IFDP Notes

June 01, 2017

Emerging Market Nonfinancial Corporate Debt: How Concerned Should We Be?1

Daniel Beltran, Keshav Garud, and Aaron Rosenblum

1. Introduction

Nonfinancial corporate (NFC) debt in emerging market economies (EMEs) has tripled since the global financial crisis (GFC), reaching roughly $25 trillion, or 112 percent of GDP, in mid-2016. Several factors have contributed to the surge: the low interest rate environment since the GFC, financial deepening and maturation of EMEs, on-going financial globalization, and policy-induced stimulus channeled through EME state-owned banks. The rapidity of the rise in EME corporate debt to now significant levels has raised concerns about the risk this debt poses for EME countries and the global economy (IMF, 2016; BIS, 2016). In particular, many fear that a rise in global interest rates could lead to higher debt-service costs, more depreciated currencies, capital outflows, and lower earnings. Such developments could put further pressure on EME corporates, especially those that have issued dollar-denominated debt, and potentially trigger broader financial stress (Shin, 2013; McCauley et al., 2015; Acharya et al., 2015).2

In this note, we assess these concerns. We begin by providing an overview of the run-up in EME corporate debt. We then focus on the vulnerability of EME corporate balance sheets to shocks, including increases in global interest rates and exchange rate depreciations. Note that in this paper we look at the vulnerabilities side only and not at how much resources different countries would have to address the problems, if some of the risks discussed were to materialize.3 We evaluate the extent to which corporate borrowers could experience financial distress using balance sheet and income statement data for roughly 8,500 firms and in 15 emerging market economies.4 Finally, we assess the degree to which moves in financial markets would exacerbate the vulnerabilities of EME corporates. To do so, we stress test EME corporate balance sheets by imposing shocks to firms' borrowing costs, earnings, and the exchange rate.

We find a moderate degree of vulnerability at present. Only a few EMEs exhibit significant levels of risky corporate debt as a share of total debt. The results become even more positive when we scale the share of risky debt by GDP to gauge systemic importance. By this metric, outside of China, risky debt for most EMEs is around a tenth of GDP, which is considerably lower than the share of 50 percent for the East Asian economies before the Asian Financial Crisis. That said, the amount of risky debt appears quite sensitive to earnings, interest rate, and exchange rate shocks. Under our stress exercise, risky debt rises to notable shares of GDP in a number of countries, importantly China but also Brazil, Turkey, India, and Korea. For EMEs overall, the earnings and interest rate shocks are the most material. EME corporates appear less vulnerable to currency devaluations, because the portion of EME corporate debt denominated in foreign currency has been steadily declining for over a decade.

Other studies on EME corporate vulnerabilities also stress test the shares of risky corporate debt (IMF, 2014; Chow, 2015; IMF, 2016), but provide little guidance on what constitutes an elevated share of risky debt, which makes it difficult to interpret their findings. Furthermore, these studies do not opine on which types of shocks may be most consequential. For example, in the event of a depreciation of EME currencies and higher global interest rates, which of these channels would be more detrimental for EME debt servicing capacity? We therefore make two contributions to the debate on the riskiness of EME corporate debt. First, we assess the health and resilience of the EME corporate sector by comparing two key metrics--leverage and the systemic importance of the risky debt-- to levels seen in the past, including for the East Asian economies on the eve of the Asian Financial Crisis. Alfaro et al. (2017) previously used the Asian Financial Crisis as a benchmark; they find that emerging markets post-GFC (2009-2014) have lower leverage ratios than the five Asian crisis countries in the run-up to the Asian Financial Crisis (1992-1997). Second, we try to assess which of the shocks we consider are most detrimental for the EME corporate sector.

2. A Bird's Eye View of EME Corporate Vulnerabilities

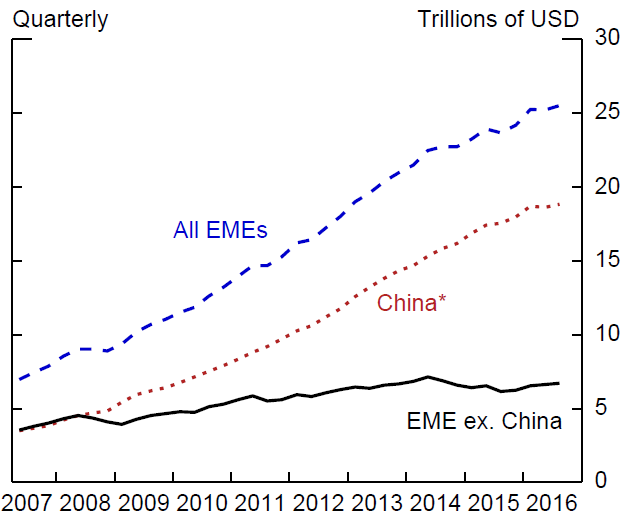

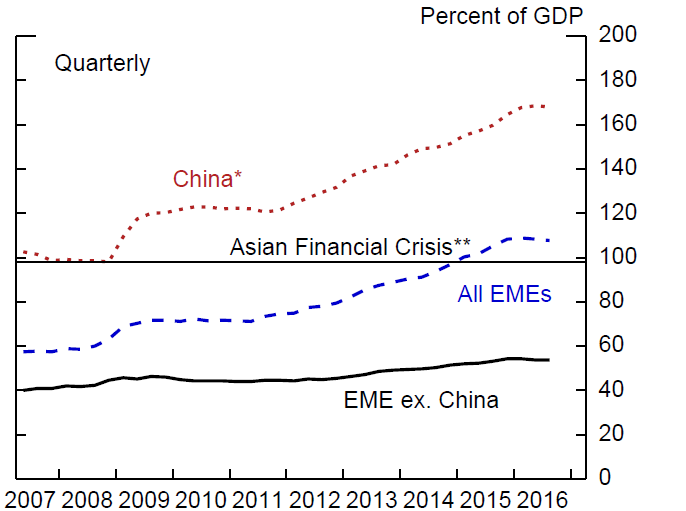

Since 2007, EME nonfinancial corporate debt (or NFC debt) has tripled in dollar value (Figure 1a) and roughly doubled as a share of EME GDP (Figure 1b). The majority of this increase is accounted for by China, where NFC debt is now 170 percent of GDP. NFC debt in several other EMEs (Figure 2) has also risen sharply. For some EMEs, the expansion in overall credit has exceeded that seen in emerging Asia and Mexico in the run-up to their crises.

