FEDS Notes

May 08, 2026

Subprime Auto Lending: Trends in Buy Here Pay Here Auto Lending

Olena Chyruk, David Cox, Lily Liu, James Wang, and Stephen Zoulalian

Introduction

Buy Here Pay Here (BHPH) auto dealers occupy a unique position in the auto market by serving as both the seller and financier of vehicles to their customers. This contrasts with traditional auto dealers, who connect buyers to financing options from third-party banks, credit unions, or auto finance companies, including the captive financing arms of auto manufacturers. While BHPH auto dealers have operated in the United States for decades, the sector has attracted renewed attention since the high-profile bankruptcy of one of the largest BHPH auto dealers, Tricolor, alongside allegations of fraud in 2025.1 Against this backdrop, this note investigates what distinguishes BHPH auto dealers from traditional auto finance, examining their customer profile, risk mitigation strategies, and their bank funding sources to better understand the risks of this increasingly scrutinized, high-risk sector.

We highlight three main findings. First, using credit registry data, we document that the typical BHPH customer profile is higher risk, with lower credit scores and higher delinquency rates compared to traditional auto finance. Direct financing allows for more flexible underwriting standards, including providing credit to subprime borrowers or those with limited or no credit histories. In many cases, these subprime borrowers would likely have had difficulty accessing credit from banks, credit unions, or captive finance companies. Despite deep subprime borrowers constituting a majority of BHPH customers, in recent years BHPH auto dealers have expanded to less risky borrowing segments reducing their share of deep subprime borrowers from 70% of their loans in 2018 to slightly above 50% of their loans in 2025.

Second, we show that BHPH auto dealers attempt to offset and compensate for their risky borrower base with higher interest rates and more aggressive repayment schedules – often with weekly loan repayments that create more opportunities to miss a payment. Using vehicle repossession data, we further document that BHPH auto dealers more frequently employ auto repossessions, a loss mitigation tool, compared to traditional auto finance.

Finally, using name-matched corporate lending data on individual BHPH auto dealers in regulatory reports, we identify that the largest banks are a source of funding for BHPH auto dealers. Despite banks being historically cautious toward subprime consumer lending, our results find that banks have indirect exposure to this high-risk sector through inventory and loan receivable-based lending. While our name-match process is not intended as a full inventory of funding to BHPH auto dealers, we document that the more than $2 billion in loan commitments that we identify were rated by these large banks as being of lower risk compared to loans to traditional auto dealers. We attribute the loans' lower perceived risk partly to structural protections that banks build in, such as lower loan advance rates resulting in over-collateralization, to mitigate the higher risk profile of the underlying BHPH vehicle loans. Combined with these loan protections, we posit that the higher repossession rate of BHPH dealers also serves to improve the collateral quality of the auto loans that underpin bank loan commitments.

However, in recent years, our bank-reported risk measures of BHPH lenders have converged closer to those of traditional auto lenders. This convergence has also accelerated in the aftermath of Tricolor's bankruptcy, suggesting that banks have become more cautious in their risk assessment of this high-risk sector following the large write-downs for Tricolor's lenders and associated public scrutiny for BHPH auto lenders.2

Data and Methodology

Our analysis requires identifying the auto loans originated by BHPH auto dealers to their vehicle customers as well as identifying the bank loans to BHPH auto dealers. For the former, we use data from the Federal Reserve Bank of New York – Equifax Consumer Credit Panel (CCP) to identify loans originated by BHPH auto dealers. This loan-level data includes loan characteristics and loan performance metrics such as default and vehicle repossession. For the latter, while we recognize that BHPH auto dealers have a variety of bank and nonbank funding sources, we focus on bank lending as a proxy to gain insights into overall BHPH funding characteristics. This is because the FR Y-14Q Corporate Schedule H.1 (Y-14Q) allows for identification of large bank lending facilities to individual BHPH auto dealers and includes bank-assessed risk characteristics.3

