April 14, 2011

Small Business Credit Availability

Governor Elizabeth A. Duke

At the 2011 International Factoring Association Conference, Washington, D.C.

It's a pleasure to be here this morning. I appreciate the opportunity to take part in this conference and to talk with you about credit conditions--especially conditions in the small business lending market. Credit availability is a necessary component of economic recovery, and factoring represents an important source of credit for large and small businesses.

Credit markets normally recover slowly following financial crises, and the most recent episode was no exception. However, after declining throughout 2009 and much of 2010, recent measures of aggregate credit outstanding have shown some signs of improvement. Nonrevolving consumer credit outstanding, which includes auto and student lending, has increased for the past seven months. Issuance of corporate bonds has been robust for several quarters, and new issuance of commercial mortgage-backed securities picked up in the first quarter of 2011, albeit from very low levels. Commercial and industrial (C&I) loans outstanding have resumed growing modestly on average.

While credit availability seemed to improve for large companies throughout the past year, small businesses still complained of difficulty in gaining access to credit. Recent anecdotes lead me to believe that conditions are improving for small businesses, but data are scarce for this market. Today I will pull together information from a variety of sources, including surveys of small businesses and surveys of lenders, to paint a picture of the credit conditions currently facing small businesses.

Sources of Financing for New and Existing Small Businesses

Small businesses are central to creating jobs and to restoring our economic prosperity. The economic importance of small businesses is due in part to the fact that about one-half of all Americans are employed by firms with fewer than 500 employees. In addition, business start-ups are a critical component of the experimentation process that contributes to restructuring and growth in the United States on an ongoing basis. Indeed, each wave of firm start-ups creates a substantial number of jobs. Over the past two decades, firms less than two years old accounted for about one-fourth of gross job creation even though such enterprises employed less than 10 percent of the workforce.1 But, as a note of caution, these young firms also have high job destruction rates; within five years of starting up, about 40percent of the jobs initially created have been eliminated by the firms' exit from their market. The "up or out" dynamics of start-ups and young firms are consistent with the innovation, learning, and market selection that is associated with entrepreneurship.

Given the key role that start-up and established small businesses play in job creation, it is useful to consider how start-ups are typically funded and how the owners of more-mature, but still small, businesses tend to support their ongoing operations. To this end, the Federal Reserve's 2010 Survey of Consumer Finances (SCF) provides some new and very preliminary data regarding the primary sources of money used to start, acquire, or expand closely held businesses.2 The survey was conducted largely over the second half of 2010.

In this discussion, I will focus on the responses by owners of businesses with fewer than 500 employees that were in operation at the time of our survey. For these small and nascent businesses, more than 70 percent were initiated using personal savings or assets, about 6 percent were initiated using a personal loan from a bank or savings institution, about 3 percent were initiated using a personal or business credit card, and just 3 percent were initiated using a business loan from a bank or savings institution. Even smaller percentages of start-up small businesses appear to have received funding from credit unions, other institutions, or investors. In short, our survey data suggest that the personal resources of entrepreneurs are the most important funding source for small business formation.

The importance of personal resources in financing small businesses is supported by other recent survey evidence. In our 2009 panel SCF, we found that families make loan guarantees for their businesses using personal assets as collateral, and that loans between business owners and their businesses are common in both directions.3 Moreover, according to the most recently available data from the U.S. Census Bureau's Survey of Business Owners, 6 in 10 small business owners use personal savings or assets to finance or expand their businesses.

These responses highlight the role personal wealth plays in business formation. Looking back at wealth outcomes in 2009, we found that 43 percent of families saw a wealth decline equal to or greater than six months of their usual income, and almost one-third saw a loss greater than an entire year of the usual income.4 Such wealth declines would, of course, reduce the likelihood that such households would start a small business.

Over the same period, however, about one-fifth of families saw a gain in wealth that was greater than six months of their usual income. Moreover, a higher percentage of business owners who participated in the survey saw larger wealth gains relative to their incomes than was the case for the overall population. These findings suggest that there just might be a pool of potential entrepreneurs who have both the resources and relevant experience to start successful businesses.

