FEDS Notes

October 23, 2020

Closing the Monetary Policy Curriculum Gap: A Primer for Educators Making the Transition to Teaching the Fed's Ample-Reserves Framework

Jane Ihrig and Scott Wolla1

The Federal Reserve (the Fed), the central bank of the United States, has a Congressional mandate to promote maximum employment and price stability. While those goals were articulated in 1977,2 the approach and tools used to implement those objectives have changed over time. Before the Financial Crisis of 2007-09, the Fed implemented monetary policy with limited reserves in the banking system and relied on open market operations as its key tool. Today, the Fed implements monetary policy with ample reserves and relies on one of its administered rates, interest on reserves (IOR), as its primary tool. These changes might seem subtle, but the current framework is very different from the previous one. And, this shift is not reflected in many teaching resources, from economics standards to principles textbooks. This Note provides an overview of how policy implementation has changed, and it provides teaching guidance for educators as they transition materials to the Fed's current implementation framework.

Teaching Monetary Policy

The Federal Open Market Committee (FOMC) of the Federal Reserve sets the stance (position) of monetary policy to guide employment and prices (inflation) in the desired direction. Figure 1 shows the chain reaction of how the stance of monetary policy is transmitted through financial markets and ultimately affects economy activity. This Note focuses on the change in the choice of the level of reserves to supply to the banking system and the monetary policy tools used before and after 2008 that affect the first link in the chain: that is, how the Fed ensures that when the FOMC sets a particular federal funds target range (Box 1 in Figure 1) that this level is also reflected in current and expected short-term interest rates (Box 2). Within the Fed, this change in supply of reserves and policy tools reflects a change in what they call their "implementation regime." Here we will talk about it as a change in the Fed's policy implementation framework.

As Figure 1 shows, current and expected short-term interest rates influence long-term interest rates and overall financial conditions (Box 3). Those rates and conditions then influence consumers' and producers' spending decisions (Box 4)—whether they spend money or save money. Those spending decisions then affect overall spending, investment, and production, which affect employment and inflation (prices). So, ensuring that the setting of the FOMC's target range transmits to financial markets is very important for the Committee to move the economy toward its Congressional mandate.

For the public, the way the Fed implements policy is generally not evident in their everyday lives. But, because monetary policy affects the economy, the way it is implemented is included in textbooks, standards, and curricula. And, because policy can and has changed faster than these materials are updated, it is important for educators to understand the changes and adjust their instruction to explain them.

An Overview of the Old Implementation Framework: Limited-Reserves

Prior to 2008, the Fed used a framework to implement policy in which it supplied a limited amount of reserves to the banking system. Traditionally, total bank reserves are composed of two types: (i) Required reserves are funds that a depository institution must hold in reserve against specified deposits as vault cash or deposits with Federal Reserve Banks. (ii) Excess reserves are the amount of funds held by a depository institution in its account at a Federal Reserve Bank in excess of its required reserves balance.

Banks held reserves to meet the Fed's regulatory reserve requirements and to ensure they had adequate funds to meet the banking demands of their customers. Because reserves earned no interest, banks tended to hold just a bit more than what was needed to meet their reserve requirements. When banks needed extra reserves to meet their demands, they would borrow reserves in the federal funds market. Or, if banks had excess reserves, they could lend them in the federal funds market. In terms of market participation, banks that lent money acted as suppliers of reserves in the federal funds market, and banks that borrowed money acted as demanders of reserves in the federal funds market. This interaction between supply and demand determined the federal funds rate (FFR), which textbooks define as the interest rate that banks charge each other to borrow or lend reserves in the federal funds market. 3

Importantly, the FFR is the policy rate that the FOMC uses to set the stance of monetary policy in pursuit of its objectives. More specifically, the Fed sets a target for the FFR and then uses monetary policy tools (explained below) to influence the market-determined FFR to move toward the FFR target. That is, the Fed uses its tools to influence the interest rate that banks charge each other in the federal funds market to move toward the FFR target.

