FEDS Notes

May 26, 2020

Analyzing the Community Bank Leverage Ratio

Bert Loudis, Daniel Nguyen, and Carlo Wix1

Introduction

This note analyzes the newly introduced Community Bank Leverage Ratio ("CBLR") framework. The analysis covers the framework's eligibility, its capital stringency, and its potential impact on system-wide capital levels under a hypothetical adverse scenario.

Since 2013, depository institutions and depository institution holding companies ("banks") have had to comply with four different capital requirements, including the tier 1 leverage ratio requirement ("generally applicable rule").2 In 2018, Congress passed the Economic Growth, Regulatory Relief, and Consumer Protection Act ("EGRRCPA" or "the Act"). Section 201 of the EGRRCPA directed regulatory agencies to establish the CBLR framework as a simple alternative to assess the capital adequacy of banks with less than $10 billion in total consolidated assets ("community banks"). The Act provided flexibility for regulators to define the CBLR, set the minimum CBLR requirement, and consider additional eligibility criteria such as off-balance sheet ("OBS") exposures, trading assets and liabilities, and total notional derivatives exposures.3 In 2019, the regulatory agencies published the final rule entitled "Regulatory Capital Rule: Capital Simplification for Qualifying Community Banking Organizations" that defined the CBLR framework, which replaces the four capital requirements of the generally applicable rule with a single 9 percent tier 1 leverage ratio requirement, as illustrated in Table 1.4

Table 1: Requirements under the General Applicable Rule and the CBLR Framework

| Generally Applicable Rule | CBLR Framework | ||||

|---|---|---|---|---|---|

| Ratio | CET1 Capital Ratio | Tier 1 Capital Ratio | Total Capital Ratio | Tier 1 Leverage Ratio | CBLR |

| Numerator | CET1 Capital | Tier 1 Capital | Total Capital | Tier 1 Capital | Tier 1 Capital |

| Denominator | Risk-Weighted Assets | Risk-Weighted Assets | Risk-Weighted Assets | Average Total Consolidated Assets | Average Total Consolidated Assets |

| Requirement* | 7.0% | 8.5% | 10.5% | 5.0% | 9.0% |

Source: Federal Reserve Board and FDIC

*Risk-based minimum requirements include the baseline Capital Conservation Buffer ("CCB"). The 5% tier 1 leverage ratio requirement reflects the threshold for banks to be deemed well capitalized under PCA. Bank-specific buffers, such as the Global Systemically Important Bank ("G-SIB") buffer, are not included.

Under the final rule, community banks that meet all of the following eligibility criteria would be able to opt into the CBLR framework:

- Total consolidated assets of less than $10 billion;

- A tier 1 leverage ratio exceeding 9 percent;

- Average total OBS exposures of 25 percent or less of average total consolidated assets;

- Trading assets and liabilities of 5 percent or less of average total consolidated assets;

- Not an advanced approaches institution.5

The asset threshold of $10 billion and the 5 percent limit on trading exposures were mandated by the Act. Regulators chose a 9 percent CBLR requirement to minimize the reduction in the aggregate levels of regulatory capital while maximizing the number of eligible institutions. The OBS criterion provided a backstop for assets that are used by electing banks to determine capital requirements under the generally applicable rule, but not under the CBLR framework. The CBLR uses the tier 1 leverage ratio, which is an on-balance sheet, risk-insensitive capital ratio that does not capture OBS risk. The current Generally Applicable rule requires banks to hold capital for OBS assets, while the CBLR does not. Finally, the advanced approach criterion filtered out banks that may have additional risks that are not appropriately captured by the CBLR.

Eligible banks that elect to use the CBLR framework will be considered to have satisfied all capital requirements under the generally applicable rule and to be well capitalized under the Prompt Corrective Action ("PCA") rules. 6 An electing bank would be able to opt out of the framework at any time. If an electing bank later fails to meet any of the eligibility criteria, it would have a two-quarter "grace" period to return to CBLR compliance or revert to the generally applicable rule. If an electing bank's leverage ratio falls below 9 percent, the bank would be deemed well capitalized during the grace period as long as the bank's leverage ratio remains above 8 percent. If an electing bank's leverage ratio falls to 8 percent or less, it would be required to revert immediately to the generally applicable rule.

The CBLR framework is intended to simplify regulatory capital requirements and provide material regulatory compliance burden relief to qualifying community banking organizations that opt into the community bank leverage ratio framework.7 Its goals were to provide this relief to a meaningful number of well-capitalized banks with less $10 billion in total consolidated assets, while simultaneously maintaining the safety and soundness of individual banks and the banking system as a whole.