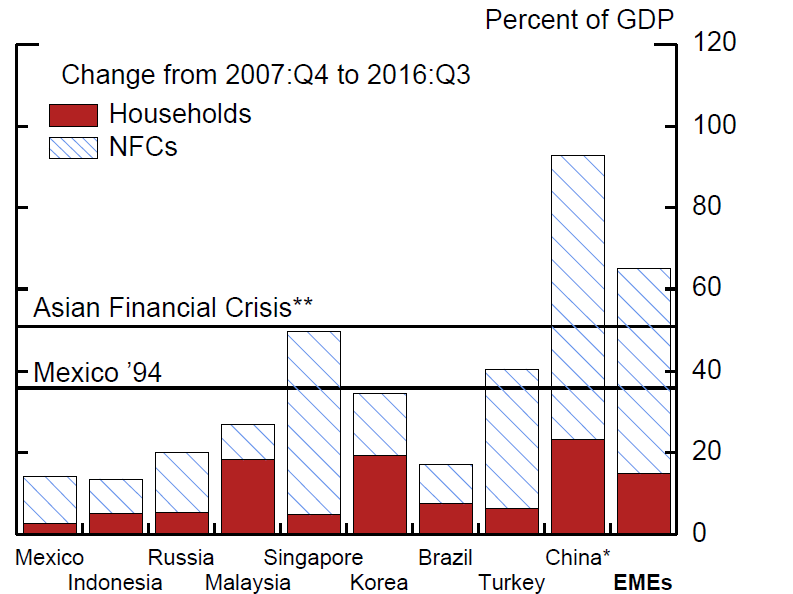

More reassuringly, though rising in nominal amounts, the portion of EME corporate debt denominated in foreign currency has been declining (Figure 3) and is smaller today than before previous financial crises (BIS, 2016). These findings suggest that the risks associated with currency mismatches in the EMEs may have been somewhat overblown. Consistent with this view, we note that EMEs have not suffered widespread corporate defaults despite substantial currency depreciations in some of them since mid-2011.

Source: BIS.

*China includes Hong Kong.

** The 1996 GDP-weighted average for Korea, Hong Kong, Singapore, and Thailand is close to 100 percent of GDP

Source: BIS.

*Includes Hong Kong

** Singapore, Malaysia, Indonesia & Korea. Horizontal lines denote credit growth over 8 years preceding each crisis.

Source: Ayala et al. (2015) and Claessens et. Al. (1999)

* Average of Indonesia, Korea, Malaysia, Philippines, and Thailand.

That said, sufficiently large depreciations would likely create problems for some firms, and the run-up in EME corporate debt is worrisome on other grounds as well. Firm-level data suggest that EME earnings have declined notably from their pre-crisis peaks (Figure 4), especially in China, which could have implications for the servicing of the corporate debt as discussed below.5

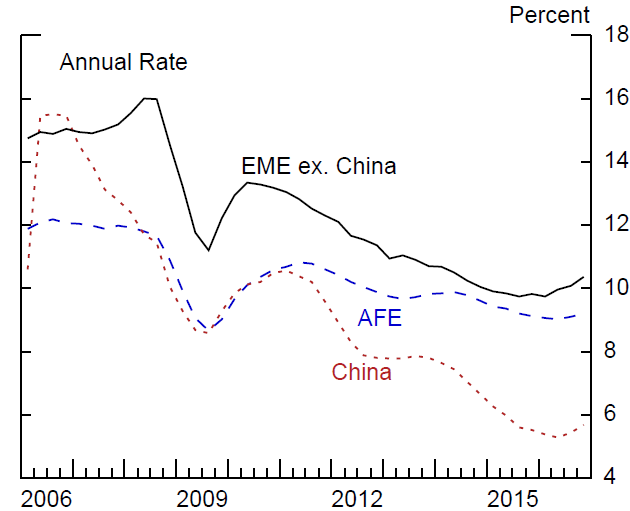

In this note, we assess corporate vulnerabilities by looking at two common metrics related to debt-servicing capacity: leverage (the ratio of debt to equity), and the interest coverage ratio (the ratio of earnings to interest expense). High leverage makes firms vulnerable to increases in borrowing costs and declines in earnings. But even a highly levered firm may be able to easily service its debt if it is highly profitable or if the interest rate on its debt is low. Conversely, a firm with moderate leverage may face difficulties in servicing its debt if it is not generating a profit from its operations, or if it pays a high interest rate on its debt. The interest coverage ratio (ICR) provides a more direct measure of the ability of firms to service their debt payments with earnings.

For EME firms, the reduction in earnings since 2010 has eroded the interest coverage ratio (Figure 5). In contrast, the ICR for the advanced foreign economies (AFEs) has remained fairly stable since 2010.6 An ICR of 2 or less is typically associated with an increased likelihood of distress. For example, just before the Asian financial crisis, firms in Korea, Thailand, and Indonesia had an average ICR of 2 (Pomerleano, 1998). In its April 2014 Global Financial Stability Report, the IMF used an ICR threshold of 2 to classify at risk borrowers, and we use the same threshold in our analysis.7

Source: Staff estimate using Capital IQ.