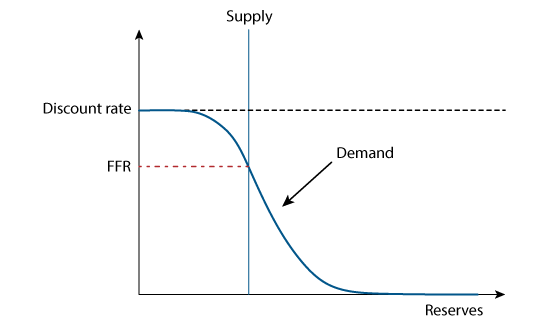

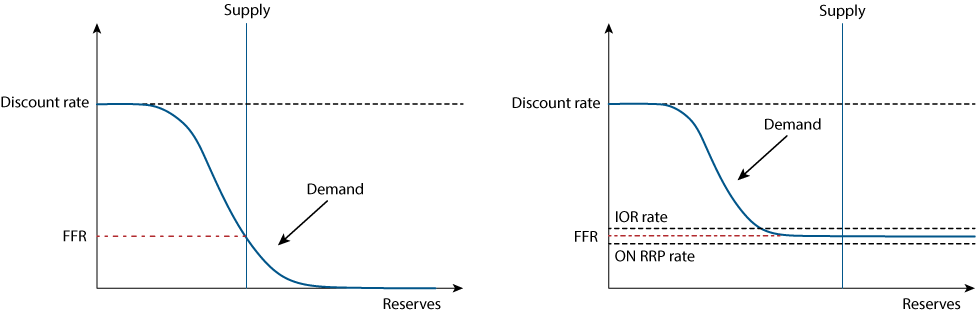

Figure 2 depicts the money market diagram that may be familiar to teachers and professors. The diagram captures the relationship between reserves and the FFR.4 The downward sloping demand curve represents banks' demand for reserves. The top of the curve is capped by the Fed's discount rate, which acts like a ceiling for the FFR because banks would be unlikely to borrow funds at a higher rate than they could get at the Fed's discount window. The demand curve slopes down to capture the idea that as the cost of borrowing decreases, banks are willing to borrow more funds to increase their holdings of reserves. The supply curve is vertical because only the Fed can supply reserves. The intersection of the two lines determines the FFR.

When reserves are limited (or scarce), relatively small increases or decreases in the supply of reserves shifts the supply curve right (left) and results in a lower (higher) FFR as follows:

- To raise the FFR, the Fed decreases the supply of reserves by selling U.S. Treasury securities in the open market.5 The decrease in reserves shifts the supply curve left, resulting in a higher FFR.

- To lower the FFR, the Fed increases the supply of reserves by buying U.S. Treasury securities in the open market. The increase in reserves shifts the supply curve right, resulting in a lower FFR.

The Fed's buying and selling of U.S. Treasury securities is referred to as open market operations, and it was the primary tool the Fed used to adjust the FFR and move the economy toward maximum employment and stable prices prior to 2008. In this framework, the Fed tended to use daily open market operations to fine tune the location of the supply curve and keep the FFR at the FOMC's target. The Fed tended to keep the spread between the discount rate and FFR roughly constant. So, when the FOMC raised or lowered its policy target, the Fed also raised or lowered the discount rate.

In summary, prior to 2008, monetary policy implementation focused on influencing the supply of reserves in the banking system (using daily open market operations) as a means for adjusting the FFR. Table 1 notes how textbooks and curricula have usually described monetary policy implementation in a limited-reserves framework and also notes how it worked in practice before 2008.

Table 1

| Limited-Reserves Framework | ||

|---|---|---|

| Tool | Definition | In Practice |

| Reserve requirements | Funds that banks must hold in cash, either in their vaults or on deposit at a Federal Reserve Bank. | Reserve requirements were an important tool driving demand for bank reserves. |

| Open market operations | The buying and selling of government securities by the Federal Reserve. | Open market operations were the principle tool of monetary policy implementation. Purchases (sales) increased (decreased) the supply of reserves, which shifted the supply of reserves left (right), thereby influencing where supply intersected demand, and lowered (raised) the FFR. Open market operations were used daily to fine-tune the market-determined FFR to the FOMC's FFR target. |

| Discount rate | The interest rate charged by the Federal Reserve to banks for loans obtained through the Fed's discount window. | The discount rate is an administered rate set by the Fed. It is the interest rate charged to banks on their loans from the Fed's discount window, which was in place primarily for emergency lending. The rate was set above the FFR target to help cap the interest rates banks paid in the federal funds market; that is, banks could borrow from the Fed at this rate instead of having to pay a higher rate. In practice, because borrowing from the Fed tends to be perceived as a stigma, banks tended not to borrow at the discount window. The spread between the discount rate and the FFR target tended to be held constant because the Fed would typically adjust the discount rate at the same time the FOMC adjusted the FFR target. |

