FEDS Notes

July 15, 2021

Does the Age at Which a Consumer Gets Their First Credit Matter? Credit Bureau Entry Age and First Credit Type Effects on Credit Score

Lucas Nathe1

Introduction

The consumer credit market plays a prominent role in the financial life of U.S. households. Consumers' credit histories and, in particular, their credit scores are key factors that determine their access to credit and the price at which they borrow. Consumers with little or no credit history often have limited access to the credit market and face higher borrowing costs. Therefore, it is important for consumers to start building their credit histories as early as they can. While having borrowed will help create one's credit file, borrowing early does not necessarily result in higher credit scores or better access to credit. The type of credit borrowed and young individuals' ability to repay that debt are also important factors.

This note presents some statistics regarding the distribution of the ages of consumers as they are added to credit reporting data and the longer-term implications of their entry-age and initial credit type. Specifically, using the Federal Reserve Bank of New York Consumer Credit Panel/Equifax (hereafter the CCP), I document the age distribution as consumers enter the credit bureau data and study whether age of entry is associated with their long-term credit score outcomes. I find that those who entered the data at age 18 have a substantially higher average credit score at age 30 than those who entered at age 19 or 20. I then document differences in credit score growth among young people based on their first credit type, finding that individuals whose first consumer credit is a student loan or a credit card fare better than those who initially take out other forms of credit. Finally, I present suggestive evidence that late entry into the credit bureau data could reflect an individual's immigration to the United States.

Entry into Credit Bureau Data

The CCP is a consumer-level nationally representative panel data set that contains detailed and anonymized individual credit records for 5 percent of U.S. consumers with a credit file. The longitudinal structure allows me to identify the quarter an individual first appears in the sample (the entry time). The CCP data contain rich credit history information, including Equifax Risk Score. 2

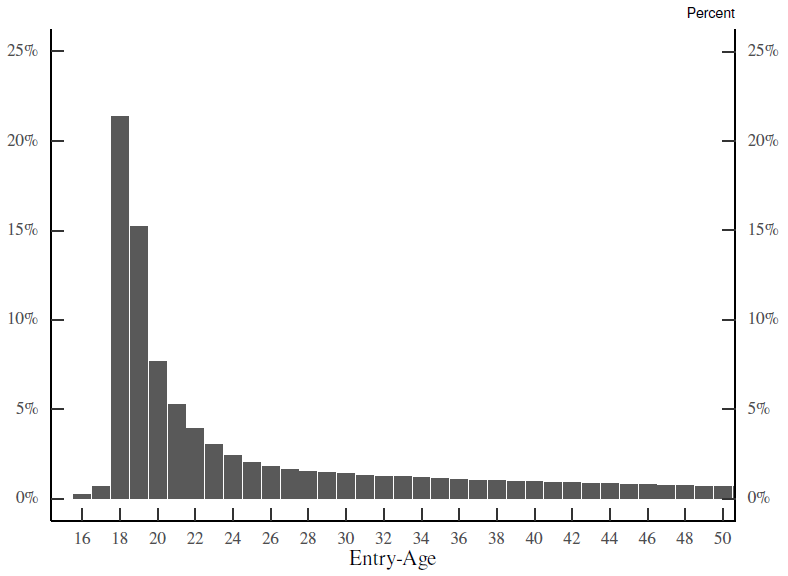

The data also have information on birth year but not the exact date of birth. Accordingly, I define an individual's age at a point in time as the difference between the year of the credit report and their birth year and follow Debbaut, Ghent, and Kudlyak (2014) to focus on the fourth quarter of a given year. I find that over 70 percent of consumers in the CCP entered before age 30 (figure 1). In particular, the three ages that see the most entries are 18, 19, and 20, whereas consumers entering younger than 18 account for a trivial share of the sample. However, it is noteworthy that 30 percent of consumers in the CCP entered after turning 30 years old. Later in the note, I explore factors that may be related to such late entries.

Note: The percent of observations that enter the CCP by age. The ages shown are limited to 16-50, while percentages are calcaulted across all ages. Individuals entering the CCP after age 50 represent 11% of all observations.

Source: Federal Reserve Bank of New York Consumer Credit Panel/Equifax.

