February 07, 2013

Overheating in Credit Markets: Origins, Measurement, and Policy Responses

Governor Jeremy C. Stein

At the "Restoring Household Financial Stability after the Great Recession: Why Household Balance Sheets Matter" research symposium sponsored by the Federal Reserve Bank of St. Louis, St. Louis, Missouri

Thank you very much. It's a pleasure to be here. The question I'd like to address today is this: What factors lead to overheating episodes in credit markets?1 In other words, why do we periodically observe credit booms, times during which lending standards appear to become lax and which tend to be followed by low returns on credit instruments relative to other asset classes?2 We have seen how such episodes can sometimes have adverse effects on the financial system and the broader economy, and the hope would be that a better understanding of the causes can be helpful both in identifying emerging problems on a timely basis and in thinking about appropriate policy responses.

Two Views of the Overheating Mechanism

I will start by sketching two views that might be invoked to explain variation in the pricing of credit risk over time: a "primitive preferences and beliefs" view and an "institutions, agency, and incentives" view. While the first view is a natural starting point, I will argue that it must be augmented with the second view if one wants to fully understand the dynamics of overheating episodes in credit markets.

According to the primitives view, changes in the pricing of credit over time reflect fluctuations in the preferences and beliefs of end investors such as households, where these beliefs may or may not be entirely rational. Perhaps credit is cheap when household risk tolerance is high--say, because of a recent run-up in wealth.3 Or maybe credit is cheap when households extrapolate current good times into the future and neglect low-probability risks.4

The primitives view is helpful for understanding some aspects of the behavior of the aggregate stock market, with the 1990s Internet bubble being one illustration. It seems clear that the sentiment of retail investors played a prominent role in inflating this bubble.5 More generally, research using survey evidence has shown that when individual investors are most optimistic about future stock market returns, the market tends to be overvalued, in the sense that statistical forecasts of equity returns are abnormally low.6 This finding is consistent with the importance of primitive investor beliefs.

By contrast, I am skeptical that one can say much about time variation in the pricing of credit--as opposed to equities--without focusing on the roles of institutions and incentives. The premise here is that since credit decisions are almost always delegated to agents inside banks, mutual funds, insurance companies, pension funds, hedge funds, and so forth, any effort to analyze the pricing of credit has to take into account not only household preferences and beliefs, but also the incentives facing the agents actually making the decisions. And these incentives are in turn shaped by the rules of the game, which include regulations, accounting standards, and a range of performance-measurement, governance, and compensation structures.

At an abstract level, one can think of the agents making credit decisions and the rulemakers who shape their incentives as involved in an ongoing evolutionary process, in which each adapts over time in response to changing conditions. At any point, the agents try to maximize their own compensation, given the rules of the game. Sometimes they discover vulnerabilities in these rules, which they then exploit in a way that is not optimal from the perspective of their own organizations or society. If the damage caused is significant enough, the rules themselves adapt, driven either by internal governance or by political and regulatory forces. Still, it is possible that at different times in this process, the rules do a better or worse job of managing the incentives of the agents.

To be more specific, a fundamental challenge in delegated investment management is that many quantitative rules are vulnerable to agents who act to boost measured returns by selling insurance against unlikely events--that is, by writing deep out-of-the-money puts. An example is that if you hire an agent to manage your equity portfolio, and compensate the agent based on performance relative to the S&P 500, the agent can beat the benchmark simply by holding the S&P 500 and stealthily writing puts against it, since this put-writing both raises the mean and lowers the measured variance of the portfolio.7 Of course, put-writing also introduces low-probability risks that may make you, as the end investor, worse off, but if your measurement system doesn't capture these risks adequately--which is often difficult to do unless one knows what to look for--then the put-writing strategy will create the appearance of outperformance.

Since credit risk by its nature involves an element of put-writing, it is always going to be challenging in an agency context, especially to the extent that the risks associated with the put‑writing can be structured to partially evade the relevant measurement scheme. Think of the AAA-rated tranche of a subprime collateralized debt obligation (CDO), where the measurement scheme is the credit risk model used by the rating agency. To the extent that this model is behind the curve and does not fully recognize the additional structural leverage and correlational complexities embedded in a second-generation securitization like the CDO, as opposed to a first-generation one, it will be particularly vulnerable to the introduction of a second-generation product.8

These agency problems may be exacerbated by competitive pressures among intermediaries and by the associated phenomenon of relative performance evaluation. A leading example here comes from the money market fund sector, where even small increases in a money fund's yield relative to its competitors can attract large inflows of new assets under management.9 And if these yield differentials reflect not managerial skill but rather additional risk-taking, then competition among funds to attract assets will only make the underlying put-writing problem worse.

But it is not all that satisfying--either intellectually or from a policy perspective--to simply list all of the ways that the delegation of credit decisions to agents inside big, complicated institutions can lead things astray. It must be the case that, on average over long periods of time, these agency problems are contained tolerably well by the rules of the game--by some combination of private governance and public policy--or else our credit markets would not be as large and as well developed as they are. A more interesting set of questions has to do with time-series dynamics: Why is it that sometimes, things get out of balance, and the existing set of rules is less successful in containing risk-taking? In other words, what does the institutions view tell us about why credit markets sometimes overheat?

