May 17, 2021

Sovereign Markets, Global Factors

Vice Chair Richard H. Clarida

At "Fostering a Resilient Economy and Financial System: The Role of Central Banks" 25th Annual Financial Markets Conference, sponsored by the Center for Financial Innovation and Stability, Federal Reserve Bank of Atlanta, Amelia Island, FL (via webcast)

Good morning, and thank you, Raphael. I am delighted to participate in the 25th Financial Markets Conference, sponsored by the Federal Reserve Bank of Atlanta, which this year focuses on the role of central banks in fostering a resilient economy and financial system.1

Central banks can indeed make important contributions to the resilience of the economy and the financial system. In the case of the Federal Reserve, our responsibilities include ensuring that banks are well supervised and regulated, working with other government agencies through the Financial Stability Oversight Council to promote financial stability, and, of course, conducting a U.S. monetary policy that aims to achieve our dual-mandate goals of maximum employment and price stability. As the title of my talk suggests, my remarks today will focus on the importance of some specific global financial linkages that are relevant to the execution and communication of U.S. monetary policy aimed at achieving our domestic mandates.

Signs of financial globalization are abundant and evident across markets for many asset classes. But why and in what possible ways is financial globalization relevant for national monetary policies charged with achieving domestic mandates? A comprehensive and complete answer to this fundamental question is, of course, beyond the scope of a single speech, and so in my remarks today, I will focus specifically on two ways in which the integration and globalization of sovereign bond markets is relevant to the execution and communication of national monetary policies.

Central banks rightly pay a lot of attention to domestic sovereign bond yields "across the curve" for at least two reasons. First, yield curves for nominal and inflation-indexed bonds provide useful—if also noisy—information about the expected future path of the policy rate, inflation, the business cycle, and the term premium required to hold sovereign bonds. Second, yields on long-maturity bonds represent, generally, a key channel in the transmission of monetary policy to the real economy and, specifically, are a fundamental building block markets use to discount cash flows relevant for valuing financial assets. To anticipate my bottom line, the message of this speech is that global integration of sovereign bond markets has important implications not only for how central banks extract relevant signals from observed yields on bonds issued by the domestic sovereign, but also for how central banks calibrate the transmission of policy and policy guidance to the real economy via the yields on long-maturity bonds that are relevant for saving, investment, and asset valuation.

Sovereign Yields Embed Global Factors

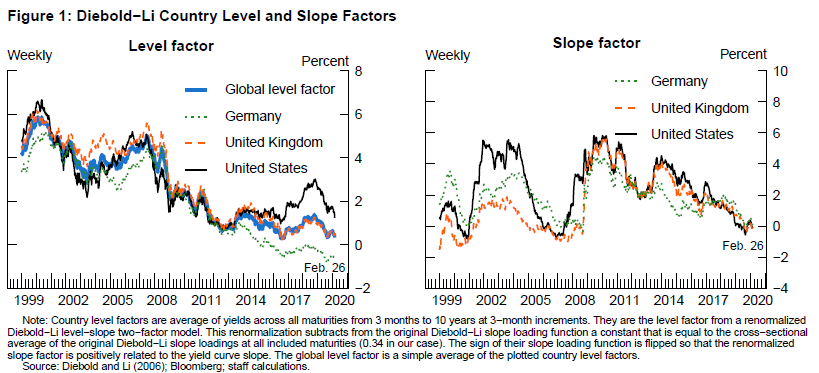

There is a rich academic and practitioner literature devoted to modeling and interpreting fluctuations in domestic sovereign yield curves. A fundamental empirical regularity that motivates much of this research is that, across time and geography, yields along any given sovereign curve tend to rise and fall—and steepen and flatten—together over time. This empirical regularity led Litterman and Scheinkman (1991) to hypothesize and demonstrate that in the market for U.S. Treasury securities, a very small number of common factors—two or, at most, three—are able to account not only for most of the time-series variation, but also for the cross-sectional dispersion in yields across the entire Treasury curve. Moreover, the two most empirically important factors extracted statistically from the Treasury yield curve have intuitive geometric interpretations as "level" and "slope." The "level" factor has approximately an equal effect on yields across the maturity spectrum—thus, changes in the level factor are often referred to as "parallel shifts" in the yield curve—and accounts for most of the variance in yields across the full range of maturities. The "slope" factor has an effect that is increasing (monotonically) in maturity—thus, changes in the slope factor are often referred to as "steepening" or "flattening" pivots in the yield curve.

