FEDS Notes

June 22, 2017

Auto Financing during and after the Great Recession

More than half of auto financing is originated by non-bank finance companies that typically rely on short-term funding markets for their own financing. During the recent financial crisis, disruptions in these short-term financing markets reduced the availability of auto credit to consumers, which contributed to the decline in auto sales (Benmelech, Meisenzahl, and Ramcharan, 2017).

This note describes the new data on sources of auto financing that was used in (Benmelech, Meisenzahl, and Ramcharan (2017). In that paper, we linked the collapse in new auto sales during the Great Recession to the reduced availability of auto loans. We plan to publish and regularly update these data on sources of auto financing, with geographical detail, as a part of the Enhanced Financial Accounts (EFAs) initiative. The EFAs were created to complement the Financial Accounts of the United States by providing a more detailed and timely picture of financial intermediation in the United States (Gallin and Smith, 2014).

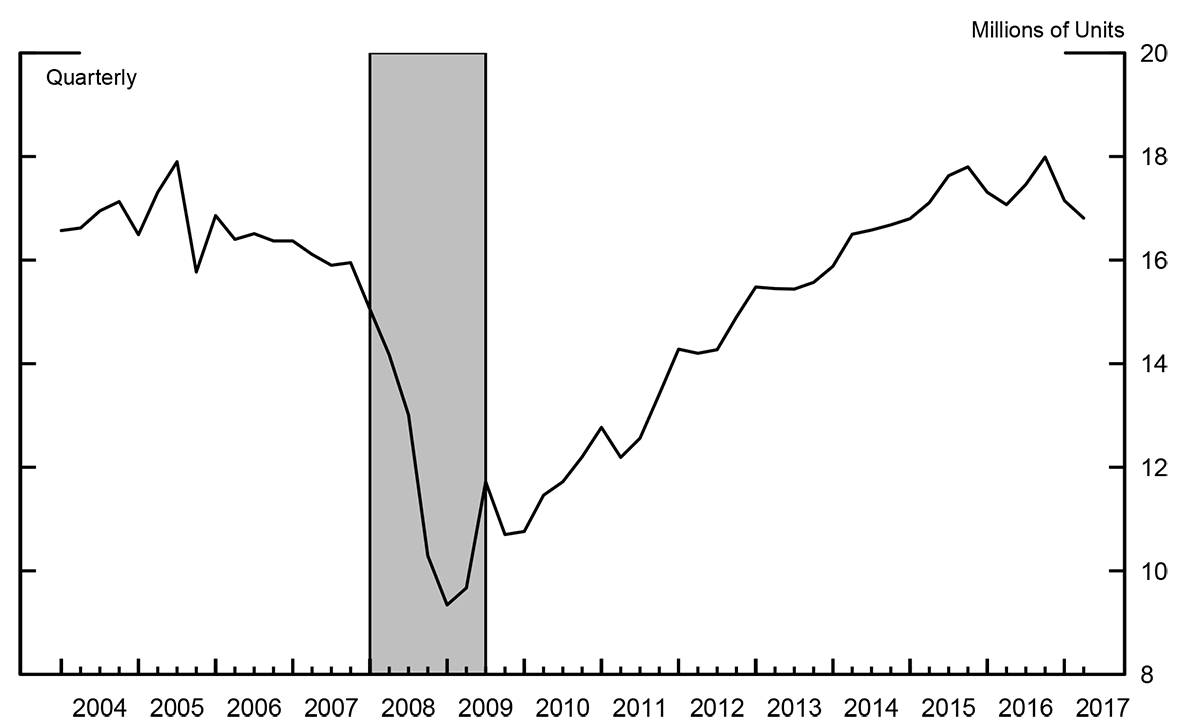

Shaded area indicates a recession period (December 2007 – June 2009) as dated by the National Bureau of Economic Research (NBER).

Source: Ward's Automotive Group. AutoInfoBank. http://wardsauto.com/miscellaneous/wards-autoinfobank

Figure 1 shows the annualized car sales per quarter. In 2007, before funding of finance companies dried up, U.S. households bought about 16 million new cars at an annual rate. Financial intermediaries, such as banks, credit unions, and finance companies provided financing for most of these retail purchases. When the financial crisis hit, retail auto sales collapsed to 7.9 million at an annual rate in 2009:Q1. A potential reason for this sharp decline in auto sales was the reduced availability of auto loans, especially around the collapse of General Motors Acceptance Corp and Chrysler Financial Inc. in fall 2008.