Let me suggest three factors that can contribute to overheating. The first is financial innovation. While financial innovation has provided important benefits to society, the institutions perspective warns of a dark side, which is that innovation can create new ways for agents to write puts that are not captured by existing rules. For this reason, policymakers should be on alert any time there is rapid growth in a new product that is not yet fully understood. Perhaps the best explanation for the existence of second-generation securitizations like subprime CDOs is that they evolved in response to flaws in prevailing models and incentive schemes.10 Going back further, a similar story can be told about the introduction of payment-in-kind (PIK) interest features in the high-yield bonds used in the leveraged buyouts (LBOs) of the late 1980s. I don't think it was a coincidence that among the buyers of such PIK bonds were savings and loan associations, at a time when many were willing to take risks to boost their accounting incomes.

The second closely related factor on my list is changes in regulation. New regulation will tend to spur further innovation, as market participants attempt to minimize the private costs created by new rules. And it may also open up new loopholes, some of which may be exploited by variants on already existing instruments.

The third factor that can lead to overheating is a change in the economic environment that alters the risk-taking incentives of agents making credit decisions. For example, a prolonged period of low interest rates, of the sort we are experiencing today, can create incentives for agents to take on greater duration or credit risks, or to employ additional financial leverage, in an effort to "reach for yield."11 An insurance company that has offered guaranteed minimum rates of return on some of its products might find its solvency threatened by a long stretch of low rates and feel compelled to take on added risk.12 A similar logic applies to a bank whose net interest margins are under pressure because low rates erode the profitability of its deposit-taking franchise.

Moreover, these three factors may interact with one another. For example, if low interest rates increase the demand by agents to engage in below-the-radar forms of risk-taking, this demand may prompt innovations that facilitate this sort of risk-taking.

Why the Distinction Matters

To summarize the argument thus far, I have drawn a distinction between two views of risk-taking in credit markets. According to the primitives view, changes over time in effective risk appetite reflect the underlying preferences and beliefs of end investors. According to the institutions view, such changes reflect the imperfectly aligned incentives of the agents in large financial institutions who do the investing on behalf of these end investors. But why should anybody care about this distinction?

One reason is that your view of the underlying mechanism shapes how you think about measurement. Consider this question: Is the high-yield bond market currently overheated, in the sense that it might be expected to offer disappointing returns to investors? What variables might one look at to shape such a forecast? In a primitives-driven world, it would be natural to focus on credit spreads, on the premise that more risk tolerance on the part of households would lead them to bid down credit spreads; these lower spreads would then be the leading indicator of low expected returns.

On the other hand, in an institutions-driven world, where agents are trying to exploit various incentive schemes, it is less obvious that increased risk appetite is as well summarized by reduced credit spreads. Rather, agents may prefer to accept their lowered returns via various subtler nonprice terms and subordination features that allow them to maintain a higher stated yield. Again, the use of PIK bonds in LBOs is instructive. A long time ago, Steve Kaplan and I did a study of the capital structure of 1980s-era LBOs.13 What was most noteworthy about the PIK bonds in those deals was not that they had low credit spreads. Rather, it was that they were subject to an extreme degree of implicit subordination. While these bonds were not due to get cash interest for several years, they stood behind bank loans with very fast principal repayment schedules, which in many cases required the newly leveraged firm to sell a large chunk of its assets just to honor these bank loans. Simply put, much of the action--and much of the explanatory power for the eventual sorry returns on the PIK bonds--was in the nonprice terms.

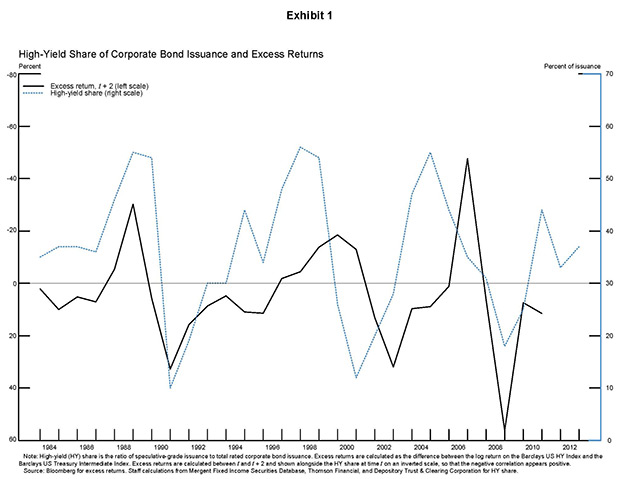

It is interesting to think about recent work by Robin Greenwood and Sam Hanson through this lens.14 They show that if one is interested in forecasting excess returns on corporate bonds (relative to Treasury securities) over the next few years, credit spreads are indeed helpful, but another powerful predictive variable is a nonprice measure: the high-yield share, defined as issuance by speculative-grade firms divided by total bond issuance. When the high-yield share is elevated, future returns on corporate credit tend to be low, holding fixed the credit spread. Exhibit 1 provides an illustration of their finding. One possible interpretation is that the high-yield share acts as a summary statistic for a variety of nonprice credit terms and structural features. That is, when agents' risk appetite goes up, they agree to fewer covenants, accept more-implicit subordination, and so forth, and high-yield issuance responds accordingly, hence its predictive power.

