FEDS Notes

August 06, 2021

Use of the Federal Reserve's repo operations and changes in dealer balance sheets

Mark Carlson, Zack Saravay, and Mary Tian

Before the 2008 financial crisis, the Federal Reserve (Fed) regularly conducted repurchase agreements (repos) in a fairly modest size with primary dealers to adjust the supply of reserves in the banking system and to keep the federal funds rate at the target set by the FOMC.1 During the economic downturn that followed the financial crisis, the Fed engaged in large scale asset purchases in order to provide additional monetary accommodation, and those purchases significantly increased the supply of reserves and eliminated the need for the Fed to engage in repo operations to increase reserves in the system. In 2015, the FOMC started to normalize monetary policy by raising its target for the federal funds rate. As normalization progressed, the Fed began to reduce the size of its balance sheet in 2017, and its total assets declined from about $4.5 trillion in October 2017 to $3.8 trillion in September 2019. While the size of the balance sheet did decrease slowly, the FOMC indicated in January 2019 that it intended to maintain an ample reserves regime that included a sufficient level of reserves such that repo operations would not be necessary to fine-tune the supply of reserves.

In September 2019, funding markets experienced significant pressures and the federal funds rate printed above the FOMC's target range. In response, the Fed re-started daily repo operations with primary dealers to provide additional reserves to the system, helping ensure that the federal funds rate stayed in the FOMC's target range and supporting the smooth functioning of short-term funding markets. In March 2020, the Fed markedly increased the size of its repo operations, especially term repo operations, in response to disruptions to Treasury market functioning that occurred as market participants reacted to news of the spread of the COVID-19 virus.

In this note, we use supervisory data to understand dealer usage of the Fed's repo operations and how those operations affected dealer balance sheets in the pre-COVID versus post-COVID outbreak periods. We find that usage of Fed repo had different implications for overall dealer repo borrowing behavior in the two periods. During the pre-COVID period, dealer borrowing from Fed repo is strongly associated with increases in the dealers' total repo borrowing and we observe only limited substitution away from other funding sources. This pattern switches in the post-COVID period, as borrowing from the Fed is much more closely associated with a partial reduction in borrowing from other sources than in the pre-COVID period, especially during the high stress period in March 2020. (It should be kept in mind however that these results are correlations and our analysis cannot determine whether dealers borrowed more from the Fed because other funding was not available or whether the dealers reduced borrowing from others because they had access to the Fed.) We also find that, in both periods, increased dealer borrowing from the Fed corresponded with an increase in dealer repo lending to their customers, although the majority of such on-lending in the post-COVID period went to institutions affiliated with the dealers, especially their bank affiliates.

Section 1. Review of the changes in Fed repo operations and dealer usage

Overnight funding markets experienced extreme upward pressure on September 16 and 17th 2019; the federal funds rate printed above the FOMC's target range and the secured overnight financing rate (SOFR) jumped more than 2.5 percentage points to above 5 percent.2 In response, the Fed announced that it was re-starting its repo operations; pressures in overnight funding markets quickly abated following the Fed's announcement on September 17 of a $75 billion repo operation.3 Soon thereafter, the Fed began conducting term repo operations in addition to its overnight operations.4 In October, the Federal Reserve announced that it would "conduct term and overnight repurchase agreement operations at least through January of next year to ensure that the supply of reserves remains ample even during periods of sharp increases in non-reserve liabilities, and to mitigate the risk of money market pressures that could adversely affect policy implementation."5 These Fed repo operations have been cited as stabilizing market conditions.

