of HQLA have increased significantly, from low levels at some firms in the lead-up to the crisis to an average of about 15 to 20 percent of total assets today.6 A sizable portion of these assets currently consists of U.S. central bank reserve balances, in part because reserve balances, unlike other types of highly liquid assets, do not need to be monetized, but also, importantly, because of the conduct of the Fed's monetary policy, a topic to which I will next turn.

How Does the LCR Interact with the Size of the Fed's Balance Sheet?

With this backdrop, a relevant question for monetary policymakers is, what quantity of central bank reserve balances will banks likely want to hold, and, hence, how might the LCR affect banks' reserve demand and thereby the longer-run size of the Fed's balance sheet? Let me emphasize that policymakers have long been aware of the potential influence that regulations may have on reserve demand and thus the longer-run size of the Fed's balance sheet. And, of course, regulatory influences on banks' behavior, my focus today, is just one of many factors that could affect policymakers' decisions regarding the appropriate long-run size of the Fed's balance sheet.7 In particular, in augmenting its Policy Normalization Principles and Plans, the FOMC stated in June 2017 that it "currently anticipates reducing the quantity of reserve balances, over time, to a level appreciably below that seen in recent years but larger than before the financial crisis" and went on to note that "the level will reflect the banking system's demand for reserve balances and the Committee's decisions about how to implement monetary policy most efficiently and effectively in the future."8

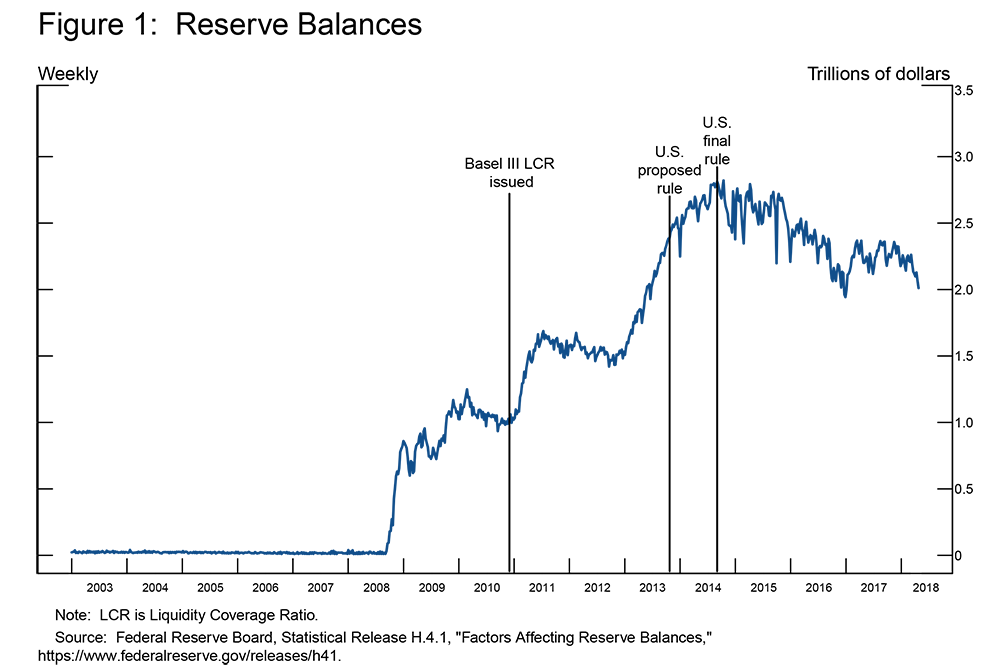

With that said, it is useful to begin by examining banks' current reserve holdings. Figure 1 plots the aggregate level of reserve balances in the U.S. banking system, starting well before the financial crisis. As you can see, the current level of reserves--at around $2 trillion--is many orders of magnitude higher than the level that prevailed before the financial crisis, a result of the Fed's large-scale asset purchase programs that aimed to mitigate the severe economic downturn and stem disinflationary pressures in the wake of the crisis. The vertical lines in the figure show key dates in the implementation of the LCR, including the initial Basel III international introduction of the regulation followed by its two-step introduction in the United States. A key takeaway from this figure is that the Fed was in the process of adding substantial quantities of reserve balances to the banking system while the LCR was being implemented--and these two changes largely happened simultaneously. As a result, banks, in aggregate, are currently using reserve balances to meet a significant portion of their LCR requirements. In addition, because these changes happened together, it is reasonable to conclude that the current environment is likely not very informative about banks' underlying demand for reserve balances.