The original Litterman and Scheinkman factor model, with its geometric interpretation of level and slope factors, has held up remarkably well over the ensuing three decades and has been replicated for sovereign yield curves across scores of countries around the world, revealing similar regularities. Indeed, many, if not most, major central banks—and certainly their central bank watchers—estimate yield curve models and extract the factors that are reflected in their domestic sovereign yield curves. So, for example, for the three major economies included in figure 1, one can easily extract—using the methodology developed in Diebold and Li (2006)—on a country-by-country basis, U.S., U.K., and German level factors as well as U.S., U.K., and German slope factors. As is clear from figure 1, level and slope factors extracted from these individual sovereign yield curves are highly correlated across these major sovereign bond markets.

{kind=link}

Economic theory suggests at least two reasons why the factors embedded in sovereign yield curves may be correlated across countries. First, this correlation will be present if the underlying macro fundamentals—for example, productivity growth, saving–investment imbalances, and longer-term inflation expectations—that drive the factors are correlated across countries.2 Second, as is emphasized in Clarida (2019c) and Obstfeld (2020), this correlation will also be present if countries are tightly financially integrated even if fundamentals themselves are independent across countries.3

Interpreting the Global Level Factor

From any set of level and slope factors extracted across a collection of sovereign yield curves, one can in turn extract a global level factor and a global slope factor that account for the correlation among the country-specific level and slope factors.4 As can be seen in figure 1, the global level factor (the blue line) accounts for most of the evident downward trend and much of the variation relative to that trend in the estimated U.S., U.K., and German level factors. But what is this global level factor? Plausibly, the global level factor embedded in these three sovereign yield curves reflects the contribution of possibly several global macro fundamental drivers—including global productivity growth, the balance between global saving and investment, and longer-term inflation expectations—and likely also other "market" or "technical" factors specific to the trading of these sovereigns in the global bond market.

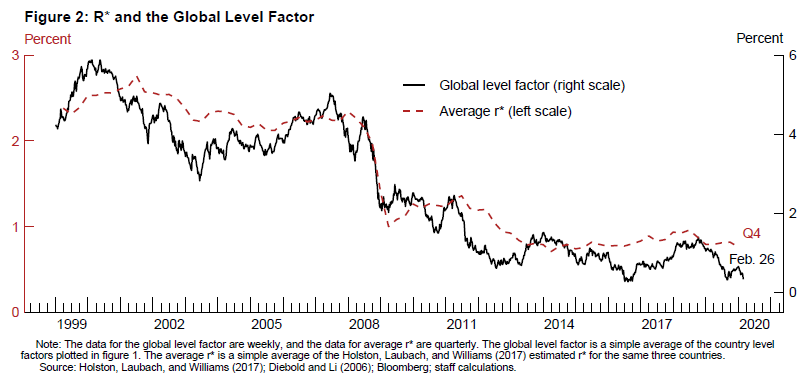

As can be seen in figure 2, however, most of the trend and variation in the global level factor about this trend can be accounted for by the evolution of estimates of the neutral real interest rates in these countries.5 Figure 2 plots the global level factor against a simple average of the Holston, Laubach, and Williams (2017, henceforth HLW) time-series estimates of $$r\ast\ $$—the neutral real interest rate consistent with trend growth and stable inflation—for the United States, the United Kingdom, and Germany. Now, while it is certainly intuitive that an $$r\ast\ $$ index for these countries would be correlated with the global level factor extracted from their yield curves, the degree to which this simple index can account for the trend and variation in the global level factor around this trend is striking. And because central banks, including the Federal Reserve, typically channel Milton Friedman (1968) and believe that the evolution of $$r\ast\ $$ primarily reflects nonmonetary factors that are beyond the central bank's control, an "$$r\ast\ $$ theory" of the level factor—if true—has important implications for how central banks extract signal from noise from sovereign yield curves as well as for how they calibrate the stance of monetary policy consistent with a credible inflation target. Under this interpretation, and as was anticipated years ago by Greenspan (2005), Bernanke (2005), Clarida (2005), and others, credible inflation-targeting central banks operating in an integrated global capital market—at least when they are operating away from their effective lower bound (ELB)—are primarily in the yield curve "slope" business, but much less so in the yield curve "level" business.6