* 4-quarter moving average of EBITDA/Assets

Source: Staff estimate using Capital IQ and World Bank

* 4- quarter moving average of EBITDA/Interest Expense

** The 1996 average of Korea, Thailand, and Indonesia's ICR during the Asian Financial Crisis was 2.

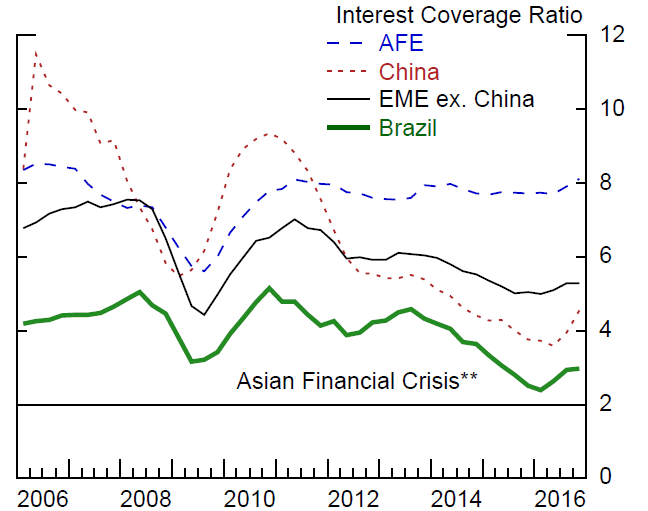

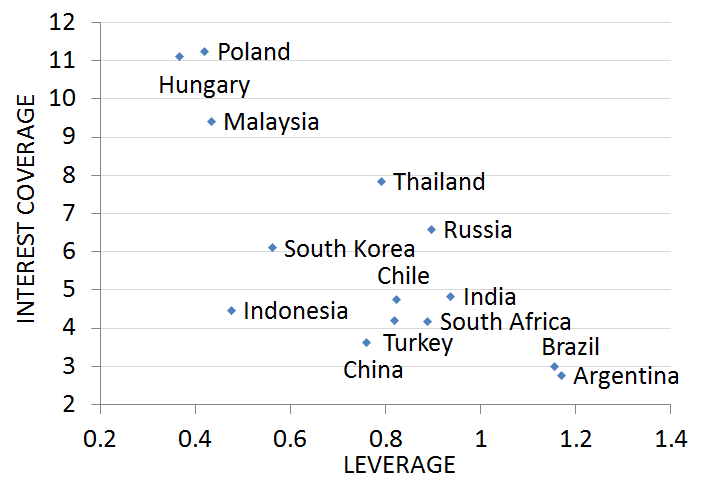

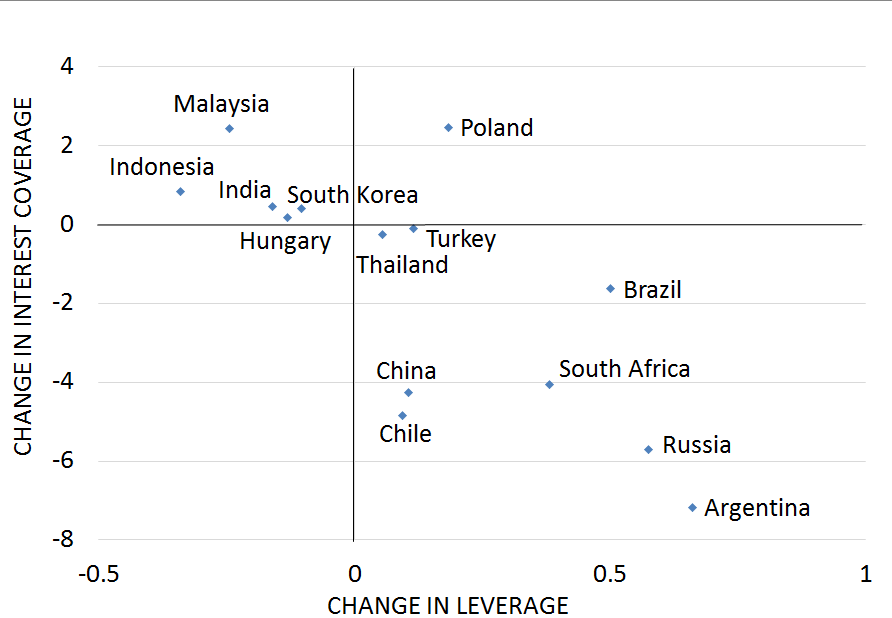

To judge the debt-servicing capacity of the firms in our sample, Figure 6 compares the levels of aggregate leverage, as measured by the ratio of debt to equity, and interest coverage as of 2016:Q3. By these measures, firms in Brazil, Argentina, Chile, China, India, South Africa, and Turkey appear to be the most vulnerable. And this vulnerability has increased over the last 5 years, as shown in Figure 7, which compares the change in leverage and interest coverage since 2011. Some of the countries with the highest leverage--Argentina, Russia, South Africa and Brazil-- are also the ones that experienced the fastest increases in leverage and the steepest declines in interest coverage. Alfaro et al. (2017) also find that corporate liquidity and solvency indicators have deteriorated for most EMEs in the post-GFC period. However, they find that average levels of various vulnerability indicators in the post-GFC period are not as severe as they were for the East Asian economies in the run-up to the East Asian crisis. With regards to China, they do not find that post-GFC leverage in China is higher than the average for the East Asian economies on the eve of the East Asian crisis. We note, however, that China's current corporate debt to GDP ratio-- a broad measure of corporate leverage--is above the average of 100 percent for the East Asian economies before the Asian Financial Crisis.

In sum, the surge in EME corporate debt has been associated with a deterioration in debt servicing capacity. However, it is difficult to assess vulnerabilities based on aggregate measures alone: An aggregate interest-coverage ratio of 8 may mask significant risks if a few large firms have extremely low coverage ratios; conversely, a much lower interest-coverage ratio may still be consistent with solid financial conditions, if the preponderance of firms meet adequate standards. To better understand the systemic risks stemming from the EME corporate sector, in the next section we use firm-level data to quantify the amount of debt which is at risk, and provide a more granular assessment of vulnerabilities across countries and sectors.

Source: Authors' Estimates using Capital IQ.

Source: Authors' Estimates using Capital IQ.

3. Debt at Risk and Leverage in the EME Nonfinancial Corporate Sector

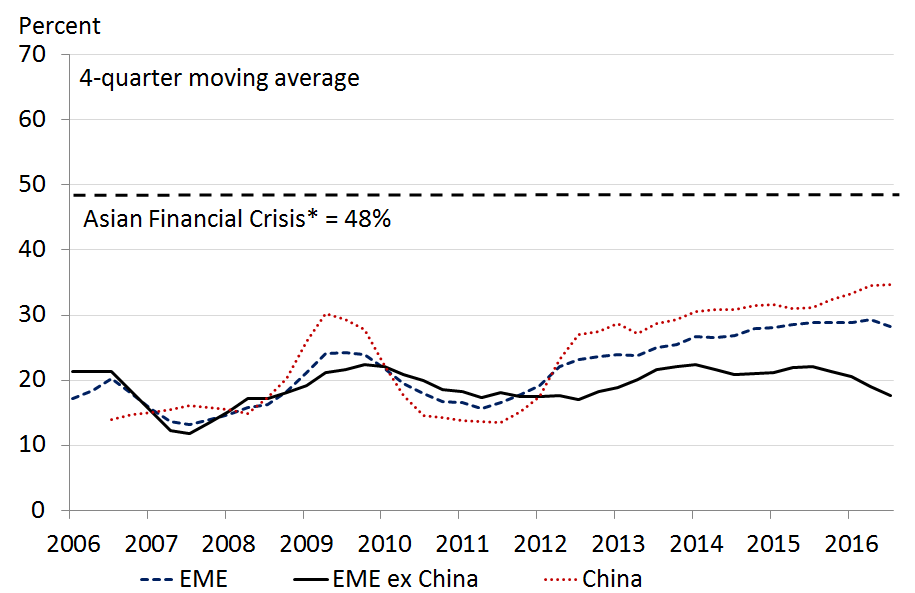

We compute the overall riskiness of the EME corporate debt stock by country and sector using balance sheet and income statement data from Capital IQ for a sample of roughly 8,500 publicly listed firms in 15 emerging market economies. For a given region, country, or sector, we measure the share of risky debt as the debt of firms with ICRs less than 2, divided by the total debt of firms in our sample. The share of risky NFC debt for the countries in our sample has nearly doubled since 2011 to roughly a quarter of total EME NFC debt (Figure 8), surpassing the previous peak. Even so, the share of risky EME corporate debt is considerably lower today than it was for the East Asian countries preceding the Asian financial crisis. Excluding China, the share of risky debt has trended down very recently, as earnings have started to recover from their post-crisis lows, and is now below its pre-GFC level.