Patterns in Credit Score by Age

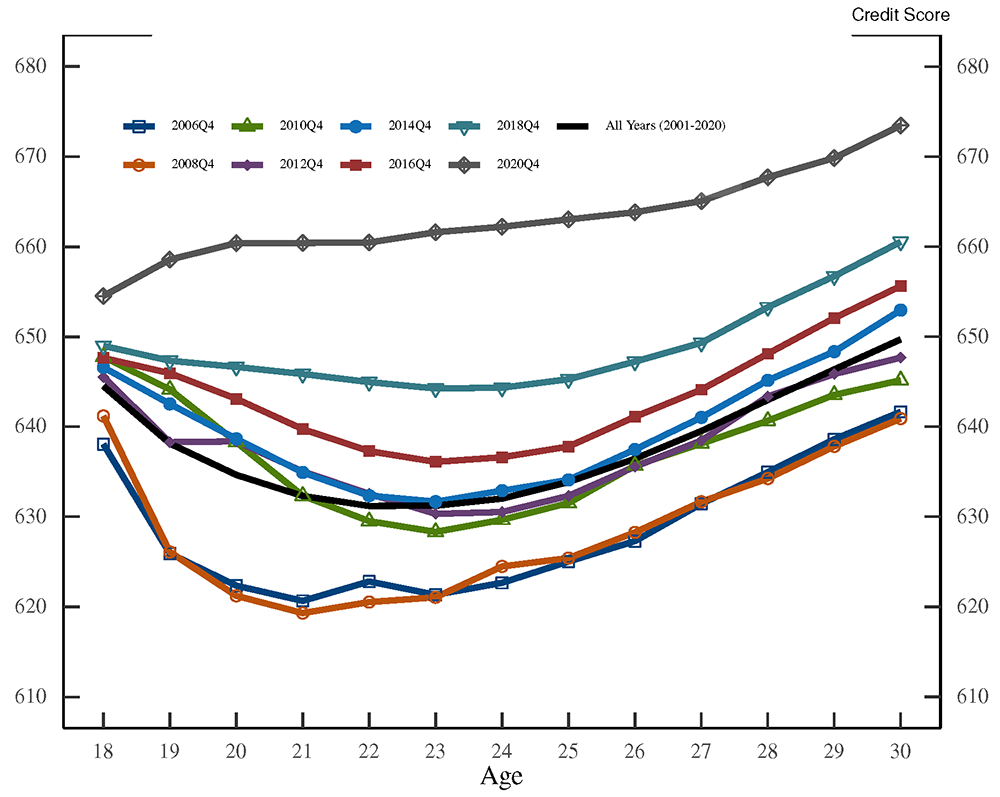

Focusing on young individuals, figure 2 shows the average credit scores for individuals aged 18 to 30 years old, irrespective of when they enter the panel. The black line, which plots the mean across all years, indicates that the average credit score of consumers starts around 645; it then declines to below 630 by age 23, before recovering in later years. While this drop in credit score is consistent across most years, it is more pronounced in the early years of the sample. The rise in average credit score across all ages over time is broadly consistent with previous research on credit score migrations (see Goodman and Ramos, 2019)3, and the significant increase in credit scores in 2020 likely reflected the Coronavirus Aid, Relief, and Economic Security Act's forbearance provisions.4

