FEDS Notes

September 04, 2019

Does Trade Policy Uncertainty Affect Global Economic Activity?

Dario Caldara, Matteo Iacoviello, Patrick Molligo, Andrea Prestipino, and Andrea Raffo1

Trade negotiations and proposals for a new approach to trade policy have become the focus of increased attention among investors, politicians, and market participants. While it is possible that negotiations will eventually lead to a more open and fair global competitive landscape, developments so far have resulted in an increase in uncertainty about the outlook for global trade. Higher uncertainty could lead firms to delay their investment and reduce their hiring, lower consumer confidence and spending, and ultimately curtail economic activity around the world.2

In this note, we first document the recent rise in trade policy uncertainty, henceforth TPU, by using two complementary measures based on text-search analysis: one focusing on newspapers articles, and another constructed from transcripts of firms' earnings calls. We then use econometric evidence on the joint movements in aggregate TPU, industrial production, and other macroeconomic and financial variables in order to provide an estimate of the effects of the recent spikes in TPU on U.S. GDP, as well as GDP in advanced foreign economies (AFEs) and emerging market economies (EMEs).

We find that the rise in TPU in the first half of 2018 accounts for a decline in the level of global GDP of about 0.8 percent by the first half of 2019. Had trade tensions not escalated again in May and June 2019, the drag on GDP would have subsequently started to ease. However, renewed uncertainty since May of 2019 points to additional knock-on effects that may push down GDP further in the second half of 2019 and in 2020.

Measurement of TPU

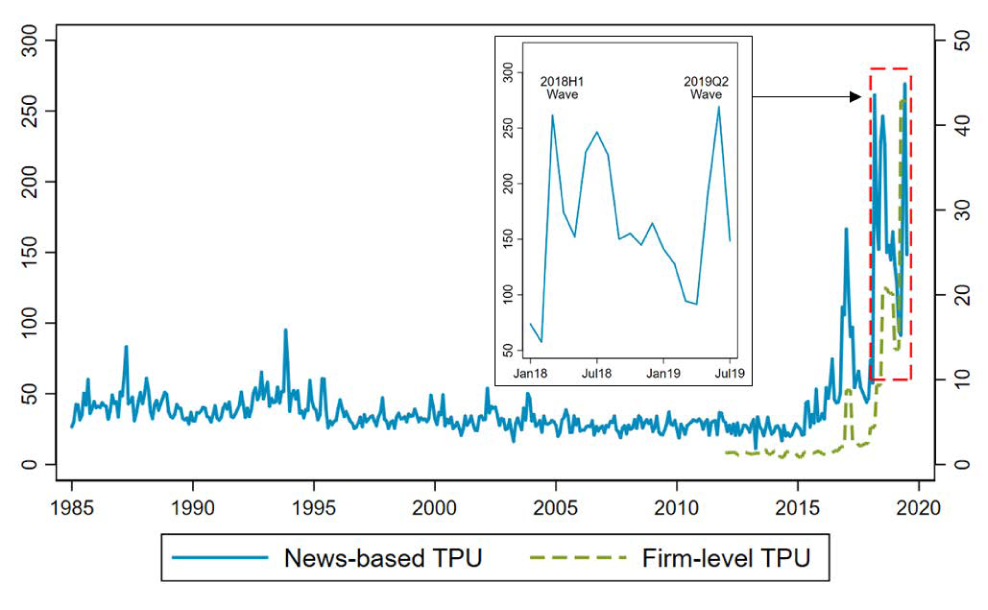

Our first measure of TPU is based on searches of newspaper articles that discuss trade policy uncertainty.3 We run automated text searches of the electronic archives of seven newspapers: Boston Globe, Chicago Tribune, Guardian, Los Angeles Times, New York Times, Wall Street Journal, and Washington Post. We select articles that discuss TPU by searching for terms related to uncertainty--such as risk, threat, uncertainty, and others--that appear in the same article as a term related to trade policy--such as tariff, import duty, import barrier, and anti-dumping. Our news-based measure of TPU is the monthly share of articles discussing trade policy uncertainty, rescaled to equal 100 for an article share of 1 percent.4