Source: Authors' estimates using Capital IQ data through 2016 Q3. EME aggregate comprises the 15 countries listed in Chart 1. Computed as the debt of firms with ICRs less than 2, divided by the total debt of the firms in our sample. Numbers for 2016 Q3 do not match those in Chart 1 because here we show the 4-quarter moving average.

* 1996 GDP-weighted average for Korea, Hong Kong, Singapore, and Thailand Asian financial crisis = 48%

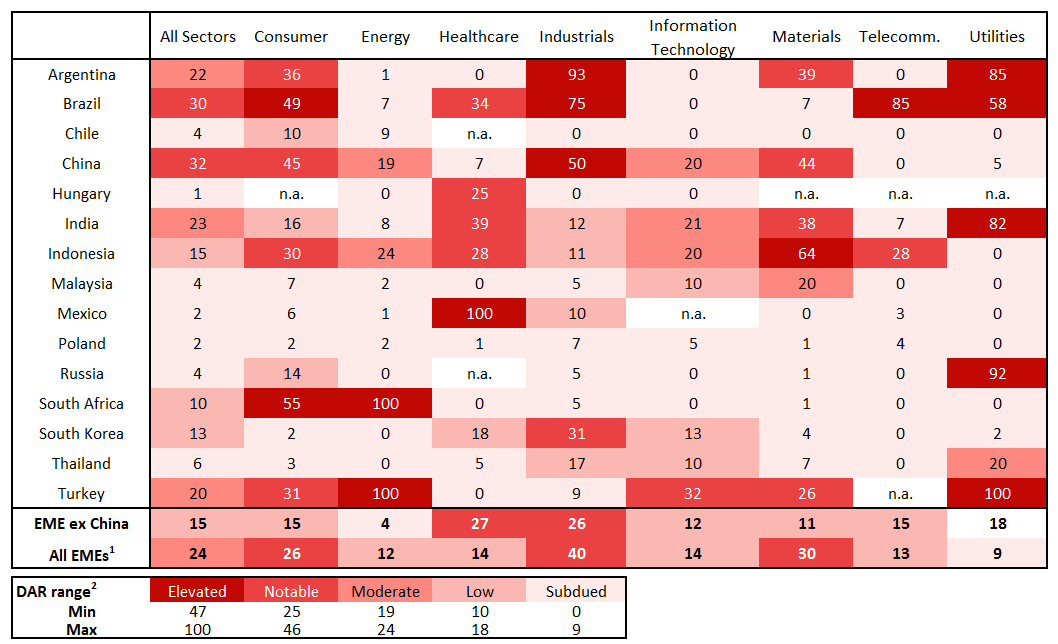

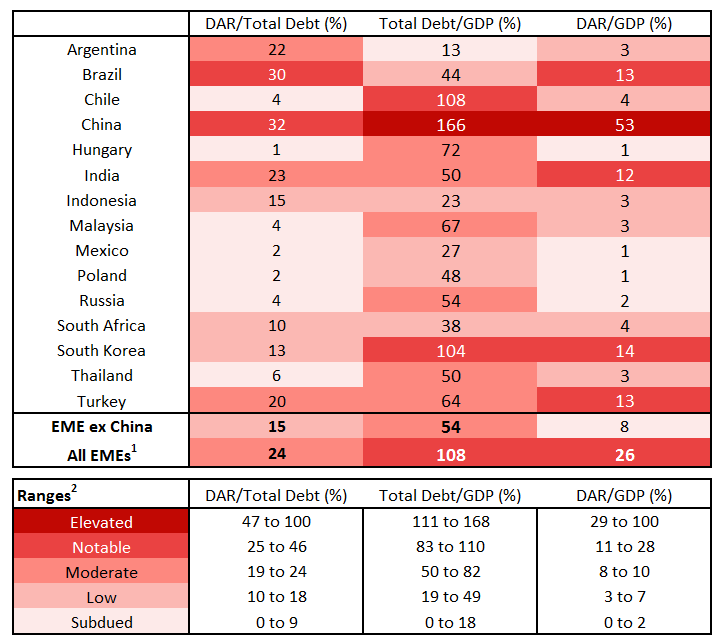

Chart 1 presents a heat map of the share of the nonfinancial corporate debt (both domestic and external) that is considered at risk by sector and country, as of 2016:Q3.8 For the heat maps shown in this table and the tables to follow, the gradations for the colors are based on where the current value lies in the distribution of values over the past 10 years. In particular, the dark red shading for 'elevated' denotes countries or sectors where the current share of debt at risk falls in the 95th percentile or higher of the values seen over the past 10 years. As shown in the first column, the share of risky debt is notable (between the 75th and 94th percentile of the historical distribution) in China and Brazil, where nearly a third of the nonfinancial corporate debt is at risk. In the next tier, India, Argentina, and Turkey have a share of risky debt ranging between a fifth and a quarter of total debt.

Source: Authors' estimates using Capital IQ, as of 2016:Q3.

1. EME aggregate includes the 15 countries listed in the table.

2. DAR=Debt at Risk. The color gradations are based on the distribution of quarterly values for all the countries in our sample since 2006. Specifically, the cutoffs are based on the following percentiles of the historical distribution: Elevated: >=95th percentile, Notable: 75th - 94th percentile, Moderate: 55th - 74th percentile, Low: 15th - 54th percentile, Subdued: 0th - 14th percentile.

Looking across sectors, most countries in our sample have at least one sector with notable or elevated shares of risky debt. For example, risky debt is elevated in the utilities sector for a third of the countries in our sample. For EMEs overall (bottom row), the industrial goods, materials, and consumer goods sectors have the highest share of debt at risk.