Source: Federal Reserve Bank of New York Consumer Credit Panel/Equifax

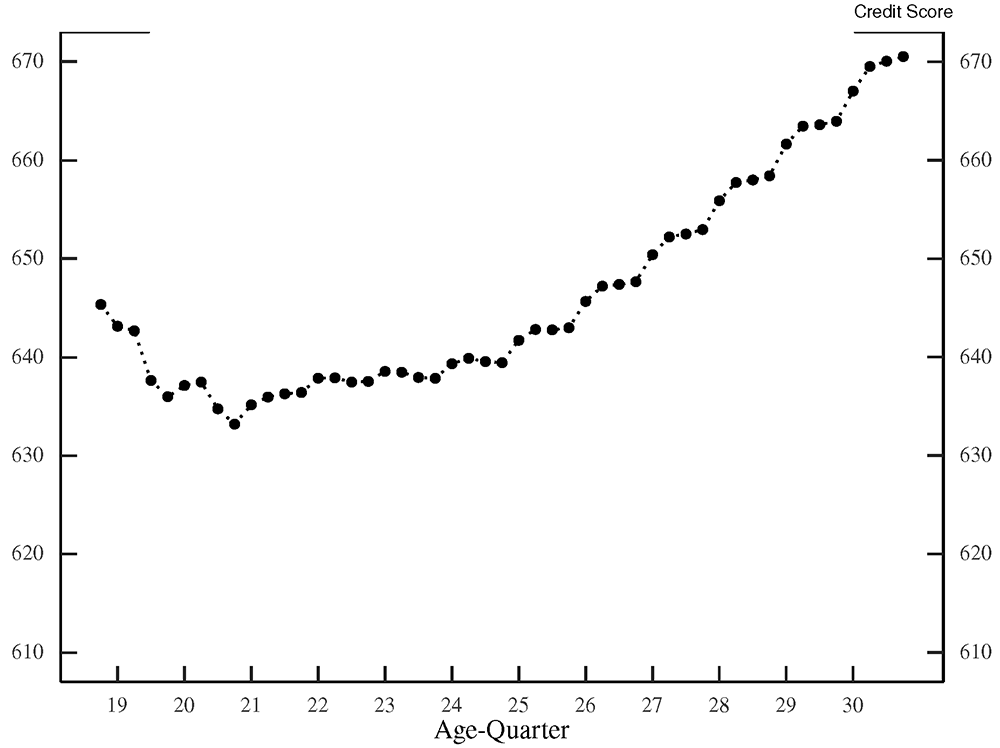

I then take a balanced panel of 18-year-olds who remained in the sample for 49 quarters until they were 30 years old. These individuals must have entered the sample between 2001 and 2008 in order to have turned 30 by 2020:Q4, the last quarter in the sample. Figure 3 displays the average credit score among these individuals. Both figures 2 and 3 show an initial drop in average credit score over an individual's first few years in the sample. It is also noteworthy that there exists a large gap between the average credit score of consumers aged 30 years old in the general cross section (646) and the average credit score of consumers aged 30 years old who entered the credit bureau data at age 18 (669), indicating a potential benefit of starting one's credit history at an early age. Individuals entering the credit bureau data at different ages may experience different longer-term credit outcomes, a possibility that I explore in the next section.

Note: Average credit score of individuals who enter the sample at age 18 and remain in the sample until age 30.