Turning to the funding needs of more-mature businesses, in the 2010 SCF, we asked small business owners whether and to what extent external sources of money were used to finance the ongoing operations of or improvements to their primary businesses in the past year. Focusing again on only businesses with fewer than 500 employees, the preliminary survey data suggest that for such purposes, slightly less than one-half of these businesses did not use any external funding. Consistent with the funding information on the start-up phase for small businesses, a significant proportion of small business owners--about one-third--used their personal savings or assets to fund operations or make improvements. And only small percentages of small business owners obtained credit from a bank or savings institution for such purposes: Among these small business owners, about 5 percent used personal or business credit cards, slightly less than 5percent used business loans, and about 3 percent used personal loans.

Taken together, these survey data suggest that many small business owners do not tap the credit markets, but instead use their own wherewithal to start and fund their businesses. Indeed, a bit less than 80 percent of small business owner survey respondents with fewer than 500 employees indicated that they had not even applied for business loans in the past five years. This is not to say that loans are not important--far from it--but that for a broad range of businesses, personal finances may be the determining factor in starting a business, and personal finances may also be most important in sustaining the health of a business once started.

So what happened to the small business owners who did apply for loans? The turndown rate was fairly modest--about 12 percent. Moreover, for those small business owners who received credit, more than 90 percent of those surveyed actually received as much credit as they had requested. These results are perhaps surprising given that two of the past five years were ones with very tight credit conditions by historical standards, and anecdotal evidence suggests that many lines of credit, for businesses and for households, were cut during the recent financial crisis.

Furthermore, small business lending is an important part of overall bank lending, especially at community banks. According to regulatory data, small loans to businesses, a proxy for loans to small businesses, constituted 23 percent of total business loans outstanding at commercial banks at the end of 2010.5 Over the past several years, this share has fluctuated between 22 and 27 percent of banks' business lending. In addition, at community banks with less than $1 billion in assets, the share is higher--around 66 percent--whereas at larger banks with more than $10 billion in assets, the share is lower--16 percent.

Small Business Concerns

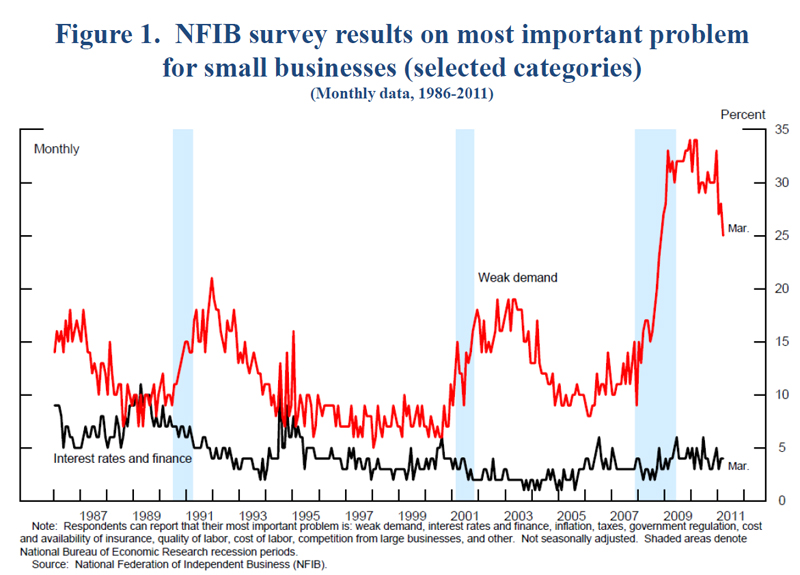

The foregoing survey data on turndown rates and credit constraints for small business owners are consistent with other survey evidence collected by the National Federation of Independent Business (NFIB). In fact, over the past five years, small business owners identified weak demand, taxes, and government regulations more frequently than interest rates and credit conditions as their most important problem. During that period, less than 5 percent of small business respondents typically identified interest rates and credit conditions as their most important problem. In contrast, 25 percent or more of small business owners considered weak demand the most important concern during much of the past three-year period (figure 1). In considering responses to this question, however, it is important to remember that the survey allows owners to identify only their most important problem, not a set of problems. It is possible that financing was the second-most-important problem, but we would not know it from this set of data.