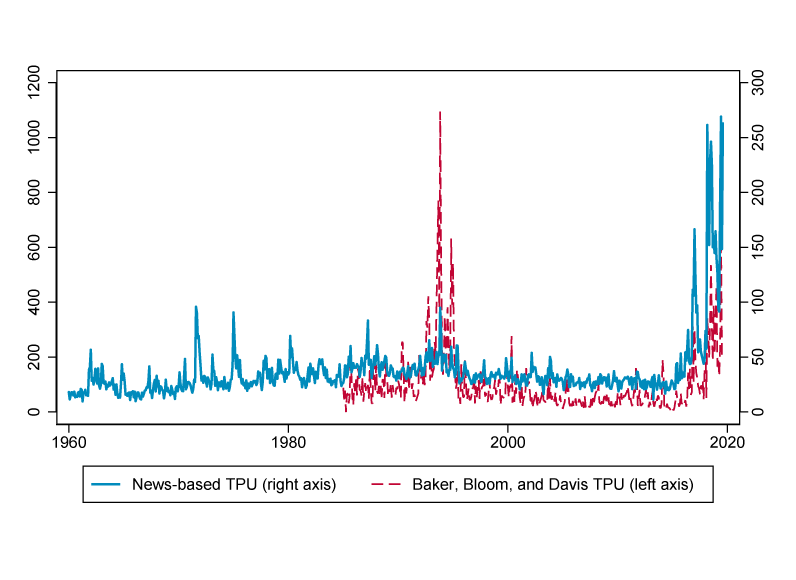

We complement this measure with a second index constructed by aggregating firm-level TPU obtained in an analogous way from automated text searches of the quarterly earnings call transcripts of U.S.-listed corporations.5 As Figure 1 shows, the two measures share very similar dynamics. In particular, according to both measures, TPU reached an initial high in the first half of 2018 (first wave), and, after subsiding, reached a new peak in the first half of 2019 (second wave). In the next section, we provide an empirical assessment of the macroeconomic effects of this increase in TPU.