This note analyzes the extent to which the final rule meets its intended goals. To assess whether the rule provides relief to a meaningful number of community banks, the analysis determines the number of banks that would be eligible for the CBLR framework, both currently and historically. To assess the effects on safety and soundness, the analysis assesses a potential systemic capital deterioration by comparing each bank's current capital levels to the capital that would be required under the CBLR framework. For banks in which the CBLR framework is less stringent, the analysis determines the system-wide capital release under a hypothetical adverse scenario.

Eligibility Analysis

In this section, we investigate the inclusiveness of the CBLR framework by analyzing the number of banks that are currently eligible to opt in according to the framework's eligibility criteria. We also conduct a historical analysis to assess the impact of changing financial conditions on CBLR inclusiveness. Finally, we provide a more detailed discussion of the inclusiveness of the off-balance sheet criterion.

Current Eligibility

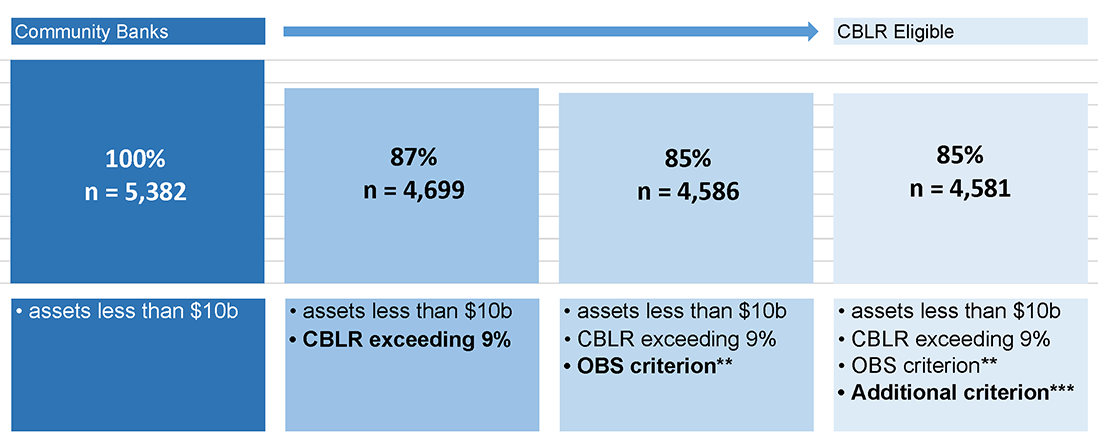

As of June 30, 2019, there were 5,312 Insured Depository Institutions ("IDIs") that filed a Consolidated Reports of Condition and Income ("Call Report") and 364 Depository Institution Holding Companies ("DI HCs") that filed a Consolidated Financial Statements for Holding Companies ("FR Y-9C"). 8 Of these filers, 5,154 IDIs and 228 DI HCs report assets of less than $10 billion and thus would be considered community banks.9

We find that the CBLR framework is inclusive of a large majority of community banks. As of the second quarter of 2019, 4,581 of 5,382 (85 percent) community banks are eligible to opt into the CBLR framework. 10 Specifically, 4,403 of 5,154 (85 percent) of community IDIs and 178 of 228 (78 percent) of community DI HCs would be eligible. Figure 1 provides a waterfall of the number of eligible community banks, as each eligibility criterion is added.11 Following the figure, 4,699 (87 percent of) community banks meet the leverage ratio requirements, 4,586 (85 percent of) community banks also meet the off balance sheet criteria, and 4,581 (85 percent of) community banks also meet the non-advanced approaches and trading exposure criterion. The majority of banks are well below $10 billion in size; 85 percent of CBLR eligible banks have total assets of less than $1 billion.

Sources: Q2 2019 FR Y-9C, FFIEC Call Reports, NBER, and author's analysis

*This sample includes depository institution holding companies (FR Y-9C) and depository institutions (Call Report).

**Off balance sheet exposure less than 25 percent of total consolidated assets.

***Trading assets plus trading liabilities less than 5 percent of total consolidated assets and not a subsidiary or affiliate of an advanced approaches bank.

