FEDS Notes

February 01, 2021

Household and Business Debt: A Fire-Sale Risk Analysis1

Fang Cai, Gene Kang, Gazi I. Kara, Nathan Swem, and Filip Zikes

Introduction

As of year-end 2019, nonfinancial business debt (BD) and household debt (HD) as a share of GDP were at similar levels of around 74 percent, and yet Federal Reserve Financial Stability Report suggested that BD posed greater risks to financial stability than HD2. Since the onset of the pandemic, the size of aggregate BD has increased considerably as a result of roughly $1.25 trillion of new issuance, while HD has grown by less than $100 billion. This note looks through the lens of fire-sale risks to show why nonfinancial BD is more concerning for financial stability than the HD. We examine BD and HD according to holder types, credit quality, and market liquidity features, and we highlight the areas of greatest concern for fire sales. Although extensive policy measures have helped ease the strains, fire-sale risks, especially with BD, remain salient at least in the near term.

Key takeaways:

Our analysis suggests greater fire-sale vulnerabilities for BD than for HD.

- A significant share of BD is borderline investment grade (25%) and held by types of institutions (banks, insurers, and mutual funds) that are more prone to fire sales if the debt is downgraded to speculative grade. In contrast, the majority of HD is owed by prime borrowers and held by institutions (GSEs) less prone to fire sales.

- The U.S Federal Government or the GSEs hold or guarantee a large share of HD, mitigating fire-sale risks of HD relative to BD.

- A large fraction of BD exists in the form of relatively illiquid securities (risky corporate bonds and CLOs) with potentially significant fire-sale losses, while a large share of HD tends to be relatively liquid and has Federal Reserve backstops in times of stress (e.g. MBS), making it less susceptible to fire sales.

Although the COVID-19 pandemic is not over and it is too early to draw definitive conclusions, our analysis takes into account the economic impact seen in recent months, such as the increase in the level and riskiness of business debt in the first half of 2020. We also address how several of the recent Federal Reserve policy measures have helped mitigate the fire-sale risks we have identified, and we discuss where such risks remain. In addition, in the wake of the COVID-19 crisis, business leverage may continue to increase relative to HD. Therefore, the BD fire-sale risks that we raise in our analysis may be an even greater concern in the post-COVID-19 period.

Motivation

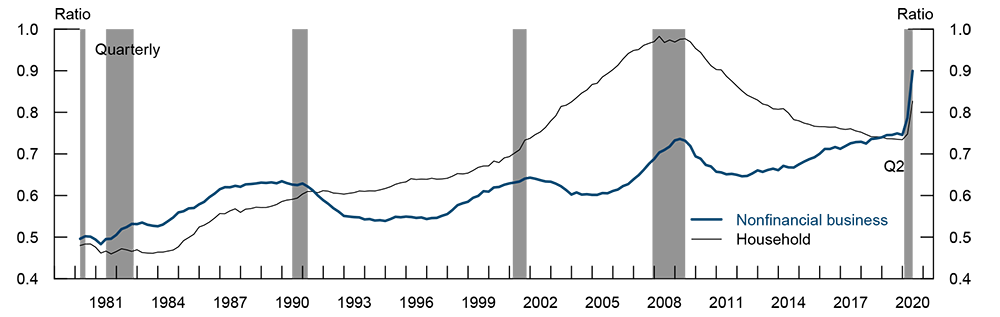

Household and nonfinancial business debt both stood at around $16.1 trillion as of year-end 2019, or 74 percent of GDP. Since the onset of the COVID-19 crisis, the GDP has contracted sharply as a result of the economic slowdown, while corporate debt issuances accelerated. As of 2020 Q2, the HD and BD debt-to-GDP ratios rose to 82% and 90% of GDP, respectively (Figure 1). The assessment provided by the Federal Reserve in recent Financial Stability Reports suggests that business debt poses greater risks to financial stability than household debt3 . This assessment is based on various measures of leverage, credit quality, and lending standards. In the business sector, leverage is at historically high levels with a relatively large share of the debt outstanding concentrated among high-risk borrowers, and credit standards for some business loans appear to have been deteriorating. In addition, since the onset of the Covid-19 crisis in March 2020, over $1.25 trillion of new BD has been issued. Although roughly 80 percent of this new issuance has been investment grade (IG), 55 percent of this (or 45 percent of the total new issue) is BBB-rated (or “borderline” IG) and therefore vulnerable to future downgrades. By contrast, borrowing by households has grown at a modest pace relative to incomes, about two-thirds of household debt balances are held by borrowers with prime credit scores, and the debt growth has been concentrated among prime-rated borrowers. Furthermore, households cut back consumption and spending in response to COVID-19, which lead to a sharp decrease in consumer credit in the early stages of the pandemic4. This note extends the existing work by decomposing the two types of debt by holder profile, credit quality and market liquidity, and compares them through the lens of fire-sale vulnerabilities.

Note: The shaded bars indicate periods of business recession as defined by the National Bureau of Economic Research: January 1980-July 1980, July 1981-November 1982, July 1990-March 1991, March 2001-November 2001, December 2007-June 2009, and February 2020-June 2020. GDP is gross domestic product.

Source: Federal Reserve Board staff calculations based on Bureau of Economic Analysis, national income and product accounts, and Federal Reserve Board, Statistical Release Z.1, "Financial Accounts of the United States."

