FEDS Notes

July 19, 2019

Who Owns U.S. CLO Securities?

Emily Liu and Tim Schmidt-Eisenlohr1

A previous version of this note was published in July 2019 using TIC SHC data for year-end 2017, which at the time were the most recent available data. As of October, the data for TIC SHC 2018 have been published, and this update reflects these newly available data.

1. Introduction

The U.S. leveraged loan market has grown substantially in recent years with more and more loans bought by collateralized loan obligations (CLOs). Despite the increasing importance of U.S. CLOs, information on the holders of U.S. CLO securities is very limited. Information on who owns CLOs is, however, essential for quantifying the full exposures of investors to the leveraged loan market, as indirect holdings through CLOs represent a growing share of the total. This note fills part of that gap, providing (to our knowledge) the first breakdown of CLO investors by location and by investor type, combining data from the Treasury International Capital (TIC) system and the Securities Industry and Financial Markets Association (SIFMA). We find that most U.S. CLOs are held by U.S. investors and that the holdings are concentrated in insurance companies, mutual funds, and depository institutions. Foreign holdings are limited, as are holdings by hedge funds and other investment vehicles.

2. A Primer on CLOs

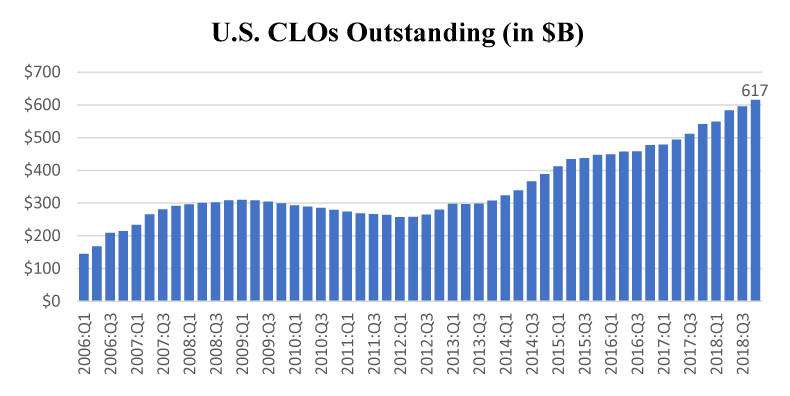

Collateralized loan obligations (CLOs) are a class of securities backed by an underlying portfolio of corporate loans. U.S. CLOs are primarily backed by U.S. dollar-denominated leveraged loans, typically to U.S. firms. The U.S. CLO market accounts for approximately half of U.S. leveraged loans outstanding.2 U.S. CLO issuance outstanding has grown dramatically over the past several years following a lull in the market after the crisis, reaching $617 billion in 2018:Q4 (see figure 1). At the same time, the composition of loans underlying the CLOs has shifted. Notably, the percentage of so-called "covenant-lite" loans in the leveraged loan market has grown substantially over time. Covenant-lite loans have no financial maintenance covenants, making them more like high-yield bonds.

Billions of dollars

Source: SIFMA U.S. CLOs Outstanding.

The typical U.S. CLO is structured as an offshore special purpose entity in order to benefit from legal isolation of assets as well as from a favorable tax treatment.3 Most U.S. CLOs are issued out of the Cayman Islands by a Cayman-resident primary issuer, with a smaller percentage issued in Delaware. The CLO issuer markets a variety of debt and equity tranches to investors and then uses the proceeds to purchase a portfolio of underlying assets. Any loans sold to an offshore vehicle must be placed with a U.S. bank that serves as trustee of the portfolio.