Historical Eligibility

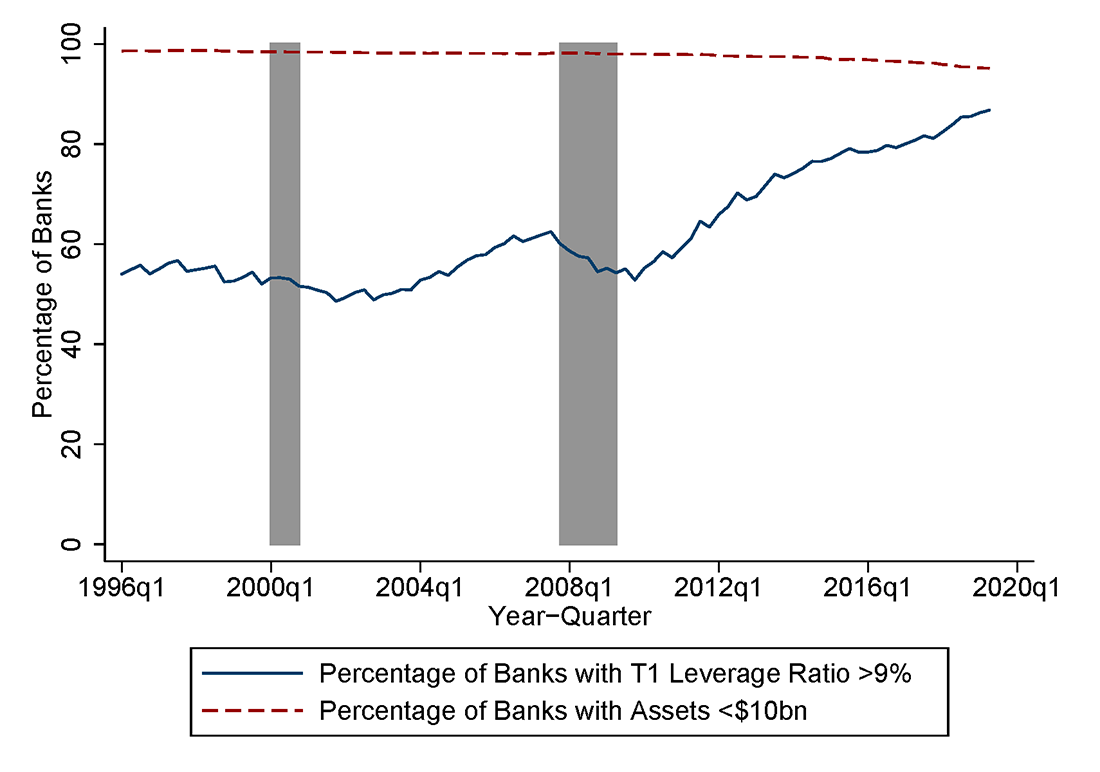

The high level of inclusiveness as of the second quarter of 2019 is driven by the current high capitalization of banks by historical standards. Figure 2 illustrates the historical trend in the hypothetical percentage of banks which would have been eligible for the CBLR framework based on the capitalization threshold (T1 leverage ratio exceeding 9 percent) and the size threshold (total consolidated assets of less than $10 billion) since the first quarter of 1996.12

The solid blue line in Figure 2 illustrates the increase in CBLR eligibility over time due to changes in banks' capitalization levels. While only 50 percent to 60 percent of banks had T1 leverage ratios of more than 9 percent in the period from 1996 to 2010, this fraction has steadily increased over recent years to its current high level of 87 percent. The recent upwards trend can be attributed to the increase in banks' capital levels since the end of the global financial crisis. Thus, the newly introduced CBLR framework could help to preserve these current high capitalization levels of eligible banks opting into the framework, thereby maintaining the current standard of safety and soundness for these institutions.

Sources: FFIEC Call Reports, FR Y-9C, NBER, and authors' analysis

*The gray shaded areas indicate NBER recession periods. There were changes in the sample of banks due to filing requirement adjustments in Q1 2006, Q1 2015, and Q3 2018, which do not materially affect our analysis.

The size threshold of the CBLR framework is set by the Economic Growth, Regulatory Relief, and Consumer Protection Act at $10 billion. Nominal inflation of banks' asset values could reduce the number of eligible banks in the future.13 The dashed red line in Figure 2 shows that size eligibility tapers off modestly over time. While the fraction of banks with total consolidated assets of less than $10 billion was 99 percent in 1996, this fraction stands at 95 percent as of the second quarter of 2019. This is a difference of only 4 percentage points over a period of 23 years. Projecting this trend forwards, the effect of asset value inflation on eligibility should remain modest in the near future.