{kind=link}

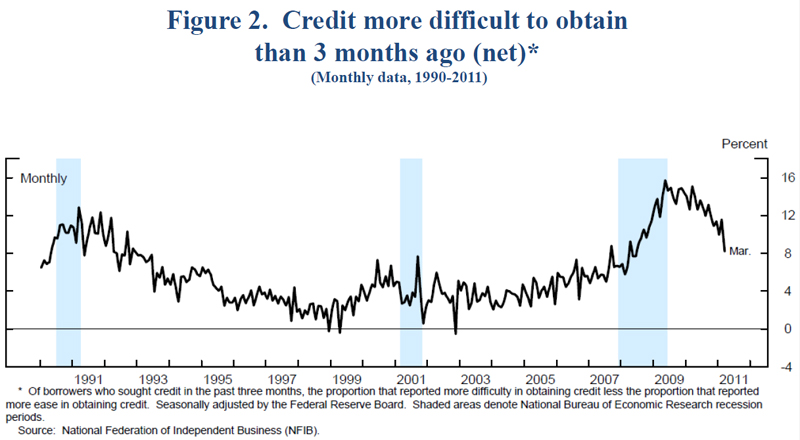

Even if tight credit is not the most important concern, perceptions of tight credit still might significantly influence the decisions made by current and prospective small business owners. Among the small business borrowers surveyed by the NFIB, a fairly high net percentage--about 8 percent in March--continues to report that credit is more difficult to obtain than it was three months ago (figure 2). This level of self-reported perceptions of tighter credit for small businesses is about the same as was observed in 2007--a period prior to the recent business cycle peak. It is also well below the 16percent of small business respondents, on net, who perceived that credit had become more difficult to obtain in 2009.

{kind=link}

Looking back to 2009, a Ewing Marion Kauffman Foundation longitudinal study of small businesses that were founded in 2004 and tracked since then found that 89 percent of the surviving firms that were denied loans in that year felt that banks' heightened requirements played a role in their denials.6 Among the small businesses that were tracked, 21 percent had chosen not to apply for loans for fear of being denied credit, and 5 percent also refrained from seeking external equity financing for fear of being denied such financing. So it seems that perceptions of credit tightness may lead some small business owners to decide not even to try to obtain additional funding.

At this time, however, the net percentage of survey respondents telling the NFIB that they expect credit conditions to become tighter over the next three months has come down considerably from what small business owners reported during 2009. This decrease suggests that, compared with the previous few years, far fewer small business owners are expecting that credit conditions will remain tight.

Overall, what seems to matter most with regard to funding, from the small business owner's viewpoint, is one's personal savings or assets, the internally generated funds derived from operating the business, expected sales, and the fact that credit conditions seem to be less tight, so money is available, if and when it is needed.