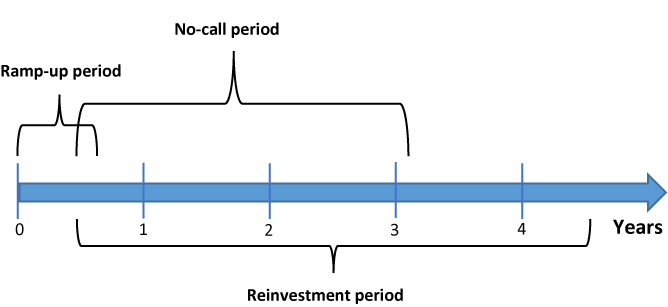

Figure 2 shows the life stages of a typical U.S. CLO, which consists of a short ramp-up period, during which the manager assembles the initial portfolio, a two-year no-call period, during which the issued securities are non-callable, and a reinvestment period. During the reinvestment period, which typically lasts four to five years, the portfolio of loans is actively managed by the CLO manager, who is free to make opportunistic changes to the asset mix within the limitations set forth by the CLO prospectus. The CLO prospectus dictates the permissible currency, nationality, industry, and rating mix of assets in the portfolio. Additionally, the CLO manager must maintain certain performance ratios over the life of the CLO. U.S. CLOs are not required to mark-to-market their assets, and early redemption by investors is generally not permissible. These features make the structure unsusceptible to "runs," and the AAA-rated tranches (which have never defaulted, even during the crisis) are popular with institutional investors. Table 1 shows a breakdown of CLO investors by tranche according to a public report by Fitch Ratings. The sub-investment grade (mezzanine) and equity tranches are generally held by more speculative investors, such as hedge funds and the CLO managers themselves.

Table 1: CLO Investors by Tranche

| AAA Notes | Mezzanine Notes | Equity |

|---|---|---|

| Insurance Companies | Hedge Funds | Private Equity |

| Foreign Banks | Asset Managers | CLOs |

| Pension Funds | Insurance Companies | Credit Opportunity Funds |

| U.S. Regional Banks | CLOs | CLO Managers |

| U.S. Investment Banks |

Source: Fitch Ratings Leveraged Finance Annual Manual for the Americas, May 2017.

3. CLO Holdings in the TIC Data

The Treasury International Capital (TIC) data are a collection of cross-border data on financial securities holdings owned by the U.S. Treasury and collected under the purview of the Federal Reserve. Because the TIC system defines foreign securities by residency of the issuer,4 U.S. CLO notes issued out of the Cayman Islands are considered foreign securities under TIC definitions, even if the underlying assets are U.S. leveraged loans. For our analysis of CLO holdings, we use the TIC annual surveys of U.S. holdings of foreign securities, also known as the "claims surveys," which measure holdings at the security level.

Our calculations based on the TIC data suggest that at end-2018 around $457 billion (74%) of U.S. CLO securities were issued out of the Cayman Islands and that of these Cayman-issues, $409 billion (89%) were held by U.S. investors at year-end 2018. We estimate that U.S. investors held an additional $147 billion of domestically-issued U.S. CLOs, for a total of $556 billion held by U.S. investors, or 90% of total U.S. CLOs outstanding. TIC data further suggest that foreigners held about $12 billion of domestically-issued U.S. CLOs, and we estimate that foreigners held $48 billion of Cayman-issued CLOs. In total, we estimate that only $60 billion (10%) of U.S. CLOs are held by investors that are not U.S. residents.5

The claims surveys also allow us to parse U.S. investor holdings of Cayman-issued CLOs by U.S. investor type, as shown in Table 2.6

Table 2: Domestic holdings ($ millions) of Cayman-issued U.S. CLO securities, by investor type

| Investor Type | 2018 | 2017 | 2016 | 2015 | ||||

|---|---|---|---|---|---|---|---|---|

| Insurance Company | 113,152 | 27.7% | 83,526 | 24.2% | 74,434 | 24.2% | 64,231 | 25.2% |

| Mutual Fund | 63,328 | 15.5% | 61,629 | 17.9% | 52,873 | 17.2% | 43,287 | 17.0% |

| Depository Institution | 61,557 | 15.0% | 60,798 | 17.6% | 51,431 | 16.7% | 37,203 | 14.6% |

| Other Financial Org (incl. BHCs) | 49,264 | 12.0% | 35,051 | 10.2% | 30,100 | 9.8% | 26,052 | 10.2% |

| Fund or Other Investment Vehicle | 42,928 | 10.5% | 32,072 | 9.3% | 34,887 | 11.3% | 24,175 | 9.5% |

| Pension Fund | 40,681 | 9.9% | 36,674 | 10.6% | 33,186 | 10.8% | 32,181 | 12.6% |

| Nonfinancial Org (incl. household) | 38,250 | 9.3% | 35,018 | 10.2% | 30,997 | 10.1% | 28,059 | 11.0% |

| Total Domestic Holdings | 409,160 | 344,769 | 307,910 | 255,188 | ||||

Source: TIC SHC(A).