The Off-Balance Sheet Criterion

Due to historical changes in reporting practices, we do not conduct historical eligibility analyses with regard to the off-balance sheet or the trading assets and liabilities criteria. However, we find that, since 2015, the number of firms that exceed the upper bound of the off-balance sheet criterion is relatively stable over time, at around 130 institutions at any given time. This sample of excluded institutions, however, fluctuates over time, as 409 distinct entities would have been excluded by the off-balance sheet criterion at some point since 2015. The grace period provided by the final CBLR rule helps alleviate these fluctuations, as it gives banks time to return to CBLR compliance before reverting back to the generally applicable rule. In contrast to the off balance sheet criterion, the trading assets and liabilities criterion would not have excluded any more than three institutions during any quarter since 2015.

Firms excluded by the OBS exposure threshold typically have off-balance sheet exposures – such as loan commitments, securitizations, and repo-style transactions – that far exceed those of their peers. In addition to its function as an inclusionary factor for the CBLR framework, the OBS criterion also acts as a backstop for assets that are not reported by electing banks. This backstop ensures that firms do not acquire material amounts of OBS assets without having to capitalize them. The OBS criterion is a necessary feature of the CBLR framework because the CBLR uses the tier 1 leverage ratio, which is an on-balance sheet, risk-insensitive capital ratio that does not capture OBS risk.

Stringency Analysis

In this section, we analyze the stringency of the 9 percent CBLR framework relative to the generally applicable rule. In discussing this analysis, we note that the CBLR framework is optional and only available for banks already holding capital in excess of minimum requirements, and thus the CBLR framework does not constitute a mandatory increase in capital requirements for any bank. The analysis defines stringency in terms of an excess capital methodology. Excess capital levels for each respective capital definition are calculated by subtracting a bank's required capital from the bank's actual capital holdings. The resulting dollar amount represents the capital a bank holds in excess of its minimum required capital. For each bank, the requirement that yields the least amount of excess capital is considered the most stringent. Table 2 provides an example calculation of stringency for a hypothetical bank with average assets of $120 million, risk-weighted assets of $100 million, and total capital holdings of $16 million. In this example, the hypothetical IDI has $5.5 million of capital in excess of its most stringent requirement under the generally applicable rule.

Table 2: Stringency calculation for hypothetical bank (in $ millions)

| Capital Definition | Leverage Ratio | Risk-Based Capital Ratios | ||

|---|---|---|---|---|

| Tier 1 | CET1 | Tier 1 | Total | |

| Actual Capital Holdings | 15 | 14 | 15 | 16 |

| Required Capital* | 6 | 7 | 8.5 | 10.5 |

| Excess Capital | 9 | 7 | 6.5 | 5.5 |

Note: Assuming average assets of $120 million and risk-weighted assets of $100 million.

Current Stringency

We perform the stringency calculation summarized in Table 2 for all community banks in our sample. Table 3 summarizes the most stringent capital requirement for each community bank. Under the generally applicable rule, the total risk-based capital ratio is the most stringent requirement for the vast majority of community banks. As of the second quarter of 2019, 85 percent of community banks have the lowest amount of excess capital over the 10.5 percent total capital requirement. The current leverage ratio requirement (5 percent to be well capitalized) is the most stringent capital requirement for only 13 percent of community banks.

Table 3: Regulatory Requirement Stringency (percent and number of institutions*)

| Leverage Ratio | Risk-Based Capital Ratios | |||

|---|---|---|---|---|

| Tier 1 | CET1 | Tier 1 | Total | |

| Generally Applicable Rules | 13% | 0.70% | 0.90% | 85% |

| (n = 5,382) | -722 | -40 | -50 | -4,570 |

Sources: Q2 2019 FR Y-9C, FFIEC Call Reports, and authors' analysis

*This sample includes both depository institutions and depository institution holding companies. It does not include holding companies subject to the small parent exemption (12 CFR Part 225 Appendix C).

Notes: Stringency is defined using the excess capital methodology described earlier in this section. The leverage ratio minimum is set to 5 percent to reflect the well-capitalized level. CET1, Tier 1, and Total minimums are 7, 8.5, and 10.5 percent, respectively. The capital conservation buffer is treated as part of the minimum for the purposes of this analysis. For example, the CET1 7 percent minimum represents a 4.5 percent requirement plus 2.5 percent capital conservation buffer.

Under the CBLR framework, the leverage ratio requirement nearly doubles from the 5 percent under the generally applicable rule (and PCA) to 9 percent. At 9 percent, the leverage ratio would become the most stringent capital requirement for 97 percent of CBLR-eligible community banks – a substantial increase from 13 percent under the generally applicable rule. Thus, a vast majority of community banks that opt into the CBLR will experience a decrease in their levels of excess capital as measured by their capital stringencies. Conversely, only 3 percent of CBLR-eligible community banks would be entering into a less stringent capital regime by opting in to the CBLR framework.