Business Conditions for Small Businesses

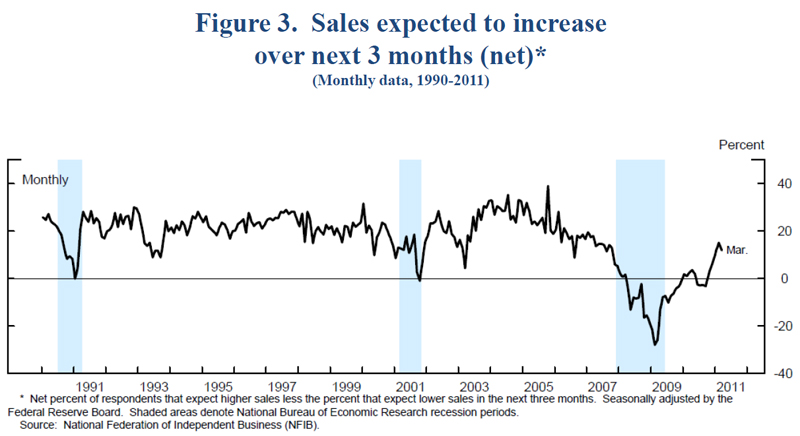

Currently, expectations about future sales seem to be more important than expectations about the availability of credit in driving business spending decisions and demand for business loans. Recently, small business owners appear to have become more optimistic about their outlook for sales. For example, in recent NFIB surveys, the net percentage of respondents who expected their sales to increase rose to levels not seen since mid-2007 (figure 3).

{kind=link}

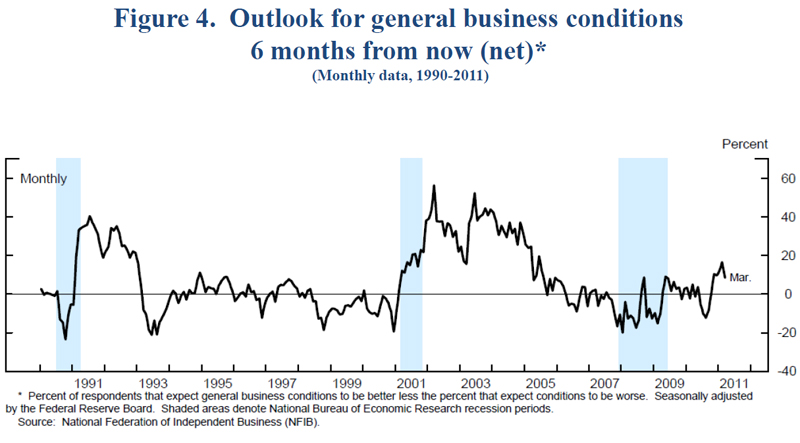

More generally, small business owners surveyed by the NFIB indicate that they currently expect business conditions to improve in the near future. In fact, the net percentage of small business respondents who expected business conditions to improve six months from now climbed in February to its highest level in several years (figure 4). Even with some backtracking in March, this barometer of business conditions remains at a level not seen since mid-2007.

{kind=link}

Other survey data collected by the NFIB are also consistent with more-favorable conditions for small businesses. The percentages of small business respondents who believe it is a good time to expand, and who plan to make capital expenditures over the next three to six months, have recently risen to levels not seen since mid-2007.

The Bankers' Perspective on Lending to Small Businesses

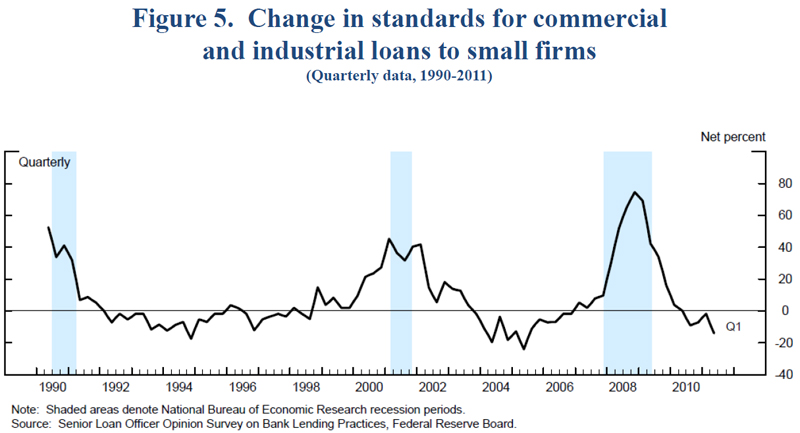

Mirroring small business respondents views with respect to credit conditions are bankers' views on credit standards and their terms of credit. To consider the bankers' perspective, I will draw on two other Federal Reserve surveys: the Senior Loan Officer Opinion Survey on Bank Lending Practices (SLOOS) and the Survey of Terms of Business Lending (STBL). With regard to credit standards, we found that about 5percent of banks, on net, reported in January that they had eased their bank's lending standards on commercial and industrial loans to small firms in the fourth quarter of last year (figure 5).7 A similar net fraction of banks reported having eased standards in the previous survey. This finding is consistent with small business owners' perceptions that credit conditions have eased somewhat.