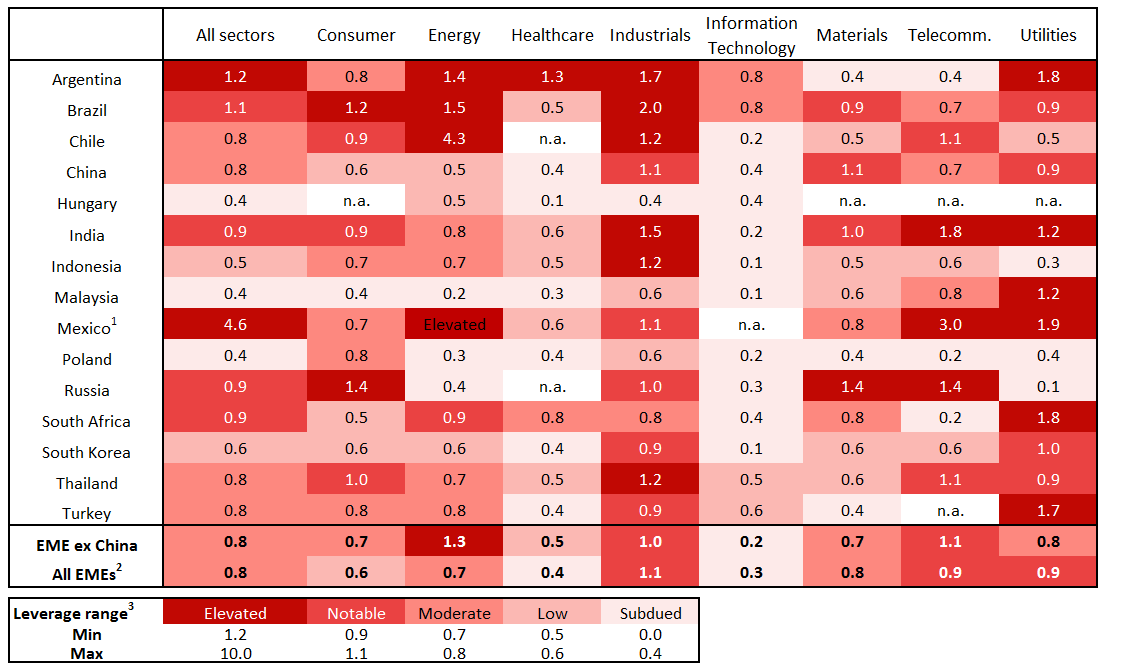

Chart 2 provides a similar heat map, but for the leverage ratio (total domestic and external debt relative to equity) across countries and sectors. As shown in the first column, corporates in Mexico and Argentina have elevated levels of leverage (at or above the 95th percentile of their historical distribution), followed by those in Brazil, India, Russia, and South Africa, where leverage is notably high (between the 75th and 94th percentile).9 Leverage is low or moderate in most other EMEs. Looking across sectors, most of the countries in our sample have at least two sectors with elevated or notable leverage ratios. And, in most countries, the industrial and utilities sectors appear to have high leverage. Thus, overall, corporate leverage seems moderate relative to historical levels.

Source: Authors' estimates using Capital IQ, as of 2016:Q3.

1. Because Pemex has negative equity, we cannot compute leverage for the energy sector in Mexico. See footnote 9 in the main text for details.

2. EME aggregate includes the 15 countries listed in the table.

3. The color gradations are based on the distribution of quarterly values for all the countries in our sample since 2006. Specifically, the cutoffs are based on the following percentiles of the historical distribution: Elevated: >=95th percentile, Notable: 75th - 94th percentile, Moderate: 55th - 74th percentile, Low: 15th - 54th percentile, Subdued: 0th - 14th percentile.

Previous studies examining EME corporate vulnerabilities have focused on the share of debt that is risky. But even if a high share of corporate debt is at risk in a particular country, it may pose limited systemic risk if corporate debt is itself a small share of GDP. Conversely, systemic risk may be greater if corporate debt outstanding is large relative to GDP, even with a smaller share of debt at risk. To provide an estimate of the systemic importance of the risky corporate debt, we scale risky debt for each country by GDP. This can help us gauge the potential costs to the government of bailing out these companies or their lenders if the debt were to turn bad.10

However, because our sample does not include all the firms in a country, we need to scale up our estimate of risky debt to approximate its likely total size. We use BIS data on credit to the nonfinancial private sector (total debt) as a share of GDP as the scale factor. Specifically, we compute the ratio of debt at risk to GDP as follows:

$$$$\frac{\text{Debt at Risk}}{\text{GDP}}=\frac{\text{Share of risky debt x Total debt}}{\text{GDP}}=\frac{\text{Debt at Risk}}{\underbrace{\text{Total Debt}}_{\text{Capital IQ}}}\times\frac{\text{Total Debt}}{\underbrace{\text{GDP}}_{\text{BIS}}}$$$$

Implicit in this scaling is the assumption that the share of risky debt of the firms in our sample is the same as that of the entire corporate sector in each country.11

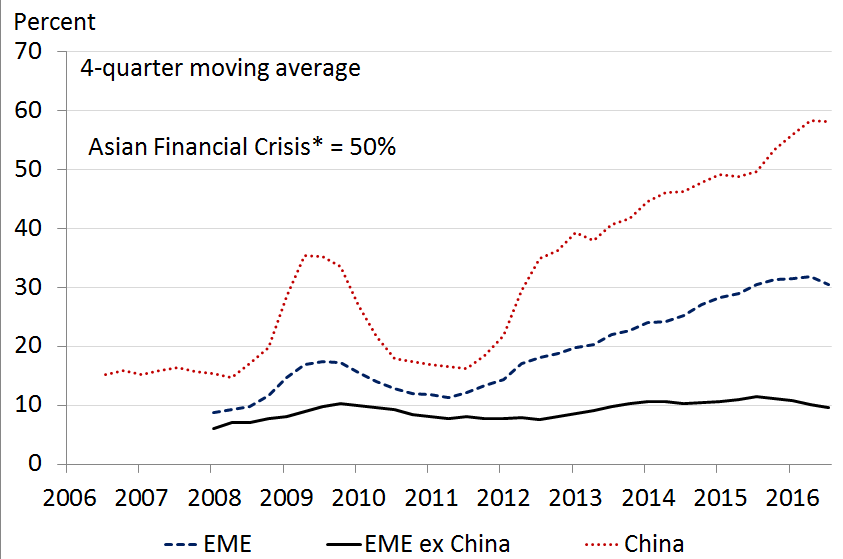

As shown in Figure 9, when scaled by GDP, EME debt at risk has well surpassed its previous pre-GFC peak and is approaching one third of EME GDP. Most of this increase, however, is coming from China, where risky debt as a share of GDP has climbed steeply since 2011, exceeding the share for the East Asian economies before the Asian Financial Crisis. Excluding China, EME NFC debt at risk has been fairly stable at around 10 percent of GDP, which seems manageable.

Chart 3 shows the estimates of the ratio of debt at risk (DAR) to GDP for different countries. The first column shows our estimated share of risky corporate debt from Chart 1. The second column shows the ratio of corporate debt to GDP (from the BIS data). By multiplying these shares, we obtain the DAR/GDP estimates shown in the last column. Among these EMEs, China stands out as having both the largest share of risky corporate debt and the highest corporate debt-to-GDP ratio, which gives rise to its elevated share of risky debt to GDP in the last column. Risky debt ranges from 12-14 percent of GDP in Brazil, South Korea, Turkey, and India, which is still significantly lower than the average of 50 percent for the East Asian economies before the Asian Financial Crisis. For the other EMEs, the share of risky debt to GDP is low. For example, although nearly a quarter of the corporate debt stock in Argentina is at risk, this risky debt makes up only 3 percent of GDP, making it less of a concern.