Data from the CCP does not allow for the granular identification of BHPH auto dealers. However, using the CCP auto tradeline data, we are able to isolate loans from independent auto dealers separate from credit unions, banks, captive finance companies, other auto finance companies, and lenders with missing industry codes. We label this restricted sample independent auto dealer lending, which we use as a proxy for direct loans from BHPH auto dealers. Our definition is conservative as we only attribute a loan as being originated by a BHPH auto dealer if the CCP defines the lender as an auto dealer, so we may miss some instances where an auto finance company is a subsidiary of a BHPH dealer. We compare these independent dealer-originated loans to all other auto loans, representing traditional auto finance. As of 2025:Q3, our BHPH auto dealer sample represented approximately 2% of the total $1.6 trillion auto loan market and 5% of the subprime market within the CCP. Nationally, other data sources find that BHPH dealers originate approximately 6% of auto loans.4 Although BHPH auto dealers make up a small portion of the total market, their footprint is growing rapidly with loan balances increasing by 214% since 2018, compared to traditional auto finance growth of 34% over the same period.

In the Y-14Q, we identify bank lending to BHPH auto dealers by name-matching loan obligors to individual known BHPH dealerships in the corporate loan data. Our coverage includes approximately a dozen BHPH auto lenders and their local subsidiary dealerships for a total of 82 obligors, including some of the largest BHPH auto dealers such as DriveTime, Byrider, and America's Car-Mart as well as the now-defunct Tricolor. This represents lending from more than a dozen banks over time and over $2 billion in total commitments as of the end of 2025. We caution that our matched list is not an exhaustive total of BHPH auto dealers because of the challenges of identifying and matching BHPH auto dealers. For example, some lines of credit in the Y-14Q may be through special purpose entities with opaque names and corporate structures. Our empirical strategy assumes that the facilities that we do identify are broadly representative of overall bank lending facilities to BHPH auto dealers. We compare this identified BHPH auto dealer sample with bank corporate loans to a much larger control sample of overall auto dealers. We identify the control sample as the set of obligors in the Y-14Q data that have ever received an auto floor plan loan (loans backed by vehicle inventory) and have an industry classification associated with auto dealers or sales financing.

Results

Using our identified BHPH auto dealer sample in the CCP data, we identify key loan characteristics for loans originated by BHPH auto dealers and compare them to the larger control group of loans originated by traditional auto finance. Table 1 shows these results segmented by subprime and prime borrowers, which reflects the significantly different borrower populations between the two types of auto lenders. For BHPH auto dealers, approximately 78% of their lending volume is originated to subprime borrowers, while the corresponding figure is only 27% for traditional auto lenders. This customer risk profile difference is even more pronounced when considering more granular credit score categories, as we discuss next.

Table 1: Auto Loan Characteristics by Lender Type and Credit Rating

| BHPH Auto Dealers | Traditional Auto Lenders | ||||

|---|---|---|---|---|---|

| Subprime | Prime | Subprime | Prime | ||

| Average Origination Principal Balance | $15,402 | $19,340 | $17,424 | $21,122 | |

| Average Monthly Payment | $405 | $394 | $350 | $368 | |

| Average Term | 55 | 62 | 64 | 61 | |

| Weighted Average Derived Interest Rate | 25.39% | 11.81% | 14.60% | 5.65% | |

| Share of Balances with Weekly or Biweekly Payments | 14.43% | 7.42% | 0.67% | 0.38% | |

| Share of Balances | 77.52% | 22.48% | 26.94% | 73.06% | |

Note: Loan characteristics by lender type and credit rating group include all loans reported in the data from Q1:2018 through Q3:2025. Loan observations are taken from either origination or the first available observation over this sample period. If term or payment frequency information is missing for the loan in the first available observation, then the earliest observation with complete information is used to backfill the observation. Using this method, about 63% of the sample has term information and 35% has payment frequency information. The average derived interest rate is weighted by the principal balance amount and estimated for all loans with a non-zero term, monthly payment, and principal balance, and in cases when the principal balance is greater than the payment amount.