{kind=link}

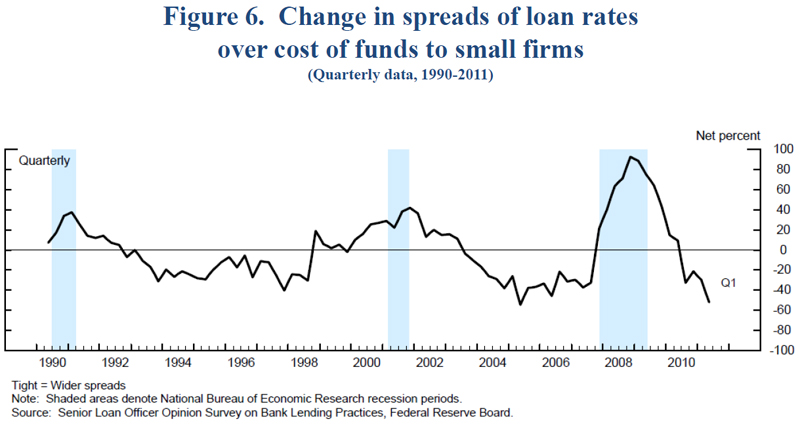

For those small business owners whose loans or credit lines were approved, the terms of credit--the interest rate spread over the bank's cost of funds, the cost of a credit line, the maturity, and the size of a loan--are practical measures that can be used to assess credit availability. The January SLOOS indicates that about one-third of banks, on net, reported that they had trimmed the spreads of C&I loan rates over their costs of funds on loans to small firms (figure 6). Somewhat smaller net fractions of these loan officers reported that they had lowered the costs of credit lines and lengthened the maximum maturities of loans to small firms. Despite the fact that such terms of credit were eased for small firms, the banks reported that the maximum sizes of C&I loans, and limits on credit lines and business credit card accounts, remained unchanged over the past two surveys. This result means that such lines were not being cut as they were during the first half of 2010. Easing of credit conditions usually does not occur until banks see improvement in the credit metrics of existing portfolios. In the January SLOOS, 77 percent of bankers reported having seen an improvement in the quality of existing loans to small firms.

{kind=link}

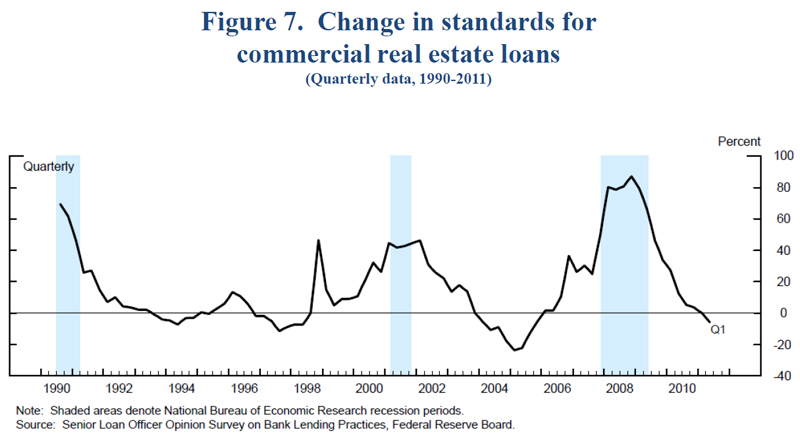

The SLOOS does not distinguish between commercial real estate loans to small firms and such loans to others, but we know that real-estate-secured lending is an important source of credit for small businesses. The respondents to the January SLOOS indicated that there was little movement, on net, in domestic banks' lending standards for commercial real estate loans over the past two surveys (figure 7). Such standards remain relatively tight even though more than one-half of banks expect an improvement in the quality of commercial real estate loans. And, importantly for small business owners, the commercial bank Call Reports indicated that as of the end of last year, the loans secured by owner-occupied property had continued to outperform other commercial real estate loans.