Effects of Higher TPU on GDP: A VAR Approach

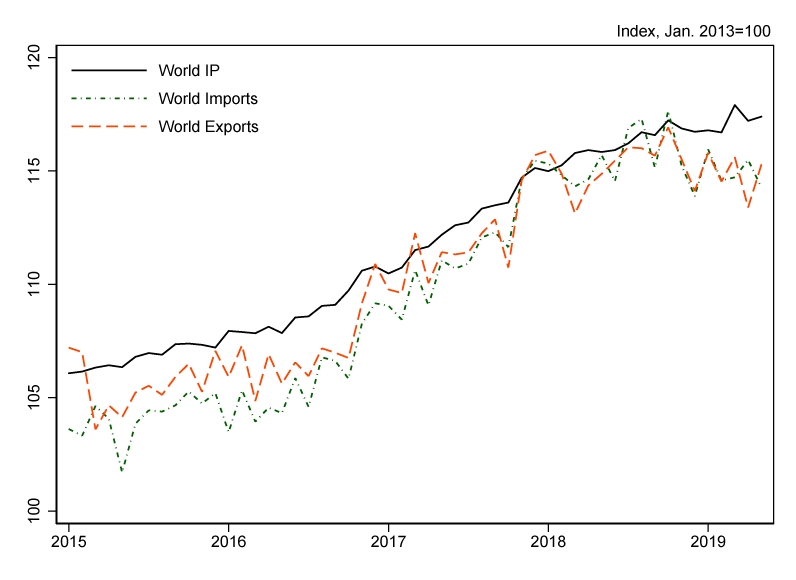

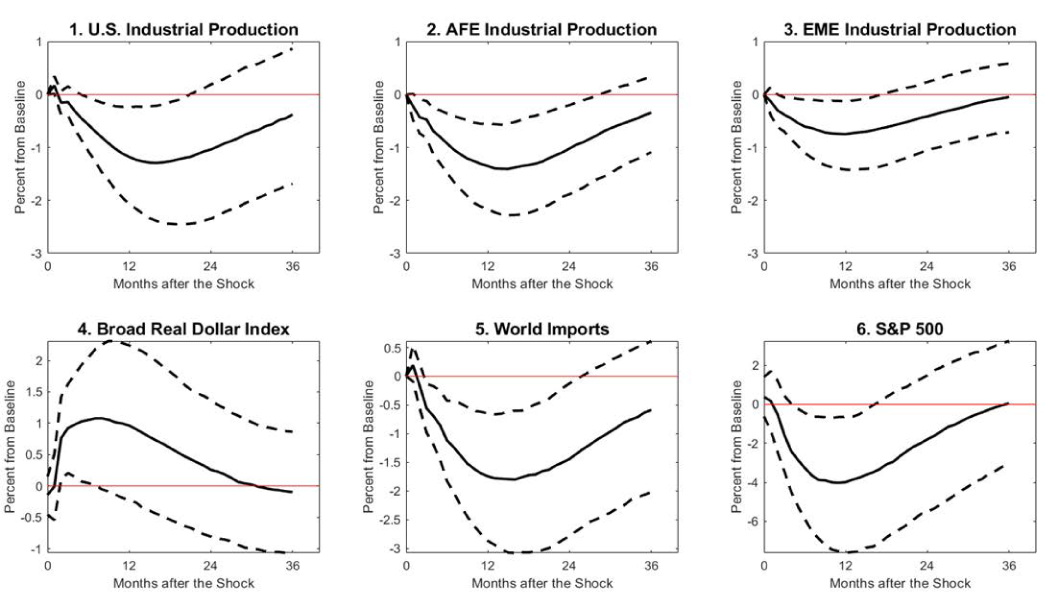

As shown in Figure 2, the rise in TPU in 2018 and 2019 has gone hand in hand with a slowdown in world industrial production and global trade. To quantify the effect of trade policy uncertainty on economic activity, we estimate a monthly vector auto-regression (VAR) that includes our news-based measure of TPU, (manufacturing) industrial production for the United States, the AFEs, and the EMEs, the broad real dollar index, world imports, U.S. stock prices, U.S. credit spreads, and U.S. import tariffs.6 The inclusion of tariffs in the VAR model allows us to isolate movements in TPU that reflect genuine trade uncertainty from those that reflect implemented trade policy actions. 7

Figure 3 shows the effects of an increase in TPU as large as the shock observed in March 2018. The increase in TPU lowers industrial production in all regions and boosts the dollar, while also lowering world imports and equity prices.