Historically, captive finance companies (finance companies owned by auto manufacturers,) have been major providers of car loans. These captive finance companies, such as General Motors Acceptance Corp, founded in 1919, emerged as a response to the lack of widely available financing options for consumer durable goods purchases.2 Auto manufacturers sold their cars nationwide but found no obvious partner to provide financing because the banking system at the time was highly fragmented due to branching regulation. Local banks were reluctant to make loans for car purchases because the underlying collateral is hard to value. Moreover, bankers generally resisted making loans for consumption fearing that credit might discourage the virtue of thrift (Phelps 1952).3 Vertically integrated captive finance companies addressed informational frictions regarding the collateral value and made car loans available nationwide.

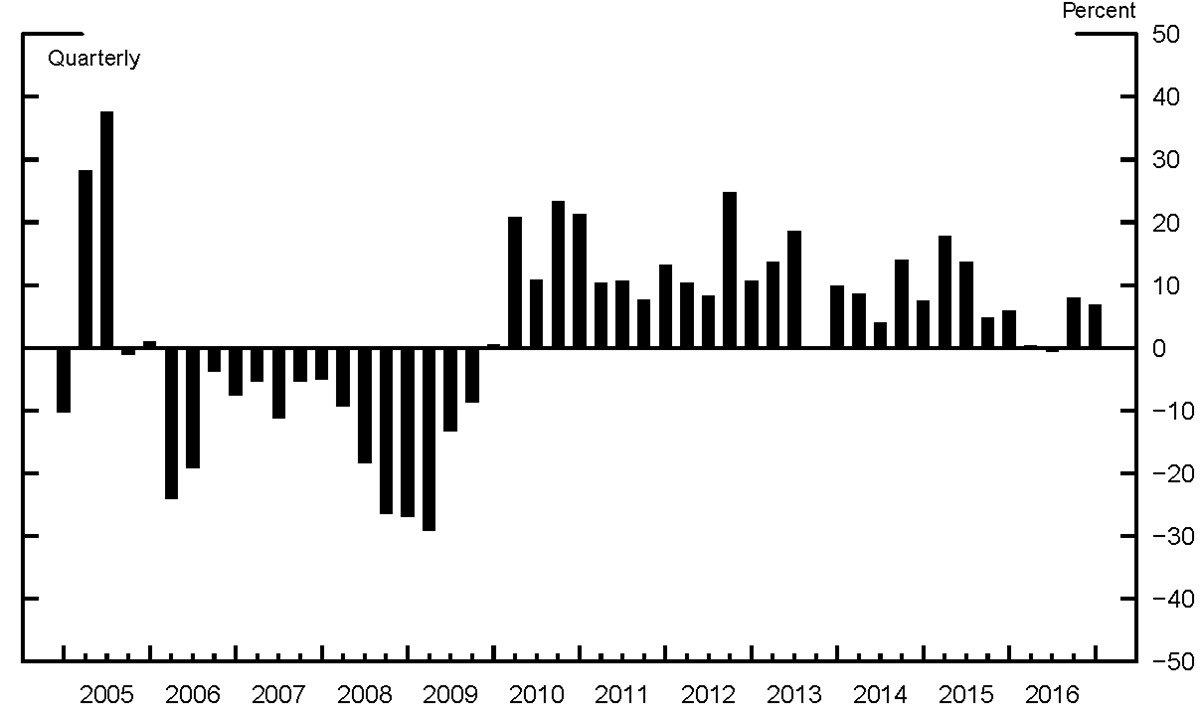

Source: FRBNY Consumer Credit Panel/Equifax Data

Auto loan balances totaled $1.1 trillion in 2016. Banks, credit unions, and finance companies are the major lenders in the auto credit market. Figure 2 shows the year-over-year growth rates in total new auto loan originations. Loan originations dropped by almost 30 percent (year-over-year) during the financial crisis. While these aggregate figures suggest that financial intermediaries play an important role in consumption and auto sales, they mask potential variation in how different financing sources are used across the United States. Unmasking this variation can be crucial to understanding the effects of financial sector shocks on auto sales. For instance, the collapse of General Motors Acceptance Corp and Chrysler Financial Inc. in fall 2008 may have had the greatest impact on car sales in counties in which consumers relied most heavily on those companies (as opposed to banks or credit unions) for financing their car purchases. We use new data to examine the regional variation in the sources of auto financing.