Fire-sale vulnerabilities refer to spillover effects and pecuniary externalities imposed on the rest of the financial system by financial institutions engaging in forced sales of assets at prices below fundamental values. As such, they capture the risk that shocks to individual institutions or assets prices get transmitted to other institutions and amplified through cascading sales in falling markets. Such risks are closely related to the fire-sale tendencies of institutions holding these assets and to the liquidity features of the underlying debt, which are generally not explicitly accounted for by simple measures of vulnerability, such as lending standards, credit quality, and leverage.

Overall, we find greater fire-sale risks for business debt than for household debt. A far larger share of business debt is directly traded in secondary markets, and a large share of this debt is currently rated borderline investment grade and held by banks, insurers, and mutual funds. These holders of the debt face various constraints making fire sales more likely should a wave of corporate downgrades occur. In contrast, a large share of household debt is held in non-securitized forms on banks’ balance sheets (e.g. credit cards) or in the form of securities with an explicit government guarantee and relatively higher market liquidity (e.g. mortgages), which makes fire sales in these debt markets less likely.

The rest of the note is organized as follows. Section 2 describes our framework for assessing fire-sale vulnerabilities in the household and business sectors. Sections 3, 4, and 5 present our analysis of the key determinants of fire-sale risks in these sectors, namely the debt holder profile, credit quality, and market liquidity. Section 6 discusses the recent market turmoil and its implications for fire-sale vulnerabilities going forward.

Framework

Existing literature modelling fire-sale risks assumes that in periods of stress banks (and asset managers) sell assets in equal proportion5. In contrast, our analysis takes into account the possibility that in periods of stress financial institutions might sell their most liquid holdings (liquid securities trading in centrally-cleared markets) earlier and/or in greater proportion relative to less liquid assets (whole loans, less liquid securities traded in OTC markets, etc.). There is empirical evidence that supports our approach. For example, Haddad, Moreira and Muir (2020) show that investors tried to sell safer, more liquid securities to raise cash during acute phase of the COVID-19 crisis. We focus on three main factors that, in our view, determine the likelihood and severity of fire-sale risks in debt markets: 1) holder profile, 2) credit quality, and 3) market liquidity.

Holder Profile

Different financial institutions may engage in fire sales for different reasons. Banks face regulatory constraints on capital and may resort to fire sales if their capital levels drop below regulatory minima or internal targets, as in the models of Greenwood et al. (2015), Duarte and Eisenbach (2019), and Shin (2020). Large banks also have to comply with liquidity regulations requiring them to hold sufficient quantities of liquid assets to be able to sustain liquidity outflows in times of stress (LCR). Breaching the minimum liquidity requirements may force banks to sell assets. Additionally, banks may resort to liquidity hoarding in times of stress and thus indirectly contribute to the deterioration of market liquidity (Diamond and Rajan (2011), Gale and Yorulmazer (2013)).

Insurance companies are also subject to regulatory constraints. Specifically, insurers face significantly higher risk-based capital charges on downgraded corporate bonds (“fallen angels”), which incentivizes them to sell these bonds, especially if they are unable to quickly raise new capital. Such sales have been shown to generate temporary prices pressures in the corporate bond market (Ellul et al. (2011)). Additionally, life insurance companies have been increasing their reliance on runnable short-term liabilities in recent years, and they continue investing in illiquid assets. Sudden withdrawals or refusals to roll over such short-term debt may force life insurer to sell assets to cover their short-term funding needs (Foley-Fisher et al. (2019)).

Open-end mutual funds are exposed to run risks stemming from their liquidity transformation and the first-mover advantage. If investors believe redemptions would negatively affect the liquidity of the funds going forward, they may be incentivized to redeem ahead of others. Such runs may trigger fire sales and generate a material price impact in the corporate bond market, as recently documented by Falato et al. (forthcoming) and modeled by Cetorelli et al. (2016).

Finally, hedge funds are typically subject to funding liquidity risks and margin constraints, which tend to tighten when market volatility increases. That tightening forces the funds to deleverage and liquidate outstanding positions, contributing to the well-known liquidity spirals studied by Brunnermeier and Pedersen (2009).

To summarize, the holder profile matters because financial institutions that are less likely to face binding constraints in times of stress are generally less likely to engage in forced selling. Debt primarily held by less constrained institutions is thus less likely to experience fire-sale losses. The findings of Nanda et al. (2019) support this idea. Those finding suggest that when capital-constrained insurance companies hold more of a corporate bond, those bonds tend to be cheaper ex-ante, as market participants price the risk that such bonds are more likely to experience price pressures when insurers’ capital constraints tighten.

Credit Profile

The second determinant of fire-sale risk we consider is the risk profile of the debt, especially the amount of debt near the investment grade/high yield boundary. A large quantity of debt near this boundary leaves that debt vulnerable to fire sales should downgrades occur (“triple-B cliff”). The triple-B cliff has grown larger over the recent years and many policy makers have flagged it as one of the most salient financial stability vulnerabilities stemming from the corporate business sector6. In contrast, in the HD sector, where mortgages and student loans---both of which enjoy government backing---account for the majority of near-subprime debt, the vulnerabilities stemming from downgrades are less concerning7.

Similar to debt at the triple-B cliff, information-sensitive debt or debt that is difficult to price, which is typically the case for low- or unrated issuers, may be more susceptible to fire sales than the debt of highly rated, publicly traded companies.