How the Financial Crisis of 2007-09 Changed Monetary Policy Implementation

In response to economic and financial conditions in 2008, the Federal Reserve lowered the FFR target to near zero. And, it also shifted from setting a single FFR target to setting a FFR target range, with the upper and lower limits on the range consistently 0.25 percentage points apart. For example, starting in December 2008, the target range was set at 0 to 25 basis points (i.e., 0.0 percent to 0.25 percent). But even with that low range, the economy still needed more stimulus.6 As a result, between 2008 and 2014 the Fed conducted a series of large-scale asset-purchase programs to lower longer-term interest rates, ease broader financial market conditions, and thus support economic activity and job creation.7 In particular, the Fed purchased a sizable amount of longer-term securities issued by the U.S. government and issued or guaranteed by government-sponsored agencies such as Fannie Mae or Freddie Mac. These purchases not only increased the Fed's level of securities holdings but also increased the total level of reserves in the banking system from around $15 billion in 2007 to about $2.7 trillion in late 2014. At this point, reserves were no longer limited but instead quite plentiful, or "ample."

The Financial Crisis also resulted in the implementation of new monetary policy tools. The most significant was IOR. Congress had given the Fed authority to pay interest on reserves in 2006, with a start date of 2011. The start date was pushed up to October 2008 so the Fed could use the tool during the Financial Crisis.

Interest on reserves applies to both required reserves (IORR) and excess reserves (IOER).

- IORR: Prior to the Financial Crisis, when banks held their required reserves on deposit at Federal Reserve Banks they received no interest compensation, which they recognized as a lost opportunity to earn interest elsewhere. For this reason, it was seen as regulation that imposed an "implicit tax" on banks. IORR eliminated the implicit tax on reserve requirements.

- IOER: Because banks did not receive interest on their reserves held at the Fed, banks often minimized their holdings of excess reserves. The Fed's decision to start paying IOER changed the incentives for the marginal excess dollar in reserves. The IOER rate became a tool to influence banks to hold more or fewer excess reserves. For example, a higher IOER rate relative to market (alternative) interest rates increased the incentive for banks to hold excess reserves at the Fed. As such, IOER gave the Fed a powerful new tool for implementing monetary policy.

Since late-November 2008, IORR and IOER have been set to the same rate. And, effective March 26, 2020, the Board of Governors of the Federal Reserve System announced that it was reducing reserve requirement ratios to zero, making IORR effectively irrelevant.8 Reflecting both these factors, one can think of this policy tool as setting a single rate—the IOR rate.

As the economy recovered from the Great Recession, the Fed took steps to reduce the supply of reserves from its peak in October 2014 of about $2.7 trillion. Over the next few years, the Fed reduced reserves to about $1.7 trillion. They still remained ample, however. In fact, in January 2019, the FOMC released a statement saying it would continue to implement policy with ample reserves over the longer run.9,10

The Current Implementation Framework: Monetary Policy with Ample Reserves

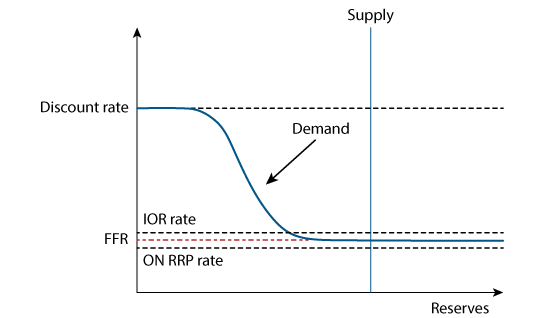

When there is a large quantity of reserves in the banking system, the Federal Reserve can no longer influence the FFR by making relatively small changes in the supply of reserves (Figure 3). That is, because the supply curve intersects the flat, horizontal, portion of the demand curve, small shifts in the supply curve to the right or left will not move the FFR higher or lower. Rather, in the ample-reserves framework, the Fed uses its administered rates, which include the IOR rate and the overnight reverse repurchase agreement (ON RPP) rate, to influence the FFR. This section describes how this new framework works.

Figure 3 shows the demand and supply curves in the current ample-reserves framework. The top of the demand curve is still influenced by the Fed's discount rate. Now, however, the demand curve turns flat near the Fed's new administered rates, which helps steer the FFR into the FOMC's target range. The supply curve is such that it intersects the demand curve where it is flat. With this "ample" level of reserves, the Fed does not need to make daily open market operations to purchase or sell securities, as it did in the limited-reserves framework to hit the FFR target (because now small shifts of the supply curve have little or no effect on the FFR rate ).