Historical Stringency

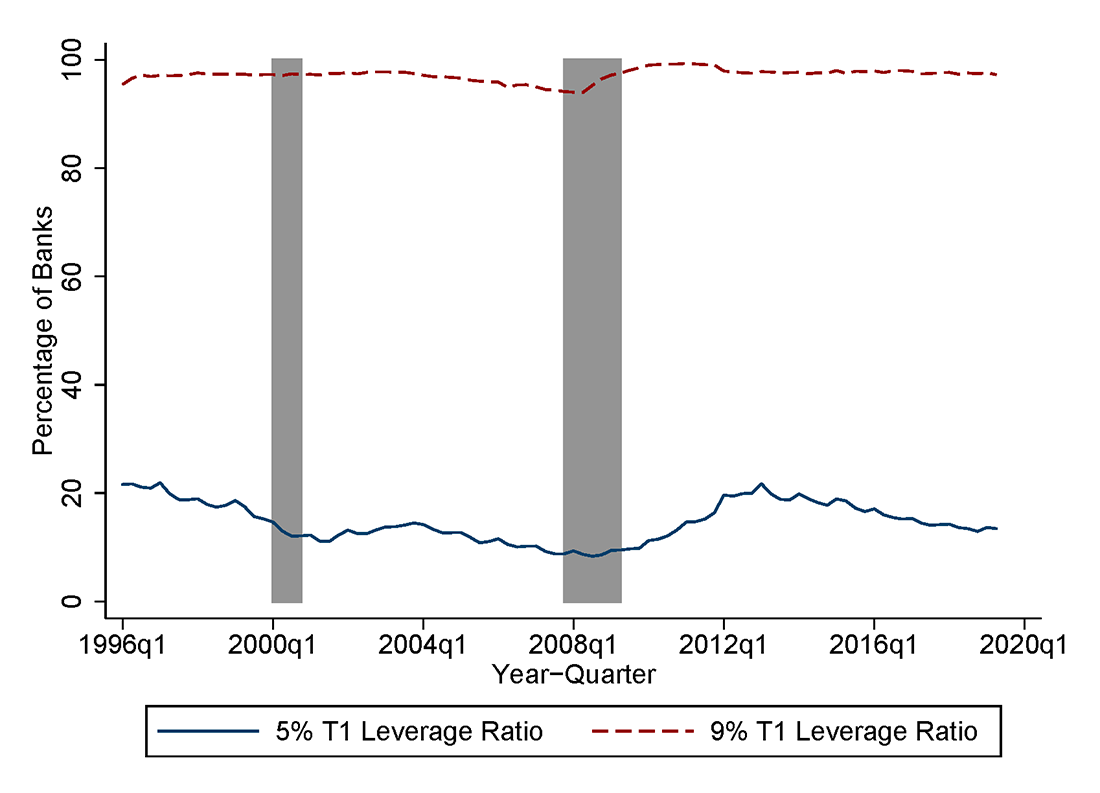

Analogous to the historical eligibility analysis, we also study the stringency of the CBLR framework over time. We analyze the stringency of the CBLR over time by investigating how stringent a hypothetical 9 percent Tier 1 leverage ratio requirement would have been historically in each quarter since the first quarter of 1996. Using the same excess capital methodology, we calculate the fraction of banks for which the 5 percent T1 leverage ratio (under the generally applicable rule) and the 9 percent T1 leverage ratio requirement (under the CBLR framework) would have been the most stringent requirement relative to a 8.5 percent T1 capital ratio and a 10.5 percent total capital ratio requirement.14

Figure 3 illustrates that a 5 percent T1 leverage ratio requirement would have been historically most stringent for only 22 percent or less of all banks. On the other hand, a 9 percent T1 leverage ratio requirement would have been most stringent for 94 percent or more of all banks. Therefore, the high stringency of the CBLR is stable over time. The high level of stringency of the 9 percent leverage ratio provides evidence that the potential for capital release of this framework is minimal.

Sources: FFIEC 031 Call Reports, FR Y-9C, NBER, and authors' analysis

*The gray shaded areas indicate NBER recession periods. There were changes in the sample of banks due to filing requirement adjustments in Q1 2006, Q1 2015, and Q3 2018, which do not materially affect our analysis.