Market Liquidity

The third, and final, determinant of fire-sale risk we consider is the ease with which debt can be sold in times of stress. Two factors are at play here: the degree of standardization of the debt and the level of market liquidity. Regarding debt standardization, an active secondary market does not exist for some bespoke forms of debt held by banks on their balance sheets, such as credit cards or bank loans. While the lack of a market for such debt may increase the price impact of forced sales, it makes it harder for banks to sell the debt in times of stress, incentivizing banks to sell other forms of debt that are more easily brought to the market first. In addition, because non-standardized debt is not generally marked to market on a regular basis, forced sales of such debt are less likely to cause direct losses to other financial institutions holding similar debt and to trigger further rounds of fire sales.

Regarding the level of market liquidity, debt in the form of relatively illiquid securities, such as high-yield corporate bonds, may generate considerable fire-sale losses to those who hold it, especially in response to downgrades or large investor redemptions. This result is obtained because when an institution holding these securities is forced to sell, the lack of liquidity in the market and the forced selling puts greater downward pressure on the prices of the securities. In contrast, forced sales of more liquid debt, such as agency MBS or Treasury securities, may generate only small fire-sale externalities, because the price impact of trades in deep markets tends to be small or because the markets for these securities enjoy explicit government support in times of stress (e.g. MBS).

Holder Profile

Table 1 summarizes the current holdings of BD and HD by institution type. Clearly, BD and HD have very different holder profiles. Banks are the largest holder of both BD and HD, accounting for a little less than half of each. The 2019 stress test showed that banks were well-capitalized and should be able to continue lending even in a severely adverse scenario. For example, as the COVID-19 shock hit, strong capital and liquidity buffers enabled banks to accommodate a dramatic increase in drawdowns on credit lines both by financial and nonfinancial firms. Thus, fire-sale risks at banks are judged to be low.

Table 1. Outstanding debt by holder type as of 2020-Q2

| Business debt (BD) | Household debt (HD) | |||

|---|---|---|---|---|

| USD billion | % | USD billion | % | |

| Banks | 7,774 | 44% | 7,647 | 48% |

| Gov/GSEs | 94 | 1% | 5,897 | 37% |

| Insurance companies | 2,214 | 13% | 786 | 5% |

| Mutual funds | 1,518 | 9% | 1,047 | 7% |

| Pension funds | 792 | 4% | 438 | 3% |

| Hedge funds | 382 | 2% | 12 | 0% |

| Other/ROW | 4,832 | 27% | 219 | 1% |

Source: Z.1 Financial Accounts of the United States, S&P LCD, TIC SHC(A), SIFMA, Liu and Schmidt-Eisenlohr (2019), and staff calculations.

While the risk is judged to be low, we wanted to quantify the fire-sale risk. One way to quantify potential fire-sale losses at banks is to utilize the results of the annual stress test (DFAST). The Severely Adverse Scenario is designed to generate losses that implicitly account for spillover effects and other non-linearities that are expected to be at play in deep recessions but that are difficult to model explicitly. The difference between the DFAST losses under the Severely Adverse Scenario and those from the Adverse Scenario may thus serve as a proxy for fire-sale losses in times of severe market stress. That said, some types of debt may be hit particularly hard in the severely adverse scenario and yet be less prone to fire sales, as only a relatively small fraction of this debt is traded in a standardized form in secondary markets, e.g. credit card debt8.

Table 2 reports this proxy for the past four DFAST cycles separately for BD and HD. In 2019, the second-round effects implicit in the stress test equal around $102 billion, while in the previous three DFAST cycles, these effects were $141 billion on average9. Consistently through the years, BD and HD account for around 60% and 40% for the second-round losses, respectively. According to this metric, BD is therefore more vulnerable to additional losses from potential spillovers in severe downturns.

Table 2: Second-round effects implicit in DFAST scenarios

| Business debt (BD) | Household debt (HD) | |||

|---|---|---|---|---|

| USD billion | % | USD billion | % | |

| 2019 | 82 | 59% | 57 | 41% |

| 2018 | 100 | 60% | 66 | 40% |

| 2017 | 77 | 61% | 49 | 39% |

| 2016 | 79 | 60% | 53 | 40% |

| Average | 85 | 60% | 56 | 40% |

Moving on to GSEs, they are the second largest holder of household debt (37%), being especially prominent in the residential mortgage segment of HD, where they hold or guarantee roughly two-thirds of all mortgage balances10. By contrast, because GSE are established to support the mortgage market, they only hold negligible amounts of business debt. Of the GSEs, Fannie Mae and Freddie Mac are currently under the conservatorship of the FHFA and enjoy the full backing of the federal government, similar to that of Ginnie Mae11. Funding pressures and fire-sale risks at GSEs are therefore low.

Insurance companies and mutual funds, which could face potentially binding requirements and investor redemption pressures in a stress event, hold around 22% of BD and 12% of HD, respectively. Thus, should the constraints of liquidity pressures at these institutions tighten, the BD sector will likely be affected to a larger degree than the HD sector. Additional pressures in the BD sector may come from hedge funds, which hold around 2% of BD, but virtually no HD.

In summary, based on the holder profile, we judge that BD is more susceptible to fire-sale risks than HD.

Credit Profile

To simplify the exposition, we group debt by credit quality into four mutually exclusive buckets: high investment grade (A- and above), borderline investment grade (BBB-, BBB, and BBB+, referred to as BBB thereafter), high yield (BB+ and below), and unrated (NA). Using this categorization, high investment grade debt is all debt rated A- or above, and this debt would have to be downgraded multiple notches before falling into the high-yield category. Borderline investment grade is all debt with a BBB rating and, while still considered investment grade by rating agencies, this segment of debt is the most vulnerable to fire sales: a single downgrade could take a substantial amount of this debt to the speculative grade territory (“triple-B cliff”). High yield debt includes all debt with a credit rating of BB+ and below, and the unrated category includes all debt for which a credit rating is currently not available. For HD, the four corresponding rating buckets are prime, near prime, subprime, and unrated respectively12.