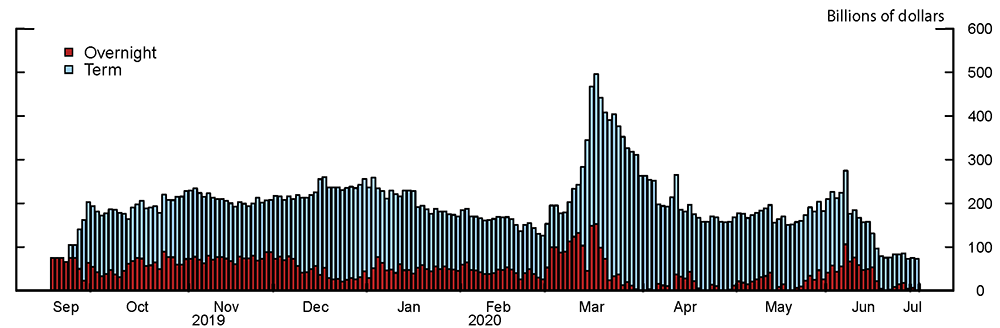

Substantial pressures in funding markets materialized suddenly in early March 2020 as concerns about COVID and the economic impacts of efforts to contain it surged. Simultaneously, liquidity in the Treasury market deteriorated markedly. In response, the Fed announced a series of increases in the size of its repo operations, offering several $500 billion one- and three-month term repo operations during the week of March 12, along with continuing its $175 billion limit on overnight operations.6 As shown in Figure 1, dealer take-up in these operations rose significantly in the following days, peaking at $495 billion on March 17, with notable take-up in both overnight and term repo.7 Over the next few weeks, dealers' participation in overnight operations declined, and dealers allowed some of the shorter-term operations to roll off, bringing total usage of the operations to about $200 billion by April. Use of Fed repo declined further in subsequent months as market functioning normalized.8

A notable change during and after the COVID pressures is that Fed repo operations shifted toward a much higher proportion of term repo (blue portions in Figure 1). As funding market liquidity deteriorated in early March, many market participants found it particularly difficult to obtain term financing. In the first few days after the Fed announced expanded term operations on March 12, there was significant take-up in the three-month term repo operations. As liquidity began to improve in the second half of March, dealers' overnight repo with the Fed declined sharply, and by the end of March, the outstanding balance was almost entirely term repo.

Despite the reports of severe liquidity problems in the Treasury market during mid-March, the Fed’s expanded repo operations were undersubscribed. Even during the March 17 peak, the total volume of Fed repo was $495 billion, short of the combined limit for overnight and term repo. Because repo with the Fed increases balance sheet size, it may have been the case that dealers were constrained or were reluctant to increase their usage of the repo operations.

Dealers’ usage of Fed repo operations during March was likely also affected by other Fed actions taken to support market functioning. As the Fed ramped up asset purchases and took other actions to stabilize markets, conditions in the Treasury market began to improve. In particular, asset purchases reduced dealers’ Treasury positions, and conditions in repo markets normalized.9 This was most likely another driver of the reduction in take-up in late March.

Section 2. Comparison of dealer behavior between pre- and post-COVID outbreak periods

In this section, we analyze how dealers' use of the Fed's repo was related to their borrowing and lending in the broader repo market during the pre-COVID and the post-COVID outbreak periods. On the liability side, we examine whether dealers used the Fed's repo operations to expand the size of their repo book, to replace borrowing from other sources, or both. On the asset side, we examine, in particular, whether dealers used the increase in funding obtained from the Fed's repo operations to increase their repo lending to their counterparties.

As we consider the behavior of the individual dealers, we limit our analysis to the dealers that provide daily balance sheet data in the FR 2052A report.10 Being able to associate balance sheet developments at a fairly high frequency with changes in repo usage is key for understanding how the Fed's repo operations related to dealer behavior. Although the total volume of Fed repo increased during mid-March, the dealers who used the operations most heavily remained largely stable and tended to be the dealers with the largest holdings of Treasuries.