Source: New York Fed Consumer Credit Panel/Equifax

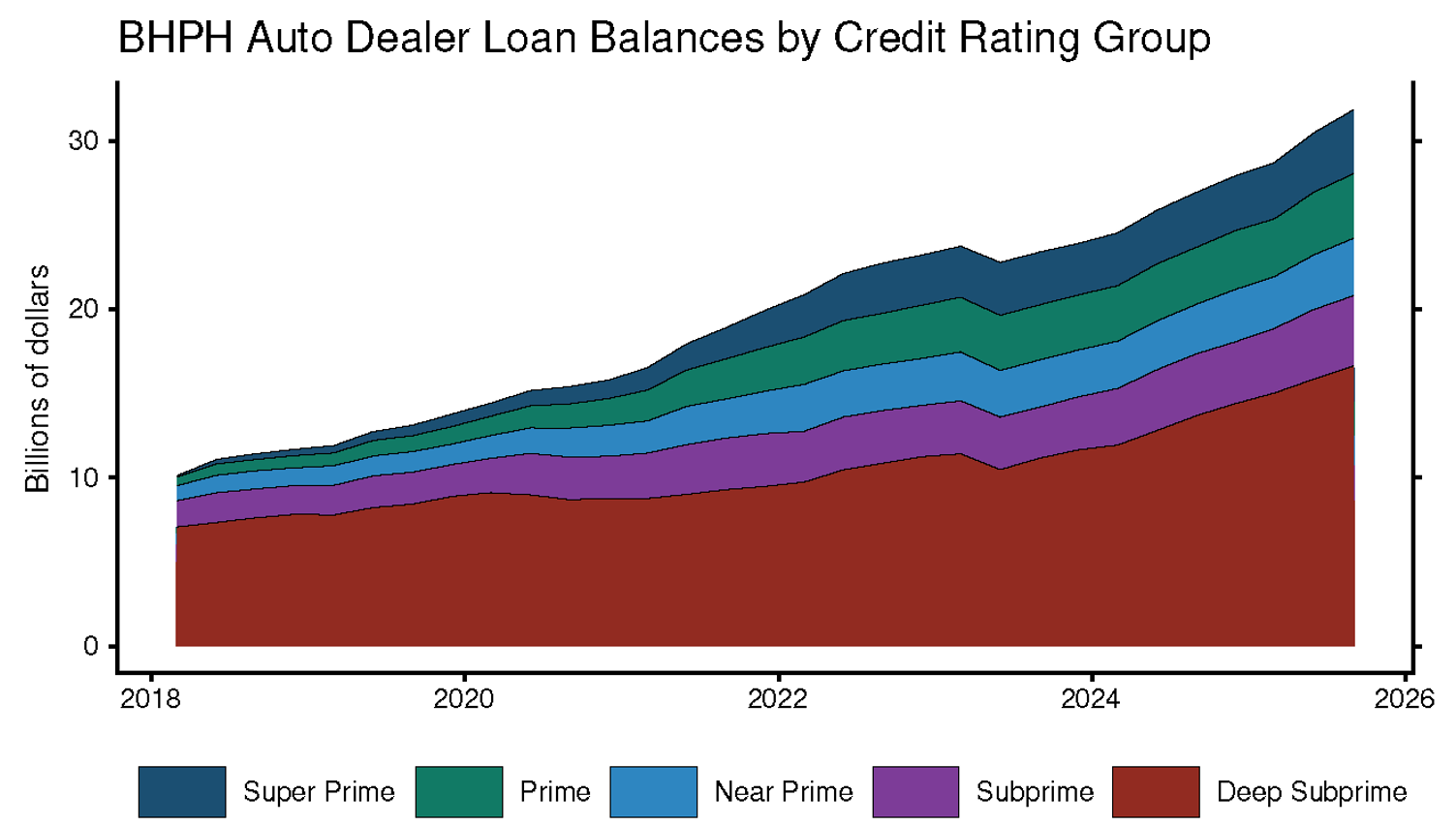

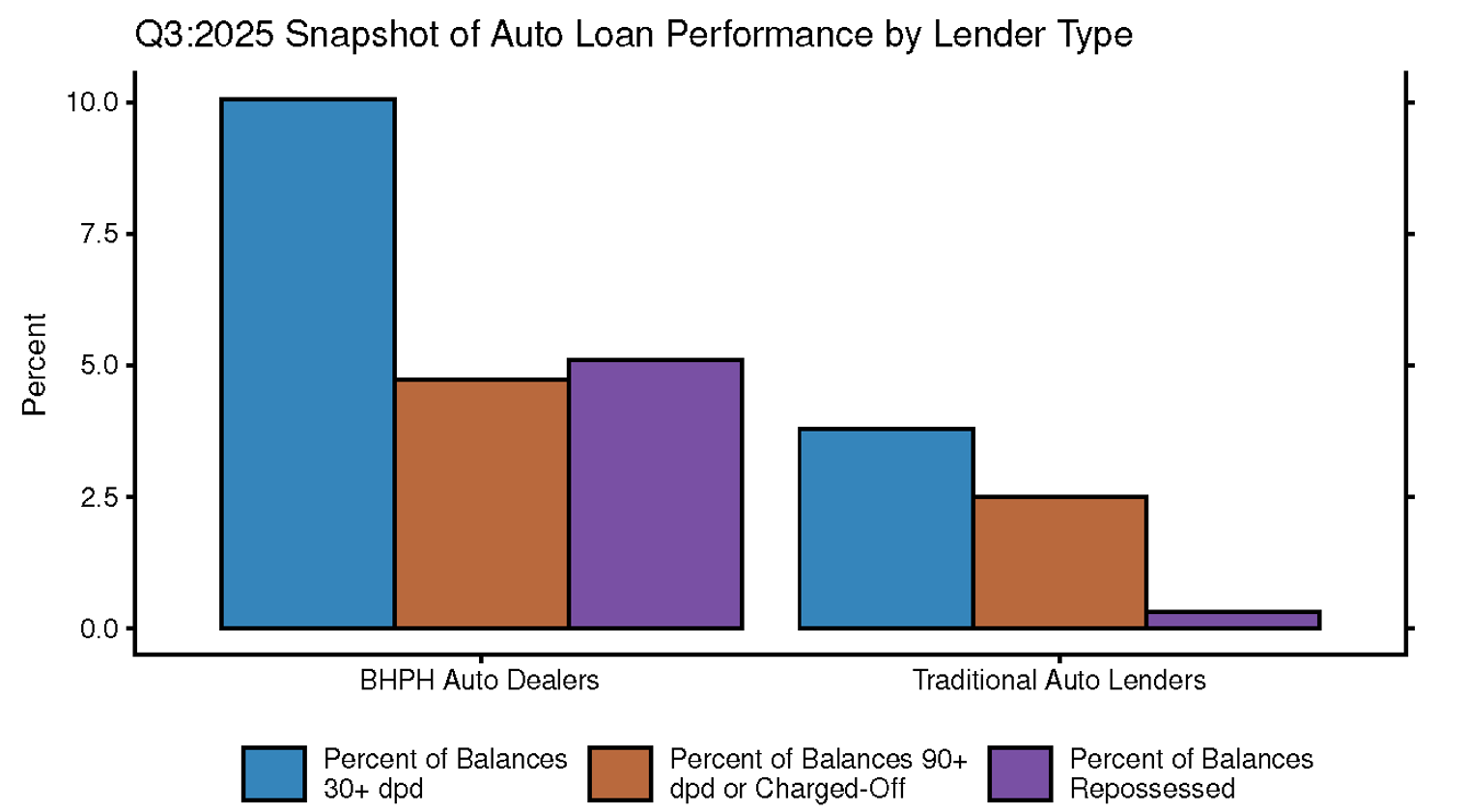

Figure 1 shows the breakdown of overall BHPH auto dealer loans by credit score category. Within overall borrowing of approximately $32 billion in loans outstanding by BHPH auto dealers in 2025, loans to deep subprime borrowers, or those with credit scores less than 580, account for more than 50%. While this degree of loan volume to the riskiest segment of subprime borrowers may seem large, this represents a decrease since 2018 (when deep subprime accounted for approximately 70% of total loan volume). Comparatively, the deep subprime share of loans issued by traditional auto finance has remained flat at approximately 15% since 2018. This suggests that in recent years, BHPH auto dealers are not ceding deep subprime borrowers to traditional auto finance but may be attempting to broaden their borrower base and become less concentrated toward this high-risk segment. Despite this, recent loan performance metrics unsurprisingly reflect the higher risk associated with BHPH loans. As shown in Figure 2, 10% of BHPH loan balances in 2025:Q3 are delinquent,5 compared to 3.8% for traditional auto lender loans. Loan origination balances in Table 1 are also correspondingly different, with a gap of approximately $2,000 between subprime