{kind=link}

But now the situation is changing, albeit very slowly. Last October, the Fed began to gradually and predictably reduce the size of its balance sheet.9 The Fed is doing so by reinvesting the principal payments it receives on its securities holdings only to the extent that they exceed gradually increasing caps--that is, the Fed is allowing securities to roll off its portfolio each month up to a specific maximum amount. This policy is also reducing reserve balances. So far, after the first seven months of the program, the Fed has shed about $120 billion of its securities holdings, which is a fairly modest amount when compared with the remaining size of its balance sheet. Consequently, the level of reserves in the banking system is still quite abundant.

So, how many more reserve balances can be drained, and how small will the Fed's balance sheet get? Let me emphasize that this question is highly speculative--policymakers have not decided the desired long-run size of the Fed's balance sheet, nor, as I noted earlier, do we have a definitive handle on banks' long-run demand for reserve balances. Indeed, the FOMC has said that it "expects to learn more about the underlying demand for reserves during the process of balance sheet normalization."10 Nonetheless, let me spend a little time reflecting on this challenging question.

How banks respond to the Fed's reduction in reserve balances could, in theory, take a few different forms. One could envision that as the Fed reduces its securities holdings, a large share of which consists of Treasury securities, banks would easily replace any reduction in reserve balances with Treasury holdings, thereby keeping their LCRs roughly unchanged. According to this line of thought, because central bank reserve balances and Treasury securities are treated identically by the LCR, banks should be largely indifferent to holding either asset to meet the regulation. In that case, the reduction in reserves and corresponding increase in Treasury holdings might occur with relatively little adjustment in their relative rates of return. Alternatively, one could argue that banks may have particular preferences about the composition of their liquid assets. And since banks are profit-maximizing entities, they will likely compare rates of return across various HQLA-eligible assets in determining how many reserves to hold. If relative asset returns are a key driver of reserve demand, then interest rates across various types of HQLA will adjust on an ongoing basis until banks are satisfied holding the aggregate quantity of reserves that is available.

