January 03, 2016

Monetary Policy, Financial Stability, and the Zero Lower Bound

Vice Chairman Stanley Fischer

At the Annual Meeting of the American Economic Association, San Francisco, California

Vice Chairman Fischer presented identical remarks to the Banque de France and Bank for International Settlements Farewell Symposium for Christian Noyer on January 12, 2016.

Thank you. It is a great pleasure to be here today and to participate in this panel together with such a distinguished group.

Much has happened in the world of central banking in the past 10 years. The list of challenges we face is long and includes fundamental issues such as lender-of-last-resort policies in the modern financial system, the role of central banks in the supervision of the financial sector, and the appropriate role of forward guidance in monetary policy communications. Those are the topics I will not discuss today.

Rather, I will focus primarily on three related issues associated with the zero lower bound (ZLB) on nominal interest rates and the nexus between monetary policy and financial stability: first, whether we are moving toward a permanently lower long-run equilibrium real interest rate; second, what steps can be taken to mitigate the constraints imposed by the ZLB on the short-term interest rate; and, third, whether and how central banks should incorporate financial stability considerations in the conduct of monetary policy.1

Are We Moving Toward a World With a Permanently Lower Long-Run Equilibrium Real Interest Rate?

We start with a key question of the day: Are we moving toward a world with a permanently lower long-run equilibrium real interest rate? The equilibrium real interest rate--more conveniently known as r*--is the level of the short-term real rate that is consistent with full utilization of resources. It is often measured as the hypothetical real rate that would prevail in the long-run once all of the shocks affecting the economy die down.2 In terms of the Federal Reserve's approach to monetary policy, it is the real interest rate at which the economy would settle at full employment and with inflation at 2 percent--provided the economy is not at the ZLB.

Recent interest in estimates of r* has been strengthened by the secular stagnation hypothesis, forcefully put forward by Larry Summers in a number of papers, in which the value of r* plays a central role.3 Research that was motivated in part by attempts that began some time ago to specify the constant term in standard versions of the Taylor rule has shown a declining trend in estimates of r*. That finding has become more firmly established since the start of the Great Recession and the global financial crisis.4

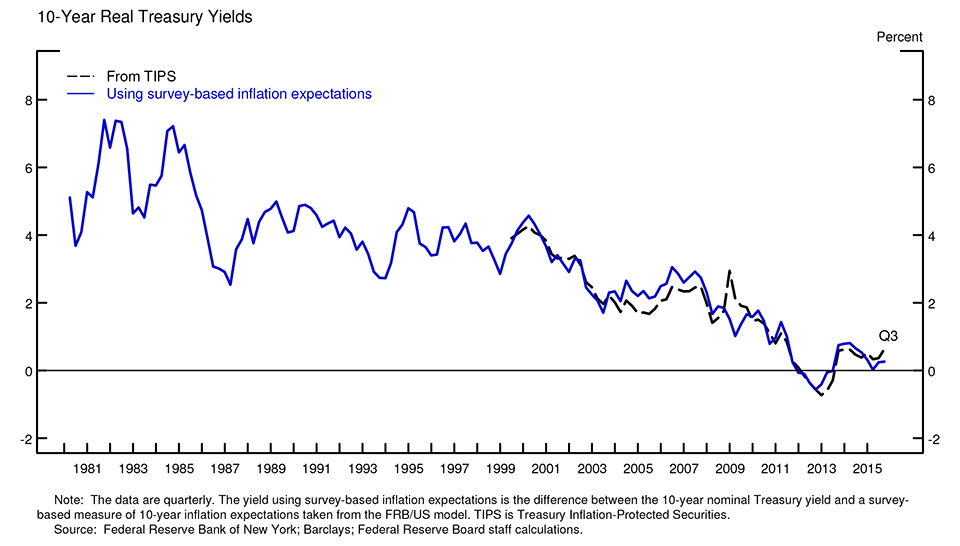

A variety of models and statistical approaches suggest that the current level of short-run r* may be close to zero. Moreover, the level of short-run r* seems likely to rise only gradually to a longer-run level that is still quite low by historical standards. For example, the median long-run real federal funds rate reported in the Federal Reserve's Summary of Economic Projections prepared in connection with the December 2015 meeting of the Federal Open Market Committee has been revised down about 1/2 percentage point over the past three years to a level of 1-1/2 percent.5 As shown in the figure, a decline in the value of r* seems consistent with the decline in the level of longer-term real rates observed in the United States and other countries.