{kind=link}

A second implication of the institutions view is what one might call the "tip of the iceberg" caveat. Quantifying risk-taking in credit markets is difficult in real time, precisely because risks are often taken in opaque ways that escape conventional measurement practices. So we should be humble about our ability to see the whole picture, and should interpret those clues that we do see accordingly. For example, I have mentioned the junk bond market several times, but not because this market is necessarily the most important venue for the sort of risk-taking that is likely to raise systemic concerns. Rather, because it offers a relatively long history on price and nonprice terms, it is arguably a useful barometer. Thus, overheating in the junk bond market might not be a major systemic concern in and of itself, but it might indicate that similar overheating forces were at play in other parts of credit markets, out of our range of vision.

Recent Developments in Credit Markets

With these remarks as a prelude, what I'd like to do next is take you on a brief tour of recent developments in a few selected areas of credit markets. This tour draws heavily on work conducted by the Federal Reserve staff as part of our ongoing quantitative surveillance efforts, under the auspices of our Office of Financial Stability Policy and Research.

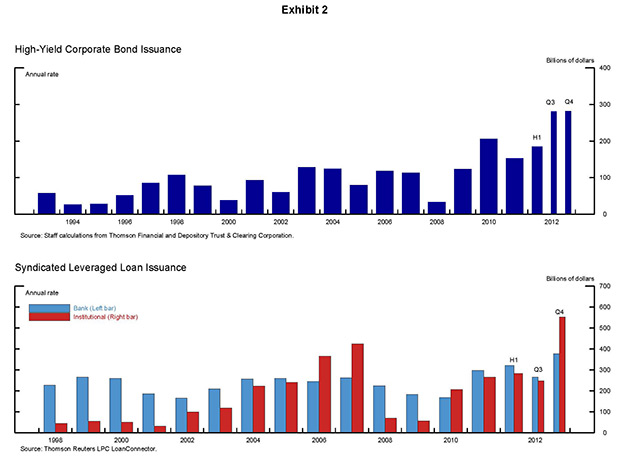

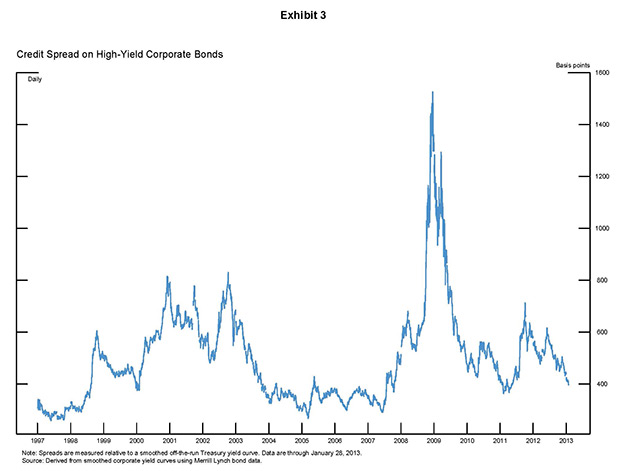

The first stop on the tour is the market for leveraged finance, encompassing both the public junk bond market and the syndicated leveraged loan market. As can be seen in exhibit 2, issuance in both of these markets has been very robust of late, with junk bond issuance setting a new record in 2012. In terms of the variables that could be informative about the extent of market overheating, the picture is mixed. On the one hand, credit spreads, though they have tightened in recent months, remain moderate by historical standards. For example, as exhibit 3 shows, the spread on nonfinancial junk bonds, currently at about 400 basis points, is just above the median of the pre-financial-crisis distribution, which would seem to imply that pricing is not particularly aggressive.15

{kind=link}

{kind=link}

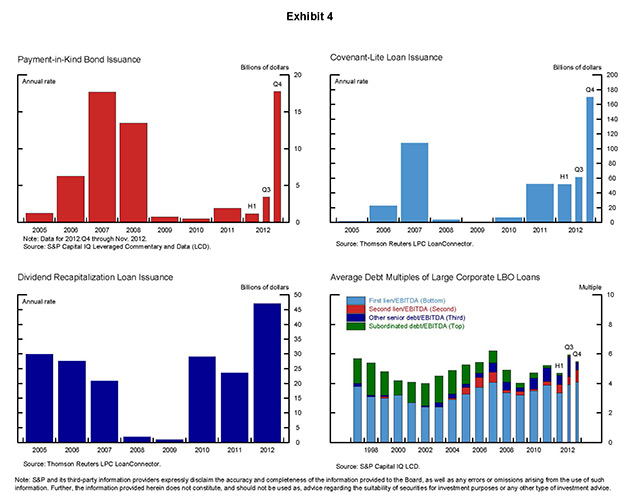

On the other hand, the high-yield share for 2012 was above its historical average, suggesting--based on the results of Greenwood and Hanson--a somewhat more pessimistic picture of prospective credit returns.16 This notion is supported by recent trends in the sorts of nonprice terms I discussed earlier (exhibit 4). The annualized rates of PIK bond issuance and of covenant-lite loan issuance in the fourth quarter of 2012 were comparable to highs from 2007. The past year also saw a new record in the use of loan proceeds for dividend recapitalizations, which represents a case in which bondholders move further to the back of the line while stockholders--often private equity firms--cash out.17 Finally, leverage in large LBOs rose noticeably, though less dramatically, in the third and fourth quarters of 2012.