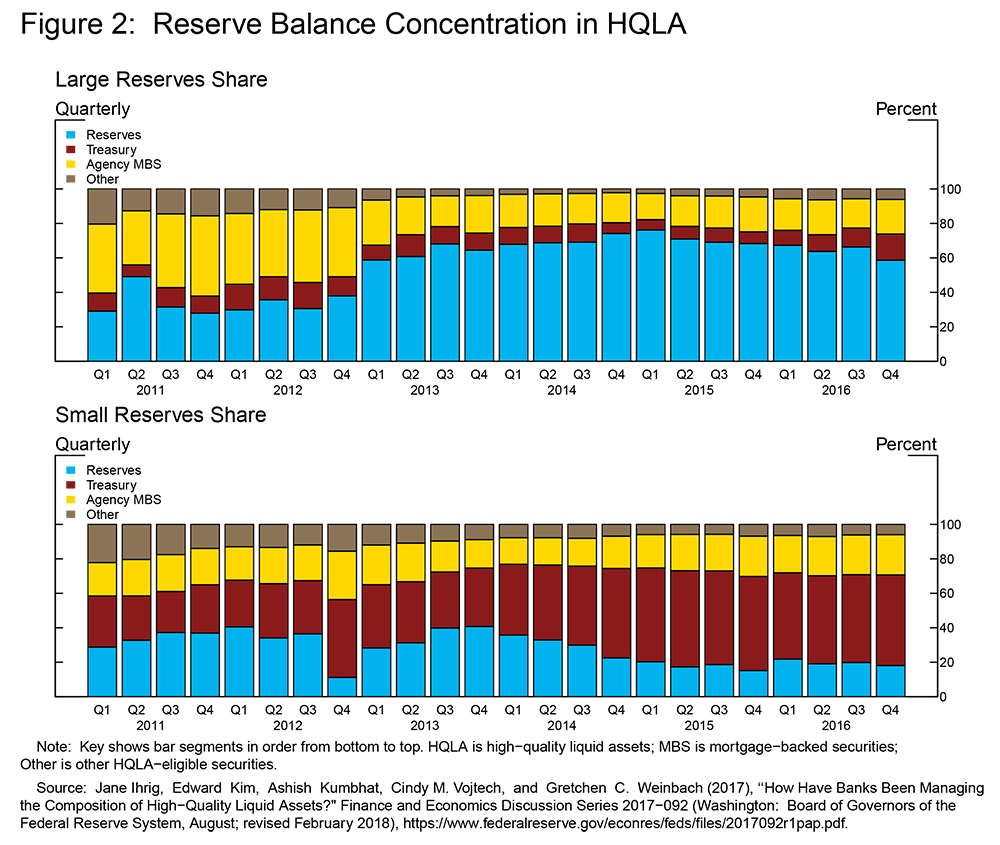

Recent research by the Board staff shows that banks currently display a significant degree of heterogeneity in their approaches to meeting their LCR requirements, including in their chosen volumes of reserve balances.11 Figure 2 shows a subset of this research to illustrate this point. The top and bottom panels represent estimates of how two large banks have been meeting their HQLA requirements over time. In each panel, the blue portions of the bars denote the share of HQLA met by reserve balances, while the red, yellow, and brown slices of the bars represent the share met by Treasury securities, agency mortgage-backed securities, and other HQLA-eligible assets, respectively. Despite holding roughly similarly amounts of HQLA, the two banks exhibit very different HQLA compositions, with the bank depicted in the top panel consistently holding a much larger share of HQLA in the form of reserve balances than the bank shown in the bottom panel. This finding suggests that there likely is no single "representative bank" behavioral model that can capture all we might want to know about banks' demand for central bank reserve balances.

{kind=link}

Some of the differences we see in bank behavior likely relate to banks' individual liquidity needs and preferences. Indeed, banks manage their balance sheets in part by taking into account their internal liquidity targets, which are determined by the interaction between the specific needs of their various business lines and bank management's preferences. In any case, this picture illustrates the complexities that are inherent in understanding banks' underlying demand for reserve balances, a topic for which more research would be quite valuable to policymakers.

So, what does this finding say about the longer-run level of reserve balances demanded by banks? The answer is that there is a large degree of uncertainty. In fact, the Federal Reserve Bank of New York surveyed primary dealers and market participants last December to solicit their views about the level of reserves they expect to prevail in 2025.12 A few features of the survey responses stand out. All respondents thought that the longer-run level of reserve balances would be substantially lower than the current level of more than $2 trillion. In addition, there appeared to be a widely held view that the longer-run level of reserves will be significantly above the level that prevailed before the financial crisis. But even so, the respondents did not agree about what that longer-run level will be, with about half anticipating a level ranging between $400 billion and $750 billion.

It is important to point out that the Fed's balance sheet will remain larger than it was before the crisis even after abstracting from the issue of banks' longer-run demand for reserve balances. The reason is that the ultimate size of the Fed's balance sheet also depends on developments across a broader set of Fed liabilities. One such liability is the outstanding amount of Federal Reserve notes in circulation--that is, paper money--which has doubled over the past decade to a volume of more than $1.6 trillion, growing at a rate that generally reflects the pace of expansion of economic activity in nominal terms. Other nonreserve liabilities have also grown since the crisis, including the Treasury Department's account at the Fed, known as the Treasury's General Account. Recent growth in such items means that the longer-run size of the Fed's balance sheet will be noticeably larger than before the crisis regardless of the volume of reserve balances that might ultimately prevail.