{kind=link}

What determines r*? Fundamentally, the balance of saving and investment demands does so. A very clear systematic exposition of the theory of r* is presented in a 2015 paper from the Council of Economic Advisers. Several trends have been cited as possible factors contributing to a decline in the long-run equilibrium real rate. One a priori likely factor is persistent weakness in aggregate demand. Among the many reasons for that, as Larry Summers has noted, is that the amount of physical capital that the revolutionary IT firms with high stock market valuations have needed is remarkably small. The slowdown of productivity growth, which has been a prominent and deeply concerning feature of the past four years, is another factor reducing r*.6 Others have pointed to demographic trends resulting in there being a larger share of the population in age cohorts with high saving rates.7 Some have also pointed to high saving rates in many emerging market countries, coupled with a lack of suitable domestic investment opportunities in those countries, as putting downward pressure on rates in advanced economies--the global savings glut hypothesis advanced by Ben Bernanke and others at the Fed about a decade ago.8

Whatever the cause, other things being equal, a lower level of the long-run equilibrium real rate suggests that the frequency and duration of future episodes in which monetary policy is constrained by the ZLB will be higher than in the past. Prior to the crisis, some research suggested that such episodes were likely to be relatively infrequent and generally short lived.9 The past several years certainly require us to reconsider that basic assumption.

Moreover, the experience of the past several years in the United States and many other countries has taught us that conducting monetary policy effectively at the ZLB is challenging, to say the least.10 And while unconventional policy tools such as forward guidance and asset purchases have been extremely helpful, there are many uncertainties associated with the use of such tools.11

I would note in passing that one possible concern about our unconventional policies has eased recently, as the Federal Reserve's normalization tools proved effective in raising the federal funds rate following our December meeting. Of course, issues may yet arise during normalization that could call for adjustments to our tools, and we stand ready to do that.

The answer to the question "Will r* remain at today's low levels permanently?" is that we do not know. Many of the factors that determine r*, particularly productivity growth, are extremely difficult to forecast. At present, it looks likely that r* will remain low for the policy-relevant future, but there have in the past been both long swings and short-term changes in what can be thought of as equilibrium real rates Eventually, history will give the answer.

But it is critical to emphasize that history's answer will depend also on future policies, monetary and other, notably including fiscal policy.

What Steps Can Be Taken to Mitigate the Constraints Associated with the ZLB?

Against that backdrop, a second key question for central banks is, What steps, if any, can be taken to mitigate the constraints associated with the ZLB?

-

Raising the Inflation Target: One step that has been proposed by many, including Olivier Blanchard, is the possibility of raising the target rate of inflation from 2 percent to some higher level. One concern I have raised in the past about such proposals is that high levels of inflation may also be associated with higher inflation variability. The welfare costs of high and variable inflation could be substantial. For example, more variable inflation would make long-run planning more difficult for households and businesses. And higher and more variable inflation would likely also lead to higher levels of indexation in the economy over time that, in turn, would make it more difficult for central banks to achieve their inflation goals.

- Negative Interest Rates: Another possible step would be to reduce short-term interest rates below zero if needed to provide additional accommodation. Our colleagues in Europe are busy rewriting economics textbooks on this topic as we speak--and also helping us to remember earlier discussions of negative interest rates by Keynes, Irving Fisher, Hicks, and Gesell.12

To provide further monetary accommodation amid weak inflation prospects, the European Central Bank lowered its deposit rate into negative territory in June 2014 and twice cut it further, most recently to minus 0.30 percent in December. The Riksbank has lowered its key repurchase agreement, or repo, rate to a similar level, while the central banks of Denmark and Switzerland have cut their key policy rates more deeply, to minus 0.75 percent, in large part to offset considerable appreciation pressures on their currencies.