{kind=link}

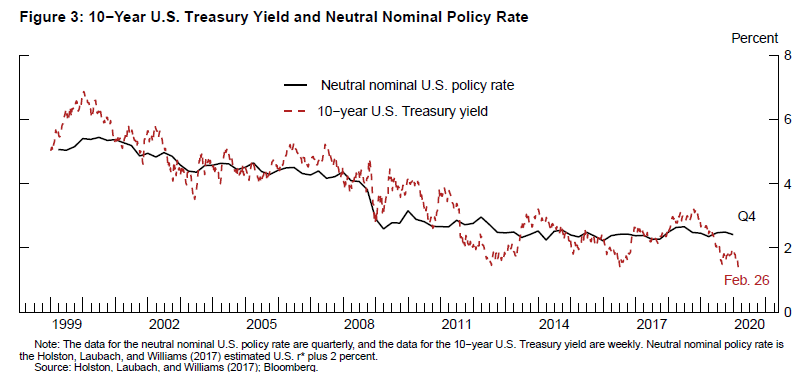

Figure 3 shows the relationship between the yield on a 10-year Treasury note and an estimate of the neutral nominal U.S. policy rate, which I set equal to the HLW estimate of $$r\ast\ $$ for the United States plus a 2 percent inflation objective, a proxy for the neutral nominal interest rate when longer-term inflation expectations are anchored at the 2 percent target. As is evident from the figure and as can be verified econometrically, there has been since at least the 1990s a stable, mean-reverting dynamic relationship between the benchmark nominal Treasury yield and a neutral nominal interest rate proxy derived from the HLW time-series estimates for $$r\ast\ $$ in the United States.

{kind=link}

Interpreting the Slope Factor

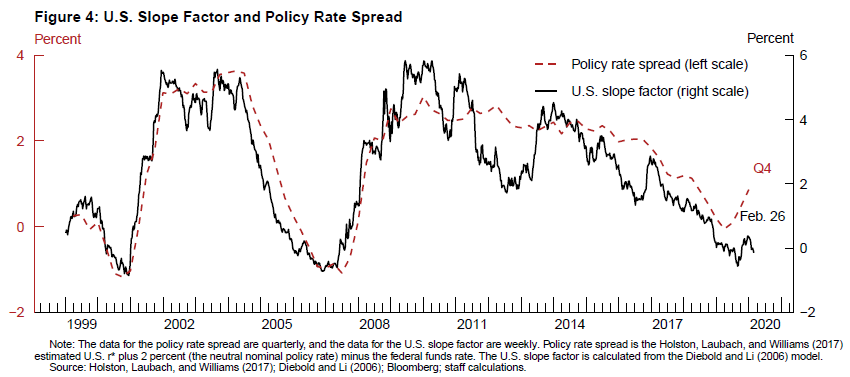

I would now like to illustrate what I mean when I say that the slope of the yield curve is an important channel through which monetary policy is transmitted. Figure 4 plots the Diebold-Li (DL) slope factor for the United States—which is included in figure 1—against the spread between the HLW estimate of the U.S. neutral nominal policy rate and the actual federal funds rate (hereafter the "policy rate spread"). As is evident from figure 4, most of the variation in the DL slope factor for the Treasury yield curve can be accounted for by changes in the U.S. policy rate spread.7 A simple regression over the 1999:Q1 to 2019:Q4 sample of the slope factor on the policy rate spread shown in figure 4 yields an R2 of 0.84 with a coefficient on the policy rate spread of 1.23. In other words, over the past 20 years, more than three-fourths of the variance of the Treasury slope factor can be accounted for by the policy rate spread, which is obviously something the Federal Reserve can control when it sets the federal funds rate. The remaining variance of the benchmark Treasury slope factor is, by construction, accounted for by factors that are uncorrelated with the U.S. policy rate spread. A similar empirical relationship between the policy rate spread and the slope factor embedded in gilt and bund yield curves is also evident in the data, although there is some evidence in these markets of a structural break in these relationships between the slope factor and the policy rate spread sometime after the Global Financial Crisis.8 In the interest of time, I shall not put forward a theory of what accounts for the residual variance of yield curve slope factors after accounting for the policy rate spread itself, but obvious candidates (certainly at the ELB) would include forward guidance about the path of the future policy rate as well as actual and prospective large-scale asset purchase (LSAP) programs.