Source: Federal Reserve Bank of New York Consumer Credit Panel/Equifax

Long Term Effects of Entry-Age

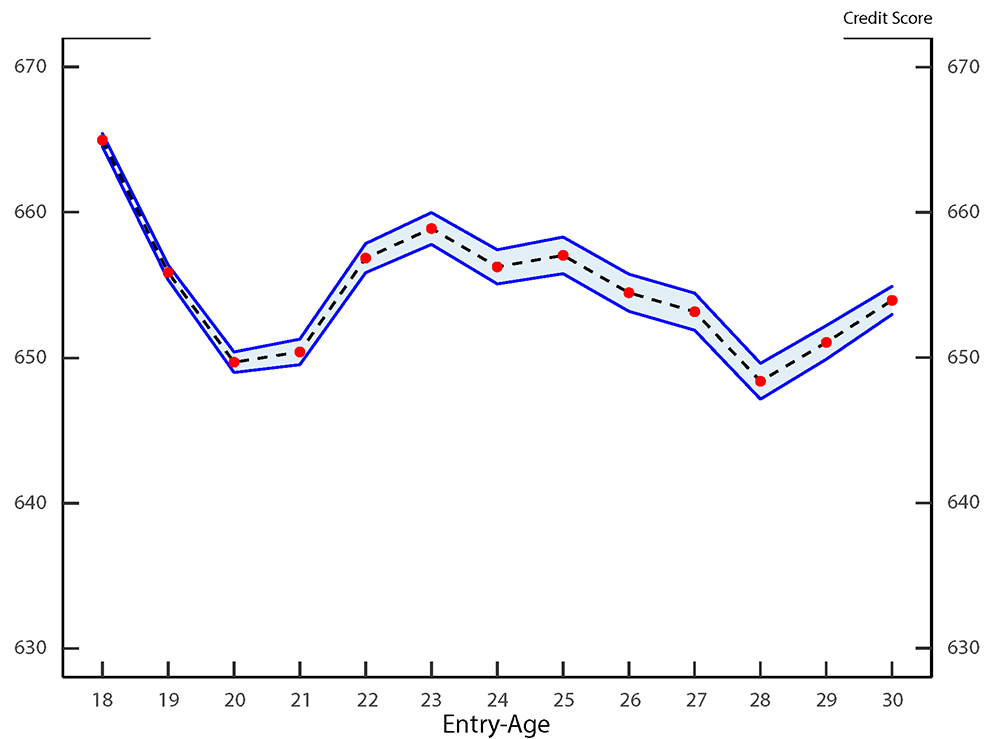

While a longer history in the credit market may be correlated with a higher credit score as figure 3 suggests, systematic differences may also exist between those who enter the data at different ages. In figure 4, I plot the average credit score of 30-year-old consumers by the age in which they entered the data. Figure 4 suggests that a significant credit score gap exists among those who enter the CCP between ages 18 and 20, a group representing nearly half of all individuals entering the CCP. Specifically, at age 30, those who entered at age 18 have an average credit score 10 points higher than those who entered at age 19 and 18 points higher than those who entered at age 20. The relationship between credit score at age 30 and the age of entry into the data is not monotonic. Consumers who entered at age 23 have a higher average credit score at age 30 than those who entered at a slightly younger or older age. However, consumers who entered the CCP at these ages represent a much smaller share of the sample than those who entered before age 20.

Note: Average credit score of individuals at age 30 by the age they enter the Consumer Credit Panel, within a 95 percent confidence interval.

Source: Federal Reserve Bank of New York Consumer Credit Panel/Equifax

Patterns in Credit Score by Type

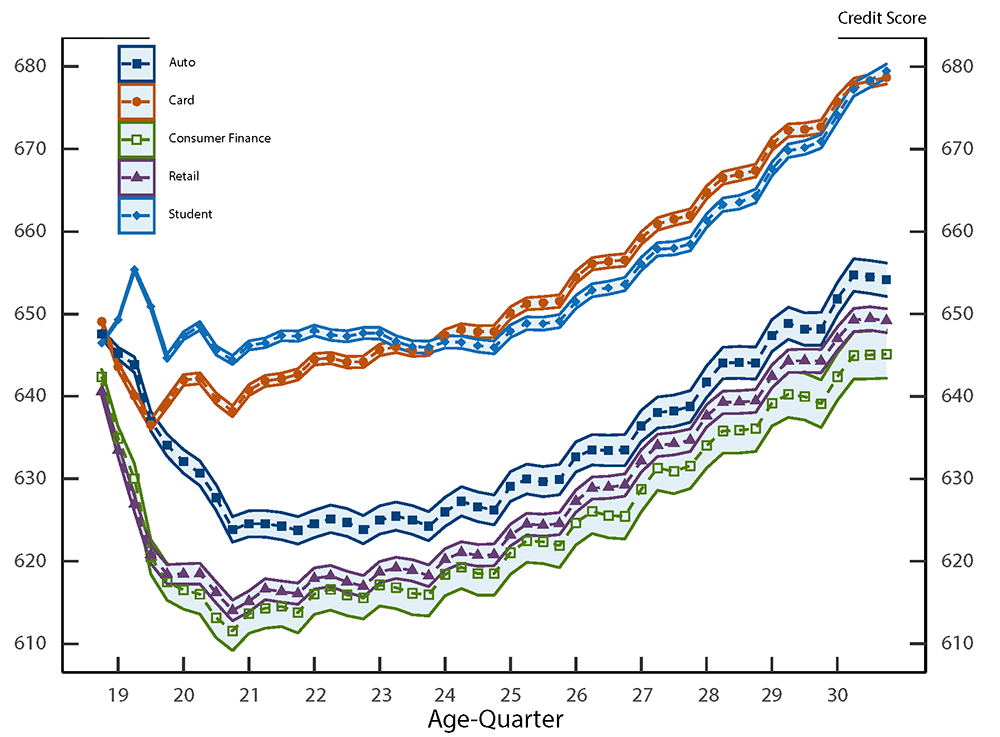

There may also be systematic differences between individuals based on the type of credit they first use. A young borrower who needs to take out a car loan to get to work is likely to have a different credit experience than a student whose parents take out a credit card in their name for the purpose of building credit. In figure 5 I plot the credit score evolution of individuals who enter the CCP at 18 and remain in the sample until the age of 30 by the type of credit they first took out. I set the first credit type of an individual to the first account with a positive balance, and when more than one first credit type is opened within the same quarter, I set the first credit type to be the account with a larger balance. Removing individuals who first opened more than one account within the same quarter does not affect results. I also drop all borrowers who first took out a mortgage loans as they represent only 0.11 percent of observations. Figure 5 shows that, with the exception of student loan borrowers, young borrowers often experience credit score decreases in the first few years of their credit history followed by subsequent increases. Further, initial credit card and student loan borrowers exhibit a much steeper growth in credit score than other types of borrowers.