{kind=link}

Putting it all together, my reading of the evidence is that we are seeing a fairly significant pattern of reaching-for-yield behavior emerging in corporate credit. However, even if this conjecture is correct, and even if it does not bode well for the expected returns to junk bond and leveraged-loan investors, it need not follow that this risk-taking has ominous systemic implications. That is, even if at some point junk bond investors suffer losses, without spillovers to other parts of the system, these losses may be confined and therefore less of a policy concern.

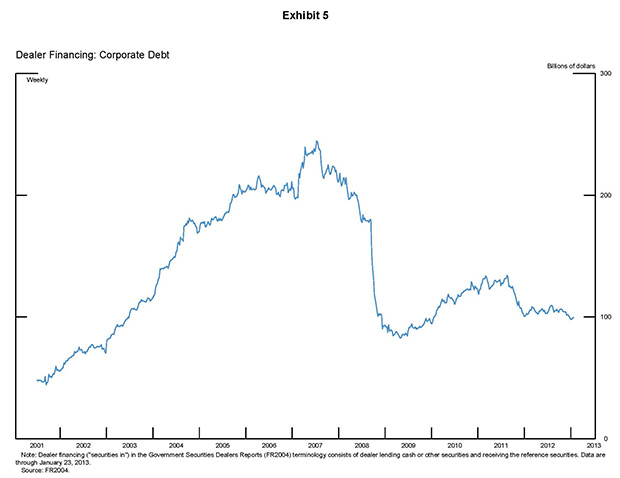

In this regard, one lesson from the crisis is that it is not just bad credit decisions that create systemic problems, but bad credit decisions combined with excessive maturity transformation. A badly underwritten subprime loan is one thing, and a badly underwritten subprime loan that serves as the collateral for asset-backed commercial paper (ABCP) held by a money market fund is something else--and more dangerous. This observation suggests an idealized measurement construct. In principle, what we'd really like to know, for any given asset class--be it subprime mortgages, junk bonds, or leveraged loans--is this: What fraction of it is ultimately financed by short-term demandable claims held by investors who are likely to pull back quickly when things start to go bad? It is this short-term financing share that creates the potential for systemic spillovers in the form of deleveraging and marketwide fire sales of illiquid assets.

This short-term financing share is difficult to measure comprehensively, but exhibit 5 presents one graph that gives some comfort. The graph shows dealer financing of corporate debt securities, much of which is done via short-term repurchase agreements (repos). This financing rose rapidly in the years prior to the crisis, then fell sharply, and remains well below its pre-crisis levels today. So, on this score, there appears to be only modest short-term leverage behind corporate credit, which would seem to imply that even if the underlying securities were aggressively priced, the potential for systemic harm resulting from deleveraging and fire sales would be relatively limited.

{kind=link}

Nevertheless, I want to urge caution here and, again, stress how hard it is to capture everything we'd like. As I said, ideally we would total all of the ways in which a given asset class is financed with short-term claims. Repos constitute one example, but there are others. And, crucially, these short-term claims need not be debt claims. If relatively illiquid junk bonds or leveraged loans are held by open-end investment vehicles such as mutual funds or by exchange-traded funds (ETFs), and if investors in these vehicles seek to withdraw at the first sign of trouble, then this demandable equity will have the same fire-sale-generating properties as short-term debt.18 One is naturally inclined to look at data on short-term debt like repo, given its prominence in the recent crisis. But precisely because it is being more closely monitored, there is the risk that next time around, the short-term claims may take another form.

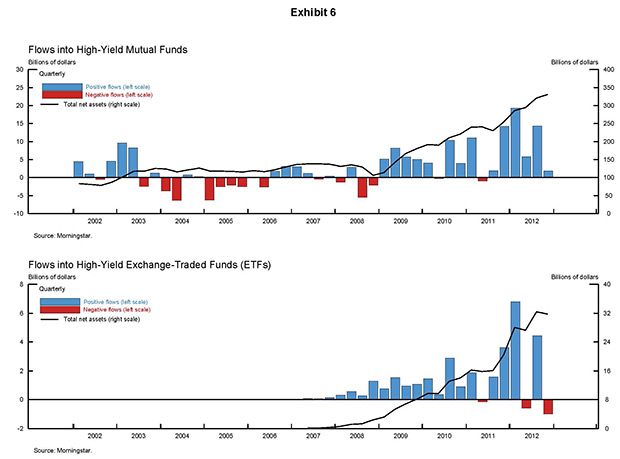

With this caveat in mind, it is worth noting the pattern of inflows into mutual funds and ETFs that hold high-yield bonds, shown in exhibit 6. Interestingly, the picture here is almost the reverse of that seen with dealer financing of corporate bonds. Assets under management in these vehicles were essentially flat in the years leading up to the crisis, but they have increased sharply in the past couple of years.19 This observation suggests, albeit only loosely, that there may be some substitutability between different forms of demandable finance. And it underscores the importance of not focusing too narrowly on any one category.