borrowers from traditional auto lenders and those from BHPH auto dealers. While this gap may reflect differences in loan underwriting between the two types of lenders, it also captures that BHPH auto dealers specialize in used cars as opposed to traditional auto lenders who maintain a mix of new and used car inventories. For prime borrowers, the results are similar with lower loan origination amounts for BHPH auto dealers compared to borrowers who acquired credit from traditional auto finance.

Note: Credit rating groups are defined as super prime if the reported Equifax Risk Score is >= 720, prime if >=660 and <720, near prime if >=620 and <660, subprime if >=580 and <620, and deep subprime if <580. Total balances for all loans reported in a given quarter are shown. Key identifies in order from top to bottom.

Source: New York Fed Consumer Credit Panel/Equifax

Note: Loan status and balances are taken as of Q3 2025. Loan balances reported as more than 30 days through 120 days past due are in the 30+ dpd group. Loan balances reported as more than 90 days through 120 days past due or as charged off are in the 90+ dpd group. Loan balances reported as repossessed are in the repossessed group. Key identifies in order from left to right.

Source: New York Fed Consumer Credit Panel/Equifax

Our identification of loans from BHPH auto dealers also allows us to examine the steps that BHPH auto dealers take to mitigate and compensate for their higher credit risk. Average monthly payments and interest rates are correspondingly higher conditional on credit score segment. While we do not observe down payments in the CCP data, this is another dimension where subprime borrowers are likely to face greater requirements from BHPH auto dealers than from traditional auto finance. For subprime borrowers, BHPH auto dealers charge on average an interest rate of 25%, which is more similar to high-interest credit cards than the 5.6% interest rate – closer to secured mortgage loans — charged to prime borrowers by traditional auto finance (see Table 1).

In addition to charging higher interest rates to offset credit risk, BHPH auto dealers also originate loans with more frequent payment dates. While payment frequency data is only available for 39% of BHPH observations in the CCP sample period, approximately 14% of subprime loan balances and even 7% of prime balances are on weekly or biweekly payment plans, compared to traditional auto lenders, where almost all loans with reported payment frequency are on monthly payment plans. Higher payment frequencies provide more consistent cash flow and allow for earlier identification of borrower payment difficulty, information which the BHPH dealer may then use to mitigate potential losses.