In each of these countries, short-term money market rates declined along with policy rates. Moreover, while it is hard to distinguish the effects of the rate cuts from those of concurrent asset purchase expansions, the easing appears to have been transmitted to assets of longer maturity and greater risk. Bond yields and bank lending rates declined, and, in the euro area, the volume of lending to corporations and households picked up notably. In addition, the rate cuts into negative territory have acted as expected through the exchange rate channel.

Negative policy rates have generally not been associated with the problems that likely were anticipated. Adverse effects on money market functioning have been limited. Cash holdings have not risen significantly in these countries, in part because of nonnegligible costs of insuring, storing, and transporting physical cash. These favorable outcomes may be partly because significant shares of deposits at central banks in these countries are not subject to negative rates. It is unclear how low policy rates can go before cash holdings rise or other problems intensify, but the European experience has certainly shown that zero is not the effective lower bound in those countries.

Could negative interest rates be a policy response that the Federal Reserve could choose to employ in a future crisis? One possible concern with a strategy of this sort in the United States is the potential for destabilizing effects in money markets. For example, various observers have noted that negative rates could lead to scenarios in which money funds "break the buck" or simply shut down, either of which could generate strains in money markets. Another concern is whether the complex and interconnected infrastructure supporting securities transactions in the U.S. financial system could readily adapt to a world of negative interest rates. For example, similar to the types of issues addressed ahead of the year 2000, there could well be automated systems that simply are not coded properly at present to process transactions based on instruments with negative rates. All of these are, of course, transitional problems, but they might be sufficient to make a move to negative rates difficult to implement on short notice.

- Raising the Equilibrium Real Rate: An even more ambitious approach to ease the constraints posed by the zero lower bound would be to take steps aimed at raising the equilibrium real rate. For example, expansionary fiscal policy would boost the equilibrium real rate. In particular, the need for more modern infrastructure in many parts of the American economy is hard to miss. And we should not forget that additional effective investment in education also adds to the nation's capital.

As another example, numerous studies of the effects of the Federal Reserve's asset purchases suggest that these operations have reduced the level of the term premium embedded in long-term interest rates.If aggregate demand depends primarily on the level of long-term interest rates, it might be possible, in principle, to maintain a level of long-term rates consistent with full employment and stable prices by lowering term premiums while at the same time raising the level of short-term rates by a compensating amount. This result could be accomplished, for example, if the Treasury took steps to shorten the average maturity of Treasury debt outstanding or, alternatively, if the Federal Reserve maintained large holdings of long-term assets.

- Eliminating the ZLB Associated with Physical Currency: While the European experience suggests that interest rates can be pushed somewhat below zero, the existence of physical currency likely still limits how deeply interest rates can be pushed into negative territory. That observation has led some to ask whether it would it be possible for the financial system to operate effectively without physical currency provided by the central bank. This is a theoretical question that has fascinated economists for decades and, with advances in technology, could possibly have practical implications as well. Indeed, the Scandinavian countries have embraced the development of new payments technologies that seem to be reducing the need for physical currency for transactions in those countries.13 Nonetheless, a transition to a cashless economy in the United States seems very far off; indeed, U.S. currency outstanding has been increasing relative to nominal gross domestic product over recent decades, driven importantly by foreign demands for U.S. bank notes. Moreover, to eliminate the ZLB associated with physical currency by going cashless, countries would need to transition to an economy that did not require widespread use of physical currency, and central banks in those countries would need to cease issuing physical currency on demand (for example, in response to demands spurred by negative rates on so-called inside money).14 For all of these reasons, as a practical matter at least for the United States, it seems highly unlikely that the constraints associated with the ZLB could be meaningfully addressed by steps to encourage a transition to a cashless economy.