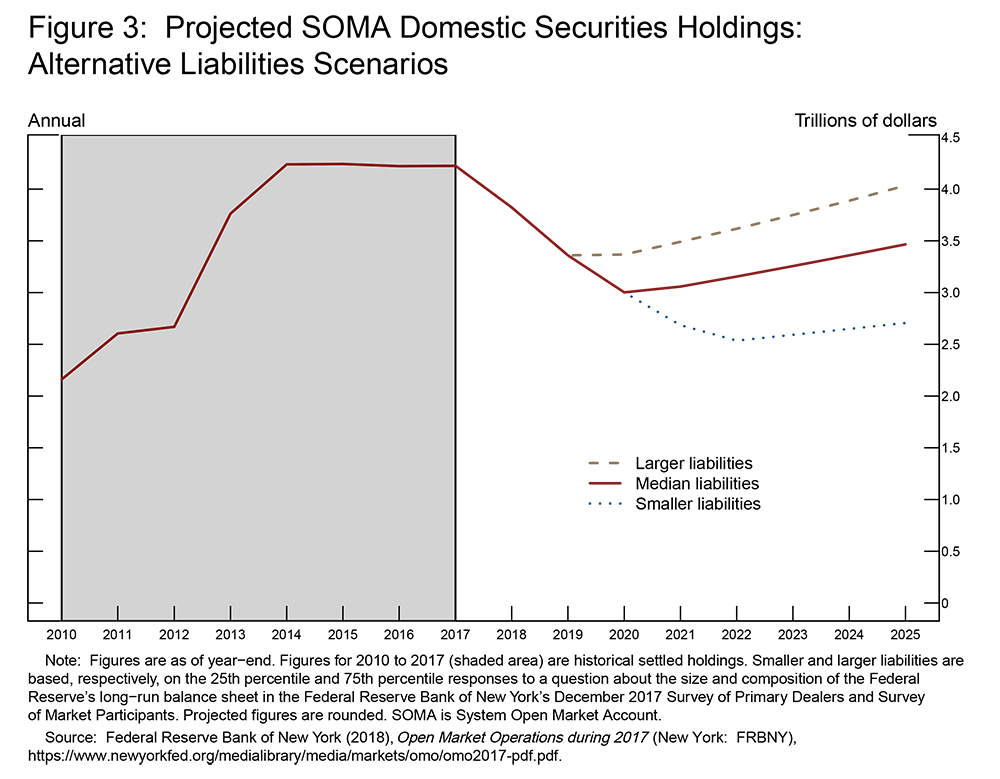

Putting the various pieces together, figure 3 illustrates how the overall size of the Fed's balance sheet may evolve. Given the uncertainties I have described, I have chosen to show three different scenarios, drawn from the most recent annual report released by the Federal Reserve Bank of New York, which was published last month.13 These scenarios highlight the degree to which the longer-run size of the Fed's domestic securities portfolio--also known as the System Open Market Account, or SOMA, which accounts for the vast majority of the Fed's assets--will be affected by choices about the future level of reserve balances and the evolution of nonreserve liabilities. The assumptions underlying the scenarios are based on the distribution of responses from the surveys I described earlier, as those surveys also asked respondents to forecast the likely longer-run levels of several liabilities on the Fed's balance sheet other than reserves. The "median" scenario, represented by the red (middle) line in the figure, is based on the 50th percentile of survey responses, while the "larger" and the "smaller" scenarios, denoted by the gold dashed (top) and blue dotted (bottom) lines, are based on the 75th and 25th percentiles, respectively.

{kind=link}

The figure illustrates that the Fed's securities holdings are projected to decline about $400 billion this year and another $460 billion next year as Treasury and agency securities continue to roll off gradually from the Fed's portfolio. The kink in each curve captures what the FOMC has referred to as the point of "normalization" of the size of the Fed's balance sheet--that is, the point at which the balance sheet will begin to expand again to support the underlying growth in liabilities items such as Federal Reserve notes in circulation. All else being equal, greater longer-run demand for currency, reserve balances, or other liabilities implies an earlier timing of balance sheet normalization and a higher longer-run size of the balance sheet, as illustrated by the top line. And the converse--smaller demand for these liabilities and a later timing of normalization, illustrated by the bottom line--is also possible. In the three scenarios shown, the size of the Fed's securities portfolio normalizes sometime between 2020 and 2022. That is quite a range of time, so as the balance sheet normalization program continues, the Fed will be closely monitoring developments for clues about banks' underlying demand for reserves.