Table 3 summarizes the current breakdown of outstanding BD and HD by rating category. HD has generally higher credit quality, with prime borrowers accounting for 66% of outstanding debt, compared with 49% in the high investment grade category of BD. The amount of debt at the speculative-grade boundary is also higher in the BD sector (25%) than in the HD sector (19%). Combined with the fact the holders of BD are much more sensitive to rating downgrades than those of HD, the triple-B cliff poses greater fire-sale risks in the BD sector.

Table 3: Outstanding debt by credit rating as of 2020-Q2

| Business debt (BD) | Household debt (HD) | |||

|---|---|---|---|---|

| USD billion | % | USD billion | % | |

| High investment grade (>= A- or Prime) | 8,671 | 49% | 10,631 | 66% |

| Borderline investment grade (BBB- to BBB+, or Near-prime) | 4,340 | 25% | 2,991 | 19% |

| High yield (<= BB+ or Subprime) | 3,642 | 21% | 1,461 | 9% |

| Unrated | 952 | 5% | 983 | 6% |

Source: Z.1 Financial Accounts of the United States, Capital Assessments and Stress Testing Report (FR-Y14Q report), eMAXX, Mergent, Inc., Fixed Investment Securities Database (FISD), U.S. Dept. of the Treasury, Treasury International Capital (TIC) Data, https://www.treasury.gov/resource-center/data-chart-center/tic/Pages/ticsec.aspx., and staff calculations.

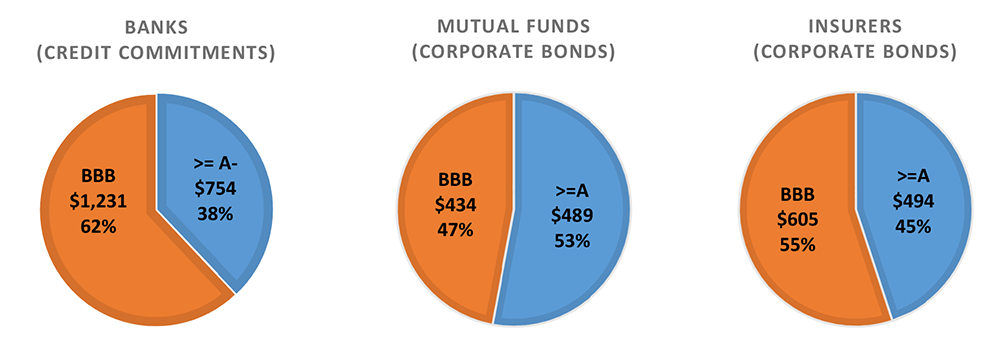

To zoom in on the vulnerabilities associated with the triple-B cliff in the BD sector, Figure 2 shows a decomposition of investment-grade debt held by banks, mutual funds, and insurers into borderline investment grade (BBB) and high investment grade (>= A-). At banks, almost two thirds, or around $1.2 trillion, of the current credit commitments to nonfinancial firms are to borrowers rated BBB. The majority of insurers’ IG corporate bond holdings are also rated BBB (55%, or $605 billion), while at mutual funds the share of BBB-rated bonds is around 47%, or $434 billion. The total amount of BBB-rated corporate bonds at mutual fund and insurers stands at around $1 trillion. On average across different holders of investment-grade BD, more than half of all debt is sitting at the BBB-cliff, with banks and insurance companies particularly exposed to this class of debt.

Source: FR Y-14 (banks; Q2/2020), Morningstar (mutual funds; Q2/2020), eMAXX (insurers; Q2/2020). The BBB category includes BBB-, BBB and BBB+.

To estimate the fraction of this debt that is at risk of being downgraded to speculative grade, we rely on historical downgrade frequencies observed in episodes of significant stress emanating from the corporate sector. J.P. Morgan (2018) estimate that when the dot-com bubble burst in March 2000, around 10% of outstanding BBB bonds experienced a downgrade to speculative grade over the following year and around 25% experienced a downgrade over the next 3 years. Using these downgrade rates, around $140 ($345) billion worth of corporate bonds held by mutual funds and insurers are currently at risk of becoming fallen angels over the next year (three years) should the current recession becomes prolonged.

Although banks do not face the same fire-sale risks associated with fallen angels as insurers and mutual funds do, credit downgrades can have significant impact on banks as well. In addition to causing direct losses on outstanding loans due to a simultaneous increase in default rates, an economic shock causing a wave of corporate downgrades would likely also involve additional liquidity pressure on banks. The newly downgraded firms may face tighter funding conditions in primary debt markets and resort instead to drawing on bank credit lines and looking to banks to roll over their existing debt. Additionally, downgrades can trigger a breach of loan covenants, limiting the amount of liquidity newly downgraded firms can access under their existing credit agreements with banks13.

Market Liquidity

It is generally difficult to estimate market liquidity of various types of debt in times of stress. Previous fire-sale analyses have relied on statistical estimates using historical transactional data (Baranova et al., 2017) or assumptions embedded in bank liquidity regulations (Cetorelli et al, 2016; Duarte and Eisenbach, 2019). We take a simpler approach and group BD and HD into four liquidity buckets: liquid, moderately liquid, least liquid and illiquid (Table 4)14. Our ranking of assets by market liquidity is informed by the empirical market microstructure literature (Fleming, et al., 2016; He and Mizrach, 2017; Bao et al., 2018), market liquidity metrics (see for example the box titled “What Has Been Happening to the Liquidity of U.S. Treasury and Equity Futures Markets?” in November 2019 Financial Stability Report), and our own judgement. We also take into account the relative performance of the various markets in the COVID-19 crisis and the government support provided to these markets to improve market functioning.