Source: Authors' estimates using Capital IQ data (through 2016 Q3) and BIS data (through 2016 Q3). EME aggregate comprises the 15 countries listed in Chart 1. Numbers for 2016 Q3 do not match those in Table 4 because here we show the 4-quarter moving average.

* 1996 GDP-weighted average for Korea, Hong Kong, Singapore, and Thailand Asian Financial Crisis = 50%.

Source: Authors' estimates using Capital IQ and BIS, as of 2016 Q3.

1. EME aggregate includes the 15 countries listed in the table.

2. DAR=Debt at risk. The color gradations are based on the distribution of quarterly values for all the countries in our sample since 2006. Specifically, the cutoffs are based on the following percentiles of the historical distribution: Elevated: >=95th percentile, Notable: 75th - 94th percentile, Moderate: 55th - 74th percentile, Low: 15th - 54th percentile, Subdued: 0th - 14th percentile.

4. Stress-testing the EME Corporate Sector

The analysis above has assessed the current state of the corporate sector. Next we examine its vulnerability to a range of plausible shocks. During bouts of financial stress, it is not unusual for EMEs to simultaneously experience higher borrowing costs, currency depreciations, and slower growth (Calvo and Talvi, 2005). Therefore, we now investigate how corporate vulnerabilities in emerging markets would change if EME firms are faced with adverse shocks arising from these sources.

4.1 Calibrating the shocks

Starting with the current amount of debt at risk, we cumulatively stress each firm's financials by: 1) reducing earnings 20 percent; 2) increasing the average interest rate paid by each firm on its debt 1 percentage point; and 3) imposing a 20 percent exchange rate devaluation on the amount of debt that is denominated in foreign currency. These shocks are large but, as discussed below, we regard them as plausible.

The earnings shock corresponds to roughly half of the decline in EME earnings experienced in the aftermath of the GFC. We note that even among the advanced economies, a 20 percent annual decline in earnings is not unusual. Since 2010, earnings have declined by this magnitude at least once in Canada, Italy, Spain, and the United Kingdom. We shy away from making the earnings shocks bigger than this as EME earnings are already depressed relative to their pre-crisis levels; in 2016:Q3 the average return on assets (EBITDA/Assets) of the EME firms in our sample was 7.5 percent per annum, compared to 15 percent in mid-2007.

The interest rate shock is an increase of 100 basis points in the average borrowing cost on both domestic and external debt.12 We estimate that the average borrowing cost of EMEs declined from about 7 percent in 2009 to 4-1/2 percent in 2016, partly reflecting the low interest rate global environment and strong demand for EME bonds. Our interest rate shock undoes less than half of this decline. Given that the average interest rate for the EME firms in our sample is 4-1/2 percent per annum, the 1 percentage point interest rate shock increases the interest expense (and lowers the ICR) by about 20 percent, similar to the earnings shock. Although a 1 percentage point increase does not seem extraordinary--global rates may rise much more than that over the next couple of years--this metric reflects the average interest rate of the entire debt stock, not just the increase on the newly issued debt.

We also consider an exchange rate depreciation shock of 20 percent, which would seem to be well within the range of possibilities. In 2015, for example, the Brazilian real, South African rand, and Malaysian ringgit depreciated against the dollar by more than this. Because firm-level data on the currency composition of assets and liabilities are scarce, we compute the effect of this shock on the level of debt at risk by using aggregate foreign currency shares of debt provided by Ayala et al. (2015). That is, we assume that each firm within a country holds the same share of foreign currency debt, equal to the aggregate share.13 Then, for the share of debt denominated in foreign currencies, we increase interest expense by 20 percent, which arises from the currency depreciation. Because we do not take into account any hedging of foreign currency exposures, whether natural or using derivatives, we are likely overstating the effect of the exchange rate shock on the level of debt at risk.