One such loss mitigation strategy is auto repossession, in which BHPH dealer behavior appears to noticeably differ from that of traditional auto lenders. Figure 2 shows the 2025:Q3 snapshot of the percentage of balances that are delinquent, in default or charged off, and the percentage of balances with active repossession status. While BHPH loans have delinquency and default rates that are respectively 2.65 and 1.88 times higher than those of loans from traditional auto lenders, BHPH loans are 16.63 times more likely to be in active repossession status. In 2025:Q3, approximately 5% of BHPH balances were in active repossession, compared to less than half a percent for traditional auto lender balances. This aligns with media reporting that the integrated BHPH model allows auto dealers to initiate repossessions earlier, more frequently, and often more aggressively than traditional auto lenders.6

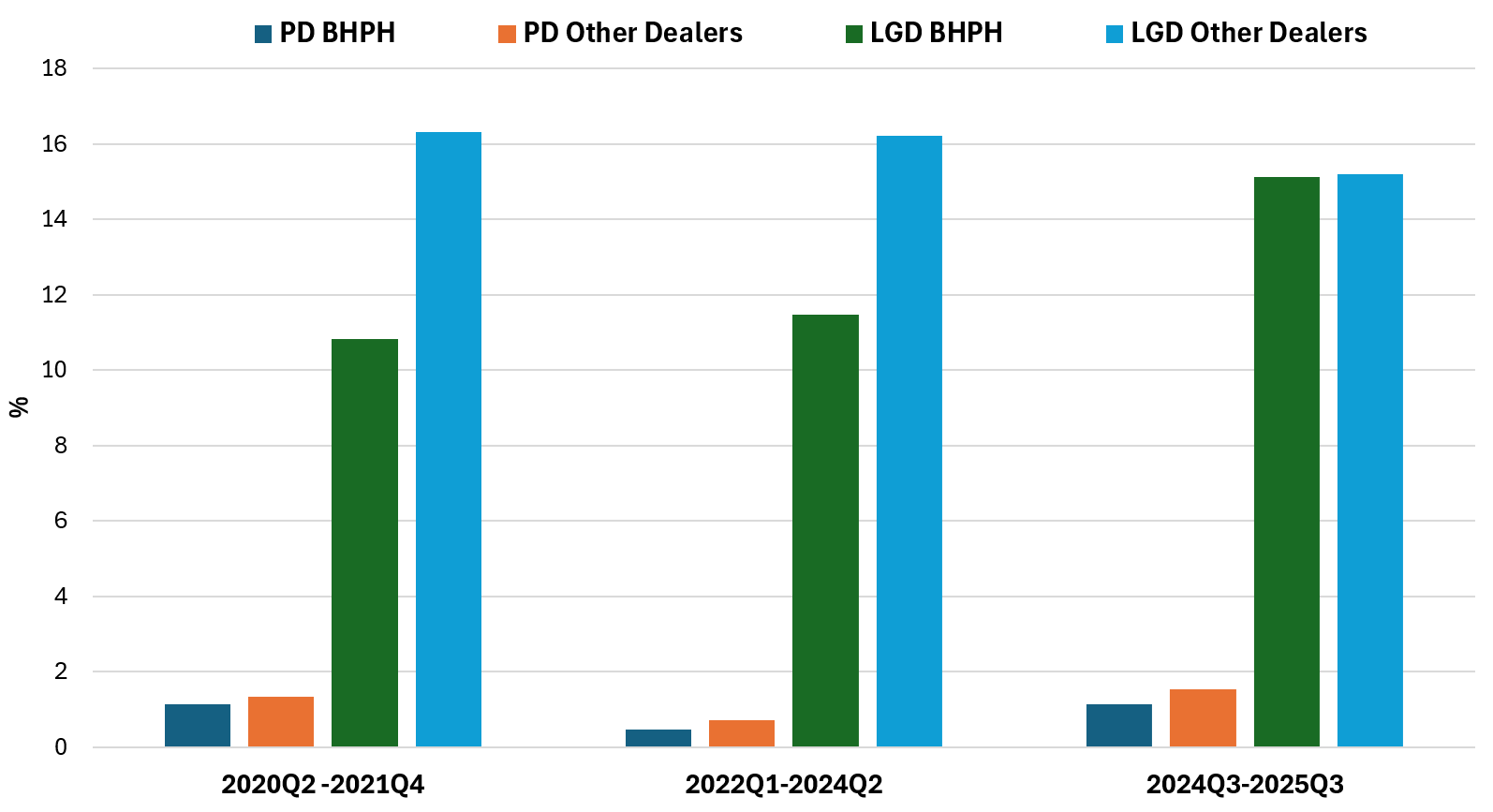

To fund these loan originations, BHPH auto dealers often rely on credit lines from banks to provide dealer floor plan financing, working capital, and bridge financing before asset securitization to a broader set of investors. We identify these credit lines, which can be backed by the vehicles themselves or by loan payment receivables, in the Y-14Q corporate lending data to examine their risk characteristics. Figure 3 shows the predicted probability of default (PD) and loss given default (LGD) of the bank loans as assessed by the banks themselves. Compared to other auto dealers, BHPH auto dealers have a slightly lower predicted probability of default since 2020, with correspondingly lower interest rate spreads and better internal loan ratings.

Note: Both the probability of default and loss given default are calculated as averages across corporate loan borrowers and represented in percentage terms. The Buy-Here Pay-Here sample is constructed by name-matching borrower names to industry-known Buy-Here Pay-Here auto dealers. The sample of all other auto dealers includes any borrower that received a dealer floor plan financing loan at least once in the data and have industry NAICS codes of 441110 “New Car Dealers”, 441120 “Used Car Dealers”, 441210 “Recreational Vehicle Dealers”, 522220 “Sales Financing”, 522291 “Consumer Lending”, 525990 “Other Financial Vehicles”, 532112 “Passenger Car Leasing”, and excludes the identified Buy-Here Pay-Here dealers. The sample period is Q2:2020 –Q3:2025. Key identifies in order from left to right.