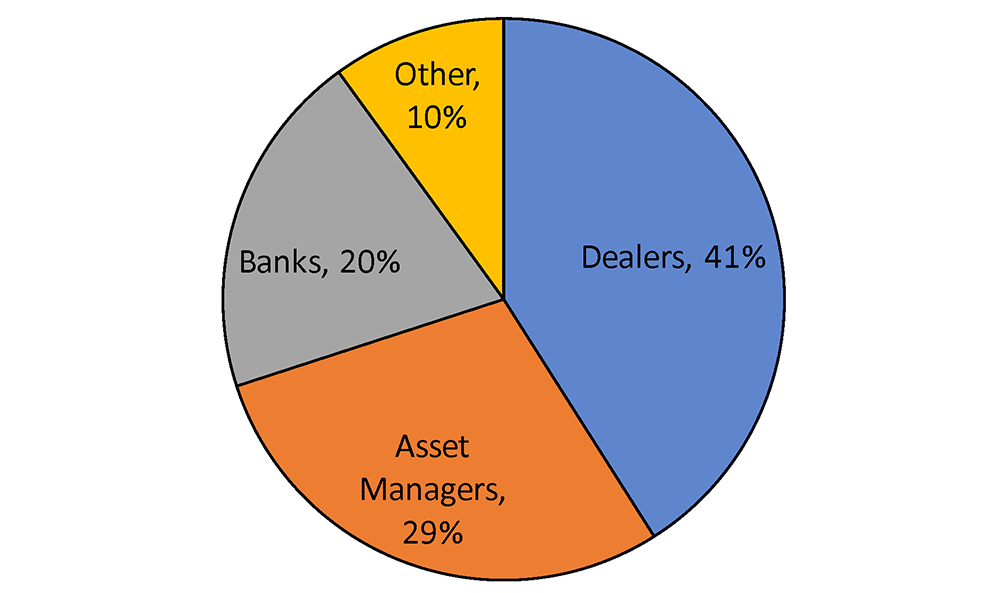

To better understand the context of the Fed's repo operations, it is helpful to consider the breakdown of dealers' typical repo counterparties. Figure 2 shows the percentage of dealers' average daily repo that is sourced from each counterparty type, for the period from Jan. 2016 to Sept. 2019.11 During this period, the 10 dealers in our sample averaged about $1.5 trillion in daily outstanding repo volume. The most common repo counterparties were other dealers, asset managers, and banks.12

Source: Form FR2052a

We start our analysis by examining how dealers' usage of the Fed's repo operations was related to their total borrowing in the repo market. To see how dealers acted, we regress daily changes in the total dollar amount of dealer repo borrowing, as well as borrowing from major counterparty types, on each dealer's daily change in dollars borrowed from the Fed's repo operations. The resulting regression coefficients essentially represent a decomposition of how, on average, each dollar increase in borrowing from the Fed is allocated towards the different components of dealer repo borrowing. We separate the analysis into a pre-COVID outbreak period (September 18, 2019 to February 14, 2020) and a post-COVID outbreak period (February 15, 2020 to April 30, 2020). We also consider separately the "high stress" sub-period of March 12-31, 2020.

The results, shown in Table 1, indicate that during the pre-COVID period, dealers used the Fed's repo operations primarily to increase their total repo borrowing and only to a lesser extent to shift borrowing away from other funding sources. In particular, as shown in row 1, for each $1 increase in borrowing from the Fed's repo operations, $0.76 was used to increase dealers' repo book size, while the remainder was used to shift borrowing away from other sources, most notably other dealers.13 During the post-COVID outbreak period, we find that borrowing from the Fed's repo operations continued to be associated with an increase in their total repo borrowing, though to a smaller extent (row 2). However, borrowing from the Fed was associated with a larger decline in borrowing from others post-COVID than pre-COVID, especially dealers' borrowing from other dealers (column 2). Even during the high stress sub-period, not all repo borrowing from the Fed was associated with a substitution away from other counterparties, although substitution was occurring to a greater extent than at other times.