4.2 Results

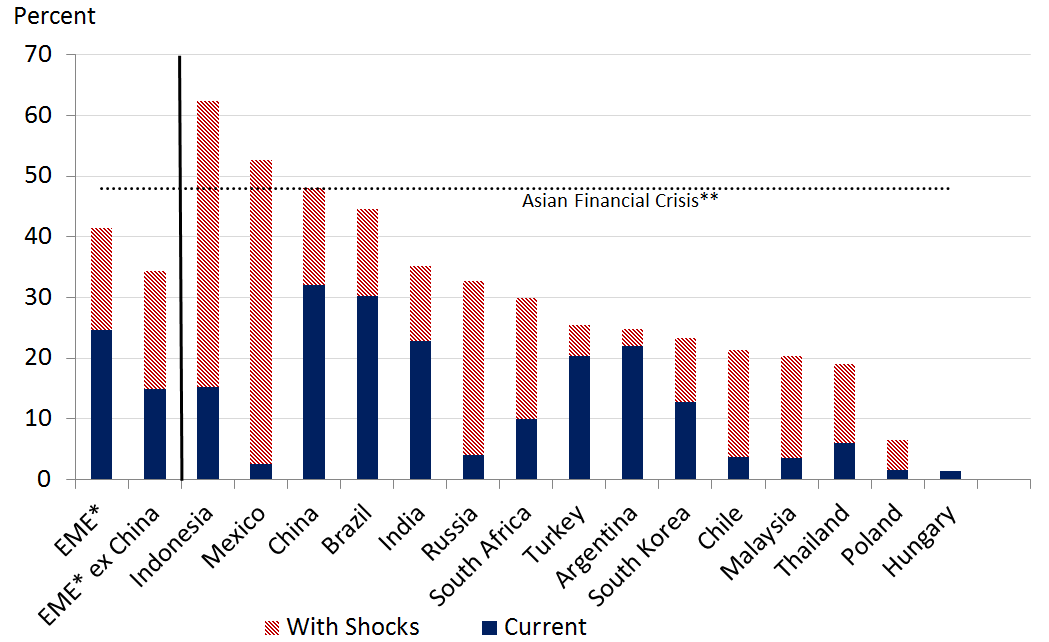

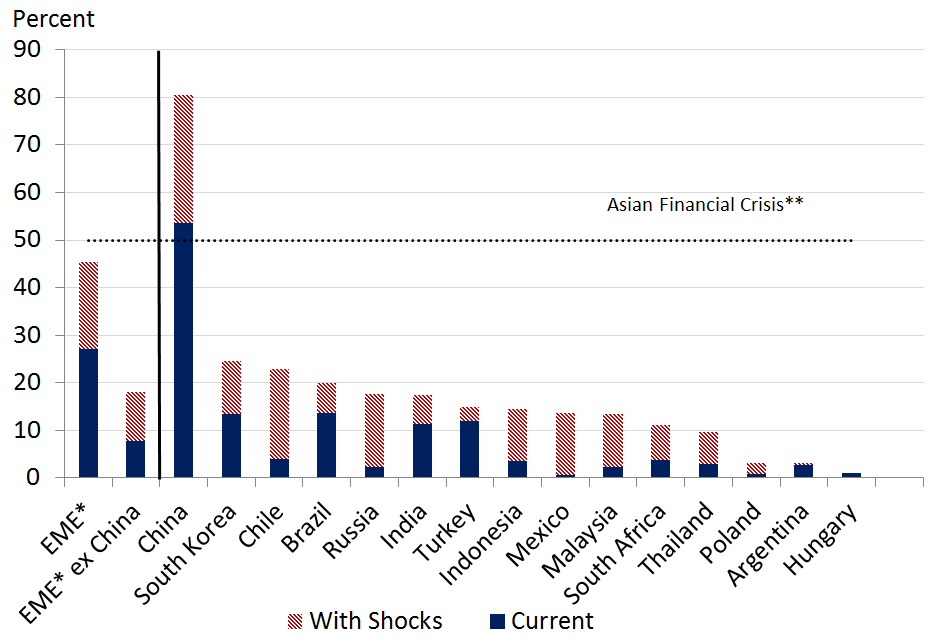

Taken together, the shocks boost the share of risky debt for the EME aggregate from 24 percent to roughly 40 percent (Figure 10). Excluding China, the share of risky debt more than doubles from 15 percent to 35 percent. Thus, the EME corporate sector appears to be vulnerable to negative shocks, consistent with the results in Chow (2015) and IMF (2016). Currently, only two countries (China and Brazil) have a notable share of risky debt (between the 75th and 94th percentile of their historical distribution). After the shocks, the share of risky debt is notable or elevated for 9 of the 15 countries shown. As a share of GDP, the shocks applied simultaneously boost the level of aggregate EME risky debt from roughly 26 percent to 45 percent (Figure 11). The increase comes mainly from China, where risky debt jumps to 80 percent of GDP.

Even outside of China, the share of risky debt appears highly sensitive to the three shocks.14 In particular, after the shocks are applied, the share of risky debt more than doubles in Mexico, Russia, Indonesia, Chile, Malaysia, Poland, Thailand, and South Africa. For some countries, such as Mexico and Indonesia, this heightened sensitivity arises from the fact that a large portion of the corporate debt is concentrated in just a few large firms whose debt moves to the at risk category after the shocks. Although the shocks boost risky debt in Indonesia and Mexico to over half of total debt (Figure 10), this risky debt is still a much smaller share of GDP, around 15 percent (Figure 11). All told, even under our stress scenario, the only emerging market economy whose level of risky debt (as a share of GDP) exceeds that of the East Asian economies on the eve of the Asian financial crisis is China.

Source: Authors' estimates using Capital IQ.

* EME aggregate comprises the 15 EMEs shown individually.

** 1996 GDP-weighted average for Korea, Hong Kong, Singapore, and Thailand, based on a sample of 262 firms is 48% (Asian financial crisis).

4.2.1 Relative importance of shocks

Next, we explore which shocks are most relevant for each country, by applying the shocks individually. The results are summarized in Table 4. For EMEs overall, the earnings shock and interest rate shock each boost the share of risky debt from 25 percent of debt to 31 percent of debt. Excluding China, the earnings shock appears to be somewhat more detrimental than the interest rate shock. In contrast, the exchange rate shock boosts overall risky debt by only 1 percentage point (to 26 percent). Thus, although much attention has been paid to the risks associated with currency mismatch facing emerging market NFCs, in most cases (with the exception of Indonesia and Mexico, which have a fairly large portion of debt denominated in foreign currency) a 20 percent exchange rate depreciation shock against the dollar does not change the share of risky debt much. This result holds partly because a 20 percent devaluation would boost debt service on foreign-currency debt by about the same amount as the other two shocks being considered (20 percent fall in earnings, one percentage point rise in interest rates), but the share of debt denominated in foreign-currency is relatively low for most countries. For other countries (Hungary, Turkey, and Chile, for example), despite a relatively high share of foreign currency debt, a 20 percent currency depreciation still does not change the amount of risky debt much because firms in these countries have sufficiently high ICRs.15

Source: Authors' estimates using Capital IQ.

* EME aggregate comprises the 15 EMEs shown individually.

** 1996 GDP-weighted average for Korea, Hong Kong, Singapore, and Thailand, based on a sample of 262 firms.

Table 1 – Debt at Risk Sensitivity to Shocks

Level of DAR/Total Debt (%)

| Country | Current | After only earnings shock | After only interest rate shock | After only currency deval. shock | After all 3 shocks together | Memo: FX share of debt (%) |

|---|---|---|---|---|---|---|

| All EMEs | 25 | 31 | 31 | 26 | 41 | 16 |

| EMEs ex. China | 15 | 20 | 18 | 15 | 34 | 32 |

| China | 32 | 39 | 40 | 35 | 48 | 9 |

| Brazil | 30 | 37 | 34 | 30 | 45 | 28 |

| India | 23 | 29 | 28 | 23 | 35 | 16 |

| Argentina | 22 | 23 | 22 | 22 | 25 | 37 |

| Turkey | 20 | 21 | 20 | 20 | 26 | 48 |

| Indonesia | 15 | 20 | 20 | 20 | 62 | 56 |

| South Korea | 13 | 18 | 15 | 13 | 23 | 14 |

| South Africa | 10 | 10 | 10 | 10 | 30 | 26 |

| Thailand | 6 | 15 | 17 | 6 | 19 | 18 |

| Russia | 4 | 32 | 4 | 4 | 33 | 44 |

| Chile | 4 | 4 | 4 | 4 | 21 | 47 |

| Malaysia | 4 | 5 | 7 | 4 | 20 | 16 |

| Mexico | 2 | 3 | 3 | 3 | 53 | 63 |

| Poland | 2 | 4 | 3 | 2 | 7 | 49 |

| Hungary | 1 | 1 | 1 | 1 | 1 | 68 |

Source: Authors' estimates using Capital IQ data as of 2016: Q3, and Ayala et al. (2015) for foreign-currency share of debt. DAR = Debt at Risk. The EME aggregate includes the 15 countries shown individually.

References

Acharya, V., S. G. Cecchetti, J. D. Gregorio, S. Kalemli-Ozcan, P. R. Lane, and U. Panizza (2015): "Corporate Debt in Emerging Economies: A Threat to Financial Stability," Discussion paper, Brookings Institution, Committee on International Economic Policy and Reform.