{kind=link}

Identifying Causation from Bond Yield Correlations

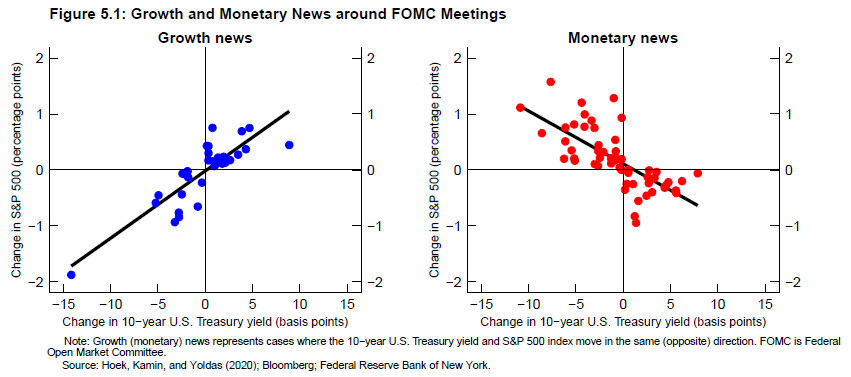

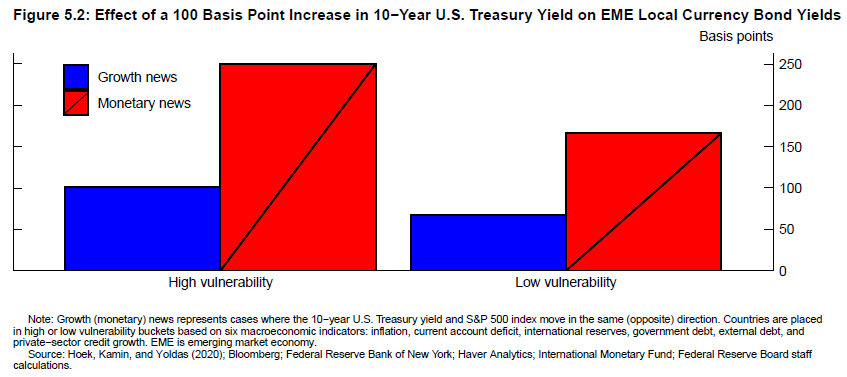

It is a truism that "correlation is not causation," and this is especially the case when trying to interpret contemporaneous correlation among asset prices generally and among bond yields in particular. Having identified one possible, parsimonious set of economic fundamentals that can help account for yield curve fluctuations in three major sovereign markets, I will now review what the empirical evidence has to say about the direction of causality reflected in observed correlations among sovereign yields.9 I will explore two possibilities. The first possibility is that, in reality, there are no latent "global" factors whatsoever, but rather there are just U.S. factors that exogenously fluctuate and cause the global correlations in bond yields we observe in the data. There is a vast literature (Claessens, Stracca, and Warnock, 2016, provide an overview) that documents the existence of spillovers from U.S. monetary policy, especially to emerging market (EM) financial conditions, although the recent paper by Hoek, Kamin, and Yoldas (2020) suggests that the degree of those spillovers depends importantly on the source of the shock that triggers changes in Federal Open Market Committee (FOMC) policy. In particular, as summarized in figure 5.1, they identified FOMC actions associated with "growth news" as those that were immediately followed by changes in the 10-year Treasury yield and the S&P 500 index in the same direction, whereas actions associated with "monetary news" elicited changes in yields and equity prices in opposite directions. Their key finding, illustrated in figure 5.2, was that FOMC policy rate surprises attributed to stronger U.S. growth generally have only moderate spillovers to EM financial conditions, whereas FOMC policy rate surprises attributed to U.S. inflationary pressures trigger more substantial spillovers to EM financial conditions. Regardless of the type of FOMC policy action, Hoek, Kamin, and Yoldas (2020) also found compelling evidence that the size of the spillover effects from the United States depends importantly on the degree of macroeconomic vulnerability of each emerging market economy (EME), with more vulnerable EMEs experiencing larger spillovers.

