FEDS Notes

June 23, 2021

Are Rising U.S. Interest Rates Destabilizing for Emerging Market Economies?

Jasper Hoek, Emre Yoldas, and Steve Kamin1

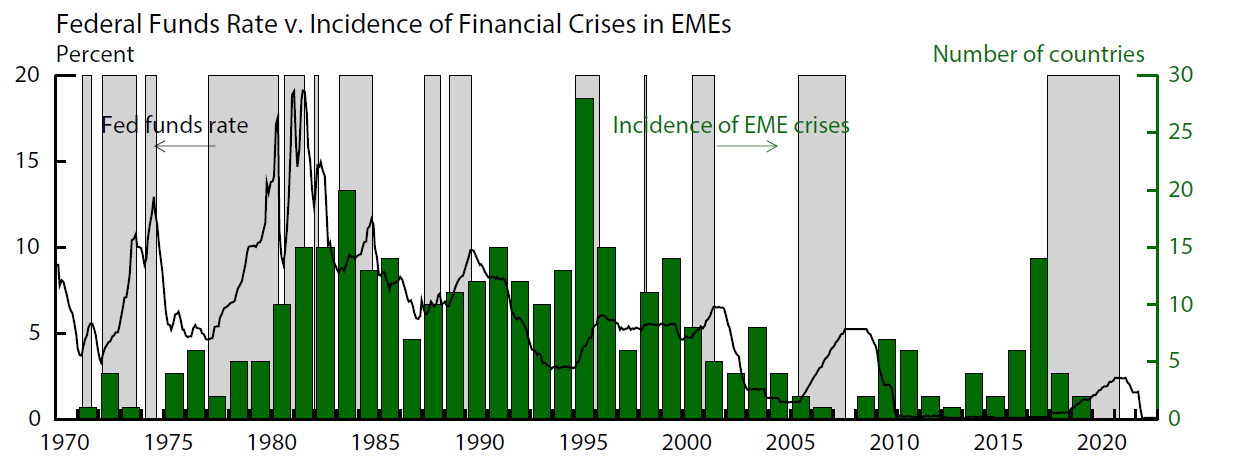

Rising U.S. interest rates are often thought to be bad news for emerging market economies (EMEs) as they increase debt burdens, trigger capital outflows, and generally cause a tightening of financial conditions that can lead to financial crises. Indeed, as shown in Figure 1 below, the rise in the federal funds rate (the black line) during the Volcker disinflation of the early 1980s was associated with a sharp rise in the incidence of financial crises in EMEs (the green bars). However, on other occasions, such as in the mid-2000s, EMEs weathered rising U.S. rates with few difficulties.

Note: Fed funds rate data are from Haver. Crisis data are from Laeven and Valencia (2018) and run through 2017. Gray areas are times when the FFR is increasing.

What accounts for differences in the so-called "spillovers" of U.S. monetary policy to emerging markets? Our recent research shows that financial spillovers to EMEs of U.S. monetary policy depend on two key factors.2 The first of these is the reason for the change in U.S. interest rates. A rise in interest rates driven by favorable growth prospects is likely to have relatively benign effects on emerging financial markets, since the benefits of higher U.S. GDP through increased import demand from its trading partners and increased investor confidence should mute the costs of higher rates. Conversely, if higher rates are driven mainly by worries about inflation or a hawkish turn in Fed policy, which we jointly describe as monetary news, this will likely be more disruptive for emerging markets. The second key factor influencing the spillovers from U.S. monetary policy is the domestic conditions in the EMEs themselves; financial conditions in economies with higher macroeconomic vulnerabilities tend to be more sensitive to a given rise in U.S. interest rates.

Our findings help to explain why the rise in U.S. Treasury yields in recent months has had fairly muted effects on financial conditions in EMEs. Despite some uptick in response to recent inflation readings, much of that rise likely owes to mounting expectations of a swift economic recovery in the United States, which should redound to the benefit of the global economy more generally. In addition, despite a notable rise in EME debt in recent years, which was accelerated by the pandemic, macroeconomic vulnerabilities are still generally lower than in the tumultuous years of the 1980s and 1990s: macroeconomic policies are more prudent, currencies are generally freer to respond to shocks, and financial sectors are more resilient.