{kind=link}

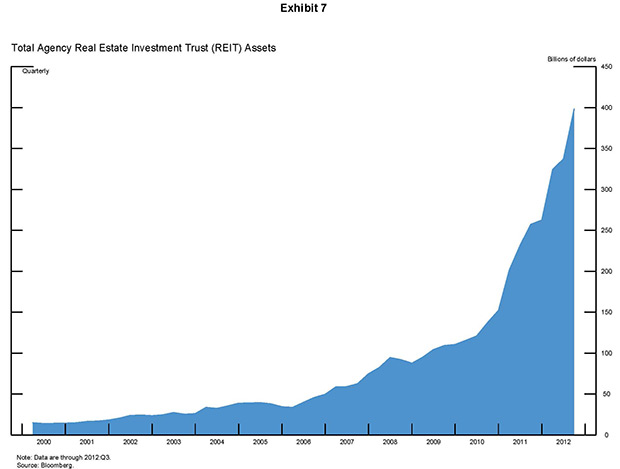

Continuing on with the theme of maturity transformation, the next brief stop on the tour is the agency mortgage real estate investment trust (REIT) sector. These agency REITs buy agency mortgage-backed securities (MBS), fund them largely in the short-term repo market in what is essentially a levered carry trade, and are required to pass through at least 90 percent of the net interest to their investors as dividends. As shown in exhibit 7, they have grown rapidly in the past few years, from $152 billion at year-end 2010 to $398 billion at the end of the third quarter of 2012.

{kind=link}

One interesting aspect of this business model is that its economic viability is sensitive to conditions in both the MBS market and the repo market. If MBS yields decline, or the repo rate rises, the ability of mortgage REITs to generate current income based on the spread between the two is correspondingly reduced.

Another place where the desire to generate yield can show up is in commercial banks' securities holdings. In recent work, Sam Hanson and I documented that the duration of banks' non-trading-account securities holdings tends to increase significantly when the short rate declines.20 We hypothesized that this pattern was due to a particular form of agency behavior--namely, that given the conventions of generally accepted accounting principles, a bank can boost its reported income by replacing low-yielding short-duration securities with higher-yielding long-duration securities.

Something along these lines seems to be happening today: The maturity of securities in banks' available-for-sale portfolios is near the upper end of its historical range. This finding is noteworthy on two counts. First, the added interest rate exposure may itself be a meaningful source of risk for the banking sector and should be monitored carefully--especially since existing capital regulation does not explicitly address interest rate risk. And, second, in the spirit of tips of icebergs, the possibility that banks may be reaching for yield in this manner suggests that the same pressure to boost income could be affecting behavior in other, less readily observable parts of their businesses.

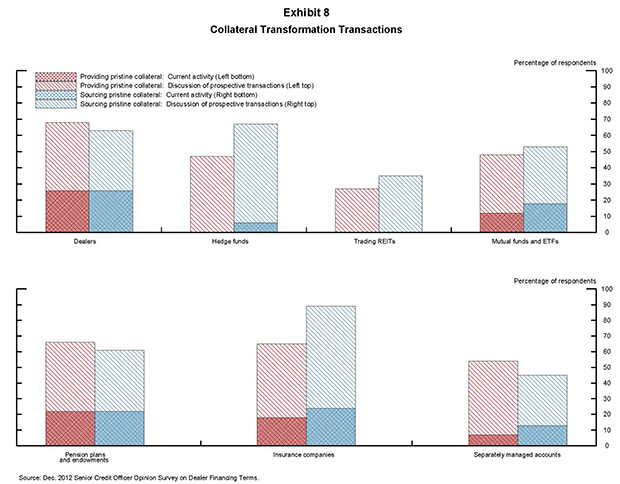

The final stop on the tour is something called collateral transformation. This activity has been around in some form for quite a while and does not currently appear to be of a scale that would raise serious concerns--though the available data on it are sketchy at this point. Nevertheless, it deserves to be highlighted because it is exactly the kind of activity where new regulation could create the potential for rapid growth and where we therefore need to be especially watchful.

Collateral transformation is best explained with an example. Imagine an insurance company that wants to engage in a derivatives transaction. To do so, it is required to post collateral with a clearinghouse, and, because the clearinghouse has high standards, the collateral must be "pristine"--that is, it has to be in the form of Treasury securities. However, the insurance company doesn't have any unencumbered Treasury securities available--all it has in unencumbered form are some junk bonds. Here is where the collateral swap comes in. The insurance company might approach a broker-dealer and engage in what is effectively a two-way repo transaction, whereby it gives the dealer its junk bonds as collateral, borrows the Treasury securities, and agrees to unwind the transaction at some point in the future. Now the insurance company can go ahead and pledge the borrowed Treasury securities as collateral for its derivatives trade.

Of course, the dealer may not have the spare Treasury securities on hand, and so, to obtain them, it may have to engage in the mirror-image transaction with a third party that does--say, a pension fund. Thus, the dealer would, in a second leg, use the junk bonds as collateral to borrow Treasury securities from the pension fund. And why would the pension fund see this transaction as beneficial? Tying back to the theme of reaching for yield, perhaps it is looking to goose its reported returns with the securities-lending income without changing the holdings it reports on its balance sheet.