{kind=link}

{kind=link}

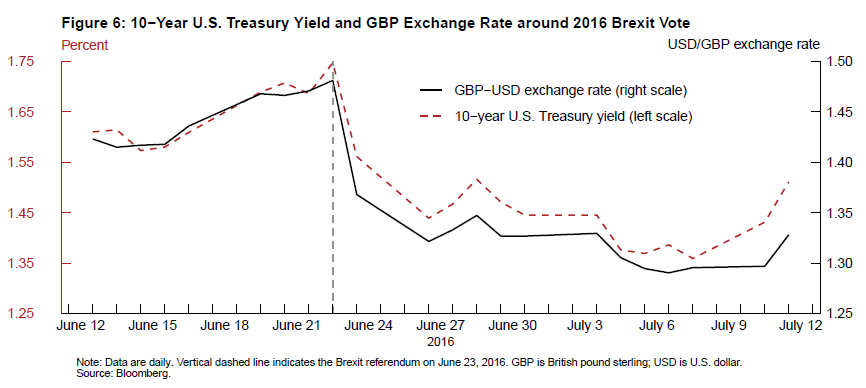

While I certainly believe that both fundamental and financial shocks originating in the United States propagate throughout the global financial system and likely account for a significant share of the asset price correlations across global markets that we observe in the data, the evidence—and introspection—suggests to me that causality can and often does run both ways.10 Anecdotally, it is not difficult to recall events—plausibly exogenous to the United States—that have triggered spillovers from foreign sovereign markets to the U.S. Treasury market. A prominent example would be the surprise Brexit vote of June 23, 2016. As the news of the Brexit vote filtered through global markets that day, sovereign yields plunged in both Germany and the United States. Indeed, as is shown in figure 6, on that day, the 10-year Treasury yield fell almost 20 basis points, the single largest one-day decline in the eight years—and over 2,000 trading days—between January 2012 and March 2020.11

{kind=link}

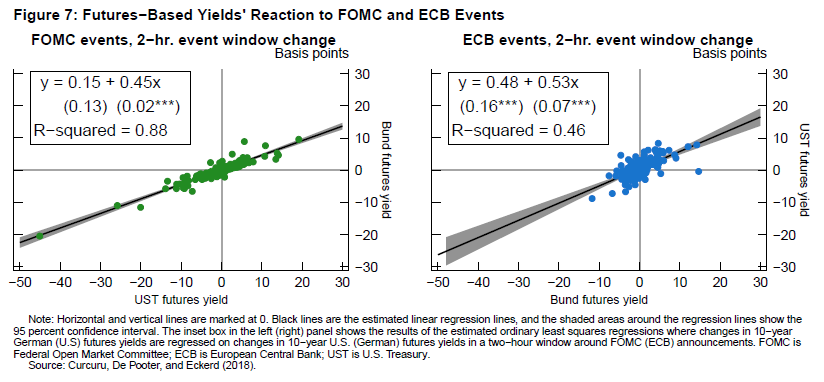

The evidence that two-way causality is reflected in sovereign bond yield correlations is not limited to one-off geopolitical events such as Brexit. For instance, Curcuru, De Pooter, and Eckerd (2018) examined 12 years of monetary policy announcements by the FOMC and the European Central Bank (ECB)—a combined total of 266 monetary policy communications—focusing on how sovereign yields in one jurisdiction responded to monetary policy announcements made in the other. Their main findings are summarized in the two panels in figure 7. The left panel presents some of the evidence of the well-known, statistically significant spillovers from FOMC policy announcements to euro-area bond markets. But, as is shown in the right panel, the authors found that the spillover effect from ECB policy announcements to U.S. yields is roughly as large as that from the FOMC announcements to bund yields.12

{kind=link}

In another influential study using a very different identification methodology, Ehrmann, Fratzscher, and Rigobon (2011) estimated significant and approximately equal spillovers from U.S. bond market shocks to EU bond markets, and from EU bond market shocks to the U.S. Treasury market.13 They attributed their findings to significant incipient and anticipated portfolio allocation flows across the two jurisdictions that respond elastically to expected rate-of-return differentials.14

Concluding Remarks

To sum up, I believe that in extracting signal from noise from the Treasury yield curve, it is essential to incorporate the fact that observed yields in the United States and other major sovereign markets are determined in a global general equilibrium that is reflected, at least in part, in the global level of neutral policy rates and the state of longer-term global inflation expectations.15 Conditional on neutral policy rates and longer-term inflation expectations, the Federal Reserve and other major central banks can be thought of as calibrating and conducting the transmission of policy—be it through rates, forward guidance, or LSAPs—primarily through the slopes of their yield curves and much less so via their levels.16 Thank you very much for your time and attention. I look forward to my conversation with Raphael.