None of these options for dealing with the difficulties of the ZLB suggest that it will be easy either to raise the equilibrium real rate or to mitigate the constraints associated with the ZLB. But when the real rate is close to zero, even small effects can make a noticeable difference. And, of course, such issues are clearly worthy of additional research.

How Should Central Banks Incorporate Financial Stability Considerations in the Conduct of Monetary Policy?

The challenges associated with the ZLB and the potential risks resulting from an environment of extremely low rates for a prolonged period of time bring me to the third question: How should central banks incorporate financial stability considerations in the conduct of monetary policy? Or, put another way, can we conduct monetary policy in a way that reduces the likelihood of financial instability?15

The first response of policymakers to the question of whether monetary policy--defined as the short-term policy interest rate--should be used to support financial stability is to say that macroprudential tools, rather than adjustments in short-term interest rates, should be the first line of defense.

Macroprudential tools are primarily regulatory or supervisory in nature and target specific activities, markets, and financial institutions. In the United States, we now have some experience with such tools. The interagency guidance on leveraged lending issued in 2013 and the annual coordinated stress tests (the Dodd-Frank Act stress test, or DFAST, mandated by the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010; and the Comprehensive Capital Analysis and Review, or CCAR), focused on the capital adequacy of the largest banking firms, are two examples implemented for a few years now and for which data are available for an assessment of their effectiveness.16

An important new element of the post-crisis capital regime is the Countercyclical Capital Buffer (CCyB), which the Federal Reserve put out for comment on December 21, 2015.17 The CCyB is designed to be activated when there is an elevated risk of above-normal losses in the future and released when the risk of above-normal losses recedes. The higher levels of capital would increase the resilience of the largest banks because they would be better positioned to absorb the losses.

Despite the tools that the Fed can use to support financial stability, including the Fed's authority to impose margin requirements on secured financing transactions, the Fed has fewer macroprudential tools at its command than some other central banks, particularly with respect to real estate. Regulators in many countries facing or anticipating problems with rising real estate prices often turn to controls over loan-to-value or debt-to-income ratios. Such measures are potentially important, as the real estate sector is the most common source of the beginnings of financial instability. In the United States, responding to such problems with these tools would require interagency coordination, which could make their use cumbersome at critical moments.

It is important to acknowledge that there remain cases in which macroprudential tools are either not available or have not been sufficiently tested in the United States, or they may be in conflict with other objectives such as widespread access to credit. The effective lack of such tools has two important consequences. First, it requires placing greater weight on the ability of financial institutions and the financial system as a whole to withstand financial shocks without the authorities having to use macroprudential instruments--that is to say, on structural reforms to the financial system. Second, in such instances, one could consider using monetary policy--the short term policy interest rate--to lean against the wind of financial stability risks.18

The use of monetary policy to address financial stability concerns raises two distinct but closely related sets of questions. The first is whether adjustments in the policy rate can indeed enhance financial stability by reducing either the odds of a financial crisis or the severity of such a crisis once it is under way--and, if so, through which channels.19

Provided that the first question is answered in the affirmative, the second question is how leaning against the wind interacts with the traditional objectives of monetary policy--namely, the employment and inflation mandates in the United States. This tradeoff could be small or even nonexistent when both traditional macro objectives and financial stability objectives call for the same policy action--for example, when the credit cycle is approaching its peak, output is above potential, and inflation pressures appear to be building. In contrast, when different objectives call for different policy actions--for example, when some financial assets appear overvalued but economic growth remains tepid and inflation is subdued--policymakers may find this tradeoff much more difficult to assess and will search for macroprudential tools. Perhaps unsurprisingly, recent contributions in the literature that quantify this tradeoff point to a range of recommendations, with some reporting an optimal monetary policy that leans against the wind and some suggesting otherwise.20