Alfaro, L., G. Asis, A. Chari, and U. Panizza (2017): "Lessons Unlearned? Corporate Debt in Emerging Markets," Mimeo.

Ayala, D., M. Nedeljkovic, and C. Saborowski (2015): "What Slice of the Pie? The Corporate Bond Market Boom in Emerging Economies," IMF Working Paper 148, International Monetary Fund.

Bank for International Settlements (2016): "2016 Annual Report," June 26, 2016.

Bruno, V., and H. S. Shin (2015): "Global dollar credit and carry trades: a firm-level analysis," BIS Working Papers 510, Bank for International Settlements.

Caballero, J., U. Panizza, and A. Powell (2015): "The second wave of global liquidity: Why are firms acting like financial intermediaries?" IHEID Working Papers 21-2015, Economics Section, The Graduate Institute of International Studies.

Calvo, G., and E. Talvi (2005): "Sudden Stop, Financial Factors and Economic Collapse in Latin America: Learning from Argentina and Chile," NBER Working Paper 11153, National Bureau of Economic Research.

Chow, J. (2015): "Stress Testing Corporate Balance Sheets in Emerging Economies," IMF Working Paper 216, International Monetary Fund.

Claessens, S., S. Djankov, and G. Ferri (1999): "Corporate Distress in East Asia," Public Policy for the Private Sector Discussion Paper 172, The World Bank Group.

International Monetary Fund (2014): "Moving From Liquidity- to Growth-Driven Markets," Chapter 1, April 2014.

International Monetary Fund (2016): "Global Financial Stability Report: Financial Stability Challenges in a Low-Growth Era," October 2016.

Maliszewski, W., Arslanalp, S., Caparusso, J., Garrido, J., Guo, S., Kang, J.S., Lam, W. R., Law, T. D., Liao, W., Rendak, N., Wingender, P., Yu, J., Zhang, L. "Resolving China's Corporate Debt Problem," IMF Working Paper 203, International Monetary Fund.

McCauley, R., P. McGuire, and V. Sushko (2015): "Global dollar credit: links to US monetary policy and leverage," BIS Working Papers 483, Bank for International Settlements.

Pomerleano, M. (1998): "Corporate Finance Lessons from the East Asian Crisis," Discussion Paper 155, The World Bank Group.

Shin, H. S. (2013): "The Second Phase of Global Liquidity and Its Impact on Emerging Economies," Keynote address at the Federal Reserve Bank of San Francisco Asia Economic Policy Conference on November 7, 2013.

1. The views in this paper are solely the responsibility of the authors and should not be interpreted as reflecting the views of the Board of Governors of the Federal Reserve System or any other person associated with the Federal Reserve System. We thank Shaghil Ahmed, Stijn Claessens, Steven Kamin, and Beth Anne Wilson for helpful comments. We also thank Chris Collins for excellent research assistance. All errors are our own. Return to text

2. Bruno and Shin (2015) show that EME corporates tend to borrow in dollars to maintain higher levels of cash and liquid assets during periods when domestic interest rates exceed U.S. rates and thus the dollar carry trade is favorable, and Caballero et al. (2015) show that this especially true for countries that have tighter capital controls. Return to text

3. For example, even though China has greater vulnerabilities with respect to corporate debt, it is also generally believed that they have relatively more resources to address problems that may arise. Return to text

4. The 15 countries are those for which we have data on total corporate debt outstanding (Bank for International Settlements), foreign-currency shares of debt (Ayala et al., 2015), and firm-level balance sheets and income statements (Capital IQ), namely: Argentina, Brazil, Chile, China (includes Hong Kong), Hungary, India, Indonesia, Malaysia, Mexico, Poland, Russia, South Africa, South Korea, Thailand, and Turkey. We combine China and Hong Kong, as many firms domiciled in Hong Kong conduct significant business in China, and vice-versa. Return to text

5. Throughout, earnings refers to earnings before interest, taxes, depreciation, and amortization, or EBITDA. Return to text

6. The United States is not included in the AFEs. Return to text

7. To compute ICRs, we use the 4-quarter average of both earnings and interest expense. Return to text

8. For most countries in Chart 1, our estimates of the share of risky corporate debt (using an ICR cutoff of 2) are very close to those in the IMF (2016), with the exception of China, Turkey, and Mexico (where we estimate a higher share of risky debt). Return to text

9. The elevated aggregate leverage ratio for Mexico owes mostly to the large, negative equity reported by the state-controlled oil company Petroleos Mexicanos (Pemex). Leverage of the Mexican energy sector is elevated if we use an alternative definition of leverage, Debt/(Debt+Equity). Return to text

10. Chow (2015) and IMF (2016) assess the adequacy of EME banks' capital and loan loss reserves in absorbing an increase in corporate nonperforming loans (NPLs). As they point out, however, bank buffers are often overstated, and the level of nonperforming loans are often understated. Return to text

11. This assumption may be adequate for Latin America and the Asian EMEs excluding China, where our sample comprises roughly two-thirds of their total NFC debt. For China, however, the debt of the firms in our sample is just a quarter of total Chinese NFC debt. Even so, we believe our estimates may understate the true share of risky corporate debt in China because the larger state-owned enterprises (SOEs), which are over-represented in our sample, have fairly healthy ICRs. The healthy ICRs for Chinese SOEs partly reflects their easy access to cheap credit from state-owned banks (Maliszewski et al. 2016). Return to text

12. To apply this shock, we first calculate the average interest rate each firm pays on its debt by dividing its annualized interest expense by its debt stock. We then shock this interest rate by 100 basis points and use the new rate to determine the firm's interest expense. Return to text

13. We do not consider the possibility that, in some countries, debt may be concentrated in large firms with elevated shares of foreign-currency debt, which would heighten the sensitivity of DAR to the exchange rate depreciation shock. Return to text

14. Chow (2015) also finds that debt in Indonesia, Mexico, and China is quite sensitive to earnings, interest rate, and exchange rate shocks. For India, however, the (higher) estimate of debt at risk changes little in response to the shocks. Return to text

15. Using more recent data on Turkey's foreign-currency share of corporate debt, which is closer to two-thirds, we arrive at almost identical estimates of risky debt for Turkey. Return to text

Beltran, Daniel, Keshav Garud, and Aaron Rosenblum (2017). "Emerging Market Nonfinancial Corporate Debt: How Concerned Should We Be?," IFDP Notes. Washington: Board of Governors of the Federal Reserve System, June 2017, https://doi.org/10.17016/2573-2129.32.

Disclaimer: IFDP Notes are articles in which Board economists offer their own views and present analysis on a range of topics in economics and finance. These articles are shorter and less technically oriented than IFDP Working Papers.