References

Bauer, Michael D., and Glenn D. Rudebusch (2020). "Interest Rates under Falling Stars," American Economic Review, vol. 110 (May), pp. 1316–54.

Bernanke, Ben S. (2005). "The Global Saving Glut and the U.S. Current Account Deficit," speech delivered at the Sandridge Lecture, Virginia Association of Economists, Richmond, Va., March 10.

Bomfim, Antulio N. (1997). "The Equilibrium Fed Funds Rate and the Indicator Properties of Term-Structure Spreads," Economic Inquiry, vol. 35 (October), pp. 830–46.

Clarida, Richard H. (2005). "Our Post-Bubble World," Wall Street Journal, April 11.

——— (2019a). "Global Shocks and the U.S. Economy," speech delivered at "The Euro Area: Staying the Course through Uncertainties," BDF Symposium and 34th SUERF Colloquium, sponsored by Banque de France and the European Money and Finance Forum, Paris, March 28.

——— (2019b). "Monetary Policy, Price Stability, and Equilibrium Bond Yields: Success and Consequences," speech delivered at the High-Level Conference on Global Risk, Uncertainty, and Volatility, cosponsored by the Bank for International Settlements, the Board of Governors of the Federal Reserve System, and the Swiss National Bank, Zurich, November 12.

——— (2019c). "The Global Factor in Neutral Policy Rates: Some Implications for Exchange Rates, Monetary Policy, and Policy Coordination," International Finance, vol. 22 (Spring), pp. 2–19.

Clarida, Richard H., Jordi Galí, and Mark Gertler (2000). "Monetary Policy Rules and Macroeconomic Stability: Evidence and Some Theory," Quarterly Journal of Economics, vol. 115 (February), pp 147–80.

Claessens, Stijn, Livio Stracca, and Francis E. Warnock (2016). "International Dimensions of Conventional and Unconventional Monetary Policy," Journal of International Money and Finance, vol. 67 (October), pp 1–7.

Curcuru, Stephanie E., Michiel De Pooter, and George Eckerd (2018). "Measuring Monetary Policy Spillovers between U.S. and German Bond Yields," International Finance Discussion Papers 1226. Washington: Board of Governors of the Federal Reserve System, April.

Diebold, Francis X., and Canlin Li (2006). "Forecasting the Term Structure of Government Bond Yields," Journal of Econometrics, vol. 130 (February), pp. 337–64.

Diebold, Francis X., Canlin Li, and Vivian Z. Yue (2008). "Global Yield Curve Dynamics and Interactions: A Dynamic Nelson-Siegel Approach," Journal of Econometrics, vol. 146 (October), pp. 351–63.

Ehrmann, Michael, Marcel Fratzscher, and Roberto Rigobon (2011). "Stocks, Bonds, Money Markets and Exchange Rates: Measuring International Financial Transmission," Journal of Applied Econometrics, vol. 26 (September-October), pp. 948–74.

Ferreira, Thiago, and Samer Shousha (2021). "Supply of Sovereign Safe Assets and Global Interest Rates," International Finance Discussion Papers 1315. Washington: Board of Governors of the Federal Reserve System, April.

Friedman, Milton (1968). "The Role of Monetary Policy," American Economic Review, vol. 58 (March) pp. 1–17.

Gospodinov, Nikolay (2020). "Global Factors in U.S. Yield Curve," working paper, July, available at https://sites.google.com/site/gospodinovfed.

Greenspan, Alan (2005). "Testimony of Chairman Alan Greenspan," statement before the Committee on Banking, Housing, and Urban Affairs, U.S. Senate, February 16.

Hoek, Jasper, Steve Kamin, and Emre Yoldas (2020). "When Is Bad News Good News? U.S. Monetary Policy, Macroeconomic News, and Financial Conditions in Emerging Markets," International Finance Discussion Papers 1269. Washington: Board of Governors of the Federal Reserve System, January.

Holston, Kathryn, Thomas Laubach, and John C. Williams (2017). "Measuring the Natural Rate of Interest: International Trends and Determinants," Journal of International Economics, vol. 108 (May, S1), pp. S59–75.

Laubach, Thomas, and John C. Williams (2003). "Measuring the Natural Rate of Interest," Review of Economics and Statistics, vol. 85 (November), pp. 1063–1070.

Litterman, Robert B., and Josè Scheinkman (1991). "Common Factors Affecting Bond Returns," Journal of Fixed Income, vol. 1 (Summer), pp. 54–61.