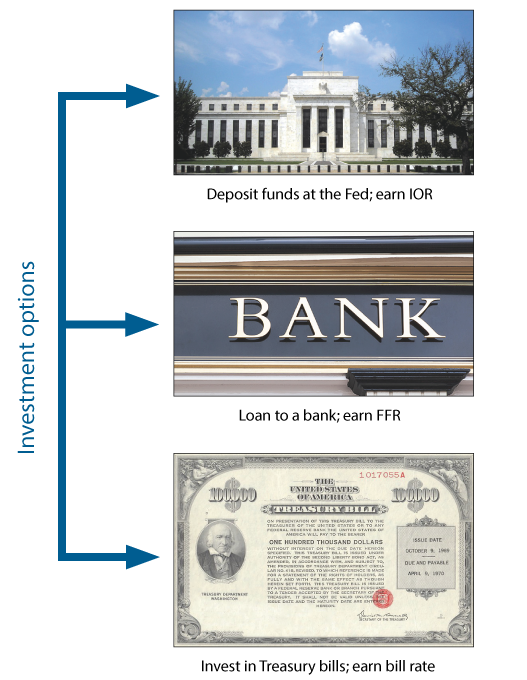

The primary tool for keeping the FFR in its target range and driving the demand curve flat is the IOR rate. Although banks have several short-term investment options (Figure 4) for their money, the IOR rate offers them a safe overnight option. Because IOR makes cash deposited at the Fed a risk-free investment option, banks are unlikely to lend reserves in the federal funds market for less than the IOR rate. In other words, the IOR serves as a reservation rate for banks—the lowest rate that banks are likely willing to accept for lending out their funds. And, if the FFR were to fall very far below the IOR rate, banks would be likely to borrow in the federal funds market and deposit those reserves at the Fed, earning a profit on the difference. This concept is known as arbitrage, an important aspect of the way financial markets, and monetary policy implementation, work. Arbitrage ensures that the FFR does not fall much below IOR.

These financial incentives (i.e., the reservation rate and arbitrage) are such that when the Fed raises or lowers the IOR rate, the FFR also moves up or down. As such, the Federal Reserve can steer the FFR into the target range set by the FOMC by adjusting the IOR rate. And, because the Fed sets the IOR rate directly, the rate serves as an effective monetary policy tool. Currently, IOR is the primary tool used by the Fed for influencing the FFR.

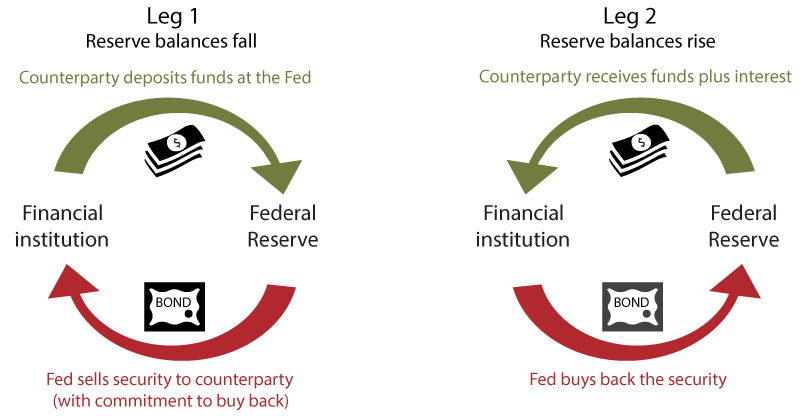

However, not all institutions with reserve accounts can earn interest on their deposits at the Federal Reserve and not all important institutions in financial markets are allowed to have an account at the Fed. This leaves the possibility that important short-term rates (including the FFR) might drop below the IOR rate. So, in 2014, the FOMC announced that it intended to use the overnight reverse repurchase (ON RRP) facility to help control the FFR. The ON RRP facility is a form of open market operations where the Fed interacts with many nonbank financial institutions, such as large money market funds and government-sponsored enterprises.11 When one of these institutions uses the ON RRP facility, it essentially deposits reserves at the Fed overnight, receiving a security as collateral. The next day the transaction is "unwound"—the Fed buys back the security and the institution earns the ON RRP rate (which the Fed sets) on the cash it deposited at the Fed (Figure 5).

Because this is a risk-free investment option, the given institutions will likely never be willing to lend funds for lower than the ON RRP rate. As such, the ON RRP rate acts as a reservation rate and institutions can use it to arbitrage other short-term rates. Thus, the rate paid on ON RRP transactions, which is set below the IOR rate, acts like a floor for the FFR and serves as a supplementary policy tool.

Table 2 provides a summary of the tools used in an ample-reserves framework. It is these concepts that should be covered in textbooks and curricula. In fact, the IOR and ON RRP rates should be the focus of policy implementation discussions.