Institutional investors, including insurance companies (28%), mutual funds (16%), and pension funds (10%) held roughly half of Cayman-issued CLOs at year-end 2018. However, depository institutions also held a non-trivial share at nearly 15%. Data from prior surveys suggest that these holding patterns have held relatively stable since 2015 with some increase in the percentage held by insurance companies.7

We estimate total holdings at end-2018 by applying the investor shares from the 2018 claims survey (from table above) to the total CLO issuance outstanding of $617 billion from SIFMA for end-2018.8 Of this total issuance, we estimate that $556 billion was held by U.S. investors, of which institutional investors held $295 billion and depository institutions held $83 billion. The residual $178 billion were held by other types of financial organizations (including holding companies and broker-dealers), hedge and other types of managed funds, and non-financial organizations.

Although the TIC system cannot capture information on foreign holdings of Cayman-issued CLOs, news reports suggest that Japanese banks hold as much as $60 billion in AAA-rated tranches of U.S. and European CLOs.9 While we do not know how much of these holdings are of U.S. CLOs, the TIC liabilities survey confirms that at least some domestically-issued CLO securities are indeed held by investors in Japan. Other foreign holders of domestically-issued CLO securities include investors in European financial centers.

4. European CLOs

The European CLO market is much smaller than the U.S. CLO market, with $99 billion in principal liabilities as-of 2018Q4.10 European CLOs are typically backed by euro-denominated assets and are subject to complex regulations that differ significantly from the U.S. CLO market. While demand for these securities appears to be dominated by European and Asian investors, the TIC data suggest that U.S. investors also hold small amounts of these securities, roughly $8 billion at year-end 2018.