Hypothetical Negative Scenarios

This section is meant to provide hypothetical adverse scenarios that could potentially pose a threat to the safety and soundness of the banking system. The first scenario examines the effect of community banks acquiring the maximum allowable amount of off balance sheet assets while still maintaining CBLR eligibility. The second scenario assumes that community banks that face less stringent capital requirements under the CBLR will decrease the amount of capital they hold such that they maintain their levels of excess capital. We find that even if these severe and unlikely events unfold, the results would not materially threaten the safety and soundness of the banking system as a whole.

Acquisition of Risky Off Balance Sheet Assets

In this subsection, we calculate the extent to which the OBS backstop would permit an electing bank to acquire OBS assets while maintaining CBLR framework eligibility. A well-functioning OBS threshold should not allow material amounts of capital deterioration. To test this, we conduct a forward looking hypothetical case study. In this case study, a typical CBLR eligible bank, referred to as "Example Bank", accumulates the maximum amount of OBS assets permitted by the 25 percent OBS criterion. Prior to its accumulation of OBS assets, Example Bank's financials are equal to the mean of corresponding line items of CBLR eligible banks (including a 15.6 percent total risk-based capital ratio). The analysis then examines the impact of these new assets on Example Bank's total risk-based capital ratio. The total capital ratio is used in this analysis because it is generally the most stringent capital requirement for community banks under the generally applicable rule. This is a hypothetical calculation, as banks that elect to use the CBLR framework will not be required to calculate or report risk-based ratios.

Example Bank's accumulation of OBS assets affects its total risk-based capital ratio by changing its value of risk-weighted assets ("RWA"). In the calculation of RWA, notional OBS amounts are multiplied by a credit conversion factor ("CCF") and risk weight. The CCF is intended to reflect loan equivalent appropriate exposure values, while RWA is intended to reflect risk according to the obligor.

As RWA constitute the denominator of the total risk-based capital ratio, higher RWA values result in lower total risk-based capital ratios. Thus, higher OBS assets, especially those with higher CCF and/or risk weights, will drive up the calculated RWA and lower the resulting total risk-based capital ratio. As a result, the hypothetical change in Example Bank's capital ratio depends on the risk characteristics of Example Bank's accumulated OBS assets.

Three hypothetical scenarios are used for this analysis: high risk, average risk, and low risk. In each scenario, Example Bank is assumed to acquire OBS assets with CCFs and risk weights that, on average, are equal to the CCF and risk weight of one of three representative assets. Table 4 shows the FR Y-9C line item of the representative asset, with CCF and risk weight, in each of these scenarios. For example, if Example Bank acquires high risk OBS items that have CCFs and risk-weights that are similar to high-risk financial standby letters of credit, then their total risk-based capital ratio will deteriorate by 290 basis points. On the other hand, if Example Bank acquires low risk OBS items with CCF and risk-weights resembling Unused commitments with maturity one year or less, its total risk-based capital ratio would decline by only 40 basis points.15

Table 4: Off-Balance Sheet Criterion Case Study Scenarios (percent)

| Scenario | Line Item | CCF | Risk-Weight | Decline in Total Risk-Based Capital Ratio (basis points) |

|---|---|---|---|---|

| Average Risk Scenario | Typical financial standby letters of credit | 100 | 100 | 210 |

| Low Risk Scenario | Unused commitments with maturity one year or less | 20 | 100 | 40 |

| High Risk Scenario | High-risk financial standby letters of credit | 100 | 150 | 290 |

Sources: FR Y-9C and authors' analysis

The analysis addresses the concern that a bank could be well capitalized under the CBLR framework while it would be less than well capitalized if it were subject to risk-based capital requirements. The analysis shows this will generally not be the case. Depending on the hypothetical scenario, Example Bank's total risk-based capital ratio would decline by 40-290 basis points. As a result, its total risk-based capital ratio would decline from 15.6 percent to 15.2, 13.5, or 12.7 percent in the low, average, and high risk scenarios, respectively. Even in the high risk scenario, Example Bank remains above the minimum requirement of 10.5 percent under the generally applicable rule. To put another way, the 25 percent OBS limit does not permit Example Bank to accumulate enough high-risk OBS assets to cause its capital holdings to fall below the minimum requirements under the generally applicable rule. As such, the OBS criteria serves as an effective backstop to the CBLR regime.