Open market operations are still used in this framework; however, purchases of securities are only made as needed to maintain an ample level of reserves. That is, over time, factors outside the Fed's control may drain reserves to the point where the Fed will want to purchase securities to keep the supply of reserves on the flat portion of the demand curve (as in figure 3).12 This use of open market operations is quite different than that in the limited-reserves framework.

Table 2

| Ample-Reserves Framework | ||

|---|---|---|

| Tool | Definition | In Practice |

| IOR | Interest paid on reserves that banks hold in their accounts at a Federal Reserve Bank. | IOR is an administered rate set by the Fed. Banks are unlikely to lend their reserves in the federal funds market for less than they get paid by the Fed. As such, IOR works as a reservation rate and works through arbitrage to guide the FFR into the FOMC's target range. In fact, interest on reserves is the primary tool for moving the FFR within the target range. |

| ON RPP | An overnight transaction in which the Federal Reserve sells a security to an eligible counterparty and simultaneously agrees to buy the security back the next day. | The ON RRP rate is an administered rate set by the Fed. More types of financial institutions can participate in the ON RRP facility than can earn IOR. Because these institutions are unlikely to lend funds for lower than the ON RRP rate, and institutions can arbitrage the difference between short-term rates, the FFR is unlikely to fall below the ON RRP rate. As such, the ON RRP rate is a supplementary tool that acts like a floor for the FFR. NOTE: The ON RRP facility is a form of open market operations. |

| Open market operations | The buying and selling of government securities by the Federal Reserve. | While daily purchases and sales are no longer used to adjust the supply of reserves and influence the FFR, open market operations are an important tool for ensuring that reserves remain ample. |

| Discount rate | The interest rate charged by the Federal Reserve to banks for loans obtained through the Fed's discount window. | The discount rate is an administered rate set by the Fed. It is set above the FFR target range with the intention of it serving as a ceiling for FFR transactions because banks are unlikely to borrow at a higher rate than they can borrow from the Fed at the discount window. The perceived stigma of borrowing from the Fed, however, generally dampens the rate's effectiveness as a ceiling. The spread between the discount rate and the FFR target tends to be constant; the Fed typically adjusts the discount rate at the same time the FOMC moves the FFR target range. |

| Reserve requirements | Funds that banks must hold in cash, either in their vaults or on deposit at a Federal Reserve Bank. | With reserves ample, and many banks holding excess reserves, reserve requirements do not play a significant role in policy implementation. In fact, as of March 26, 2020, reserve requirement ratios have been set to zero. |

During recent times of severe stress, the ample-reserves framework has continued to support the implementation of monetary policy. The Fed's response to the COVID-19 pandemic has been somewhat similar to its response to the Financial Crisis of 2007-09. With the ultimate goal of stimulating the economy, it has lowered the FFR target range to 0 to 25 basis points (lowered the IOR and ON RRP rates to near zero); and taken other, often nontraditional, actions to help market functions, support credit flows to households and businesses, and lower longer-term interest rates.13 The majority of the Fed's special facilities enabled it to buy, borrow, or swap less-liquid financial assets in return for reserves. Now, as during the Financial Crisis of 2007-09, these actions have shifted the supply curve in Figure 3 to the right and resulted in reserves becoming quite abundant. Though these actions were quick and substantial, implementation of monetary policy remained smooth as the Fed continued to operate in its existing (ample-reserves) implementation framework.

Comparing the Ample-Reserves Framework with the Limited-Reserves Framework

The classic model for teaching monetary policy in the classroom features a money supply and demand model. A key difference between the limited-reserves framework and the ample-reserves framework lies in where the supply curve intersects the demand curve.

- In the limited-reserves framework (Panel A of Figure 6), the supply curve intersects the demand curve on the downward sloping part of the demand curve. In this region, relatively small shifts of the supply curve to the right (left) move the FFR rate higher (lower).

- In the ample-reserves framework (Panel B of Figure 6), the supply curve intersects the demand curve on the flat portion of the demand curve. In this region, relatively small shifts of the supply curve have little or no effect on the FFR rate.

Based on the supply of reserves, the Fed uses different primary tools to steer interest rates into the desired range.

- The limited-reserves framework leans on the Federal Reserve's use of open market operations to make adjustments to the supply of reserves to ensure the market FFR is at the FOMC's FFR target. This tool's effect on the FFR requires students to understand the abstract topic of how open market operations work and then link this action back to the demand-supply diagram.

- The ample-reserves framework relies on the Federal Reserve's administered rates—in particular the IOR rate—to influence the FFR. The linkage between the Fed's tools and the FFR requires an understanding of the concepts of reservation rate and arbitrage.