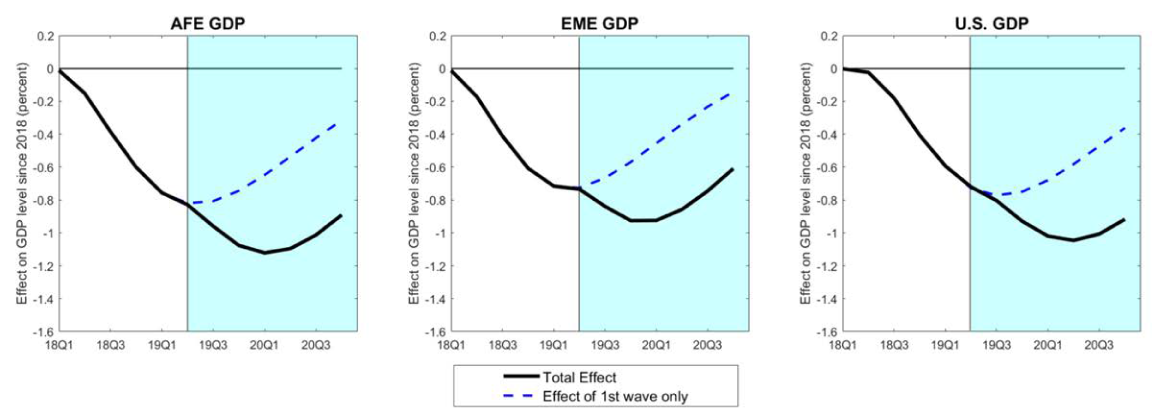

Using our estimated VAR, we gauge the GDP effects of the recent rise in TPU in two steps. First, we trace out the dynamic response of industrial production to the two recent waves of (estimated) shocks. The first wave includes the TPU shocks from the beginning 2018 through the first quarter of 2019. The second wave includes the TPU shocks in the second quarter of 2019. We then convert the effects on industrial production into GDP effects using the historical elasticity of GDP growth to industrial production growth.8

Figure 4 presents our main result. The total drag on GDP from the two waves of trade tensions (the black solid lines) is expected to increase through early 2020, cumulating to an impact of just above 1 percent. The effects are similar across the United States, the AFEs, and the EMEs. The blue dashed lines show the effect on GDP of the first wave of TPU alone. Had trade tensions not escalated again in May and June of 2019, the drag on GDP would have already started to ease in the second half of 2019.

How strong is the evidence?

The confidence intervals in the VAR responses point to some degree of uncertainty around these estimates (see Figure 3), perhaps reflecting the limited historical variation in the news-based TPU measure.

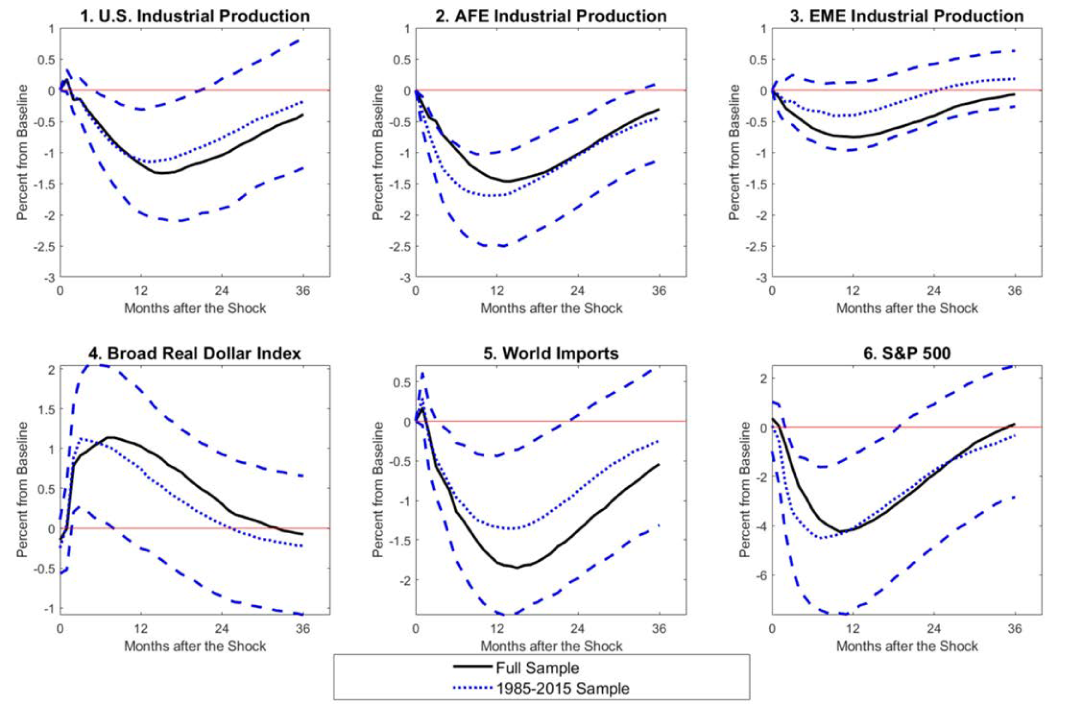

We address this issue in two ways. First, we investigate whether the estimated effects are unduly influenced by the recent spikes. Specifically, we truncate the estimation sample for the VAR in 2015, thus excluding the spikes in trade uncertainty in the last part of the sample. As shown in Figure 5, the estimated responses to a TPU shock in the truncated sample (the blue lines) and in the full sample (the black lines) are quite similar.