Potential Deterioration of System-wide Capital Levels

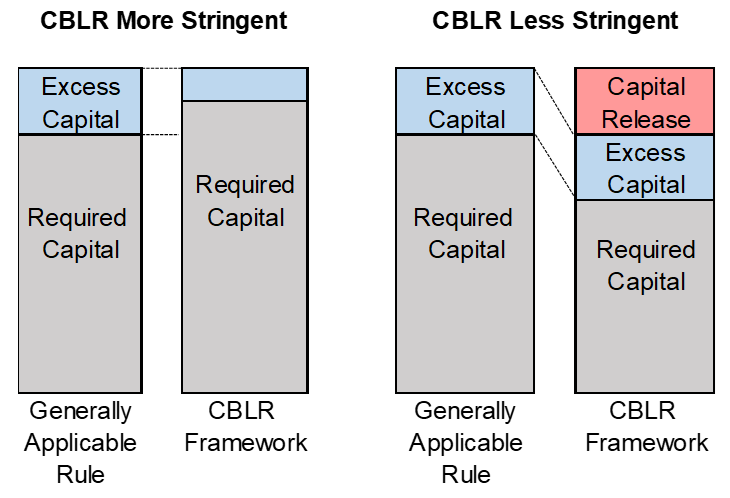

This subsection provides a conservative assessment of the impact of the CBLR framework on system-wide capital levels under a hypothetical adverse scenario. The analysis assumes that eligible banks that face less stringent capital requirements under the CBLR framework will lower their capital levels to match their levels of excess capital under the generally applicable rule. On the other hand, eligible banks that face more stringent capital requirements under the CBLR framework are assumed to hold their capital levels constant, accepting a reduction in their excess capital buffers.16 Thus, by assumption, banks only reduce but never increase their capital levels in response to the adoption of the CBLR framework. These assumptions are therefore conservative with regard to a potential deterioration of system-wide capital levels, in the sense that they would overstate the potential reductions in actual capital holdings. Yet, as the analysis below shows, this conservative assessment of the capital release is immaterial relative to the aggregate amount of capital in the system.

Figure 4 illustrates the excess capital methodology and the assumptions used in this analysis to assess the capital impact of the CBLR framework. The two left bars in Figure 4 illustrate the response of banks for which requirements are more stringent under the CBLR framework than under the generally applicable rule. An increase in stringency implies a higher level of minimum required capital, as indicated by the grey bars. As overall capital holdings are assumed to be constant for these banks, this implies a reduction in excess capital, as indicated by the blue bars. The two bars on the right illustrate the response of banks for which requirements are less stringent under the CBLR framework. Conversely, a reduction in stringency implies lower levels of minimum required capital, as indicated by the grey bars. In this scenario, banks are assumed to reduce their capital holdings to match their levels of excess capital under the generally applicable rule. This reduction in capital holdings leads to a capital release, represented by the red bar.

As discussed in the stringency section above and shown in Table 5 below, 97 percent of eligible banks would face a more stringent minimum capital requirement if they opted in to the CBLR framework. As of the second quarter of 2019, these banks hold $266 billion of tier 1 capital and $2.3 trillion of total consolidated assets. Thus, in aggregate, these banks currently have a tier 1 leverage ratio equal to 11.41 percent, or 241 basis points higher than the requirement set by the final rule, as is illustrated on the left hand side of Figure 4. As some of these banks might also raise their capital levels to maintain the size of their current excess capital buffer, the assumptions in this analysis would likely overstate the potential reductions in capital holdings.

Table 5: Assessment of the Impact on System-Wide Capital Levels

| CBLR More Stringent (97% of eligible community banks) |

CBLR Less Stringent (3% of eligible community banks) |

|||

|---|---|---|---|---|

| T1 Capital Holdings | Generally Applicable Rule | CBLR Framework | Generally Applicable Rule | CBLR Framework |

| Excess T1 Capital | $98.7 | $56.2 | $4.8 | $4.8 |

| + Required T1 Capital | $167.7 | $210.2 | $12.2 | $11.2 |

| = T1 Capital | $266.4 | $266.4 | $17.0 | $16.0 |

| Capital Release under CBLR: | $0.0 | $1.0 | ||

The right hand side of Table 5 shows results for the 3 percent of eligible banks that face less stringent capital requirements under the CBLR framework. As of the second quarter of 2019, these banks hold $17 billion of tier 1 capital and $124 billion of total consolidated assets. Assuming that all of these banks would reduce their capital holdings to match their current levels excess capital, as illustrated by the right hand side of Figure 4, there would be an aggregate system-wide capital release of $1 billion.

The $1.0 billion capital release is approximately 0.3 percent of the $283 billion in aggregate capital held by all eligible banks. Even this conservative assessment of aggregate capital release implies a negligible impact on the safety and soundness of the banking system.