{kind=link}

Information contained in the February STBL also indicated a recent easing of terms on bank loans. More specifically, recent loan rate spreads on C&I loans at domestic banks were lower, on average, regardless of the bank's size, and the average number of days to maturity had lengthened.

The recent easing in banks' lending policies and banks' improved expectations with respect to credit quality are indications that financing conditions for at least some small businesses are likely improving.

By and large, small business owners' perceptions about the tightness of credit conditions seem to be aligned fairly well with bankers' perceptions of late. Such perceptions are also consistent with recent turndown statistics. According to the National Small Business Association (NSBA), the percentage of small business owners reporting an inability to obtain adequate financing declined to 36 percent at year-end from 41 percent in July 2010.8 These data, of course, apply to members of the NSBA, whereas the SCF data I discussed earlier apply in principle to all small business owners, even owners of quite small businesses who might be unlikely to join an association. This may explain the much higher credit use among NSBA members.

Lending to Small Businesses

So far, I have discussed measures of business credit. But, as I noted earlier, small businesses also rely on personal accounts and loans, household credit cards, trade credit from other nonfinancial firms, and other sources, including factoring. The effect of these other sources of funding on businesses' finances is even more difficult to determine from available data.

Changes in personal wealth during the downturn were not uniform across households, and there were some big winners and losers. While the households that disproportionately increased their wealth are more likely to start businesses, those that disproportionately lost wealth are less likely to do so. In particular, the recent housing downturn has made it more difficult to use cash-out refinancing or home equity lending as a funding vehicle for small business formation. It has also made it more difficult for some small business owners to fund the purchase of equipment or to cover business operating expenses.

Even though our survey data suggest that only 3 to 5 percent of small business owners tend to rely on personal or business credit cards, the decline in bank credit card outstandings over most of the past two years indicates that this source of credit may still be quite limited.

While balance sheet data for financial institutions are readily available, the relative contributions to changes in outstanding balances of new lending, paydowns, and write-downs and the levels of line usage are not available. To focus on the link between lending and new business activity, we need measures of loan originations. Indeed, a loan or lease origination is what typically generates an investment in equipment and signals business growth.9

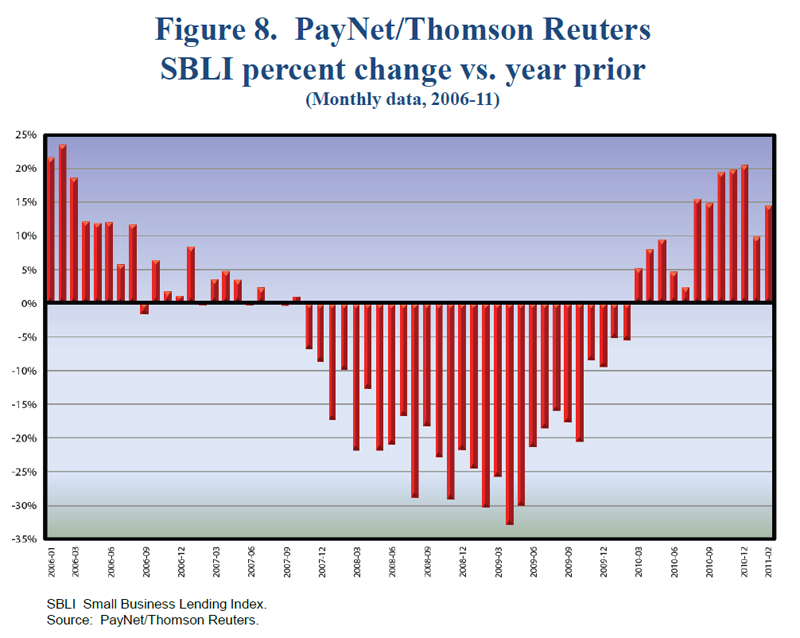

To explore recent loan and lease originations to small businesses, we can look at the PayNet/Thomson Reuters Small Business Lending Index (SBLI). For inclusion in this index, a loan or lease must be originated to a business borrower who has total loan outstandings across all qualifying lenders of less than $1 million at both the start and the end of the month in question. While some such loans and leases may be to established firms that employ more than 500 workers, small businesses are generally viewed as much more likely to borrow in these relatively small loan denominations. The lenders that provide the data used to construct the index are banks and finance companies.