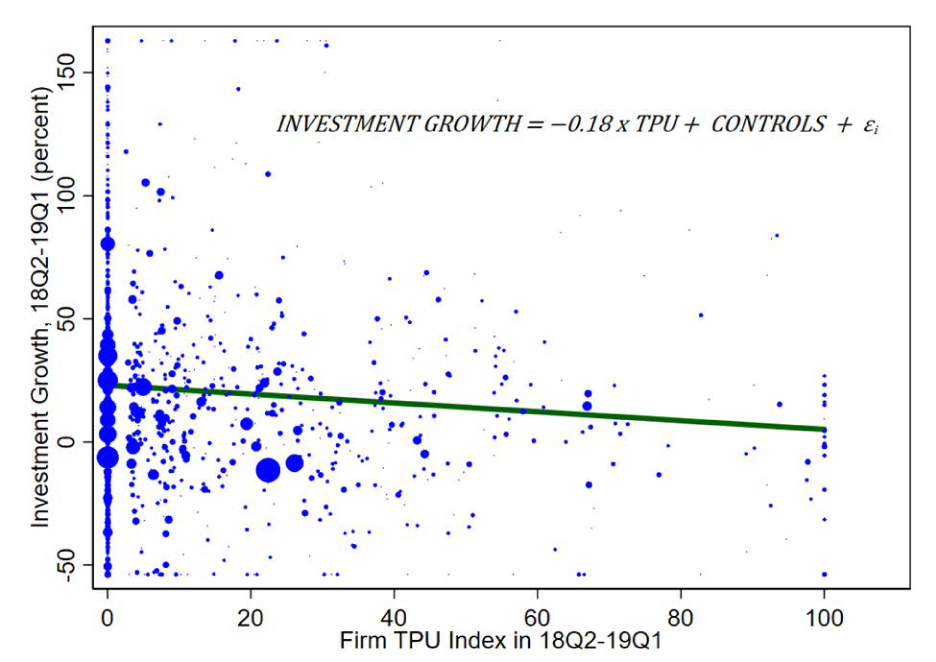

Second, we look for cross-sectional evidence on the effects of TPU at the level of individual firms by looking at a sample of about 1,500 listed firms over the four quarters ending in 2019Q1.9 In particular, we run a regression of firm-level investment growth from 2018Q2 to 2019Q1 on our firm-level measures of TPU, controlling for firm size and industry effects.

Figure 6 shows a scatterplot of TPU and investment growth across firms, together with the estimated regression line.10 A unit increase in a firm's TPU, keeping other controls fixed, reduces its investment growth by 0.18 percentage point with these effects being statistically significant. To get a sense of the economic magnitude of this coefficient, note that the average of TPU across firms is about 10 units. Given this value, one can estimate an average drag of trade uncertainty on investment growth of about 10 x 0.18 = 1.8 percentage points.11

These firm-level estimates are broadly consistent with our VAR analysis. On the face of it, a decline in investment of 1.8 percent would not appear to account for a GDP decline of around 1 percent (seen in the VAR), given the small share of business investment in total GDP. However, there are reasons to expect that the aggregate estimate of the GDP effect could be larger than the "partial equilibrium" average investment effect. First, even firms that do not explicitly mention TPU concerns in their earnings calls might be adversely affected by an overall decline in aggregate demand.12 Second, higher trade policy uncertainty is likely to affect other components of aggregate demand in addition to investment, such as spending on durable goods.13

In sum, both the aggregate time-series analysis and the cross-sectional evidence suggest that higher trade policy uncertainty has adverse effects on GDP and investment, with these effects estimated to be protracted through time. This evidence is consistent with a large body of recent academic literature that documents the negative effects of other kinds of economic and policy uncertainty on economic activity. That said, the unprecedented size of the recent increases in trade policy uncertainty points to some degree of "uncertainty" around these estimates.