Obstfeld, Maurice (2020). "Global Dimensions of U.S. Monetary Policy," International Journal of Central Banking, vol. 16 (February), pp. 73–132.

Panetta, Fabio (2021). "Monetary Autonomy in a Globalised World," welcome address delivered at the joint BIS, BOE, ECB, and IMF conference "Spillovers in a 'Post-Pandemic, Low-for-Long' World," Frankfurt, April 26.

Rigobon, Roberto (2003). "Identification through Heteroskedasticity," Review of Economics and Statistics, vol. 85 (November), pp. 777–92.

Appendix

We derive in this appendix a simple model that can be used to interpret the empirical relationship between Treasury yields, the neutral real interest rate, and the policy rate spread. Begin with the identity that the policy rate spread equals the difference between the neutral interest rate $$(r_t^\ast+\pi^\ast)$$ and the current policy rate:

$$s_t=r_t^\ast+\pi^\ast-R_{t,1}.$$

Now define the n-period term premium $$ \tau_{t,n} $$ through the long-term rate definition:

$$R_{t,n}=E_t\left(\frac{1}{n}\right)\ \sum_{i=0}^{n-1}{R_{t+i,1}+\ \tau_{t,n}}.$$

Consider a simple data-generating process consistent with Laubach and Williams (2003) for the neutral real interest rate

$$r_t^\ast=\ r_{t-1}^\ast+w_t$$

and a simple first-order autoregression for the policy rate spread

$$s_t=\ \rho\ s_{t-1}+e_{t,}$$

where $$ w_t $$ and $$ e_t $$ are assumed to be some unforecastable disturbances.

Then at any horizon $$ n $$ we have

$$R_{t,n}=\ r_t^\ast+\ \pi^\ast-\frac{1}{n}\left.\frac{\left(1-\rho^n\right)}{\left(1-\rho\right)}\right.s_t+\ \tau_{t,\ n}.$$

Regress $$ \tau_{t,n} $$ on the policy rate spread

$$\tau_{t,n}=\ \tau_{0,n}+\beta_ns_t+v_{t,n,}$$

where $$ \tau_{0,n} $$ and $$ \beta_n $$ are regression parameters and $$ v_{t,n} $$ is the residual, and we have (cf. figure 3)

$$R_{t,n}=\ r_t^\ast+\ \pi^\ast+\ \tau_{0,n}+\left[\beta_n-\left.\frac{1}{n}\frac{\left(1-\rho^n\right)}{\left(1-\rho\right)}\right.\right]s_t+v_{t,n}\ .\ $$

So yields at each maturity are anchored by the common neutral nominal rate $$ r_t^{\ast} + \pi^{\ast} $$ (Bauer and Rudebusch, 2020). The difference between the long rates $$ R_{t,n} $$ and the neutral interest rate $$ (r_t^{\ast} + \pi^{\ast}) $$ is a linear function of the policy rate spread with a loading that depends on the dynamics of the policy rate spread as well as the covariance between the spread and the term premium.

On May 27, 2021, this speech was updated to add a sentence to footnote 10 and add the following to the "References" section: Gospodinov, Nikolay (2020). "Global Factors in U.S. Yield Curve," working paper, July, available at https://sites.google.com/site/gospodinovfed.

1. The views expressed are my own and not necessarily those of other Federal Reserve Board members or Federal Open Market Committee participants. I am grateful to Antulio Bomfim for assistance in drafting these remarks, to Canlin Li for contributing the empirical work, and to Hannah Firestone for preparing the figures. Return to text

2. For instance, Clarida (2019b) discusses the role of falling neutral real rates and longer-term inflation expectations worldwide in the decline in global sovereign bond yields. Return to text

3. See Ferreira and Shousha (2021) for a rigorous econometric study of the fundamental determinants of real interest rates in global general equilibrium. Return to text

4. Diebold, Li, and Yue (2008) extended the single-country model developed by Diebold and Li (2006) to a multicountry framework that allows for both global and country-specific factors to affect domestic yield curves. In these remarks, for ease of exposition, I define the global level factor as the simple average of the Diebold-Li country level factors (renormalized as discussed in the notes to figure 1). Return to text

5. Recent work by Bauer and Rudebusch (2020) highlights the role of movements in neutral real interest rates in the dynamics of the yield curve. Return to text