There are two points worth noting about these transactions. First, they reproduce some of the same unwind risks that would exist had the clearinghouse lowered its own collateral standards in the first place. To see this point, observe that if the junk bonds fall in value, the insurance company will face a margin call on its collateral swap with the dealer. It will therefore have to scale back this swap, which in turn will force it to partially unwind its derivatives trade--just as would happen if it had posted the junk bonds directly to the clearinghouse. Second, the transaction creates additional counterparty exposures--the exposures between the insurance company and the dealer, and between the dealer and the pension fund.

As I said, we don't have evidence to suggest that the volume of such transactions is currently large. But with a variety of new regulatory and institutional initiatives on the horizon that will likely increase the demand for pristine collateral--from the Basel III Liquidity Coverage Ratio, to centralized clearing, to heightened margin requirements for noncleared swaps--there appears to be the potential for rapid growth in this area. Some evidence suggestive of this growth potential is shown in exhibit 8, which is based on responses by a range of dealer firms to the Federal Reserve's Senior Credit Officer Opinion Survey on Dealer Financing Terms.21 As can be seen, while only a modest fraction of those surveyed reported that they were currently engaged in collateral transformation transactions, a much larger share reported that they had been involved in discussions of prospective transactions with their clients.

{kind=link}

Policy Implications

Let me turn now to policy implications. The question of how policymakers should respond to different manifestations of credit market overheating is a big and difficult one, and I won't attempt to deliver a set of specific prescriptions here. However, I would like to provoke some discussion around one specific aspect of the question--namely, what are the respective roles of traditional supervisory and regulatory tools, on the one hand, versus monetary policy, on the other, in addressing the sorts of market-overheating phenomena that we have been talking about? To lend a little concreteness and urgency to this issue, imagine that it is 18 months from now, and that with interest rates still very low, each of the trends that I identified earlier has continued to build--to the point where we believe that there could be meaningful systemic implications. What, if any, policy measures should be contemplated?

It is sometimes argued that in such circumstances, policymakers should follow what might be called a decoupling approach. That is, monetary policy should restrict its attention to the dual mandate goals of price stability and maximum employment, while the full battery of supervisory and regulatory tools should be used to safeguard financial stability. There are several arguments in favor of this approach. First, monetary policy can be a blunt tool for dealing with financial stability concerns. Even if we stipulate that low interest rates are part of the reason for, say, a worrisome boom in one segment of credit markets, they are unlikely to be the whole story. So, would one really want to raise rates, and risk choking off economic activity, in an effort to rein in that one part of the market? Wouldn't it be better to use a more narrowly focused supervisory or regulatory approach, with less potential for damage to the economy?

A related concern is that monetary policy already has its hands full with the dual mandate, and that if it is also made partially responsible for financial stability, it will have more objectives than instruments at its disposal and won't do as well with any of its tasks.22 These are important points to bear in mind. In some cases, supervisory and regulatory tools are clearly better targeted and more likely to be effective than monetary policy could be. For example, the Federal Reserve's supervisory responsibilities for the banking sector put it in the right position to carefully monitor duration risk in banks' securities portfolios and to take corrective action if necessary.

Nevertheless, as we move forward, I believe it will be important to keep an open mind and avoid adhering to the decoupling philosophy too rigidly. In spite of the caveats I just described, I can imagine situations where it might make sense to enlist monetary policy tools in the pursuit of financial stability. Let me offer three observations in support of this perspective. First, despite much recent progress, supervisory and regulatory tools remain imperfect in their ability to promptly address many sorts of financial stability concerns. If the underlying economic environment creates a strong incentive for financial institutions to, say, take on more credit risk in a reach for yield, it is unlikely that regulatory tools can completely contain this behavior. This, of course, is not to say that we should not try to do our best with these tools--we absolutely should. But we should also be realistic about their limitations. These limitations arise because of the inherent fallibility of the tools in a world of regulatory arbitrage; because the scope of our regulatory authority does not extend equally to all parts of the financial system; and because risk-taking naturally tends to be structured in a nontransparent way that can make it hard to recognize. In some cases, regulatory tools may also be difficult to adjust on a timely basis--if, for example, doing so requires extended interagency negotiation.

Second, while monetary policy may not be quite the right tool for the job, it has one important advantage relative to supervision and regulation--namely that it gets in all of the cracks. The one thing that a commercial bank, a broker-dealer, an offshore hedge fund, and a special purpose ABCP vehicle have in common is that they all face the same set of market interest rates. To the extent that market rates exert an influence on risk appetite, or on the incentives to engage in maturity transformation, changes in rates may reach into corners of the market that supervision and regulation cannot.23

Third, in response to concerns about numbers of instruments, we have seen in recent years that the monetary policy toolkit consists of more than just a single instrument. We can do more than adjust the federal funds rate. By changing the composition of our asset holdings, as in our recently completed maturity extension program (MEP), we can influence not just the expected path of short rates, but also term premiums and the shape of the yield curve. Once we move away from the zero lower bound, this second instrument might continue to be helpful, not simply in providing accommodation, but also as a complement to other efforts on the financial stability front.

To see why, recall the central role that maturity transformation--the funding of long-term assets with short-term, run-prone liabilities--can play in propagating systemic instabilities. Moreover, as illustrated by the mortgage REIT sector that I described earlier, the economic appeal of maturity transformation hinges on the shape of the yield curve--in that particular case, on the spread between the yield on agency MBS and the so-called general collateral (GC) repo rate at which these securities can be funded on a short-term basis. And it would appear that our policies have at times put pressure on this spread from both sides. Our purchases of long-term Treasury securities and agency MBS have clearly helped reduce long-term yields, and a number of observers have suggested that an unintended byproduct of our MEP--and the associated sales of short-term Treasury securities--was to exert an upward influence on GC repo rates.