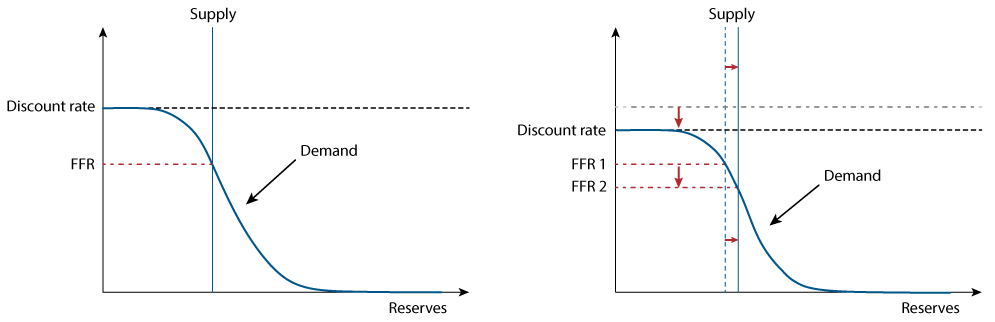

Explaining the implementation of monetary policy is often a focus of textbooks, standards, and curricula. Discussion of the monetary policies tools used, then, needs to differ according to the policy framework. For example, say the FOMC has lowered the target for the FFR rate. How does the Fed ensure that this lower target is transmitted to financial markets? Let's consider the key tools used in each framework. 14

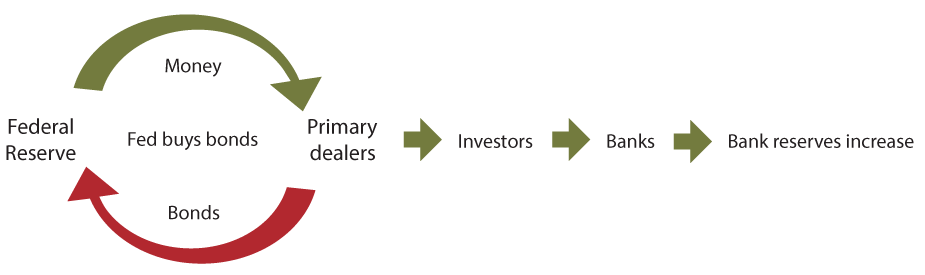

In the limited-reserves framework, the Fed would purchase securities in the open market to influence the FFR rate to move toward the new lower target. More specifically, as shown in Figure 7, the New York Fed's Open Market Trading Desk would use open market operations: It would purchase government securities from its primary dealers, who sell these securities on behalf of their clients (investors). The money received from the sales would then be deposited in banks, resulting in an increase in the level of reserves in the banking system. The increase in the level of reserves (a rightward shift of the supply curve) would result in a decrease in the federal funds rate, as shown in Figure 8.

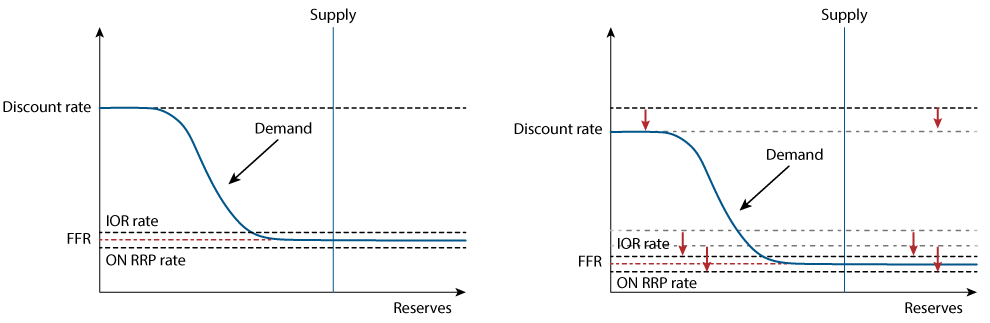

In an ample-reserves framework, the Fed would lower its administered rates, in particular the IOR rate. This action would lower the reservation rate for reserves, putting downward pressure on the FFR.

Graphically, in the ample-reserves framework, as the Fed lowers its administered rates (including the discount rate) the endpoints of the demand curve shift down, as shown in the right panel of Figure 9. The lower discount rate pushes down the top of the demand curve. The discount rate acts as a ceiling for the FFR because banks (aside from the perceived stigma) would be unlikely to borrow funds at a higher rate than they could borrow from the Fed at the discount window. The bottom of the demand curve shifts down to reflect the Fed's lower reservation rates (the IOR and ON RRP rates) for depositing financial institutions' excess funds. This lower demand curve then intersects with the supply curve at a lower FFR.