Source: FR Y-14Q Schedule H.1

While it may seem paradoxical that bank loans to BHPH dealers would be deemed similar to, or lower risk than, loans to other auto dealers, we speculate that bank lending to BHPH dealers incorporates more structural protections to offset risk. For instance, in 2025:Q3, 81% of the loans to BHPH dealers are fully backed by a guarantor compared to 62% for other dealers. 65% of the BHPH facilities are classified as asset-based lending – a form of financing backed by inventory or loan receivables that are often overcollateralized relative to the value of the loan – compared to around 50% for other auto dealers. Finally, in our sample, approximately 13% of BHPH dealers secure financing through special purpose entities (SPEs) compared to less than 1% for loans to other auto dealers. SPEs legally isolate and protect the underlying collateral in the event of bankruptcy. These protections are commonplace in bank loans to BHPH dealers and can be combined to create multiple layers of security. Loans to Tricolor, for instance, were typically advanced at only 60-80% of the underlying auto loans' value and were often structured through SPEs. While these safeguards are not foolproof against loss, particularly through misrepresentation7, they nonetheless help mitigate lender exposure by limiting advance rates and preserving priority claims on legitimate assets.

Our analysis of BHPH consumer auto loans leads us to suggest another reason: the earlier, more frequent, and more aggressive vehicle repossession process also contributes to better risk ratings for loans to BHPH auto dealers. While credit protections are likely an important factor, banks may view the integrated model of BHPH auto dealers as having advantages in recovering the underlying vehicle in the event of consumer default. The repossession and subsequent vehicle sale could reduce loss-given-default for the consumer auto loans, which should translate to reduced credit risk for bank lending to BHPH dealers when these consumer auto loan receivables serve as collateral.