This sort of compression of term spreads is the twist in Operation Twist. And you can see the financial stability angle as well as a possible response to concerns over numbers of instruments. Suppose that, at some point in the future, once we are away from the zero lower bound, our dual mandate objectives call for an easing in policy. Also suppose that, at the same time, there is a general concern about excessive maturity transformation in various parts of the financial system, and that we are having a hard time reining in this activity with conventional regulatory tools. It might be that the right combination of policies would be to lower the path of the federal funds rate--thereby effectuating the needed easing--while at the same time engaging in MEP-like asset swaps to flatten the yield curve and reduce the appeal of maturity transformation.

Conclusion

I hope you will take this last example in the spirit in which it was intended--not as a currently actionable policy proposal, but as an extended hypothetical meant to give some tangible substance to a broader theme. That broader theme is as follows: One of the most difficult jobs that central banks face is in dealing with episodes of credit market overheating that pose a potential threat to financial stability. As compared with inflation or unemployment, measurement is much harder, so even recognizing the extent of the problem in real time is a major challenge. Moreover, the supervisory and regulatory tools that we have, while helpful, are far from perfect.

These observations suggest two principles. First, decisions will inevitably have to be made in an environment of significant uncertainty, and standards of evidence should be calibrated accordingly. Waiting for decisive proof of market overheating may amount to an implicit policy of inaction on this dimension. And, second, we ought to be open-minded in thinking about how to best use the full array of instruments at our disposal. Indeed, in some cases, it may be that the only way to achieve a meaningfully macroprudential approach to financial stability is by allowing for some greater overlap in the goals of monetary policy and regulation.

Thank you very much.

References

Amromin, Gene, and Steve Sharpe (2012). "From the Horse's Mouth: How do Investor Expectations of Risk and Return Vary with Economic Conditions? (PDF) ," Federal Reserve Bank of Chicago Working Paper 2012-08.

Bernanke, Ben S., and Mark Gertler (1989). "Agency Costs, Net Worth, and Business Fluctuations," American Economic Review, vol. 79 (March), pp. 14-31.

Borio, Claudio, and Mathias Drehmann (2009). "Financial Instability and Macroeconomics: Bridging the Gulf," paper prepared for the Twelfth Annual International Banking Conference, "The International Financial Crisis: Have the Rules of Finance Changed?" held at the Federal Reserve Bank of Chicago, Chicago, September 24-25.

Campbell, John Y., and John H. Cochrane (1999). "By Force of Habit: A Consumption-Based Explanation of Aggregate Stock Market Behavior," Journal of Political Economy, vol.107 (April), pp. 205-51.

Coval, Joshua, Jakub Jurek, and Erik Stafford (2009). "The Economics of Structured Finance," Journal of Economic Perspectives, vol. 23 (Winter), pp. 3-25.

DeMarzo, Peter M. (2005). "The Pooling and Tranching of Securities: A Model of Informed Intermediation," Review of Financial Studies, vol. 18 (Spring), pp. 1-35.

DeMarzo, Peter, and Darrell Duffie (1999). "A Liquidity-Based Model of Security Design," Econometrica, vol. 67 (January), pp. 65-99.

Gennaioli, Nicola, Andrei Shleifer, and Robert Vishny (2012). "Neglected Risks, Financial Innovation, and Financial Fragility," Journal of Financial Economics, vol. 104 (June), pp.452‑68.

Gorton, Gary, and George Pennacchi (1990). "Financial Intermediaries and Liquidity Creation," Journal of Finance, vol. 45 (March), pp. 49-71.

Greenwood , Robin, and Samuel G. Hanson (2012). "Issuer Quality and Corporate Bond Returns (PDF) ," unpublished paper, Harvard University, September.

Greenwood, Robin, and Andrei Shleifer (2012). "Expectations of Returns and Expected Returns (PDF) ," unpublished paper, Harvard University, October.

Griffin, John M., Jeffrey H. Harris, Tao Shu, and Selim Topaloglu (2011). "Who Drove and Burst the Tech Bubble?" Journal of Finance, vol. 66 (August), pp. 1251-90.

Hanson, Samuel G., and Jeremy C. Stein (2012). "Monetary Policy and Long-Term Real Rates," Finance and Economics Discussion Series 2012-46. Washington: Board of Governors of the Federal Reserve System, July.

Jensen, Michael C., and William H. Meckling (1976). "Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure," Journal of Financial Economics, vol. 3 (October), pp. 305-60.

Jurek, Jakub W., and Erik Stafford (2011). "The Cost of Capital for Alternative Investments (PDF) ," Working Paper Series 12-013. Cambridge, Mass.: Harvard Business School, September.

Kacperczyk, Marcin, and Philipp Schnabl (2012). "How Safe Are Money Market Funds? (PDF) " unpublished paper, New York University, June.

Kaplan, Steven, and Jeremy C. Stein (1993). "The Evolution of Buyout Pricing and Financial Structure in the 1980s," Quarterly Journal of Economics, vol. 108 (May), pp.313-57.