Table 1. Results from Dealer Repo Regressions

| Increase in size of repo book (1) | Substitution away from: | Observations | |||

|---|---|---|---|---|---|

| Dealers (2) | Asset managers (3) | Banks (4) | |||

| Pre-COVID | 0.76*** | -0.11* | -0.03 | -0.05 | 1010 |

| Post-COVID | 0.53*** | -0.25*** | -0.06 | 0.06 | 510 |

| High Stress Period | 0.39*** | -0.45*** | -0.1 | 0.05 | 130 |

Note. The coefficients in each column are estimated in separate regressions. Dealer repo book size roughly equals the sum of dealer repo borrowing from each counterparty type plus dealer borrowing through Federal Reserve repo (there is also an "other" category not shown in the table). The symbols *** and * indicate statistical significance at the 1 percent and 10 percent levels, respectively.

Another way of assessing how the Fed's repo shaped dealer borrowing is to look at how it related to dealer borrowing from affiliated institutions and non-affiliated institutions. When looking at the substitution away from affiliated institutions in this way, we observe that in the pre-COVID period, the substitution away from other counterparties was split roughly evenly between affiliated and unaffiliated counterparties. There was a notable change in behavior in the post-COVID period when virtually all of the substitution was away from unaffiliated counterparties (Table 2, columns 1 and 2). In all periods, the majority of dealers' substitution away from unaffiliated counterparties was from other dealers.

Table 2. Dealer Repo–Affiliated vs. Unaffiliated Counterparties Split

| Total: Affiliated (1) | Total: Unaffiliated (2) | Observations | |

|---|---|---|---|

| Pre-COVID | -0.14*** | -0.10* | 1010 |

| Post-COVID | -0.01 | -0.31*** | 510 |

| High Stress Period | -0.01 | -0.53*** | 130 |

Note. The symbols *** and * indicate statistical significance at the 1 percent and 10 percent levels, respectively.

A similar exercise looks at the other side of dealers' balance sheets to see how changes in dealers' repo lending were associated with their use of the Fed's repo operations. As dealers appear to have used some of the funds obtained from the Fed to expand their total repo borrowing, this analysis provides insight into how those additional funds were used. The results in Table 3 show that a notable share of funds that dealers borrowed from the Fed did appear to be, in turn, lent by the dealers to their own customers. For instance, in the pre-COVID period (row 1), each $1 increase in dealers' repo borrowing from the Fed corresponds to a $0.55 increase in repo lending by the dealers.14 A decomposition of the increase in repo lending shows that most of it went to banks (column 4). This is particularly true in the high stress sub-period where each $1 increase in repo with the Fed increased repo lending to banks by $0.40. In the pre-COVID period, increased repo borrowing from the Fed by the dealers also corresponded with a notable increase in repo lending to other dealers and asset managers. There is a considerably weaker relationship with lending to these counterparties in the post-COVID period, when each $1 increase in dealers' borrowing from the Fed corresponds to only a $0.39 increase in repo lending. This seems consistent with developments in the Treasury market at that time, when the large-scale selling of off-the-run Treasury securities in March left dealers with increased financing needs and thus increased usage of the Fed's repo operations.15

Table 3. Dealer Reverse Repo Regression Results

| Total (1) | Increase in reverse repo with: | Observations | |||

|---|---|---|---|---|---|

| Dealers (2) | Asset managers (3) | Banks (4) | |||

| Pre-COVID | 0.55*** | 0.17*** | 0.10*** | 0.29*** | 1010 |

| Post-COVID | 0.39*** | 0.08 | 0.04* | 0.29*** | 510 |

| High Stress Period | 0.35*** | -0.07 | 0.02 | 0.40*** | 130 |

Note. The symbols *** and * indicate statistical significance at the 1 percent and 10 percent levels, respectively.

Further analysis in Table 4 sheds light on the share of the increase in dealers' repo lending going to their affiliated versus unaffiliated counterparties. During the pre-COVID period (row 1), $0.29 of the $0.55 of the increase in total repo lending went to affiliated counterparties (column 1), where affiliated banks account for nearly all of this increase (column 3). The remainder ($0.26 of the $0.55) went to unaffiliated counterparties (column 2). In contrast, during the post-COVID period (row 2) and in particular high stress period (row 3), there were signs of pullback from external capital markets—nearly all of the increase in total repo lending went to affiliated counterparties, while the share that went to unaffiliated counterparties was statistically insignificant. While dealers were still on-lending funds received from the Fed during the high stress period, nearly all of the on-lending was to affiliated banks.