The year-over-year changes in the SBLI are consistent with a view that loan originations are a pro-cyclical indicator (figure 8). Strikingly, such year-over-year changes were mainly positive, but smaller through time, until the recent business cycle peak in December 2007. During the recession, however, the year-over-year changes in the SBLI were increasingly negative until the business cycle trough, which occurred in June 2009. Then, shortly after the recent business cycle trough, the year-over-year negative changes in the index became smaller until they turned positive in early 2010. In February, the most recent month for which data are available, the SBLI measure of business loan and lease originations rose 15 percent from a year earlier.

{kind=link}

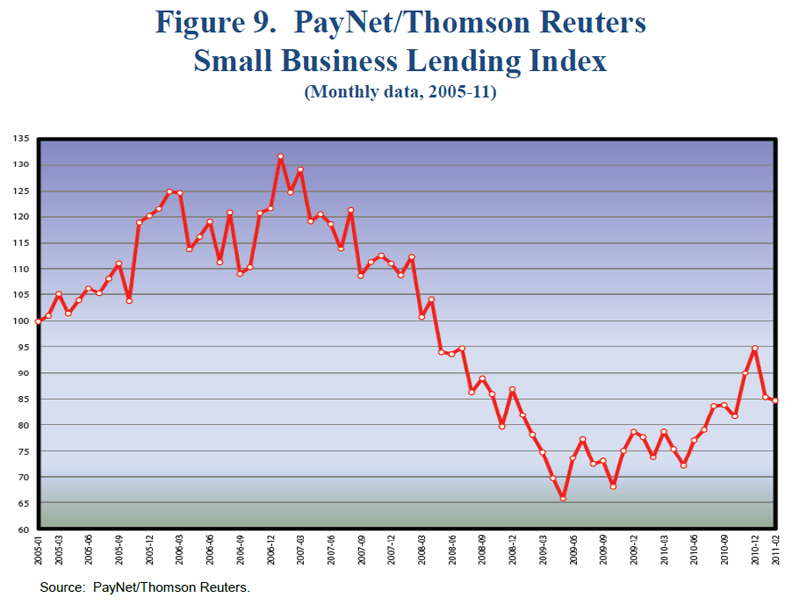

The seasonally adjusted index, which is normalized to 100 in January 2005, provides a different take on small business originations (figure 9). This measure of lending, which allows comparisons across different months, has not yet rebounded to its level in mid-2007 even though many of the measures of small business owners' and bankers' perspectives have returned to their pre-recession levels. Despite the magnitude of the rebound, there has been an apparent turnaround in loan and lease originations using the seasonally adjusted SBLI measure. These data add to the evidence that credit availability to small businesses is gradually improving.