In both regimes, open market operations are an important tool of policy implementation. However, the use is quite different. In the limited-reserves regime, open market operations are the primary tool, with daily purchases or sales to adjust the supply of reserves in order to precisely hit the FOMC's FFR target. In an ample-reserves regime, open market operations are more behind the scenes, with purchases of securities being made only when outside factors contract the supply of reserves and the Fed deems it is time to purchase securities (boost reserves) to ensure reserves remain ample.

Finally, one can see a difference in what each framework can do when the Fed is confronted with severe economic strains and needs to introduce unconventional tools. The use of large-scale asset purchases or emergency credit programs are needed during these times and result in very large increases in reserves in the banking system. Only one of the two frameworks would continue to be feasible:

- A limited-reserves framework would no longer be functional. As we saw during the Financial Crisis of 2007-09, reserves became super abundant and the Fed had to shift to operating in an ample-reserves framework, using IOR as the key tool.

- An ample-reserves framework would continue to work as expected, as we saw with the onset of the COVID-19 pandemic.

Summary

The way the Fed implements monetary policy has changed. It is important for teachers and professors to understand the current framework so they are teaching their students accurately. Here we have provided a discussion of the key concepts of an ample-reserves regime and contrasted the features of the old and new frameworks to support instructors in this endeavor.

Glossary of Key Terms

Administered rate: An interest rate that is set directly rather than being influenced by the market forces of supply and demand.

Arbitrage: The simultaneous purchase and sale of a good in order to profit from a difference in price.

Discount rate: The interest rate charged by the Federal Reserve to banks for loans obtained through the Federal Reserve's discount window.

Discount window: Federal Reserve lending to depository institutions to support the liquidity and stability of the banking system and the effective implementation of monetary policy.

Facility: A formal financial assistance program offered by a lending institution to help a targeted set of counterparties (those eligible to borrow) with funding needs. The Federal Reserve has permanent facilities (like the discount window) and temporary facilities (like those implemented during the Financial Crisis of 2007-09 and the COVID-19 pandemic).

Federal funds rate (FFR): The interest rate depository institutions charge each other to borrow or lend reserves in the federal funds market; these funds are immediately available.

Federal Open Market Committee (FOMC): A Committee created by law that consists of the seven members of the Board of Governors; the president of the Federal Reserve Bank of New York; and, on a rotating basis, the presidents of four other Reserve Banks. Nonvoting Reserve Bank presidents also participate in Committee deliberations and discussion.

Open market operations: The buying and selling of government securities by the Federal Reserve.

Policy rate: The interest rate that is used by a central bank to set and communicate its monetary policy stance (or position). In the United States, the FOMC uses the federal funds rate as the policy rate.

Reserves: The sum of cash that banks hold in their vaults and the deposits they maintain with Federal Reserve banks.

Reserve requirement: The percentage of a bank's deposits it is required by law to hold.

U.S. Treasury securities: Bonds, notes, and other debt instruments sold by the U.S. Treasury to finance U.S. government operations.

Additional Resources

Ihrig, Jane, Zeynep Senyuz, and Gretchen C. Weinbach (2020a). "The Fed's "Ample Reserves" Approach to Implementing Monetary Policy." Board of Governors of the Federal Reserve System, February 2020.

Ihrig, Jane, Zeynep Senyuz, and Gretchen C. Weinbach (2020b). "Implementing Monetary Policy in a "Ample-Reserves" Regime: The Basics (Note 1 of 3)," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, July 01, 2020.

Ihrig, Jane, Zeynep Senyuz, and Gretchen C. Weinbach (2020c). "Implementing Monetary Policy in an "Ample-Reserves" Regime: Maintaining an Ample Quantity of Reserves over the Long Run (Note 2 of 3)," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, August 28, 2020.

Ihrig, Jane, Zeynep Senyuz, and Gretchen C. Weinbach (2020d). "Implementing Monetary Policy in an "Ample-Reserves" Regime: When in Crisis (Note 3 of 3)," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, October 02, 2020.

Ihrig, Jane and Scott Wolla (2020). "Fixing the 'Curriculum Lag' in Economics: The New Tools the Fed is Using to Influence the Economy." National Council for the Social Studies Social Education, 84(2), pp. 93-99.

Ihrig, Jane, Gretchen C. Weinbach, and Scott Wolla (2020). "COVID-19's Effects on the Economy and the Fed's Response," Page One Economics®, September 2020.

Wolla, Scott. "A New Frontier: Monetary Policy with Ample Reserves." Federal Reserve Bank of St. Louis Page One Economics®, May 2019.