Table 4: Liquidity buckets

| Market liquidity | Type of debt |

|---|---|

| Liquid | Agency MBS, IG corporate bonds |

| Moderately liquid | ABS (credit cards, auto and student loans), HY corporate bonds |

| Least liquid | Non-agency MBS, CMBS, CMO, CLO, unrated corporate bonds |

| Illiquid | Non-securitized debt |

Table 5 summarizes the current outstanding debt by market liquidity. According to our current best estimates, 49% of outstanding BD is in the form of securities (either corporate bonds or otherwise securitized debt), compared with 74% in the HD sector. The remaining 51% of BD and 26% of HD are individual loans (not in securitized form) on balance sheets of banks and other financial institutions. Turning to market liquidity, we estimate that around 54% of HD is liquid, primarily in the form of GSE-backed MBS, while only around 35% of BD is liquid (IG corporate bonds). Thus, we judge that, should fire sales occur, the price impact and the associated spillover losses would be higher in the BD sector.

Table 5: Outstanding debt by securitization and market liquidity as of 2020-Q2

| Business debt (BD) | Household debt (HD) | |||

|---|---|---|---|---|

| USD billion | % | USD billion | % | |

| Securitized | 8,671 | 49% | 11,849 | 74% |

| - Liquid | 6,195 | 35% | 8,728 | 54% |

| - Moderately liquid | 1,441 | 8% | 2,167 | 13% |

| - Least liquid | 1,035 | 6% | 954 | 6% |

| Non-securitized (illiquid) | 8,934 | 51% | 4,216 | 26% |

Source: Z.1 Financial Accounts of the United States, FR Y-9C, FR-Y14Q, eMAXX, FISD, S&P LCD, SIFMA, and staff calculations.

Recent events and impending fire-sale risks

Since February 19th, in reaction to concerns regarding COVID-19, large price dislocations and liquidity problems have occurred in both BD and HD markets, including those with high quality collateral such as agency MBS. We believe that many of the fire-sale dynamics that we highlight above have contributed to the dramatic increases in volatility and illiquidity in BD markets, particularly for the riskier segments of the credit markets, such as high-yield bonds.

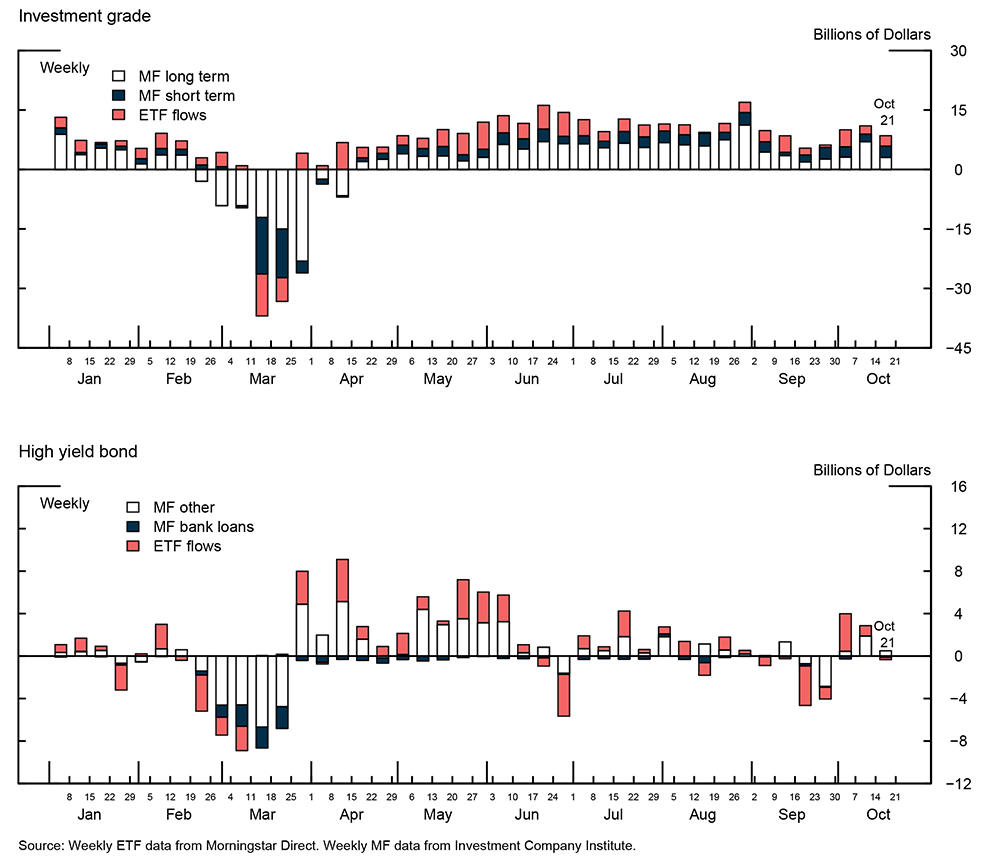

The Federal Reserve has undertaken several extraordinary policy actions, to support the flow of credit to businesses and households, many of which have helped improve market conditions and restore investor confidence15. Of these, the Secondary Market Corporate Credit Facility (SMCCF) is most relevant for the BD markets16. Since its announcement on March 23, 2020, this facility appears to have had a calming effect across corporate bond markets. Even though it was initially targeted at the IG portion of the market, outflows from both IG and HY bond funds have mostly reversed since then, which likely have mitigated some of the imminent fire-sale risks (Figure 3).