Note: Average credit score of individuals who enter the sample at age 18 and remain in the sample until age 30 by first credit type within a 95 percent confidence interval.

Source: Federal Reserve Bank of New York Consumer Credit Panel/Equifax.

Late Entries into Credit Bureau Data

As noted earlier, around 30 percent of individuals enter the CCP after the age of 30. Late entry into the credit bureau data could reflect an individual's recent immigration to the United States and receipt of a social security number. The primary sample of the CCP is restricted to individuals whose credit file contains a social security number. Therefore, only U.S. citizens, permanent residents, and temporary working residents will be included in the CCP. As suggested by Lee & van der Klaauw (2010), individuals may enter the credit bureau data later in life after immigrating to the United States.

I provide some support for this hypothesis by calculating the correlation between the percent of individuals who enter the CCP after age 30 and the percent of non-citizens in a county in the American Community Survey. Results are shown in table 1. I find a strong positive relationship between the percent of late entries into the panel and the percent of non-citizens as well as a negative relationship with the percent of U.S. citizens within a county. Further, I find a positive relationship between late entries and the percent of naturalized citizens within a county.5 Taken together these correlations suggest that immigration to the United States and subsequent receipt of a social security number may cause people to enter the credit bureau data, particularly later in life.

Table 1: Late-Entry & Immigration

| County Population | Correlation |

|---|---|

| Naturalized Citizen | 0.256 |

| Non-citizen | 0.345 |

| U.S. Citizen | -0.312 |

Note: Correlation of the percent of individuals who entered the CCP after age 30 in a county from 2010 - 2018 with a county's citizenship composition in that year.

Source: Federal Reserve Bank of New York Consumer Credit Panel/ Equifax; American Community Survey

Conclusion

Success in building a credit history is a key determinant to an individual's access to credit later in life. I document the timing of entry into credit bureau data and find suggestive evidence that early entry into the data may differentially influence individuals' credit scores based on their age at that time. I find that more than 70 percent of individuals enter by the time they are 30, with 18 and 19-year-olds representing the largest share of any age. It also appears that there may be a benefit to one's credit score specifically associated with entering the data at 18 years of age. Further, the type of credit a young borrower first takes out also appears to be related to important factors that determine future access to credit. Of those who enter the data after turning 30 years old, there is suggestive evidence that they may have entered the data as a result of immigration to the United States. This analysis will inform future research using credit bureau data and will shed light on the dynamics of credit score evolution.

References

Debbaut, Peter and Ghent, Andra C. and Kudlyak, Marianna (2013). “Are Young Borrowers Bad Borrowers?” Working Paper Series 13-09R. Richmond: Federal Reserve Bank of Richmond, July (revised June 2014).

Goodman, Sarena, and Steve Ramos (2019). "Understanding Changes in Household Debt by Credit Risk Category: The Role of Credit Score Transitions," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, June 25, 2019.

Goodman, Sarena, Geng Li, Alvaro Mezza, and Lucas Nathe (2021). "Developments in the Credit Score Distribution over 2020," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, April 26, 2021.

Lee, Donghoon and van der Klaauw, H. Wilbert (2010). “An Introduction to the FRBNY Consumer Credit Panel (PDF),” Staff Report 479. New York: Federal Reserve Bank of New York, November

1. I thank Geng Li for providing valuable guidance, encouragements, and comments. Return to text

2. For a detailed description of the data please see Lee and van der Klaauw (2010). Return to text

3. Goodman and Ramos, (2019) find that in mid-2018, the share of prime- and subprime- scored borrowers were at their highest and lowest levels, respectively, since 2001. Return to text

4. See Goodman, Li, Mezza, and Nathe (2021) for a detailed description of credit score increases among the bottom decile of the credit score distribution in 2020, and credit attributes effected by the CARES act. Return to text

5. All correlations are statistically significant at the 99 percent confidence level. Return to text

Nathe, Lucas (2021). "Does the Age at Which a Consumer Gets Their First Credit Matter? Credit Bureau Entry Age and First Credit Type Effects on Credit Score," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, July 09, 2021, https://doi.org/10.17016/2380-7172.2918.

Disclaimer: FEDS Notes are articles in which Board staff offer their own views and present analysis on a range of topics in economics and finance. These articles are shorter and less technically oriented than FEDS Working Papers and IFDP papers.