REFERENCES

Altig, David, Nick Bloom, Steven Davis, Brent Meyer, and Nick Parker. 2019. "Tariff Worries and U.S. Business Investment, Take Two." Tech. rep., Atlanta Fed.

Baker, Scott R., Nicholas Bloom, and Steven J. Davis. 2016. "Measuring Economic Policy Uncertainty." The Quarterly Journal of Economics 131 (4):1593-1626.

Bloom, Nicholas. 2014. "Fluctuations in Uncertainty." Journal of Economic Perspectives, 28 (2): 153-76.

Caldara, Dario, Michele Cavallo, and Matteo Iacoviello, 2019. "Oil price elasticities and oil price fluctuations." Journal of Monetary Economics, 103: 1-20.

Caldara, Dario, Matteo Iacoviello, Patrick Molligo, Andrea Prestipino, and Andrea Raffo (2019) "The Economic Effects of Trade Policy Uncertainty (PDF)." IFDP 2019-1256. Washington: Board of Governors of the Federal Reserve System.

Gilchrist, Simon, and Egon Zakrajšek. "Credit spreads and business cycle fluctuations." American Economic Review 102.4 (2012): 1692-1720.

Hassan, Tarek A., Stephan Hollander, Laurence van Lent, and Ahmed Tahoun. 2019. "Firm-Level Political Risk: Measurement and Effects." The Quarterly Journal of Economics, forthcoming.

Left scale: News-based TPU (data through July 2019). At an index value of 100, 1 percent of news articles contain references to trade policy uncertainty. The articles are from seven major daily newspapers: Boston Globe, Chicago Tribune, Guardian, Los Angeles Times, New York Times, Wall Street Journal, and Washington Post.

Right-scale: Firm-level TPU index, average across firms (data through June 2019).

Inset: News-based TPU from January 2018 through July 2019. Two waves of heightened trade policy uncertainty are labelled as 2018H1 and 2019 Q2.

Source: Caldara, Dario, Matteo Iacoviello, Patrick Molligo, Andrea Prestipino, Andrea Raffo (2019), "The Economic Effects of Trade Policy Uncertainty".

Source: Netherlands Bureau for Economic Policy Analysis; Haver (data through May 2019).

Note: Impulse responses to a TPU shock of 150 points (dashed lines: 1 standard deviation confidence interval). Sample from 1985M1 through 2019M5. The size of the shock matches the increase in TPU in March 2018.

Source: Authors’ calculations.

Note: We use the estimated TPU shocks from the VAR from 2018M1 to construct a counterfactual path for the variables in the VAR, assuming only TPU shocks are active. We then construct GDP estimates using the historical sensitivity of GDP growth to IP growth (estimated elasticity of GDP to IP is 0.33 for the United States, 0.32 for the AFEs, and 0.51 for the EMEs).

Source: Authors’ calculations.

Note: Impulse responses to a TPU shock of 150 points (dashed lines: one standard deviation confidence interval). Sample from 1985M1 through 2019M5. The size of the shock matches the surprise increase in TPU in March 2018.

Source: Authors’ calculations.

Note: The scatterplot relates firm-level investment growth to firm-level trade policy uncertainty over the four quarters ending in 2019Q1. The standard error of the regression coefficient is 0.076 with a p-value of 0.02. Firm TPU is the average value of trade policy uncertainty over the four quarters, and is normalized so that it ranges from zero to 100. Investment growth is the sum of capital expenditures for the four quarters ending in 2019Q1 relative to capital expenditures for the four quarters ending in 2018Q1. The size of each dot is proportional to firm investment in 2017. Investment growth and trade uncertainty have been winsorized at the 5th and 95th, 1st and 99th, percentiles, respectively.

Source: Proquest, Compustat, and authors' calculations.

Note: News-based TPU from Caldara, Iacoviello, Molligo, Prestipino, and Raffo (2019) compared with the categorical trade policy uncertainty index of Baker, Bloom, and Davis (2016).