In recent years, however, our sample of bank-reported risk metrics for BHPH auto dealers have all worsened, with probabilities of default, loss given default, interest rate spreads and internal ratings all converging closer to those of traditional auto lenders. For example, Figure 3 shows the reported PD and LGD for BHPH rising relative to those of traditional auto lenders. Notably, since Tricolor's bankruptcy, this trend has only accelerated, with the reported probability of default of loans to BHPH borrowers increasing by nearly 150% from the second to third quarter of 2025. This rapid convergence suggests that banks have become more guarded towards the sector, which could be in direct response to Tricolor and the increased scrutiny regarding BHPH repossessions.8

Conclusion

Using consumer credit registry data and regulatory data on corporate bank loans, we document several key trends for BHPH auto dealers. We find that their business model depends heavily on a high-risk, deep subprime population that may be unable to access traditional auto finance options. These deep subprime borrowers constitute a majority of BHPH customers, although their share has been declining in recent years as BHPH auto dealers have expanded to less risky borrowing segments. BHPH-originated loans exhibit substantially higher delinquency rates compared to traditional auto finance. To mitigate and compensate for this elevated credit risk, BHPH auto dealers rely on higher interest rates, more frequent repayment schedules, and significantly greater use of vehicle repossessions.

By matching BHPH auto dealers with corporate obligor names in regulatory data, we find that large banks maintain direct exposure to this sector through corporate lending. Notably, these loan commitments show lower probabilities of default and lower loss given default compared to loans to traditional auto dealers, which we attribute to more structural protections, such as loan guarantees, over-collateralization, the use of SPEs, and BHPH auto dealers' advantages in vehicle repossessions. At the same time, bank ratings of BHPH credit quality have deteriorated over the last few years, including immediately after the Tricolor bankruptcy, suggesting BHPH's risk differential may not be permanent as banks re-adjust their outlook of BHPH auto dealers. As the sector continues evolving post-Tricolor, our findings highlight the importance of understanding this unique business model, as well as the need for continued monitoring of both consumer-level risks and the interconnections between BHPH dealers and the banking system.

1. https://www.justice.gov/usao-sdny/media/1421041/dl. Return to text

2. According to FT article, Fifth Third Bank and JPMorgan Chase both recorded losses of around $200 million as a result of their exposure to Tricolor, see https://www.ft.com/content/ca014f40-7d51-489b-b76a-5def9377daff. Return to text

3. The CCP is anonymous consumer credit registry data capturing a 5% snapshot of consumers with credit score reporting. The Y-14Q is a regulatory schedule designed to collect data from the largest bank holding companies in the United States with total assets greater than $100 billion. Return to text

4. https://www.federalreserve.gov/publications/files/consumer-community-context-20231128.pdf. Return to text

5. We classify a loan as delinquent if it is 30-119 days past due. Return to text

6. For example, Tricolor was known to equip sold vehicles with GPS devices and predominantly operated in states with more relaxed regulations around car repossessions. See Tricolor Collapse Exposes Risks in Opaque 'Buy Here, Pay Here' Model - Bloomberg (https://www.bloomberg.com/news/articles/2025-10-10/tricolor-collapse-exposes-risks-in-opaque-buy-here-pay-here-model) and Presale: Tricolor Auto Securitization Trust 2025-2 | S&P Global Ratings (https://www.spglobal.com/ratings/es/regulatory/article/-/view/sourceId/13500998). Return to text

7. https://www.justice.gov/usao-sdny/media/1421041/dl. Return to text

8. https://www.banking.senate.gov/newsroom/minority/with-trump-sidelining-cfpb-warren-launches-probe-into-the-auto-lending-industry-as-car-repossessions-skyrocket. Return to text

Chyruk, Olena, David Cox, Lily Liu, James Wang, and Stephen Zoulalian (2026). "Subprime Auto Lending: Trends in Buy Here Pay Here Auto Lending," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, May 08, 2026, https://doi.org/10.17016/2380-7172.4047.

Disclaimer: FEDS Notes are articles in which Board staff offer their own views and present analysis on a range of topics in economics and finance. These articles are shorter and less technically oriented than FEDS Working Papers and IFDP papers.