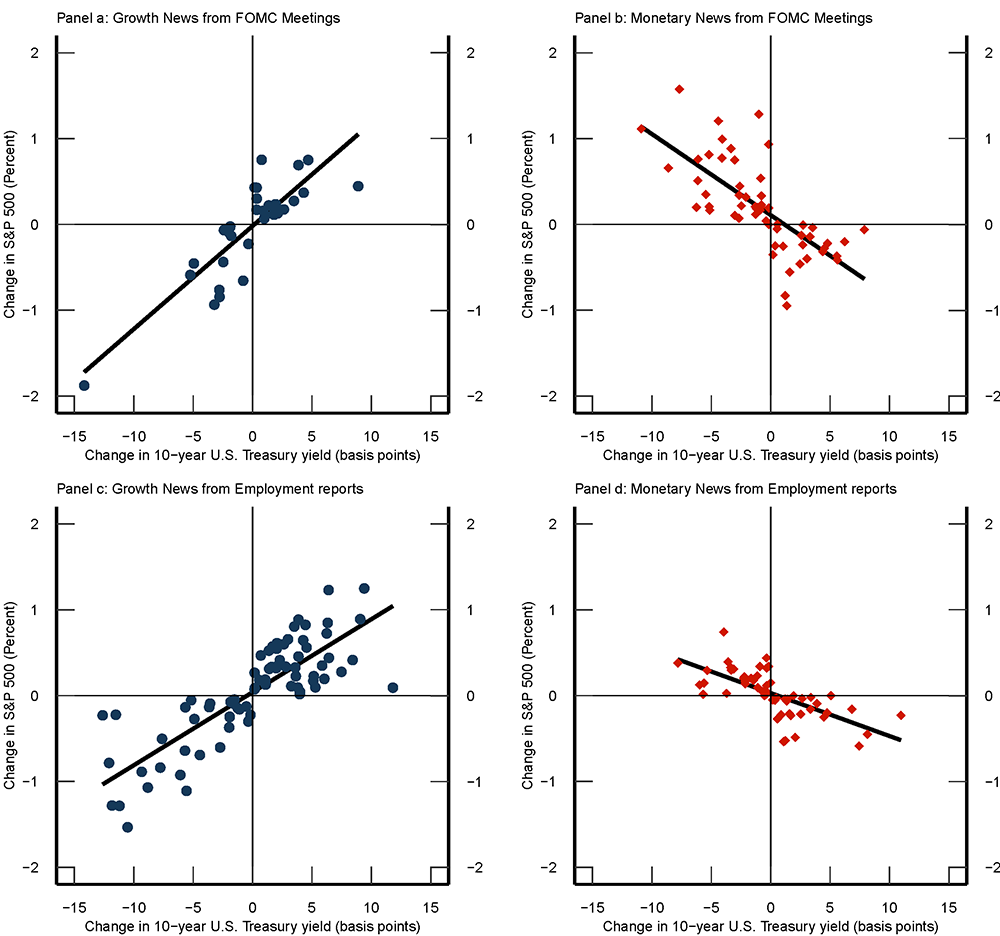

In the remainder of this note, we will summarize the analysis underlying the findings described above and present new evidence on the effects of higher longer-term U.S. Treasury yields on EME financial conditions. We start by looking at changes in the 10-year U.S. Treasury yield in a one-hour window around two different types of events—meetings of the Federal Open Market Committee (FOMC) and U.S. employment reports.3 We then classify FOMC meetings and employment reports according to whether they primarily conveyed growth news (i.e., information about future growth prospects) or monetary news (i.e., information about future inflation or the Fed's reaction function). To do this, we examine the simultaneous movement in the S&P 500 equity index. Thus, FOMC announcements and payroll releases are categorized as conveying primarily growth news if the 10-year U.S. Treasury yield and the S&P 500 index move in the same direction. For example, an FOMC communication that increased investor confidence about U.S. growth might cause both U.S. Treasury yields and stock prices to rise.4 By the same token, a very weak employment situation report that indicated poor prospects for growth and profits might be associated with declines in both yields and stock prices. The scatterplots with the blue dots in Figure 2 show the combination of changes in the 10-year yield and the S&P 500 index for all FOMC meetings and employment reports since 2010 that we classify as conveying primarily growth news. These account for about a third and half of all observations for FOMC meetings and employment reports, respectively.