Source: Weekly ETF data from Morningstar Direct. Weekly MF data from Investment Company Institute.

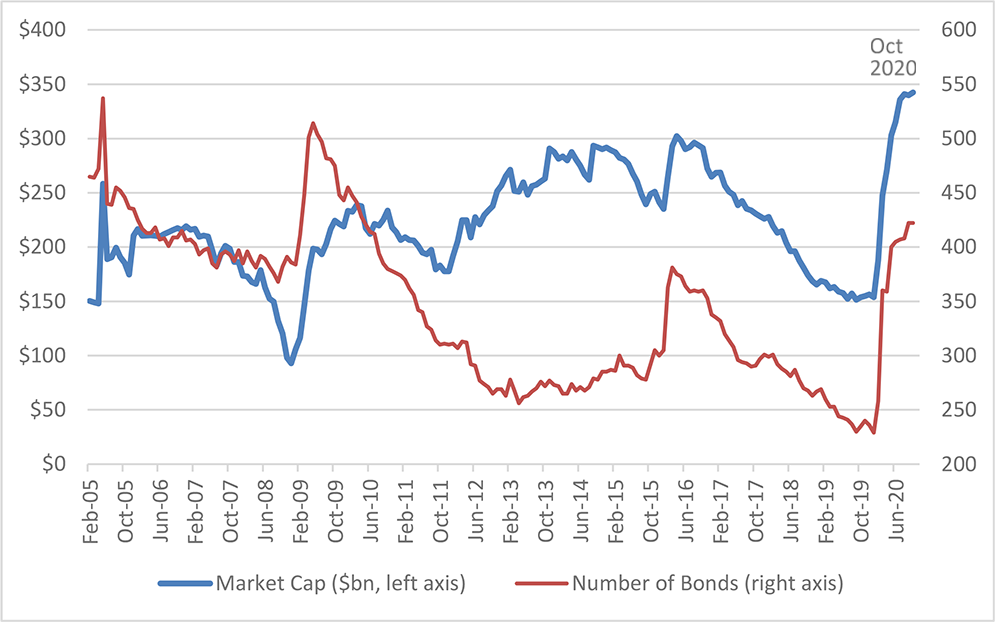

While conditions in corporate bond markets have eased since the Fed interventions, the number of fallen angels has jumped. According to Moody’s data, $48 billion of debt was downgraded to fallen-angel status in March, with most of those downgrades occurring in the final two weeks of the month. As a result, the market capitalization and the number of constituents of the Bloomberg Barclay Fallen Angel Index increased dramatically (Figure 4). While at the end of February, the index covered around 260 bonds, it reached 360 by the end of March and 422 by the end of October.

Source: Bloomberg

In response to the growing concerns about “fallen angels,” the Federal Reserve Board extended the SMCCF on April 9 to include corporate bonds that have been downgraded below investment grade but no lower than BB- after March 22, 2020 as well as high-yield ETFs. This intervention is expected to mitigate fire-sale risks associated with “fallen angels”. However, the fire-sale risks could persist in the medium to long term, well beyond the time horizon of the emergency facilities put in place in response to the COVID crisis.

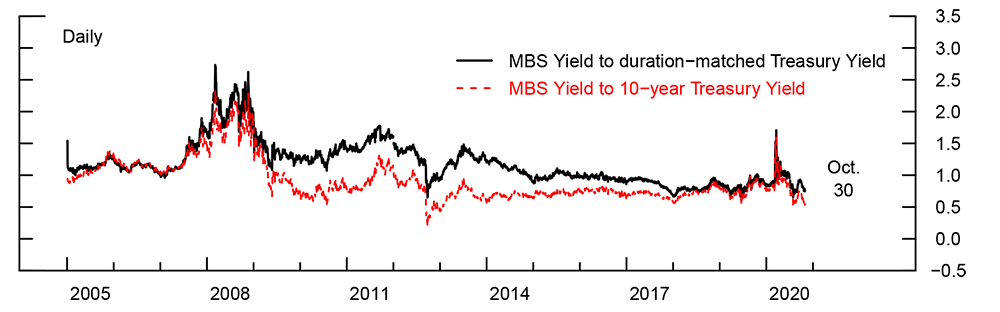

Conditions also deteriorated significantly in some household debt markets. Notably, in mortgage markets, primary mortgage rates increased sharply in early March amid deteriorating secondary market liquidity and elevated volatility. MBS spreads widened significantly and exceeded levels last seen during the European debt crisis (Figure 5). To restore orderly market functioning in the primary and secondary mortgage markets, on March 15 the FOMC announced that over the coming months the Committee will increase its holdings of agency mortgage-backed securities by at least $200 billion. After the Fed announced the MBS purchases, mortgage market functioning gradually improved and spreads returned to normal levels.

Note: Dotted lines at last reported values.

Source: J.P. Morgan Chase & Co., Copyright 2021.