Source: Authors' calculations, www.policyuncertainty.com

1. Contact: [email protected]. At the time of writing, all authors worked at the Federal Reserve Board. All errors and omissions are our own responsibility. The views expressed in this paper are solely the responsibility of the authors and should not be interpreted as reflecting the views of the Board of Governors of the Federal Reserve System or of anyone else associated with the Federal Reserve System. Return to text

2. See Bloom (2014) for a review of the theoretical and empirical literature on the links between uncertainty and economic activity. Return to text

3. More details on the construction of our index can be found in Caldara, Iacoviello, Molligo, Prestipino, and Raffo (2019). The index is updated monthly and is available at https://www2.bc.edu/matteo-iacoviello/tpu.htm. Return to text

4. Baker, Bloom, and Davis (2016) also construct an indicator, available from 1985, of trade policy uncertainty. Relative to theirs, our index adds an additional 25 years of data, extending back to 1960. In addition, the search terms differ, as we do not search for mentions of legislation or institutions such as NAFTA and the WTO. Figure 7 (later) compares our news-based index with theirs. Return to text

5. The methodology to identify TPU in the earnings calls closely follows the one for our news-based measure. See Caldara, Iacoviello, Molligo, Prestipino, and Raffo (2019) for details. Hassan, Hollander, van Lent, and Tahoun (2019) construct measures of political risk using textual analysis of firms' earnings calls. Return to text

6. The VAR uses three lags. We apply a recursive identification scheme where shocks to TPU may affect the dollar, stock prices, and credit spreads contemporaneously, and all other variables with a one-month delay. We measure stock prices with the S&P 500 Index and credit spreads with the excess bond premium of Gilchrist and Zakrajšek (2012). Tariffs are the ratio of customs duties to total U.S. goods imports. Industrial production, world imports, and the S&P 500 are in logs and linearly detrended. TPU and the real broad dollar are in logs. The methodology to construct industrial production in the AFEs and the EMEs follows Caldara, Cavallo and Iacoviello (2019). Return to text

7. Like many news-based uncertainty indicators, our measure of trade uncertainty may also capture news about future changes in tariffs, regardless of whether they happen or not. Return to text

8. We compute distinct elasticities for the United States, the AFEs, and the EMEs by using a simple univariate regression of yearly GDP growth on yearly industrial production growth. The resulting elasticities are 0.33 for the United States, 0.32 for the AFEs, and 0.51 for the EMEs. Return to text

9. See Altig, Bloom, Davis, Meyer, and Parker (2019) for survey evidence on the effects of trade policy developments on firm-level investment, which points to similar results. Return to text

10. For the purposes of the figure, the firm-level TPU is normalized to range from zero to 100 depending on the intensity of TPU mentions over the year ending in 2019Q1. The intensity of TPU mentions is measured by the number of mentions divided by the length of the transcript. Return to text

11. A cross sectional average TPU of 10 means that the average firm in the sample mentions TPU 10 percent as frequently as the firm that mentions it most frequently. The results are robust to weighting the observations by the size of each firm. Return to text

12. Several airline companies, for instance, reported in their transcripts concerns about falling demand despite not having been directly exposed to tariff increases. Return to text

13. Caldara, Iacoviello, Molligo, Prestipino, and Raffo (2019) study the effects of TPU within a conventional New-Keynesian DSGE model with firms entering and exiting the export market. Within that model an increase in TPU sized to reflect recent developments leads to a contraction in both investment and consumption, and results in an overall output contraction that is very similar in size to what is predicted by our VAR analysis here. Return to text

Caldara, Dario, Matteo Iacoviello, Patrick Molligo, Andrea Prestipino, and Andrea Raffo (2019). "Does Trade Policy Uncertainty Affect Global Economic Activity?," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, September 4, 2019, https://doi.org/10.17016/2380-7172.2445.

Disclaimer: FEDS Notes are articles in which Board staff offer their own views and present analysis on a range of topics in economics and finance. These articles are shorter and less technically oriented than FEDS Working Papers and IFDP papers.