In contrast, we classify FOMC meetings and employment reports as conveying primarily monetary news if the 10-year Treasury yield and the S&P 500 index move in opposite directions after the meeting. For example, an FOMC announcement referencing rising inflationary pressure, or interpreted as reflecting a more hawkish policy stance, might cause yields to rise and the S&P index to fall as higher real discount rates weigh on stock valuations. Or, an employment report might lead to lower yields but higher stock prices as investors may view it as just weak enough to avert a future Fed tightening. The scatterplots in Figure 2 with the red diamonds show the observations that we classify as conveying primarily monetary news.

Note: S&P 500 futures are used in case of employment reports. Source: Bloomberg; FRBNY New Price Quote System.

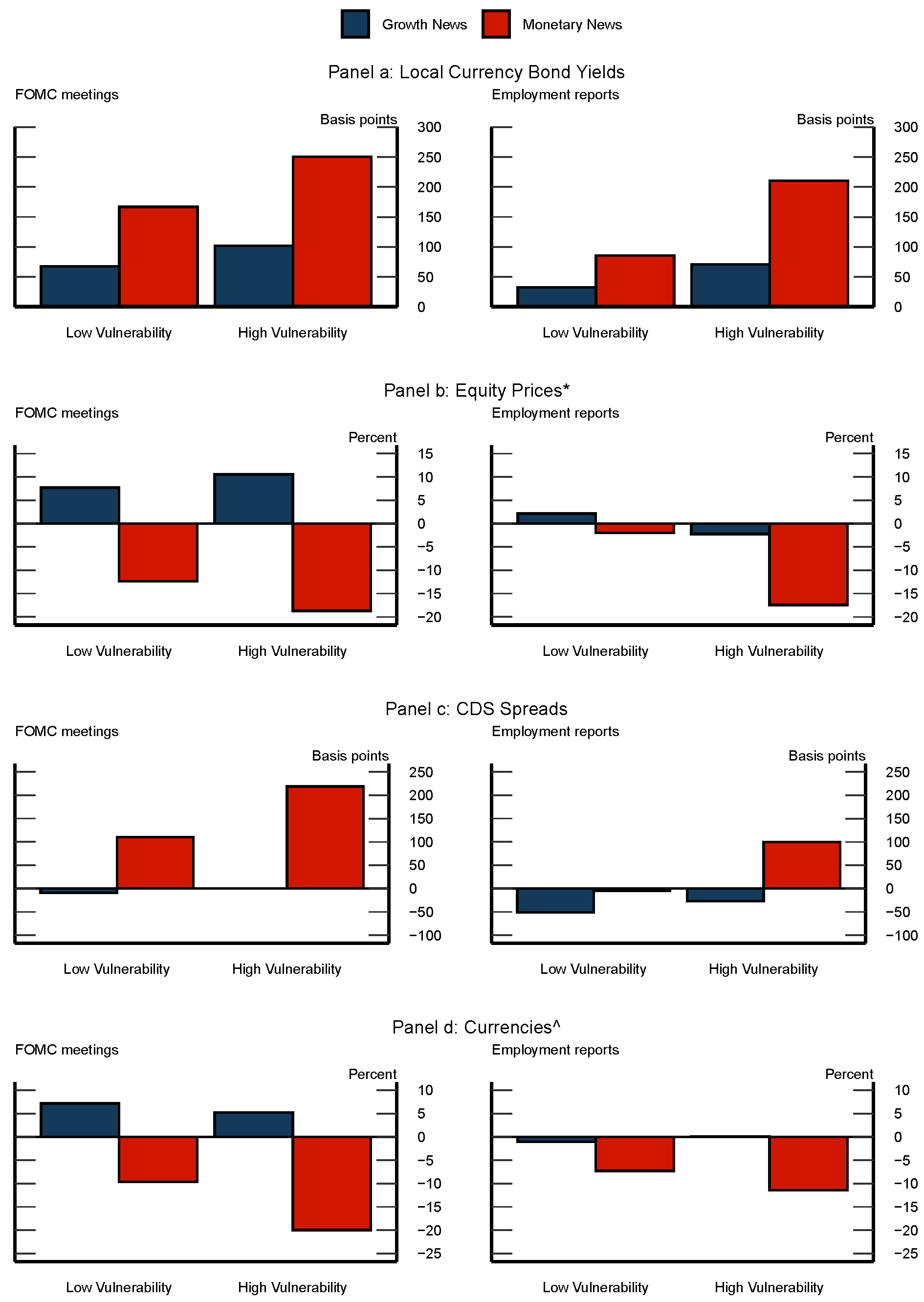

With this classification in hand, we next estimate how emerging market asset prices—domestic-currency bond yields, equity indexes, CDS spreads, and currencies—respond to movements in U.S. Treasury yields. We run separate panel regressions of each of these four asset prices on changes in the 10-year U.S. Treasury yield around FOMC meetings and employment reports, drawing on a sample of 22 EMEs from January 2010 to March 2021.5 We allow the estimated responses to differ based on (1) whether the FOMC meeting or employment report is categorized as revealing growth news or monetary news, according to the methodology discussed above, and (2) EMEs' own macroeconomic vulnerabilities prior to the event.6 To quantify EMEs' vulnerabilities, we used a composite measure developed by Ahmed et al. (2017), which combines information from six indicators: inflation, current account deficits, international reserves, government debt, external debt, and private-sector credit growth.

Our main results are presented in figure 3.7 The charts show the effect of a 100 basis-point rise in the 10-year Treasury yield on EME asset prices. The blue bars show spillovers from growth news, the red bars from monetary news. The charts make our two key findings abundantly clear: (1) changes in Treasury yields driven by monetary news have much larger effects on EME asset prices than yields driven by growth news; and (2) asset prices in the more vulnerable economies are more sensitive to Treasury yields than