What will the Fed be monitoring as reserves are drained and the balance sheet shrinks? I would first like to emphasize that the Fed regularly monitors financial markets for a number of reasons, so I do not mean to imply that we will be doing anything that is very much different for our normal practice. As reserves continue to be drained, we will want to gauge how banks are managing their balance sheets in continuing to meet their LCRs, watching in particular how the distribution of reserve balances across the banking system evolves as well as monitoring any large-scale changes in banks' holdings of other HQLA-eligible assets, including Treasury securities and agency mortgage-backed securities.

And on the liabilities side of banks' books, we will be keeping our eye on both the volume and the composition of deposits, as there are reasons why banks may take steps, over time, to hold onto certain types of deposits more than others. In particular, retail deposits may be especially desired by banks going forward because they receive the most favorable treatment under the LCR and also tend to be relatively low cost.

Retail deposits have grown quite a bit since the crisis, especially in light of the prolonged period of broad-based low interest rates and accommodative monetary policy, limiting the need for banks to compete for this most stable form of deposits. However, the combination of rising interest rates and the Fed's shrinking balance sheet, together with banks' ongoing need to meet the LCR, may alter these competitive dynamics.

Of course, importantly, deposits will not necessarily decline one-for-one with reserve balances as the Fed's balance sheet shrinks. The overall effects of the decline in the Fed's balance sheet will depend both on who ultimately ends up holding the securities in place of the Fed and on the full range of portfolio adjustments that other economic agents ultimately make as a result.14

We will also be monitoring movements in interest rates. In part, we will be tracking how the yields and spreads on the various assets that banks use to meet their LCR requirements evolve. For example, to the extent that some banks will wish to keep meeting a significant portion of their LCR requirements with reserves, the reduction in the Fed's balance sheet and the associated drop in aggregate reserves could eventually result in some upward pressure on the effective federal funds rate and on yields of Treasury securities. This situation could occur if some banks eventually find that they are holding fewer reserves than desired at a given constellation of interest rates and, in response, begin to bid for more federal funds while selling Treasury securities or other assets. Interest rates will adjust up until banks are indifferent with regard to holding the relatively smaller volume of reserves available in the banking system.

Overall, policymakers will be monitoring to make sure that the level of reserves the Fed supplies to the banking sector, which influences the composition of assets and liabilities on banks' balance sheets as well as market interest rates, provides the desired stance of monetary policy to achieve the FOMC's dual mandate of maximum employment and stable prices. Of course, we will need to be very careful to understand the precise factors that underlie any significant movements in these areas, because factors that are unrelated to the Fed's balance sheet policies might also cause such adjustments.

Conclusion

To conclude, I would like to reemphasize that I have touched on some highly uncertain issues today--issues that, I would like to stress again, have not been decided by the FOMC. One such issue that closely relates to my remarks today, and one I believe the upcoming panel will likely address, is which policy implementation framework the Fed should use in the long run. That is, broadly speaking, should the Fed continue to use an operational framework that is characterized by having relatively abundant reserves and operate in what is termed a "floor regime," or should it use one in which the supply of reserves is managed so that it is much closer to banks' underlying demand for reserves as in a "corridor regime"?

Of course, a host of complex issues underlie this decision, so I would just like to emphasize two general points. First, a wide range of quantities of reserve balances--and thus overall sizes of the Fed's balance sheet--could be consistent with either type of framework. Second, while U.S. liquidity regulations likely influence banks' demand for reserves, the Fed is not constrained by such regulations in deciding its operational framework, because U.S. banks will be readily able to meet their regulatory liquidity requirements using the range of available high-quality liquid assets, of which reserve balances is one type.

Importantly, additional experience with the Federal Reserve's policy of gradually reducing its balance sheet will help inform policymakers' future deliberations regarding issues related to the long-run size of the Fed's balance sheet, issues that will not need to be decided for some time.