Wolla, Scott. "Fixing the 'Textbook Lag' with FRED (Part I): Monetary Policy in a World of Ample Reserves." Federal Reserve Bank of St. Louis FRED® Blog, June 10, 2019.

Wolla, Scott. "Fixing the 'Textbook Lag' with FRED (Part II): Monetary Policy in a World of Ample Reserves." Federal Reserve Bank of St. Louis FRED® Blog, June 13, 2019.

1. Jane Ihrig is a Senior Adviser at the Federal Reserve Board. Scott Wolla is the Economic Education Coordinator at the Federal Reserve Bank of St. Louis. This FEDS note was published jointly as a Page One Economics® primer, which is the original source of the figures. The views expressed here are solely the responsibility of the authors and should not be interpreted as reflecting the views of the Board of Governors of the Federal Reserve System or of anyone else associated with the Federal Reserve System. Return to text

2. In 1977, Congress amended the Federal Reserve Act, directing the Board of Governors of the Federal Reserve System and the Federal Open Market Committee to "maintain long run growth of the monetary and credit aggregates commensurate with the economy's long run potential to increase production, so as to promote effectively the goals of maximum employment, stable prices and moderate long-term interest rates." Return to text

3. On any given day, there are many transactions that settle at slightly different FFRs. The effective FFR is the volume-weighted median rate of these transactions. The effective FFR is the rate we use in the figures in this article. Return to text

4. Many textbooks link the money supply to interest rates. The inclusion of that link dates back to the 1970s and 1980s, when measures of the money supply exhibited fairly close relationships with important economic variables such as nominal gross domestic product and the price level. Based partly on these relationships, the Fed conducted monetary policy by targeting growth rates of various measures of money. Since the mid-1990s, however, these relationships have been quite unstable. As a result, the importance of the money supply as a guide for the FOMC in its conduct of monetary policy has diminished and the Fed has shifted to targeting the level of the FFR, which is influenced by the supply of reserves in the banking system as well as the Fed's administered rates. Return to text

5. The term "open market" refers to the fact that the Fed doesn't buy securities directly from the U.S. Treasury. Instead, securities dealers compete in the open market based on price, submitting bids or offers to the Open Market Trading Desk of the Federal Reserve Bank of New York through an electronic auction system. Return to text

6. The Fed also implemented a number of credit and liquidity programs early on in the Financial Crisis to support financial institutions and foster improved conditions in financial markets. These special programs expired or were closed after some time. Return to text

7. For a description of the Fed's large-scale asset purchases, see Board of Governors of the Federal Reserve System. "What Were the Federal Reserve's Large-Scale Asset Purchases?" FAQs. Return to text

8. This decision reflects the fact the Federal Reserve shifted to an ample-reserves framework, and reserve requirements are not necessarily a tool in this framework. Return to text

9. See Board of Governors of the Federal Reserve System. "Statement Regarding Monetary Policy Implementation and Balance Sheet Normalization." Press release, January 30, 2019. Return to text

10. More recently, in response to the COVID-19 pandemic, reserves have grown substantially. By April 2020, reserves expanded and stood above $3 trillion, at a higher level than their peak during the aftermath of the Great Recession. Return to text

11. A list of the Federal Reserve's reverse repo counterparties is found at: https://www.newyorkfed.org/markets/rrp_counterparties. Return to text

12. For a detailed discussion of the factors that drain reserves and how the Fed responds see Ihrig et al (2020c). Return to text

13. See Ihrig, Weinbach, and Wolla (2020) for a high-level overview of COVID-19's effects on the economy and the Federal Reserve's response. Ihrig et al. (2020d) provides additional information about how the Fed implements monetary policy with ample reserves in a crisis, with an specific look at the response to the COVID-19 shock. Finally, a complete list of the Fed's policy tools can be found at the Board of Governors of the Federal Reserve System website: https://www.federalreserve.gov/monetarypolicy/policytools.htm. Return to text

14. In most instances, the discount rate would be adjusted by the same amount as the target for the federal funds rate to keep the spread between the discount rate and the FFR constant. Return to text

Ihrig, Jane, and Scott A. Wolla (2020). "Closing the Monetary Policy Curriculum Gap: A Primer for Educators Making the Transition to Teaching the Fed's Ample-Reserves Framework," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, October 23, 2020, https://doi.org/10.17016/2380-7172.2754.

Disclaimer: FEDS Notes are articles in which Board staff offer their own views and present analysis on a range of topics in economics and finance. These articles are shorter and less technically oriented than FEDS Working Papers and IFDP papers.