prices in less vulnerable economies. Higher yields driven by monetary news hit the more vulnerable economies hard: domestic-currency bond yields rise by more than twice the change in U.S. yields, CDS spreads soar, and stock prices and currencies collapse. Conversely, when higher Treasury yields reflect growth news, effects on EME financial conditions are generally limited and, statistically speaking, indistinguishable from zero in most cases.

In conclusion, higher U.S. Treasury yields can result in a significant tightening of EME financial conditions but such effects importantly depend on the drivers of higher yields and domestic conditions in EMEs. Our results help explain limited financial spillovers to EMEs from higher U.S. Treasury yields so far this year, as the increases appear to have been substantially driven by improved growth prospects for the United States. That said, were future increases in interest rates to reflect heightened concerns about inflation, vulnerable EMEs would likely come under pressure.

Note: 'Low vulnerability' and 'High vulnerability' refer to the five least and five most vulnerable countries in our sample, respectively.

* Equity prices denominated in local currency.

^Positive values indicate local currency appreciation.

Sources: Bloomberg, FRBNY New Price Quote System, Haver Analytics, IMF, and Author's calculations.

Key identifies bars in order from left to right.

References

Ahmed, S., Coulibaly, B. and Zlate, A., 2017. International financial spillovers to emerging market economies: How important are economic fundamentals?. Journal of International Money and Finance, 76, pp.133-152.

Cieslak, A. and Schrimpf, A., 2019. Non-monetary news in central bank communication. Journal of International Economics, 118, pp. 293-315.

Hoek, J., Kamin, S. and and Yoldas, E. 2020. When is Bad News Good News? U.S. Monetary Policy, Macroeconomic News, and Financial Conditions in Emerging Markets. International Finance Discussion Papers 1269. https://doi.org/10.17016/IFDP.2020.1269

International Monetary Fund (IMF), 2021, "Chapter 4: Shifting Gears: Monetary Policy Spillovers During the Recovery from COVID-19," World Economic Outlook, April.

Jarociński, M. and Karadi, P., 2020. Deconstructing monetary policy surprises: the role of information shocks. American Economic Journal: Macroeconomics, 12(2), pp. 1-43.