I would like to conclude on this issue by saying that the issue is a bit more complicated than suggested so far--for, given that financial variables are a critical part of the transmission mechanism of monetary policy, when policymakers say the economy is overheating, they may well be considering the behavior of asset prices as a critical part of that phenomenon and part of the reason to tighten monetary policy. Thus, I believe that the real issue of whether adjustments in interest rates should be used to deal with problems of potential financial instability is macroeconomic, and that if asset prices across the economy--that is, taking all financial markets into account--are thought to be excessively high, raising the interest rate may be the appropriate step. Further discussion of this issue will probably bear considerable similarity to the analysis of how to deal with asset bubbles that took place in the United States in the decade starting about two decades ago.

Conclusion

In closing, let me concede that it is easier to pose these questions than it is to answer them definitively. The issues are both deep and interesting. Along with other monetary policy issues, particularly the role of the lender of last resort in a world of significant uncertainty, they deserve the attention the profession in both academic and governmental institutions is, will be, and should be giving them.

References

Adrian, Tobias, Daniel Covitz, and Nellie Liang (2014). "Financial Stability Monitoring," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, August 4.

Agarwal, Ruchir, and Miles Kimball (2015). "Breaking through the Zero Lower Bound (PDF) ," IMF Working Paper WP/15/224. Washington: International Monetary Fund, October.

Ajello, Andrea, Thomas Laubach, David Lopez-Salido, and Taisuke Nakata (2015). "Financial Stability and Optimal Interest-Rate Policy (PDF)," working paper. Washington: Board of Governors of the Federal Reserve System, February.

Alderman, Liz (2015). "In Sweden, a Cash-Free Future Nears," New York Times, December 26, www.nytimes.com/2015/12/27/business/international/in-sweden-a-cash-free-future-nears.html.

Bernanke, Ben S. (2005). "The Global Saving Glut and the U.S. Current Account Deficit," speech delivered at the Homer Jones Lecture, St. Louis, April 14.

Blanchard, Olivier, and John Simon (2001). "The Long and Large Decline in U.S. Output Volatility (PDF) ," Brookings Papers on Economic Activity, 1, pp. 135-74.

Board of Governors of the Federal Reserve System (2015). "Federal Reserve Board Seeks Public Comment on Proposed Policy Statement Detailing the Framework the Board Would Follow in Setting the Countercyclical Capital Buffer (CCyB)," press release, December 21.

Buiter, Willem H., and Nikolaos Panigirtzoglou (2003). "Overcoming the Zero Bound on Nominal Interest Rates with Negative Interest on Currency: Gesell's Solution," Economic Journal, vol. 113 (October), pp. 723-46.

Caballero, Ricardo J., Emmanuel Farhi, and Pierre-Olivier Gourinchas (2008). "An Equilibrium Model of 'Global Imbalances' and Low Interest Rates," American Economic Review, vol. 98 (1), pp. 358-93.

Carlson, Mark, Burcu Duygan-Bump, Fabio Natalucci, William R. Nelson, Marcelo Ochoa, Jeremy Stein, and Skander Van den Heuvel (forthcoming). "The Demand for Short-Term, Safe Assets and Financial Stability: Some Evidence and Implications for Central Bank Policies," International Journal of Central Banking.

Champ, Bruce (2008). "Stamp Scrip: Money People Paid to Use ," Economic Commentary. Cleveland: Federal Reserve Bank of Cleveland, April.

Fisher, Irving (1933). Stamp Scrip. New York: Adelphi Company.

Goodfriend, Marvin (2000). "Overcoming the Zero Bound on Interest Rate Policy," Journal of Money, Credit and Banking, vol. 32 (November), pp. 1007-35.

Gordon, Robert J. (2014). "The Demise of U.S. Economic Growth: Restatement, Rebuttal, and Reflections," NBER Working Paper Series 19895. Cambridge, Mass.: National Bureau of Economic Research, February.