6. Interestingly, it was the success of credible inflation targeting, in addition to financial globalization, that has put central banks in the "slope" business. In a world in which inflation expectations are not well anchored, monetary policy can have a major effect on the level of interest rates by shifting, for better or worse, longer-term inflation expectations, as was the case in the United States from the 1960s through the early 1990s (Clarida, Galí, and Gertler, 2000). Return to text

7. See Bomfim (1997) for an early exploration of the "policy rate spread" as a factor embedded in the Treasury yield curve as well as an early effort to obtain an estimate of $$r\ast\ $$ consistent with medium-term macroeconomic equilibrium. See also the appendix for a simple model linking the neutral nominal interest rate, the yield curve, the policy rate spread, and the term premium. Return to text

8. For example, over the subsample 1999:Q1–2014:Q1, a regression of the DL slope factor embedded in the gilt (bund) yield curve on the U.K. (euro area) policy rate spread yields an R2 of 0.83 (0.61) with a coefficient on the policy rate spread of 0.91 (0.96), results that are comparable with the estimates for the Treasury curve discussed earlier. However, in the remaining subsample 2014:Q2 to 2019:Q4, the slope factor in these two countries is much flatter than predicted by the empirical relationship with the policy rate spread that holds in the earlier subsample. Return to text

9. I think of $$r\ast\ $$ and the policy rate spread as mapping a potentially large set of macroeconomic fundamentals into two scalars and thus enabling dimension reduction compatible with a factor model structure. For example, the Ferreira and Sousha (2021) specification for $$r\ast\ $$ includes six explanatory variables, one of which is a trade-weighted index of global productivity and demographic trends. Likewise, one can always write the policy rate spread as $$r\ast\ +\ \pi\ast\ -\ \{{r\ast\ +\ \pi\ast\ +\ 1.5(\pi\ -\ \pi\ast)\ +\ 0.5(gap)\ +\ dev}\ \} =\ 1.5(\pi\ -\ \pi\ast)\ -\ 0.5(gap)-\ dev$$, where $$dev$$ is the deviation from a Taylor rule with a time-varying intercept equal to $$r\ast\ +\ \pi\ast\ $$. Return to text

10. For example, Ferreira and Sousha (2021) attribute 85 basis points of the decline in U.S. neutral real interest rates since 2000 to global spillovers. Moreover, in their model, foreign central bank purchases of U.S. Treasury securities are a significant contributor to fluctuations in the supply of safe assets, which in turn empirically account for much of the variation in global real interest rates in their model. The notion of two-way causality was also examined empirically by Gospodinov (2020), who added a global factor to an otherwise standard affine term structure model of the U.S. Treasury curve. Return to text

11. Also note from figure 6 that in the weeks before and after the Brexit vote, the 10-year Treasury yield and the dollar–pound exchange rate were rising and falling together as the market assessed the likelihood of a Brexit vote (before) and the implications of a Brexit vote (after). Return to text

12. The finding of two-way causality suggests that major central banks (not just the Federal Reserve) still retain a fair amount of "monetary autonomy," as discussed recently by Panetta (2021). Return to text

13. Ehrmann, Fratzscher, and Rigobon (2011) also examined potential spillovers between the United States and the euro area in the money and equity markets, finding that, particularly in the latter, spillovers from the euro area to the United States were very small, whereas those from the United States to the euro area were quite sizable. They attributed this asymmetry to the central role that U.S. equity markets play in world equity markets. Ehrmann, Fratzscher, and Rigobon (2011) used Rigobon's (2003) identification-through-heteroskedasticity methodology to estimate a structural model where various asset prices are determined simultaneously in the United States and the euro area. Return to text

14. The evidence of two-way causality is also consistent with the U.S. economy's increasing integration with the rest of the world, which has made it more exposed to foreign shocks (Clarida, 2019a). Return to text

15. Of course, there are very likely other fundamentals—such as equilibrium term premiums required to hold long-duration sovereign bonds and, in many countries, default and illiquidity premiums required to hold riskier sovereign debt—that are embedded in yield curve level and slope factors in addition to neutral policy rates and longer-term inflation expectations. Return to text

16. The focus of these remarks has been on sovereign bond markets and monetary policy, but monetary policy is, of course, also transmitted through the foreign exchange market. See Clarida (2019c) for a global model of monetary policy, exchange rates, and neutral real interest rates. Return to text