Appendix: CLOs in the TIC Data

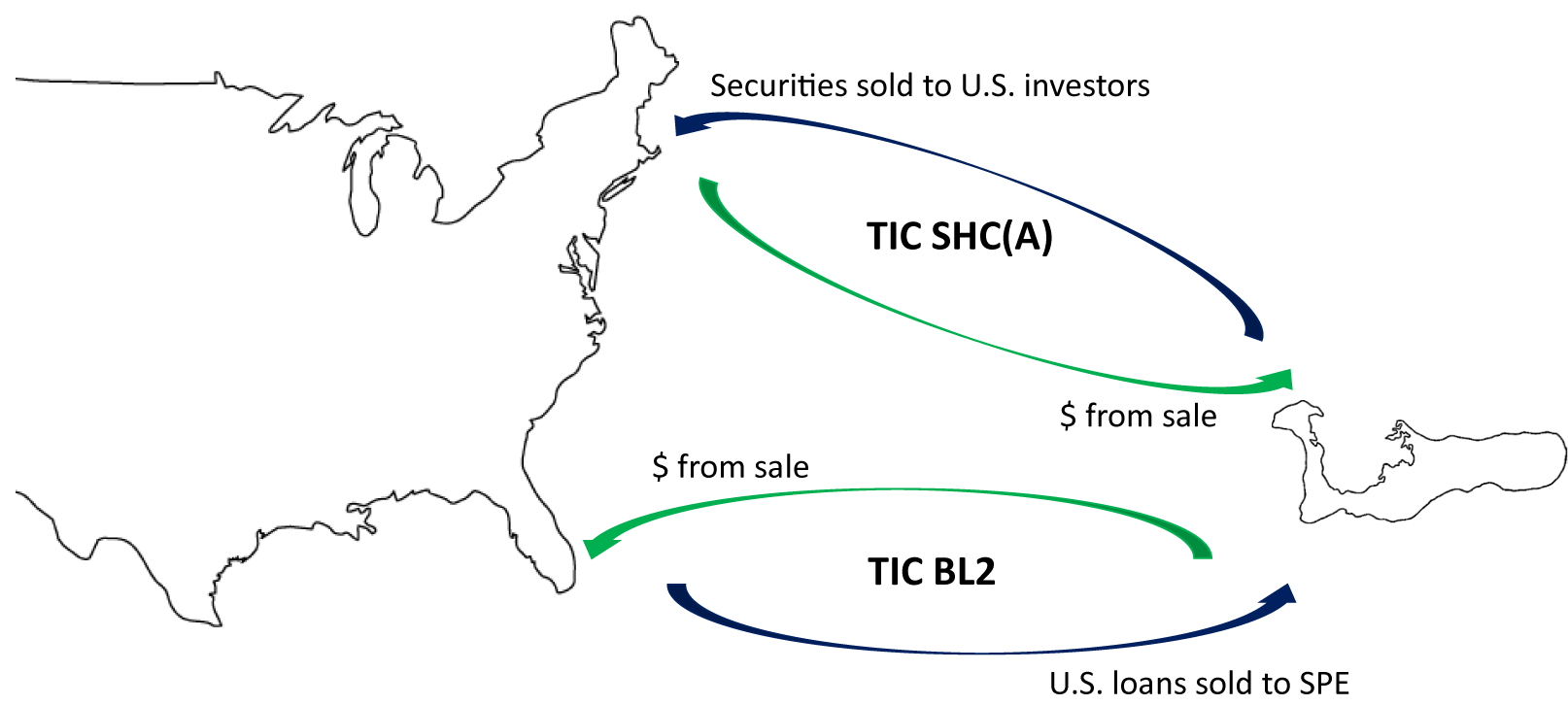

Because U.S. CLO notes are frequently issued by Cayman-resident entities, these securities are considered foreign under the TIC data definitions and are reportable on several of the TIC reports (see figure 3). All holdings of such Cayman-issued securities by U.S. investors are reportable on the TIC SHC/SHCA (annual survey of foreign securities claims of U.S. residents). Conversely, any securities issued by a CLO entity incorporated in the United States and held by foreign investors are reportable on the TIC SHL/SHLA (annual survey of U.S. securities liabilities to foreigners). Because the TIC data only pick up cross-border claims and liabilities, any securities issued by a Cayman-incorporated CLO and held by foreign investors or any securities issued by a U.S.-incorporated CLO and held by domestic investors would not be reportable anywhere in the TIC system.

Holdings of Cayman-issued CLO notes by U.S. investors have been observed and reported in the Annual Report of U.S. Portfolio Holdings of Foreign Securities since 2014. However, the offsetting reportable liabilities—the U.S. loans sold offshore to be pooled into CLOs—were largely missed by the TIC system prior to 2018. Beginning with the June 2018 as-of date, the TIC BL2 instructions were clarified such that the reporting of loans placed overseas and pooled into CLOs are the explicit responsibility of the CLO U.S. trustee, resulting in a much-improved reporting of such liabilities.11

For a typical U.S. CLO issuing out of the Cayman Islands

Table 3 shows the total outstanding U.S. CLO issuance compared with the reported TIC BL2, TIC SHC(A), and TIC SHL(A) positions. The liabilities reported on the TIC BL2 (column 2) represent the U.S. loans underlying Cayman-issued U.S. CLOs, while the TIC SHC(A) positions (column 3) are the U.S. holdings of Cayman-issued U.S. CLOs, and the TIC SHL(A) positions (column 4) are the foreign holdings of U.S.-issued U.S. CLOs.

Domestic holdings of Cayman-issued U.S. CLO securities (column 3) have risen steadily in the past few years, in tandem with the rise in overall U.S. CLOs outstanding (column 1). At year-end 2018, U.S. investors held $409 billion in Cayman-issued U.S. CLO notes. When combined with the amount not accounted for by the TIC data (column 6), which we assume to be domestically-issued notes held by U.S. investors, this brings estimated U.S. investors' total holdings of U.S. CLO notes to $556 billion—the vast majority of total U.S. CLO issuance.

Table 3: U.S. CLO Positions ($ millions)

| 1 | 2 | 3 | 4 | 5 | 6 | |

|---|---|---|---|---|---|---|

| U.S. CLOs Outstanding | U.S. loans underlying Cayman-issued CLOs | U.S. holdings of Cayman-issued CLOs* | Foreign holdings of US-issued CLOs** | Estimated Cayman-issues held by foreign investors† | Estimated US-issues held by U.S. investors‡ | |

| 18:Q4 | 616,944 | 457,060 | 409,160 | 12,420 | 47,900 | 147,465 |

| 18:Q3 | 595,616 | 437,258 | 379,537 | 11,991 | 57,721 | 146,368 |

| 18:Q2 | 583,540 | 414,537 | 371,842 | 11,748 | 42,695 | 157,255 |

| 18:Q1 | 548,830 | 349,724 | ||||

| 17:Q4 | 541,053 | 344,769 |

* Reported as-of 2017:Q4 and as-of 2018:Q4. Intermeeting quarters are extrapolated for quarters based on the quarterly increase in CLOs outstanding. A prior version of this FEDS Note was released before the 2018:Q4 data were available. Return to table

** Reported as-of 2018:Q2 and extrapolated for additional quarters based on the quarterly increase in CLOs outstanding. Return to table

† Estimated KY = BL2 – SHC Return to table

‡ Estimated US = Outstanding – SHC – SHL – Estimated KY Return to table

Source: TIC BL2, SHC(A), SHL(A), SIFMA.