We use a proprietary data set from R. L. Polk & Company that records all new car registrations in the United States, which very closely resemble sales reported by the manufacturers. Beginning in 2002, for each new car purchased in the United States, the data set identifies the vehicle make and model and the type of buyer (retail, corporation, or government). Since this note focuses on household consumption, corporate and government transactions are excluded from the analysis below. For 2008:Q1 to 2013:Q4, the data also include the lender name. If the lender name is missing, we assume it is a cash purchase. In the upcoming EFA project, we plan to provide county-level information on the share of car sales financed by finance companies, banks, credit unions, and cash from 2008:Q1 to 2013:Q4, as illustrated in the chart below.

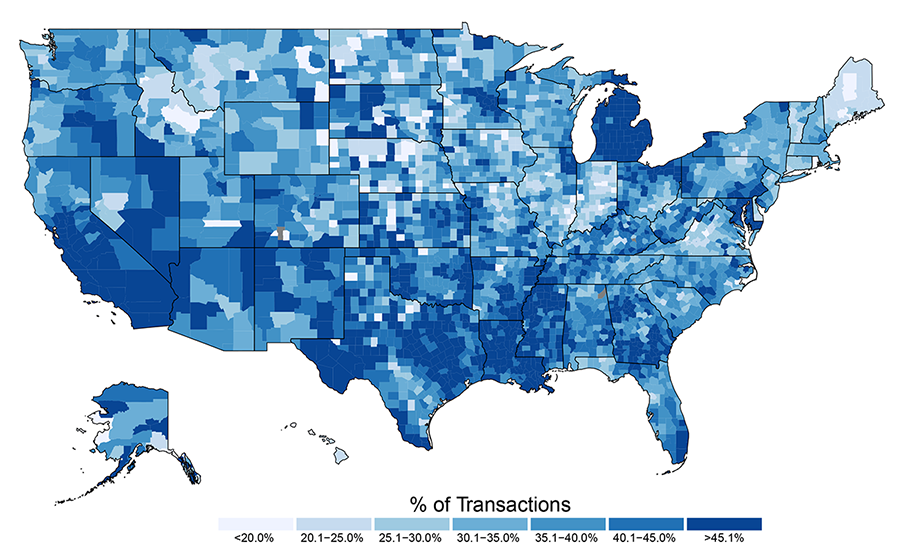

Source: IHS. Polk's New Vehicle Registration Data. https://www.ihs.com/btp/polk.html

Prior research suggests that banks and finance companies target different segments of the market for car loans (Barron, Chong, and Staten, 2008). Finance companies also tend to dominate where auto manufacturers have a presence, for instance in Michigan and Tennessee. Figure 3 shows the county-level share of retail new cars financed by finance companies in the first quarter of 2008. The market share of finance companies exhibits considerable spatial variation, suggesting that the collapse of captive finance companies in fall 2008 had widely heterogeneous effects on car sales across counties.

Source: IHS. Polk's New Vehicle Registration Data. https://www.ihs.com/btp/polk.html