The final and most general point is simply to underscore the premise with which I began these remarks: Financial regulation and monetary policy are, in important respects, connected. Thus, it will always be important for the Federal Reserve to maintain its integral role in the regulation of the financial system not only for the visibility this provides into the economy, but precisely in order to calibrate the sorts of relationships we have been talking about today.

1. The views I express here are my own and not necessarily those of the Federal Reserve Board or the Federal Open Market Committee. Return to text

2. Required capital at the bank subsidiaries of these firms would be reduced by larger amounts--and would only allow the firm to move that capital to different subsidiaries within the firm--but, more importantly, the overall capital regime prevents this capital from being distributed out of the banking organization as a whole except in this de minimis amount. Thus, the overall organization retains the same capital levels without the structure of capital regulation creating an incentive to add risk to the system. Return to text

3. While deposit insurance helps mitigate the incentive for many depositors to run, it cannot fully eliminate this risk. For a discussion of this vulnerability, see Douglas W. Diamond and Philip H. Dybvig (1983), "Bank Runs, Deposit Insurance, and Liquidity," Journal of Political Economy, vol. 91 (June), pp. 401-19. Return to text

4. See Senior Supervisors Group (2009), Risk Management Lessons from the Global Banking Crisis of 2008 (PDF) (New York: Federal Reserve Bank of New York, October). Return to text

5. For a full description of the U.S. LCR, including which banks are covered, see Regulation WW--Liquidity Risk Management Standards, 12 C.F.R. pt. 249 (2017). Return to text

6. See Jane Ihrig, Edward Kim, Ashish Kumbhat, Cindy M. Vojtech, and Gretchen C. Weinbach (2017), "How Have Banks Been Managing the Composition of High-Quality Liquid Assets? (PDF)" Finance and Economics Discussion Series 2017-092 (Washington: Board of Governors of the Federal Reserve System, August; revised February 2018). Return to text

7. For example, a separate factor that is relevant for policymakers in this regard is the FOMC's choice of long-run framework for monetary policy implementation. For policymakers' discussions of this factor, see Board of Governors of the Federal Reserve System (2016), "Minutes of the Federal Open Market Committee, July 26-27, 2016," press release, August 17; and Board of Governors of the Federal Reserve System (2016), "Minutes of the Federal Open Market Committee, November 1-2, 2016," press release, November 23, Return to text

8. See Board of Governors of the Federal Reserve System (2017), "FOMC Issues Addendum to the Policy Normalization Principles and Plans," press release, June 14, paragraph 6. Return to text

9. The FOMC announced this change to its balance sheet policy in its September 2017 postmeeting statement; see Board of Governors of the Federal Reserve System (2017), "Federal Reserve Issues FOMC Statement," press release, September 20. Return to text

10. See Board of Governors, "FOMC Issues Addendum," paragraph 6, in note 7. Return to text

11. See Ihrig and others, "Managing the Composition of High-Quality Liquid Assets," in note 5. Return to text

12. The December 2017 Survey of Primary Dealers is available on the Federal Reserve Bank of New York's website at https://www.newyorkfed.org/medialibrary/media/markets/survey/2017/dec-2017-spd-results.pdf. The December 2017 Survey of Market Participants is available at https://www.newyorkfed.org/medialibrary/media/markets/survey/2017/dec-2017-smp-results.pdf. Return to text

13. See Federal Reserve Bank of New York (2018), Open Market Operations during 2017 (New York: FRBNY, April), available at https://www.newyorkfed.org/markets/annual_reports.html. Among other things, the report reviews the conduct of open market operations and other developments that influenced the System Open Market Account of the Federal Reserve in 2017. Return to text

14. For a discussion of the overall effects of the decline in the Fed's balance sheet, see Jane Ihrig, Lawrence Mize, and Gretchen C. Weinbach (2017), "How Does the Fed Adjust Its Securities Holdings and Who Is Affected? (PDF)" Finance and Economics Discussion Series 2017-099 (Washington: Board of Governors of the Federal Reserve System, September). Return to text