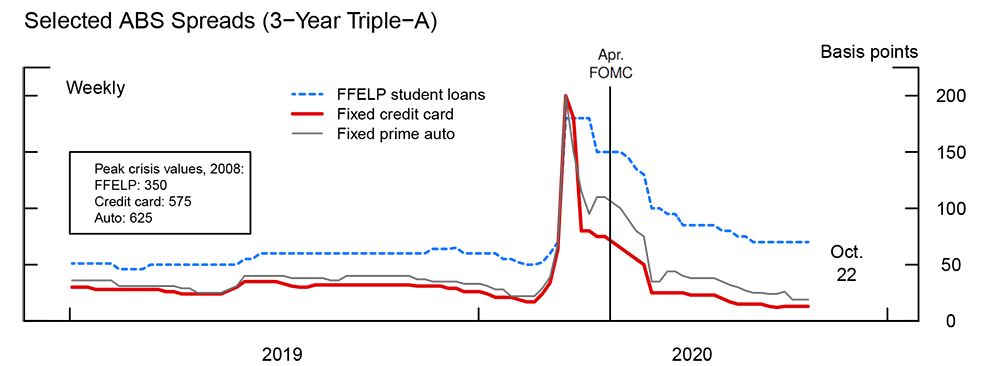

Starting in late February 2020, prior to the announcements of the initial Federal Reserve actions, conditions deteriorated sharply in other securitized markets, such as those for asset-backed securities (ABS) and commercial mortgage-backed securities (CMBS); primary market issuance slowed, secondary market trading became impaired, and spreads widened sharply (Figure 6). To alleviate the strains in these markets, the FOMC decided to include agency CMBS in its MBS purchase program and re-established the Term Asset-Backed Securities Loan Facility (TALF), which will enable the issuance of asset-backed securities (ABS) backed by student loans, auto loans, credit card loans; loans guaranteed by the Small Business Administration (SBA); and certain other assets. Shortly after these measures were announced, strains in the consumer ABS markets began to ease.

Note: Spreads are to swap rate for credit card and auto asset-backed securities (ABS) and to 3-month LIBOR for student loans. FFELP is Federal Family Education Loan Program.

Source: J.P. Morgan Chase & Co., Copyright 2021.

While the interventions by the Federal Reserve have helped restore orderly market functioning in household debt markets, some risks remain. For example, liquidity pressures at mortgage service companies, if left unaddressed, could diminish investors’ appetite for MBS and lead to large declines in prices and potentially fire sales of these securities.

Conclusion

We conclude by evaluating how the COVID-19 crisis might affect leverage in the business and household sectors going forward. An indicator of the leverage of businesses—the ratio of debt to assets for all publicly traded nonfinancial firms—was at its highest level in 20 years at the end of the second quarter of 2020. Moreover, for highly leveraged public firms—defined as firms above the 75th percentile of the leverage distribution—this indicator is close to a record high. As the economic effects of COVID-19 continue to unfold, earnings declines could trigger a sizable increase in firm defaults. Policy interventions may help businesses withstand a period of weak earnings by issuing new debt and restructuring existing credit. As a result, many of these businesses will emerge with even higher amounts of leverage, suggesting that vulnerabilities stemming from the business sector, including nonpublic companies and small businesses, could become even more elevated for some time. On the other hand, households debt has grown modestly, and only among borrowers with prime credit scores. Taken together, in the wake of the COVID-19 crisis, business leverage has increased further relative to HD. Therefore, the BD fire-sale risks that we identify in our analysis present a greater concern in the post-COVID-19 period.

References

Baranova, Y., J. Cohen, P. Lowe, J. Noss, and L. Sivestri, 2017, Simulating stress across the financial system: the resilience of corporate bond markets and the role of investment funds, Financial Stability Paper No. 42, Bank of England.

Bao, J., M. O’Hara, and A. Zhou, 2018, The Volcker Rule and corporate bond market making in times of stress, Journal of Financial Economics, 130(1), 65—113.

Board of Governors of the Federal Reserve System, 2019, Financial Stability Report (Washington: Board of Governors, May), pp. 22-25, http://federalreserve.gov/publications/files/financial-stability-report-201905.pdf.

Brunnermeier, M. and L. H. Pedersen, 2009, Market liquidity and funding liquidity, Review of Financial Studies, 22(6), 2201-2238.

Cetorelli, N., F. Duarte, and T. Eisenbach, 2016, How vulnerable are mutual funds to fire sales?, Federal Reserve Bank of New York.

Diamond, D. W. and R. G. Rajan, 2011, Fear of fire sales, illiquidity seeking, and credit freezes, The Quarterly Journal of Economics 126(2), 557–591.

Duarte, F. and T. Eisenbach, 2019, Fire-sale spillovers and systemic risk, Federal Reserve Bank of New York.

Ellul, A., C. Jotikasthira, and C. T. Lundblad, 2011, Regulatory pressure and fire sales in the corporate bond market, Journal of Financial Economics 101(3), 596–620.

Falato, A., A. Hortaçsu, D. Li, and C. Shin, forthcoming, Fire-sale spillovers in debt markets, Journal of Finance.

Fleming, M., A. Fuster, L. Molloy, and R. Podjasek, 2016, Has MBS market liquidity deteriorated?, Liberty Street Economics, Federal Reserve Bank of New York.

Foley-Fisher, N., B. Narajabad, and S. Verani, 2019, Assessing the size of the risks posed by life insurers' nontraditional liabilities, FEDS Notes 2019-05-28. Board of Governors of the Federal Reserve System (U.S.).

Gale, D. and T. Yorulmazer, 2013, Liquidity hoarding. Theoretical Economics 8(2), 291–324.

Greenwood, R., A. Landier, and D. Thesmar, 2015, Vulnerable banks. Journal of Financial Economics 115(3), 471–485.