Laeven, L. and F. Valencia, 2018. Systemic Banking Crises Revisited. IMF Working Paper No. 18/206. https://www.imf.org/en/Publications/WP/Issues/2018/09/14/Systemic-Banking-Crises-Revisited-46232

Appendix: Detailed Regression Results

| Currencies | CDS spreads | LC Bond yields | Equity prices | |||||

|---|---|---|---|---|---|---|---|---|

| FOMC | Employment | FOMC | Employment | FOMC | Employment | FOMC | Employment | |

| 10-year U.S. treasury, Growth | -6.216 | 0.492 | -4.680 | -40.050 | 0.822* | 0.513** | 9.101 | -0.007 |

| (5.878) | (2.440) | (55.070) | (33.580) | (0.441) | (0.208) | (7.215) | (6.688) | |

| 10-year U.S. treasury, Monetary | 14.71*** | 9.305*** | 159.0* | 42.230 | 2.027*** | 1.469*** | -15.47* | -9.527* |

| (5.319) | (2.593) | (87.300) | (26.480) | (0.663) | (0.168) | (9.092) | (5.463) | |

| EME vulnerability | -0.019 | 0.001 | -0.307 | -0.121 | -0.002 | -0.002 | -0.012 | 0.002 |

| (0.035) | (0.030) | (0.280) | (0.217) | (0.004) | (0.003) | (0.042) | (0.038) | |

| EME vulnerability x 10-year U.S. Treasury, Growth | 0.231 | -0.132 | 1.198 | 3.177 | 0.047 | 0.047 | 0.349 | -0.534 |

| (0.756) | (0.305) | (8.349) | (3.792) | (0.062) | (0.045) | (0.790) | (0.424) | |

| EME vulnerability x 10-year U.S. Treasury, Monetary | 1.259** | 0.509 | 14.27** | 13.80*** | 0.114 | 0.152*** | -0.770 | -1.886*** |

| (0.588) | (0.367) | (6.567) | (4.285) | (0.072) | (0.047) | (0.883) | (0.492) | |

| No. of observations | 741 | 1239 | 728 | 1333 | 595 | 1039 | 737 | 1223 |

| R-squared | 0.138 | 0.038 | 0.141 | 0.033 | 0.082 | 0.078 | 0.097 | 0.013 |

1. Jasper Hoek and Emre Yoldas are economists at the Federal Reserve Board; Steve Kamin is at the American Enterprise Institute. We thank John Caramichael, Ethan Lewis, Dylan Kirkeeng, and Henry Young for excellent research assistance. The views expressed in this paper are solely those of the authors and should not be interpreted as reflecting the views of the Board of Governors or the staff of the Federal Reserve System. Return to text

2. Hoek, Jasper, Steve Kamin, and Emre Yoldas (2020). When is Bad News Good News? U.S. Monetary Policy, Macroeconomic News, and Financial Conditions in Emerging Markets. International Finance Discussion Papers 1269. https://doi.org/10.17016/IFDP.2020.1269 . Later analysis by IMF (2021), based on an event-study approach that is broadly similar to our own, comes to similar conclusions. Return to text

3. The short time window ensures that changes in yields reflect responses to the FOMC or payroll announcements rather than to other events that might influence yields. Return to text

4. Such information effects may be driven by either perceptions of private information revealed by central bank communications or a change in investors' thinking about the outlook in light of the central bank's viewpoint; see for example Cieslak and Schrimpf (2019) and Jarociński and Karadi (2020). Return to text

5. For EME asset prices, we use a 2-day window from the day before the event to the day after, which allows us to capture market reactions in different asset segments in all time zones. Return to text

6. More specifically, we rank the 22 EMEs in our sample based on their values for the following indicators: (1) current account deficit as a percent of GDP, (2) gross government debt as a percent of GDP, (3) average annual inflation over the past three years, (4) the five-year change in bank credit to the private sector as a share of GDP, (5) the ratio of external debt to exports, and (6) the ratio of foreign exchange reserves to GDP. By construction, the higher the rankings on each measure, the higher the vulnerability. We average the rankings across indicators for each EME. Return to text

7. Detailed results for the underlying regression are shown in the appendix. Return to text

Hoek, Jasper, Steve Kamin, and Emre Yoldas (2021). "Are Rising U.S. Interest Rates Destabilizing for Emerging Market Economies?," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, June 23, 2021, https://doi.org/10.17016/2380-7172.2930.

Disclaimer: FEDS Notes are articles in which Board staff offer their own views and present analysis on a range of topics in economics and finance. These articles are shorter and less technically oriented than FEDS Working Papers and IFDP papers.