{kind=link}

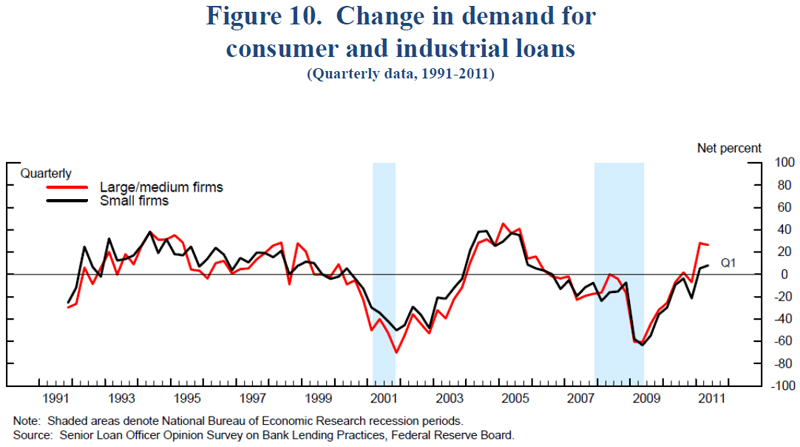

While at first glance stronger demand for bank loans by large and medium-sized firms may seem irrelevant for analyzing credit to small businesses, that perception would ignore the fact that such demand may signal that larger firms are becoming more willing to provide trade credit to smaller firms that are their suppliers or customers. In the most recent SLOOS, the net percentage of respondents reporting higher loan demand by large and medium-sized firms rose above 20 percent for the first time since 2005 (figure 10). That said, banks report that loan demand from smaller firms remains fairly weak. Only a small net percentage of banks reported stronger demand from such firms.

{kind=link}

Conclusion

To sum up, the financial conditions that would be necessary for small businesses to start up and thrive would include positive conditions for personal wealth building and a full range of consumer and business credit availability. In the wake of the financial crisis, small business owners and potential small business owners likely experienced a substantial reduction in the personal resources necessary to start or sustain a business. At the same time, small business loans became harder to get, and when they were available, both price and nonprice credit terms were likely quite restrictive. Many small business owners were so convinced that their requests would be denied that they did not even apply for credit. Despite this restricted credit availability, small business owners, by a large margin, still considered their most significant problem to be weak sales. Although no definitive data source exists, the combination of a variety of recent survey results paints a picture of increasing optimism about future sales and business conditions and a corresponding easing of credit availability for small businesses.

1. See John C. Haltiwanger, Ron S. Jarmin, and Javier Miranda (2010), "Who Creates Jobs? Small vs. Large vs. Young," NBER Working Paper Series 16300 (Cambridge, Mass.: National Bureau of Economic Research, August). Return to text

2. The report with the results of the 2010 SCF is expected to be released in early 2012 after all data from the survey have been assessed and analyzed. Return to text

3. Unlike the 2010 Survey of Consumer Finances, which is a point-in-time cross-sectional survey, the 2009 survey is based on follow-up interviews with participants in the 2007 SCF that update their information. For a research paper that provides an overview of the 2009 data, see Jesse Bricker, Brian Bucks, Arthur Kennickell, Traci Mach, and Kevin Moore (2011), "Surveying the Aftermath of the Storm: Changes in Family Finances for 2007 to 2009," Finance and Economics Discussion Series 2011-17 (Washington: Board of Governors of the Federal Reserve System, March). Return to text

4. See Elizabeth A. Duke (2011), "Changed Circumstances: The Impact of the Financial Crisis on the Economic Condition of Workers Near Retirement and of Business Owners," speech delivered at the Virginia Association of Economists Sandridge Lecture, Richmond, Va., March 24. Return to text

5. The data are from the quarterly Call Reports, which ask banks to report their holdings of C&I loans made in original amounts of less than $1 million. Return to text

6. See Alicia Robb and E.J. Reedy (2011), An Overview of the Kauffman Firm Survey: Results from 2009 Business Activities (Kansas City, Mo.: Ewing Marion Kauffman Foundation, March). Return to text

7. In this and later figures, shaded bars indicate periods of business recession as defined by the National Bureau of Economic Research. Return to text

8. National Small Business Association (2011), 2010 Year-End Economic Report (1.7 MB PDF) (Washington: NSBA). Return to text

9. Thomson Reuters provides some statistical tests showing that changes in the prior month's Small Business Lending Index values can predict the current month's change in the U.S. Leading Economic Indicators Index. See Andrew Clark and Thomas Ware (2010), "Looking into the Future with the Thomson Reuters/PayNet Small Business Lending Index (SBLI)," white paper (Thomson Reuters, May). Return to text