Haddad, V., A. Moreira, and T. Muir, 2020, When Selling Becomes Viral: Disruptions in Debt Markets in the COVID-19 Crisis and the Fed’s Response, working paper.

He, A. and B. Mizrach, 2017, Analysis of securitized asset liquidity, Research Note, FINRA Office of the Chief Economist.

J.P. Morgan, 2018, How big is the BBB- problem? Likely a problem for the next downturn but not for now.

Liu, Emily and Tim Schmidt-Eisenlohr (2019). "Who Owns U.S. CLO Securities?," FEDS Notes 2019-07-19. Washington: Board of Governors of the Federal Reserve System.

Nanda, V., W. Wu, and X. Zhou, 2019, Investment commonality across insurance companies: Fire-sale risk and corporate yield spreads, Journal of Financial and Quantitative Analysis, 54(6), 2543—2574.

Shin, C., 2020, Fire-sale vulnerabilities of DFAST BHCs, Federal Reserve Board of Governors.

1. Authors: Fang Cai, Gene Kang, Gazi I. Kara, Nathan Swem, and Filip Zikes. We thank Geng Li, Teodora Paligorova, John Schindler, Chaehee Shin, Skander van den Heuvel, and Alex Vardoulakis for useful comments and suggestions. We also thank Keely Adjorlolo, Matthew Hoops, Lucas Nathe, Maria Perozek, and Irina Stefanescu for generous help with data. Return to text

2. Board of Governors of the Federal Reserve System (2019), Financial Stability Report (Washington: Board of Governors, November), https://www.federalreserve.gov/publications/files/financial-stability-report-20191115.pdf. Return to text

3. See https://www.federalreserve.gov/publications/financial-stability-report.htm. A more comprehensive analysis of business debt is provided in the box “Vulnerabilities Associated with Elevated Business Debt” in the May 2019 report; see Board of Governors of the Federal Reserve System (2019), Financial Stability Report (Washington: Board of Governors, May), pp. 22-25, http://federalreserve.gov/publications/files/financial-stability-report-201905.pdf. Return to text

4. In the second quarter, consumer credit decreased at a seasonally adjusted annual rate of 5.6 percent. https://www.federalreserve.gov/releases/g19/current/ Return to text

5. See for example Greenwood et al (2012), Duarte and Eisenbach (2019), and Shin (2020). Return to text

6. See, for example, Board of Governors of the Federal Reserve System (2019), Financial Stability Report (Washington: Board of Governors, May), pp. 22-25, http://federalreserve.gov/publications/files/financial-stability-report-201905.pdf. Return to text

7. Our analysis does not directly compare the aggregate credit quality of HD and BD. Rather, our analysis illustrates the implications of several constraints that exist, primarily for holders of BD, that can result in fire sales during periods of stress when credit conditions deteriorate. Return to text

8. We note that more liquid holdings at banks can represent a greater fire-sale risk relative to less-liquid holdings in the event that banks sell more liquid holdings first (or in greater proportion) in a stress event. However, greater holdings of less-liquid assets are likely to contribute to run-risk (if banks are unable to liquidate), which is a subject we do not explore in this analysis. Return to text

9. In 2019, the Federal Reserve Board announced that some less complex Bank Holding Companies and Intermediate Holding Companies will not be subject to the stress test in that year. As a result, only 18 banks participated in the stress test and hence the aggregate results for 2019 are not directly comparable to those from previous years. Return to text

10. 37% reflects the net holdings of HD by GSEs that include mortgages and student debt after subtracting agency MBS and GSE debt held by banks, insurance companies and other financial institutions. We redistribute MBS and GSE debt to ultimate holders using the Financial Accounts of the United States. We also use this data to redistribute ABS backed by consumer credit loans to the ultimate holders. Return to text

11. Ginnie Mae is a government-owned corporation within HUD, but is loosely included here as GSEs. There has been renewed effort by the current administration to end the conservatorship and privatize the GSEs. The economic fallout from the pandemic adds to the uncertainty about the timing of the GSEs’ exit. Return to text

12. We make these groupings for qualitative comparisons. The corresponding BD and HD buckets do not precisely match with regard to default rates. Unrated HH debt category corresponds to debt owed by borrowers without a credit score. Return to text

13. While covenant breaches would mitigate liquidity draws for banks, they would exacerbate funding problems for corporations. Return to text

14. We assume that securitized forms of debt are more liquid than non-securitized debt, all else equal. Return to text

15. For more information, see the box “The Federal Reserve’s Monetary Policy Actions and Facilities to Support the Economy since the COVID-19 Outbreak” in Board of Governors of the Federal Reserve System (2020), Financial Stability Report (Washington: Board of Governors, May), pp. 9-15, https://www.federalreserve.gov/publications/files/financial-stability-report-20200515.pdf. Return to text

16. See Board of Governors of the Federal Reserve System. Term Sheet: Secondary Market Corporate Credit Facility. https://fraser.stlouisfed.org/archival/6116/item/589433 (April 9, 2020). Return to text

Cai, Fang, Gene Kang, Gazi I. Kara, Nathan Swem, and Filip Zikes (2021). "Household and Business Debt: A Fire-Sale Risk Analysis," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, February 1, 2021, https://doi.org/10.17016/2380-7172.2625.

Disclaimer: FEDS Notes are articles in which Board staff offer their own views and present analysis on a range of topics in economics and finance. These articles are shorter and less technically oriented than FEDS Working Papers and IFDP papers.