Table 4. Dealer Reverse Repo–Affiliated vs. Unaffiliated Counterparties Split

| Total Affiliated (1) | Total Unaffiliated (2) | Banks Affiliated (3) | Banks Unaffiliated (4) | Observations | |

|---|---|---|---|---|---|

| Pre-COVID | 0.29*** | 0.26*** | 0.28*** | 0.01** | 1010 |

| Post-COVID | 0.31*** | 0.08 | 0.28*** | 0.01 | 510 |

| High Stress Period | 0.46*** | -0.11 | 0.39*** | 0.01 | 130 |

Note. The symbols ***, **, and * indicate statistical significance at the 1 percent, 5 percent, and 10 percent levels, respectively.

1. In a repo operation, the Federal Reserve lends funds to a dealer against Treasury securities, agency debt securities, or agency mortgage-backed securities. The provision of funds to the dealer is associated with an increase in the account balance maintained by the dealer's commercial bank at the Federal Reserve (i.e. the commercial bank's reserves). Return to text

2. Anbil, Anderson, and Senyuz (2020) provides more detail on the September 2019 money market turmoil. Return to text

3. https://www.newyorkfed.org/markets/opolicy/operating_policy_190917. Return to text

4. https://www.newyorkfed.org/markets/opolicy/operating_policy_190920. Return to text

5. https://www.federalreserve.gov/newsevents/pressreleases/monetary20191011a.htm. Return to text

6. See for instance, https://www.newyorkfed.org/markets/opolicy/operating_policy_200316. Return to text

7. For comparison, usage at the end of January 2020 was about $170 billion. Return to text

8. Fed repo usage fell to zero shortly after the Desk's announcement on June 11 of an increase in the minimum bid rate on repo operations. Return to text

9. Our analysis shows that total Fed asset purchases have a statistically significant negative association with aggregate Fed repo usage during the post-COVID period. Return to text

10. The FR 2052a report collects quantitative information on selected assets, liabilities, and funding activities at the consolidated holding company level and at the subsidiary level. Foreign Banking Organization Large Institution Supervision Coordinating Committee (LISCC) firms and US Firms with $700 billion or more in total consolidated assets or $10 trillion or more in assets under custody must submit daily reports. For additional detail, see https://www.federalreserve.gov/reportforms/forms/FR_2052a20200630_f.pdf. Return to text

11. Repo volume includes all collateral, though the vast majority is OMO-eligible collateral. Return to text

12. The counterparty types used in this note are representative of broader categories in the FR 2052a report. Dealers represent the "supervised non-bank financial institution" category, asset managers represent the "other financial entity" category, and "banks" are their own category. For more details, see the FR2052a reporting instructions. Return to text

13. For brevity, we only report the three largest counterparty types, by volume, with which dealers engage in repo activity. Return to text

14. The response of total repo lending by the dealers to a $1 increase in borrowing from the Fed is slightly smaller than the response in total repo borrowing. We do not know how the remaining funds were used. Return to text

15. While the increase in net repo borrowing was smaller per dollar of Fed borrowing in the post-COVID outbreak period, the total volume of repo borrowing, particularly from the Fed, was much greater. Return to text

Carlson, Mark, Zack Saravay, and Mary Tian (2021). "Use of the Federal Reserve's repo operations and changes in dealer balance sheets," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, Auguest 06, 2021, https://doi.org/10.17016/2380-7172.2961.

Disclaimer: FEDS Notes are articles in which Board staff offer their own views and present analysis on a range of topics in economics and finance. These articles are shorter and less technically oriented than FEDS Working Papers and IFDP papers.