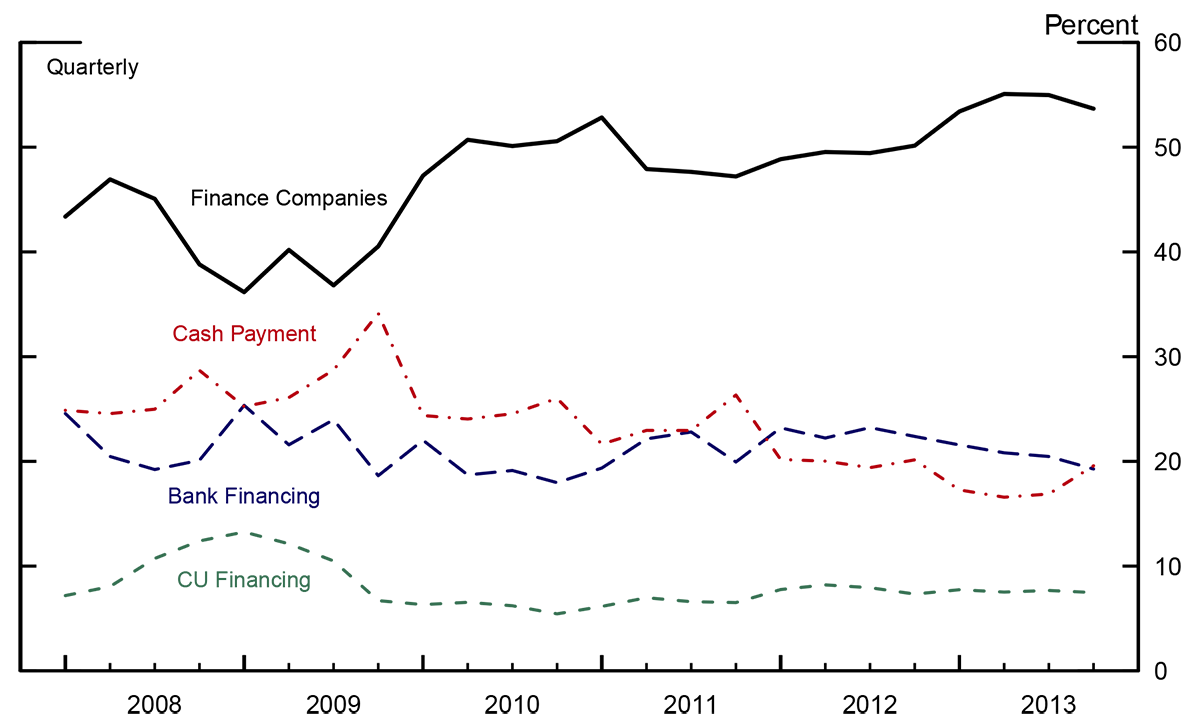

Unlike banks and credit unions, which rely mostly on deposits for funding, finance companies raise funds in short-term funding markets, for instance, by issuing asset-backed commercial paper (ABCP), and through on- and off-balance sheet securitization (Benmelech, Meisenzahl, and Ramcharan, 2017). Specifically, finance companies use ABCP facilities to warehouse auto loans before issuing ABS and to obtain funding for new loans.4 Auto loan-related ABCP is typically bought by money market funds and amounted to about $40 billion in 2006. After the Lehman Brothers bankruptcy led the Reserve Primary Fund to "break the buck" on September 16, 2008, money market funds experienced large outflows and pulled back from ABCP, and finance companies were unable to finance themselves from that source. As a result, General Motors Acceptance Corp and Chrysler Financial Inc. collapsed, and other finance companies sharply reduced their origination of car loans. When credit from finance companies dried up, consumers were more likely to finance their cars with loans from credit unions, banks, or cash payments (figure 4).5

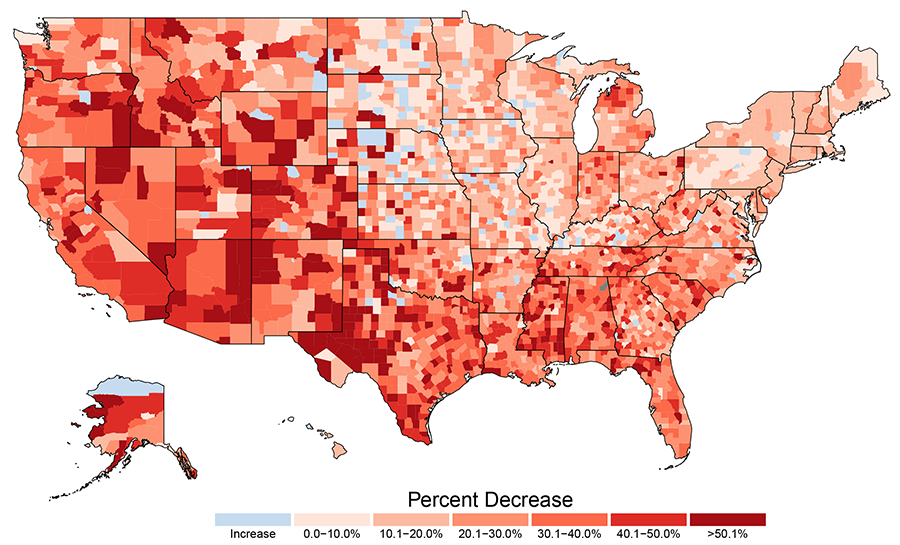

Source: IHS. Polk's New Vehicle Registration Data. https://www.ihs.com/btp/polk.html