-------- (forthcoming). The Rise and Fall of American Growth: The U.S. Standard of Living since the Civil War. Princeton, N.J.: Princeton University Press.

Hall, Robert E. (2014). "Quantifying the Lasting Harm to the U.S. Economy from the Financial Crisis," in Jonathan Parker and Michael Woodford, eds., NBER Macroeconomics Annual 2014, vol. 29. Chicago: University of Chicago Press.

Hamilton, James D., Ethan S. Harris, Jan Hatzius, and Kenneth D. West (2015). "The Equilibrium Real Funds Rate: Past, Present and Future," NBER Working Paper Series 21476. Cambridge, Mass.: National Bureau of Economic Research, August.

Hicks, J.R. (1937). "Mr. Keynes and the 'Classics': A Suggested Interpretation," Econometrica, vol. 5 (April), pp. 147-59.

International Monetary Fund (2015). Monetary Policy and Financial Stability (PDF) , IMF staff report. Washington: International Monetary Fund, September.

Keynes, John Maynard (1936). The General Theory of Employment, Interest, and Money. London: Macmillan.

Kiley, Michael T. (2015). "What Can the Data Tell Us about the Equilibrium Real Interest Rate? (PDF)" Finance and Economics Discussion Series 2015-077. Washington: Board of Governors of the Federal Reserve System, August.

Laubach, Thomas, and John C. Williams (2003). "Measuring the Natural Rate of Interest ," Review of Economics and Statistics, vol. 85 (November), pp. 1063-70.

McAndrews, James (2015). "Negative Nominal Central Bank Policy Rates: Where Is the Lower Bound? " speech delivered at the University of Wisconsin, Madison, Wis., May 8.

Mendoza, Enrique G., Vincenzo Quadrini, and José-Víctor Ríos-Rull (2009). "Financial Integration, Financial Development, and Global Imbalances," Journal of Political Economy, vol. 117 (3), pp. 371-416.

Reifschneider, David, and John C. Williams (2000). "Three Lessons for Monetary Policy in a Low-Inflation Era," Journal of Money, Credit, and Banking, vol. 32 (November), pp. 936-66.

Reinhart, Carmen M., and Kenneth S. Rogoff (2009). This Time Is Different: Eight Centuries of Financial Folly. Princeton, N.J.: Princeton University Press.

Rogoff, Kenneth (2014). "Costs and Benefits to Phasing out Paper Currency (PDF) ," paper presented at the NBER Macroeconomics Annual Conference, Cambridge, Mass., April 11.

Stein, Jeremy C. (2013). "Overheating in Credit Markets: Origins, Measurement, and Policy Responses," speech delivered at "Restoring Household Financial Stability after the Great Recession: Why Household Balance Sheets Matter," a research symposium sponsored by the Federal Reserve Bank of St. Louis.

Stock, James H., and Mark W. Watson (2003). "Has the Business Cycle Changed and Why?" NBER Macroeconomics Annual 2002, vol. 17 (January).

Summers, Lawrence H. (2014). "U.S. Economic Prospects: Secular Stagnation, Hysteresis, and the Zero Lower Bound," Business Economics, vol. 49 (2), pp. 65-73.

-------- (2015). "Low Real Rates, Secular Stagnation & the Future of Stabilization Policy," remarks delivered at the Bank of Chile Research Conference, November 20, http://larrysummers.com/2015/11/20/low-real-rates-secular-stagnation-the-future-of-stabilization-policy.

Svensson, Lars E.O. (2015). "Cost-Benefit Analysis of Leaning Against the Wind: Are Costs Always Larger than Benefits, and Even More So with a Less Effective Macroprudential Policy? (PDF) " unpublished paper, September.

U.S. Executive Office of the President, Council of Economic Advisers (2015). Long-Term Interest Rates: A Survey (PDF). Washington: EOP.

Williams, John C. (2013). "A Defense of Moderation in Monetary Policy (PDF) ," Working Paper Series 2013-15. San Francisco: Federal Reserve Bank of San Francisco, July.