Our estimates (columns 5 and 6) are based on several assumptions. Note that the reported U.S. loans underlying Cayman-issued CLOs (column 2) account for only 74% of the total outstanding U.S. CLO market (column 1). This suggests that either a) some U.S. CLOs are both issued and held domestically or b) some of the loans underlying Cayman-issues have foreign obligors. Although the TIC data also capture domestically-issued CLO notes held by foreigners (column 4), such positions are small and the gap persists (column 6). In either case, the majority of these issues are likely held by U.S. investors, and thus we assign the entire gap to U.S. investors, for an estimate of total holdings of $556 billion.

Similarly, the holdings of U.S. investors (column 3) do not account for all the reported CLO loan liabilities (column 2). However, this gap is almost certainly due to foreign holdings of Cayman-issues, which would not be reportable in the TIC.

1. Emily Liu, [email protected], Division of International Finance, Federal Reserve Board; Tim Schmidt-Eisenlohr, [email protected], Division of Financial Stability, Federal Reserve Board. We thank our colleagues Daniel Beltran, Carol Bertaut and Seung Lee for their help. We are grateful to SIFMA, the RADAR Group at the Federal Reserve Bank of Philadelphia, the Markets group at the Federal Reserve Bank of New York, and the TIC group at the Department of the Treasury for their willingness to share their expertise. The views expressed in this paper are those of the authors and should not be interpreted as representing the views of the Federal Reserve Board or any other person associated with the Federal Reserve System. Return to text

2. Rennison, Joe and Colby Smith. "Debt Machine: are risks piling up in leveraged loans?" Financial Times, 21 January 2019, https://www.ft.com/content/64c9665e-1814-11e9-9e64-d150b3105d21. Return to text

3. Legal isolation refers to the independence of the special purpose entity from the issuer. This allows the risk rating of the CLO to depend on the quality of the underlying assets only and to be independent of the issuer. Return to text

4. The TIC system defines foreign securities by residency of the issuer. A security issuer's residency is determined by the country in which the issuer is legally incorporated or otherwise resident, as opposed to the nationality of an issuer, which is determined by the residency of the issuer's ultimate parent. Return to text

5. The gap between total U.S. CLOs outstanding (as reported by SIFMA) and the amount that can be accounted for in the TIC data may also partially reflect the fact that U.S. CLOs include loans to foreign obligors. TIC only requires reporting the value of CLOs related to underlying loans to U.S. obligors. This factor might upwardly bias our estimates of domestically issued CLOs and downwardly bias our estimates of Cayman Islands issued CLOs. Return to text

6. Also published in the 2018 TIC claims survey report, "U.S. Portfolio Holdings of Foreign Securities," https://ticdata.treasury.gov/Publish/shca2018_report.pdf Return to text

7. A previous version of this Note included data from 2014. See: https://www.federalreserve.gov/econres/notes/feds-notes/who-owns-us-clo-securities-20190719.htm. Return to text

Note that this assumes that patterns of ownership among investors do not differ between Cayman-issued U.S. CLOs and Delaware-issued U.S. CLOs.

9. Smith, Robert and Leo Lewis. "How Japan's farmers and fishermen backed the leveraged loan boom." Financial Times, 18 February 2019, https://www.ft.com/content/2689cc0a-32cf-11e9-bb0c-42459962a812. Return to text

10. CreditFlux CLO Manager Rankings, 2018:Q4 Return to text

11. For more information, please see the section "Improved Reporting of Certain Short-Term Liabilities" in the U.S. Department of the Treasury's press release from 15 August 2018, "Treasury International Capital Data for June" at https://home.treasury.gov/news/press-releases/sm459. Return to text

Liu, Emily and Tim Schmidt-Eisenlohr (2019). "Who Owns U.S. CLO Securities?," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, July 19, 2019, https://doi.org/10.17016/2380-7172.2423.

Disclaimer: FEDS Notes are articles in which Board staff offer their own views and present analysis on a range of topics in economics and finance. These articles are shorter and less technically oriented than FEDS Working Papers and IFDP papers.