Overall, new auto sales fell 21 percent nationwide between 2008 and 2009. However, as shown in Figure 5, the decline in car sales was uneven across the country; the southern and western regions suffered the most significant declines, while the reduction in sales appears to be modest in the Northeast. Comparing figures 3 and 5 reveals that the largest declines in retail car sales appear to have taken place in counties that relied most heavily on auto loans from finance companies. Indeed, using the county-level variation in the captive financing market share, Benmelech, Meisenzahl, and Ramcharan (2017) find that reductions in finance company car loan origination induced by the collapse of the ABCP market might explain about 31 percent of the drop in car sales in 2009 relative to 2008 even with the unprecedented interventions aimed at unfreezing short-term funding markets in 2008 and 2009, as well as the bailout of the U.S. automakers and their financing arms.6

Conclusion

A considerable share of consumer credit is originated by nonbanks that rely on short-term funding markets. During the financial crisis, counties in which consumers historically relied most on nonbank financing for auto purchases exhibited the largest drop in auto sales. These new data on the evolution of source of auto loans during the financial crisis on the county level allow researchers to better understand the heterogeneous effect of shocks to credit suppliers on consumption.

Data

County-level data on finance company, bank, credit union, and cash share (CSV)

References

Acharya, Viral V., Phillip Schnabl, and Gustavo Suarez. 2011. "Securitization without Risk Transfer," Journal of Financial Economics, 107,515–536.

Barron, John M., Byung-Un Chong, and Michael E. Staten. 2008. "Emergence of Captive Finance Companies and Risk Segmentation in Loan Markets: Theory and Evidence," Journal of Money, Credit and Banking 40,173–192.

Benmelech, Efraim, Ralf R. Meisenzahl, and Rodney Ramcharan. 2017. "The Real Effects of Liquidity during the Financial Crisis: Evidence from Automobiles." Quarterly Journal of Economics 132, 132-147.

Campbell, Sean, Daniel Covitz, William Nelson, and Karen Pence. 2011. "Securitization Markets and Central Banking: An Evaluation of the Term Asset-Backed Securities Loan Facility," Journal of Monetary Economics, 58, 518–531.

Hyman, Louis. 2011. Debtor Nation: The History of America in Red Ink. Princeton: Princeton University Press.

Mian, Atif, Kamalesh Rao, and Amir Sufi. 2013. "Household Balance Sheets, Consumption and the Economic Slump," Quarterly Journal of Economics, 128, 1687–1726.

Mian, Atif and Sufi, Amir 2014. What Explains the 2007–2009 Drop in Employment? Econometrica, 82: 2197–2223.

Olney, Martha L. (1991). Buy Now, Pay Later: Advertising, Credit, and Consumer Durables in the 1920's. Chapel Hill: University of North Carolina Press.

Phelps, Clyde William. 1952. The Role of the Sales Finance Companies in the American Economy. Baltimore: Commercial Credit.

Ramcharan, Rodney, Stephane Verani, and Skander J. Van den Heuvel (2016). "From Wall Street to Main Street: The Impact of the Financial Crisis on Consumer Credit Supply," Journal of Finance, vol. 71, no. 3, pp. 1323-1356.

1. I would like to thank Marco Cagetti, Geng Li, Maria Perozek, Paul Smith, and Dan Vine for helpful comments. Bryan Kevan provided excellent research assistance. Return to text

2. Olney (1991) documents the emergence of consumer credit for durable purchases in the 1920s more generally and highlights the importance of financing provided by the manufacturer. Return to text

3. The seasonality in car sales also affected the ability of dealers to finance their inventory (Hyman 2011). Return to text

4. For a detailed discussion of ABCP structures, see Acharya, Schnabl, and Suarez (2011). Return to text

5. Later in the financial crisis, credit unions had to absorb losses from corporate credit unions and subsequently reduced lending (Ramcharan, Verani, and Van den Heuvel, 2016). Return to text

6. Deleveraging by households--a reduction in demand--is another factor causing consumer spending to fall (Mian and Sufi (2014), Mian, Rao and Sufi (2013)). Return to text

Meisenzahl, Ralf R. (2017). "Auto Financing during and after the Great Recession," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, June 22, 2017, https://doi.org/10.17016/2380-7172.2015.

Disclaimer: FEDS Notes are articles in which Board staff offer their own views and present analysis on a range of topics in economics and finance. These articles are shorter and less technically oriented than FEDS Working Papers and IFDP papers.