Merton, Robert C. (1974). "On the Pricing of Corporate Debt: The Risk Structure of Interest Rates," Journal of Finance, vol. 29 (May), pp. 449-70.

Rajan, Raghuram G. (2006). "Has Finance Made the World Riskier?" European Financial Management, vol. 12 (September), pp. 499-533.

Shleifer, Andrei, and Robert W. Vishny (1997). "The Limits of Arbitrage," Journal of Finance, vol. 52 (March), pp. 35-55.

Tinbergen, Jan (1952). Contributions to Economic Analysis, vol. 1: On the Theory of Economic Policy (Amsterdam: North-Holland).

1. The thoughts that follow are my own and do not necessarily reflect the views of my colleagues on the Board of Governors or the Federal Open Market Committee. I am grateful to Burcu Duygan-Bump, Matt Eichner, Jon Faust, Michael Kiley, Nellie Liang, Fabio Natalucci, and Bill Nelson for numerous helpful conversations and suggestions. Return to text

2. I am using the term "overheating" in an asset-pricing sense, so when I say that the market for a particular class of credit instruments is overheated, I mean that forecasted returns on this class of instruments, in excess of those on riskless Treasury bills, are abnormally low, or even negative, over some horizon. This usage contrasts with models in the genre pioneered by Bernanke and Gertler (1989), where time-variation in collateral values can lead to large changes in the supply of certain types of credit but where expected returns on credit are constant over time. Return to text

3. Habit-formation models have this property. See, for example, Campbell and Cochrane (1999). Return to text

4. See Gennaioli, Shleifer, and Vishny (2012). Return to text

5. For example, Griffin and others (2011) document that during the run-up of the Internet bubble, from January 1997 to March 2000, individual investors were substantial net buyers of tech stocks, via both direct purchases as well as investments in tech-sector-specific mutual funds. Return to text

6. See Amromin and Sharpe (2012), and Greenwood and Shleifer (2012). Return to text

7. Jurek and Stafford (2012) argue that implicit put-writing of this sort accounts for much of the apparent measured alpha in hedge funds. Return to text

8. To be clear on terminology: A subprime CDO is a securitization where the collateral is composed of the mezzanine tranches of residential mortgage-backed securities (RMBS), as opposed to a collection of the underlying mortgages. Thus, in this case, the RMBS is the first-generation securitization, and the CDO, which takes as its input a specific tranche of the RMBS, is the second-generation product. See Coval, Jurek, and Stafford (2009) for an analysis of the relative risks and modeling uncertainties of first and second-generation securitizations. Return to text

9. See Kacperczyk and Schnabl (2012). Return to text

10. To be clear, I do not intend this critique to apply to first-generation securitizations, such as RMBS, asset-backed securities collateralized by auto and credit card loans, or collateralized loan obligations (where the collateral pool is composed of bank loans). As a number of academic studies have emphasized, the basic pooling-and-tranching structure of these securitizations can help reduce adverse selection problems in markets, and thereby increase liquidity and reduce financing costs. See, for example, Gorton, and Pennacchi (1990), DeMarzo and Duffie (1999), and DeMarzo (2005). Return to text

11. See Rajan (2006) for an early exposition of the reach-for-yield phenomenon. Return to text

12. This mechanism is the classic risk-shifting effect described by Jensen and Meckling (1976).Return to text

13. See Kaplan and Stein (1993). Return to text

14. See Greenwood and Hanson (2012). Return to text

15. To be precise, the spread was at 397 basis points as of January 28, 2013, as compared to a median value of 388 basis points over the period January 1997 to July 2007, and a mean of 447 basis points over the same period. Return to text

16. See Greenwood and Hanson (2012). Return to text

17. One factor that complicates the interpretation is that, in late 2012, one might have expected an increase in dividend-recap loans even absent any change in investor risk appetite, based on the anticipation of future dividend tax increases. Return to text

18. Indeed, Shleifer and Vishny's (1997) classic treatment of fire sales is based not on a leverage mechanism, but on rapid performance-based flows out of open-end funds. Return to text

19. Some observers point to the significant increase in collateralized loan obligation (CLO) issuance in 2012 as a further symptom of "leverage" in the market. While demand for leveraged loans from CLOs may play a role in driving loan issuance, pricing and loan structure, it should be noted that CLO equity does not represent a form of demandable short-term financing and hence does not have the potential to contribute to fire-sale dynamics in the same way as, say, repo financing. Return to text

20. See Hanson and Stein (2012). Return to text

21. The Senior Credit Officer Opinion Survey on Dealer Financing Terms is available on the Federal Reserve's website. Return to text

22. This concern is sometimes related to the "Tinbergen principle" (Tinbergen (1952)), which states that if the number of policy targets exceeds the number of instruments, then some targets may not be hit. However in a world with multiple instruments, the Tinbergen principle does not imply anything about decoupling. That is, it does not imply that each instrument must be dedicated to a single target. Return to text

23. A similar argument is made by Borio and Drehmann (2009), who write: "But in sophisticated and open financial systems, in which the scope for regulatory arbitrage is high, the interest rate has the merit of setting the universal price of leverage. It reaches parts that other instruments cannot reach." Return to text