Conclusion

The CBLR framework established an optional capital framework that would exempt qualifying banks from risk-based capital requirements. This note finds that over 85 percent of community banks would be eligible to opt into the CBLR framework. For 97 percent of eligible community banks, the CBLR framework would result in a more stringent minimum capital ratio than the existing generally applicable risk-based capital requirements. Under the assumption that the remaining 3 percent will lower their capital ratios to maintain their current levels of excess capital, this study assesses an aggregate capital release of approximately $1 billion. This amount is approximately 0.3 percent of the $283 billion in aggregate capital held by all eligible banks.

Additionally, the study finds that the off balance sheet criterion provides an effective backstop to the CBLR, which prevents CBLR banks from acquiring material amounts of potentially risky off balance sheet assets. Thus, this study concludes that the CBLR framework will provide burden relief to a meaningful number of community banks without undermining the safety and soundness of the financial system.

1. Bert Loudis and Carlo Wix, Federal Reserve Board of Governors, Division of Supervision & Regulation. Daniel Nguyen, Federal Deposit Insurance Corporation, Division of Insurance and Research. We thank Chris Finger, George French, Ryan Singer, Andrew Willis, and Missaka Warusawitharana for helpful comments. Return to text

2. Generally applicable requirements are described in 12 CFR 3, 12 CFR 217, and 12 CFR 324. Return to text

3. See EGRRCPA Section 201(a)(3)(B). Return to text

4. See 84 FR 61776. Return to text

5. An advanced approaches institution is generally defined as a banking organization with at least $250 billion in total consolidated assets or at least $10 billion in total on-balance sheet foreign exposure, and depository institution subsidiaries of those firms. Proposed rulemakings to tailor capital and liquidity requirements applicable to large banking organizations may result in changes to the definition of advanced approaches institution. See 83 FR 66024 (December 21, 2018) and 84 FR 24296 (May 24, 2019). Return to text

6. PCA requirements are described in 12 CFR 208.43 and 12 CFR 324.403. Return to text

7. 64 FR 61776 at 61777. Return to text

8. This analysis considers only those DI HCs that have filed an FR Y-9C for the three months ending on June 30, 2019, which generally comprises those DI HCs with at least $3 billion in assets. DI HCs with less than $3 billion in assets are generally not subject to the minimum capital requirements and thus would not be affected by the CBLR rule. (see 12 CFR 217 and 225 Appendix C as amended by 83 FR 44195) Return to text

9. For the purpose of this analysis, we use data as of June 30, 2019 data to estimate eligibility. Return to text

10. Although some community IDIs in the data are wholly owned by community DI HCs in the data, the counts of eligible IDIs and DI HCs are additive in this section because either, or both, of these legal entities can opt in to the framework. Top tier holding companies that do not use the small parent exemption (12 CFR Part 225 Appendix C) are included in this analysis. Return to text

11. The criteria are added sequentially for exposition. The framework will consider all eligibility criteria simultaneously. Return to text

12. Due to historical data availability limits, additional CBLR qualification criteria beyond asset size and capital levels are not included in this analysis. Return to text

13. In addition, the number of eligible banks could be affected by changes in the lower size threshold for FR Y-9C filing requirements, which has occurred several times in the past. See historical FR Y-9C filing requirements at https://www.federalreserve.gov/apps/reportforms/reportdetail.aspx?sOoYJ+5BzDal8cbqnRxZRg==. Return to text

14. Due to data availability constraints, we do not take into account the 7 percent CET1 capital ratio requirement in the historical stringency analysis. However, as indicated in Table 3, the CET1 Capital Ratio requirement is likely the most stringent requirement only for a negligible number of banks. We therefore do not believe that our historical analysis is materially affected by not taking into account the 7 percent CET1 Capital Ratio requirement. Return to text

15. Note that this is a partial equilibrium model, as potential management adjustments that may accompany the OBS criterion are not accounted for. Return to text

16. If these bank's capital levels fall below the CBLR minimums, they would revert to the minimums under the generally applicable rule. Thus, we assume these banks' behaviors are constrained by the generally applicable rule minimums, rather than the CBLR framework minimums. Return to text

Loudis, Bert, Daniel Nguyen, and Carlo Wix (2020). "Analyzing the Community Bank Leverage Ratio," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, May 26, 2020, https://doi.org/10.17016/2380-7172.2516.

Disclaimer: FEDS Notes are articles in which Board staff offer their own views and present analysis on a range of topics in economics and finance. These articles are shorter and less technically oriented than FEDS Working Papers and IFDP papers.