Woodford, Michael (2012). "Inflation Targeting and Financial Stability," NBER Working Paper Series 17967. Cambridge, Mass.: National Bureau of Economic Research, April.

1. I am grateful to James Clouse, William English, Thomas Laubach, Nellie Liang, David Lopez-Salido, Jeff Marquardt, David Mills, Fabio Natalucci, David Reifschneider, Stacey Tevlin, David Wilcox, and Paul Wood for their assistance. I have benefited also from discussions with John Williams. My comments today reflect my own views and are not an official position of the Board of Governors or the Federal Open Market Committee. Return to text

2. See Laubach and Williams (2003). Return to text

3. See Summers (2014, 2015). Return to text

4. This research includes recent work by Kiley (2015) and others that uses extensions of the original Laubach and Williams (2003) framework. An international perspective on medium-to-long-run real interest rates is provided by U.S. Executive Office of the President (2015). Reinhart and Rogoff (2009) and Hall (2014) discuss the long-lived effects of financial crises on economic performance. See also Hamilton and others (2015). Return to text

5. The projections materials associated with the Federal Open Market Committee's December 2015 meeting are available on the Board's website at www.federalreserve.gov/monetarypolicy/fomccalendars.htm. Return to text

6. It is also a major factor explaining the phenomenon of the economy's impressive performance on the jobs front during a period of historically slow growth. Return to text

7. See, for instance, Gordon (2014, forthcoming). Return to text

8. See Bernanke (2005). See also the recent work by Caballero, Farhi, and Gourinchas (2008) and Mendoza, Quadrini, and Rios-Rull (2009). Return to text

9. See, for instance, Reifschneider and Williams (2000), Blanchard and Simon (2001), and Stock and Watson (2003). Return to text

10. For a discussion of various issues reviewed by the Federal Open Market Committee in late 2008 and 2009 regarding the complications of unconventional monetary policy at the ZLB, see the set of staff memos on the Board's website at www.federalreserve.gov/foia/fomc/readingrooms.htm. Return to text

11. See Williams (2013). Return to text

12. The Europeans have long been intrigued by the possibility of negative rates, beginning with Gesell's stamp scrip proposal in 1906 and some apparently successful experiments with stamp scrip in Austria in the 1930s. See Keynes (1936), Fisher (1933), and Hicks (1937). For an extensive discussion of Gesell's work, see Keynes (1936), chap. 23, pp. 353-58. Return to text

13. See Alderman (2015). Return to text

14. As an alternative to eliminating currency, a number of authors--including Goodfriend (2000), Buiter (2003), Agarwal and Kimball (2015), McAndrews (2015), and Rogoff (2014)--have discussed various mechanisms that could effectively implement a Gesell tax on physical currency. Return to text

15. See International Monetary Fund (2015) for a broad discussion of many issues in this area. Return to text

16. More information about DFAST and CCAR is available on the Board's website at www.federalreserve.gov/bankinforeg/stress-tests-capital-planning.htm. Return to text

17. See Board of Governors (2015). Return to text

18. See, for instance, Stein (2013) and Carlson and others (forthcoming) for a discussion on the possible use of monetary policy tools to foster financial stability objectives. Return to text

19. Implicit in this discussion is some degree of confidence that the central bank could identify a buildup of financial stability risks. Adrian, Covitz, and Liang (2014) offer some views on effective financial stability monitoring. Return to text

20. This variability is in part due to different model set-ups, such as how financial instability builds up and how it affects economic outcomes. For example, Woodford (2012) finds that leaning against the wind does not change the basis for traditional stabilization objectives in a standard New Keynesian model, whereas the cost-benefit analysis in Svensson (2015) finds little basis for the "leaning against the wind" strategy. Ajello and others (2015) find that optimal adjustment of the policy rate, when the possibility of a crisis is taken into account, is small unless the policymaker is assumed to be quite uncertain about the likelihood and severity of the crisis. Return to text